Automotive Advanced Shifter System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

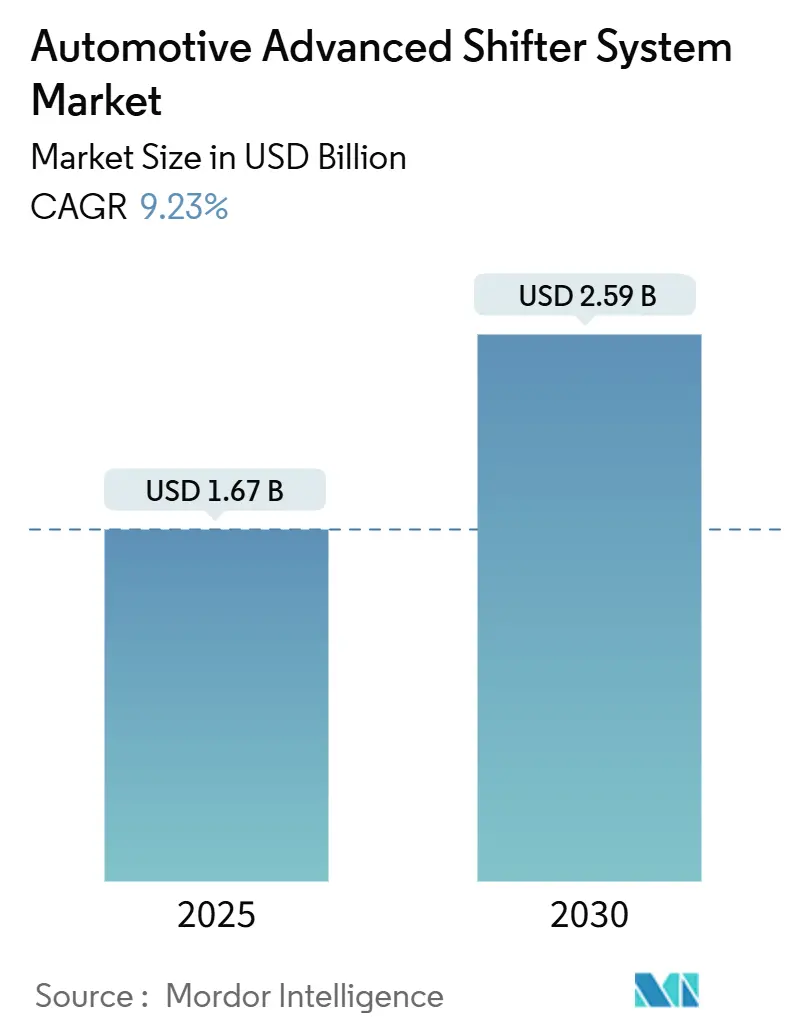

| Market Size (2025) | USD 1.67 Billion |

| Market Size (2030) | USD 2.59 Billion |

| Growth Rate (2025 - 2030) | 9.23% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Advanced Shifter System Market Analysis by Mordor Intelligence

The Automotive Advanced Shifter System Market size is estimated at USD 1.67 billion in 2025, and is expected to reach USD 2.59 billion by 2030, at a CAGR of 9.23% during the forecast period (2025-2030). Strong demand arises from automakers’ migration to shift-by-wire (SBW) architectures that synchronise with electric powertrains, over-the-air (OTA) software updates and consolidated cockpit electronics. Growth is reinforced by rising automatic transmission fit‐rates, stringent emissions standards that favour electronically controlled gear strategies and fleet operators’ push for predictive maintenance. Competitive pressure intensifies as software-centric suppliers enter the value chain, prompting established tier-ones to integrate shifter controls with steering, braking and chassis domains in unified by-wire platforms. Regional momentum is most significant in Asia-Pacific, where government incentives for new-energy vehicles and local innovation in simulated transmission feel like the adoption of electronic selectors has accelerated. Across applications, continuously variable transmissions (CVTs) record the quickest uptake as OEMs leverage their infinitely variable ratios to meet tightening fuel-efficiency targets.

Key Report Takeaways

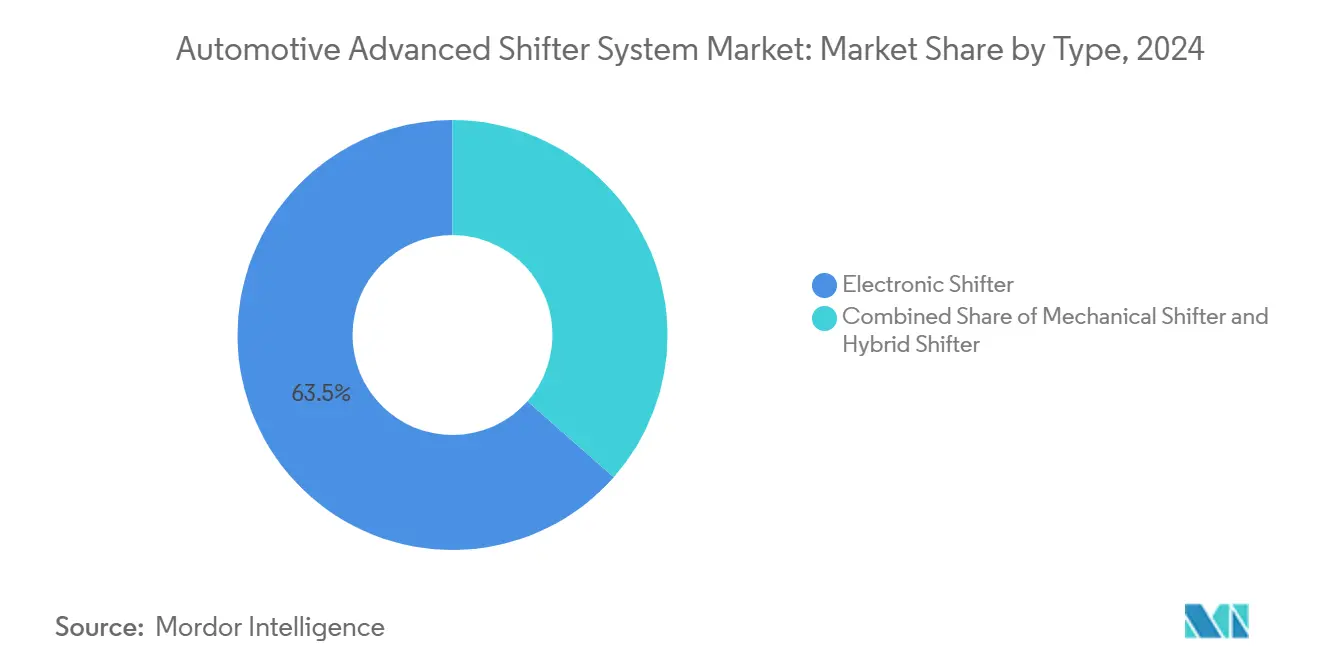

- By type, electronic shifters held 63.47% of the automotive advanced shifter system market share in 2024, and the same segment is expected to continue growing at a 9.25% CAGR during the forecast period (2025-2030).

- By vehicle class, passenger cars led with a 61.21% share of the automotive advanced shifter system market in 2024. In contrast, the commercial vehicles segment is expected to grow at a 9.31% CAGR during the forecast period (2025-2030).

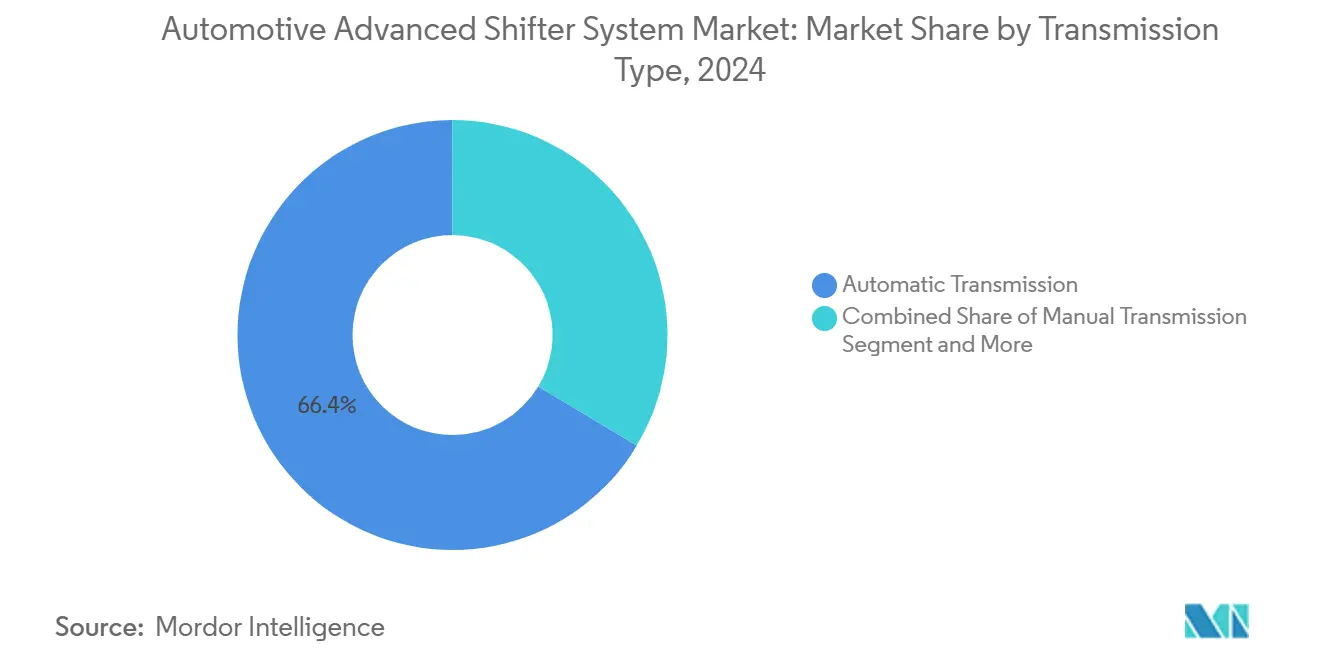

- By transmission, automatic units captured a 66.35% share of the automotive advanced shifter system market in 2024; the CVT category is forecast to expand at a 9.34% CAGR during the forecast period (2025-2030).

- By driving mechanism, the internal combustion segment dominated, with a 74.35% share of the automotive advanced shifter system market in 2024. Yet, the battery-electric platforms segment is expected to grow at a 9.28% CAGR during the forecast period (2025-2030).

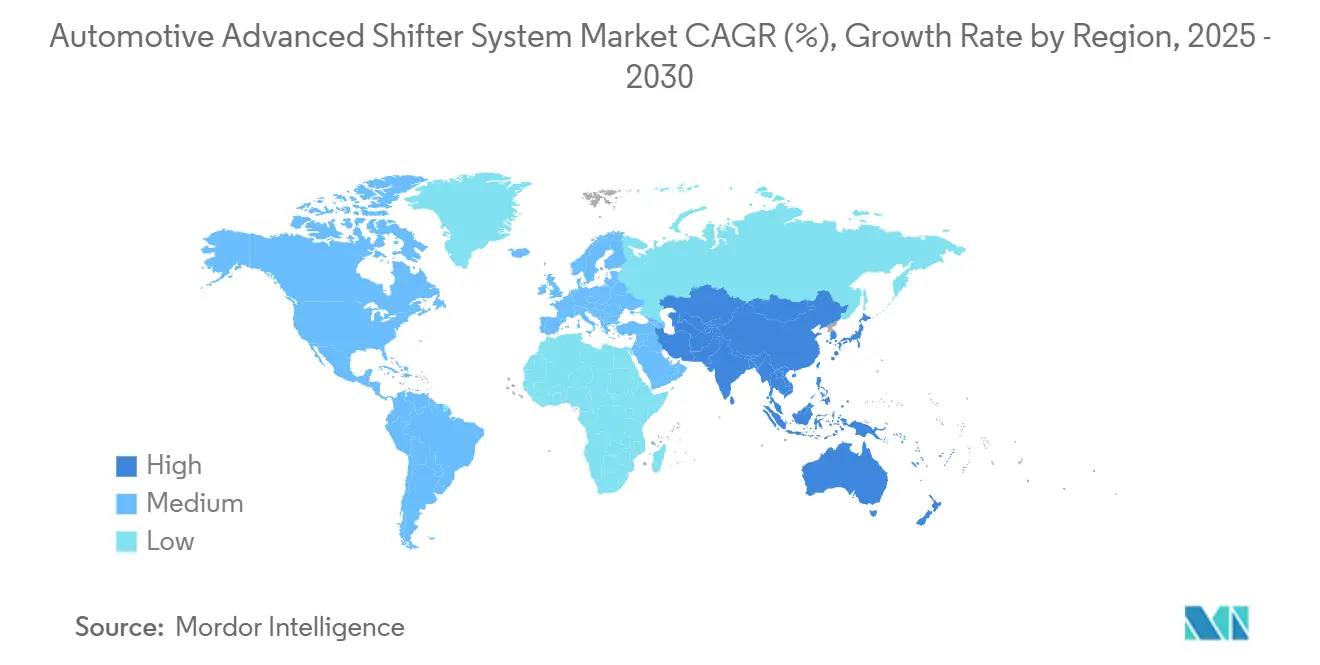

- By geography, Asia-Pacific led with 38.71% revenue share in 2024, and Asia-Pacific is also projected to post the fastest 9.26% CAGR during the forecast period (2025-2030).

Global Automotive Advanced Shifter System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge In Electric and Hybrid Vehicle Production | +2.3% | Asia Pacific core, spill-over to North America and EU | Short term (≤ 2 years) |

| Rising Adoption Of Automatic and Shift-By-Wire Transmissions | +2.1% | Global, with early gains in North America and EU, Asia Pacific acceleration | Medium term (2-4 years) |

| Stricter Fuel-Efficiency / Emission Regulations | +1.8% | EU and North America core, expanding to Asia Pacific markets | Long term (≥ 4 years) |

| OEM Demand For Modular, Space-Saving Console Layouts | +1.4% | Global, premium segments first | Medium term (2-4 years) |

| OTA-Enabled, Software-Defined Shifter Features | +1.2% | North America and EU early adoption, Asia Pacific following | Long term (≥ 4 years) |

| Interior Personalization and Haptic-Feedback Differentiation | +0.9% | Premium segments globally, luxury-first adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Electric & Hybrid Vehicle Production

Battery-electric drivetrains rely on single-speed reducers, so the shifter evolves into a drive-mode commander that manages regenerative braking, one-pedal control and performance mapping. Hyundai’s N e-Shift in the IONIQ 5 N emulates eight virtual gears by modulating motor torque and artificial engine braking to satisfy performance drivers [1]“IONIQ 5 N Technical Briefing,” Hyundai Motor Company, hyundai.com . Tesla’s Auto Shift employs exterior cameras and artificial intelligence to choose forward or reverse automatically, cutting driver interaction while retaining manual override. These examples illustrate how electrification reframes the functional brief of the selector and enlarges the total addressable portion of the automotive advanced shifter system market.

Rising Adoption of Automatic & Shift-By-Wire Transmissions

Shift-by-wire designs replace mechanical linkages with electronic signals that relay driver commands to the transmission control unit. The layout reduces weight, frees cabin packaging and enables safety logic such as emergency override. Patent activity from Ford for simulated manual shifters illustrates how haptic feedback lets enthusiasts preserve engagement in electric cars without mechanical complexity. Integrated software like ZF’s Cubix Tuner further personalises gear-change feel through cloud updates that can arrive long after the vehicle leaves the factory. These capabilities accelerate OEM migration from mechanical levers to digital selectors, solidifying the automotive advanced shifter system market as a pivotal enabler of software-defined vehicles.

Stricter Fuel-Efficiency / Emission Regulations

Euro 7 and California LEV III rules tighten tailpipe limits and extend compliance to real-world driving. Electronic shifters support predictive shift strategies, leveraging connected road gradient and traffic data to keep engines in optimal efficiency bands [2]“Euro 7 Proposal Details,” European Commission, europa.eu . Incorporating functional safety requirements from ISO 26262 drives redundant actuators and dual sensors that maintain gear control under fault, elevating electronic architectures over mechanical alternatives. Regulators thus provide a structural tailwind to the automotive advanced shifter system market.

OEM Demand for Modular, Space-Saving Console Layouts

Large infotainment screens and minimalist interiors require compact selectors that retain intuitive ergonomics. Yanfeng’s XiM25 interior concept embeds the shifter into a steer-by-wire armrest, showing how modular assemblies trim cockpit part counts by two-thirds compared with traditional layouts [3]“XiM25 Experience in Motion Concept,” Yanfeng Automotive Interiors, yanfeng.com . AUO’s Smart Cockpit prototype features morphing centre controls that rise only when needed, proving that advanced materials and actuators can deliver dynamic haptic surfaces. Suppliers such as CCL Design integrate touch sensors, backlighting and decoration in single films, cutting assembly time and enabling streamlined console designs. These advances underpin the automotive advanced shifter system market as a central contributor to cockpit flexibility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High System Cost and Complexity Vs. Mechanical Shifters | -1.6% | Global, cost-sensitive segments most affected | Short term (≤ 2 years) |

| Reliability and Safety Concerns | -1.1% | Global, regulatory compliance focus | Medium term (2-4 years) |

| Semiconductor Shortages | -0.9% | Global, with Asia Pacific supply chain dependencies most affected | Short term (≤ 2 years) |

| Cyber-Security Risks | -0.8% | Global, with EU and North America leading regulatory focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High System Cost & Complexity vs. Mechanical Shifters

Electronic selectors require precision actuators, microcontrollers, haptic motors and cybersecurity modules that lift bill-of-materials costs two-to-threefold over cable-based levers. Dealers must invest in diagnostic tablets and software subscriptions to service firmware faults, raising lifetime ownership expenses for price-sensitive buyers. Semiconductor shortages have exposed longer lead times for Hall-effect sensors and 32-bit controllers, prompting some emerging-market OEMs to delay SBW rollouts in entry trims. Although scale effects narrow the gap, elevated upfront pricing continues to temper the automotive advanced shifter system market adoption curve in value segments.

Reliability & Safety Concerns of Electronic SBW Systems

Shift-by-wire introduces new failure modes such as sensor drift, software bugs and electromagnetic interference. UNECE Regulation R155 obliges automakers to harden in-vehicle networks against cyber threats, compelling shifter suppliers to adopt encrypted communication and intrusion detection. Field recalls for early electronic column shifters underscore the reputational risk when diagnostic routines fail to detect latent actuator wear. To counter these concerns, tier-ones add dual-coil motors and fallback electromechanical locks. However, the engineering burden modestly drags the automotive advanced shifter system market CAGR relative to its technical potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Electronic Dominance Accelerates Through Software Integration

The electronic category captured 63.47% of 2024 revenue and is expected to advance at a 9.25% CAGR through 2030. Its lead springs from seamless pairing with battery-electric drivetrains and OTA update capability that lengthen feature life cycles. The automotive advanced shifter system market size for electronic units is forecast to grow exponentially by 2030, underscoring its scale advantage. Mechanical designs persist in off-road pickups and cost-sensitive vans where simplicity trumps flexibility. Hybrid solutions that layer a mechanical fallback beneath electronic actuation attract brands seeking functional redundancy without forgoing digital experience benefits.

OEMs embed electronic selectors into centralised domain controllers so that a single software image manages shifting, drive modes, and chassis response. This consolidation limits wiring harness mass and shortens validation cycles. Given these gains, the automotive advanced shifter system market expects mechanical share to decline steadily, although not disappear, due to niche durability and tactile preferences.

By Vehicle Type: Commercial Vehicles Drive Innovation Through Fleet Requirements

Passenger cars remained dominant at 61.21% of 2024 sales, but commercial platforms exhibit a sharper 9.31% expansion pace because fleet economics reward predictive diagnostics and remote calibration. For example, ZF’s TraXon automatic for heavy trucks marries SBW interfaces with route-based gear maps that trim fuel use in long-haul duty cycles. The automotive advanced shifter system market share for commercial applications is projected to cross two-fifths of incremental revenue gains through 2030.

Fleet operators value SBW for driver convenience and data: continuous actuation logs feed analytics that flag clutch wear or coaching opportunities, cutting downtime and insurance premiums. As regulators tighten CO₂ ceilings on urban delivery vans, electronic selectors simplify the step to hybrid or battery variants, further anchoring growth.

By Transmission Type: CVT Growth Reflects Efficiency Demands

Automatic transmissions commanded a 66.35% share in 2024 owing to global consumer preference for self-shifting convenience. Yet CVTs are set to grow faster at a 9.34% CAGR because their seamless ratio variance complements small turbo engines and hybrid splits. The automotive advanced shifter system market size tied to CVTs is forecast to grow exponentially between 2025 and 2030.

Electronic selectors orchestrate simulated stepped shifts to deliver familiar tactile cues when marketing teams aim to preserve sporty identity, a task impossible with mechanical cable CVTs. Manual gearboxes remain in enthusiast sub-segments, though even there, rev-matching actuators and hill-start aids introduce partial electronic content. These crossovers gradually tilt share toward digitally managed solutions.

By Driving Mechanism: Electric Vehicles Reshape Shifter Requirements

Internal-combustion platforms supplied 74.35% of 2024 demand, yet battery-electric lines will log a 9.28% CAGR through 2030. Their selectors evolve from gear pickers into multi-modal drive controllers. The automotive advanced shifter system market size for electric applications is expected to grow exponentially by 2030.

Interfaces like Tesla’s sliding touch-bar in the Model S or BMW’s rocker toggle in the iX present minimalistic gestures. Software derives gear intent from navigation data to pre-arm regenerative braking ahead of downhill stretches, optimising range. Hybrids pose mixed challenges as they must juggle clutch engagement states and electromotor boosts, amplifying validation workload yet cementing reliance on electronic actuation.

Geography Analysis

Asia-Pacific held 38.71% of 2024 revenue and is projected to compound at 9.26% annually through 2030, driven by Chinese new-energy mandates and South Korean interface innovation. The automotive advanced shifter system market share here benefits from vertically integrated supply chains that allow local sourcing of precision actuators and MCU chips. Regional incumbents such as Hyundai continue to debut virtual-gear experiences that build emotional bridges for buyers transitioning to electric mobility.

North America ranks second as homegrown EV pioneers leverage computer-vision auto-shift features. Stringent Corporate Average Fuel Economy (CAFE) targets and Inflation Reduction Act incentives sustain hybrid and battery assembly, reinforcing the need for responsive SBW designs. Continued patent filings by Ford and GM reveal a focus on tactile engagement overlays that differentiate brand personality without hardware changes.

Due to Euro 7 rules and a robust luxury segment embracing haptic personalisation, Europe maintains steady progress. Suppliers integrate redundant CAN-FD and Ethernet channels to meet ISO 26262 ASIL D goals, pushing up per-unit value. Although Western European growth is slower in percentage, high unit revenue and premium mix keep the region a profit centre within the automotive advanced shifter system market. Emerging Middle East and African hubs are now localising wiring harnesses for electronic selectors, but uptake remains limited to premium imports until cost structures fall.

Competitive Landscape

The supplier field remains moderately concentrated. Top players ZF Friedrichshafen, Continental and BorgWarner accounted for roughly half of 2024 revenue. Each firm bundles shifter controls into holistic by-wire portfolios that merge braking, steering and ride functions. ZF’s multiple-vehicle brake-by-wire award confirmed OEM readiness to source integrated chassis stacks that include shifter logic, signalling a shift from component sales to system-level contracting.

New entrants with software heritage, such as Silicon Valley-based Canoo Components, target OTA analytics layers that sit above generic actuators, eroding the traditional moat of mechanical know-how. Meanwhile, vehicle makers insource domain controller software, narrowing the hand-off to tier-ones. Continental’s spin-off Aumovio positions to license micro-services that run on OEM hardware, a model that could compress hardware margins yet elevate lifetime subscription revenue.

Partnerships arise to share the cost of cybersecurity compliance, seen in the joint task force between Bosch and BlackBerry QNX that hardens SBW communication stacks against emerging Regulation R155 audits. Aftermarket retrofits also emerge: EnhanceAuto markets steering-wheel shift paddles for Tesla owners who miss physical stalks. Competitive dynamics therefore pivot around code ownership, cloud infrastructure and human-machine interface finesse rather than bushing tolerances, reshaping value capture across the automotive advanced shifter system market.

Automotive Advanced Shifter System Industry Leaders

ZF Friedrichshafen AG

Kongsberg Automotive ASA

Continental AG

BorgWarner Inc.

Robert Bosch GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: ZF secured a contract to deliver brake-by-wire and steering gear to 5 million vehicles that integrate electronic shifter logic within a unified chassis domain.

- November 2024: Kia unveiled virtual gear shift features in the 2025 EV6 GT, expanding software-based simulated transmission technology first seen in the IONIQ 5 N.

Global Automotive Advanced Shifter System Market Report Scope

| Electronic Shifter |

| Mechanical Shifter |

| Hybrid Shifter |

| Two Wheeler |

| Passenger Vehicle |

| Commercial Vehicle |

| Automatic Transmission |

| Manual Transmission |

| Continuously Variable Transmission |

| Internal Combustion Engine |

| Electric Vehicle |

| Hybrid Vehicle |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Electronic Shifter | |

| Mechanical Shifter | ||

| Hybrid Shifter | ||

| By Vehicle Type | Two Wheeler | |

| Passenger Vehicle | ||

| Commercial Vehicle | ||

| By Transmission Type | Automatic Transmission | |

| Manual Transmission | ||

| Continuously Variable Transmission | ||

| By Driving Mechanism | Internal Combustion Engine | |

| Electric Vehicle | ||

| Hybrid Vehicle | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What revenue does the global advanced shifter system segment generate today and how quickly is it growing?

It reached USD 1.67 billion in 2025 and is expected to expand at a 9.23% CAGR during the forecast period (2025-2030).

Which vehicle category is showing the fastest uptick in advanced shifter adoption?

Commercial fleets top the growth table with a 9.31% CAGR during the forecast period (2025-2030), as operators seek predictive maintenance and fuel-saving features.

What advantages are helping electronic shift-by-wire units replace mechanical levers?

They free cabin space, integrate with electric drivetrains and accept over-the-air software updates that add new drive modes after purchase.

Which region accounts for the largest share of global sales?

Asia-Pacific leads with 38.71% of 2024 revenue and is also expected to grow at a 9.26% CAGR during the forecast period (2025-2030)..

How do fuel-efficiency rules influence transmission choice and shifter design?

Tighter standards steer OEMs toward CVTs and advanced automatics, both of which rely on electronic selectors for optimal ratio control and real-world emissions compliance.

Who are the main suppliers shaping competitive dynamics?

ZF Friedrichshafen, Continental and BorgWarner together controlled roughly half of 2024 revenue, yet software-centric newcomers are intensifying rivalry.

Page last updated on: