Exhaust System Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

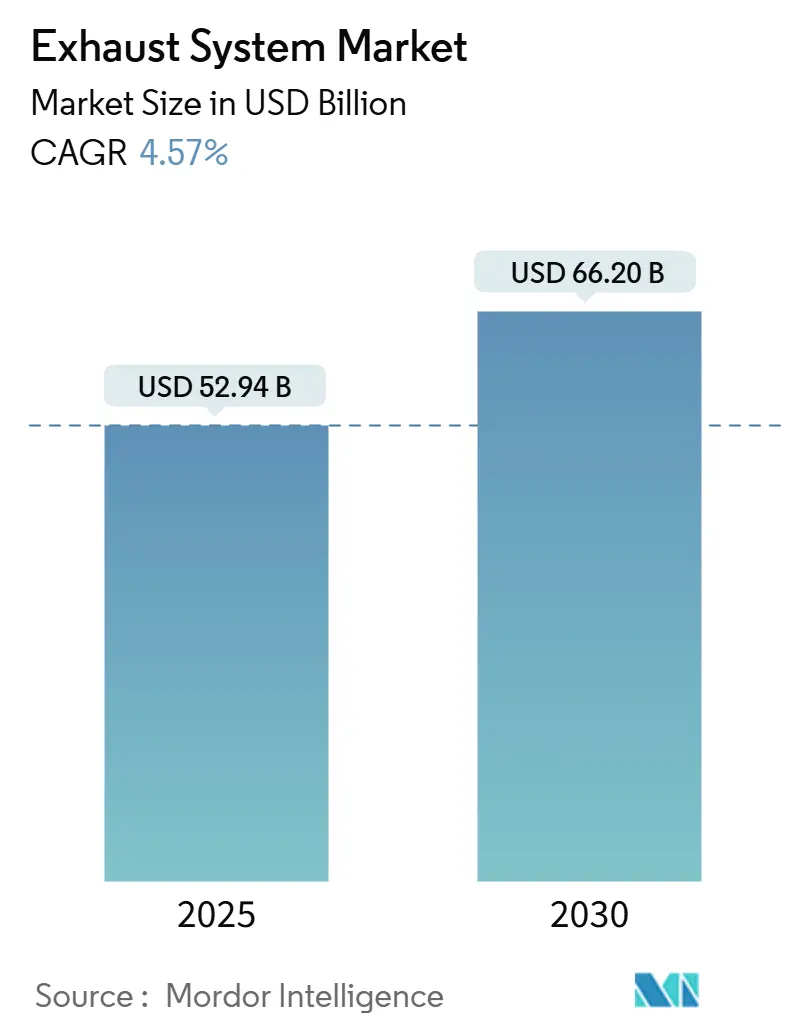

| Market Size (2025) | USD 52.94 Billion |

| Market Size (2030) | USD 66.20 Billion |

| Growth Rate (2025 - 2030) | 4.57% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Exhaust System Market Analysis by Mordor Intelligence

The Exhaust System Market size is estimated at USD 52.94 billion in 2025, and is expected to reach USD 66.20 billion by 2030, at a CAGR of 4.57% during the forecast period (2025-2030).

Heightened emission‐control rules, notably Euro 7 in Europe and National VI-b in China, are obliging automakers to adopt close-coupled catalysts, electrically heated substrates, and denser sensor arrays, thereby lifting per-vehicle content even as battery-electric sales rise.[1]European Commission, “Commission Adopts Euro 7 Proposal,” ec.europa.eu Hybrid and plug-in hybrid volumes reinforce short-term demand because every PHEV still requires a full exhaust train but endures harsher thermal cycling that accelerates catalyst aging.[2]International Energy Agency, “Global EV Outlook 2024,” iea.org Off-highway diesel retrofits in mining, agriculture, and power generation add an ancillary growth stream, while e-commerce parcel fleets shorten light-commercial-vehicle replacement intervals, expanding aftermarket sales. Material substitution is another theme: stainless steel dominates, yet titanium and nickel alloys are gaining share as OEMs chase weight reduction and higher operating temperatures.

Key Report Takeaways

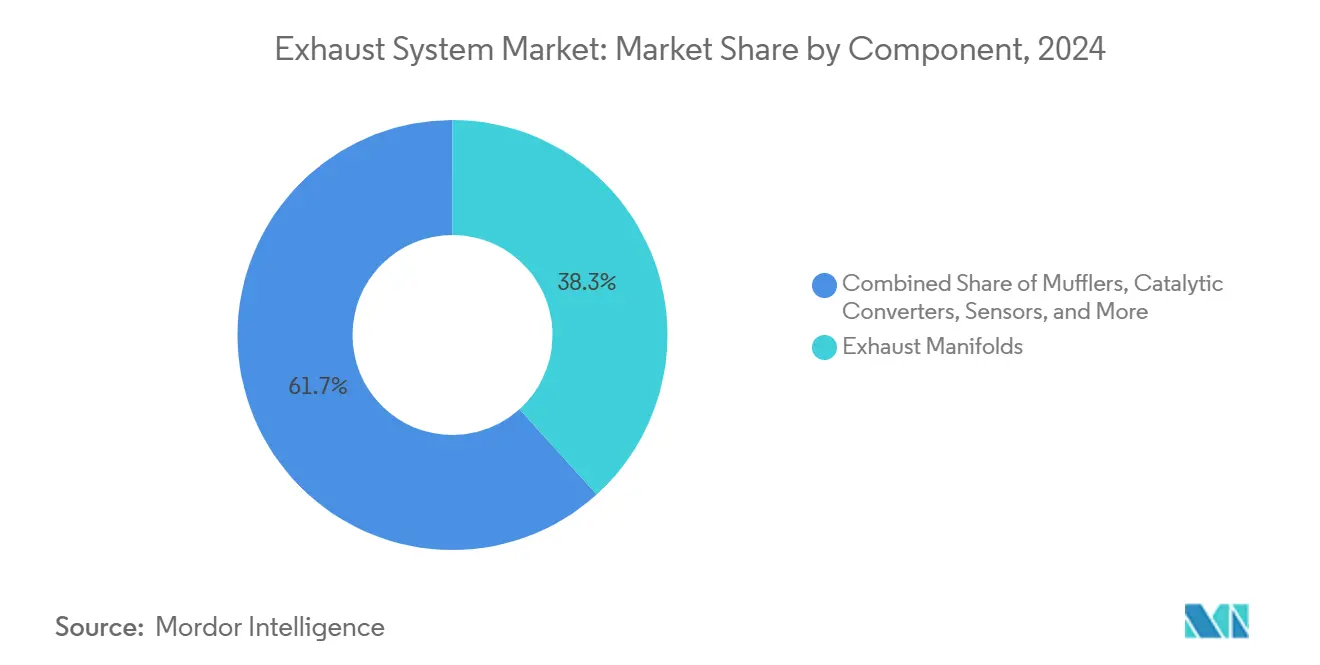

- By component, exhaust manifolds led with 38.3% of the exhaust systems market share in 2024; sensors are advancing at an 8.8% CAGR through 2030.

- By material, stainless steel accounted for 44.9% revenue in 2024, while titanium is forecast to expand at a 10.2% CAGR to 2030.

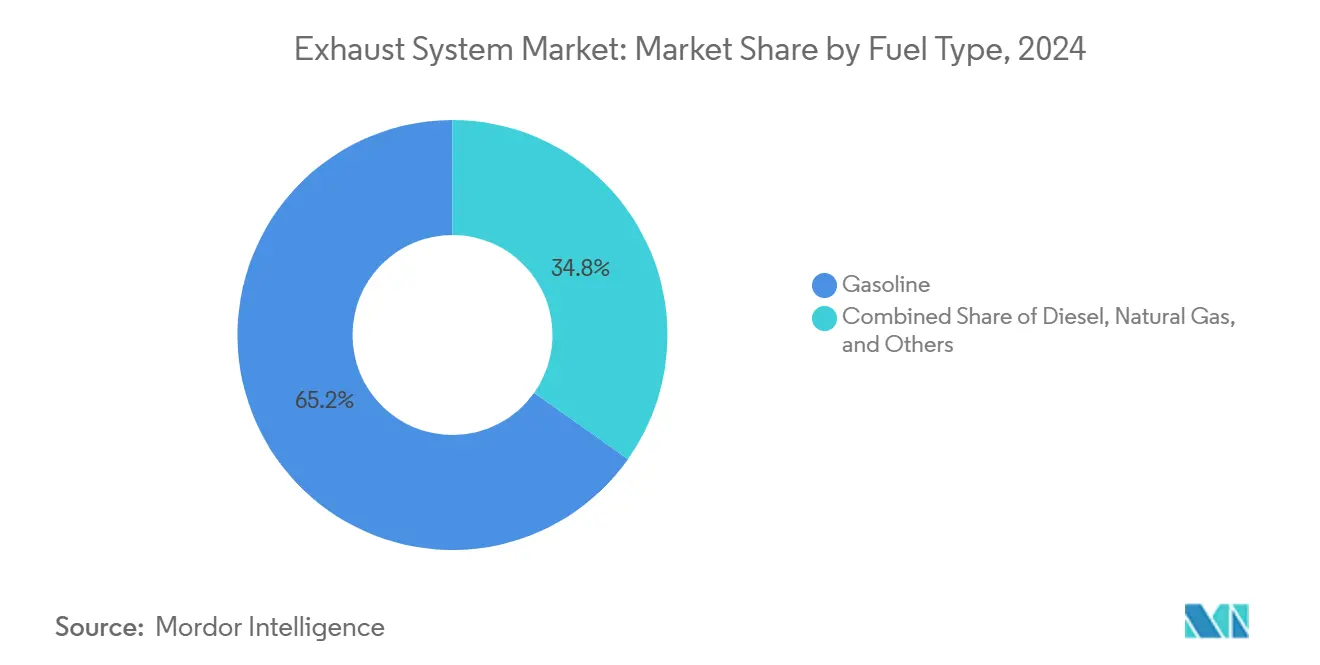

- By fuel type, gasoline systems held a 65.2% share of the exhaust systems market size in 2024, and natural-gas technology is set to climb at a 7.5% CAGR during 2025-2030.

- By end-user, automotive captured 92.7% revenue in 2024; industrial retrofits are rising but remain below 10% share.

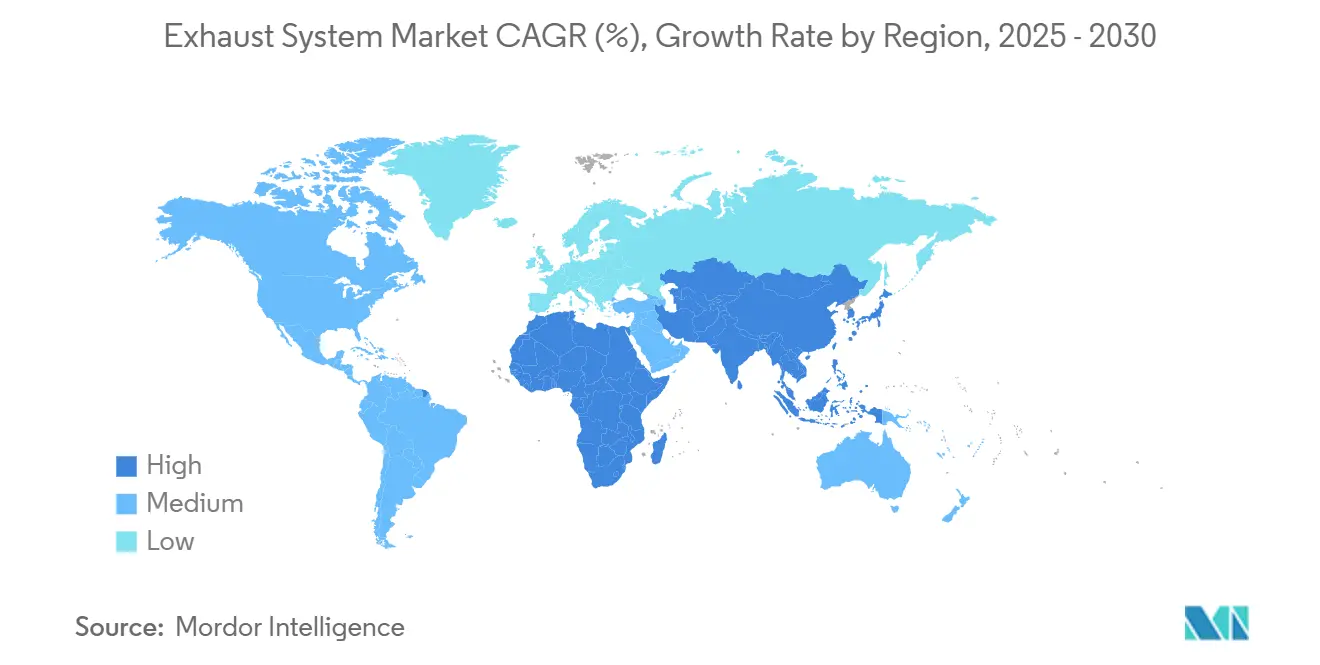

- By geography, Asia Pacific commanded 48.4% of the global exhaust systems market in 2024 and is poised for a 6.9% CAGR to 2030.

Global Exhaust System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening global emission norms | +1.2% | EU, China, India | Medium term (2-4 years) |

| Rising hybrid & plug-in hybrid volumes | +0.9% | North America, Europe, China | Short term (≤ 2 years) |

| Rapid growth of off-highway diesel retrofits | +0.6% | APAC, South America | Medium term (2-4 years) |

| OEM shift to integrated manifold-catalyst units | +0.7% | Global | Long term (≥ 4 years) |

| Surge in e-commerce driving LCV cycles | +0.5% | Europe, North America, APAC | Short term (≤ 2 years) |

| Smart exhausts with on-board sensors | +0.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening Global Emission Norms Drive Aftertreatment Complexity

Euro 7’s 10 mg/km particle limit and cold-start testing at -10 °C obligate electrically heated catalysts that light off within 30 seconds, adding cost and high-temperature alloy demand. China’s National VI-b extends ammonia-slip monitoring to heavy trucks and non-road machinery, pushing retrofit orders across 2.8 million units in 2024.[3]Ministry of Ecology and Environment China, “National VI-b Standards,” mee.gov.cn India’s Bharat Stage VII draft likewise proposes particle-number limits for gasoline direct-injection engines, forecasting gasoline particulate filter fitment on 85% of new cars by 2028. These overlapping rules require a single exhaust architecture flexible enough for EU cold-start needs, Chinese ammonia-slip thresholds, and Indian particle-number targets, inflating global platform engineering budgets by up to 20% per program. ISO 16183 OBD compliance has therefore become a de facto gatekeeper for global homologation.

Hybrid and PHEV Volumes Sustain ICE Exhaust Demand

Plug-in hybrid sales climbed 35% to 4.3 million units in 2024, and each vehicle retains a full exhaust system despite intermittent engine use. Frequent thermal cycling accelerates precious-metal sintering, positioning dual-layer catalysts, such as the palladium-plus-rhodium design in Toyota’s 2024 Prius PHEV, as premium solutions that maintain conversion efficiency over 240,000 km. Europe remains the largest PHEV region, led by Germany’s 780,000 registrations, which sustains demand for gasoline three-way catalysts even as the BEV share crests 22%.[4]European Automobile Manufacturers Association, “Commercial Vehicle Registrations 2024,” acea.auto Because catalysts cool below 200 °C during electric operation, lambda and temperature sensors must trigger rapid regeneration at engine restart, elevating sensor content per vehicle.

Off-Highway Diesel Retrofits Accelerate

China extended National VI-b limits to non-road machinery above 560 kW in 2024, prompting 340,000 mining truck retrofits averaging USD 12,000 per unit. Australia imposed Tier 4 Final equivalents across major mining states, spurring SCR adoption on excavators and loaders. U.S. state subsidies encouraged agricultural retrofit uptake; Deere installed 28,000 DPF-SCR kits on legacy tractors, generating USD 420 million aftermarket revenue. The retrofit cycle extends demand beyond new-equipment builds, guaranteeing exhaust module replacements every 8,000 operating hours into the next decade.

OEM Shift to Integrated Manifold-Catalyst Units

Close-coupled catalysts, located within 300 mm of the manifold, reach operating temperature 40% faster than underbody designs. Volkswagen’s MQB Evo integration trimmed part counts by 30% and cut assembly time by 12 minutes per vehicle, while Stellantis’s STLA Medium platform achieved a 2.8 kg weight cut through cast-aluminum manifolds brazed to catalysts. High-temperature nickel alloys such as Inconel 625 replaced 409 stainless steel in 18% of 2024 passenger-car launches, albeit at higher service-repair complexity that shifts aftermarket share toward dealer networks.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating BEV adoption eroding ICE parc | –1.4% | China, EU, North America | Long term (≥ 4 years) |

| Precious-metal price volatility | –0.8% | Global | Short term (≤ 2 years) |

| Divergent regional regulations | –0.5% | EU, China, India, North America | Medium term (2-4 years) |

| Catalytic-converter theft | –0.4% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating BEV adoption eroding ICE parc | –1.4% | China, EU, North America | Long term (≥ 4 years) |

| Precious-metal price volatility | –0.8% | Global | Short term (≤ 2 years) |

| Divergent regional regulations | –0.5% | EU, China, India, North America | Medium term (2-4 years) |

| Catalytic-converter theft | –0.4% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating BEV Adoption Erodes the ICE Vehicle Parc

Battery-electric vehicles captured 18% of global light-vehicle sales in 2024, and their share is projected to exceed 40% by 2030, trimming the ICE passenger-car parc by 100 million units over the period. China accounted for 8.1 million BEV sales in 2024, a 60% global share, signaling a 12 million-unit annual drop in future gasoline and diesel production. Europe’s planned 2035 ICE phase-out magnifies the risk; each BEV eliminates roughly USD 400 in exhaust content, compelling integrators to pivot toward fuel-cell balance-of-plant components with lower margins.

Precious-Metal Price Volatility Inflates Converter Cost

Palladium averaged USD 1,050/oz, and rhodium fluctuated near USD 5,000/oz in 2024, translating to USD 85-140 in metal per gasoline converter. OEMs thin washcoats or deploy BASF’s TriMetal catalyst to cut palladium by 25%, yet validation for 150,000 km durability is ongoing. Converter theft added USD 1.5 billion in U.S. insurance claims, prompting VIN etching laws in 16 states that add USD 10 per vehicle in compliance cost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Sensors Outpace Manifolds Amid Regulatory Complexity

Exhaust manifolds generated the largest revenue slice at 38.3% in 2024, reflecting their integration with close-coupled catalysts and high-temperature alloy adoption. Sensors, however, are forecast to grow at 8.8% CAGR through 2030 as Euro 7 and China VI-b mandate continuous monitoring, lifting average sensor count to six per light vehicle and up to ten per heavy truck.

Rising sensor density favors suppliers with algorithm expertise, while manifold suppliers differentiate via nickel-alloy welding and laser-cutting capacity. Selective catalytic reduction modules are likewise expanding in heavy-duty and industrial niches, though their growth lags sensors. Mufflers and EGR valves have become cost-focused commodities with limited margin upside.

By Material: Titanium Expands on Lightweighting Pressure

Stainless steel retained 44.9% revenue share in 2024 thanks to its cost-performance balance, yet titanium is projected to clock 10.2% CAGR on super-sport motorcycle and premium car demand, delivering 45% mass reduction relative to stainless steel.

Nickel alloys, capturing 6% share, serve integrated manifold-catalyst units that face 1,050 °C exhaust gas. Composite ceramics, silicon-carbide particulate filters, are pushing into marine and industrial turbines, aided by superior thermal shock resistance. Mild steel endures in entry-price cars, but its share declines as coated stainless steel becomes mainstream.

By Fuel Type: Natural Gas Gains Momentum

Gasoline accounted for 65.2% of 2024 revenue, anchoring three-way catalyst demand. Natural-gas exhaust systems, forecast at a 7.5% CAGR, benefit from municipal bus conversions and industrial combined-heat-and-power installations that need stainless-steel systems resistant to acidic condensate. Diesel remains vital in heavy trucks and off-highway equipment despite shrinking passenger-car relevance; stringent NOx caps keep SCR modules essential.

By End-User: Automotive Leads, Industrial Retrofits Climb

Automotive captured 92.7% revenue in 2024 and still expands at a 4.6% CAGR as hybrids dominate powertrain mixes. Industrial users, power generation, oil and gas, and data centers are installing SCR retrofits to meet sub-25 ppm NOx limits, slowly increasing their slice of the exhaust systems market.

Passenger cars shift to close-coupled catalysts, commercial vehicles roll out ammonia-slip sensors, while off-highway machinery drives retrofit volume. Data-center diesel generators, constrained by local permits, add another long-tail demand layer through 2030.

Geography Analysis

Asia Pacific, at 48.4% share in 2024, remains the exhaust systems market’s growth engine with a 6.9% CAGR outlook to 2030, propelled by China’s 26.1 million-unit vehicle production rebound and India’s planned Bharat Stage VII rollout. OEMs in the region are expanding SCR capacity and localizing sensor supply to hedge tariff risks. Japan and South Korea emphasize hybrid powertrains and hydrogen combustion prototypes, diversifying catalyst formulation R&D.

Europe is buoyed by aftermarket demand and pre-Euro 7 engineering activity, even as BEV share touched 22% in 2024. OEMs invested EUR 2.8 billion in exhaust R&D to meet cold-start limits, and the region’s 32 million ICE vehicle parc keeps catalyst replacement demand healthy. Nordic markets approach full BEV penetration, yet legacy fleet inspection regimes sustain modest exhaust replacement revenue.

In North America, the United States dominates light-vehicle sales at 15.5 million units, and gasoline powertrains are still at a 76% share. California’s future ZEV mandate accelerates BEV growth but does not erode the replacement market for the incumbent 14.8 million ICE fleet. Heavy-duty diesel adoption of advanced SCR systems remains robust ahead of the 2027 EPA rule. South America and the Middle East & Africa, together at 7.6%, are catching up via Euro 4–5 equivalents, creating lift for three-way catalysts and SCR modules in previously unregulated segments.

Competitive Landscape

Tier-one integrators FORVIA Faurecia, Tenneco, and Eberspächer jointly secure roughly 45% of OEM exhaust module revenue, leveraging scale in stainless-steel forming and automated welding. Cost pressure from precious-metal volatility remains acute, prompting a mix of forward-hedging and palladium-thrifting catalyst designs. Catalyst specialists Johnson Matthey and BASF compete on washcoat chemistry; Johnson Matthey’s platinum-palladium-ceria tri-layer patent underscores a pivot toward IP-heavy differentiation.

Sensor suppliers Bosch, Continental, and NGK grow in influence by embedding diagnostics that control urea dosing and catalyst regeneration, effectively co-owning emission compliance. Aftermarket players Bosal, Walker, and Sango exploit faster delivery cycles but struggle to fund sensor-software R&D.

Industrial exhaust retrofits open a white-space arena where stationary-source NOx limits converge with automotive thresholds; Cummins Emission Solutions’ USD 420 million Indian Railways SCR award typifies the opportunity. Smaller regional companies like Sejong and Katcon win cost-sensitive programs but remain exposed to rhodium price swings due to limited hedging capacity.

Exhaust System Industry Leaders

Tenneco Inc.

Eberspächer Group

FORVIA Faurecia

Benteler International

Bosal

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Tata Motors and Hindustan Petroleum Corporation introduced co-branded “Genuine DEF” diesel exhaust fluid across 23,000 HPCL stations and 2,000 Tata Motors outlets.

- October 2024: Flowmaster launched the Signature Series premium truck exhaust line for major light-pickup models.

- April 2024: FORVIA divested Hug Engineering, a high-power depollution specialist, for EUR 55 million.

- March 2024: At Hy-Fcell 2024, Purem by Eberspächer showcased its innovative solutions tailored for hydrogen and fuel-cell vehicles. These included modular exhaust-air systems, silencers, and Balance-of-Plant components, emphasizing advancements in exhaust technology for enhanced fuel-cell water management and noise control.

Global Exhaust System Market Report Scope

Exhaust systems play a crucial role in collecting, treating, and safely releasing by-products from combustion and industrial processes. They effectively remove gases, minimize harmful emissions, dampen noise, and ensure safe operating conditions for engines and industrial equipment.

The exhaust systems market is segmented by component, material, fuel type, end-user, and geography. By component, the market is segmented into mufflers, catalytic converters, particulate filters, SCR systems, EGR systems, exhaust manifolds, sensors, and others. By material, the market is segmented into stainless steel, mild steel, titanium, nickel alloys, and composite and ceramic materials. By fuel type, the market is segmented into gasoline, diesel, natural gas, and others. By end-user, the market is segmented into automotive and industrial. The report also covers the market size and forecasts for the exhaust systems market across major countries across major regions. For each segment, the market sizing and forecasts have been done based on value (USD).

| Mufflers |

| Catalytic Converters |

| Particulate Filters |

| Selective Catalytic Reduction (SCR) Systems |

| Exhaust Gas Recirculation (EGR) Systems |

| Exhaust Manifolds |

| Sensors |

| Others (Combination and Control Modules) |

| Stainless Steel |

| Mild Steel |

| Titanium |

| Nickel Alloys |

| Composite and Ceramic Materials |

| Gasoline |

| Diesel |

| Natural Gas |

| Others |

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Off-Road and Agricultural Equipment | |

| Marine | |

| Railways | |

| Aviation | |

| Industrial | Power Generation (incl CHP systems) |

| Oil and Gas | |

| Industrial Facilities | |

| Commercial Facilities (Hospitals, Datacenters, etc.) | |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Component | Mufflers | |

| Catalytic Converters | ||

| Particulate Filters | ||

| Selective Catalytic Reduction (SCR) Systems | ||

| Exhaust Gas Recirculation (EGR) Systems | ||

| Exhaust Manifolds | ||

| Sensors | ||

| Others (Combination and Control Modules) | ||

| By Material | Stainless Steel | |

| Mild Steel | ||

| Titanium | ||

| Nickel Alloys | ||

| Composite and Ceramic Materials | ||

| By Fuel Type | Gasoline | |

| Diesel | ||

| Natural Gas | ||

| Others | ||

| By End-User | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Off-Road and Agricultural Equipment | ||

| Marine | ||

| Railways | ||

| Aviation | ||

| Industrial | Power Generation (incl CHP systems) | |

| Oil and Gas | ||

| Industrial Facilities | ||

| Commercial Facilities (Hospitals, Datacenters, etc.) | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the exhaust systems market today?

The exhaust systems market size stood at USD 52.94 billion in 2025 and is forecast to reach USD 66.20 billion by 2030 at a 4.57% CAGR.

Which component is growing fastest?

Sensors lead growth at an 8.8% CAGR through 2030 because Euro 7 and China VI-b require continuous emissions monitoring.

Why is Asia Pacific the key region?

The region hosts 48.4% of revenue owing to China’s production rebound and India’s upcoming Bharat Stage VII, together driving new installations and retrofits.

How are suppliers coping with precious-metal volatility?

Integrators hedge forward contracts while catalyst firms deploy tri-layer washcoats that lower palladium content by up to 25%.

What impact will BEVs have on exhaust demand?

Rising BEV penetration removes roughly USD 400 of exhaust content per car, trimming the ICE parc and pushing suppliers to diversify into fuel-cell and thermal-management hardware.

Page last updated on: