GPU Cold Plate Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

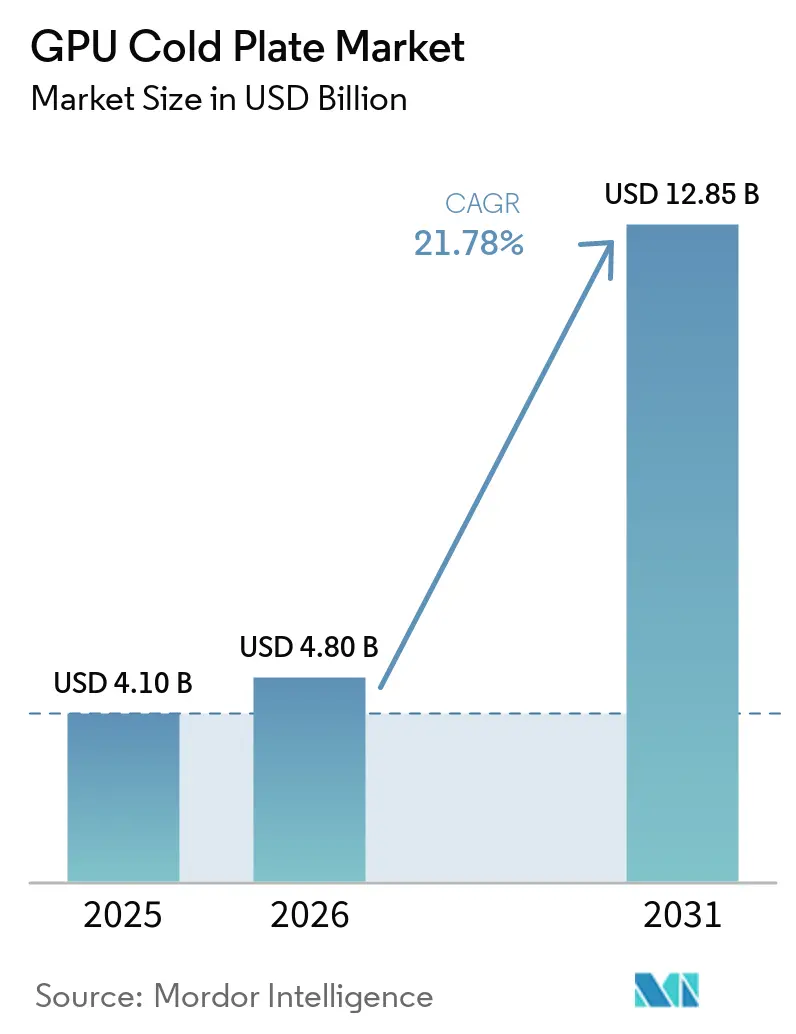

| Market Size (2026) | USD 4.80 Billion |

| Market Size (2031) | USD 12.85 Billion |

| Growth Rate (2026 - 2031) | 21.78% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GPU Cold Plate Market Analysis by Mordor Intelligence

The GPU cold plate market size is expected to increase from USD 4.1 billion in 2025 to USD 4.8 billion in 2026 and reach USD 12.85 billion by 2031, growing at a CAGR of 21.78% over 2026-2031. The growth trajectory reflects three reinforcing forces: soaring GPU power envelopes that already average 700 watts per device, hyperscale operators racing to push power usage effectiveness below 1.2, and the mounting realization that air-cooling throttles AI workload performance. Direct-to-chip liquid cooling improves rack energy efficiency by up to 40%, allowing datacenter operators to reclaim megawatts for revenue-generating compute. Standardization by open-hardware bodies has lowered switching costs, while government incentives have shortened payback periods to under 3 years for facilities with utilization above 60%. Collectively, these dynamics set a robust demand floor that will keep the GPU cold plate market on a double-digit expansion path through the forecast horizon.

Key Report Takeaways

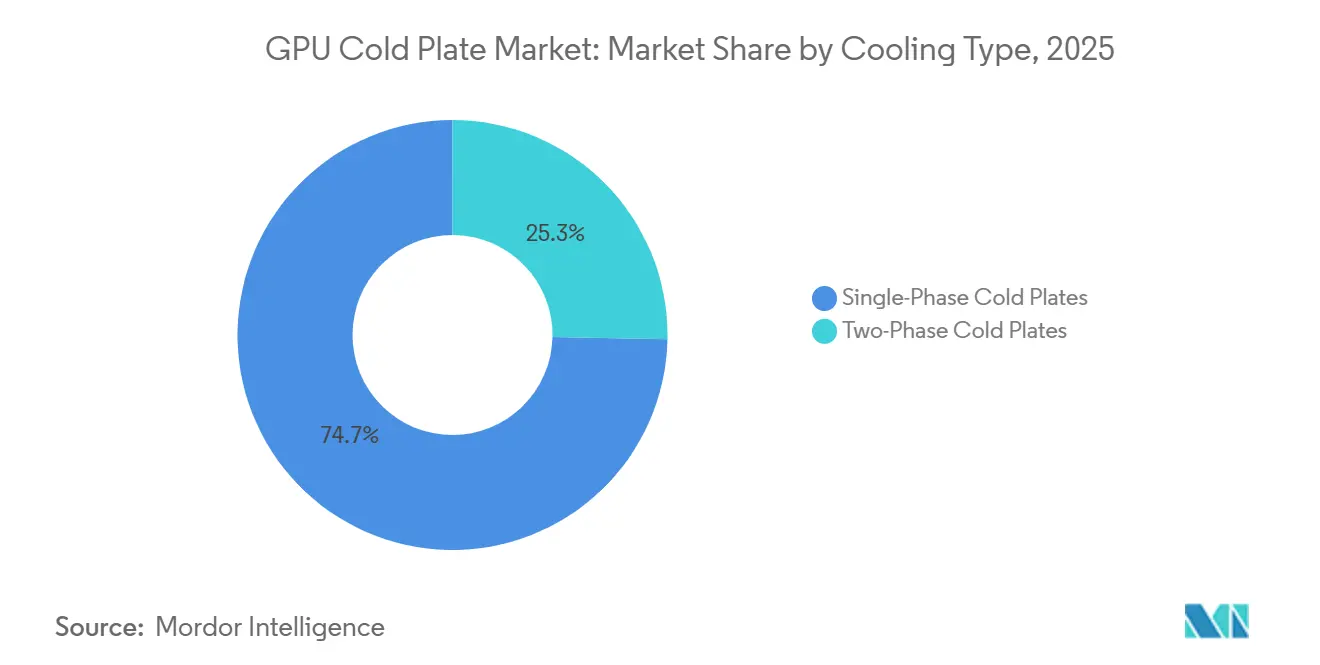

- By cooling type, single-phase technology commanded 74.69% revenue share in 2025, while two-phase systems are projected to expand at a 21.98% CAGR through 2031.

- By design, microchannel architectures captured 63.56% of the GPU cold plate market share in 2025, whereas jet impingement is poised to rise at a 22.38% CAGR.

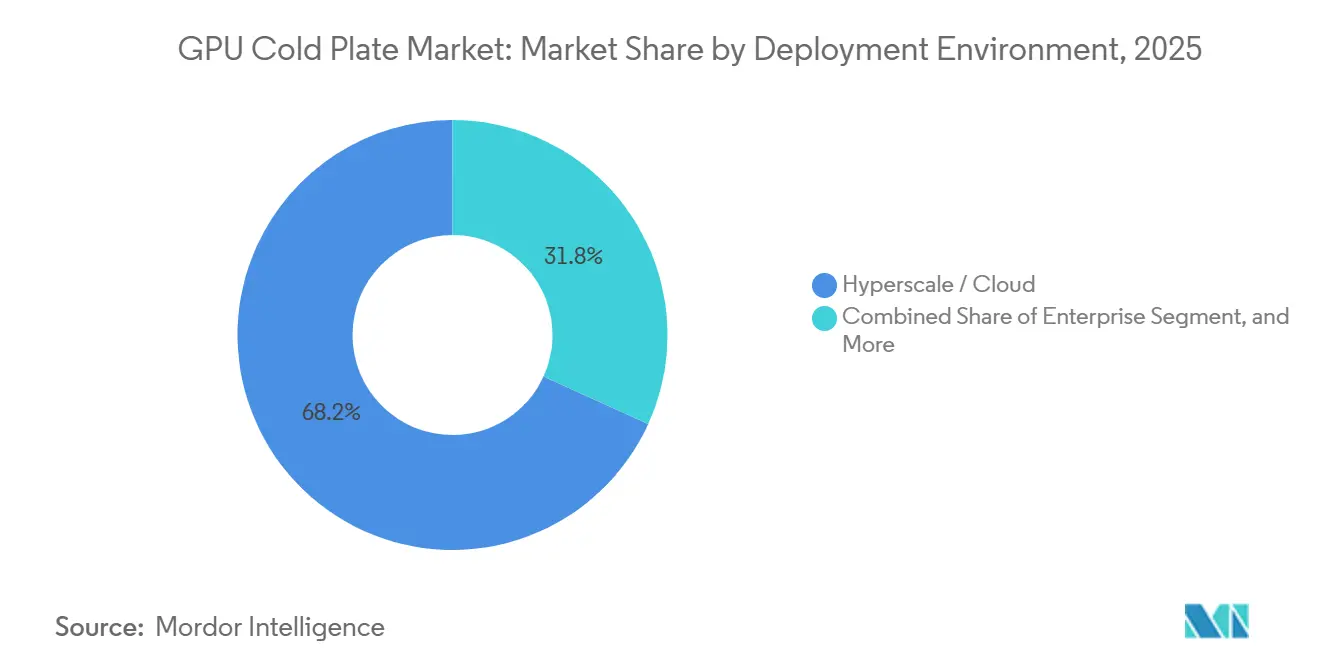

- By deployment environment, hyperscale and cloud operators led with 68.21% of 2025 revenue, and enterprise installations are advancing at a 22.58% CAGR through 2031.

- By GPU power density, the 300-watt-to-700-watt band accounted for 52.74% of the GPU cold plate market size in 2025, yet the above-700-watt segment is moving ahead at a 22.43% CAGR.

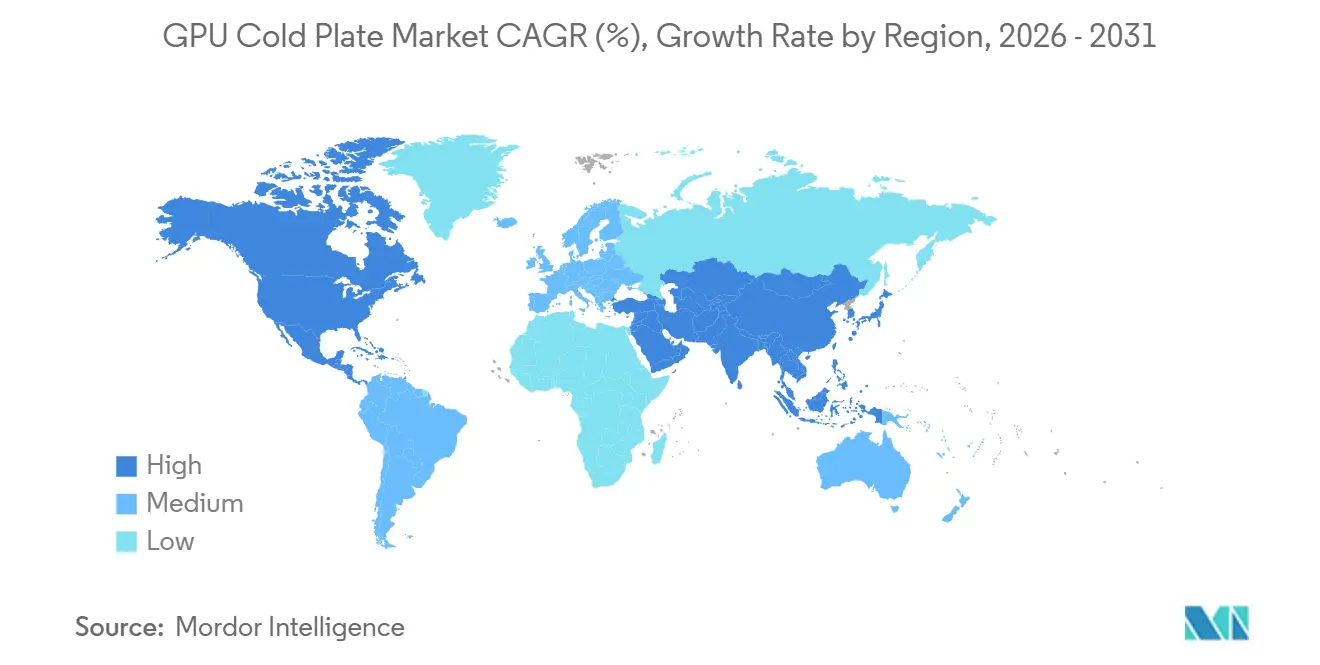

- By geography, Asia-Pacific controlled 68.53% of 2025 revenue and is forecast to grow at 22.78% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global GPU Cold Plate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Adoption of Liquid Cooling in Hyperscale Data Centers | +6.2% | Global, with concentration in North America and Asia-Pacific | Short term (≤ 2 years) |

| Rising GPU Power Densities Surpassing Air Cooling Limits | +5.8% | Global | Short term (≤ 2 years) |

| Government Incentives for Energy-Efficient Data Center Infrastructure | +3.4% | North America, Europe, Singapore | Medium term (2-4 years) |

| Increasing AI Model Complexity Demanding Higher Thermal Management Performance | +3.1% | Global, led by North America and China | Medium term (2-4 years) |

| Emergence of Open-Hardware Cold Plate Standards Reducing Vendor Lock-In | +1.9% | Global, strongest in hyperscale segment | Medium term (2-4 years) |

| Advancements in Low-Fluorinated Dielectric Fluids Enabling Two-Phase Cold Plates | +1.4% | Global, early adoption in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Adoption of Liquid Cooling in Hyperscale Data Centers

Hyperscale providers added more than 200 megawatts of liquid-cooled GPU capacity during 2025, a fivefold jump from 2023 deployments, as air cooling became economically untenable once rack loads exceeded 80 kilowatts. Microsoft’s Fairwater campus validated a 40% energy-savings metric, turning capital expenditure into immediate operating profit. Meta’s mandate that every forthcoming AI cluster ship with liquid cooling set a de facto industry baseline that pushed suppliers to scale production. Higher GPU utilization reinforces the business case because liquid-cooled accelerators sustain boost clocks for longer duty cycles, directly raising training throughput. These factors combine to accelerate order volumes that, in turn, compress per-unit costs for cold plates.

Rising GPU Power Densities Surpassing Air Cooling Limits

NVIDIA H200 and AMD MI300A chips hit 760 watts in 2025, surpassing air cooling’s practical ceiling without resorting to deafening fan speeds. Air’s poor thermal conductivity caps heat-flux removal near 0.5 W cm-², while water-based plates deliver 5 W cm-² or higher, eliminating performance throttling even in 25 °C ambient conditions. Field data show that air-cooled clusters throttled during 18% of training epochs when temperatures rose past 27 °C. Cold plates remove that variability, ensuring operators extract the full value from capital-intensive accelerators, especially in tropical data center hubs such as Singapore.

Government Incentives for Energy-Efficient Infrastructure

Regulators now attach financial carrots and sticks to data center thermal performance. The European Union’s updated Energy Efficiency Directive mandates a sub-1.4 PUE target for new facilities above 500 kilowatts, effectively outlawing pure air-cooling for GPU racks.[1]European Commission, “Energy Efficiency Directive 2024 Revision,” ec.europa.euSingapore’s Green Plan 2030 grants accelerated depreciation for sub-1.3 PUE campuses, and the United States Department of Energy offers USD 45 million in matching grants for liquid-cooling retrofits. Such policies shorten the payback window for cold-plate projects, tipping investment decisions toward liquid solutions, particularly for enterprise buyers with limited balance-sheet flexibility.

Increasing AI Model Complexity Requiring Higher Thermal Performance

Training runs now extend over weeks for trillion-parameter language models, demanding rock-stable thermal environments. Liquid-cooled clusters maintain junction temperature within a 3 °C band, compared with a 9 °C spread for air-cooled equivalents, improving convergence rates and slashing idle synchronization delayS. Inference workloads converge on low-latency extremes that need GPUs to ramp from idle to full load in seconds, a transient profile that liquid cooling handles with minimal temperature overshoot. These performance benefits translate into measurable revenue gains for latency-sensitive use cases such as high-frequency trading and autonomous perception.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost of Liquid Cooling Deployment | -2.8% | Global, most acute in enterprise and edge segments | Short term (≤ 2 years) |

| Compatibility Challenges with Existing Rack Infrastructures | -1.9% | North America and Europe, legacy facilities | Short term (≤ 2 years) |

| Limited Field Expertise for Operational Maintenance of Two-Phase Systems | -1.2% | Global, excluding hyperscale operators | Medium term (2-4 years) |

| Supply Chain Constraints for High-Precision Microchannel Machining | -0.9% | Global, concentrated in Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Liquid Cooling Deployment

A 10-rack GPU cluster retrofitted with single-phase cold plates requires roughly USD 400,000 in capital, triple the outlay for a comparable air-cooled install. Two-phase systems cost even more because they add refrigerant pumps, heat exchangers, and certified piping.[2]Schneider Electric, “EcoStruxure and Edge AI Cooling Solutions,” se.com Colocation environments add customer isolation and metering hardware, which inflates rack costs by an additional USD 15,000-25,000. Payback drops below three years only where electricity rates top USD 0.10 kWh-¹, leaving many low-tariff regions unmoved. Staff training, often absent in enterprise IT budgets, further inflates life-cycle expense through mandatory vendor service contracts.

Compatibility Challenges with Existing Rack Infrastructures

Legacy facilities built for 10-20 kilowatt racks lack chilled-water loops, leak-detection systems, and floor loading to support coolant distribution units. Retrofitting consumes 40-50% of total project budgets and can trigger fire-protection upgrades under NFPA 75 that add USD 8,000-12,000 per rack. Clearance constraints prevent quick-disconnect couplings from fitting into crowded cages, forcing operators to remove adjacent equipment during installation, thereby lengthening downtime windows. Monitoring software from the 2010s seldom integrates with modern coolant distribution units, compelling parallel instrumentation and raising operational complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cooling Type: Performance-Driven Shift Toward Two-Phase Designs

Single-phase systems accounted for 74.69% of 2025 revenue, driven by their plug-and-play fit with chilled-water loops and the modest operational skills required. In the core 300-watt-to-700-watt band, single-phase plates satisfy thermal loads at 2-4 L min-¹ flow while keeping pump power manageable. Two-phase systems, although at only 25.31% share, are scaling at 21.98% because they dissipate over 200 W cm-², unlocking next-generation GPU envelopes above 1,000 watts. Hyperscale operators piloting these designs report 60% reductions in cooling energy use and the ability to dump heat directly into dry coolers, eliminating chiller plants and freeing real estate for revenue-generating racks.

Hybrid architectures that blend single-phase primary loops with two-phase hotspot modules are emerging as a pragmatic bridge. Products such as Parker-Hannifin’s HyperCool pair water-glycol circuits for bulk removal with embedded heat pipes that vaporize refrigerant at localized peaks, delivering 150 W cm-² without site-wide refrigerant handling. As two-phase expertise diffuses and low-GWP fluids mature, the GPU cold plate market is likely to witness gradual share transfer toward full two-phase plates, especially for racks exceeding 100 kilowatts, where traditional water loops hit flow-rate ceilings.

By Design Type: Jet Impingement Gains Momentum Over Microchannel

Microchannel plates retained 63.56% share in 2025 because CNC machining is mature, cost-effective, and backed by a decade of server OEM validation. However, physics impose a fourth-power rise in pressure drop as channel width narrows, capping scalability for 800-watt GPUs. Jet impingement designs circumvent this by firing high-velocity coolant jets perpendicularly onto the die, achieving above 300 W cm-² while using 30% less pumping power than equivalent microchannel solutions.[3]JetCool Technologies, “Jet Impingement Cooling for HPC,” jetcool.com

Manufacturing constraints kept jet impingement costly, yet automated laser drilling and 3D-printed nozzle arrays are closing the gap. As vendors reach cost parity by 2028, Boyu Liquid Cooling targets jet impingement to dominate the above-700-watt niche. Meanwhile, hybrid plates combining microchannel base layers with vapor chambers or nozzle inserts address workloads where cost sensitivity and hotspot intensity coexist, such as financial trading clusters demanding both reliability and extreme transient performance.

By Deployment Environment: Enterprise Uptake Accelerates

Hyperscale and cloud operators accounted for 68.21% of 2025 revenue, leveraging economies of scale to reduce per-unit costs by 30-40% and integrating liquid cooling into new campus blueprints. Meta’s vertical integration trimmed lead times from 16 weeks to 8 weeks and illustrates how supply-chain leverage reshapes vendor economics. The enterprise segment, though smaller, is expanding at 22.58% as financial services, healthcare, and advanced manufacturing deploy on-premises inference clusters to meet data-sovereignty rules and avoid cloud egress fees.

Government and academic HPC centers add steady demand at modest growth rates because tender cycles align with national budgets. Edge AI, currently accounting for less than 5% of revenue, shows technical promise but remains constrained by the need for self-contained cooling modules that operate without chilled-water feeds from the building. Vendors positioning modular, thermoelectric-assisted cold plates see this space as a green-field upsell once edge inference workloads consolidate enough GPUs per site.

By GPU Power Density: Above-700-Watt Tier Sets Innovation Pace

The 300-watt-to-700-watt category delivered 52.74% of installations in 2025, mirroring the installed base of A100 and H100 accelerators. Cost-optimized copper microchannel plates dominate here, hitting 120 W cm-² at tolerable flow rates. The above-700-watt segment, though smaller, is climbing at 22.43% as vendors roll out H200, MI300, and future B100 GPUs. These devices require either two-phase plates or single-phase solutions operating at 6-8 L min-¹, which, in turn, increase pump power and manifold diameter.

Cold-plate manufacturers are rationalizing portfolios around 400 W, 700 W, and 1,000 W SKUs to minimize tooling complexity. New thermal-interface materials such as graphene-enhanced pads with 15 W m-¹ K-¹ conductivity shave 4-6 °C off the die-to-plate delta, extending boost clock headroom. Vendors that master both high-conductivity pads and low-restriction plates stand to capture disproportionate value as the GPU cold plate market standardizes around 1-kilowatt thermal envelopes.

Geography Analysis

Asia-Pacific led the GPU cold plate market with 68.53% revenue in 2025 and is forecast to grow at 22.78% through 2031. China’s Ministry of Industry and Information Technology earmarked CNY 50 billion (USD 7 billion) for liquid-ready AI infrastructure, driving massive orders such as Alibaba Cloud’s 100,000-GPU Ulanqab campus.[4]Ministry of Industry and Information Technology, “Data Center Modernization Funding 2024,” miit.gov.cn Singapore enforces a 1.3 PUE ceiling that virtually mandates liquid cooling; Digital Realty’s USD 1.26 billion Jurong campus showcased seawater heat rejection to sidestep chiller loads. India is fast-tracking hyperscale builds, and local manufacturers like Schneider Electric’s Bangalore plant will produce 50,000 plates annually by year-end 2026, cutting import dependence.

North America contributed roughly 18% of 2025 revenue, anchored by hyperscale campuses in Wisconsin, Oregon, and Virginia. U.S. federal and state incentives shorten enterprise payback periods, and in cold-climate regions, liquid cooling is still adopted for GPU racks because ambient free cooling alone cannot handle 700-watt chips during summer peaks. Canada’s operators find that liquid cooling lets them consolidate servers, offsetting months of free-air advantage with higher annual compute density.

Europe clocked about 10% of revenue, with the Energy Efficiency Directive placing a regulatory gun to operators’ heads. Germany’s Hetzner achieved 1.25 PUE in Falkenstein and secured accelerated depreciation, while the United Kingdom earmarked GBP 200 million (USD 255 million) for university clusters that default to liquid cooling. South America and the Middle East and Africa together contributed under 4% yet display strategic importance. Brazil’s São Paulo campus leverages hydroelectric grids for low-carbon marketing, and the Emirates’ AI71 project builds two-phase immersion rigs to cope with 45 °C summers, aiming to claim a 5% global share by 2031 if water-scarcity challenges are mitigated

Competitive Landscape

The GPU cold plate market remained moderately consolidated in 2025, with the top five suppliers accounting for close to 50% of combined revenue. Asetek and CoolIT Systems maintained their dominance in the single-phase mainstream segment by securing OEM bundling agreements with major players such as Dell and HPE. These companies leveraged their patent coverage for quick-disconnect technologies to strengthen their market position.[5]Asetek A/S, “Liquid Cooling Patent Portfolio,” asetek.com Meanwhile, LiquidStack, a leader in two-phase immersion cooling, outpaced traditional designs and secured high-margin deployments in key regions, including Singapore and Texas. Schneider Electric and Rittal differentiated themselves by integrating software-defined cooling solutions into their offerings, enabling real-time optimization of pump and chiller setpoints and adding significant value to their products.

In 2024, the finalization of standardization efforts by the Open Compute Project reduced switching costs, leading to increased price competition for single-phase plates. However, this development simultaneously enhanced the strategic importance of custom two-phase and hybrid solutions. Emerging disruptors like Nidec began experimenting with 3D-printed titanium plates, significantly reducing lead times to just 3 weeks for complex geometries previously impossible to machine. Additionally, Alfa Laval utilized its expertise in marine heat exchangers to offer competitive pricing, undercutting incumbents by 15-20% on large orders exceeding 10,000 units. These advancements highlighted the growing importance of innovation and cost efficiency in the market.

As GPU vendors considered backward integration, NVIDIA's patent filings revealed bracket designs that could directly integrate with their boards, signaling a potential shift in the competitive landscape. The focus of competition is expected to move toward advanced materials, additive manufacturing techniques, and integrated telemetry systems that feed data into facility-level automation processes. These developments underscore the evolving dynamics of the GPU cold plate market, where companies are increasingly prioritizing technological advancements and operational efficiency to gain a competitive edge.

GPU Cold Plate Industry Leaders

CoolIT Systems, Inc.

Asetek A/S

JetCool Technologies, Inc.

Laird Thermal Systems Inc.

BOYD Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Schneider Electric announced a USD 150 million expansion of its Bangalore liquid-cooling plant, boosting annual capacity to 50,000 cold-plate units.

- March 2026: LiquidStack partnered with Equinix to roll out two-phase immersion across 15 megawatts of GPU load in Silicon Valley, with pilot plates for 1,000-watt chips due in Q3 2026.

- February 2026: Asetek secured a USD 75 million contract to supply single-phase plates for a 200-megawatt data center expansion in Virginia, its largest order to date.

- January 2026: Danfoss unveiled DCX series plates featuring embedded flow sensors that predict maintenance events, priced 25% above commodity units.

Global GPU Cold Plate Market Report Scope

The GPU Cold Plate Market is the global industry focused on the development, manufacturing, and deployment of liquid-cooling components specifically designed to manage the thermal output of high-performance graphics processing units (GPUs). Cold plates are critical components in direct-to-chip cooling systems, enabling efficient heat transfer from GPUs to circulating coolant and supporting higher power densities, improved performance, and energy-efficient operation in modern computing environments.

The GPU Cold Plate Market Report is Segmented by Cooling Type (Single-Phase, and Two-Phase), Design Type (Microchannel, Jet Impingement, and Hybrid/Advanced), Deployment Environment (Hyperscale/Cloud, Enterprise, Government and Research HPC, and Edge AI), GPU Power Density (Below 300W, 300W-700W, and Above 700W), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Single-Phase Cold Plates |

| Two-Phase Cold Plates |

| Microchannel Cold Plates |

| Jet Impingement Cold Plates |

| Hybrid / Advanced Designs |

| Hyperscale / Cloud |

| Enterprise |

| Government and Research (HPC) |

| Edge AI |

| Below 300W |

| 300W-700W |

| Above 700W |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Rest of South America | |

| Middle East and Africa |

| By Cooling Type | Single-Phase Cold Plates | |

| Two-Phase Cold Plates | ||

| By Design Type | Microchannel Cold Plates | |

| Jet Impingement Cold Plates | ||

| Hybrid / Advanced Designs | ||

| By Deployment Environment | Hyperscale / Cloud | |

| Enterprise | ||

| Government and Research (HPC) | ||

| Edge AI | ||

| By GPU Power Density | Below 300W | |

| 300W-700W | ||

| Above 700W | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current GPU cold plate market size and how fast is it growing?

The GPU cold plate market size stood at USD 4.8 billion in 2026 and is projected to reach USD 12.85 billion by 2031, expanding at a 21.78% CAGR.

Which cooling technology is gaining the fastest traction?

Two-phase cold plates, while smaller today, are forecast to grow at a 21.98% CAGR through 2031 because they handle heat flux beyond 200 W cm-² that next-generation 1,000-watt GPUs demand.

Why are hyperscale operators switching from air to liquid cooling?

Liquid cooling cuts rack energy use by up to 40%, eliminates thermal throttling, and helps datacenters achieve regulatory power-usage-effectiveness targets below 1.3.

Which region contributes the most to GPU cold plate demand?

Asia-Pacific leads with 68.53% of global revenue thanks to large-scale AI infrastructure investments in China, Singapore, and India.

What design trend is challenging traditional microchannel plates?

Jet impingement architectures are gaining share because they deliver 300 W cm-² cooling at lower pumping power, positioning them as the preferred option for GPUs above 700 watts.

How fragmented is supplier competition?

The top five vendors hold just under 50% of revenue, giving the market a concentration score of 6 and leaving significant opportunity for emerging specialists and regional players.

Page last updated on: