Automotive Dashboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

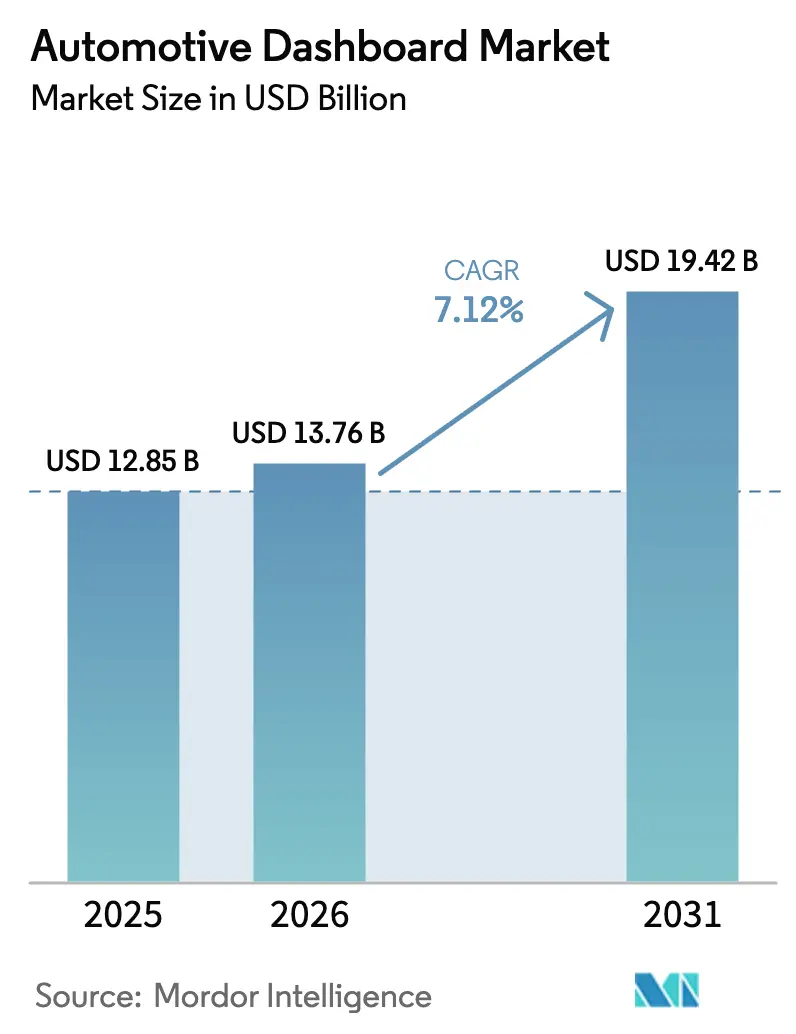

| Market Size (2026) | USD 13.76 Billion |

| Market Size (2031) | USD 19.42 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

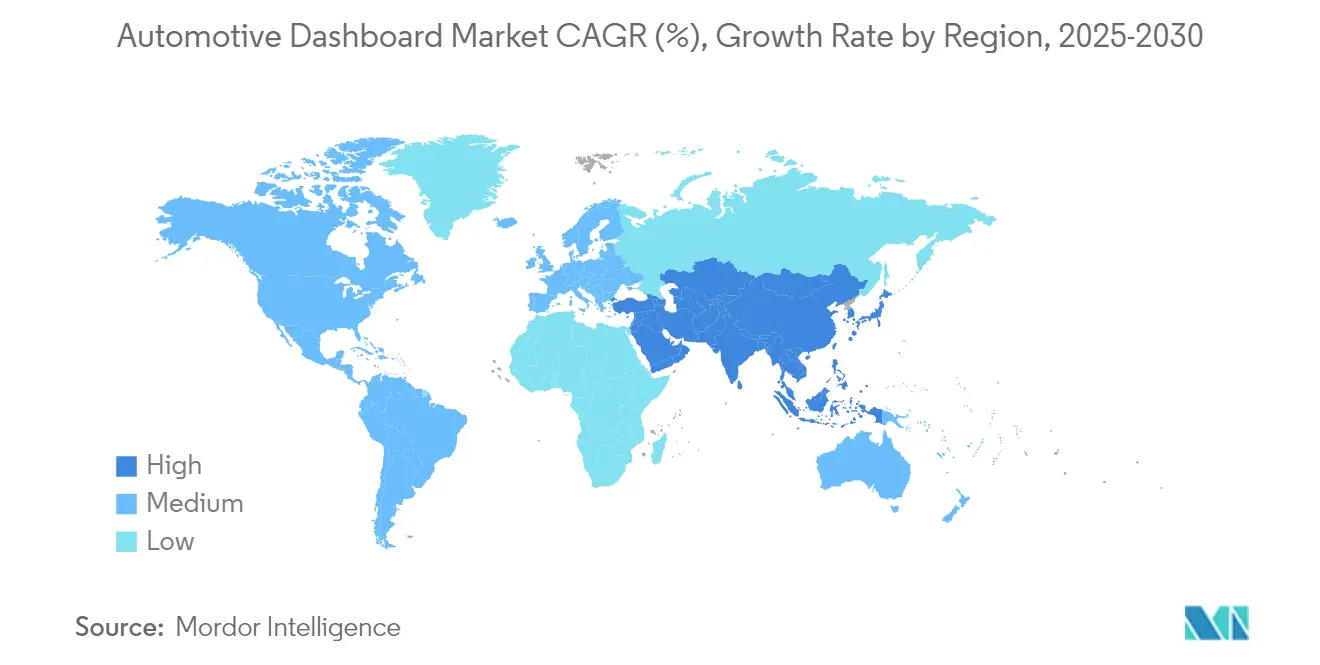

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Dashboard Market Analysis by Mordor Intelligence

The automotive dashboard market size is expected to grow from USD 12.85 billion in 2025 to USD 13.76 billion in 2026 and is forecast to reach USD 19.42 billion by 2031 at 7.12% CAGR over 2026-2031. Strong momentum comes from the shift toward fully digital cockpits, tighter global safety requirements for display readability, and rising electric-vehicle volumes that favor software-defined interiors. Original-equipment manufacturers (OEMs) are replacing analog clusters with configurable screens built on domain-controller architectures that cut electronic control unit counts and wiring complexity. Asia-Pacific continues to anchor production scale thanks to Chinese display-panel capacity and an expansive local EV supply chain. Meanwhile, hybrid dual-mode dashboards that blend physical controls with touch displays are gaining traction as OEMs prepare for European mandates that require tactile access to critical functions.

Key Report Takeaways

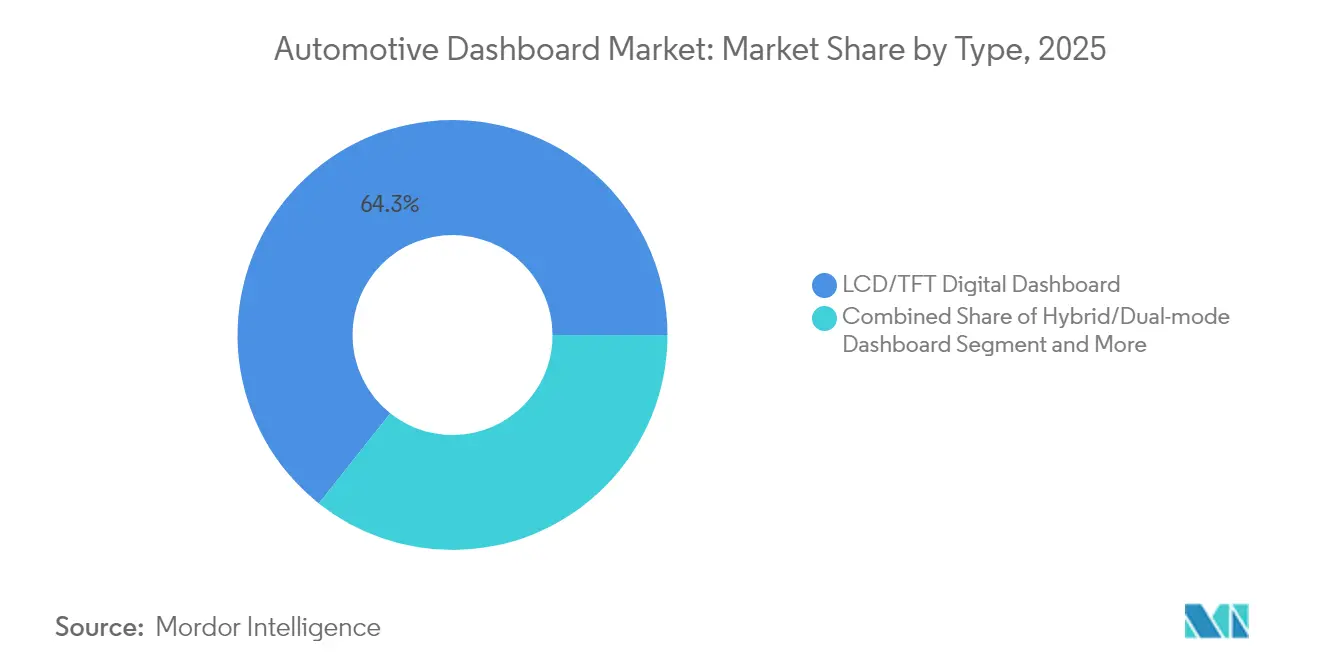

- By type, LCD/TFT digital dashboards led with 64.32% revenue share in 2025; the hybrid dual-mode segment records the fastest growth at a 8.67% CAGR to 2031.

- By vehicle type, passenger cars captured 75.58% of the automotive dashboard market share in 2025 while expanding at an 8.03% CAGR through 2031.

- By sales channel, OEM installations held 87.95% of 2025 revenue; the aftermarket is projected to grow 9.20% annually to 2031.

- By component, display panels accounted for 45.88% share of the automotive dashboard market size in 2025; control electronics and system-on-chip modules post the quickest rise at an 7.78% CAGR.

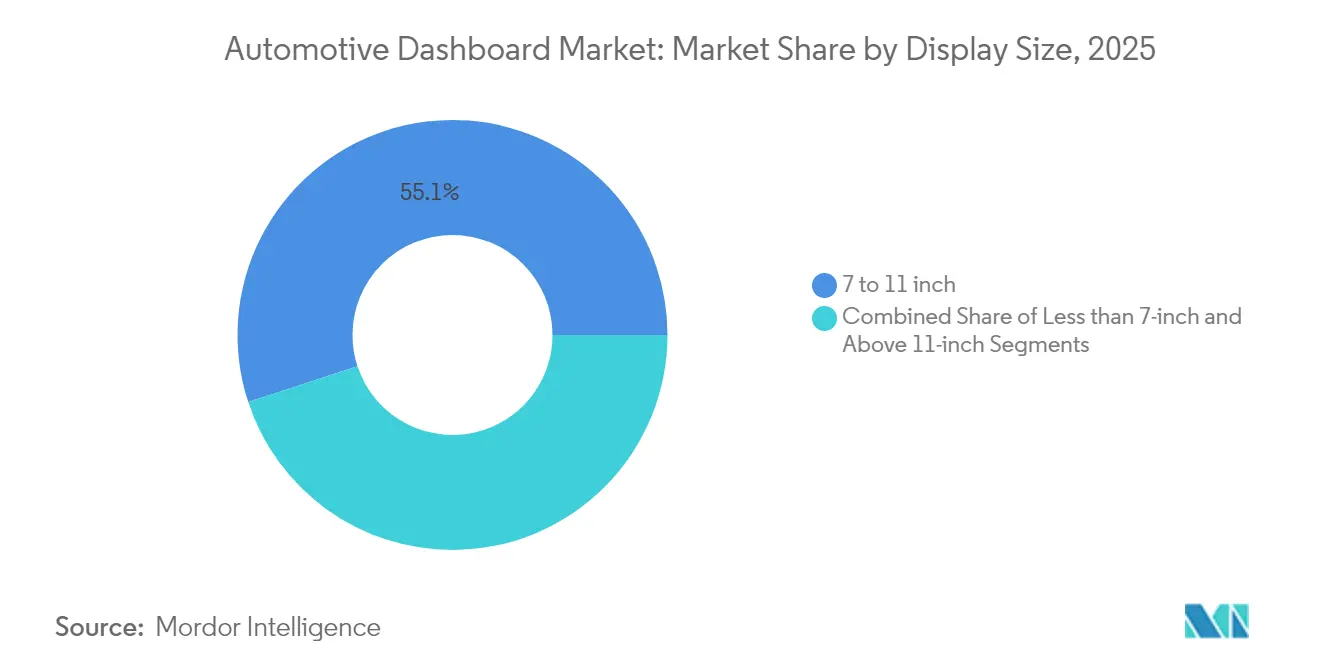

- By display size, 7-11 inch screens commanded 55.05% share in 2025, whereas panels larger than 11 inches will expand at an 8.46% CAGR.

- By technology, LCD dashboards held 66.41% revenue share in 2025; OLED and Mini-LED solutions advance fastest at a 8.98% CAGR through 2031.

- By geography, Asia-Pacific led with 49.10% revenue share in 2025; it also registers the strongest regional CAGR of 9.05% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Dashboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Production Boom & Integrated Cockpits | +2.1% | China, EU, North America | Long term (≥ 4 years) |

| Digital-Instrument-Cluster Adoption | +1.8% | Global, APAC leading | Medium term (2-4 years) |

| Demand for Connected Infotainment & HMI | +1.5% | Global, premium segments first | Medium term (2-4 years) |

| Safety Regulations for Display Readability | +1.2% | North America & EU | Short term (≤ 2 years) |

| Low-cost Domain-controller Architectures | +0.9% | APAC core, global spill-over | Medium term (2-4 years) |

| OTA-monetized Software-Defined Dashboards | +0.7% | North America & EU early adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV Production Boom & Integrated Cockpits

Battery-electric architectures remove mechanical constraints, giving designers freedom to merge clusters, infotainment, and head-up displays into seamless surfaces. Yanfeng’s EVI concept replaces the traditional instrument panel with seat-integrated Smart Cabin modules that showcase the possibilities of a flat EV floor. ECARX shipped 2 million digital cockpit units in 2024, mostly to Chinese EV makers, underscoring the scale effect of electrification.[1]ECARX Holdings, “Annual Report 2024,” ir.ecarxgroup.com

Digital-Instrument-Cluster Adoption

Automakers are rapidly phasing out mechanical gauges in favor of software-configurable instrument clusters that streamline parts counts and enable continuous feature upgrades. BMW’s Panoramic iDrive, slated for all new models from late 2025, eliminates physical dials and supports deep personalization through the BMW Operating System X.[2]BMW Group, “BMW Panoramic iDrive Unveiled at CES 2025,” press.bmwgroup.com Broader acceptance extends into high-volume models as display prices fall, while regulators evaluate distraction risks and may require tactile redundancies for core functions.

Demand for Connected Infotainment & HMI

Customers expect smartphone-grade responsiveness and voice assistance inside the vehicle. Volkswagen’s roll-out of Cerence Chat Pro adds ChatGPT-based conversational AI across European models, enabling natural-language control of climate, navigation, and media. The same connectivity that delights users also invites cyber risks, prompting stricter ISO/SAE 21434 validations before dashboards go live.

Safety Regulations for Display Readability

Display visibility rules such as FMVSS 101 obligate clear labeling and brightness management under all lighting conditions, pushing suppliers to add anti-glare coatings and adaptive luminance control.[3]National Highway Traffic Safety Administration, “FMVSS 101 Controls and Displays,” nhtsa.gov Transport Canada guidance further limits in-drive interactions, spurring the development of displays that lock non-driving tasks when the vehicle is in motion. Compliance capabilities have become a competitive differentiator, especially for global platforms that must satisfy several jurisdictions simultaneously.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor Supply Constraints | -1.8% | Worldwide automotive sector | Short term (≤ 2 years) |

| High Cost of OLED/Mini-LED Panels | -1.4% | Global, premium segments | Medium term (2-4 years) |

| Pending Rules on Display Size/Touch Distraction | -0.9% | EU primary, global spill-over | Short term (≤ 2 years) |

| Cyber-security Certification Delays | -0.6% | Regulated markets worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Semiconductor Supply Constraints

Automotive dashboards rely heavily on mature-node microcontrollers that vie with industrial and IoT applications for foundry slots. Hurricane damage to high-purity quartz mining in North Carolina spotlighted the fragility of upstream materials and pushed lead times into the 40-week range in early 2024. Manufacturers mitigated risk through multi-sourcing and redesigns that tolerate alternative chipsets, yet the episode illustrated how thin inventory buffers can delay new-model launches.

High Cost of OLED/Mini-LED Panels

Bendable OLED dashboards shown by Samsung Display at CES 2025 headline outstanding contrast and design freedom, but remain confined to luxury trims due to elevated bill-of-material costs. Energy-driven glass-substrate price increases of more than 10% in 2024 weigh further on adoption, so many OEMs reserve these panels for halo models while mainstream lines stick with enhanced LCDs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Digital Transformation Accelerates

LCD/TFT clusters dominated 2025 with a 64.32% revenue share of the automotive dashboard market. Demand grows for hybrid dual-mode layouts that integrate rotary knobs or pushbuttons around a primary display, expanding at a 8.67% CAGR as OEMs hedge against upcoming European tactile-control rules.

Hybrid solutions balance cost targets with safety compliance. Suppliers such as Continental now integrate anti-reflection coatings and anti-fog treatments to keep LCDs competitive. Premium nameplates push into full-width curved OLEDs, yet volume models favor hybrids that allow phased upgrades without re-certification.

By Vehicle Type: Passenger Cars Extend Lead

Passenger cars accounted for 75.58% of 2025 revenue, reflecting high production volumes and faster adoption of connected features. This segment is projected to advance at an 8.03% CAGR as owners value personalized interfaces and over-the-air upgrade paths.

Commercial fleets adopt digital dashboards more slowly, although light-duty delivery vans gain from telematics dashboards that automate route and maintenance data. Heavy trucks remain conservative, but electronic logging and safety mandates gradually raise digital cluster penetration.

By Sales Channel: OEM Core with Growing Aftermarket

Factory-installed systems captured 87.95% of the automotive dashboard market in 2025, supported by tight integration with vehicle networks. The aftermarket shows stronger momentum at 9.20% CAGR, driven by owners retrofitting older vehicles with Bluetooth-enabled screens and wireless CarPlay adaptors.

Independent installers face rising complexity due to advanced driver-assistance calibrations, yet growth persists because aging fleets seek connectivity upgrades long before vehicle replacement.

By Component: Processing Power Races Ahead

Display panels represented 45.88% of 2025 revenue, but control electronics and system-on-chip units are the fastest-growing slice at 7.78% CAGR. Next-generation domain controllers bundle CPU, GPU, and AI acceleration to drive multiple displays and manage secure over-the-air updates.

Software stacks and human-machine-interface toolkits generate sticky revenue streams as automakers license voice assistants and app stores. Structural trim and HVAC interfaces evolve into modular assemblies to streamline cabin customization.

By Display Size: Large Screens Gain Ground

Panels between 7 and 11 inches retained a 55.05% share in 2025, prized for cost efficiency and easy integration. Displays exceeding 11 inches are rising fastest at an 8.46% CAGR as consumers welcome tablet-like viewing areas.

Larger screens merge cluster and infotainment zones, though regulators scrutinize driver-distraction metrics. Emerging curved and segmented designs aim to deliver visual breadth while preserving quick-glance readability.

By Technology: LCD Holds, OLED Climbs

LCD technology still leads with a 66.41% share in 2025, underpinned by supply-chain maturity and falling per-unit costs. OLED panels grow at a 8.98% CAGR thanks to high contrast, thin profiles, and flexible geometries that enable wrap-around surfaces.

Micro-LED prototypes promise even higher brightness and longevity, exemplified by AUO’s transparent and rollable dashboards displayed at CES 2025. Mass adoption awaits yield improvements and cost reductions.

Geography Analysis

Asia-Pacific generated 49.10% of global revenue in 2025 and is expected to grow with a 9.05% CAGR to 2031. Chinese OEMs increasingly source dashboards and domain controllers in-house, improving cost leverage. Japan supplies high-reliability infotainment platforms, and South Korean firms secure export contracts that diversify regional production bases.

North America shows steady replacement demand as the light-vehicle parc ages. The United States light-duty aftermarket expanded 5.7% in 2024 to USD 413.7 billion, signaling headroom for retrofit dash upgrades. Connected-service subscription uptake, such as Ford Pro’s telematics plans, underscores recurring-revenue potential.

Europe shapes global design trends through stringent safety assessments. Euro NCAP’s 2026 requirement for physical access to key functions influences cockpit architectures worldwide. Software-defined vehicle strategies promise additional profit streams for regional OEMs, but success hinges on harmonizing cybersecurity and interface standards to offset cost pressure from electrification.

Regulatory Landscape

Automotive dashboards must comply with safety and human-factors requirements that govern control labeling, illumination, and legibility. In the United States, NHTSA enforces FMVSS No. 101 (Controls and Displays), which sets expectations for display identification and visibility and pushes suppliers toward adaptive brightness, anti-glare treatments, and validated tell-tale behavior on digital clusters.

Global platforms also face fast-rising software and cybersecurity compliance burdens tied to software-defined cockpits. UN Regulation No. 155 (Cyber Security Management System) and UN Regulation No. 156 (Software Update Management System) add mandatory process and evidence requirements for type approvals, while ISO 15008:2017 and ISO/TS 8231:2025 provide test-oriented guidance for in-vehicle visual presentation and interior display performance. Trade policy adds another layer of cost and sourcing complexity: the United States applied Section 232 tariffs of 25% on automobiles (effective April 3, 2025) and certain auto parts (effective May 3, 2025), with an import adjustment offset framework that uses MSRP-based offsets (3.75% from April 2025 through April 2026, then 2.5% from May 2026 through April 2027), shaping localization and bill-of-material strategies for dashboard electronics and displays.

Value Chain Analysis

The automotive dashboard value chain starts with upstream inputs such as glass substrates, polarizers and films, backlights, touch sensors, adhesives and optical bonding materials, along with mature-node semiconductors (MCUs, display drivers, GPUs/NPUs, memory) and PCB laminates. Midstream, display makers and electronics manufacturers supply panels and modules to Tier-1 and emerging Tier 0.5 integrators that deliver complete cockpit systems, typically combining the cluster, center display, HMI software, and a cockpit domain controller. These systems are then validated through OEM programs and assembled into vehicles, with service parts and aftermarket support handled through distribution and installer networks.

Recent platform moves show how compute and software dependencies affect sourcing and qualification. Visteon and Qualcomm announced an AI-focused cockpit collaboration in April 2025, while SAIC-GM, Bosch, and Qualcomm disclosed co-development of an AI-powered smart cockpit domain controller in June 2025 for the Buick ELECTRA platform using the QAM8775P. ECARX announced Volkswagen Group awards in March 2025 (global scope) and November 2025 (expansion into additional Latin America models), indicating standardization of cockpit stacks across multi-region nameplates. Qualification remains a major gating factor, with IATF 16949, AEC-Q100/Q200, and PPAP cycles that can run 18-36 months. Bottlenecks persist around mature-node supply, specialty PCB materials, and the cost and timing of multi-jurisdiction safety and cybersecurity validation.

Competitive Landscape

Tier-1 suppliers retain influence by offering complete cockpit suites that blend hardware, middleware, and cloud services. Continental, Bosch, and Visteon secure long-term platform awards that cover clusters, infotainment, and advanced driver-assistance visualization. Visteon recorded USD 934 million net sales in Q1 2025, with USD 1.9 billion of new digital-cockpit business booked.

Strategic alliances are critical. Panasonic Automotive integrates Qualcomm’s Snapdragon Cockpit Elite to add generative-AI features, while also working with Arm on transferable software foundations. Magna collaborates with NVIDIA to embed DRIVE AGX compute into dash modules that support enhanced perception mapping for future autonomy.

Competitive pressure intensifies from Chinese display makers that bundle low-cost panels with proprietary operating systems, and from tech firms that monetize in-car data. Suppliers that demonstrate ISO/SAE 21434 compliance while deploying user-centric features stand to capture premium margins despite pricing headwinds.

Automotive Dashboard Industry Leaders

Continental AG

Forvia SE (Faurecia SE)

DENSO Corporation

Robert Bosch GmbH

Visteon Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A major whitespace area is dashboards that meet tightening safety and usability expectations without rolling back the digital-cockpit experience. Euro NCAP's 2026 requirement for physical access to key functions is already pushing OEMs toward hybrid dual-mode layouts that combine touchscreens with tactile controls. This creates room for suppliers to package knobs, haptics, and clear tell-tales alongside configurable displays while maintaining FMVSS 101 and ISO 15008-aligned readability and glanceability.

UN R155/R156 compliance also raises demand for cockpit platforms with auditable cybersecurity and software-update processes, favoring Tier-1s and software stack partners that can deliver pre-validated building blocks for global programs. Another opportunity involves cockpit compute consolidation and supply-chain resilience. OEMs are moving to domain-controller architectures that reduce ECU count and wiring, and recent industry collaborations point to commercialization: Visteon and Qualcomm (April 2025) and SAIC-GM, Bosch, and Qualcomm (June 2025) both positioned AI-capable cockpit compute as a differentiator, while ECARX's Volkswagen awards (March and November 2025) support multi-model deployment of standardized digital cockpit platforms. On the supply side, localized semiconductor capacity investment can support higher-content dashboards by reducing exposure to electronics shortages; Bosch began sample production at its first US silicon carbide semiconductor plant in Roseville, California, supported by a USD 225 million CHIPS Act subsidy (reported July 2026), signaling broader efforts to harden the electronics supply base that cockpit systems rely on.

Recent Industry Developments

- May 2026: Forvia SE announced four display-technology business awards spanning China, India, and South America, with development work planned from Q2 2026 through Q4 2027. The wins reinforce local-for-local execution in high-growth regions and keep Forvia positioned to bundle display hardware with cockpit software and HMI layers across multiple vehicle programs.

- January 2026: DENSO Corporation became a Core Partner of the AUTOSAR consortium to accelerate standardization of automotive software. The move supports faster integration and reuse of cockpit software components across OEM programs, which can shorten validation cycles for instrument clusters and digital cockpit controllers.

- March 2025: Continental AG introduced Ac2ated Sound integration that embeds speaker functionality directly into display units using actuators behind the display surface. The approach reduces packaging space and weight in the instrument panel area, enabling thinner dashboards and new design freedom as OEMs expand screen area and cockpit integration.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers dashboards installed in passenger cars and commercial vehicles, including the instrument panel structure plus the integrated display and control content that presents vehicle information and key functions to the driver and occupants.

Scope exclusions: We exclude standalone infotainment head units sold as separate modules, HUD-only units when priced and shipped separately, and general interior trim parts that are not part of the dashboard assembly.

Segmentation Overview

- By Type

- LCD/TFT Digital Dashboard

- Hybrid/Dual-mode Dashboard

- Conventional Analog Dashboard

- By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Medium and Heavy Commercial Vehicles

- By Sales Channel

- OEM

- Aftermarket

- By Component

- Display Panel

- Control Electronics and SoC

- Software/HMI Layer

- Structural Trim and HVAC Interfaces

- By Display Size

- Less than 7-inch

- 7 to 11 inch

- Above 11-inch

- By Technology

- LCD

- OLED / Mini-LED

- HUD-Integrated Cluster

- Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Egypt

- Turkey

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with grounding the model in verifiable vehicle production and fleet indicators, so the final number stays tied to real build cycles. We mainly use public datasets such as OICA production statistics, U.S. Bureau of Transportation Statistics summaries, Eurostat industrial and trade tables, and UN Comtrade import export series for relevant electronic and plastic sub-assemblies.

To make the build more practical, we also review materials from company annual reports and investor presentations, customs and tariff schedules where they clarify classification, and press releases around platform launches and supply awards. When needed, a paid subscription for company financials and a shipment-level trade database is used to cross-check volumes and price bands by region. These desk sources are illustrative only, and many other public references were also checked for collection, validation, and clarification.

Primary Interviews and Surveys

Primary inputs come from interviews and short surveys with OEM-facing program teams, dashboard module suppliers, materials and display ecosystem participants, and distribution-side experts who see ordering patterns. Coverage is balanced across APAC, EMEA, and the Americas so adoption timing for digital clusters, screen sizes, and trim levels can be validated, and then assumptions can be triangulated back to the desk indicators.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 12% | APAC: 45% |

| Mid tier: 44% | Functional/Unit leaders: 43% | EMEA: 32% |

| Smaller Players: 21% | Managers: 45% | Americas: 23% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where vehicle production by region is reconstructed, and then dashboard fitment and content value are applied by vehicle class and trim mix. The model is then corroborated with selective bottom-up checks, such as supplier revenue splits, sampled program quotes, and a simple ASP times volume build for a few high-volume platforms to confirm the totals are not drifting.

Key inputs used in the model include passenger car and commercial vehicle production volumes, the share of vehicles adopting digital clusters versus analog layouts, average display size mix (for example, below 7-inch versus larger), OEM versus aftermarket replacement share, and price progression tied to display technology and electronics content. Where direct pricing is not visible, gaps are handled by using a bounded range built from interview feedback and observed trade-value per unit signals, and then narrowed through consistency checks.

For forecasting, we rely on scenario analysis supported by a light multivariate regression view, where output is tested against drivers such as vehicle production outlook, electrification and premium feature penetration, and expected cost down curves for screens and control electronics. Expert feedback is used to confirm if the modeled adoption path matches real program timing, before the final forecast is locked.

Data Validation & Update Cycle

Outputs are validated through multiple passes where unit economics, implied content per vehicle, and regional growth rates are compared against independent signals like production trends and trade values. When variances look high, we revisit the assumptions, re-check definitions, and re-contact selected respondents so the correction is explained and documented.

Before sign-off, the work is reviewed by another analyst for arithmetic accuracy and for consistency across the narrative and the model. The report is refreshed annually, and interim updates are made when material events occur, such as major platform changes, supply disruptions, or sharp currency moves. Right before delivery, a fresh review pass is completed so clients receive an updated view that reflects the latest available data.

Mordor Intelligence's Automotive Dashboard Market Size Measured Against Other Published Estimates

Published numbers for the automotive dashboard market often vary because the counted product boundary is not consistent, and because some sources lean on different base years or longer forecast windows that blend cycle effects. The spread also comes from how digital content is valued, since ASP movement depends on screen size, electronics content, and the vehicle mix in each region.

The benchmark table shows a large gap versus higher published figures, and in Mordor Intelligence's model the value is limited to dashboard assemblies and integrated dashboard display and control content supplied to OEM and aftermarket channels, rather than bundling broader cockpit or infotainment-only hardware sold as separate modules.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 13.76 B (2026) | |

| Global Consultancy A | USD 29.47 B (2025) | Uses a broader definition that appears to blend instrument panel components with adjacent cockpit items, and it uses a 2025 base year that can embed a different vehicle production and pricing cycle. |

| Industry Publisher B | USD 27.06 B (2024) | Tends to treat a wider car dashboard feature set as one pool, which can lift ASP assumptions when premium features are averaged across regions, and it anchors the estimate in a 2024 base year with different FX timing. |

Reading the three numbers together, most of the difference is explained by what is included around the dashboard, plus the base-year and pricing treatment used to convert content into dollars. By keeping the model tied to vehicle build volumes, fitment rates, and realistic ASP bands that are re-checked with interviews, the estimate stays repeatable and easier to audit over time.

Key Questions Answered in the Report

What is the current size of the automotive dashboard market?

The automotive dashboard market size is USD 13764.2 million in 2026, with a projected value of USD 19415.1 million by 2031.

Which dashboard technology holds the largest market share today?

LCD/TFT digital dashboards lead with 64.32% of 2025 revenue, owing to mature production and favorable pricing.

Why is Asia-Pacific the fastest-growing region for automotive dashboards?

The region benefits from high electric-vehicle output, integrated local display manufacturing, and strong technology adoption, supporting a 9.05% regional CAGR.

What role does the aftermarket play in the dashboard sector?

Although it held just 12.05% of 2025 revenue, the aftermarket grows 9.20% yearly as owners retrofit connectivity and infotainment features into aging vehicles.

Page last updated on: