Automotive Hydrostatic Fan Drive System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

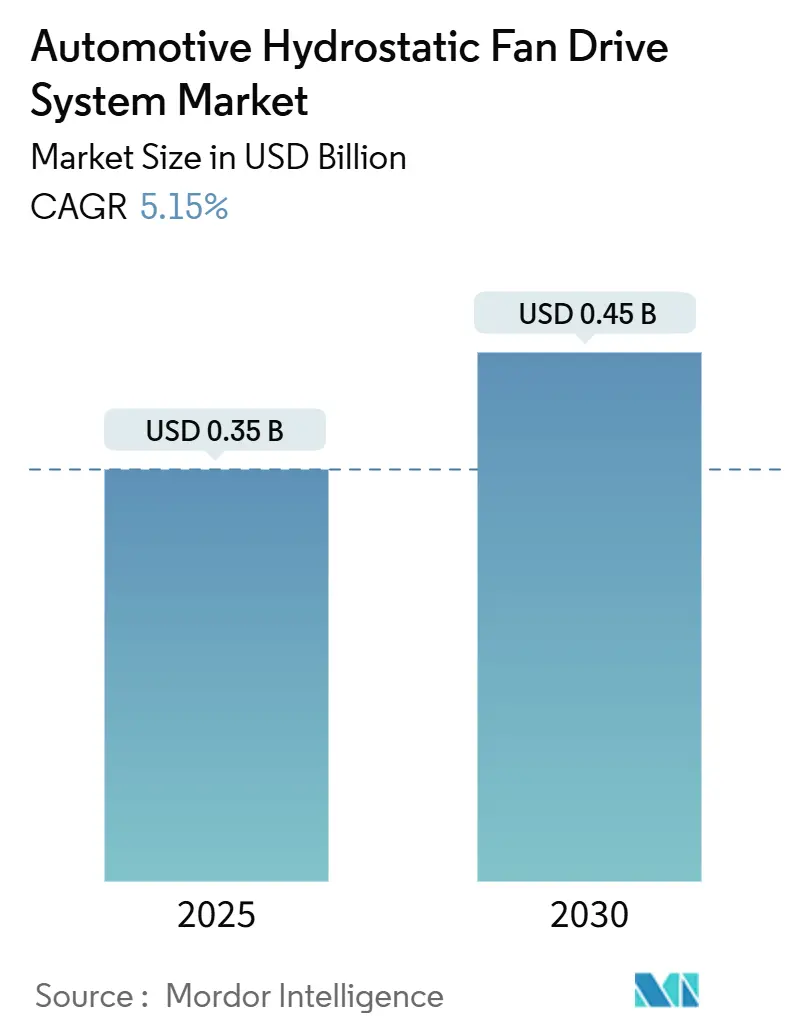

| Market Size (2025) | USD 0.35 Billion |

| Market Size (2030) | USD 0.45 Billion |

| Growth Rate (2025 - 2030) | 5.15% CAGR |

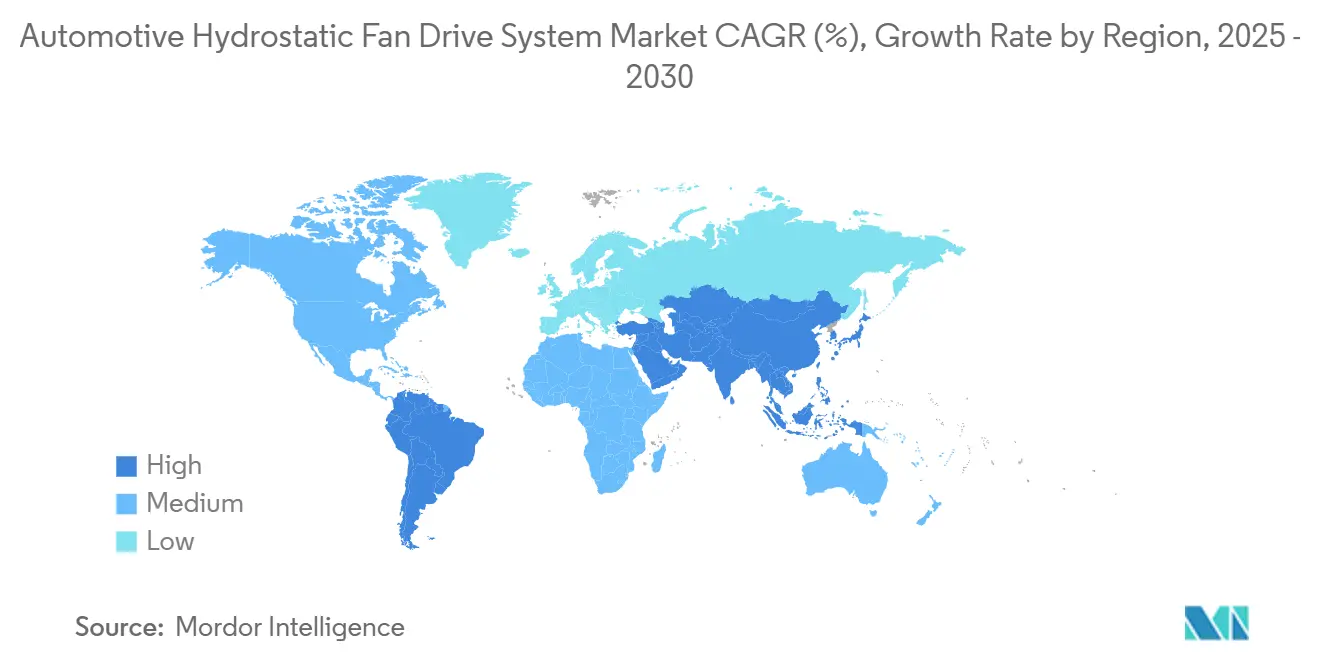

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Hydrostatic Fan Drive System Market Analysis by Mordor Intelligence

The automotive hydrostatic fan drive system market size stands at USD 0.35 billion in 2025 and is projected to hit USD 0.45 billion by 2030, translating into a robust 5.15% CAGR. The technology rises on the twin pillars of stricter global CO₂ and NOx legislation and the automotive sector’s search for cooling solutions that shave parasitic losses without compromising power-train durability. Variable-displacement pumps and hydraulic motors decouple fan speed from engine RPM, helping original-equipment manufacturers meet Euro 7 and similar rules while lowering fleet fuel use. Asia-Pacific commands volume demand thanks to heavy commercial‐vehicle and off-highway production, whereas North America and Europe accelerate adoption for compliance and noise-reduction reasons. Electrification trends add another tailwind, because electro-hydraulic hybrids carry over hydraulic cooling for internal combustion engines while supporting battery and power-electronics thermal management. Competitive intensity remains moderate; component specialists strengthen their positions by blending hydraulic expertise with electronic controls and telematics.

Key Report Takeaways

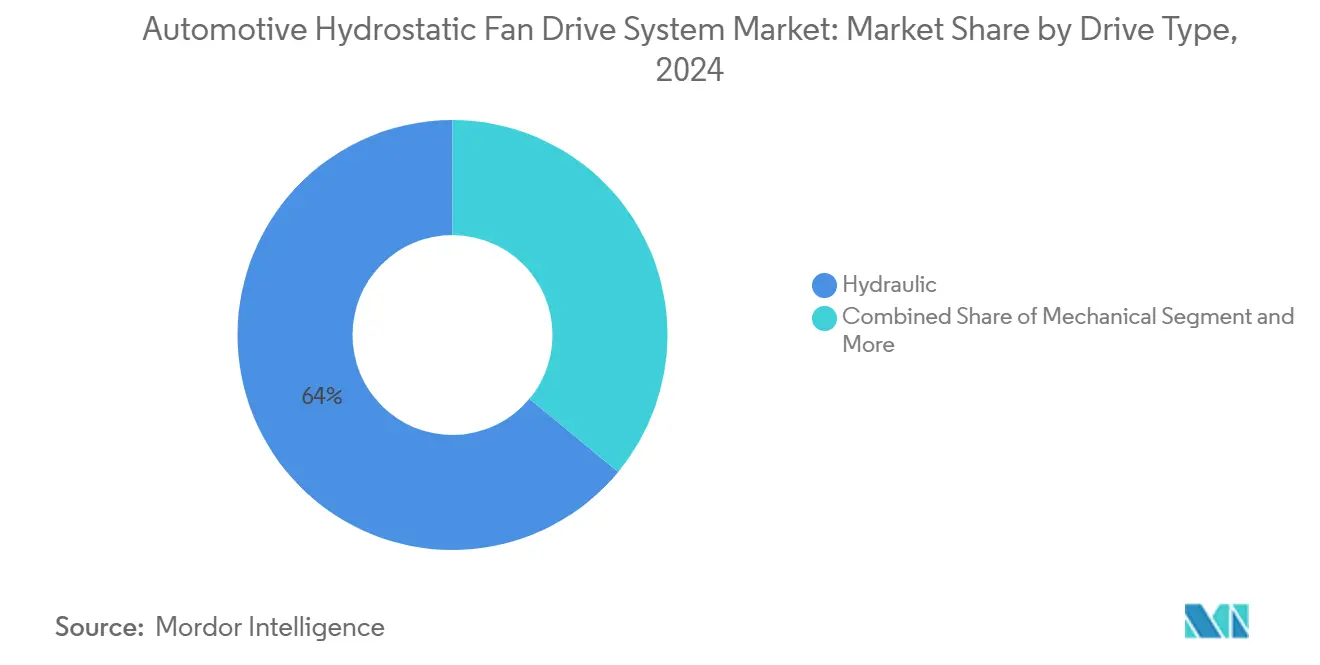

- By drive type, hydraulic configurations held 64.04% of the automotive hydrostatic fan drive system market share in 2024; electric drives are set to register an 8.12% CAGR through 2030.

- By pressure range, medium-pressure systems captured 48.14% of the automotive hydrostatic fan drive system market share in 2024, while high-pressure systems are forecast to post a 5.71% CAGR to 2030.

- By component, hydraulic pumps accounted for 33.55% of the automotive hydrostatic fan drive system market share in 2024; hydraulic valves represent the fastest riser at a 6.02% CAGR.

- By pump type, fixed-displacement designs led with 57.13% of the automotive hydrostatic fan drive system market share in 2024, whereas variable-displacement pumps will advance at 7.04% CAGR over the period.

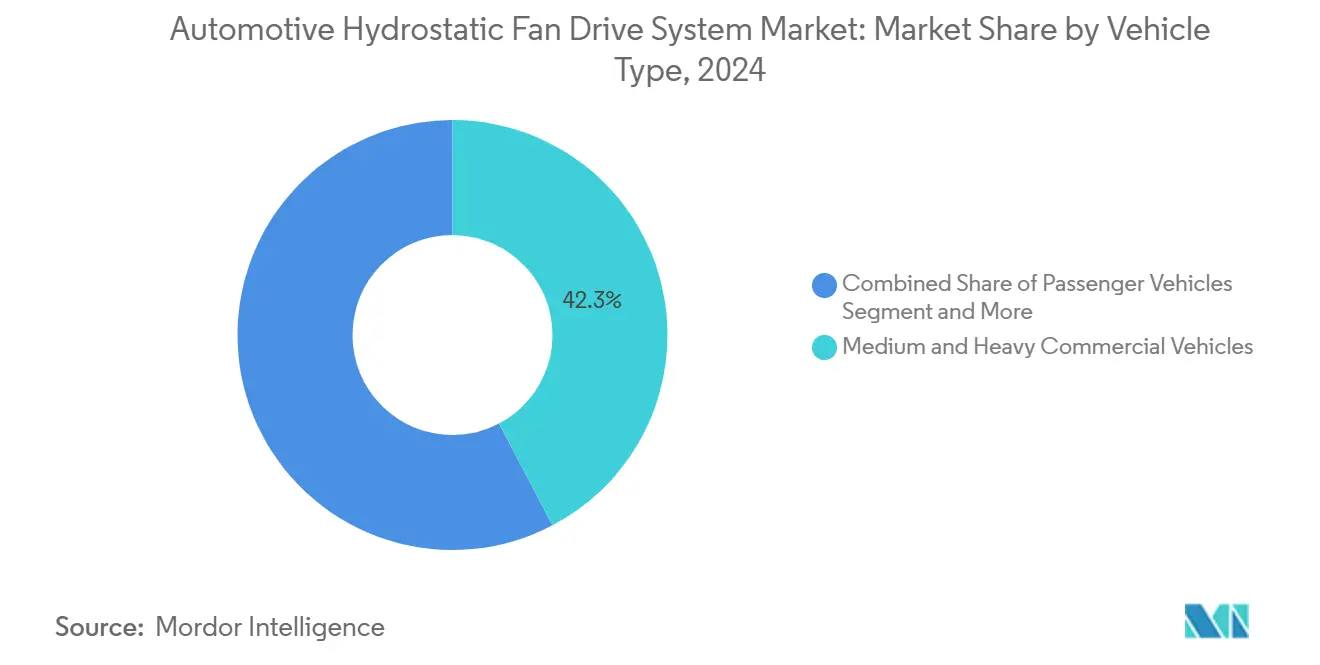

- By vehicle type, medium and heavy commercial vehicles dominated with 42.33% of the automotive hydrostatic fan drive system market share in 2024 and will expand at a 6.82% CAGR up to 2030.

- By application, engine-cooling solutions took 61.14% of the automotive hydrostatic fan drive system market share in 2024; thermal management for e-turbo and e-axle systems is projected to climb 7.26% CAGR through 2030.

- By geography, Asia-Pacific commanded 39.58% of the automotive hydrostatic fan drive system market share in 2024 and is forecast to post the quickest 6.33% CAGR to 2030.

Global Automotive Hydrostatic Fan Drive System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Global CO₂ and NOx Legislation | +1.2% | Global, strongest in the EU and North America | Medium term (2-4 years) |

| Surging Asia-Pacific Off-Highway Vehicle Output | +1.1% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| OEM Quest For Fuel And Noise-Efficient Cooling | +0.9% | Global, premium segments | Short term (≤ 2 years) |

| Electro-Hydraulic Integration in Next-Gen ICEs | +0.8% | North America and the EU, expanding to APAC | Medium term (2-4 years) |

| Predictive-Maintenance Telematics Tie-Ins | +0.6% | Global, fleet-intensive regions | Long term (≥ 4 years) |

| Tariff-Driven Regionalized Supply Chains | +0.4% | North America, secondary in the EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter Global CO₂ and NOx Legislation

Regulations such as Euro 7 are redefining thermal-management strategies. The EU’s Regulation 2024/1257 lengthens warranted life to 160,000 km and adds continuous emissions monitoring, compelling automakers to adopt fan drives that can hold tight temperature windows over wide duty cycles [1]“Regulation 2024/1257 of the European Parliament and of the Council,” European Union, europa.eu. Hydrostatic systems deliver engine-independent fan control that keeps SCR catalysts at target temperatures during low-load urban driving. Because energy savings translate directly into tested CO₂ values, variable-speed hydraulics fit both fuel and emissions targets. Functional-safety rules under ISO 26262 further multiply design requirements, ensuring these cooling modules remain fail-safe for the full life of the vehicle.

Surging Asia-Pacific Off-Highway Vehicle Output

Construction, mining, and agricultural equipment volumes in China and India lift demand for high-power cooling systems. The mobile-hydraulics sector shows the fastest CAGR regionally, driven by infrastructure spending and farm mechanization. India’s auto component industry, equal to 2.3% of GDP, singles out drive-transmission and steering hydraulics for growth. Local manufacturing lowers landed cost and shortens lead times, positioning APAC suppliers for wider global reach.

OEM Quest for Fuel and Noise-Efficient Cooling

Original-equipment makers aim to trim every gram of CO₂ before full electrification. Variable displacement hydraulics cut fan-related power draw by 40-80% compared with fixed mechanical fans. Lower parasitic losses stack directly onto fleet fuel-economy scores, and quieter operation supports premium branding as well as urban-noise limits. Electronic feedback keeps fan speed within ±1 °C of setpoint, yet complexity adds parts and service steps. Suppliers answer with modular units that drop into existing engine bays without major packaging changes.

Electro-Hydraulic Integration in Next-Gen ICEs

Pairing hydraulic power density with electronic fine-tuning gives OEMs new levers for efficiency. Systems use CAN bus links, IoT sensors, and machine-learning algorithms to forecast heat loads. Bosch Rexroth’s Sytronix platform, for example, trims oil volume 75% and slashes cabin noise [2]“Sytronix Variable-Speed Pump Drives,” Bosch Rexroth, boschrexroth.com. The hurdle is maintaining reliability for electronics that sit on vibrating, high-temperature powertrains, yet suppliers see value in fewer hoses and smarter diagnostics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BEV Adoption Shrinking ICE Demand | -1.1% | EU and China lead, North America follows | Long term (≥ 4 years) |

| High Initial and Lifecycle Cost | -0.8% | Global, price-sensitive segments | Short term (≤ 2 years) |

| Scarcity of Hydraulic-Skilled Technicians | -0.4% | Global, acute in developed markets | Medium term (2-4 years) |

| Bio-Fluid ESG Compliance Cost | -0.3% | EU and North America primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

BEV Adoption Shrinking ICE Cooling Demand

Battery electric cars bypass engine cooling altogether, substituting low-temperature loops for batteries and power electronics. Europe and China lead the shift, backed by incentives and charging grids. Hydrostatic suppliers hedge by entering hybrid architectures where both ICE and e-drive need nuanced thermal management, an area well served by variable-speed hydraulics. Off-highway and heavy trucks remain durable niches because long runtimes and payloads still favor diesel for years to come.

High Initial and Lifecycle Cost Vs. Mechanical Fans

A hydrostatic module can cost relatively more than a belt-driven fan, and it entails fluid upkeep plus specialist repairs. These premiums deter budget-focused OEM lines, even when total fuel savings promise payback. Engineering changes add tooling outlays because pumps, hoses, and controllers alter engine-bay layouts. Suppliers respond with standardized kits that drop into multiple vehicle platforms to dilute design spend over larger volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drive Type: Hydraulic Strength Anchors the Transition

Hydraulic drives locked in 64.04% of the automotive hydrostatic fan drive system market share in 2024. Variable-displacement designs deliver high torque at crawl speeds, a must for heavy trucks and off-highway gear. Electric drives, however, post the strongest 8.12% CAGR because they integrate cleanly with evolving vehicle networks. Bosch Rexroth’s 2025 HydraForce acquisition illustrates how suppliers blend hydraulic muscle with electronic brains to set up electro-hydraulic hybrids. Over the outlook, fleets will adopt mixed architectures that keep hydraulics for high force yet switch to electric actuation where precision rules.

Hydraulic systems keep an edge in dependability under mud, dust, or extreme heat, making them the go-to for mines and construction sites. Nonetheless, electric units reach more than 90% efficiency at part load compared with 60-70% for hydraulics, narrowing cost-of-ownership gaps for urban delivery trucks. As engine bays free up with downsized ICE blocks, OEMs will find mounting room for compact e-motors, and suppliers ready with dual-platform kits can ride both waves of demand.

By Pressure Range: Medium Platforms Hold Center Stage

Medium-pressure solutions (151-300 bar) claimed 48.14% of the automotive hydrostatic fan drive system market share in 2024, balancing compact size against cost and seal life. High-pressure lines above 300 bar register a 5.71% CAGR thanks to tighter engine packaging and weight-reduction drives. Danfoss Power Solutions debuted its X1P pump family rated to 310 bar continuous duty, showing the segment’s material advances. Low-pressure sets serve light vans and passenger cars where cooling loads stay limited.

The climb toward higher pressures signals thinner wall sections, better surface treatments, and refined manufacturing that keep fatigue cycles above 10,000 hours. Yet rising pressures demand cleaner fluid and tougher filtration, nudging operating cost up unless paired with smart sensors that extend service intervals. Fleets spoilt for uptime will gravitate toward mid-pressure kits unless packed engine bays force the shift upward.

By Component: Pumps Remain the Power Core

Hydraulic pumps accounted for 33.55% of the automotive hydrostatic fan drive system market share in 2024. Variable-displacement axial-piston models eclipse fixed-gear units by matching flow to real-time demand. Hydraulic valves, the fastest climber with 6.02% CAGR, gain from the pivot to refined electronic control, as metering edges must stay tight when engine and ambient temperatures swing.

Motors follow pumps in share, employing bent-axis layouts that mix high torque with compact length. Integrated cooler blocks and reservoir modules cut hose count, boosting reliability. Sensor-rich "smart blocks" that combine pressure, temperature, and contamination monitoring create fresh revenue tiers while anchoring predictive-maintenance features that fleets now expect.

By Pump Type: Variable Displacement Unlocks Efficiency

Fixed-displacement hardware still supplied 57.13% of the automotive hydrostatic fan drive system market share in 2024 because of its lower ticket price and easier rebuilds. Yet variable-displacement pumps rise at 7.04% CAGR as OEMs chase fuel savings. Matching output to exact fan power trims wasted flow, dropping energy use by up to 50%. Advanced controls enable load-sensing loops that relieve excess pressure and automatic reversals that purge debris from radiators.

The payoff multiplies for trucks in congestion or idling at ports, where airflow needs fall even as engine speed stays high. Suppliers bundle electronic control units that talk over J1939 or CAN-FD, easing integration with modern power-train controllers. Over time, economies of scale should narrow price deltas, steering most new platforms to variable technology.

By Vehicle Type: Commercial Fleets Lead Adoption Curve

Medium and heavy commercial vehicles supplied 42.33% of the automotive hydrostatic fan drive system market share in 2024 revenue and will sprint ahead at 6.82% CAGR. Long daily routes and repeated PTO idling scenarios press operators to recoup every fuel dollar. Hydrostatic cooling reduces engine drag and prolongs after-treatment life, matching Euro 7 de-rating avoidance goals.

Light commercial vans now explore the technology for last-mile deliveries because stop-start duty and urban noise caps favor variable fans. Passenger cars remain a small but visible user base, mostly in premium SUVs with tow packages that generate high heat loads. As hybrid SUVs increase, they may carry over hydraulic cooling for ICE components, lengthening the passenger-car runway.

By Application: Engine Cooling Stays the Anchor, E-Turbo Gains Pace

Engine cooling retained a 61.14% of the automotive hydrostatic fan drive system market share in 2024, cementing the category’s link to traditional power-train design. Hydrostatic drives let OEMs hit narrow thermal-window targets that protect pistons and valve seats while enabling quick catalyst light-off.

Looking forward, thermal management (e-turbo and e-axle cooling) will rise at a 7.26% CAGR. These devices pack electronics and hot gas in confined casings, pushing localized heat flux well beyond legacy turbos. A variable-flow hydraulic fan can ramp airflow at ignition and taper once temperature stabilizes, saving power yet preserving reliability. Emission control modules such as SCR bricks and DPF units also benefit when fan speeds adjust to keep wall temperatures stable during low-load traffic.

Geography Analysis

Asia-Pacific retained a 39.58% of the automotive hydrostatic fan drive system market share in 2024 and should clock a 6.33% CAGR through 2030, making it the largest as well as the fastest regional block. Construction booms in China, India, and Indonesia drive high-horsepower equipment that leans on hydrostatic fans to work amid dust, altitude, and torrid weather. India’s component sector targets hydraulic drive-train parts, aiming to lift GDP contribution and export earnings [3]“Automotive Component Sector Performance,” Ministry of Commerce & Industry, commerce.gov.in. APAC suppliers enjoy labor-cost and proximity benefits that help them win global sourcing contracts on value as well as volume.

North America ranks second, lifted by stringent EPA and CARB rules that sharpen demand for fuel-efficient cooling. Yet tariffs introduced in 2025 reshape supply chains, nudging OEMs toward U.S.-made pumps, motors, and valves. The hydraulic-valve subsector alone is set to hold significant revenue by 2034, and the United States will also grow in the coming timeframe. These stats underline domestic momentum even as some newer electric trucks skip engine-centric cooling.

Europe grows steadily under the Euro 7’s shadow, marrying emissions targets with stewardship goals such as biodegradable hydraulic fluid. Lubricant makers note new Eco-label criteria that demand at least 25% bio-carbon content. OEMs order modular fan drives that handle multiple heat sources, cutting component count to offset battery-package space loss in hybrids. While BEV push dampens long-range engine cooling demand, trucks and off-highway machines keep pulling orders for premium, low-noise hydrostatic kits.

Competitive Landscape

The automotive hydrostatic fan drive system market is moderately fragmented because no vendor owns a cross-segment monopoly. Bosch Rexroth, Danfoss Power Solutions, Parker Hannifin, Bucher Hydraulics, and Eaton make up the core, with regional champions rounding out the share. Suppliers compete on total solution value, bundling pumps, motors, valves, sensors, software, and installation know-how instead of price alone.

Recent M&A signals a pivot to wider capability. Bosch Rexroth’s 2025 HydraForce purchase widens its cartridge-valve suite and strengthens electro-hydraulic integration, while Bucher Hydraulics’ Hydman Oy deal secures Nordic manifold expertise. The acquisition of TI Fluid Systems by ABC Technologies demonstrates investor confidence in cooling and fluid-handling platforms, giving the combined firm a springboard into electro-thermals.

Strategic roadmaps stress predictive maintenance and IoT readiness. Components now ship Bluetooth or 4G gateways that sync condition data with fleet portals. In markets where technician downtime is costly, such services tilt buying decisions. Players with continent-wide service lorries and remote-assist apps add another moat, raising entry barriers for smaller rivals.

Automotive Hydrostatic Fan Drive System Industry Leaders

Bosch Rexroth AG

Danfoss Power Solutions

Eaton Corporation

Parker Hannifin Corporation

JTEKT HPI

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: ABC Technologies closed the EUR 1.8 billion (USD 2.38 billion) takeover of TI Fluid Systems, forming TI Automotive with broadened fluid-management capabilities across fuel, thermal, and brake segments.

- November 2024: Bucher Hydraulics finalized the purchase of Finland-based Hydman Oy, adding EUR 13 million in tailored hydraulic-manifold revenue and boosting its European customer proximity.

- July 2023: Bosch Rexroth completed the acquisition of HydraForce, enhancing cartridge-valve technology depth and electronic-control portfolios for mobile hydraulics.

Global Automotive Hydrostatic Fan Drive System Market Report Scope

| Hydraulic |

| Electric |

| Mechanical |

| Low Pressure (Less than/equals 150 bar) |

| Medium Pressure (151-300 bar) |

| High Pressure (Above 300 bar) |

| Hydraulic Pump |

| Hydraulic Motor |

| Oil Cooler |

| Hydraulic Valves |

| Others (Sensors, ECU, Reservoirs) |

| Fixed Displacement Pump |

| Variable Displacement Pump |

| Passenger Vehicles |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Engine Cooling |

| Thermal Management (E-Turbo, E-Axle) |

| Emission Control Sub-systems |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Drive Type | Hydraulic | |

| Electric | ||

| Mechanical | ||

| By Pressure Range | Low Pressure (Less than/equals 150 bar) | |

| Medium Pressure (151-300 bar) | ||

| High Pressure (Above 300 bar) | ||

| By Component | Hydraulic Pump | |

| Hydraulic Motor | ||

| Oil Cooler | ||

| Hydraulic Valves | ||

| Others (Sensors, ECU, Reservoirs) | ||

| By Pump Type | Fixed Displacement Pump | |

| Variable Displacement Pump | ||

| By Vehicle Type | Passenger Vehicles | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Application | Engine Cooling | |

| Thermal Management (E-Turbo, E-Axle) | ||

| Emission Control Sub-systems | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the automotive hydrostatic fan drive system market expected to grow?

It is forecast to expand at a 5.15% CAGR from USD 0.35 billion in 2025 to USD 0.45 billion in 2030.

Which vehicle category drives the greatest demand?

Medium and heavy commercial vehicles account for 42.33% of 2024 revenue and will post a 6.82% CAGR to 2030.

Why are hydraulic drives still dominant over electric drives?

Hydraulic systems deliver higher torque at low speeds and proven reliability in severe off-highway conditions, holding 64.04% share in 2024.

What is the biggest regional market today?

Asia-Pacific leads with 39.58% share and is projected to show the fastest 6.33% CAGR up to 2030.

Page last updated on: