Hydraulic Motors Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

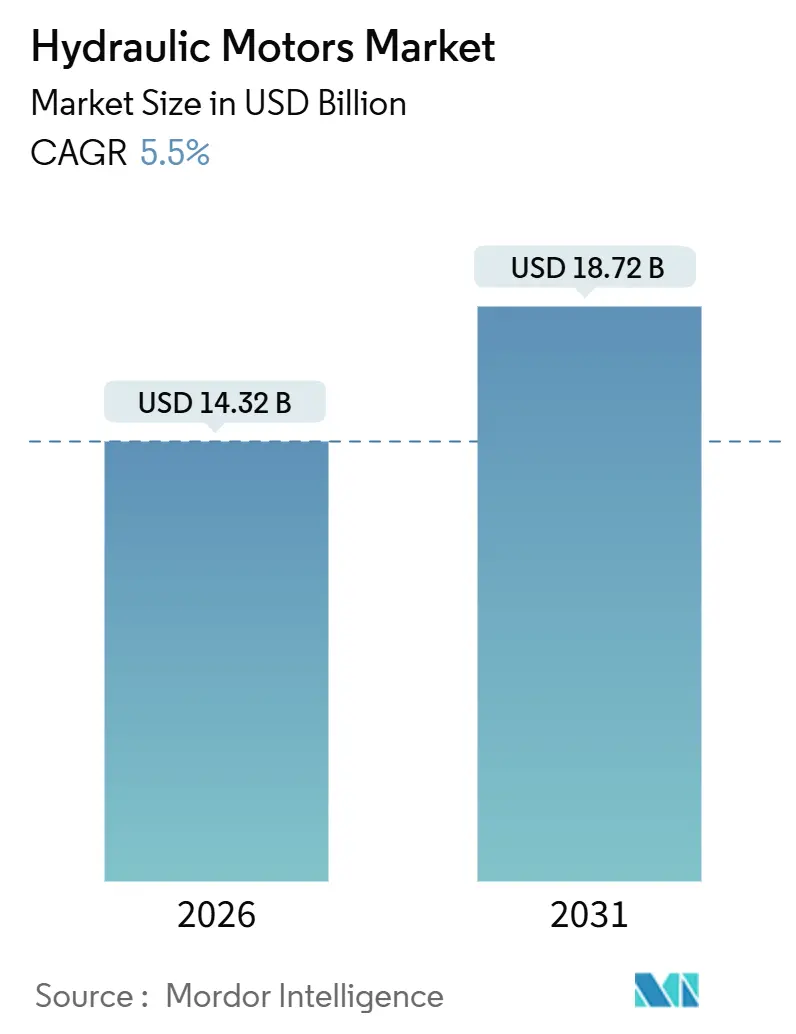

| Market Size (2026) | USD 14.32 Billion |

| Market Size (2031) | USD 18.72 Billion |

| Growth Rate (2026 - 2031) | 5.50% CAGR |

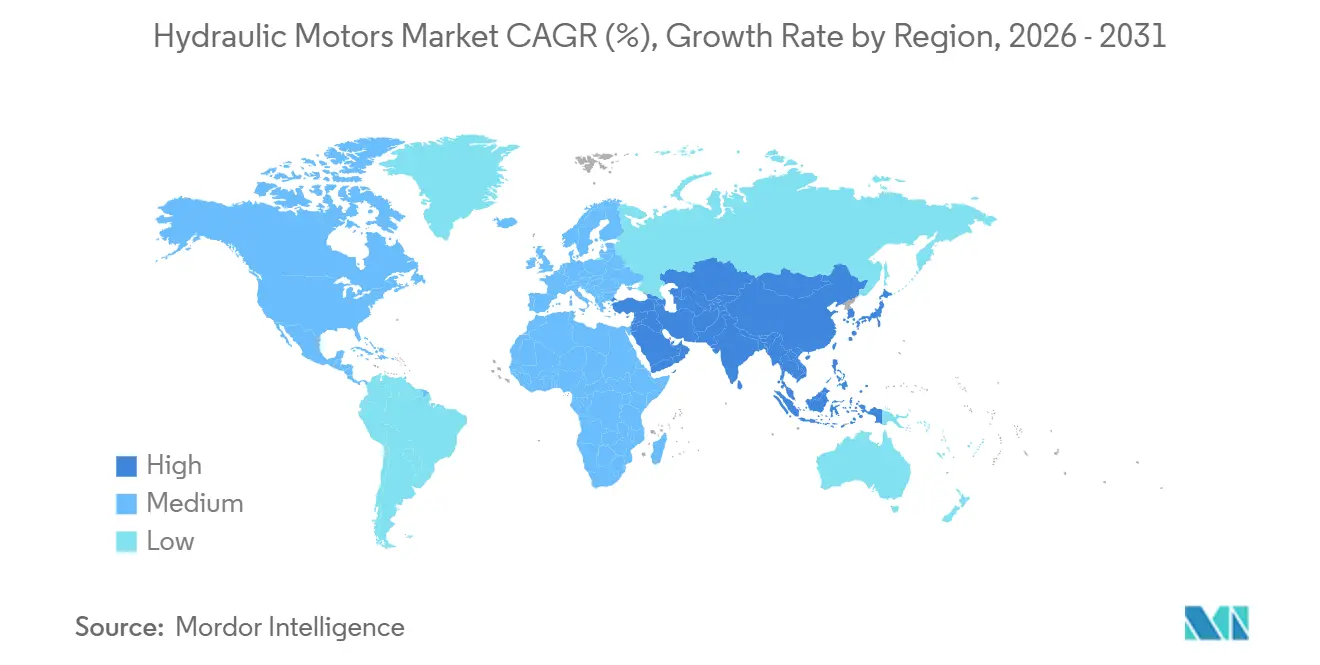

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

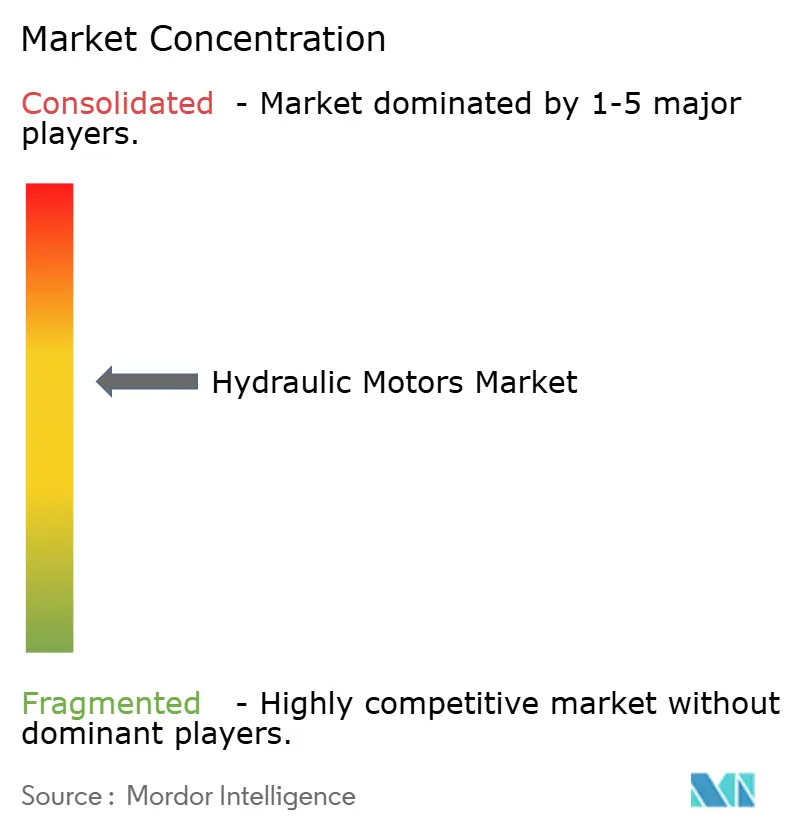

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hydraulic Motors Market Analysis by Mordor Intelligence

The hydraulic motors market size stands at USD 14.32 billion in 2026 and is projected to reach USD 18.72 billion by 2031, reflecting a 5.50% CAGR during the forecast period. Persistent demand for compact, high-torque power transmission in construction machinery and precision agriculture keeps the hydraulic motors market firmly on a mid-single-digit growth path despite encroaching electrification. Piston designs with variable-displacement control continue to win share because load-sensing accuracy yields measurable fuel savings for off-road equipment fleets. Asia-Pacific infrastructure megaprojects underpin volume gains, while IoT-enabled condition monitoring and bio-based fluid compatibility reshape the value proposition from pure hardware to uptime-driven services. Raw-material cost spikes and tighter leakage regulations temper margins, yet hybrid electro-hydraulic drivetrains point to a long runway of incremental efficiency improvements that sustain OEM investment in advanced motor architectures.

Key Report Takeaways

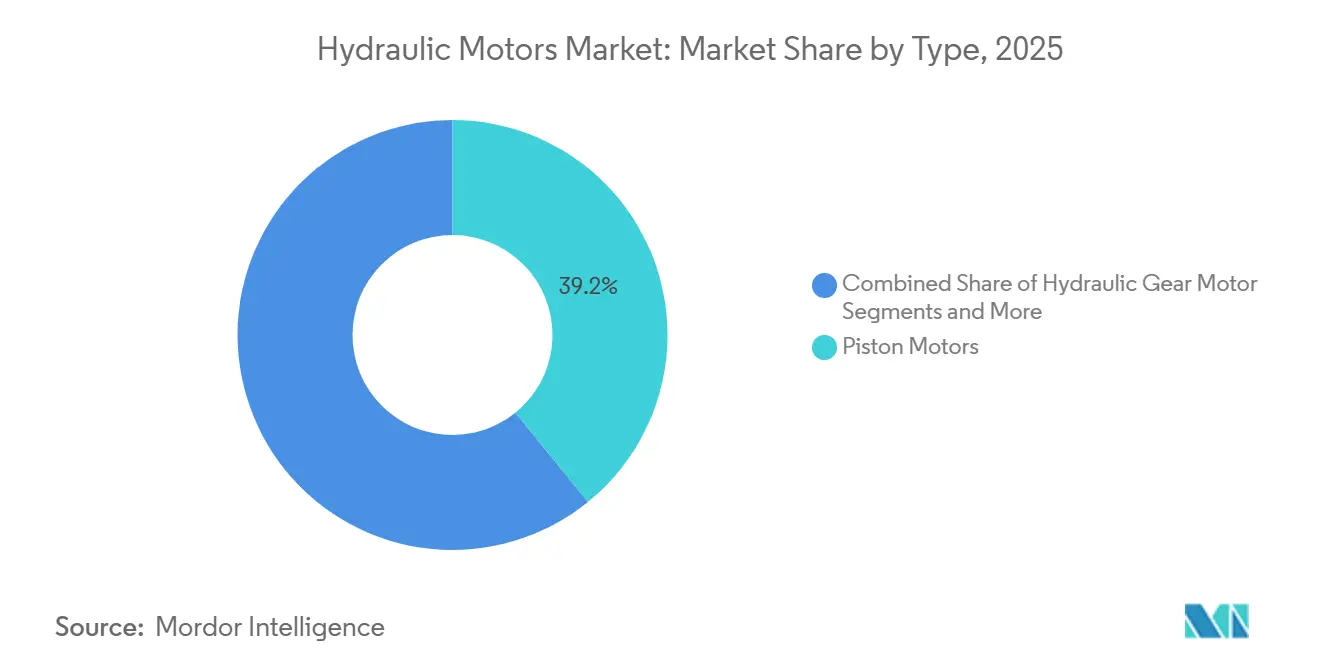

- By type, piston motors led the hydraulic motors market with 39.15% of the market share in 2025; the segment is forecast to expand at a 6.52% CAGR through 2031, outpacing gear and vane alternatives.

- By speed, low-speed motors held 57.01% of the hydraulic motors market share in 2025, while high-speed variants are projected to register the highest 8.02% CAGR through 2031.

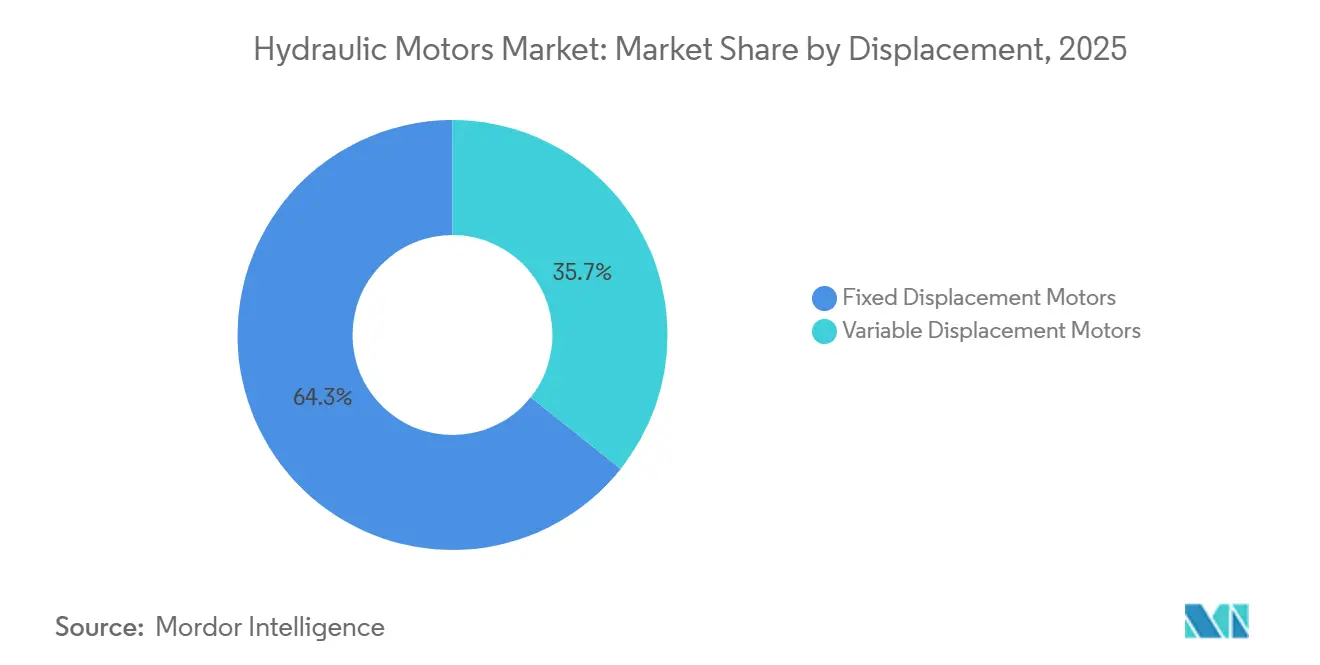

- By displacement, fixed-displacement motors captured 64.25% of the hydraulic motors market size in 2025; variable-displacement motors are poised for a 7.85% CAGR during the forecast period.

- By application, off-road machinery accounted for 52.36% of the hydraulic motors market in 2025 and is expected to grow at a 6.13% CAGR through 2031.

- By geography, the Asia-Pacific region dominated the hydraulic motors market with 45.15% market share in 2025 and is advancing at a 7.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hydraulic Motors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Construction and Mining Equipment | +1.8% | Asia-Pacific core, spill-over to the Middle East and Africa | Medium term (2-4 years) |

| Rise in Offshore Energy Projects | +1.2% | Europe, Asia-Pacific, United States Gulf | Medium term (2-4 years) |

| Electro-Hydraulic Hybrid Drivetrains | +1.1% | Asia-Pacific, North America | Medium term (2-4 years) |

| Growth of Precision Agriculture Machinery | +0.9% | North America, Europe, and early adoption in Brazil and Argentina | Long term (≥ 4 years) |

| IoT-Enabled Condition Monitoring | +0.7% | Global, led by North America and Western Europe | Short term (≤ 2 years) |

| Adoption of Bio-Based Fluids | +0.5% | Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Construction and Mining Equipment Demand in Emerging Markets

In China, India, Indonesia, and Vietnam, robust infrastructure pipelines are driving the full-throttle operation of crawler excavators, tunnel-boring machines, and mining draglines. This surge cements the hydraulic motors market as a pivotal supply node. China has seen a significant increase in construction machine production, driven by subway extensions and high-speed rail corridors. India has earmarked USD 1.4 trillion through 2025 for highways, ports, and coal mine expansions, each project relying on closed-center load-sensing circuits built around piston motors [1]“National Infrastructure Pipeline,” Government of India, india.gov.in. In Southeast Asia, megaprojects like Nusantara and the North-South Expressway are turning to radial-piston units. These units, capable of delivering high torque at low speeds, are essential for drilling through challenging geology. Meanwhile, Saudi Arabia’s NEOM and other Gulf projects are rapidly increasing imports of Japanese and European excavators. This surge is not just about the machines; it's birthing a thriving aftermarket for motor refurbishment. In Australia and Chile, mining operators are innovating by retrofitting variable-displacement motors. This move not only shortens their replacement cycles but also slashes diesel consumption during uphill hauls.

Rise in Offshore Energy Projects Demanding High-Torque Hydraulic Solutions

Offshore wind installations added 8 GW in 2024, with floating platforms favoring hydraulic slewing motors rated at 1,200 kNm because electric drives cannot match torque density within tight nacelle envelopes [2]“Global Offshore Wind Report 2025,” International Energy Agency, iea.org. Cadeler's Wind Orca and similar vessels depend on these motors for the precise positioning of large nacelles. In Brazil's pre-salt fields, subsea ROVs utilize pressure-compensated radial-piston designs to maintain torque at significant depths. Offshore cranes in the North Sea use high-speed vane motors in their winches to minimize load swing during personnel transfers. Even as new-build activities continue, the demand for massive hydraulic deck machinery persists, especially for jacket decommissioning in the United Kingdom Continental Shelf.

Electro-Hydraulic Hybrid Drivetrains Driving Demand for High-Efficiency Motors

Komatsu's HB215LC-3 excavator integrates a lithium-ion battery with variable-displacement pumps, significantly reducing fuel consumption while maintaining its full breakout force. Hybrid systems harness swing-brake energy, positioning piston motors at the heart of energy-recovery loops. Major industry players are intensifying R&D efforts, focusing on quicker swashplate actuation to maximize energy capture. Notably, Danfoss secured multiple patents for control algorithms in 2024. While Asian OEMs spearhead commercial rollouts, North American manufacturers are accelerating prototype developments, aiming for future market launches. This innovative architecture not only extends the relevance of hydraulic propulsion amidst the industry's electrification trend but also bolsters the long-term growth trajectory of the hydraulic motors market.

Growth of Precision Agriculture Machinery Requiring Hydraulic Power

In 2024, 68% of large-scale crop farms in the United States featured precision technologies that count on hydraulic steering actuators and variable-rate planters[3]“Precision Agriculture Adoption,” U.S. Government Accountability Office, gao.gov. John Deere's ExactEmerge, utilizing closed-loop hydraulic drives, achieves exceptional seed spacing precision at high speeds, a capability beyond the reach of mechanical systems. In the EU, subsidies are incentivizing vineyards to adopt hydraulic-powered robotic pruners, significantly reducing labor costs. Brazil, with its substantial sugarcane harvest, is transitioning to variable-displacement axial-piston motors, enhancing juice extraction efficiency. In Argentina, no-till equipment, experiencing steady growth, employs hydraulic down-force controls to maintain consistent seed depth, even on uneven terrain.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw Material Price Volatility | -0.6% | Global | Short term (≤ 2 years) |

| Compact Electric Drive Competition | -0.5% | North America, Europe, Japan | Long term (≥ 4 years) |

| Stringent Hydraulic Leakage Regulations | -0.4% | Europe, North America | Medium term (2-4 years) |

| Reshoring Driven Component Shortages | -0.3% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility Affecting Motor Costs

Steel indices in the United States rose sharply, while copper prices also increased, driving up costs for motor casings and windings. Neodymium oxide, a critical component in hybrid systems, has become more expensive, prompting manufacturers to explore ferrite substitutes that result in reduced torque density. In a strategic move, Eaton acquired Jiangsu Jinfan Hydraulics, securing captive casting and highlighting the importance of vertical integration as a protective measure. Meanwhile, smaller Tier-2 suppliers are transferring these rising costs downstream, exerting pressure on distributor margins. This market volatility is impacting short-term profitability in the hydraulic motors sector.

Competition from Compact Electric Drives in Low-Torque Ranges

Brushless servos in robotic assembly cells and CNC indexers offer zero-leak operation and faster response than small hydraulic drives. Electric cylinders now claim payloads up to 50 kN, encroaching on mid-tier gear-motor applications in factory automation. European automation giants bundle electric actuators with digital twins, appealing to Industry 4.0 integrators. Yet, high-torque construction and mining tasks remain solidly hydraulic, shielding the core hydraulic motors market from wholesale displacement.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Piston Motors Extend Leadership on Variable-Displacement Versatility

Piston motors captured 39.15% of the hydraulic motors market share in 2025, and the same segment is also set to expand at a 6.52% CAGR through 2031. Flexible swashplate control allows axial-piston designs to modulate flow precisely, trimming fuel burn in excavator swing drives. Radial-piston variants excel at ultra-low speeds below 10 RPM, making them a key component in mining winches and offshore cranes.

Gear motors remain cost-effective for municipal fleets, while epicyclic gearsets make compact track loaders more agile. Vane units hold niches in plastics and mixing lines, where balanced rotors cut vibration. The rise of hybrid drivetrains reinforces piston-motor demand, keeping this category ahead in the hydraulic motors market through 2031.

By Speed: High-RPM Units Gain Traction in Offshore and Compact Equipment

Low-speed motors retained 57.01% of the hydraulic motors market share in 2025, as construction and mining equipment crave torque at modest rpm. Nonetheless, high-speed designs are growing fastest at 8.02% through 2031, supplying offshore wind vessels with compact slewing drives that keep nacelle mass down.

Wheel loaders like Volvo’s L350H use gear motors in cooling circuits, freeing chassis space for emissions hardware. Agricultural harvesters mix low-speed threshing drums with high-speed cooling fans, straddling both design camps. As floating wind and mobile machinery continue to prioritize power-to-weight, high-speed motors should carve out a larger share of the hydraulic motors market over the forecast period.

By Displacement: Variable Designs Accelerate on Load-Sensing Economics

Fixed-displacement motors still hold 64.25% of the hydraulic motor market share in 2025 and dominate refuse trucks and forestry harvesters due to their simplicity. Variable-displacement motors, however, are advancing 7.85% annually, saving up to 18% input power by matching output to load.

Caterpillar’s 336 excavator throttles engine speed during light digging without cycle-time penalties, showcasing swashplate agility [4]“336 Excavator Technical Specifications,” Caterpillar Inc., caterpillar.com. Mining haul trucks recover kinetic energy on descents, thereby significantly extending brake life. By 2031, variable designs are poised to challenge and potentially diminish the dominance of fixed motors in the hydraulic motors market, driven by mounting regulatory pressures on fuel economy.

By Application: Off-Road Machinery Anchors Demand and Growth

Off-road machinery accounted for 52.36% of the hydraulic motors market share in 2025, the largest share. Construction machinery alone consumed a notable share of global volume, riding a production surge in China and India. Precision agriculture implements rely on variable-displacement motors to manage seed and chemical inputs, driving a 6.13% CAGR for the segment through 2031.

Industrial machinery demand spans plastics molding, CNC machining, and marine propulsion. Offshore vessels use hydraulic motors for dynamic positioning and crane operations at depths up to 3,000 meters. While industrial applications grow steadily, faster replacement cycles in construction and agriculture will keep off-road machinery at the forefront of the hydraulic motors market growth.

Geography Analysis

Asia-Pacific generated 45.15% of the hydraulic motors market share in 2025 and is projected to record a 7.21% CAGR through 2031. China's significant machinery production and India's large-scale infrastructure investments are driving strong demand for excavators and loaders. Japanese exporters are benefiting as Southeast Asian countries upgrade their fleets with hybrid excavators, while South Korean shipyards are increasingly specifying high-torque motors for deck equipment. Emerging megaprojects in Indonesia and Vietnam are further boosting the regional hydraulic motors market.

North America holds a notable share of the market, supported by widespread adoption of precision agriculture in the United States row crops and retrofitting activities in Canadian oil sands. Planned offshore wind capacity is also driving demand for high-speed vane motors in installation vessels. Europe captures a significant portion of revenue, driven by advancements in Germany's automation sector and wind energy projects in the North Sea. Subsidies for agricultural technology are encouraging the adoption of robotic pruners in vineyards, further supporting the uptake of hydraulic technology.

South America accounts for a smaller share, with Brazil's sugarcane harvest driving upgrades to axial-piston motors for improved cutter speed modulation, and Argentina experiencing growth in no-till farming equipment. The Middle East and Africa are witnessing steady growth, supported by large-scale infrastructure projects in Saudi Arabia and the United Arab Emirates, which are boosting excavator imports. Globally, infrastructure and agriculture remain the key drivers of growth in the hydraulic motors market.

Competitive Landscape

In the hydraulic motors market, the top suppliers—Bosch Rexroth, Eaton, Parker Hannifin, Danfoss, and Kawasaki—accounted for a significant share of revenue in 2025, indicating moderate concentration. Tier-1 suppliers are setting themselves apart with digital services. For instance, Bosch Rexroth’s CytroConnect and ABB’s Ability leverage cloud-streamed telemetry to minimize downtime. In a strategic move, Eaton heavily invested in eMobility R&D, while Parker Hannifin bolstered its portfolio by acquiring Meggitt’s electro-hydraulic actuation business.

Bio-fluid compatibility opens niches for Hydro Leduc and Sunfab, who offer ester-ready motors for forestry and marine applications. Danfoss leads patent filings in swashplate control speed, enhancing efficiency gains. Chinese challengers such as LHY Powertrain deliver piston motors at significantly lower prices, leveraging domestic economies of scale to penetrate price-sensitive customers in Asia-Pacific.

Vertical integration accelerates: Eaton’s Jiangsu Jinfan buy secures casting capacity against steel volatility. Regulatory moves, notably Per- and Polyfluoroalkyl Substances (PFAS) bans and Volatile Organic Compounds (VOCs) caps, raise R&D barriers, tilting the field toward capital-rich incumbents. Consequently, premium segments gravitate toward IoT-ready, hybrid-compatible products, while cost-conscious buyers in South America and Africa still choose fixed-displacement gear motors, preserving a two-tier competitive landscape in the hydraulic motors market.

Hydraulic Motors Industry Leaders

Bosch Rexforth AG

Parker Hannifin Corp.

Eaton Corporation plc

Danfoss Power Solutions

Kawasaki Heavy Industries, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Czechoslovak Group agreed to acquire Hydraulics s.r.o., adding linear hydraulic motors and cylinders to its land-systems portfolio.

- July 2025: Danfoss Power Solutions launched the Thorx CLM 5 C cam-lobe motor for road-roller drum drives, touting 92% total efficiency and reduced leakage.

- May 2024: Poclain introduced the MI330 torque motor, delivering 600 kW and 30% greater displacement for tunnel boring and wind farm equipment.

- April 2024: Black Bruin unveiled the X-series rotating-shaft motors, targeting the recycling, marine, and material-handling sectors, with a patent-pending design.

Global Hydraulic Motors Market Report Scope

The scope includes segmentation by type (hydraulic gear motor (gear motor and epicyclic gear motor), vane motor, and piston motor (radial piston motor and axial piston motor)), speed (low-speed motors and high-speed motors), displacement (fixed displacement motors and variable displacement motors), and application (off-road (construction machinery, agricultural machinery, and mining machinery), and industrial (manufacturing and marine)). The analysis also covers regional-level segmentation, including North America, South America, Europe, Asia-Pacific, the Middle East, and Africa. Market size and growth forecasts are presented by value in USD.

| Hydraulic Gear Motor | Gear Motor |

| Epicyclic Gear Motor | |

| Vane Motor | |

| Piston Motor | Radial Piston Motor |

| Axial Piston Motor |

| Low-Speed Motors |

| High-Speed Motors |

| Fixed Displacement Motors |

| Variable Displacement Motors |

| Off-road Machinery | Construction Machinery |

| Agricultural Machinery | |

| Mining Machinery | |

| Industrial Machinery | Manufacturing |

| Marine |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Hydraulic Gear Motor | Gear Motor |

| Epicyclic Gear Motor | ||

| Vane Motor | ||

| Piston Motor | Radial Piston Motor | |

| Axial Piston Motor | ||

| By Speed | Low-Speed Motors | |

| High-Speed Motors | ||

| By Displacement | Fixed Displacement Motors | |

| Variable Displacement Motors | ||

| By Application | Off-road Machinery | Construction Machinery |

| Agricultural Machinery | ||

| Mining Machinery | ||

| Industrial Machinery | Manufacturing | |

| Marine | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the hydraulic motors market?

The hydraulic motors market size is USD 14.32 billion in 2026 and is forecast to reach USD 18.72 billion by 2031, advancing at a 5.5% CAGR.

Which motor type leads global revenue?

Piston motors dominate with 39.15% of 2025 revenue thanks to variable-displacement capability and are set to grow at a 6.52% CAGR.

How fast are high-speed hydraulic motors growing?

High-speed variants, favored in offshore wind and compact machinery, are expected to expand at an 8.02% CAGR through 2031.

Why is Asia-Pacific the largest regional market?

Massive infrastructure programs in China and India, plus strong shipbuilding activity in Japan and South Korea, give Asia-Pacific 45.15% of 2025 revenue and the fastest 7.21% CAGR.

Page last updated on: