Automotive Ignition Coil Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 11.74 Billion |

| Market Size (2031) | USD 14.46 Billion |

| Growth Rate (2026 - 2031) | 4.26% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Ignition Coil Market Analysis by Mordor Intelligence

Automotive ignition coil market size in 2026 is estimated at USD 11.74 billion, growing from 2025 value of USD 11.26 billion with 2031 projections showing USD 14.46 billion, growing at 4.26% CAGR over 2026-2031. Rising light-vehicle output in Asia Pacific, continued dominance of coil-on-plug (COP) technology, and a resilient replacement cycle in mature fleets collectively underpin growth. OEMs are fine-tuning ignition designs for turbocharged downsized engines that must comply with near-term Euro 7 limits, while the aftermarket benefits from the 12.5-year average vehicle age in the United States. At the same time, elevated copper prices and supply risks for rare-earth magnets are compressing supplier margins, and battery-electric-vehicle (BEV) penetration sets a clear upper bound on long-term demand. These crosscurrents place the automotive ignition coil market at a strategic pivot between legacy combustion needs and a rapidly electrifying future.

Key Report Takeaways

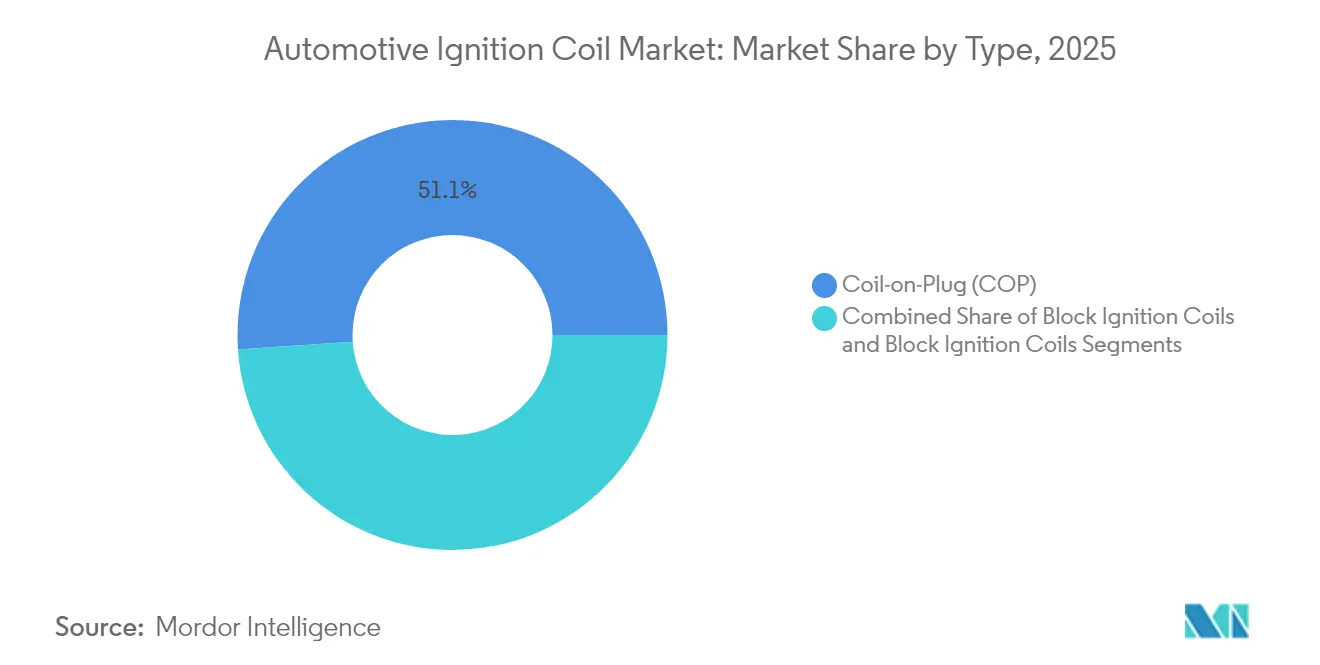

- By type, coil-on-plug systems captured 51.07% revenue share in 2025, while also recording the fastest growth at 6.08% CAGR to 2031.

- By operating principle, single-spark technology held 62.27% of the automotive ignition coil market share in 2025, whereas dual-spark designs are forecast to grow at a 5.76% CAGR.

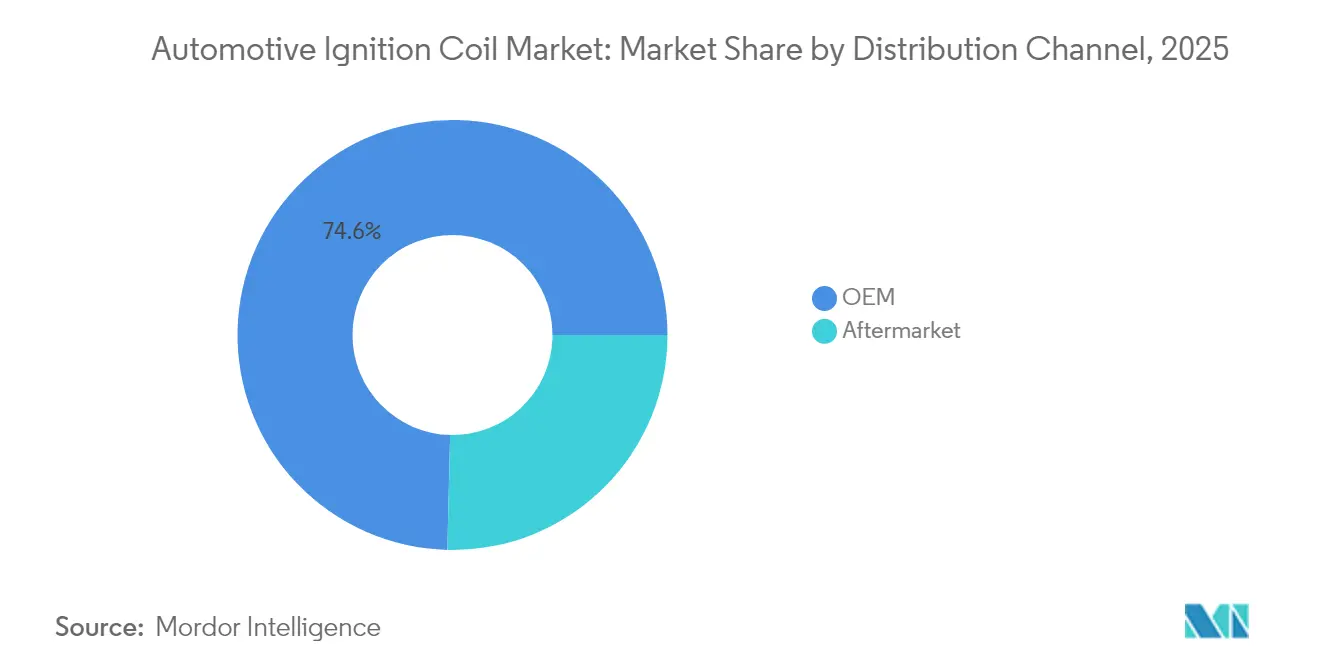

- By distribution channel, OEM accounts for 74.62% of revenue in 2025, but the aftermarket is set to grow the quickest at 6.91% CAGR through 2031.

- By vehicle type, passenger cars represented 63.95% of market value in 2025, yet commercial vehicles are poised to register the highest 6.22% CAGR to 2031.

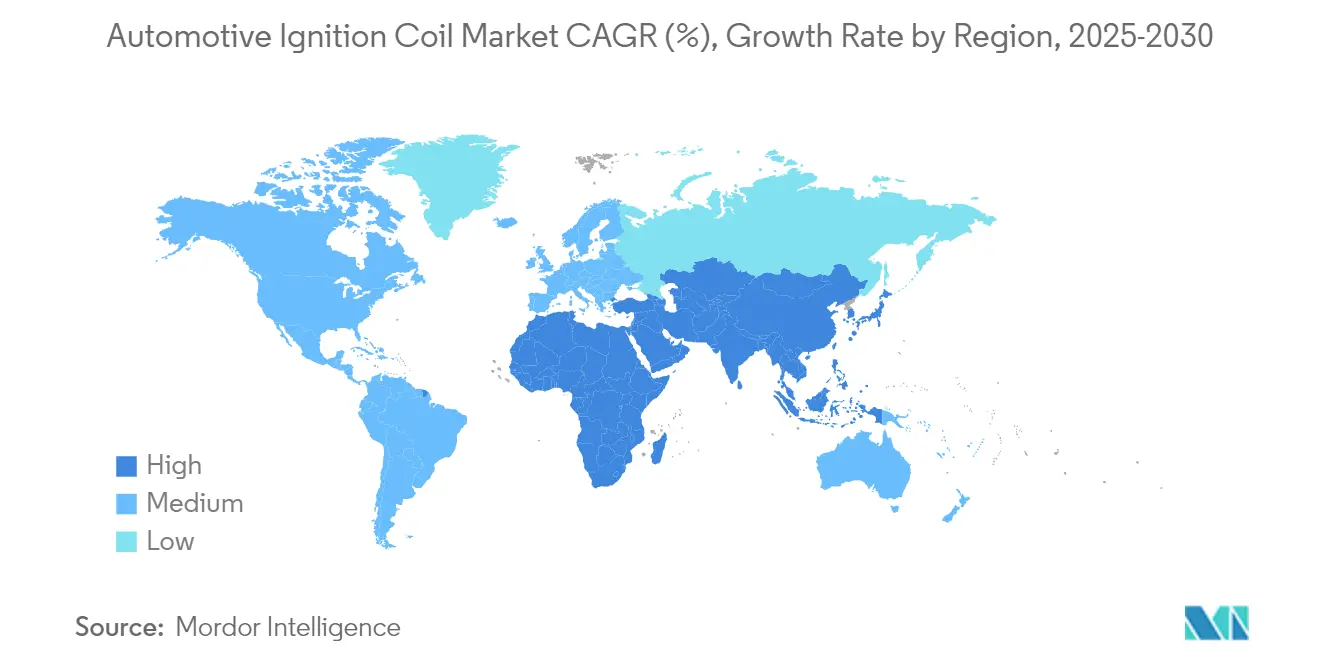

- By geography, Asia Pacific led with a 46.05% share of the automotive ignition coil market in 2025; the same region is projected to expand at a 6.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Ignition Coil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in Passenger & Light Commercial Vehicle Production | +1.2% | Global with APAC leading growth | Medium term (2-4 years) |

| Ageing Fleet Supporting Aftermarket Demand | +1.1% | North America and Europe core markets | Short term (≤ 2 years) |

| Emission Norms Driving High-Performance Coils | +0.8% | Europe and North America expanding to APAC | Long term (≥ 4 years) |

| Turbocharged Engines Requiring COP Coils | +0.7% | Global with premium segment focus | Medium term (2-4 years) |

| Flex-Fuel Adoption Needing Durable Coils | +0.4% | Brazil, India, Southeast Asia | Medium term (2-4 years) |

| Rise of Smart-Diagnostic Connected Coils | +0.3% | North America and Europe early adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Production of Passenger and Light Commercial Vehicles

Vehicle volumes continue to rebound from pandemic lows, especially in Asia Pacific, where industry revenue climbed 7% in 1H 2024. Production upswings favor the automotive ignition coil market because light commercial electrification trails passenger adoption by roughly five years. Automakers are also rolling out 48V mild-hybrid platforms that keep internal-combustion engines (ICE) in play, extending coil demand while cutting emissions. The emphasis on precise ignition timing to satisfy Euro 7 creates tailwinds for COP assemblies that support individual-cylinder control. Together, these forces add a moderate uplift to the growth trajectory.

Aftermarket Replacement Demand From Ageing Parc

Average fleet age reached 12.5 years in the United States during 2024. Older vehicles require more frequent service, which supports a vibrant aftermarket for coils. Standard Motor Products already fields 800 SKUs with 99% coverage, while NGK’s European range covers 420-part numbers that fit 87% of vehicles on the road. Independent workshops rely on broad compatibility, making the aftermarket an increasingly lucrative channel. The time buffer before legacy vehicles retire creates a durable revenue stream for at least one model cycle.

Stringent Emission Norms Pushing High-Performance Coils

Euro 7 rules and aligned global standards oblige OEMs to guarantee more complete combustion. To do so, manufacturers are integrating higher output coils with improved heat resistance and moisture sealing. Dual-spark architecture, although still niche, is gaining ground in premium models because multiple ignition points per cycle reduce particulate formation. Suppliers such as NGK Insulators cite steady sales of value-added products that help customers meet stricter thresholds. This driver lengthens the relevance of ICE ignition even as BEV momentum climbs.

Turbo-Charged Downsized Gasoline Engines Need COP Coils

Turbo share of light-duty engines jumped from 1% in 2000 to 37% in 2023 and is on pace to reach 83.3% by 2025. High boost pressure risks low-speed pre-ignition, making cylinder-specific spark control essential. COP solutions eliminate high-voltage losses and allow flexible dwell timing, which mitigates knock and improves efficiency. Leading brands such as BERU report deep penetration in volume models from Volkswagen Group and BMW Group, underlining how turbocharging aligns with premium ignition content.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BEV Shift Reducing Ignition System Demand | -2.1% | Global, with Europe and China leading the transition | Long term (≥ 4 years) |

| Copper & Rare-Earth Price Volatility | -0.6% | Global supply chain impact | Short term (≤ 2 years) |

| 48V Hybrids Lowering Coil Requirements | -0.4% | Europe and premium segments globally | Medium term (2-4 years) |

| Rise of Plasma-Based Ignition Technologies | -0.2% | Premium segments in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

BEV Penetration Eliminates Conventional Ignition Systems

Electric cars remove the entire spark-ignition assembly, cutting maintenance costs by up to 40%. DENSO projects BEVs will dominate global production by 2035, prompting suppliers to pivot toward battery, inverter, and thermal-management modules [1]“Integrated Report 2024,” DENSO Corporation, denso.com. Passenger segments will see the sharpest drop first, while heavier commercial classes will transition later due to range and payload limits. Nonetheless, the directional shift places a ceiling on future coil volumes.

Price Volatility of Copper and Rare-Earth Magnets

Copper touched USD 4.04 per lb in May 2024 and is forecast at USD 5.31 per lb during 2025. Chinese export curbs on rare-earth magnets have already forced short-term line stoppages in Europe. Coils rely on copper windings and magnet assemblies, so price spikes erode margins unless OEM contracts allow rapid pass-through. Material inflation is therefore a tangible headwind for the automotive ignition coil market until supply stabilizes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: COP Commands Premium Applications

Coil-on-plug systems accounted for 51.07% of 2025 revenue, and their 6.08% CAGR positions them as the clear growth engine for the automotive ignition coil market. The design removes high-voltage leads, reduces electromagnetic loss, and supports advanced knock-control strategies demanded by turbocharged engines. Block coils and rail assemblies stay competitive in cost-sensitive models, especially in entry-level segments across emerging economies.

OEM case studies reinforce the shift: Bosch introduced a spring-contact COP for BMW models to improve spark-plug connection reliability, while DENSO’s portfolio roadmap highlights distributor-less solutions as a core product line. Hybrid powertrains, which blend a 48 V e-motor with an ICE, still require one coil per cylinder, securing volume for COP units through 2031. Competitive pricing, simplified installation, and incremental engine-management gains will keep COP at the center of the automotive ignition coil market narrative.

By Operating Principle: Single-Spark Still Dominant

Single-spark designs owned 62.27% of sales in 2025, reflecting mature manufacturing, proven reliability, and lower cost. Yet dual-spark units are tracking a 5.76% CAGR as premium OEMs chase further combustion efficiency. In Brazil’s flex-fuel fleet, variable ethanol content makes multiple ignition points advantageous for stable flame propagation.

BorgWarner’s multi-spark line illustrates how suppliers extend dwell time or deliver sequential pulses to optimize burn time. Dual-spark value scales when regulators tighten particulate limits. Even so, single-spark’s sizeable installed base and compatibility with a broad engine mix mean that the automotive ignition coil market size for this configuration will remain substantial through the forecast horizon.

By Distribution Channel: Aftermarket Widens Its Footprint

OEM contracts delivered 74.62% of 2025 sales, but aftermarket revenue is rising at 6.91% CAGR, faster than any other channel in the automotive ignition coil market. Independent garages rely on ready availability and multi-pack options, attributes embraced by Standard Motor Products and NGK.

The aging vehicle profile in North America and Western Europe underpins parts replacement. Meanwhile, emerging markets such as India see aftermarket coils used in second-hand imports that lack dealer support. As BEVs shrink OEM coil demand, aftermarket activity will become the stabilizing pillar for the automotive ignition coil industry.

By Vehicle Type: Commercial Vehicles Provide a Growth Cushion

Passenger cars delivered 63.95% of 2025 revenue, but commercial vehicles are accelerating at 6.22% CAGR. Their longer service life and slower path to full electrification of the shelter coil demand.

Hitachi’s USD 33 million Chennai plant expansion underscores faith in sustained truck and bus production. Fleets value durability and low total ownership cost, fueling a gradual shift to higher-grade insulation and moisture-proof designs. These attributes keep the automotive ignition coil market size for commercial vehicles expanding even as the passenger-car BEV share climbs.

Geography Analysis

Asia Pacific leads the automotive ignition coil market with 46.05% share and is on pace for 6.74% CAGR. China recorded auto-industry revenue of 10 trillion yuan in 2024, and domestic brands accounted for 61.9% of sales, driving strong local coil demand. Japanese manufacturers such as NGK ship advanced units worldwide, while India’s low-cost base draws investment for OEM supply and aftermarket export. North America is a mature but profitable arena; the 12.5-year average fleet age secures steady aftermarket pull, and strict U.S. EPA rules keep premium coils relevant for remaining ICE platforms.

Europe balances aggressive BEV policy with interim Euro 7 compliance. Automakers must fit high-output coils to meet particulate limits until battery platforms scale, and NGK’s 87% aftermarket coverage ensures part availability for aging gasoline and mild-hybrid fleets. South America is driven by Brazil’s flex-fuel ecosystem, where 82% of the light-vehicle park runs on ethanol blends, a scenario that raises coil stress and boosts demand for corrosion-resistant designs; Brazil’s ethanol output reached 35.3 billion liters in 2023 . The Middle East and Africa remain smaller contributors yet record incremental gains as motorization rates climb. Political instability and currency volatility complicate logistics, but localized assembly by Japanese and Chinese brands is opening coil opportunities in Nigeria, Egypt, and South Africa. Overall, geographic diversity cushions the automotive ignition coil market against single-region shocks.

Competitive Landscape

The competitive arena is moderately concentrated. NGK/Niterra commands extensive reach through 69 subsidiaries and 34 factories and continues to diversify from spark plugs into full ignition modules. DENSO is reallocating R&D toward inverter and battery-cooling products, signaling a proactive response to BEV displacement risks. Bosch demonstrates incremental innovation, recently replacing plastic gripping features with contact springs in COP housings to assure spark-plug integrity under vibration.

Material supply is the new battleground. Copper and rare-earth volatility incentivize research into aluminum windings and ferrite magnets. Suppliers able to switch materials without compromising coil output gain a margin edge. Digital diagnostics is another frontier: embedded sensors relay coil temperature and spark energy to telematics portals, empowering predictive maintenance for fleet operators.

Aftermarket specialists carve out space below the tier-one giants. Standard Motor Products pushes monthly SKU additions to maintain 99% vehicle coverage, and its multi-pack Blue Streak line targets quick-turn repairs. Regional firms in China and India compete primarily on cost but increasingly license designs from global leaders, adding volume without disrupting the technological hierarchy. Collectively, these strategies shape an automotive ignition coil market that rewards both scale and agile adaptation.

Automotive Ignition Coil Industry Leaders

Denso Corporation

NGK Spark Plug Co. Ltd (Niterra)

Hitachi Astemo Ltd

Robert Bosch GmbH

BorgWarner Inc. (incl. Delphi Technologies)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Osaka-based Diamond & Zebra Electric Mfg. Co. launched an ignition coil for hydrogen engines featuring false-ignition prevention.

- September 2024: Standard Motor Products expanded its Standard and Blue Streak coil range beyond 700 SKUs, with multi-packs for complete service jobs.

- January 2024: NGK introduced the MOD Series Ignition Coils designed for higher reliability in modern engines.

Global Automotive Ignition Coil Market Report Scope

An automotive ignition coil is an essential component in a vehicle's ignition system that transforms the low-voltage power from the battery into high-voltage electricity. This high voltage is required to create a spark in the spark plugs, igniting the air-fuel mixture in the engine's combustion chamber, enabling the vehicle's engine to start and run.

The automotive ignition coil market is segmented by type (block ignition coils, coil on plug, and ignition coil rail), operating principle (single spark technology and dual spark technology), distribution channel (OEM and aftermarket), vehicle type (passenger cars and commercial vehicles), and geography (North America, Europe, Asia-Pacific, and the rest of the world).

The report offers forecasts for the automotive ignition coil market in volume and value (USD) for all the above segments.

| Block Ignition Coils |

| Coil-on-Plug (COP) |

| Ignition Coil Rail |

| Single Spark Technology |

| Dual Spark Technology |

| OEM |

| Aftermarket |

| Passenger Cars |

| Commercial Vehicles |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Egypt | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Block Ignition Coils | |

| Coil-on-Plug (COP) | ||

| Ignition Coil Rail | ||

| By Operating Principle | Single Spark Technology | |

| Dual Spark Technology | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Vehicle Type | Passenger Cars | |

| Commercial Vehicles | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Egypt | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the automotive ignition coil market?

The market is valued at USD 11.74 billion in 2026 and is projected to reach USD 14.46 billion by 2031.

Which region leads the automotive ignition coil market?

Asia Pacific holds the top position with 46.05% share in 2025 and is growing at a 6.74% CAGR to 2031.

Why are coil-on-plug systems growing faster than other types?

COP technology offers precise cylinder-specific spark control essential for turbocharged and downsized engines, resulting in a 6.08% CAGR.

Why is the aftermarket channel expanding more rapidly than OEM supply?

Vehicle fleets are aging, leading to higher replacement rates; aftermarket suppliers cover up to 99% of models, driving a 6.91% CAGR.

Page last updated on: