Automotive Hydraulic Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

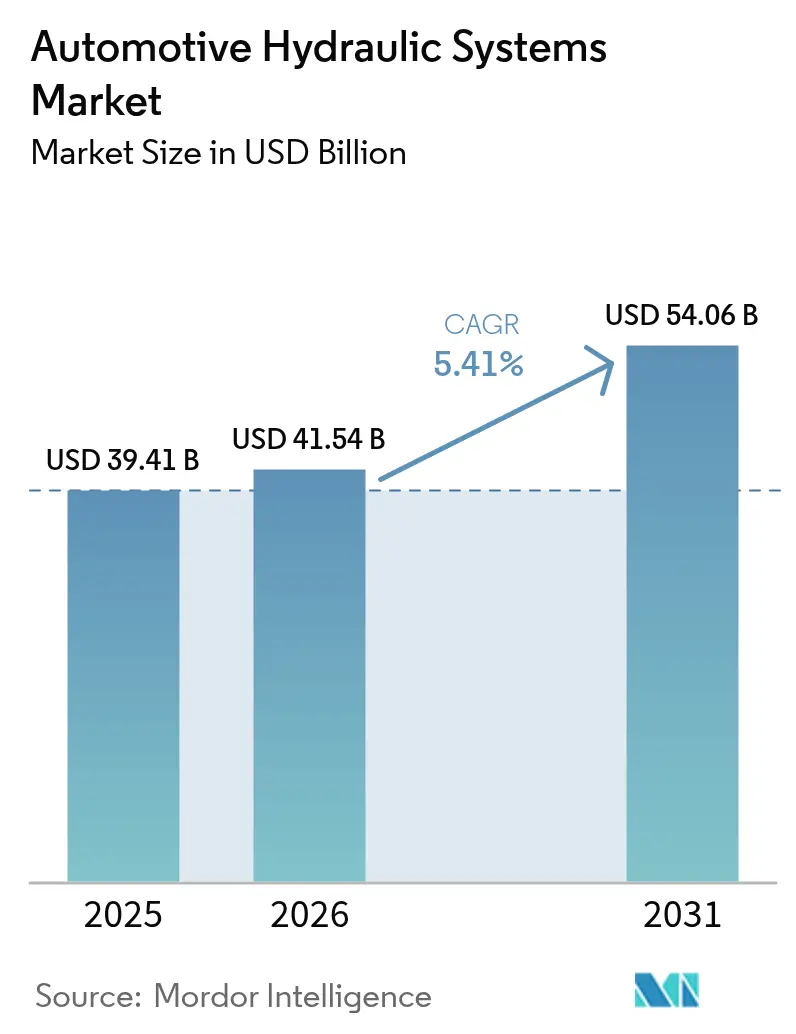

| Market Size (2026) | USD 41.54 Billion |

| Market Size (2031) | USD 54.06 Billion |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Hydraulic Systems Market Analysis by Mordor Intelligence

The Automotive Hydraulics Systems Market size was valued at USD 39.41 billion in 2025 and estimated to grow from USD 41.54 billion in 2026 to reach USD 54.06 billion by 2031, at a CAGR of 5.41% during the forecast period (2026-2031). Despite electrification, the steady advance reflects the sector’s ability to preserve its core braking, steering, and suspension roles. Stricter global brake-safety mandates, rising commercial-vehicle output, and the spread of electro-hydraulic modules into Level 3+ autonomous driving platforms continue to lift demand. Thanks to China’s production growth and India’s capacity additions, Asia-Pacific remains the manufacturing hub, while Africa represents an emerging opportunity as infrastructure spending gains traction. At the same time, premium-vehicle makers rely on hydraulic suspension to differentiate ride quality, and commercial fleets prioritize tried-and-tested hydraulic reliability over experimental alternatives.

Key Takeaways

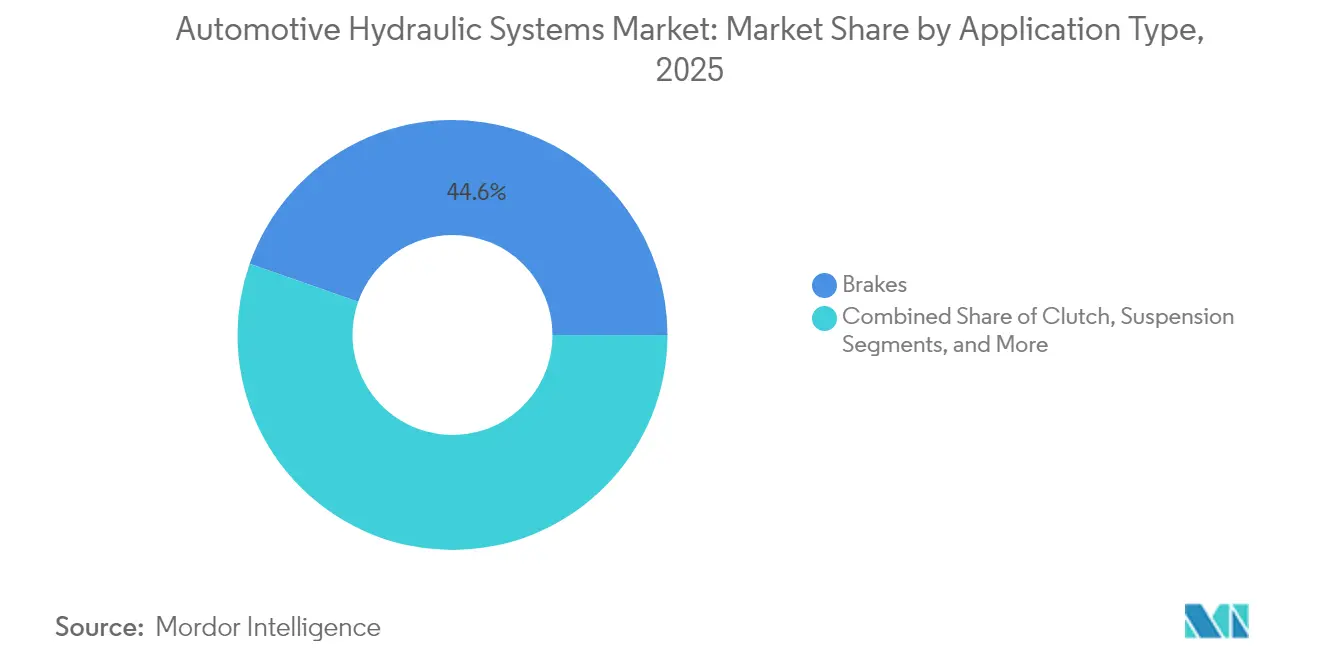

- By application, brakes held 44.62% of the automotive hydraulics systems market share in 2025, whereas power-steering assist is set to grow at a 6.19% CAGR to 2031.

- By component, master cylinders led with 34.88% revenue share in 2025; hydraulic pumps are projected to expand at a 7.05% CAGR.

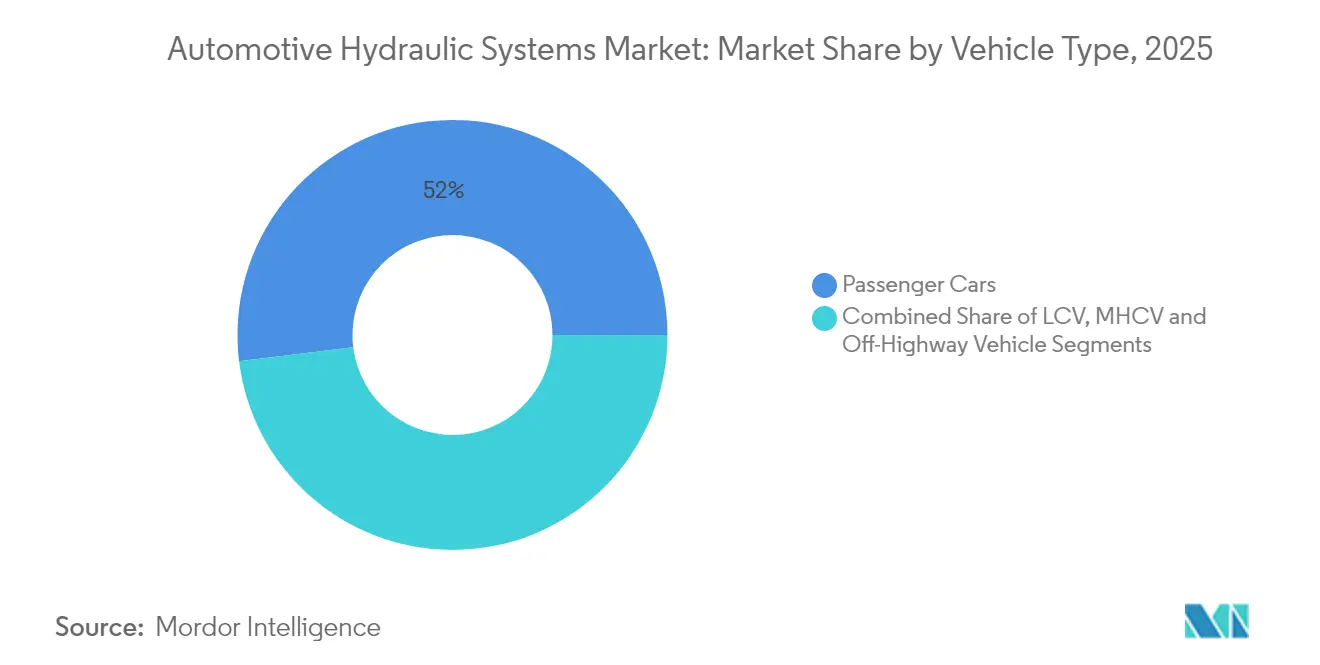

- By vehicle type, passenger cars accounted for 51.95% of the automotive hydraulics systems market size in 2025, while off-highway vehicles will post the fastest 6.9% CAGR.

- By sales channel, OEM shipments commanded a 68.55% share of the automotive hydraulics systems market size in 2025, whereas the aftermarket advances at a 6.2% CAGR.

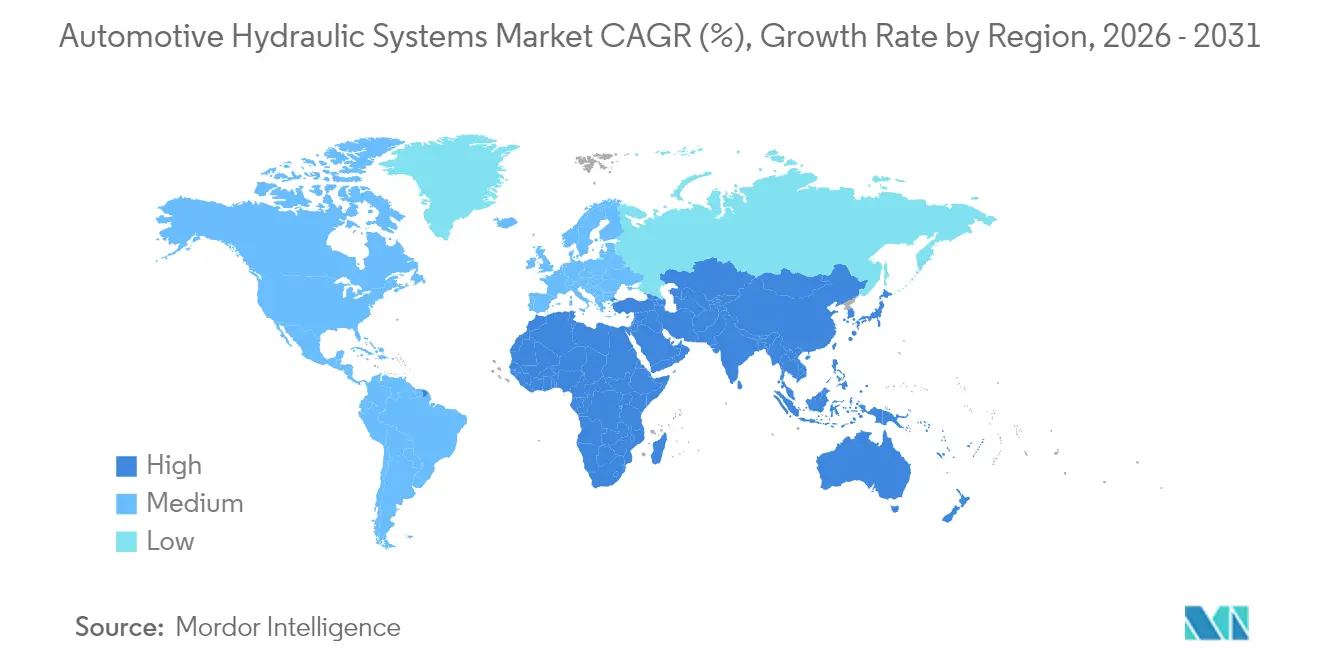

- By geography, Asia-Pacific captured 48.42% revenue share in 2025; Africa is forecast to climb at a 7.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Hydraulic Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Commercial-Vehicle Production & Sales | +1.2% | Asia-Pacific, North America | Medium term (2-4 years) |

| Stricter Brake-Safety Mandates (ABS, ESC, EBS) | +1.0% | North America, Europe | Short term (≤2 years) |

| Growing Premium-Vehicle Demand for Hydraulic Suspension | +0.8% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Electro-Hydraulic Modules for Level-3+ AD Systems | +0.7% | North America, Europe, Asia-Pacific | Long term (≥4 years) |

| Low-Cost Hydraulic Packs for Entry-Level EVs in Emerging Markets | +0.6% | Asia-Pacific, MEA, Latin America | Medium term (2-4 years) |

| Regenerative Hydraulic Energy-Storage in Hybrid Suspensions | +0.4% | Germany, Japan, California | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Global Commercial Vehicle Production & Sales

Surging truck and bus output increases hydraulic content per unit because heavy platforms need multiple high-pressure circuits for braking, steering, and auxiliary drives. India’s industry produced 30.6 million vehicles in 2024, reinforcing hydraulic demand across domestic and export markets.[1]“SIAM Annual Report 2025,” Society of Indian Automobile Manufacturers, siam.in U.S. fleet operators face chassis shortages, prompting higher utilisation of trucks requiring regular hydraulic upkeep. Electric powertrains in zero-emission trucks introduce extra thermal management loops that remain hydraulic, further sustaining component volumes. Operators value proven durability, which supports the automotive hydraulics systems market even as electrification spreads.

Stricter Brake-Safety Mandates (ABS, ESC, EBS)

New rules oblige carmakers to install automatic emergency braking and enhanced stability control that rely on precise hydraulic modulation. NHTSA’s FMVSS 127 covers all U.S. light vehicles from September 2029 and sets collision-avoidance speed targets of 62 mph.[2]“FMVSS 127 Final Rule,” National Highway Traffic Safety Administration, nhtsa.gov The EU’s upcoming Euro 7 standards bring brake particle limits, driving the adoption of low-dust hydraulic components. These requirements enlarge the addressable demand for advanced valves, boosters, and micro-pumps within the automotive hydraulics systems market

Growing Premium-Vehicle Demand for Hydraulic Suspension

Premium marques increase the use of active hydraulic suspension to separate ride comfort from road inputs in milliseconds. Germany’s passenger-car production reached 340,800 units in January 2025, driven by luxury brands that specify predictive hydraulic damping to secure a competitive advantage.[3]“German Passenger Car Production January 2025,” Verband der Automobilindustrie, vda.deThe platform-agnostic technology shifts smoothly onto battery-electric architectures, protecting future volumes.

Electro-Hydraulic Modules for Level-3+ AD Systems

Autonomous driving prioritizes redundancy, so fail-safe hydraulic subsystems back up electronic actuators. SAE Level 3+ definitions require systems that manage sudden failures independently, making electro-hydraulic converters essential. U.S. policy stresses safety redundancy, positioning hydraulic suppliers as indispensable partners in automated platforms.[4]“Automated Vehicle Policy Update,” U.S. Department of Transportation, transportation.gov Predictive diagnostics in these modules open service revenue streams in the automotive hydraulics systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Shift to Fully-Electric Brake & Steering Systems | -1.5% | Global, accelerated in Europe and California | Medium term (2-4 years) |

| Environmental Concerns Over Hydraulic-Fluid Leakage | -0.8% | North America and Europe | Short term (≤2 years) |

| Elastomer-Seal Raw-Material Shortages Inflating Costs | -0.6% | Global supply chain impact, acute in Asia-Pacific manufacturing | Short term (≤2 years) |

| OEM Preference for Dry Brake-by-Wire in Robotaxi Fleets | -0.4% | North America & Europe early deployment, Asia-Pacific following | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rapid Shift to Fully-Electric Brake & Steering Systems

Battery EV platforms target weight savings and precise control, favouring electromechanical units that omit fluid lines. EPA multi-pollutant standards accelerate this transition in the United States. German suppliers reorganise production footprints as electric models trim hydraulic content. Commercial trucks move more slowly because of higher force requirements, yet long-term substitution risk weighs on the automotive hydraulics systems market.

Environmental Concerns Over Hydraulic-Fluid Leakage

Global regulators tighten oversight of PFAS and fire-resistant fluids. The EPA requires detailed PFAS reporting between November 2024 and May 2025, prompting costly reformulations. Sealed systems and alternative technologies gain favour as OEMs seek lower liability, creating design pressure within the automotive hydraulics systems market

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application – Brakes Dominate Despite Electric Transition

Brakes generated 44.62% of 2025 revenue, giving this segment the largest stake in the automotive hydraulics systems market. Regulatory mandates such as NHTSA’s emergency braking rule lock in resilient demand, and even pure EVs retain hydraulic backup circuits. Meanwhile, power-steering assist expands at a 6.19% CAGR as electro-hydraulic racks balance energy efficiency with steering feel. This illustrates how the automotive hydraulics systems market size can keep climbing inside electrified platforms.

Brake content remains stable because collision-avoidance systems need high-pressure modulation. Steering assist rises on the back of active-lane technologies that depend on fast hydraulic response. Suspension applications benefit from premium-car demand for ride comfort, while clutch and fan-drive uses fade in line with engine electrification. Regenerative hydraulic energy storage in commercial vehicles marks an emerging sub-segment with modest but steady contributions

By Component – Master Cylinders Lead Market Share

Master cylinders constituted 34.88% of component sales in 2025, underscoring their universal fit across vehicle classes. Their dominance ensures stable volume, while hydraulic pumps post the highest 7.05% CAGR as advanced driver assistance features require on-demand pressure. These figures translate into a portion of the automotive hydraulics systems market share for pumps, signalling a pivot from passive to active control architectures.

Reservoirs, hoses, and manifolds record incremental gains driven by lightweight designs using composite lines. Valves and actuators climb in value because integrated sensors enable closed-loop control. Accumulators face mixed prospects pending PFAS-free fluid solutions, yet research promises long-term relevance in hybrid suspension energy storage.

By Vehicle Type – Passenger Cars Maintain Leadership

Passenger cars represented 51.95% of 2025 revenue, anchoring the automotive hydraulics systems market. Off-highway vehicles, though smaller, achieve a 6.9% CAGR as construction and farming machinery expand across Asia and Africa. Commercial vans and trucks preserve hydraulic adoption due to load and duty-cycle realities, offering a buffer against passenger-car electrification.

Construction equipment relies on multi-circuit systems with pressures above 250 bar, which electric alternatives cannot yet replicate economically. Agricultural machinery merges precision farming with high-flow hydraulics, widening market scope. Light commercial vehicles stay relevant through last-mile services that demand reliable brake and steering components

By Sales Channel – OEM Dominance with Aftermarket Growth

OEMs integrated hydraulics during vehicle assembly, contributing 68.55% of 2025 sales, yet the aftermarket grew 6.2% CAGR as fleets extended service life and older cars remained on the road. Aftermarket expansion adds breadth to the automotive hydraulics systems market, especially for consumables such as fluid, seals, and hoses.

Independent distributors leverage e-commerce to reach global buyers, while performance specialists offer upgraded master cylinders and pumps that outlast factory units. Tariff uncertainty encourages regional sourcing, which could reshape supply networks and open room for smaller domestic producers.

Geography Analysis

Asia-Pacific commands 48.42% of global revenue in 2025, underscoring its status as the centre of gravity for the automotive hydraulics systems market. China produced 2.353 million vehicles in May 2024, a 7.6% year-on-year rise, while new-energy models jumped 33.6%. India’s 2024 output of 30.6 million units enlarges the regional automotive hydraulics systems market size and anchors long-term demand. Japan’s subsidy-backed EV rollout reduces some power-train hydraulic applications yet preserves brake and suspension needs, prompting suppliers to recalibrate portfolios. Deep supply chains and abundant labour make Asia-Pacific the default choice for volume components, though PFAS and leakage regulations force factories to upgrade fluid-handling processes.

North America mixes rigorous safety regulations with fast-tracking electrification, creating a dual pull on hydraulic demand. NHTSA’s new assessment protocols and FMVSS 127 sustain technical complexity in brake hydraulics, while EPA emissions rules accelerate EV adoption that can trim future volumes. The United States remains a Level 3 automation hub, giving electro-hydraulic module specialists a development advantage. Canada and Mexico buttress regional scale through integrated corridors under USMCA, stabilising supply for North American assemblers despite policy shifts.

Europe leads on rule-making yet battles eroding cost competitiveness, as Euro 7 particle limits and PFAS curbs force costly redesigns that only well-funded firms can absorb. Africa delivers the fastest 7.11% CAGR through 2031 from a low base, with infrastructure spending in Nigeria, Kenya and Egypt lifting off-highway hydraulic demand. South America shows steady growth tied to mining and agriculture machinery, though macroeconomic volatility clouds visibility. Middle Eastern markets combine legacy power-train preferences with industrial-policy incentives that could seed local hydraulic assembly.

Competitive Landscape

The automotive hydraulics systems market is moderately fragmented, with broad-portfolio suppliers such as Robert Bosch, ZF Friedrichshafen and Continental setting technology benchmarks. These groups bundle braking, steering, and suspension know-how into integrated offerings that simplify OEM sourcing. Tier-ones deploy vertical integration to secure calipers, valves, and electronic control units under one roof, ensuring calibration consistency. Smaller firms survive by niching into aftermarket upgrades or specialist segments like off-highway accumulators.

European incumbents emphasise premium system features such as predictive damping and low-dust brake materials to retain share. Asian challengers focus on cost and manufacturing scale, winning contracts in volume passenger-car programmes. U.S. players pursue software-driven electro-hydraulic modules for autonomous fleets. Parker Hannifin’s 2025 results reveal softer transportation sales, prompting capacity reviews that mirror industry adaptation. Environmental compliance and PFAS-free fluids create additional barriers that favour established R&D pipelines.

Partnerships with software companies grow as hydraulic hardware must align with vehicle networks and over-the-air diagnostics. Suppliers invest in digital twins and predictive maintenance to raise lifetime value. Consolidation remains on the horizon as component commoditisation pressures margins, yet intellectual property around fail-safe designs and fluid chemistry still commands strategic premiums

Automotive Hydraulic Systems Industry Leaders

Robert Bosch GmbH

Aisin Seiki Co. Ltd

ZF Friedrichshafen AG

BorgWarner

Continental AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: NHTSA updated the New Car Assessment Program to add blind-spot and pedestrian braking evaluations starting with 2026 models.

- October 2023: EPA finalized hydrofluorocarbon phasedown regulations that indirectly affect vehicles with hydraulically driven A/C compressors.

Global Automotive Hydraulic Systems Market Report Scope

Automotive hydraulic systems are used to power machines and equipment. Hydraulic systems use a specialized fluid, typically hydraulic oil, to transmit power.

The automotive hydraulic systems market is segmented by application, component, vehicle type, and geography. By application, the market is segmented into brakes, clutch, suspension, and other applications (tappets, etc.). By component, the market is segmented into master cylinder, slave cylinder, reservoir, and hose. By vehicle type, the market is segmented into passenger cars, light commercial vehicles, and medium and heavy-duty commercial vehicles. By geography, the market is segmented into North America, Europe, Asia-Pacific, and rest of the world. The report offers the market size in value terms in USD for all the abovementioned segments.

| Brakes |

| Clutch |

| Suspension |

| Power-steering Assist |

| Fan-drive Systems |

| Valve-train (Tappets/Actuators) |

| Others |

| Master Cylinder |

| Slave / Wheel Cylinder |

| Reservoir |

| Hose & Tubing |

| Hydraulic Pump |

| Valve & Manifold |

| Actuator / Booster |

| Accumulator & Seals |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium & Heavy-duty Commercial Vehicles |

| Off-highway Vehicles (Ag & Construction) |

| OEM |

| Aftermarket |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Application | Brakes | ||

| Clutch | |||

| Suspension | |||

| Power-steering Assist | |||

| Fan-drive Systems | |||

| Valve-train (Tappets/Actuators) | |||

| Others | |||

| By Component | Master Cylinder | ||

| Slave / Wheel Cylinder | |||

| Reservoir | |||

| Hose & Tubing | |||

| Hydraulic Pump | |||

| Valve & Manifold | |||

| Actuator / Booster | |||

| Accumulator & Seals | |||

| By Vehicle Type | Passenger Cars | ||

| Light Commercial Vehicles | |||

| Medium & Heavy-duty Commercial Vehicles | |||

| Off-highway Vehicles (Ag & Construction) | |||

| By Sales Channel | OEM | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Spain | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the Automotive Hydraulics Systems Market?

The market is worth USD 41.54 billion in 2026 and is expected to reach USD 54.06 billion by 2031.

Which region holds the largest automotive hydraulics systems market share?

Asia-Pacific leads with 48.42% revenue share in 2025 owing to China’s and India’s vehicle production strength.

Which application segment grows the fastest through 2031?

Power-steering assist posts the quickest 6.19% CAGR as electro-hydraulic racks support advanced driver-assistance features.

How will environmental regulations influence hydraulic systems?

PFAS reporting, fluid leakage limits and Euro 7 brake particle caps will require new fluid chemistries and sealed designs, increasing compliance costs.

Why do autonomous vehicles still need hydraulic components?

Level 3+ platforms mandate redundant braking and steering, and electro-hydraulic modules provide fail-safe actuation if electronic systems falter.

What drives aftermarket expansion in hydraulic systems?

Extended vehicle lifecycles and fleet cost control lift demand for replacement fluids, seals and upgraded master cylinders, fueling a 6.2% CAGR in the aftermarket channel.

Page last updated on: