Automotive Cooling Fan Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

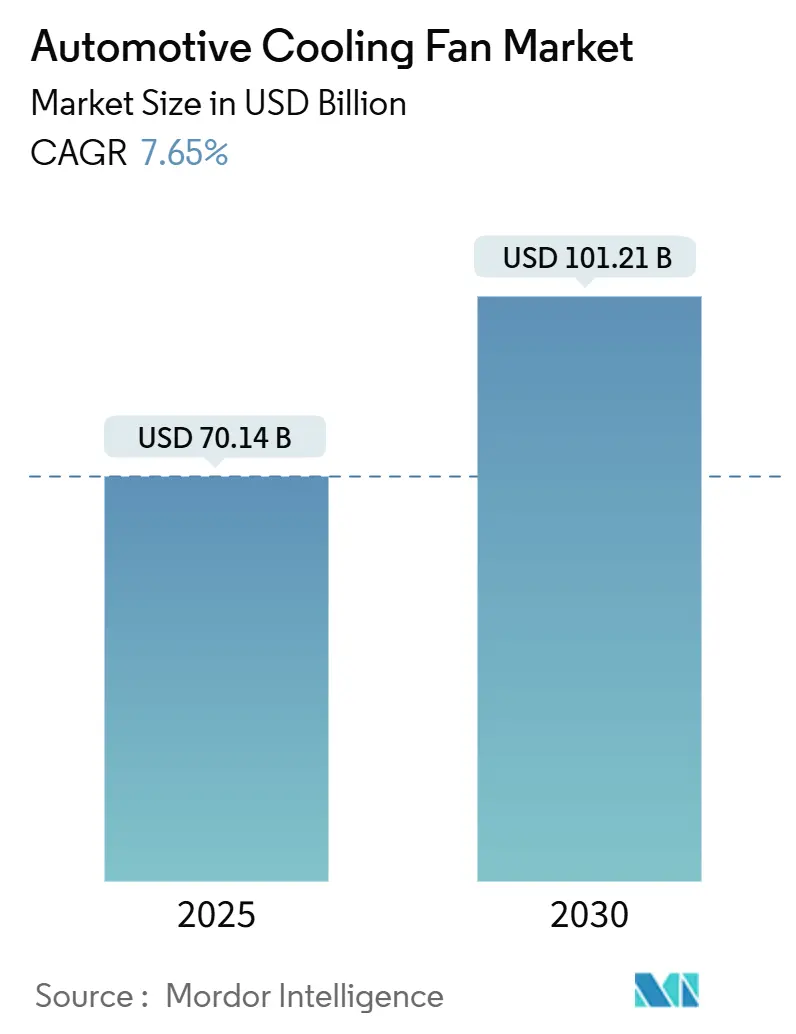

| Market Size (2025) | USD 70.14 Billion |

| Market Size (2030) | USD 101.21 Billion |

| Growth Rate (2025 - 2030) | 7.65% CAGR |

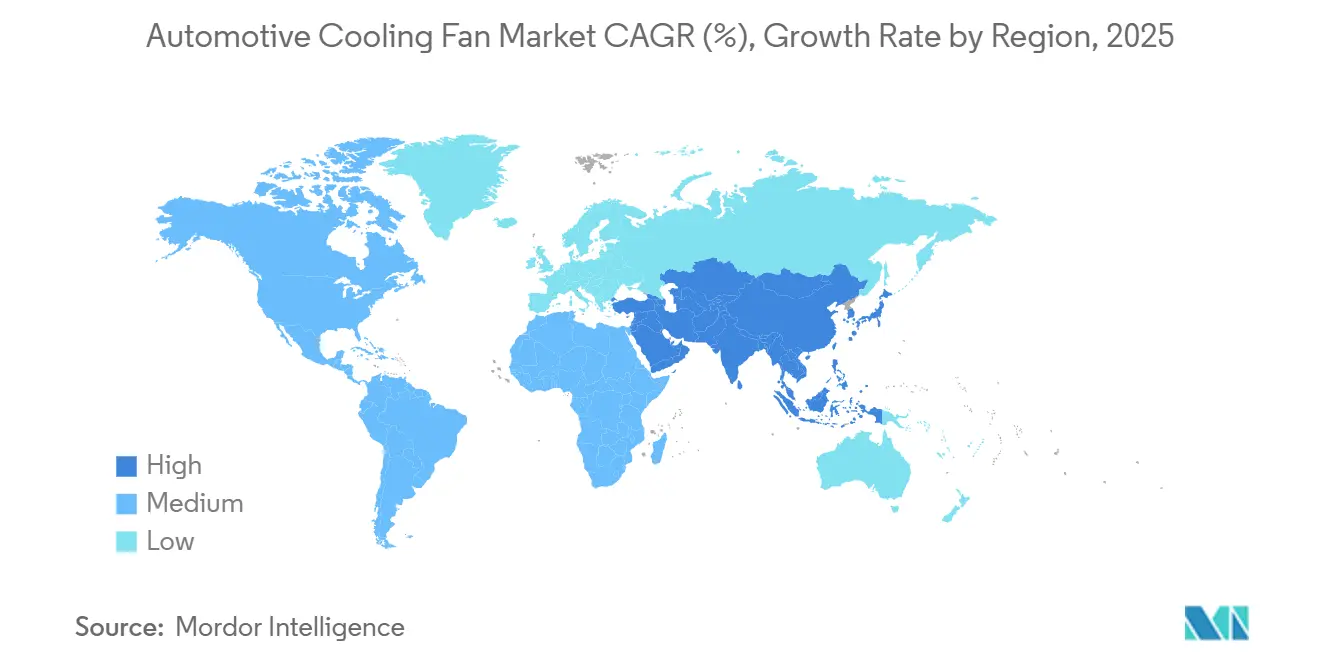

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Cooling Fan Market Analysis by Mordor Intelligence

The automotive cooling fan market size stood at USD 70.14 billion in 2025 and is projected to reach USD 101.21 billion by 2030, progressing at a 7.65% CAGR over the forecast period. The growth outlook reflects escalating demand for sophisticated thermal management across electrified, hybrid, and efficient internal-combustion powertrains. Stricter emissions rules in North America, Europe, and large Asian economies are accelerating the shift from belt-driven fans to energy-efficient electric units capable of precise temperature control. Battery electric vehicle (BEV) penetration is creating new cooling points—pack, power electronics, and cabin—while 48 V mild-hybrid platforms supply the electrical headroom needed for high-capacity brushless fans. Competitive dynamics are sharpening as Chinese suppliers go global and established Tier-1s counter with integrated modules, patented aero-acoustic designs, and data-driven control algorithms. The automotive cooling fan market therefore sits at the intersection of regulatory pressure, electrification, and digitalization.

Key Report Takeaways

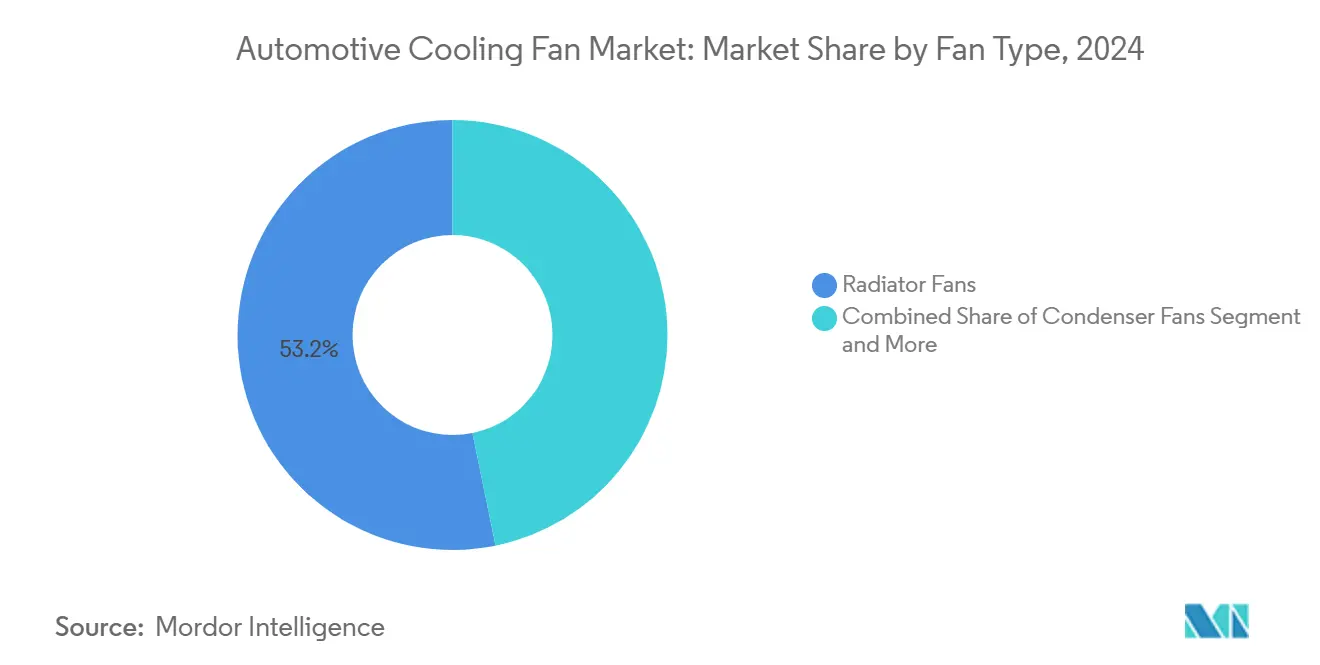

- By fan type, radiator fans held 53.19% of the automotive cooling fan market share in 2024.

- By fan type, heat ventilation fans are forecast to advance at a 9.42% CAGR through 2030.

- By vehicle type, passenger vehicles accounted for a 67.34% share of the automotive cooling fan market size in 2024.

- By vehicle type, light commercial vehicles are projected to expand at an 8.71% CAGR through 2030.

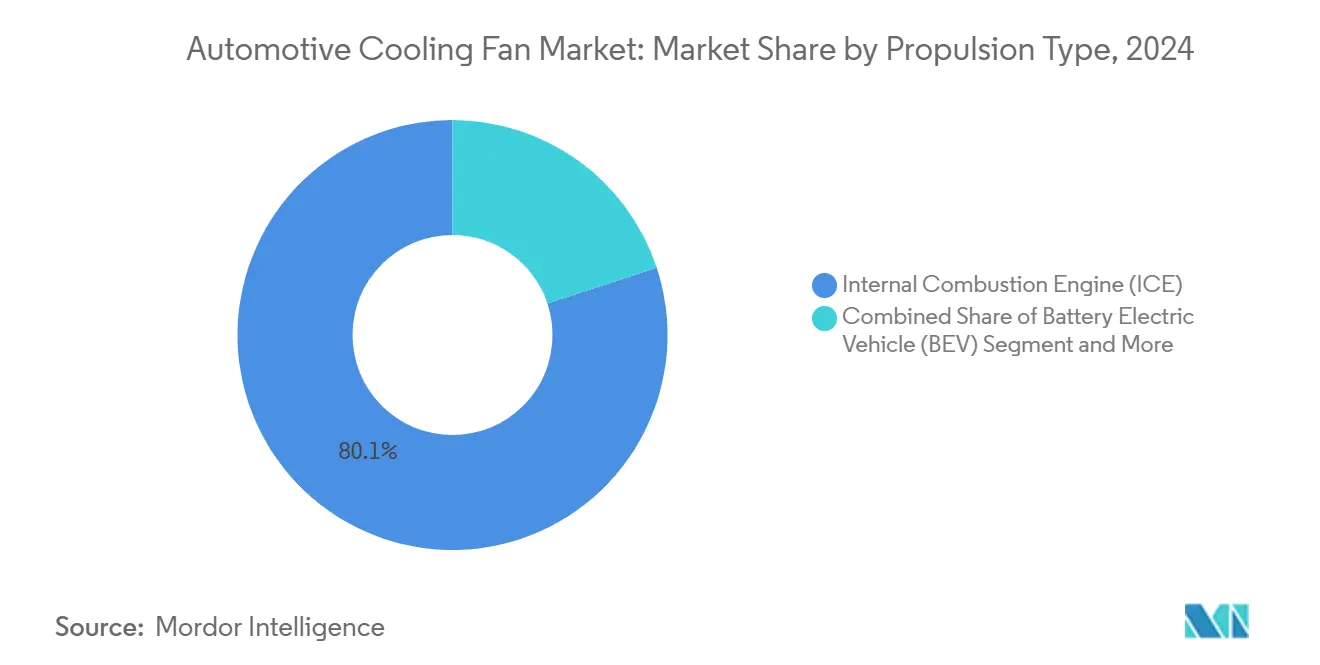

- By propulsion type, internal-combustion engines retained an 80.08% share in 2024, whereas battery electric vehicles will grow at a 22.03% CAGR to 2030.

- By geography, Asia-Pacific commanded a 50.17% revenue share in 2024; South America is anticipated to post the highest regional CAGR, at 7.26%, to 2030.

Global Automotive Cooling Fan Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Point Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Vehicle Output In Emerging Markets | +1.8% | Asia-Pacific, South America, MEA | Medium Term (2–4 Years) |

| Shift From Mechanical To Electric Fans | +1.5% | Global; Early Uptake In North America and EU | Short Term (≤ 2 Years) |

| Tighter Emissions and Fuel-Economy Rules | +1.2% | North America and EU, Expanding In Asia-Pacific | Long Term (≥ 4 Years) |

| Rapid EV/HEV Fleet Expansion | +2.1% | Global; Led By China, EU, North America | Medium Term (2–4 Years) |

| AI-Enabled Predictive Fan Controllers | +0.7% | North America and EU Premium Segments | Long Term (≥ 4 Years) |

| Aero-Acoustic Blade Designs For NVH | +0.4% | North America and EU Premium Segments | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Rising Global Vehicle Production in Emerging Markets

China produced 30.16 million vehicles in 2024, while India’s passenger-vehicle sales climbed 8.89% year-over-year, underscoring strong build rates that translate directly into cooling-system demand[1]"Optimization of Cooling Circuit for Electric Vehicle 2024-28-0092," SAE, sae.org.. Scaling plants in Indonesia, Thailand, and Brazil follow similar trajectories. As Euro-6-equivalent norms enter these jurisdictions, OEMs specify electric fans that deliver tighter temperature windows without meaningful price escalation. Suppliers localize casting, stamping, and winding to secure volume contracts and blunt logistics costs, reinforcing Asia-Pacific’s 50.17% revenue leadership within the automotive cooling fan market.

Shift from Mechanical to Energy-Efficient Electric Fans

Ford documented 0.5–1.3 g/mi CO₂ savings after adopting brushless-motor cooling fans, a result validated by the U.S. off-cycle credit program[2]"Alternative Methods for Calculating Off-Cycle Credits Under the Light-Duty Vehicle Greenhouse Gas Emissions Program: Applications From Ford Motor Company," Federal Register, federalregister.gov.. Variable-speed fans integrate via CAN or LIN to the engine control unit, enabling pulse-width-modulated airflow tailored to load, ambient temperature, and vehicle speed. This flexibility supports cylinder deactivation, idle-stop, and active grille shutters, turning formerly parasitic hardware into a fuel-savings lever. Demand is strongest where 48 V architectures proliferate because higher system voltage trims wire gauge and enables 600+ W fan modules.

Stricter Emissions and Fuel-Economy Regulations

Euro 7, effective November 2026, lengthens durability to 160,000 km and tightens particulate counting thresholds to 10 nm[3]"Regulation (EU) 2024/1257 of the European Parliament and of the Council of 24 April 2024 on type-approval of motor vehicles and engines and of systems, components and separate technical units intended for such vehicles, with respect to their emissions and battery durability (Euro 7)," EUR-Lex, eur-lex.europa.eu.. Similar greenhouse-gas curves in the United States raise the bar for transient thermal control of catalysts, SCR, and gasoline particulate filters. Electric fans must now survive extended duty cycles, integrate diagnostics for onboard monitoring, and coordinate with electrified heaters or waste-heat recovery. Suppliers shift to ball-bearing brushless motors, IP6K9K sealing, and ISO 26262-compliant electronics, raising the technology floor across the automotive cooling fan market.

Rapid Expansion of EV/HEV Fleet Requiring Advanced Thermal Management

Precise battery temperature is essential for preventing thermal runaway and sustaining cycle life. Air-assisted liquid loops deploy compact axial fans to remove heat from chillers, pack surface plates, or condenser coils. Patent activity in AI-based thermal management reached 139 filings by February 2025, a testament to burgeoning investment in predictive algorithms that schedule fan duty based on route, ambient conditions, and driving style. China, Europe, and California mandate ever-tighter degradation warranties, expanding demand for intelligent fans with embedded controllers and telematics connectivity.

Restraints Impact Analysis*

| Restraint | (~) % Point Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Raw-Material Prices | -1.4% | Global; Aluminum and Copper | Short Term (≤ 2 Years) |

| OEM Cost Pressure and Commoditization | -0.9% | Global; High-Volume Segments | Medium Term (2–4 Years) |

| Durability of Lightweight Polymer Assemblies | -0.6% | Global; Extreme Climates | Medium Term (2–4 Years) |

| Liquid Cold-Plate Adoption in EVs | -0.8% | Premium BEVs Globally | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Volatile Raw-Material Prices Driving Cost Pressures

Aluminum and copper price swings in 2024 forced many suppliers to renegotiate six-month indexation clauses rather than fixed annual contracts. Brushless stators depend on copper windings whose spot cost surged more than 20% in some months, pinching margins. Lightweight polymer housings mitigate weight and damp corrosion but require glass-fiber reinforcement to match thermal distortion requirements, elevating resin complexity and cost.

OEM Price Pressure and Product Commoditization

Platform consolidation means a single global SUV program can require 1 million fans annually, pushing OEM purchasing to treat the component as near-commodity. Chinese entrants leverage vertically integrated casting and winding, winning business on price and delivery speed. Tier-1 incumbents respond with modular fan families sharing motors and ECU cores, spreading tooling over larger runs to claw back competitiveness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fan Type: Radiator Fans Drive Market Leadership

Radiator fans command 53.19% market share in 2024, reflecting their essential role in engine cooling across all propulsion types, while heat ventilation fans demonstrate the strongest growth trajectory at 9.42% CAGR through 2030. The dominance of radiator fans stems from their universal application across internal combustion engines, hybrid systems, and electric vehicle thermal management architectures. Condenser fans maintain steady demand driven by air conditioning system requirements, though their growth moderates as heat pump technologies gain adoption in electric vehicles. Heat ventilation fans experience accelerated growth due to increasing cabin air quality requirements and the integration of advanced HVAC systems with predictive climate control capabilities.

The segment evolution reflects technological advancement in fan blade design and motor efficiency, with manufacturers developing aero-acoustic optimized blades that reduce noise while maintaining airflow performance. SPAL Automotive's introduction of 800V high-voltage brushless axial fans demonstrates the industry's progression toward higher power density solutions for heavy-duty and low-emission vehicle applications. The "Others" category encompasses specialized applications, including oil cooler fans and auxiliary cooling modules that support advanced powertrain configurations, representing emerging opportunities as vehicle architectures become more complex.

By Vehicle Type: Passenger Vehicles Maintain Dominance

Passenger vehicles are set to maintain a dominant 67.34% market share in 2024. Meanwhile, e-commerce expansion and the electrification of last-mile delivery are propelling light commercial vehicles to become the fastest-growing segment, boasting an 8.71% CAGR through 2030. The commercial vehicle segment benefits from accelerated electrification timelines as fleet operators prioritize total cost of ownership and regulatory compliance. Medium and heavy commercial vehicles demonstrate steady growth supported by stringent emissions regulations that require sophisticated thermal management for aftertreatment systems and the gradual adoption of electric powertrains in urban delivery applications.

Passenger vehicle cooling requirements evolve with autonomous driving technology integration, necessitating enhanced NVH performance and thermal stability for sensor systems and computing hardware. The segment's growth moderates compared to commercial applications due to market maturation in developed regions, though emerging market expansion provides sustained demand. Electric vehicle adoption within passenger segments creates distinct thermal management requirements, including battery cooling, power electronics thermal control, and cabin conditioning systems that operate independently of engine waste heat.

By Propulsion Type: Electric Powertrains Reshape Demand

Despite internal combustion engines (ICEs) continuing to dominate with an 80.08% market share in 2024, battery electric vehicles (BEVs) are experiencing a robust surge at a 22.03% CAGR projected through 2030. This growth is fundamentally altering cooling fan requirements. The propulsion type transformation creates distinct market segments with different thermal management priorities and performance specifications. Hybrid and plug-in hybrid electric vehicles require dual cooling architectures that support both engine thermal management and battery conditioning, creating complexity that drives demand for integrated cooling solutions.

Fuel cell electric vehicles represent an emerging segment requiring specialized cooling for fuel cell stacks, hydrogen storage systems, and power electronics. However, market penetration remains limited to specific applications and regions. The transition toward electrified powertrains necessitates cooling fan designs optimized for different duty cycles, with electric vehicles requiring intermittent high-performance cooling rather than the continuous operation typical of internal combustion engines. Machine learning-based thermal management systems enable predictive cooling strategies that optimize energy consumption while maintaining component reliability.

By Distribution Channel: Aftermarket Gains Momentum

The OEM channel controls 70.21% market share in 2024, leveraging integrated supply relationships and just-in-time delivery requirements, while the aftermarket segment accelerates at 7.84% CAGR through 2030. Aftermarket growth reflects vehicle fleet aging, increasing maintenance requirements for complex thermal management systems, and the availability of performance upgrade options for enthusiast segments. The channel dynamics shift as electric vehicle adoption increases, creating new aftermarket opportunities for battery cooling system components and thermal management upgrades.

OEM relationships remain critical for high-volume applications and new vehicle integration, though suppliers increasingly develop aftermarket strategies to capture replacement demand and performance enhancement opportunities. The distribution channel evolution reflects changing vehicle ownership patterns, with subscription and mobility services creating distinct maintenance and replacement cycles. Performance Airflow's emphasis on genuine SPAL components demonstrates the aftermarket's focus on quality differentiation and warranty support to compete against lower-cost alternatives.

Geography Analysis

Asia-Pacific dominates with 50.17% market share in 2024, driven by China's automotive manufacturing scale and India's expanding production capacity, while regional growth reflects the transition toward electric vehicle thermal management systems. China's automotive production leadership creates substantial cooling fan demand, supported by government policies promoting new energy vehicles and stringent emissions standards for conventional powertrains. India's passenger vehicle market growth of 8.89% in 2024 generates increasing demand for cost-effective cooling solutions that meet durability requirements in challenging climate conditions. Japan and South Korea contribute advanced technology development, particularly in electric vehicle thermal management and AI-driven cooling control systems. The region's manufacturing cost advantages and supply chain integration create competitive dynamics that influence global pricing structures and technology adoption patterns.

South America emerges as the fastest-growing region at 7.26% CAGR through 2030, reflecting automotive industry modernization and increasing adoption of energy-efficient cooling technologies. Brazil's automotive sector benefits from government incentives for vehicle electrification and emissions compliance, creating demand for advanced cooling solutions. Argentina's automotive production expansion and integration with global supply chains drives cooling fan market growth, particularly in commercial vehicle segments. The region's growth trajectory reflects infrastructure development, regulatory alignment with international standards, and increasing consumer demand for vehicles with advanced thermal management capabilities. Local manufacturing development reduces import dependencies and enables cost-competitive cooling fan production for regional and export markets.

North America and Europe demonstrate mature market characteristics with steady growth supported by regulatory requirements and technology advancement. The EU's Euro 7 regulation implementation creates demand for cooling fans with extended durability specifications and diagnostic integration capabilities. North American markets benefit from electric vehicle adoption acceleration and the integration of predictive maintenance technologies that optimize cooling system performance. Both regions emphasize premium cooling solutions with advanced control capabilities, NVH optimization, and integration with vehicle connectivity systems. The regulatory frameworks in these regions influence global technology development and create opportunities for suppliers developing compliance-ready cooling solutions.

Competitive Landscape

The automotive cooling fan market exhibits moderate concentration with established tier-1 suppliers leveraging OEM relationships and manufacturing scale advantages, while emerging competition from Chinese manufacturers and electric vehicle specialists intensifies pricing pressure and accelerates innovation cycles. Market leaders including DENSO, Valeo, and Bosch maintain competitive positions through integrated thermal management solutions, advanced manufacturing capabilities, and global supply chain networks that support just-in-time delivery requirements. The competitive dynamics shift as electric vehicle adoption creates opportunities for specialized suppliers offering battery cooling solutions and AI-driven thermal management systems.

Technology differentiation becomes increasingly critical as cooling fan specifications evolve toward higher efficiency, extended durability, and integration with vehicle electronics systems. Patent activity in AI-driven thermal management reached 139 filings by February 2025, indicating substantial innovation investment in predictive cooling control systems. White-space opportunities emerge in aftermarket performance cooling solutions, specialized applications for autonomous vehicles, and integrated thermal management modules for electric commercial vehicles. The competitive landscape evolution reflects the industry's transition toward electrified powertrains and the increasing importance of thermal management in vehicle performance and efficiency optimization.

Automotive Cooling Fan Industry Leaders

-

DENSO Corporation

-

Valeo SA

-

Robert Bosch GmbH

-

Continental AG

-

SPAL Automotive Srl

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Marelli Corporation signed a strategic cooperation agreement with Hilite Automotive Systems (Changshu) Co., Ltd. at its Wuxi site to cooperate on integrated New Energy Vehicle thermal management modules and electronic expansion valves, targeting comprehensive NEV thermal-management solutions.

- February 2025: Airtificial Group (Spain) signed a contract with a German Tier-1 supplier that supplies battery cooling systems for SEAT Cupra to develop, manufacture and deliver turnkey intelligent robotics for assembly equipment, executed by Airtificial's robotics intelligence business unit.

- January 2025: Hankook & Company Group completed acquisition of Hanon Systems (world's second-largest automotive thermal management solutions provider) and became majority shareholder (54.77%) after purchases in December 2024–January 2025, positioning the group among Korea's top 30 corporations by net assets.

Global Automotive Cooling Fan Market Report Scope

| Radiator Fans |

| Condenser Fans |

| Heat Ventilation Fans |

| Others |

| Passenger Vehicles |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Internal Combustion Engine (ICE) |

| Battery Electric Vehicle (BEV) |

| Hybrid Electric Vehicle (HEV) |

| Plug-In Hybrid Electric Vehicle (PHEV) |

| Fuel Cell Electric Vehicle (FCEV) |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Fan Type | Radiator Fans | |

| Condenser Fans | ||

| Heat Ventilation Fans | ||

| Others | ||

| By Vehicle Type | Passenger Vehicles | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Propulsion Type | Internal Combustion Engine (ICE) | |

| Battery Electric Vehicle (BEV) | ||

| Hybrid Electric Vehicle (HEV) | ||

| Plug-In Hybrid Electric Vehicle (PHEV) | ||

| Fuel Cell Electric Vehicle (FCEV) | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the automotive cooling fan market be by 2030?

It is forecast to reach USD 101.21 billion, advancing at a 7.65% CAGR from 2025.

Which fan type generates the highest revenue?

Radiator fans dominate with 53.19% share in 2024 due to universal engine and inverter cooling needs.

Why are electric fans replacing mechanical designs?

Electric variants cut parasitic losses, enable precise thermal control, and help automakers meet tougher emissions and fuel-economy targets.

Where is demand growing fastest?

South America leads regional growth at a projected 7.26% CAGR through 2030 as modernization and electrification accelerate.

How are BEVs changing cooling requirements?

Battery packs, inverters, and cabin heat pumps require multiple smaller fans that operate in predictive, pulse-type cycles rather than continuous engine-driven airflow.

What is driving aftermarket expansion?

Aging vehicle fleets and rising complexity boost replacement rates, while e-commerce platforms improve parts availability and installation scheduling.

Page last updated on: