Automotive Electric Water Pump Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 4.41 Billion |

| Market Size (2030) | USD 8.36 Billion |

| Growth Rate (2025 - 2030) | 13.61% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Electric Water Pump Market Analysis by Mordor Intelligence

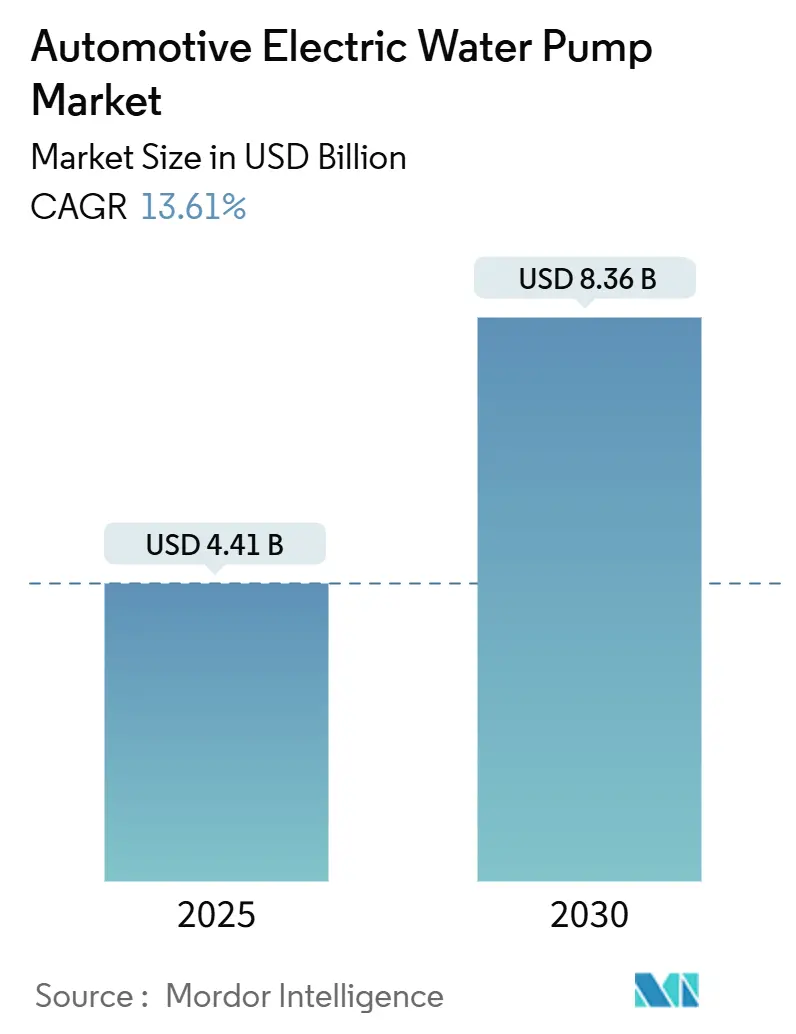

The Automotive Electric Water Pump Market size is estimated at USD 4.41 billion in 2025, and is expected to reach USD 8.36 billion by 2030, at a CAGR of 13.61% during the forecast period (2025-2030). This trajectory underscores the accelerating migration to electrified powertrains, the quest for reduced parasitic losses, and rising thermal-management complexity as vehicle architectures move to 800 V platforms. Automakers worldwide install software-controlled coolant circulation independently of engine speed, helping them comply with tightening Euro 7, CAFE, and China GB standards while extending battery and power-electronics life. Tier-1 suppliers and new entrants are embedding AI-enabled predictive algorithms in brushless DC (BLDC) pumps, improving flow accuracy and lowering warranty costs. The Asia-Pacific region leads adoption due to China’s large-scale EV manufacturing base and policy support. Europe and North America follow closely as regulators raise efficiency targets and fund electrification infrastructure.

Key Report Takeaways

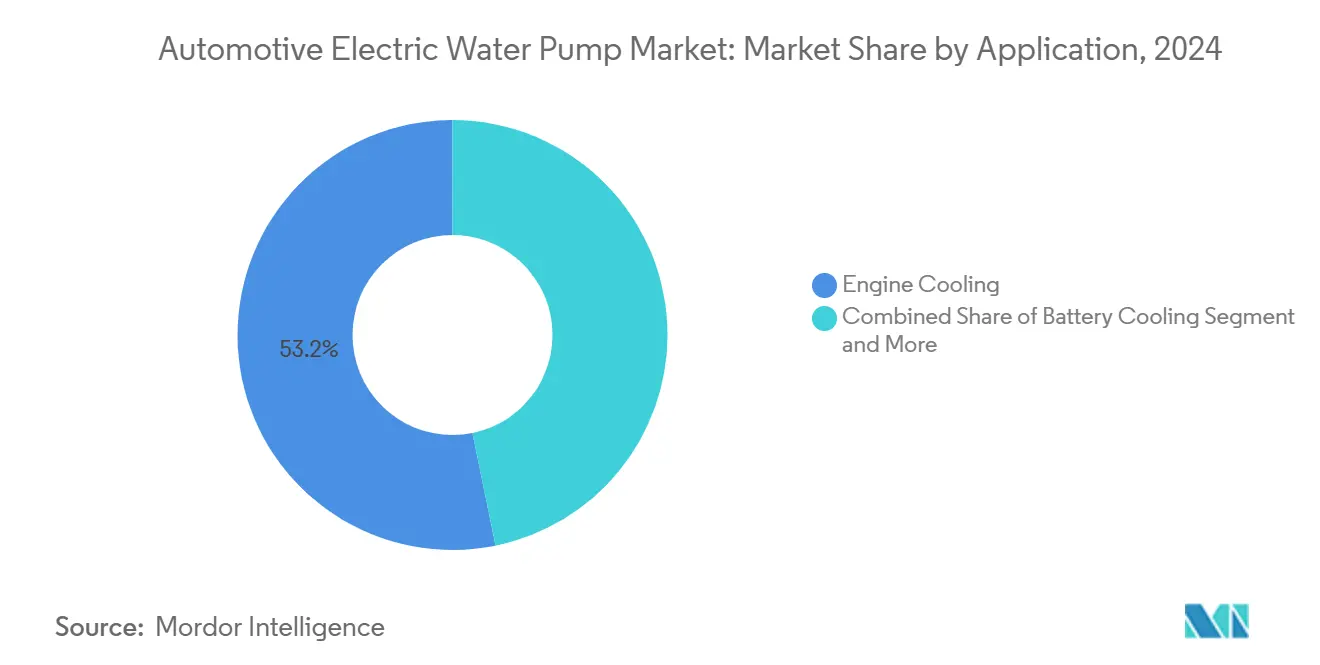

- By application, engine cooling held 53.16% of the automotive electric water pump market in 2024, whereas battery cooling is projected to expand at a 13.66% CAGR through 2030.

- By vehicle type, passenger cars commanded 63.11% of the automotive electric water pump market in 2024 and are set to post the fastest 13.65% CAGR to 2030.

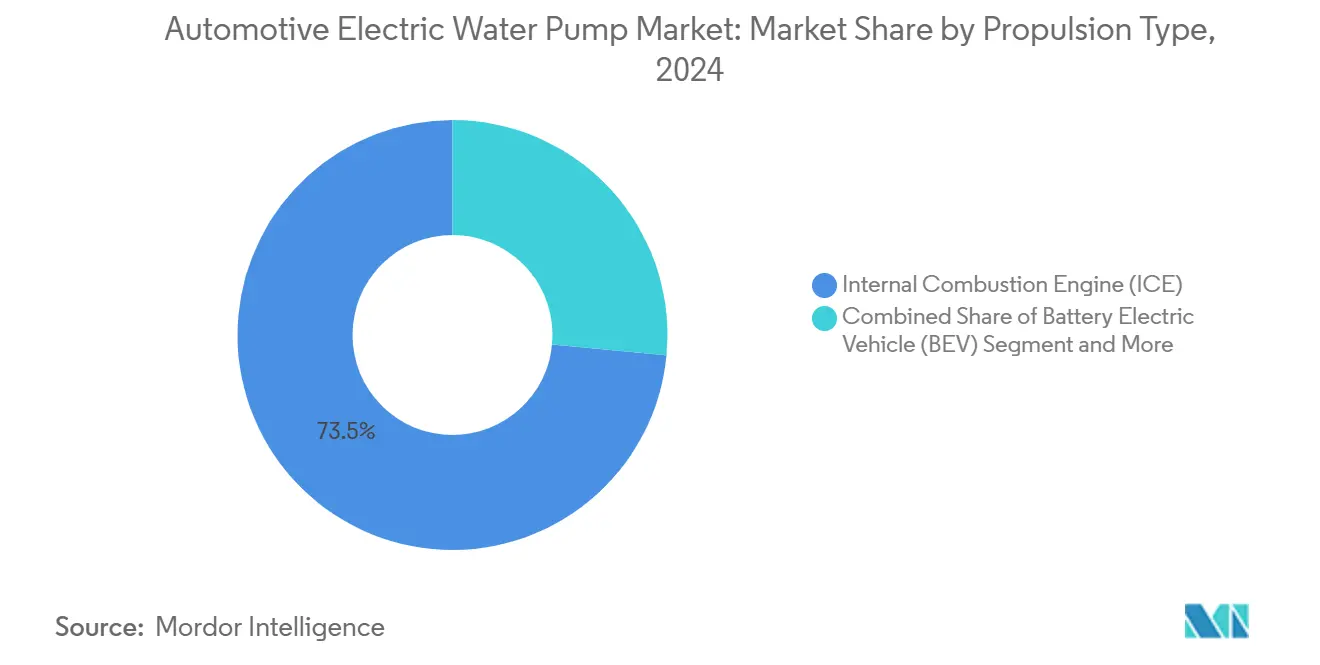

- By propulsion type, internal combustion engine (ICE) vehicles captured 73.45% of the automotive electric water pump market in 2024, while battery electric vehicles will accelerate at a 13.75% CAGR through 2030.

- By distribution channel, offline outlets accounted for 83.21% of the automotive electric water pump market in 2024; online channels are forecast to register a 13.68% CAGR to 2030.

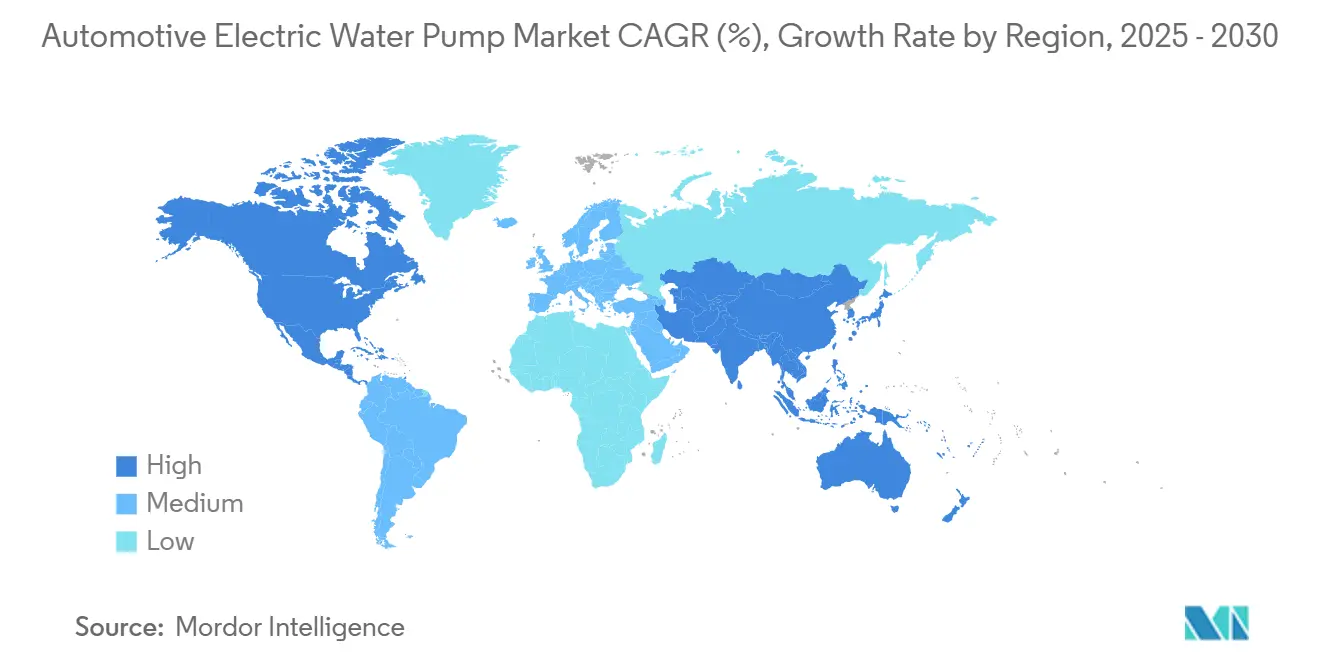

- By region, Asia-Pacific led with 38.75% of the automotive electric water pump market in 2024, and the area is on track for a 13.71% CAGR through 2030.

Global Automotive Electric Water Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption Of Evs | +3.2% | Global, with Asia Pacific and Europe leading | Medium term (2-4 years) |

| Stringent Global Fuel-Efficiency | +2.8% | Global, with EU and North America most stringent | Short term (≤ 2 years) |

| OEM Shift Toward Electrified Auxiliaries | +2.1% | North America and EU, spill-over to Asia Pacific | Medium term (2-4 years) |

| Engine Downsizing & Turbocharging | +1.9% | Global, with premium segments leading | Short term (≤ 2 years) |

| AI-Enabled Predictive Thermal-Management Software | +1.7% | Asia Pacific core, early adoption in North America | Long term (≥ 4 years) |

| 800 V Power-Electronics Platforms | +1.4% | Global EV manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of EVs & HEVs Requiring Advanced Thermal-Management Solutions

Electrified powertrains need coolant circuits that operate whether the engine is on or off, making electric pumps indispensable to maintain battery temperatures between 15 °C and 35 °C. IEEE modeling shows BLDC pumps managed by predictive control keep cells within ±1 °C, extending pack life by one-fifth [1]“Model Predictive Control for Battery Thermal Management,” IEEE Transportation Electrification Community, ieee.org . With battery capacities exceeding 100 kWh and 800 V architectures generating higher heat flux, precision flow regulation prevents thermal runaway and safeguards power-electronics reliability. Automakers specify high-efficiency pumps that deliver variable flow and support multiple loops, including battery, inverter, and cabin comfort circuits.

Stringent Global Fuel-Efficiency & Emission Regulations

The Euro 7 framework takes effect in 2026 and imposes lower NOx and particulate thresholds, while U.S. CAFE rules demand a 40.4 mpg fleet average by 2026[2]“Proposal for Euro 7 Emission Standards,” European Commission, european-union.europa.eu. Electric pumps lower engine drag by 2-5 hp compared with belt-driven units, translating into measurable fuel-consumption savings that help automakers meet those aggressive benchmarks. China’s GB standard mandates coolant systems function from -40 °C to +85 °C, driving the selection of electronically controlled pumps with advanced seals and high-temperature plastics. These overlapping regulations create an unavoidable pull for electric auxiliary adoption regardless of initial cost premiums.

OEM Shift Toward Electrified Auxiliaries to Reduce Parasitic Losses

Converting belt-driven accessories such as water pumps to electrically driven ones removes up to one-tenth of engine power losses. Modern BLDC motors achieve almost four-fifths of the efficiency, allowing dynamic flow adjustment that optimizes warm-up, cruising, and post-shutdown cooling. Commercial fleets are early beneficiaries: BYD specifies 240 W pumps delivering more than 2,000 L/h on electric buses, demonstrating the technology's scalability[3]“Electric Bus Technical Manual,” BYD Company Limited, byd.com . Across segments, electrified auxiliaries provide data for prognostics, enabling over-the-air software updates that fine-tune performance as vehicles age.

Engine Downsizing & Turbocharging Boosting Controllable Cooling Demand

Turbocharged 3- and 4-cylinder engines produce higher heat density and require active cooling even after shutdown to protect bearings. Electric pumps supply targeted flow during hot-soak conditions, mitigating coking risk and extending turbocharger life. Integration with engine-management systems allows predictive modulation based on boost maps and ambient temperatures, improving drivability and emissions. The trend locks in additional volumes as OEMs continue shrinking displacements to balance efficiency with performance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Unit Cost | -2.3% | Global, with cost-sensitive markets most affected | Short term (≤ 2 years) |

| Reliability Concerns | -1.8% | North America and EU commercial segments | Medium term (2-4 years) |

| Shortage Of High-Grade Rare-Earth Magnets | -1.5% | Global, with supply chain concentration in China | Long term (≥ 4 years) |

| End-Of-Life Electronics Recycling Compliance Costs | -0.9% | European Union primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher Unit Cost vs. Mechanical Pumps

Electric water pumps carry a reasonable price premium over mechanical counterparts, mainly due to BLDC motors, controllers, and sensing hardware. A standard 80 W unit retails around USD 300-400, while a comparable mechanical pump can cost below par. Yet lifecycle analyses reveal that fuel savings and reduced maintenance offset the initial outlay within five years. Still, in price-sensitive segments, particularly entry-level ICE vehicles, OEMs hesitate to absorb the differential, slowing near-term penetration.

Shortage of High-Grade Rare-Earth Magnets for BLDC Motors

Neodymium-iron-boron magnets, vital for high-temperature BLDC efficiency, derive more than four-fifths of global supply from China, exposing the value chain to geopolitical risk. Recent export-quota tightening prompted spot-price spikes that squeezed pump makers’ margins. Recycling initiatives like the EU-funded REMHub project show almost complete rare-earth recovery rates, but commercial scaling needs three to five years. In response, suppliers investigate ferrite-based motors, although these sacrifice up to two-fifths of efficiency and add weight.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Battery Cooling Drives Next-Generation Demand

Engine cooling retained a 53.16% share in 2024, while battery cooling represented the fastest-expanding slice of the automotive electric water pump market, advancing at a 13.66% CAGR. The automotive electric water pump market size attached to battery cooling is forecast to double by 2030 as pack capacities grow and fast-charging becomes mainstream. Battery thermal uniformity safeguards cell longevity, enhances regenerative-braking performance, and minimizes warranty claims. BLDC pumps equipped with AI controllers modulate flow in real time according to load, ambient conditions, and charge state, achieving sub-1 °C gradients. By contrast, engine cooling remains volume-dominant because hybrid and efficient ICE architectures dominate global production, especially in cost-sensitive regions.

Turbocharger cooling and HVAC auxiliary loops represent emerging niches where modular pump platforms let OEMs mix and match flow rates to reduce part numbers. Suppliers market integrated manifolds that feed battery, motor, and cabin circuits simultaneously, cutting hose complexity and assembly time. The shift toward multipurpose pumps increases average selling prices and encourages tier-1s to bundle software services for predictive maintenance, strengthening customer lock-in across the automotive electric water pump market.

By Vehicle Type: Passenger Cars Lead Market Penetration

Passenger cars captured 63.11% of the automotive electric water pump market in 2024 and are projected to expand at a 13.65% CAGR, underscoring how household adoption of EVs underpins the broader market. Urban duty cycles with frequent start-stops magnify the efficiency benefit of variable-speed pumps, boosting their appeal in compact crossovers and sedans. Meanwhile, commercial vans and light trucks increasingly specify electric pumps to support last-mile delivery electrification; their rigorous uptime demands favor remote diagnostics enabled by pump-embedded sensors.

Medium and heavy commercial vehicles pose harsh thermal loads and vibration challenges, pushing suppliers to develop ruggedized housings and sensor redundancy. Field data shows that pumps rated for 20,000 hours at 80 °C coolant exposure maintain less than one-tenth of flow degradation, a threshold essential for transit-bus fleets. As autonomous driving computers proliferate, they add significant heat sources, creating secondary coolant loops that further enlarge the automotive electric water pump market size across all vehicle categories.

By Propulsion Type: ICE Dominance Gives Way to EV Growth

While ICE platforms held a 73.45% of the automotive electric water pump market share in 2024, battery electric vehicles will record the highest 13.75% CAGR, reshaping the automotive electric water pump market landscape. EVs frequently employ two to three electric pumps per vehicle to cool batteries, power electronics, and sometimes cabins, multiplying unit demand despite lower vehicle volumes. Plug-in hybrids exhibit the most intricate architectures, juggling ICE, battery, and charger thermal loops; consequently, they often use higher-head pumps capable of 500 kPa pressures.

Recent patents reveal canned-motor designs that embed electronics within the coolant flow, eliminating shaft seals and leakage risk while reducing acoustic noise. The resulting durability gains attract trucking OEMs experimenting with fuel-cell electric drivetrains, which operate continuously at steady temperatures yet need reliable coolant circulation. ICE platforms are also evolving: variable-speed pumps shorten warm-up time, improving combustion efficiency and tailpipe emissions, thus keeping demand resilient even as EV sales surge.

By Distribution Channel: Digital Transformation Accelerates Online Growth

Offline wholesalers retained 83.21% of the automotive electric water pump market share in 2024 because electric water pumps require specialized installation and calibration equipment. Workshops trust local distributors that bundle technical training and warranty handling, especially as pump failures can cause catastrophic engine damage. However, the online channel’s 13.68% CAGR illustrates the sector’s digital pivot: professional mechanics increasingly order parts via e-commerce marketplaces that provide VIN-matched catalogs and real-time inventory.

Manufacturers leverage direct-to-consumer portals to supply performance upgrades, firmware downloads, and remote diagnostics, differentiating themselves in the automotive electric water pump market. These platforms also streamline recall campaigns and ensure compliance with Europe’s WEEE Directive for end-of-life electronics collection. As EVs mature, owners comfortable with software updates at home will likely demand similar convenience for service parts, further expanding online penetration.

Geography Analysis

Asia-Pacific commanded 38.75% of the automotive electric water pump market in 2024 and is forecast to grow at a 13.71% CAGR through 2030, reflecting aggressive electrification policies and cost advantages in China, Japan, and South Korea. China’s GB thermal-management standards require pumps that remain operational for long periods, pushing local OEMs to select high-specification BLDC units. Domestic suppliers collaborate with research institutes to improve magnet retention at elevated temperatures, bolstering export competitiveness. Japan’s Denso and Aisin focus on lightweight aluminum housings and integrated controllers, capitalizing on their hybrid dominance to preserve market sway. Meanwhile, South Korean battery giants LG Energy Solution and Samsung SDI partner with pump makers to co-design battery-integrated cooling modules, accelerating design cycles.

Europe ranks highly, buoyed by stringent Euro 7 emissions and a 2035 zero-tailpipe target that forces rapid EV proliferation. German suppliers Bosch, Continental, and Schaeffler implement AI-enabled flow algorithms linked to vehicle domain controllers, ensuring pumps consume only the necessary power and extending range. The EU’s End-of-Life Vehicle regulations push companies to embed recyclability, such as detachable electronics and standardized connectors, reinforcing circular-economy priorities.

North America’s expansion stems from ambitious CAFE rules, state-level ZEV mandates, and a growing EV manufacturing footprint in the United States and Mexico. U.S. infrastructure legislation funds charging corridors, increasing demand for 800 V platforms that need high-flow pumps. Mexico’s cost-competitive plants attract global OEMs, promoting regional pump capacity to mitigate tariff and logistics risks. Canadian suppliers explore silicon-carbide inverter cooling loops, a niche that requires high-dielectric coolant compatibility a capability electric pumps can support using seal materials resistant to ethylene-glycol blends.

Competitive Landscape

The automotive electric water pump market remains moderately fragmented, though consolidation is accelerating as suppliers pursue scale and software depth. Bosch, Continental, and Mahle leverage decades of thermal-management know-how alongside robust manufacturing footprints. New entrants often spun from electronics or software domains, focusing on predictive analytics that transform pumps into data hubs for fleet maintenance. Schaeffler’s March 2024 merger with Vitesco Technologies illustrates vertical integration, combining mechanical components with power-electronics expertise to deliver system-level efficiency gains.

Competitive differentiation now centers on firmware upgradability, cybersecurity compliance, and integration with vehicle centralized architectures. Patent activity concentrates on impurity-resistant impellers, magnetic-drive canned motors, and self-learning controllers that adapt flow curves based on component aging. Partnerships between pump makers and silicon-carbide inverter suppliers underscore the convergence of cooling hardware with power-electronics design, locking in cross-selling opportunities within the automotive electric water pump market.

Tier-1s also court battery manufacturers to bundle pumps within thermal-module assemblies, securing volume commitments and reducing OEM integration complexity. Start-ups experiment with axial-flow designs for ultra-low packaging height, a trait valued in skateboard EV platforms. The competitive field thus blends legacy scale with agile innovation, and market concentration is projected to tighten as regulatory complexity and software investment raise entry barriers.

Automotive Electric Water Pump Industry Leaders

Robert Bosch GmbH

Continental AG

Rheinmetall AG

Mahle GmbH

Denso Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Volkswagen Group and Rivian Automotive formed a USD 5.8 billion joint venture to create software-defined vehicle platforms integrating electric water pumps with AI-driven thermal-management systems.

- November 2024: Ceer Motors and Rimac Technology partnered to engineer Middle-East-optimized EV platforms featuring electric pumps designed for ambient temperatures above 50 °C.

- October 2024: Schaeffler AG finalized its merger with Vitesco Technologies, establishing a unified electrification and thermal-management business unit centered on next-generation electric pump solutions.

Global Automotive Electric Water Pump Market Report Scope

| Engine Cooling |

| Battery Cooling |

| Turbo-charger Cooling |

| HVAC Systems |

| Passenger Cars |

| Light Commercial Vehicles (LCVs) |

| Medium & Heavy Commercial Vehicles (MHCVs) |

| Internal Combustion Engine (ICE) |

| Battery Electric Vehicle (BEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Hybrid Electric Vehicle (HEV) |

| Fuel Cell Electric Vehicle (FCEV) |

| Offline |

| Online |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | Engine Cooling | |

| Battery Cooling | ||

| Turbo-charger Cooling | ||

| HVAC Systems | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCVs) | ||

| Medium & Heavy Commercial Vehicles (MHCVs) | ||

| By Propulsion Type | Internal Combustion Engine (ICE) | |

| Battery Electric Vehicle (BEV) | ||

| Plug-in Hybrid Electric Vehicle (PHEV) | ||

| Hybrid Electric Vehicle (HEV) | ||

| Fuel Cell Electric Vehicle (FCEV) | ||

| By Distribution Channel | Offline | |

| Online | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the automotive electric water pump market in 2025?

The automotive electric water pump market will be USD 4.41 billion in 2025.

What CAGR is expected for automotive electric water pumps through 2030?

The market is projected to grow at a 13.61% CAGR between 2025 and 2030.

Which application segment is expanding the fastest?

Battery cooling is the quickest-growing segment, advancing at a 13.66% CAGR through 2030.

Which region leads to the demand for electric water pumps?

Asia-Pacific holds the largest 2024 share at 38.75% and is set for the highest 13.71% CAGR through 2030.

Who are the key players in electric water pumps?

Bosch, Continental, Mahle, Schaeffler, and several electronics-focused entrants dominate shipment volumes.

What is the main barrier to broader adoption?

Higher upfront costs versus mechanical pumps remain the chief obstacle, especially in cost-sensitive vehicle classes.

Page last updated on: