Automotive Piston Engine System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.02 Billion |

| Market Size (2031) | USD 4.94 Billion |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

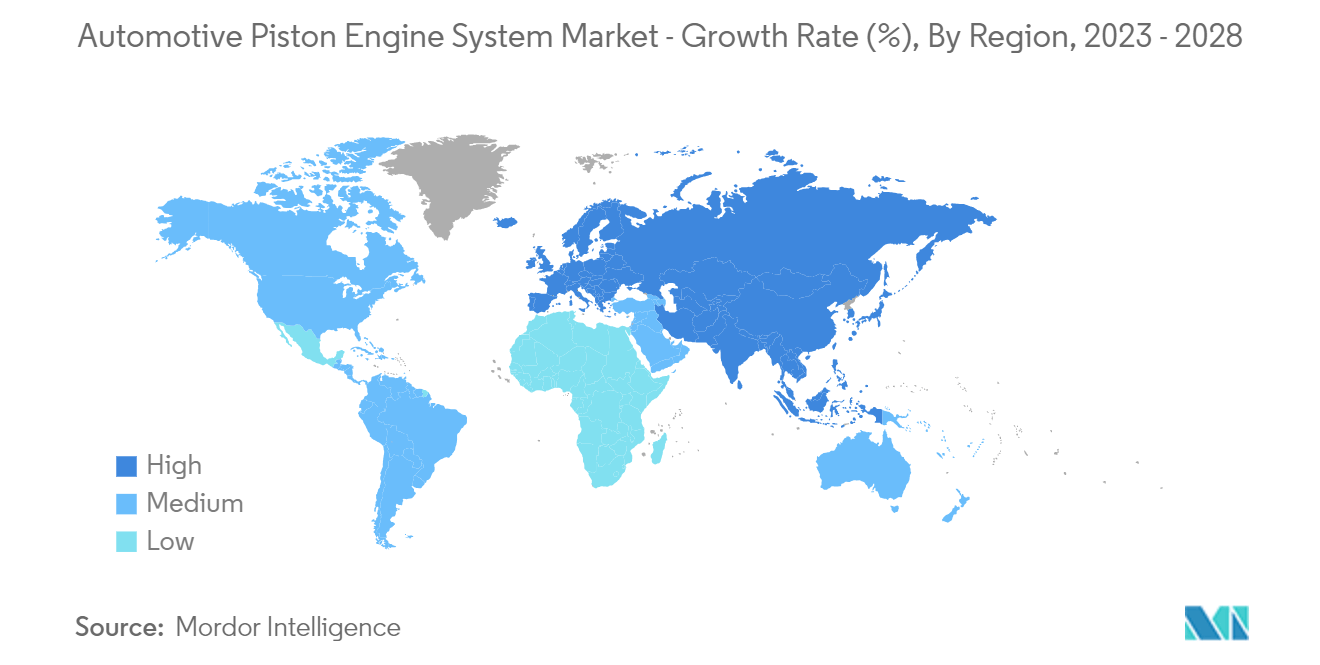

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Piston Engine System Market Analysis by Mordor Intelligence

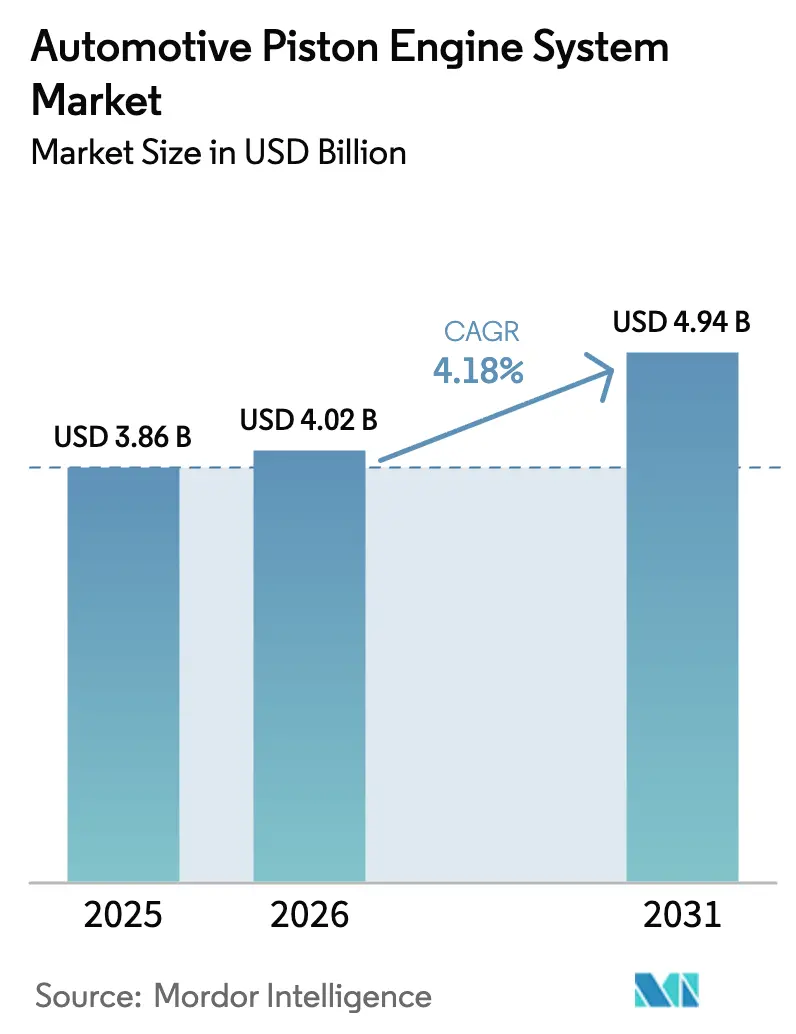

The automotive piston engine system market size is expected to grow from USD 3.86 billion in 2025 to USD 4.02 billion in 2026 and is forecast to reach USD 4.94 billion by 2031 at 4.18% CAGR over 2026-2031.

Innovations and prototypes of engines from major automakers and original equipment manufacturers (OEMs), coupled with consumer preferences for high-performance and fuel-efficient automobiles, are some of the major factors propelling the market growth. Engine downsizing trends are on the rise, with automakers developing smaller engines with better fuel injection systems. Further, the rapid transformation of the automotive industry in integrating lightweight components in their vehicle models is propelling the growth of the automotive piston engine system market. It is owing to the enhancement in technology and commitment by several parts and component manufacturers to develop advanced pistons, which assist in improving vehicle efficiency.

With the increasing focus of the government to promote the usage of electric vehicles to combat carbon emissions, the sales trends of fuel-operated vehicles are significantly being affected. It poses a major challenge for the automotive piston engine system market, as the integration of pistons in electric vehicles is optional. On the other hand, the production of piston systems is gaining traction in the aftermarket channels, owing to the growth in vehicle parc. Consumers availing of used cars are constantly in need of upgrading their vehicle's parts and components. These positively impact the demand for the automotive piston engine systems market.

With China, India, and Japan growing as global automotive manufacturer hubs, the Asia-Pacific region is expected to continue as a major market for automotive piston systems due to the increase in manufacturing of alternative fuel vehicles such as liquefied petroleum gas (LPG), compressed natural gas (CNG), and diesel engines. Further, the market is anticipated to witness the development of various lightweight piston components to improve the efficiency of vehicles and better fuel consumption capability.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Piston Engine System Market Trends and Insights

Passenger Car Segment is Anticipated to Dominate the Market

Increasing preference of consumers to avail alternative fuel vehicles, such as LPG CNG operated cars, is anticipated the growth of the piston engine system market. Various auto manufacturers are constantly spending hefty sums in developing new-age vehicles, which require lightweight piston components to be utilized in the vehicles. Coupled with that, the growing demand for used cars in several regions and increasing vehicle parc, owing to consumers' preference towards availing private transportation medium, is positively impacting the demand for automotive piston engine system market. The increasing age of vehicles requires constant upgradation, and therefore, changing piston systems in the aftermarket for fuel-operated vehicles is expected to drive this segment of the market.

On the other hand, the rise in sales of electric vehicles is hindering the growth of the automotive piston engine system market. The spike in sales is the result of an increase in regulatory norms by various organizations and governments to control emission levels and to propagate zero-emission vehicles. As a result, automakers are continually working and focusing on increasing their expenditure on the R&D of electric vehicles, which may aid OEMs in marketing electric vehicles in the future.

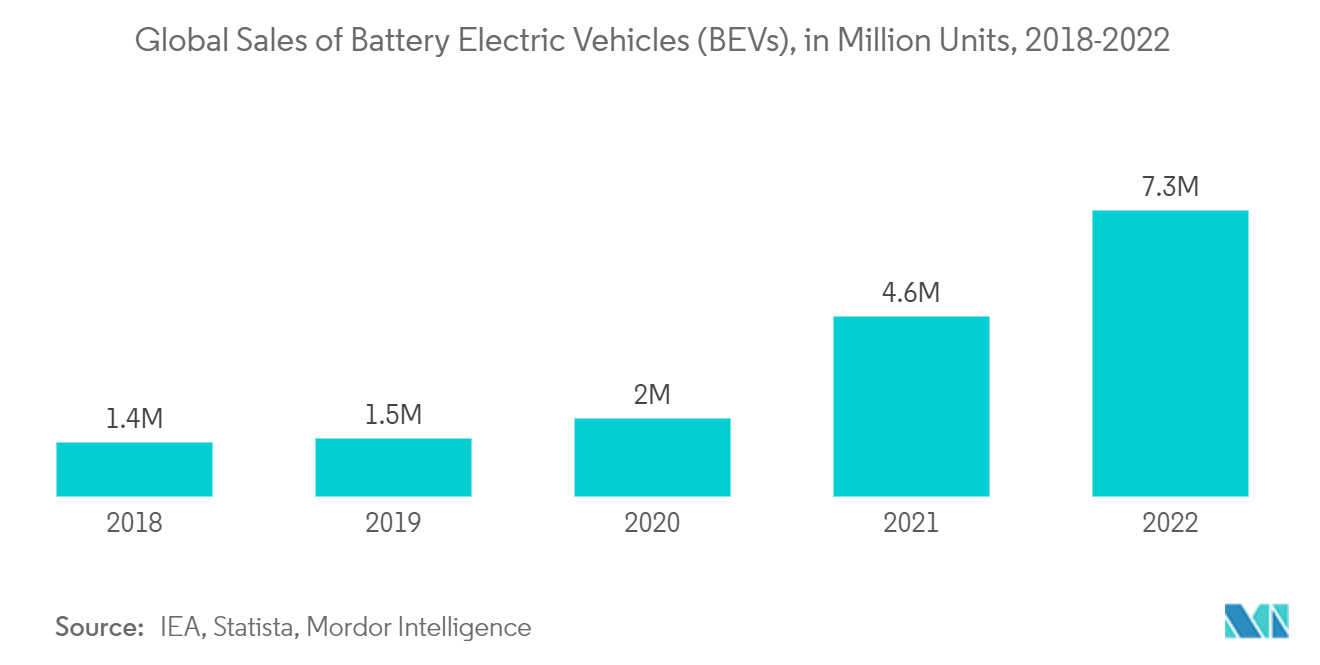

The global electric vehicles (including battery electric vehicles, fuel cell electric vehicles, and plug-in hybrid vehicles) market observed a tremendous increase in the number of sales registered every year since 2018. This increase was registered in almost all segments of vehicles, which include passenger vehicles and commercial vehicles. For instance-

- In 2022, global sales of battery electric vehicles (BEVs) touched 7.3 million units, compared to 4.6 million units in 2021, representing a 58.7% Y-o-Y growth between 2021 and 2022.

With the increased inclination toward electric vehicles, governments of different countries offering subsidies, and the growing need for automation and reduced emissions, the electrification of the automotive industry will serve as a major restraint for the market during the forecast period.

Asia-Pacific to Dominate the Market during the forecast period

Asia-Pacific region is projected to be the leading region for the automotive piston engine system market during the forecast period. It is mainly due to the heavy reliance on internal combustion engines, especially in the commercial vehicles sector. For instance,

- In 2022, India witnessed sales of 933 thousand units of commercial vehicles, compared to 677 thousand units in 2021, recording a Y-o-Y growth of 37.8% between 2021 and 2022.

- Similarly, new sales of commercial vehicles in Indonesia touched 264 thousand units in 2022, compared to 227 thousand units in 2021, representing a 16.3% Y-o-Y between 2021 and 2022.

Although electric commercial vehicles in the Asia-Pacific region gained traction in recent years, the market of ICE commercial vehicles remained strong as of 2022. However, with the increasing penetration of ICE commercial vehicles in the Asia-Pacific market, the automotive piston engine system market might witness falling growth in the coming years.

The increasing urbanization rate, growing vehicle parc, and the rising per capita disposable income of consumers are driving the automotive market in the Asia-Pacific region. As more consumers migrate to urban for better employment and financial opportunities, the preference towards availing private transportation medium shoots up, which positively impacts the passenger car market in the region. It, in turn, positively impacts the position engine system market in this region.

Despite the ramping penetration of electric vehicles at a faster rate, there remains a massive potential in the aftermarket for piston manufacturers to cater to consumers who avail of fuel-operated used cars. With the immense market for conventional IC engines in the regions, despite the growing inclination toward electric vehicles, the growth potential for automotive piston engine systems is expected to be high in Asia-Pacific during the forecast period.

Competitive Landscape

The automobile piston engine system market is consolidated and highly competitive, with only a few companies dominating the market. Some of the major companies operating in the market are Aisin Seiki, Federal-Mogul Holding LLC, Mahle GmbH, Tenneco Inc, Rheinmetall Automotive AG, Hitachi Automotive Systems, and Riken Corporation, among others. These players actively engage in forming long-term partnerships with auto manufacturers to enhance their brand portfolio by offering various piston components for gasoline or diesel vehicles.

- In January 2023, Rheinmetall officially transferred its large-bore pistons production to Koncentra Verkstads AB (KVAB) of Gothenburg, Sweden. In October 2022, Rheinmetall announced the sale, which reflected the Düsseldorf tech group's strategic reorientation towards an improved focus on developing small-bore pistons.

- In August 2022, Nippon Piston Ring and Riken Corporation announced a Memorandum of Understanding (MoU) agreement to establish a joint holding company formed by mutual stock transfer. It is to consolidate the two companies on equal terms. As per the agreement, the trading name of the new joint company will be NPR-Riken Corporation. The company aims to facilitate the development of advanced position solutions for the automotive industry.

The market is anticipated to witness the launch of various advanced lightweight piston components in the coming years as these players try to gain a competitive edge with the diversification of their product portfolio.

Automotive Piston Engine System Industry Leaders

Aisin Seiki

Federal Mogul Holding LLC

Mahle GmbH

Rheinmetall

Tenneco Inc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The clearest whitespace for piston engine system suppliers is extending the installed-base opportunity, including service and replacement pistons, rings, and pins, as the global vehicle parc ages and used gasoline and diesel vehicles stay in operation longer. This is most visible where conventional powertrains remain high-volume in daily use, while component makers lift performance and durability through lightweighting, coatings, and friction-reduction solutions that target fuel efficiency and emissions compliance without a full powertrain change.

A second opportunity is upgrading piston systems for alternative-combustion use cases that keep reciprocating engines relevant in specific duty cycles, particularly in heavy-duty and hybrid applications. In April 2026, MAHLE Powertrain reported a hydrogen conversion of a 13-liter heavy-duty engine that matched diesel-baseline torque and kept NOx below 0.2 g/kWh. In 2026, Horse Powertrain and Repsol also disclosed work on a hybrid concept engine designed to run on 100% renewable gasoline, reflecting active programs that support demand for advanced pistons, rings, pins, and related tribology knowledge. Alongside OEM programs, the performance aftermarket continues to drive product refresh cycles, including MAHLE Motorsport launching a new POWERPAK piston kit for the 6.6L Duramax L5P in May 2026.

Recent Industry Developments

- June 2026: Rheinmetall finalized the divestment of its civilian division, the business area that had housed its piston operations. The divestment sharpened Rheinmetall's portfolio focus and changed competitive positioning and capacity ownership in piston-related product lines for automotive and industrial applications.

- May 2026: MAHLE Motorsport launched a new POWERPAK Piston Kit for model year 2024 and newer GM 6.6L Duramax L5P engines, using M174+ alloy and a GRAFAL skirt coating. The release highlights continued innovation in high-load diesel performance segments and supports demand for upgraded piston systems through specialty channels.

- April 2026: MAHLE Powertrain reported converting a 13-liter heavy-duty engine to run on hydrogen while matching the diesel baseline torque and keeping NOx emissions below 0.2 g/kWh. The milestone reinforces the direction of piston system development toward hydrogen-capable designs in commercial-vehicle duty cycles, supporting demand for advanced pistons, ring packs, and pins engineered for new combustion conditions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of piston system components used in automotive internal combustion engines, counted at the point they are sold into vehicle production and replacement demand across major regions.

Scope exclusions: We exclude non-automotive pistons and rings, raw materials sold without conversion into piston parts, and engine subsystems where piston components are not separately priced.

Segmentation Overview

- By Raw Material Type

- Cast Iron

- Aluminum Alloy

- Other Raw Materials (Steel, etc.)

- By Vehicle Type

- Passenger Cars

- Commerical Vehicles

- By Fuel Type

- Gasoline

- Diesel

- By Component Type

- Piston

- Piston Ring

- Piston Pin

- By Geography

- North America

- United States

- Canada

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- South Korea

- Rest of Asia-Pacific

- Rest of the World

- South America

- Middle-East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the base structure for demand and supply, and to keep assumptions realistic before we spoke to industry participants. Public sources such as OICA vehicle production statistics, US EPA and EU emissions rules, national transport agencies, and trade data from UN Comtrade helped us map where engine builds are still concentrated and how powertrain mixes are shifting.

We also reviewed technical and standards information from organizations such as SAE publications, patent databases for material and coating trends, and peer reviewed papers on friction reduction and durability to understand what changes are happening inside the piston system. Company annual reports, investor presentations, and press releases were used to validate capacity adds, plant footprints, and product mix signals, and then a paid subscription database for company financials and a shipment-level trade database were selectively used to cross-check revenue ranges and import-export patterns. These desk sources are not exhaustive, and many other public references were used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and surveys with component manufacturers, engine part distributors, and aftermarket channel participants, and we also spoke with independent technical experts who track engine design changes. Inputs were used to confirm component scope boundaries, typical pricing movement, and the pace of shift across gasoline and diesel applications in APAC, EMEA, and the Americas, before final assumptions were locked.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 12% | APAC: 47% |

| Mid tier: 47% | Functional/Unit leaders: 35% | EMEA: 34% |

| Smaller Players: 16% | Managers: 53% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where vehicle production by region is translated into an engine build pool and then into component demand, using penetration and replacement logic that fits piston, ring, and pin consumption. The totals are then checked through selective bottom-up approximations, where we sanity-test the outcome using sampled price bands times estimated volumes and supplier revenue ranges, and then adjust when the two views drift beyond a reasonable band.

Key inputs in the model include passenger car and commercial vehicle output, the split of gasoline versus diesel engines, the average cylinder count and engine mix trends, replacement rates linked to vehicle parc aging, and typical ASP movement tied to material choices like aluminum alloy versus cast iron. Where direct volume signals are thin, gaps are handled through proxy indicators such as trade flow direction and the share of production in engine-heavy regions, and then the assumptions are confirmed again during follow-up calls.

For forecasting, scenario analysis is used around the speed of electrification and the resilience of ICE and hybrid production, and the final year-by-year path is aligned to expert consensus on powertrain mix and pricing change rather than a single straight-line CAGR.

Data Validation & Update Cycle

Outputs are validated using triangulation across independent signals such as vehicle production, trade movement for key engine parts, and the implied price-volume relationship over time. When a region shows a sudden jump or drop, the drivers are reviewed, assumptions are rechecked, and primary respondents are re-contacted if the change cannot be explained by known capacity moves, regulation shifts, or demand cycles.

Before sign-off, the model is reviewed in multiple steps by another analyst to ensure math consistency, scope discipline, and that the narrative matches the numbers. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery check is done so clients receive the most current view available.

Mordor Intelligence's Automotive Piston System Market Size Compared With Other Published Estimates

Published market sizes for this topic can look far apart, even when the market name sounds the same, because firms often count different components, different revenue points, and different vehicle coverage. The year chosen as the starting point and the way pricing is carried forward also tends to create visible gaps.

By tracking vehicle production-to-engine build linkages and refreshing component-scope checks, Mordor Intelligence keeps the piston, ring, and pin totals tied to automotive demand pools rather than broader powertrain bundles. Some estimates appear to include connecting rods or wider engine assemblies, while others start from a trade-heavy view that can overstate value when parts cross borders multiple times, and these choices can widen the spread quickly.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.02 B (2026) | |

| Trade Publisher A | USD 9.95 B (2024) | Uses a broader piston system definition that can roll in adjacent engine hardware and may mix production and consumption values, which can inflate totals when cross-border shipment counting is not netted out. |

| Industry Publisher B | USD 2.30 B (2025) | Starts from a narrower demand lens with a different base year and product taxonomy, and its pricing progression can be conservative if aftermarket coverage and material-driven ASP uplift are constrained. |

The table shows that the biggest swings come from what is included in the component basket and whether the number represents net demand versus gross trade and production activity. Our approach stays repeatable because the inputs are traceable to clear demand drivers, and assumptions are confirmed through direct industry validation before finalizing the totals.

Key Questions Answered in the Report

What is the current Automotive Piston Engine System Market size?

The Automotive Piston Engine System Market size is USD 4.02 billion in 2026 and is projected to register a CAGR of 4.18% during the forecast period (2026-2031)

Who are the key players in Automotive Piston Engine System Market?

Aisin Seiki, Federal Mogul Holding LLC, Mahle GmbH, Rheinmetall and Tenneco Inc are the major companies operating in the Automotive Piston Engine System Market.

Which is the fastest growing region in Automotive Piston Engine System Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Automotive Piston Engine System Market?

In 2025, the North America accounts for the largest market share in Automotive Piston Engine System Market.

What years does this Automotive Piston Engine System Market cover?

The report covers the Automotive Piston Engine System Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Automotive Piston Engine System Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: