Automotive Charge Air Cooler Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

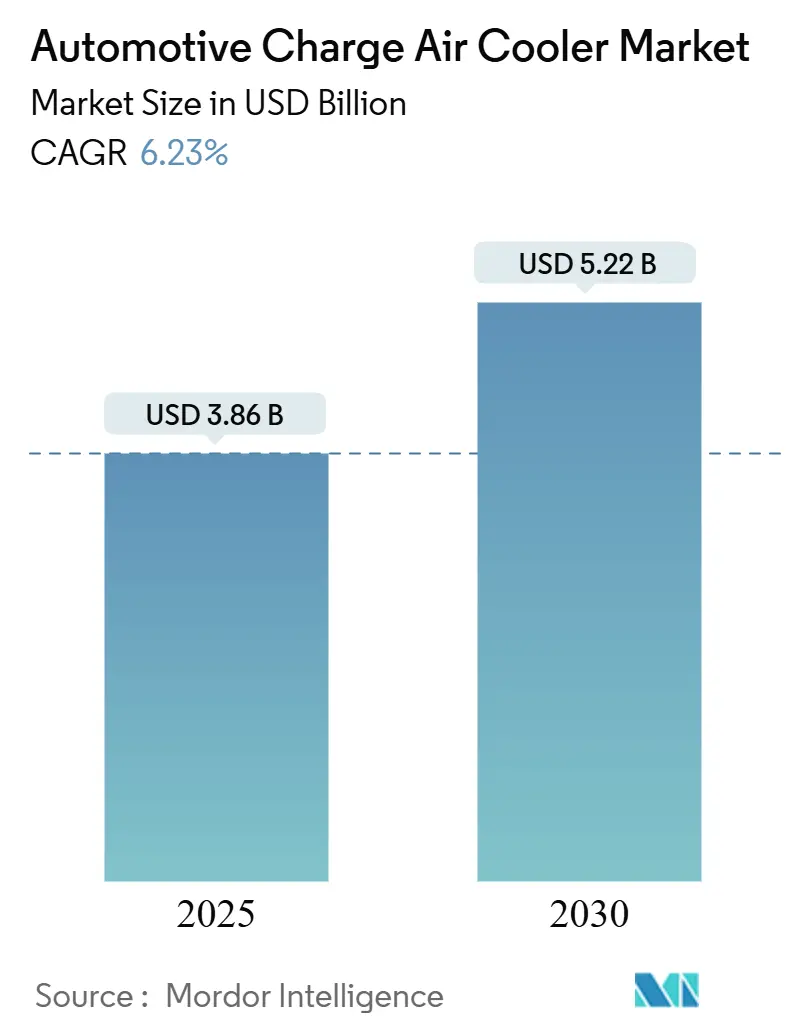

| Market Size (2025) | USD 3.86 Billion |

| Market Size (2030) | USD 5.22 Billion |

| Growth Rate (2025 - 2030) | 6.23% CAGR |

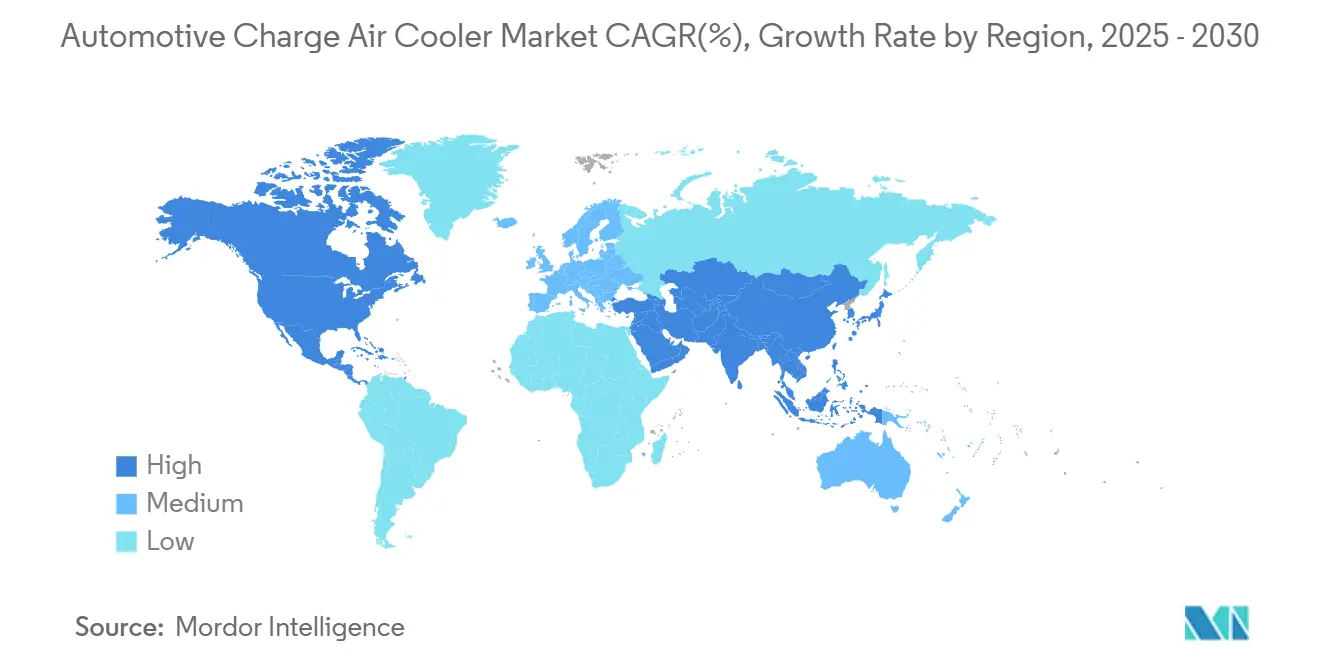

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Charge Air Cooler Market Analysis by Mordor Intelligence

The Automotive Charge Air Cooler Market size stands at USD 3.86 billion in 2025, and it is forecast to reach USD 5.22 billion by 2030, reflecting a 6.23% CAGR from 2025 to 2030. Rising turbo-downsizing strategies to meet post-2025 emissions rules, continued demand for high-output internal-combustion engines in commercial vehicles, and modular thermal-module adoption by vehicle makers propel sustained expansion. Asia-Pacific commands the most significant regional footprint, while North America shows the fastest growth as new EPA standards maintain an ICE compliance pathway. Tightening durability rules, volatile aluminum pricing, and the gradual flattening of global ICE production after 2027 present counterweights, yet aftermarket momentum, hydrogen-ready stainless-steel designs, and liquid-cooled architectures unlock fresh opportunities for suppliers and distributors. Medium-duty delivery fleets, range-extended BEVs, and high-boost off-road machinery are emerging pockets of outsized demand as operators deploy total-cost-of-ownership (TCO) analytics to cut downtime and fuel overheads.

Key Report Takeaways

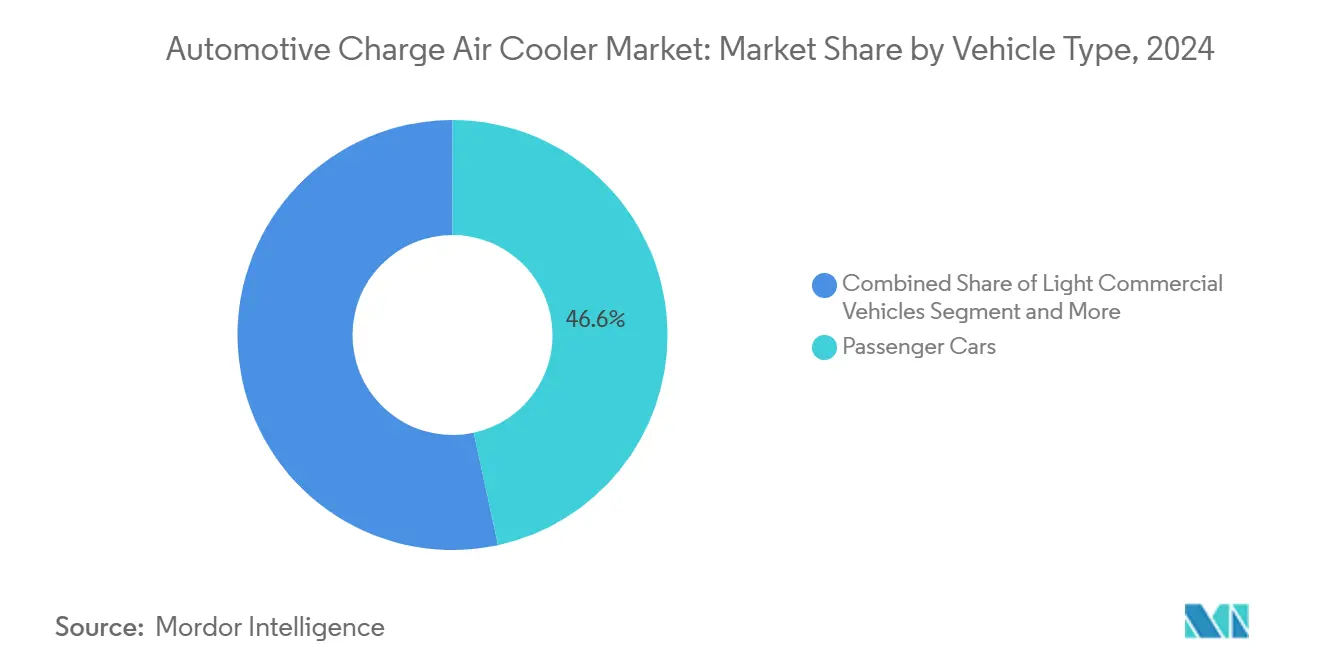

- By vehicle type, passenger cars held 46.61% of the automotive charge air coolers market share in 2024, while off-road vehicles are projected to grow at a 7.32% CAGR through 2030.

- By product type, air-cooled units captured 72.63% of the automotive charge air coolers market share in 2024; liquid-cooled designs are advancing at a 7.43% CAGR between 2025 and 2030.

- By engine type, diesel applications accounted for 54.79% of the automotive charge air coolers market share in 2024; CNG/LPG units exhibit the highest CAGR at 8.18% to 2030.

- By design, fin-and-tube heat exchangers led 65.31% of the automotive charge air coolers market share in 2024; bar-and-plate formats are on track for a 7.87% CAGR over the forecast window.

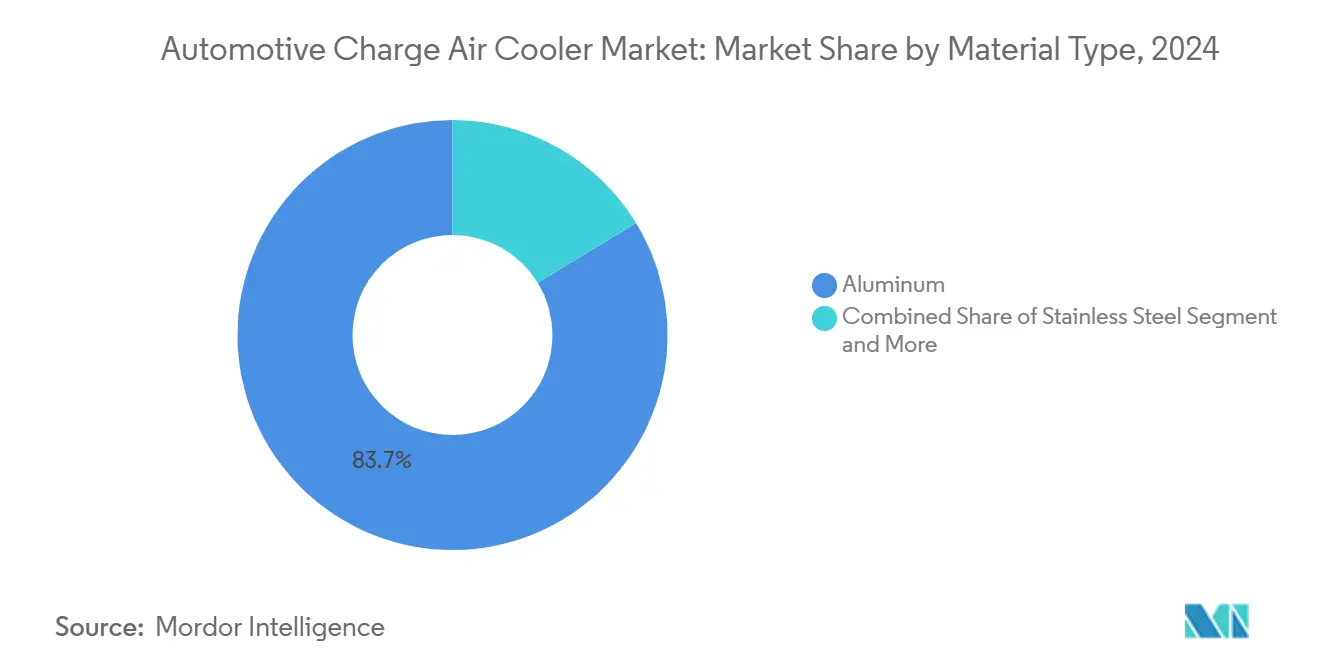

- By material, aluminum dominated the automotive charge air coolers market, with 83.73% of the share in 2024, while stainless steel is forecast to expand at a 7.94% CAGR owing to hydrogen ICE pilots.

- By sales channel, OEMs represented 79.49% of the automotive charge air coolers market share in 2024; the aftermarket is rising at 8.23% CAGR as fleets seek performance replacements.

- By geography, Asia-Pacific captured 53.83% of the automotive charge air coolers market share in 2024, and North America emerges as the fastest-growing region with a 7.28% CAGR through 2030.

Global Automotive Charge Air Cooler Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent CO₂ and NoX Regulations | +1.8% | Europe and North America | Medium term (2-4 years) |

| Fuel-Economy-Linked Tax Incentives | +1.2% | Europe and China | Short term (≤2 years) |

| Adoption of 48 V Electric Turbochargers | +1.1% | Europe and Asia-Pacific | Medium term (2-4 years) |

| OEM Shift to Modular Thermal Modules | +0.9% | Global | Long term (≥4 years) |

| Liquid Manifolds in BEV Skateboard Platforms | +0.7% | North America and Europe | Medium term (2-4 years) |

| Fleet-Operator TCO Spotlight on CAC Leaks | +0.5% | Global | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Stringent CO₂ and NOx Regulations (Post-2025) Driving Turbo-Downsizing

Global emissions frameworks have tightened sharply; the EPA mandates light-duty fleet targets of roughly 82 g/mi CO₂ by 2032, nearly halving 2026 levels[1]“Multi-Pollutant Emissions Standards for Model Years 2027 and Later,”, Environmental Protection Agency, federalregister.gov. Similar Euro 7 rules focus on real-world operation, demanding lower intake-air temperatures for catalyst light-off. Automakers therefore specify intercoolers with higher effectiveness and lower pressure drop to retain combustion stability. Tougher particulate caps at 0.5 mg/mi push gasoline turbo engines toward optimized charge density to mitigate soot. Medium-duty delivery fleets face a 274 g/mi CO₂ ceiling by 2032, expanding commercial CAC demand. Collectively, these policies embed premium cooling hardware into future vehicle cycles.

Adoption of 48 V Electric Turbochargers Raising Boost and CAC Efficiency Needs

In Europe and Korea, the passenger vehicle segment is witnessing a notable evolution in mild-hybrid powertrain architectures, focusing on enhanced performance and efficiency. A growing trend is seen in these systems integrating electric compressors with high-ratio turbochargers, significantly raising charge-air temperatures. Manufacturers are turning to larger, denser intercooler cores to counteract this thermal surge and avert engine knock. These cores boast refined fin geometries, optimizing heat dissipation without compromising responsiveness.

This strategy facilitates a quicker throttle response and dovetails with the industry's movement towards compact, high-efficiency engines that adhere to rigorous emissions and performance benchmarks. This trend underscores a wider industry pivot towards innovative thermal management and meticulous component optimization in mild-hybrid systems, particularly in regions at the forefront of adoption.

OEM Shift to Modular, Scalable Thermal-Modules (Platform Strategy)

Manufacturers consolidate cooling, battery, and HVAC functions into shared modules to cut part complexity and validation cost. TRATON’s commercial-vehicle thermal kit exemplifies this trend, enabling suppliers to amortize R&D across global chassis lines. Digital twin tools allow precise, duty-cycle-specific performance mapping, while standard interfaces simplify aftermarket service. Vendors offering system-level co-design skills gain an edge; component-only players risk margin squeeze as platform scopes widen.

Data-Center Style Liquid Manifolds in BEV Skateboard Platforms

High-flux liquid loops echo hyperscale IT cooling, channeling coolant via centralized manifolds around batteries, fuel cells, and range-extender engines. These loops demand compact liquid-cooled CACs with low pressure drop and aluminum-braze integrity compatible with long-life glycol blends. Integrated sensors enable predictive maintenance and waste-heat reuse for cabin or battery pre-conditioning, creating fresh value-added layers for intercooler vendors [2]“Annual Report 2024,”, Hanon Systems, hanonsystems.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Flatter ICE Production Curve After 2027 | −1.4% | Global | Medium term (2-4 years) |

| Raw-Material Price Spikes for Aluminum and Copper | −0.8% | Global | Short term (≤2 years) |

| Rising Durability and Leak-Rate Validation Cost | −0.6% | Developed markets | Medium term (2-4 years) |

| Thermal-Runaway Concerns in Hydrogen ICE Demos | −0.3% | Europe and Japan | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Flatter ICE Production Curve After 2027 Due To XEV Mix

China's NEV quotas and the United States goal of achieving a 50% EV share by 2030 dampen long-term ICE volumes, reducing baseline CAC unit demand. However, the shift in engine configurations toward higher-boost duty cycles is driving sustained demand for premium cooler specifications. This trend is particularly evident in range-extended hybrids, which rely on advanced cooling systems to optimize performance and efficiency, and vocational trucks, where durability and reliability are critical for heavy-duty operations. These developments highlight the evolving requirements in the automotive cooling market as the industry transitions toward electrification and hybridization.

Raw-Material Price Spikes for Aluminum Alloy 3003 and Copper

Aluminum prices rise as energy-driven smelting costs fluctuate, driven by the increasing reliance on energy-intensive processes and global energy market dynamics. Meanwhile, copper's volatility continues to pressure liquid-cooled core expenses, as fluctuating copper prices directly impact production costs. Automotive supply contracts restrict cost pass-throughs, squeezing profit margins for manufacturers and suppliers alike. Although stainless steel is an alternative material for hydrogen programs, it requires a re-validation process, adding to overall costs and operational complexities[3]“Aluminum Alloy 3003 Historical Data,”, London Metal Exchange, lme.com.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Off-Road Performance Gains Underpin Growth

In 2024, the passenger car segment accounted for the largest charge air coolers market share, representing 46.61% of the total. Meanwhile, the off-road vehicle segment is projected to grow at the fastest compound annual growth rate (CAGR) of 7.32%. Heavy tractors and excavators increasingly feature variable-geometry turbochargers that intensify charge temperature, compelling OEMs to specify thicker core stacks and high-durability braze joints. Rural equipment dealers also embrace premium aftermarket cores to cut unplanned downtime during harvest seasons. Passenger-car intercoolers progress toward lighter fin geometries to preserve frontal-area aerodynamics, and liquid-cooled variants appear in top-tier hot-hatch and plug-in hybrid trims.

Urban delivery vans, part of light commercial vehicles, integrate compact bar-and-plate designs that allow frontal crash-beam compatibility while handling daily stop-start duty. The sector benefits from e-commerce growth, stimulating the charge air coolers market. Heavy commercial trucks retain large air-cooled units with between-frame mounting for serviceability, yet fleets now measure leak losses via telematics, guiding preemptive core swaps. Altogether, mixed vehicle-type demand patterns secure volume resiliency in the 2025-2030 horizon.

By Product Type: Liquid-Cooled Adoption Accelerates

Air-cooled technologies still account for 72.63% of 2024 revenue, but liquid-cooled lines are expanding at a 7.43% CAGR as packaging envelopes shrink and frontal drag targets tighten. BEV range-extender engines and fuel-cell air loops demand water-glycol cores that can sit anywhere along the skateboard, decoupled from the direct air stream. The shift fosters co-development between intercooler and battery-thermal teams, an integration point that entrenches system-level supply contracts.

Air-cooled models remain economical for mass-market sedans, aided by recent fin-press upgrades that raise heat-rejection density 12% without cost spikes. Meanwhile, high-altitude applications, such as Latin American mines, increasingly specify dual-stage charge air coolers to offset rarefied-air density losses—often favoring liquid circuits for thermal predictability. The parallel aftermarket sees hobbyist tuners gravitating toward air-to-air upgrades that bolt directly to existing plumbing, ensuring enduring replacement demand.

By Engine Type: Alternative Fuels Expand the Horizon

Diesel retains a 54.79% foothold in the charge air coolers market share thanks to heavy-duty trucking, mining, and marine markets. Steady sulfur-cap and selective catalytic reduction (SCR) systems require precise intake temperatures, favoring premium intercoolers. Gasoline downsizing in passenger cars keeps demand stable, though volumes will slowly taper after 2028 amid electrification.

CNG/LPG engines attract an 8.18% CAGR on rising gas infrastructure and fuel-tax incentives, especially in refuse and transit fleets. Dedicated CNG engines use lower compression ratios and advanced ignition, yet still mandate tight charge-temperature control to mitigate methane knock. Hydrogen ICE pilots in Japan and Europe adopt stainless-steel liquid-cooled cores due to higher flame speed and water-vapor content. This creates a niche but technologically influential sub-market that can lift stainless-steel supplier margins.

By Design: Bar-and-Plate Platforms Move Upmarket

Fin-and-tube assemblies cover 65.31% of 2024 volumes courtesy of low cost and entrenched tooling. However, bar-and-plate units climb at 7.87% CAGR because they tolerate higher boost pressures and lend themselves to additive-manufactured end tanks that optimize pressure uniformity. Vacuum-brazed bar-and-plate cores with turbulence-enhancing internal bars achieve 20% higher effectiveness at a similar frontal area.

Fin-and-tube producers counter with variable louver orientation to enhance boundary-layer disruption, maintaining competitiveness in cost-sensitive compact cars. Hybrid constructions join fin-tube cores to bar-plate tanks, balancing price and strength for medium trucks. As duty-cycle diversity widens, design flexibility becomes a procurement differentiator for OEMs seeking platform rationalization.

By Material: Stainless-Steel Finds Hydrogen Niches

Aluminum keeps an 83.73% share because its thermal conductivity, weight, and established recycling loop align with automotive cost constraints. Yet stainless-steel use expands 7.94% CAGR to serve hydrogen engines operating beyond aluminum’s 200 °C continuous threshold. 321 and 347 grades curb carbide precipitation, lengthening life at 700 °C exhaust recirculation temps.

Copper remains confined to motorsport and premium liquid-cooled applications where density is paramount. Powder-bed-fusion printed copper micro-channels debut in endurance racing, hinting at future commercial trickle-down. Material hybridity—aluminum fins, stainless tanks—emerges as a creative route to balance cost versus durability in next-gen CACs.

By Sales Channel: Aftermarket Captures TCO-Driven Spend

OEM supply still controls 79.49% of 2024 sales, underpinned by platform-based sourcing and long-term cost-down contracts. Nevertheless, the aftermarket records an 8.23% CAGR as fleet managers link cooler degradation to fuel spikes, prompting proactive replacements with higher-grade cores. Independent distributors stock expanded part lists—Valeo’s European catalog now lists 175 SKUs—to service older fleets where OEM supply lines wane.

Performance enthusiasts also propel aftermarket volumes, purchasing large-volume intercoolers to sustain 30 psi-plus boost maps on remapped turbo gasoline engines. Spectra Premium’s Canadian-built heavy-duty coolers find traction in vocational trucks, benefiting from fast-turn logistics to Midwest depots. As vehicles age past warranty and telematics pinpoint efficiency losses, service-bay demand should remain buoyant through 2030.

Geography Analysis

Asia-Pacific contributed 53.83% of global revenue in 2024, anchored by China’s NEV policy mix, BS-VI turbo adoption in India, and Japan’s hydrogen ICE R&D pipeline. The charge air coolers market size across the region benefits from scale production clusters in Guangdong, Pune, and Chonburi that supply domestic and export demand. Chinese OEMs specify higher-performance cores to hit CAFC penalties, while Indian commercial fleets retrofit durable intercoolers to combat hot-soak in 45 °C ambient summers. Japan’s automakers co-engineer stainless-steel liquid cores for hydrogen race cars, exporting design know-how across Asia.

With a 7.28% CAGR forecast, North America leverages the EPA Multi-Pollutant rule that validates high-efficiency ICE alongside electrification. Hanon Systems’ USD 284 million Ontario compressor plant anchors regional thermal-module production, shortening logistics chains for Detroit's three OEMs. Freight-corridor investment and last-mile parcel demand expand heavy-truck intercooler needs. CARB refrigeration unit mandates spill technology into broader heavy-duty charge air cooling, stimulating system upgrades.

Europe maintains regulatory leadership via Euro 7, forcing real-world durability and low-temperature performance, translating into higher-spec cores with corrosion-resistant coatings. German Tier-1s iterate digital twin validation across modular platforms shared among passenger and light-commercial vehicles. Eastern European assembly plants import intercooler modules, sustaining intra-EU trade amid Brexit realignment. Robust aftermarket networks in France and Spain support rising replacement volume for aging diesel vans, reinforcing the charge air coolers market’s long-tail revenue stream.

Competitive Landscape

A select group of leading suppliers in the aluminum BIW thermal management arena commands a notable share, yet none dominate the landscape. This setup fuels competition and spurs innovation, with firms carving out niches through tech integration and diverse service offerings. MAHLE, Valeo, and Hanon Systems are capitalizing on modular thermal-module contracts. These contracts combine cooling solutions for batteries, power electronics, and charge-air systems into cohesive assemblies. Such an integrated strategy resonates with OEMs favoring streamlined sourcing and holistic system optimization.

Second-tier players like Modine and Dana pursue specialty niches, including stainless-steel hydrogen cores and 48 V electric turbo cooling loops. Additive-manufacture start-ups produce lattice-enhanced bar-and-plate prototypes that cut pressure drop. Suppliers expand digital twin capabilities—using cloud CFD to predict real-world fouling—strengthening their negotiation stance in multiyear sourcing bids.

Strategic investment gravitates toward raw-material risk hedging and regionalized capacity to buffer aluminum volatility and geopolitical freight shocks. ISO 14001 compliance and recycled-content aluminum commitments become selection criteria as automakers audit Scope 3 emissions footprints, nudging suppliers toward closed-loop scrap programs.

Automotive Charge Air Cooler Industry Leaders

MAHLE GmbH

Valeo SA

Dana Incorporated

Modine Manufacturing Company

Hanon Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Hanon Systems, a supplier of automotive thermal management solutions for electrified vehicles, has announced plans to establish a new manufacturing facility in Woodbridge, Ontario, Canada. The new plant aims to enhance production capabilities and strengthen its partnerships with global vehicle manufacturers. This expansion aligns with the growing demand for thermal management systems in electric vehicles and demonstrates Hanon Systems' commitment to serving the North American automotive market.

- February 2024: Pacific Avenue Capital Partners acquired Sogefi Group's filtration business unit for USD 399 million, allowing Sogefi to sharpen its focus on air intake & cooling systems and suspension components.

Global Automotive Charge Air Cooler Market Report Scope

| Passenger Cars |

| Light Commercial Vehicles (LCVs) |

| Heavy Commercial Vehicles (HCVs) |

| Off-road Vehicles |

| Air-Cooled Charge Air Coolers |

| Liquid-Cooled Charge Air Coolers |

| Gasoline Engines |

| Diesel Engines |

| CNG/LPG-Powered Engines |

| Fin and Tube |

| Bar and Plate |

| Aluminum |

| Stainless Steel |

| Copper |

| Others |

| OEM (Original Equipment Manufacturer) |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCVs) | ||

| Heavy Commercial Vehicles (HCVs) | ||

| Off-road Vehicles | ||

| By Product Type | Air-Cooled Charge Air Coolers | |

| Liquid-Cooled Charge Air Coolers | ||

| By Engine Type | Gasoline Engines | |

| Diesel Engines | ||

| CNG/LPG-Powered Engines | ||

| By Design | Fin and Tube | |

| Bar and Plate | ||

| By Material | Aluminum | |

| Stainless Steel | ||

| Copper | ||

| Others | ||

| By Sales Channel | OEM (Original Equipment Manufacturer) | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the charge air coolers market in 2030?

The charge air coolers market size is forecast to reach USD 5.22 billion by 2030, up from USD 3.86 billion in 2025.

How quickly is the liquid-cooled segment expanding?

Liquid-cooled intercoolers are expected to post a 7.43% CAGR between 2025 and 2030 as OEMs adopt centralized liquid manifolds.

Why are stainless-steel intercoolers gaining attention?

Stainless steel offers superior high-temperature and corrosion resistance, making it essential for hydrogen internal combustion engine prototypes.

What factors drive the aftermarket opportunity?

Fleet TCO analytics linking charge-air leaks to fuel costs and performance enthusiasts seeking higher boost stability contribute to an 8.23% CAGR in the service channel.

Which region leads future growth?

North America registers the fastest expansion at 7.28% CAGR as EPA rules sustain demand for advanced ICE thermal components.

Page last updated on: