Embedded Systems In Automobiles Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

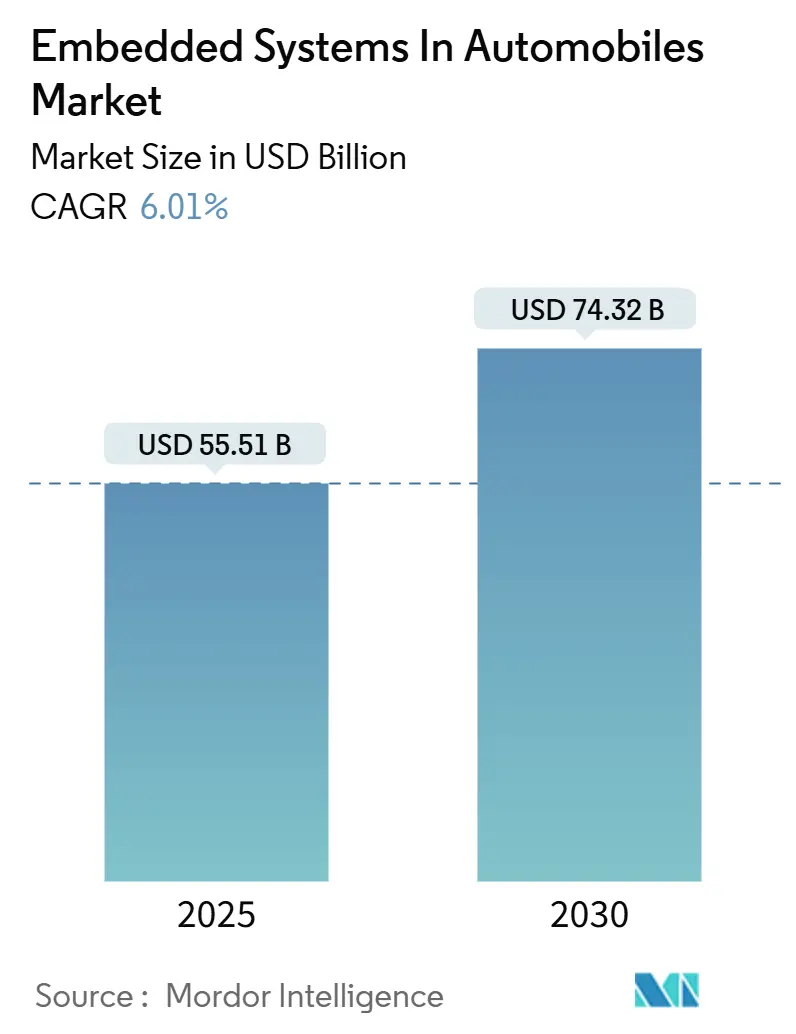

| Market Size (2025) | USD 55.51 Billion |

| Market Size (2030) | USD 74.32 Billion |

| Growth Rate (2025 - 2030) | 6.01% CAGR |

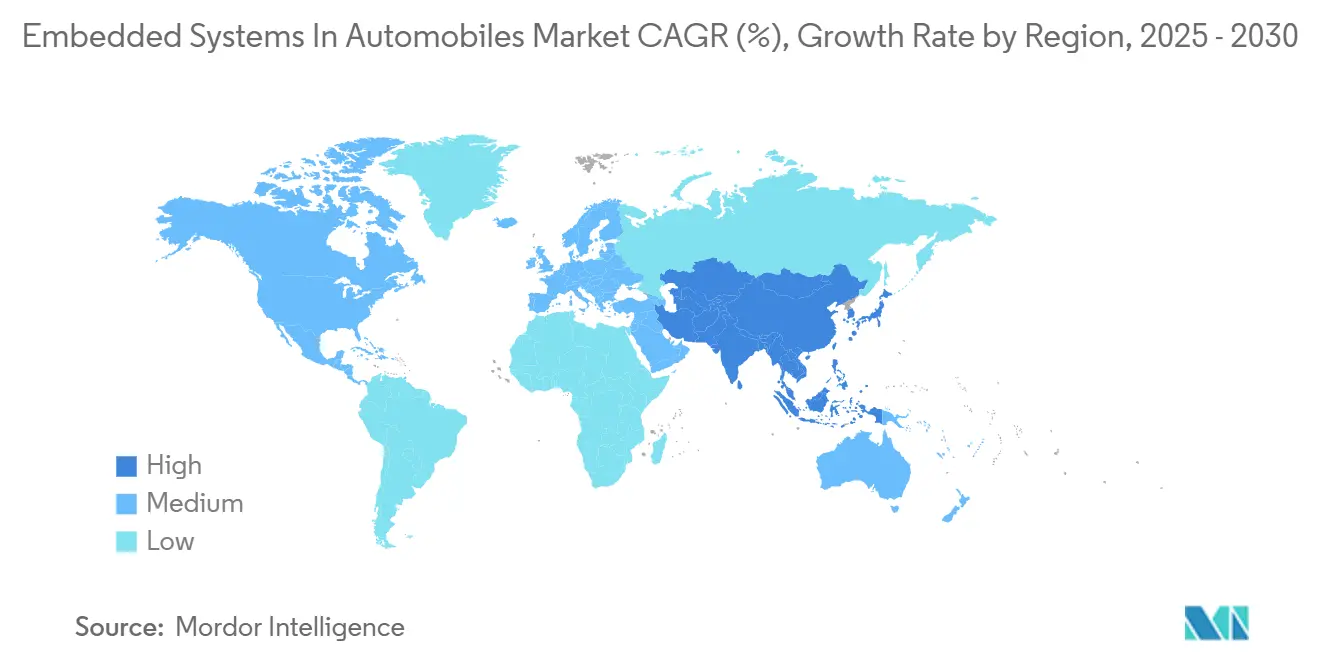

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

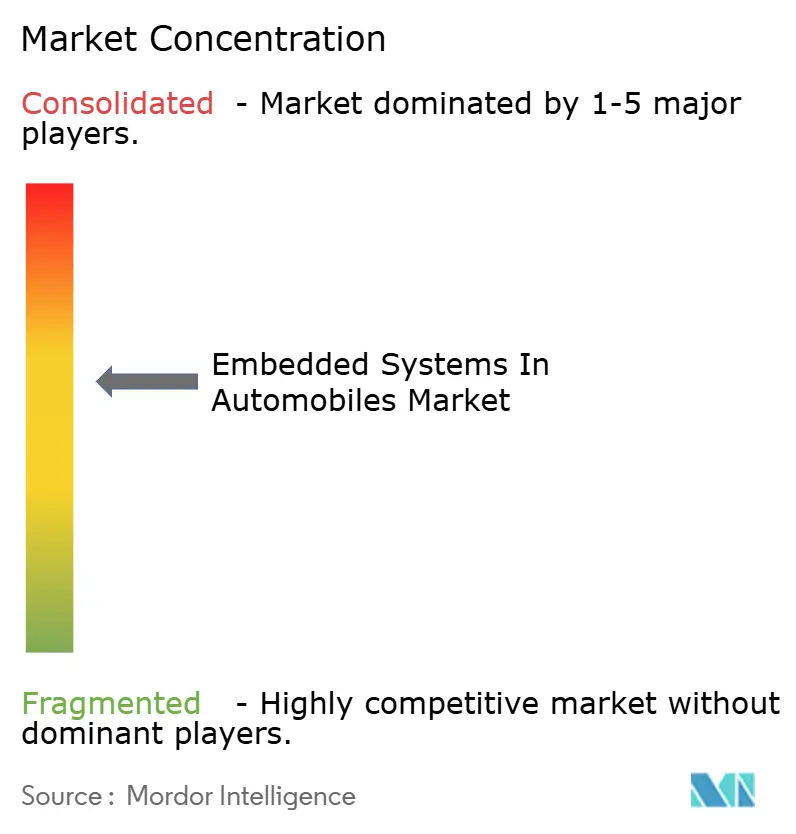

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Embedded Systems In Automobiles Market Analysis by Mordor Intelligence

The embedded systems in the automobile market size stands at USD 55.51 billion in 2025 and is expected to reach USD 74.32 billion by 2030, reflecting a 6.01% CAGR over the forecast period. Rising regulatory pressure for advanced driver assistance, the surge in electronic content per electric vehicle, and the shift toward zonal electrical architectures collectively underpin this expansion. Consolidation of multiple functions into centralized computing platforms is lowering wiring weight and enabling over-the-air feature deployment, reinforcing long-term demand. Meanwhile, aggressive investments in wide-bandgap semiconductors for power electronics, expanding cloud connectivity, and localization policies in the Asia-Pacific continue to shape supplier strategies and competitive dynamics. Heightened cybersecurity compliance under UNECE R155/R156 is also steering purchasing toward components with built-in hardware security modules.

Key Report Takeaways

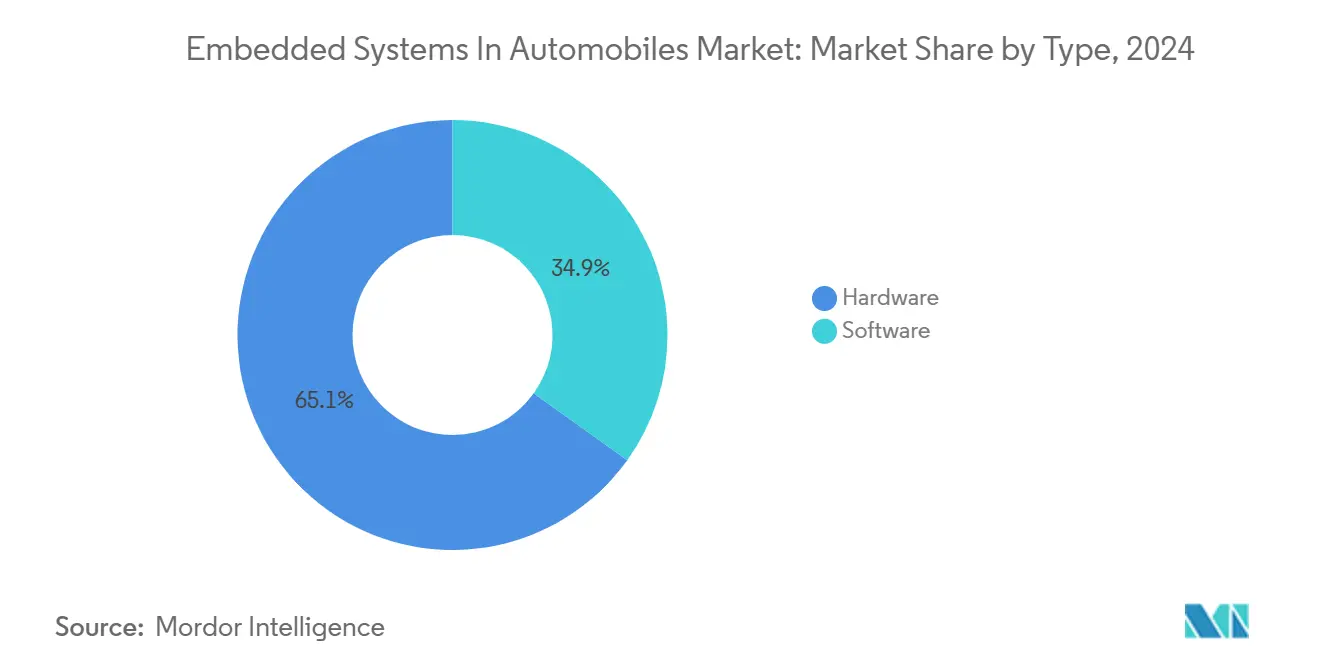

- By type, hardware led with 65.12% of the embedded systems in the automobile market share in 2024, while software is projected to grow at an 8.05% CAGR to 2030.

- By vehicle type, passenger cars held 70.55% of the embedded systems in the automobile market share in 2024; buses and coaches are forecast to advance at a 7.22% CAGR through 2030.

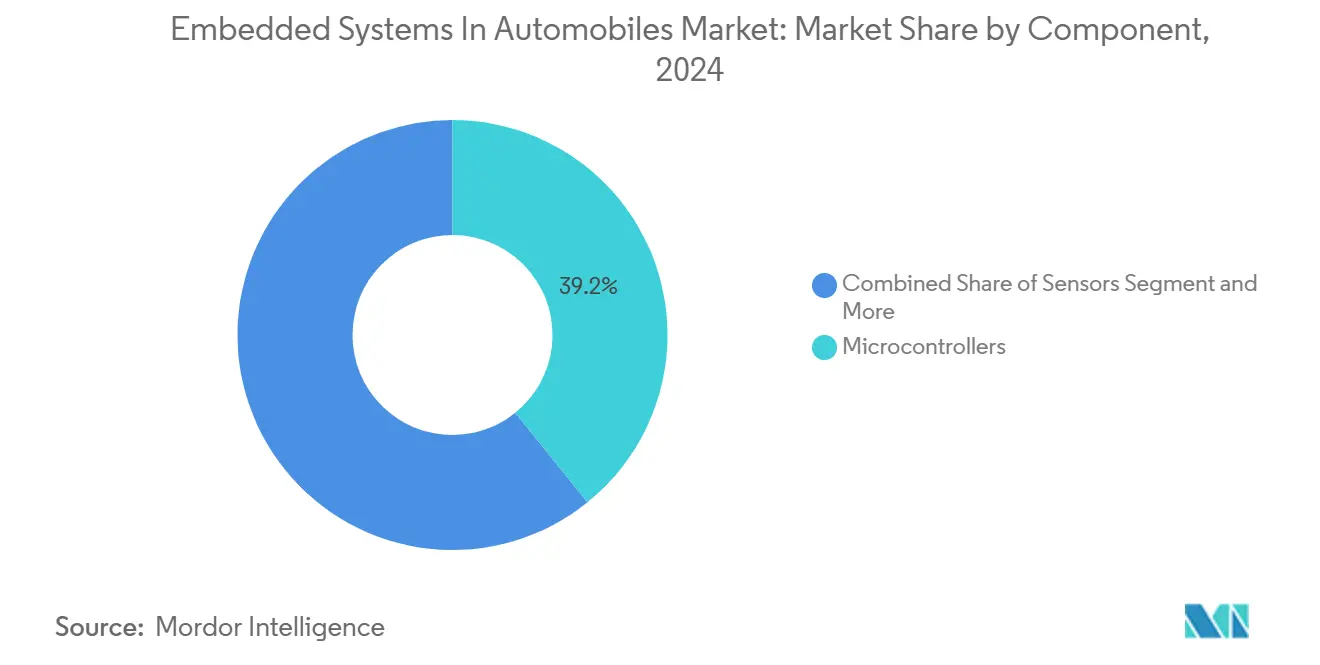

- By component, microcontrollers captured 39.22% of the embedded systems in the automobile market share in 2024, whereas memory devices are expected to expand at an 8.33% CAGR by 2030.

- By application, safety and security systems accounted for 36.45% of the embedded systems in the automobile market share in 2024; infotainment and telematics are set to grow at a 7.55% CAGR over the same horizon.

- By geography, Asia-Pacific commanded 44.38% of the embedded systems in the automobile market share in 2024 and is poised to rise at a 6.67% CAGR to 2030.

Global Embedded Systems In Automobiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV-Led Surge in Electronic Content | +1.5% | APAC core, adoption in North America and the EU | Long term (≥4 years) |

| Stricter ADAS and Safety-Regulation Push | +1.2% | EU and North America, global spillover | Medium term (2-4 years) |

| ADAS Sensor Expansion Across All Vehicles | +1.0% | Global, mass-market acceleration | Medium term (2-4 years) |

| Shift to Zonal/Centralized E/E Architectures | +0.9% | Global, led by premium OEMs | Long term (≥4 years) |

| Connected-Infotainment and OTA Proliferation | +0.8% | Global, premium segments first | Short term (≤2 years) |

| Localization of Supply Chains via Tariffs | +0.6% | APAC and North America primarily | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

EV-Led Surge in Electronic Content

Battery-electric vehicles consume significantly more semiconductors than combustion counterparts, primarily due to power-train inverters, battery-management units, and thermal regulation modules. OEMs are moving toward custom power devices based on silicon carbide to extend driving range, igniting multi-billion-dollar investments in dedicated foundry capacity. Vertical integration successes at Tesla have spurred legacy manufacturers to forge exclusive wafer-supply agreements, tightening availability for non-aligned competitors. The proliferation of 800-volt architectures is also expanding demand for high-speed communication links between battery packs and vehicle control domains, sustaining robust volume growth for safety-certified transceivers.

Stricter ADAS and Safety-Regulation Push

Global safety mandates are compelling every automaker to embed automated emergency braking, driver monitoring, and lane keeping systems that each require multiple redundant control units. ISO 26262 certification has become a non-negotiable entry barrier, steering procurement toward semiconductor platforms with integrated lock-step cores and safety diagnostics. Tier-1 suppliers report higher bill-of-materials costs but also note that mandated features reduce price sensitivity, allowing premium pricing for automotive-grade chips. Commercial fleets are accelerating adoption to mitigate liability exposure, creating additional volume. As regulations tighten, demand for zonal controllers capable of aggregating sensor data is set to escalate through the middle of the decade.

Expansion of ADAS Sensor Suites Across All Vehicle Classes

Multi-modal sensing that fuses camera, radar, and lidar inputs is migrating to economy models as component prices fall. Bosch’s acquisition of TSI Semiconductors underscored the strategic value of proprietary sensor-interface know-how [1]“Bosch closes TSI Semiconductors acquisition,” Bosch, bosch.com. Centralized domain controllers must execute real-time perception algorithms under 10 ms latency to satisfy functional-safety budgets, driving uptake of high-performance microprocessors with integrated AI accelerators. Standardization on automotive Ethernet and CAN-FD supports bandwidth-heavy sensor data streams without compromising backward compatibility, broadening addressable volumes for communication chipsets.

Shift to Zonal/Centralized E/E Architectures

Premium OEMs are replacing up to 100 stand-alone ECUs with four to six high-bandwidth zonal computers that communicate over automotive Ethernet backbones. The consolidation slashes wiring harness weight by 40 kg in large SUVs, improving range for electric powertrains and freeing cabin space. Centralization also simplifies over-the-air credential management because security keys reside in fewer gateways, lowering validation costs. Suppliers of multi-core microprocessors with integrated hypervisors are therefore experiencing notable growth, especially where functional-safety and infotainment workloads must coexist. The architectural transition further enables feature deployment through software, giving OEMs a path to post-sale revenue without new hardware. As economies of scale emerge, mass-market brands will adopt similar architectures, making zonal design a mainstream growth catalyst after 2027.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor Supply-Chain Volatility | -0.8% | Global, APAC manufacturing concentration | Short term (≤2 years) |

| High Integration Cost and Complexity | -0.6% | Global, impact greatest on small OEMs | Medium term (2-4 years) |

| Rising Cybersecurity-Compliance Burden | -0.4% | EU and North America strictest | Long term (≥4 years) |

| Trade Restrictions on Connected-Vehicle | -0.3% | United States-China primarily, spill-over effects | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Semiconductor Supply-Chain Volatility

Automotive-grade lead times ballooned during 2024, and although easing, remain twice consumer-electronics norms, exposing the embedded systems in the automobile market to allocation risks. TSMC revealed that automotive still commands a minimal share of its wafer output, underscoring vulnerability to smartphone and AI server demand swings. OEMs have responded by dual-sourcing critical microcontrollers and redesigning boards around “available” pinouts, adding engineering overhead and depressing gross margins. Governments in Japan and the United States have pledged subsidy packages for automotive-specific fabs, but meaningful capacity will not come online before 2027, sustaining near-term tightness.

High Integration Cost and System Complexity

Transitioning to service-oriented software architectures demands cross-disciplinary talent spanning embedded coding, cybersecurity, and functional-safety engineering. Continental estimates that the average embedded development budget per vehicle program has climbed since 2020, with test-bench footprints doubling to handle mixed-criticality workloads [2]“Continental Annual Report 2024,” Continental AG, continental-ag.com. Smaller suppliers struggle to amortize these fixed costs, accelerating mergers and vertical partnerships. Complexity also magnifies field-failure liability, pushing OEMs toward fewer, larger suppliers able to guarantee system-level performance across an eight-year design life.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Software Gains Momentum within Hardware-Dominated Platforms

The embedded systems in the automobile market size for hardware components held a 65.12% share in 2024, as every vehicle still requires physical sensors, power devices, and control units. Software’s 8.05% CAGR from 2025-2030, outpaces the growth of hardware as automakers monetize features via code, not metal. The embedded systems in the automobile market share for software are rising because consolidating up to 100 discrete electronic control units into a handful of zonal computers unlocks economies of scale in compute silicon while shifting differentiation to operating systems, middleware, and cybersecurity stacks.

Ongoing investments in real-time Linux distributions and hypervisors capable of mixed-criticality execution are reducing integration pain points and enabling life-cycle upgrades. Infineon generated significant revenue in automotive during 2024, showing that silicon still anchors platform value. Nonetheless, software subscription models provide recurring income streams that cushion hardware price erosion and justify higher up-front R&D. Middleware suppliers that bundle AUTOSAR-Adaptive frameworks with diagnostic stacks are now positioned as essential partners rather than bolt-on vendors, reshaping procurement hierarchies.

By Vehicle Type: Passenger Cars Dominate, Yet Commercial Fleets Accelerate

Passenger cars accounted for 70.55% of the embedded systems in the automobile market share in 2024 thanks to global light-vehicle volumes and rising content per unit. Infotainment refresh cycles have shortened to smartphone-like cadences, compelling greater embedded flash and compute headroom. The embedded systems in the automobile market size tied to buses and coaches grow at 7.22% through 2030, outperforming all categories as cities electrify public transit fleets.

Urban agencies view electric buses as rolling data hubs that require sophisticated battery diagnostics, predictive maintenance analytics, and remote software management, lifting semiconductor demand per vehicle. Light commercial trucks also integrate telematics and Electronic Logging Devices to meet regulatory reporting, driving modest growth. Daimler’s pilot autonomous freight corridor with Waymo has signaled that high-throughput domain controllers will move beyond passenger cars, widening supplier addressable markets.

By Component: Microcontrollers Lead, Memory Devices Surge

Microcontrollers delivered 39.22% of embedded systems in the automobile market share in 2024, acting as deterministic brains for anti-lock braking, power steering, and body functions. Their leadership remains secure as zonal controllers still rely on fail-safe real-time cores for actuation. The embedded systems in the automobile market size for memory devices, however, is projected to climb fastest at an 8.33% CAGR because sensor-rich architectures require high-bandwidth storage to buffer perception data during autonomous maneuvers.

Emerging LPDDR5X devices are entering volume production, addressing thermal stresses unique to under-hood installations. Demand for high-density NOR flash is concurrently rising to support secure firmware-over-the-air rollbacks. Transceiver ICs add steady but slower growth, reflecting rising penetration of automotive Ethernet and 5G-V2X modems that enable software-defined feature activation throughout the vehicle life cycle.

By Application: Safety Dominates, Infotainment Expands

Safety and security systems commanded 36.45% of the embedded systems in the automobile market share in 2024 owing to global mandates for electronic stability control, lane keeping, and pedestrian detection. These functions require redundant sensing and lock-step processing, driving volume for ASIL-D microcontrollers. The fastest expansion comes from infotainment and telematics, projected at a 7.55% CAGR through 2030 as every automaker seeks connected-service revenues. The embedded systems in the automobile market size are thus increasingly allocated to large touchscreen head-units housing up to eight CPU cores and dedicated GPUs for 3-D graphics.

Tesla’s recurring subscription for premium connectivity exemplifies the post-sale monetization potential that makes high-spec domain controllers economically attractive. Meanwhile, powertrain controllers embrace wide-bandgap gate drivers to meet stricter efficiency norms, sustaining stable demand even as volume shifts toward battery-electric topologies.

Geography Analysis

Asia-Pacific captured 44.38% of the embedded systems in the automobile market share in 2024, anchored by China’s significant EV unit sales and regional semiconductor giants that shorten logistics chains. The embedded systems in the automobile market share in China, Japan, and South Korea is bolstered by localization mandates under initiatives such as “Made in China 2025,” which targets significant domestic chip content by 2030 [3]“CAAM Vehicle Production Statistics 2024,” China Association of Automobile Manufacturers, caam.org.cn. Taiwan Semiconductor Manufacturing Company and Samsung furnish advanced nodes for high-performance controllers, while Sony and Panasonic deliver image sensors rated for automotive temperature cycles. Regional growth at a 6.67% CAGR is further propelled by government subsidies for battery-electric buses, spurring demand for high-voltage traction inverters.

North America follows as the second-largest contributor, supported by the Infrastructure Investment and Jobs Act that allocated USD 7.5 billion for nationwide charging corridors. Detroit-area OEMs are rewriting electrical architectures around centralized compute hubs that simplify OTA deployment, reinforcing orders for cybersecurity-hardened gateways. Canada’s reserves of lithium and nickel enable vertically integrated battery supply, encouraging domestic production of battery-management microcontrollers to hedge geopolitical risks.

Europe retains significant weight due to the stringent General Safety Regulation 2 requirements. Germany’s auto industry invested in EV programs during 2024, including dedicated budgets for silicon-carbide power modules and secure communication stacks. Compliance with UNECE R155/R156 accelerates demand for embedded hardware security modules, benefitting suppliers such as Infineon and NXP that ship eSIMs and secure-element co-processors. Southern Europe and Eastern Europe continue to expand electronics manufacturing footprints to diversify beyond Asia-centric supply, aiding risk mitigation but adding moderate logistics overhead.

Competitive Landscape

The embedded systems in the automobile market exhibit moderate concentration. Infineon, NXP, STMicroelectronics, Renesas, and Texas Instruments leverage long-qualification track records and automotive-grade packaging know-how to deter new entrants. Recent strategy pivots emphasize software-integrated solutions. NXP’s S32G platform bundles over-the-air secure bootloaders, while the acquisition of Nexperia’s Newport fab aims to guarantee 200-mm capacity for legacy automotive nodes.

Horizontal challengers include NVIDIA, Qualcomm, and AMD, whose data-center-derived AI accelerators are being down-binned for autonomous driving. Their entry pushes traditional suppliers to enhance graphics and machine-learning throughput. On the supply side, IDMs are forming foundry-sharing alliances to spread capital burden; for example, Infineon and United Microelectronics Corp. inked a long-term capacity reservation for 300-mm power wafers. Start-ups offering zonal gateway reference designs with pre-certified cybersecurity stacks attract OEMs seeking faster homologation cycles, indicating that niche innovation remains viable despite high capital barriers.

Value-chain power is also shifting upstream as OEMs announce joint design centers. Hyundai’s custom‐SoC initiative with Samsung Foundry demonstrates the growing appetite for bespoke silicon that optimally balances power, cost, and compliance. Conversely, suppliers lacking scalable software assets risk relegation to commodity status, prompting a wave of collaborations such as Bosch’s tie-up with Arm to co-define next-generation safety islands for heterogeneous compute clusters.

Embedded Systems In Automobiles Industry Leaders

Infineon Technologies AG

NXP Semiconductors N.V.

STMicroelectronics NV

Texas Instruments Incorporated

Renesas Electronics Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: QNX and Vector signed an MoU to co-develop a foundational vehicle software platform that helps OEMs accelerate software-defined vehicle rollouts.

- June 2025: Bosch introduced the SMP290 Bluetooth-enabled MEMS tire pressure sensor to deliver real-time monitoring for enhanced ride safety.

- June 2025: Elektrobit and Foxconn agreed to co-create EV.OS, an AI-driven software framework aimed at shortening electric vehicle development cycles.

- March 2025: Infineon announced plans for a RISC-V–based microcontroller family under its AURIX™ brand to expand architecture diversity in safety-critical domains.

Global Embedded Systems In Automobiles Market Report Scope

| Hardware |

| Software |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Buses and Coaches |

| Sensors |

| Transceivers |

| Memory Devices |

| Microcontrollers |

| Powertrain and Chassis Control |

| Infotainment and Telematics |

| Safety and Security |

| Others |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Hardware | |

| Software | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| Buses and Coaches | ||

| By Component | Sensors | |

| Transceivers | ||

| Memory Devices | ||

| Microcontrollers | ||

| By Application | Powertrain and Chassis Control | |

| Infotainment and Telematics | ||

| Safety and Security | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the embedded systems in automobiles market in 2025?

It is valued at USD 55.51 billion in 2025 with a projected CAGR of 6.01% to 2030.

Which region leads spending on automotive embedded electronics?

Asia-Pacific holds 44.38% of global revenue, driven by EV policies in China, Japan, and South Korea.

What component category is growing fastest?

Memory devices show the highest growth at an 8.33% CAGR owing to rising data storage needs in sensor-heavy vehicles.

Which application segment commands the largest revenue share?

Safety and security systems lead with 36.45% of 2024 revenue due to global regulatory mandates.

Page last updated on: