Automotive Collapsible Steering Column Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 3.64 Billion |

| Market Size (2030) | USD 4.91 Billion |

| Growth Rate (2025 - 2030) | 6.17% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Collapsible Steering Column Market Analysis by Mordor Intelligence

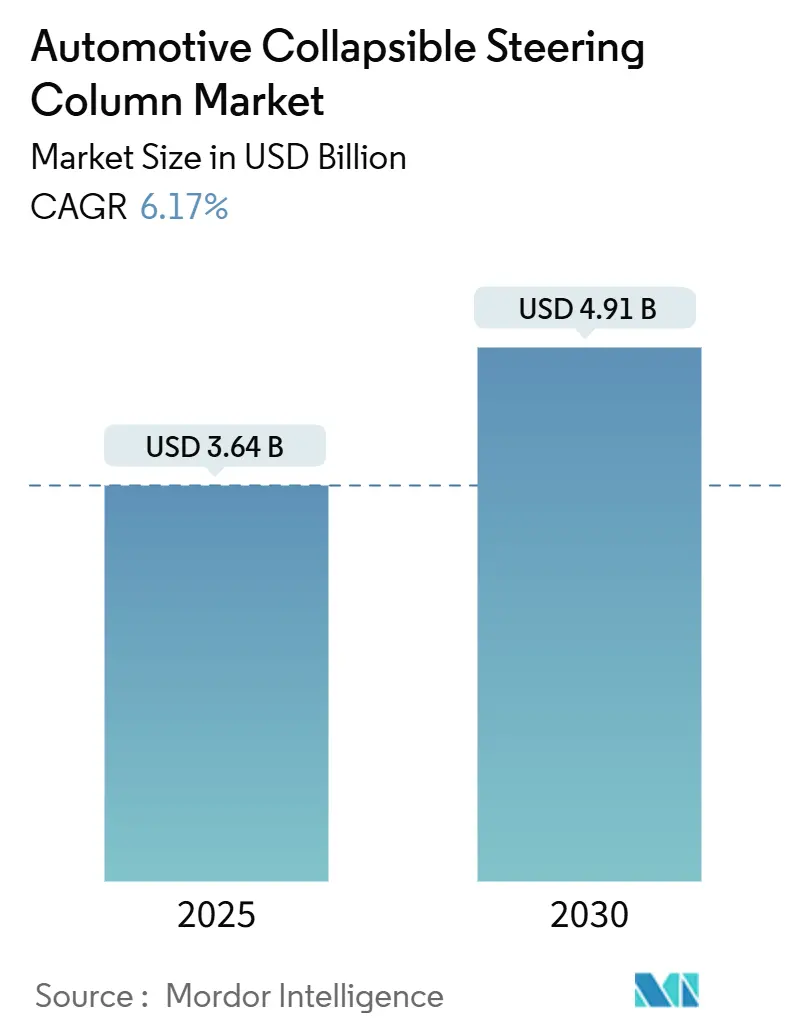

The automotive collapsible steering column market size is valued at USD 3.64 billion in 2025 and is projected to expand to USD 4.91 billion by 2030 at a 6.17% CAGR. Mandatory frontal-impact safety regulations, rapid vehicle electrification, and the migration toward steer-by-wire platforms collectively redefine design requirements, prompting suppliers to integrate sophisticated energy-absorbing mechanisms that interface seamlessly with electric power steering. Asia-Pacific’s outsized vehicle production base accelerates demand for lightweight columns, while insurance incentives and shared-mobility fleet growth broaden the addressable user base. At the same time, supply chain localization and specialty-steel volatility reshape sourcing strategies, and the absence of uniform EV-specific collapse standards injects regulatory uncertainty that suppliers must manage. Competitive pressures intensify as leading players race to commercialize steer-by-wire-ready columns and expand regional footprints to serve emerging production hubs.

Key Report Takeaways

- By type, electric collapsible steering columns led with 53.16% share of the automotive collapsible steering column market in 2024; the segment is forecasted to expand at an 8.78% CAGR to 2030.

- By material, steel captured 62.36% of the automotive collapsible steering column market share in 2024, while composite materials are projected to record the highest CAGR at 8.07% through 2030.

- By mechanism type, energy-absorbing systems commanded 77.64% of the automotive collapsible steering column market in 2024 and are advancing at a 9.61% CAGR through 2030.

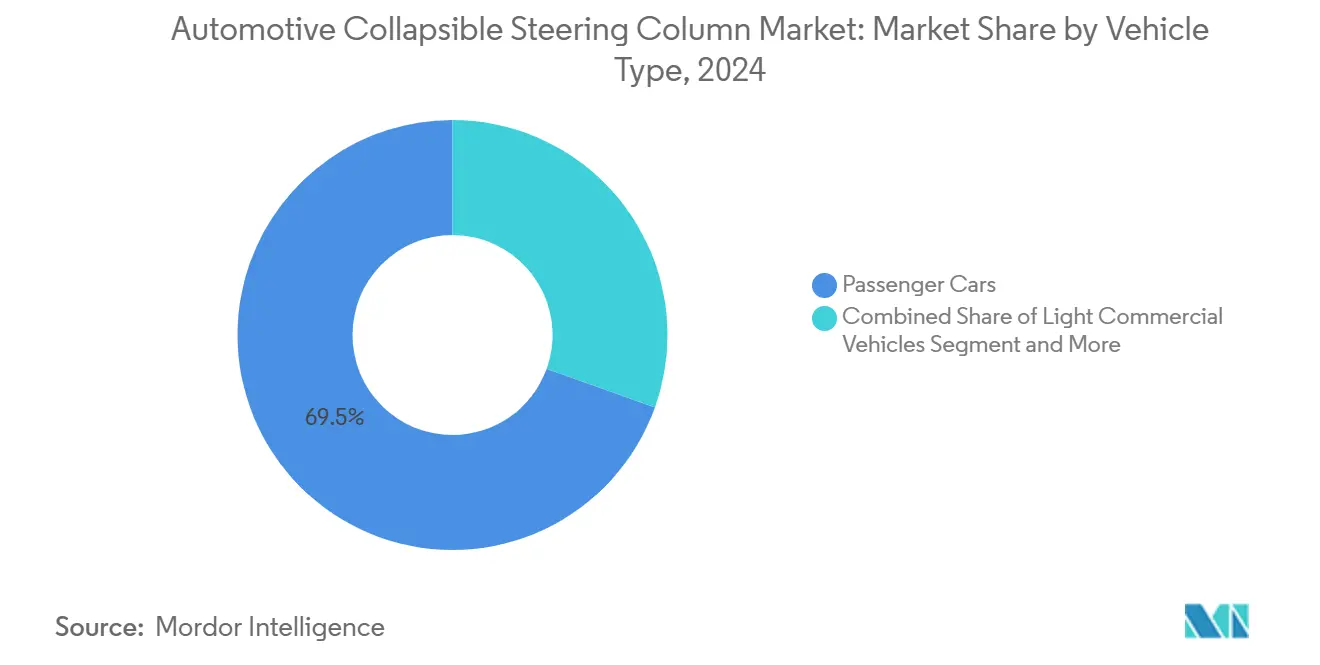

- By vehicle type, passenger cars accounted for 69.52% of the automotive collapsible steering column market size in 2024 and are projected to grow at a 7.97% CAGR through 2030.

- By distribution channel, OEM sales held 82.85% share of the automotive collapsible steering column market in 2024, whereas the aftermarket segment is projected to post the fastest 8.27% CAGR to 2030.

- By geography, Asia-Pacific dominated with 43.96% share of the automotive collapsible steering column market in 2024 and is projected to be the fastest growing at a 7.39% CAGR through 2030.

Global Automotive Collapsible Steering Column Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Global Safety Mandates | +0.9% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Rapid Vehicle Electrification | +0.7% | APAC core, spill-over to North America & EU | Short term (≤ 2 years) |

| Modular Steer-By-Wire Column Architectures | +0.6% | Global, led by premium segments in EU & North America | Long term (≥ 4 years) |

| Localization of Safety-Critical Column Supply | +0.6% | APAC, South America, with selective MEA expansion | Medium term (2-4 years) |

| Insurance for Advanced Collapsible Columns | +0.5% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Shared-Mobility Fleet Growth | +0.4% | Urban centers globally, concentrated in North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Global Safety Mandates For Frontal-Impact Protection

Crash-worthiness rules continue to tighten. The Insurance Institute for Highway Safety revised its 2025 Top Safety Pick criteria, compelling OEMs to achieve stronger second-row occupant protection and Good ratings in updated frontal and side tests[1]“IIHS makes stronger protection for back seat passengers a must for 2025,” Insurance Institute for Highway Safety, iihs.org. Stricter global safety standards are reshaping steering column design, as fewer vehicle models meet the latest benchmarks without significant upgrades. Regulatory alignment across regions driven by initiatives like Europe’s GSR II, China’s C-NCAP, and India’s Bharat NCAP creates a unified framework that raises expectations for energy absorption and occupant protection. In response, suppliers are engineering multi-stage deformation zones and adaptive restraint systems that go beyond legacy compliance norms, setting new performance baselines. As these mandates extend from luxury vehicles to more affordable segments, the demand for steering columns that balance advanced safety features with cost efficiency is growing. This shift expands the total addressable market, encouraging innovation in scalable designs that meet diverse OEM needs. The evolution positions steering column suppliers not just as component makers, but as strategic partners in global vehicle safety.

Rapid Vehicle Electrification Raising Demand for EPS-Compatible Columns

Electric powertrains eliminate hydraulic pumps and reduce steering effort, yet they introduce packaging and thermal constraints that legacy columns cannot satisfy. EPS-compatible columns feature slimmer housings and optimized collapse strokes that clear battery modules and high-voltage wiring. Automakers also demand lower parasitic mass to extend driving range, accelerating the shift toward lightweight energy-absorbing structures. Because EV product cycles are shorter than those of ICE vehicles, column suppliers must rapidly turn designs and validate them against evolving crash profiles. The rapid sales growth of battery-electric SUVs in China and Europe is a near-term catalyst for the automotive collapsible steering column market.

OEM Shift Toward Modular Steer-By-Wire Column Architectures

Steer-by-wire removes the mechanical link between the steering wheel and the rack, enabling columns to retract, tilt more aggressively, or even fold away entirely. Premium brands have started to specify modular “plug-and-play” column cores that can switch between mechanical and electronic actuation depending on trim level. Suppliers respond by integrating redundant electronic couplers and adaptive deformation sleeves that protect occupants even when the column is partially stowed. The modular approach also shortens assembly-line changeovers, supporting OEM moves toward flexible manufacturing. Over the long term, steer-by-wire readiness will determine which vendors retain share as autonomous-driving regulations mature.

OEM Localization of Safety-Critical Column Supply in Emerging Markets

Carmakers want column plants close to final assembly to cut logistics risk and meet rising local-content mandates. New facilities in Southeast Asia, Mexico, and North Africa pair automated tube-welding lines with in-house metallurgical labs, assuring consistent collapse performance. Localization strengthens just-in-time inventory models, but it also forces suppliers to replicate R&D capabilities regionally, adding fixed cost. Governments often sweeten capital-investment packages with tax incentives, lowering break-even volumes and encouraging rapid capacity ramp-ups. The result is a more geographically balanced supply base that stabilizes lead times for global EV programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Material and Manufacturing Costs | -0.5% | Global, most acute in cost-sensitive segments | Short term (≤ 2 years) |

| Integration with Steer-By-Wire Platforms | -0.4% | Premium segments globally, expanding to mass market | Medium term (2-4 years) |

| Supply-Chain Volatility | -0.2% | Global, with regional variations in material availability | Short term (≤ 2 years) |

| Collapse-Test Standard Absence | -0.2% | Global, most critical in early EV adoption markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Material and Manufacturing Costs of Energy-Absorbing Designs

Specialized materials, such as high-grade alloys and engineered composites, are becoming increasingly vital for advanced steering columns. However, the input costs for these materials remain unpredictable. While these materials enhance energy absorption and structural performance, their precise manufacturing processes necessitate significant capital investment. Consequently, budget-focused vehicle segments feel the brunt of these cost pressures. This scenario has led to a staggered adoption curve in the industry. With their capacity to absorb higher costs and a strong emphasis on innovation, Premium automakers are at the forefront, swiftly integrating next-generation column technologies. In contrast, mass-market brands adopt these technologies later, waiting for production volumes to increase and economies of scale to kick in. This gradual approach allows them to offer advanced safety and performance features to a wider range of vehicles.

Complex Integration with Steer-By-Wire ⁄ Autonomous Platforms

Full steer-by-wire columns must exchange high-speed data with vehicle-motion controllers while still guaranteeing mechanical integrity during a power loss. This dual mandate drives up sensor count, wiring complexity, and software-validation hours. Cyber-security certification under ISO 21434 adds new documentation burdens unfamiliar to traditional metal-forming specialists. OEMs impose strict functional-safety targets, forcing suppliers to adopt costly redundancy in motors and control electronics. Integration risk therefore tempers near-term volume forecasts even as long-term demand looks strong.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Electric Dominance Accelerates

Electric collapsible steering columns captured 53.16% of the automotive collapsible steering column market in 2024, evidencing the sector’s pivot toward EPS-friendly architectures. The segment’s 8.78% CAGR to 2030 surpasses the overall industry trajectory, driven by tighter packing requirements in battery-electric vehicles and lower steering-effort loads. Manual columns persist in cost-sensitive applications but cede share each model year, while hydraulic variants retain niche use in heavy-duty trucks that demand high steering torque. Insurance discounts for vehicles equipped with electric columns further stimulate adoption.

Technological convergence with steer-by-wire reshapes supplier roadmaps. Bosch’s steering-wheel actuator enables full column stowage for automated modes, illustrating how electromechanical designs lower cabin intrusion and weight. Suppliers must bridge mechanical energy absorption with redundant electronic actuation, an area where legacy experience and functional-safety mastery confer competitive advantage. Companies that align R&D with ISO 26262 and ISO 21434 requirements are positioned to capitalize on OEM rollouts of partially automated platforms from 2026 onward.

By Material: Steel Dominance Faces Composite Challenge

Steel maintained a 62.36% share of the automotive collapsible steering column market size in 2024, favored for its proven crash response, familiarity among OEM engineers, and cost efficiency. Aluminum gains in premium electric models seeking every kilogram saved, especially where range sensitivity is paramount[2]"Benefits of Aluminium Fabrication in Automotive Engineering", SIMMAL LTD, simmal.com . Plastic shrouds facilitate cosmetic customization and minor weight trimming but remain non-structural. Composite materials are expected to post the fastest 8.07% CAGR, propelled by superior energy absorption-to-mass ratios crucial for EV efficiency.

Suppliers continue to refine hybrid metal-composite architectures that exploit steel’s predictable buckling with composite crush-tubes that absorb high-frequency impact pulses. Research confirming glass-fiber-reinforced PPS composites’ high mean crushing force accelerates premium OEM interest. Yet manufacturing complexity and higher scrap rates hinder widespread deployment. Scale production will likely emerge first in Asia-Pacific, where vertically integrated supply chains allow cost-competitive composite lay-ups for regional EV giants.

By Mechanism Type: Energy-Absorbing Systems Prevail

Energy-absorbing columns held 77.64% share of the automotive collapsible steering column market in 2024 and are forecasted to rise at a 9.61% CAGR. Multi-stage deformation straps, controlled buckling beads, and telescopic tubes collectively manage crash pulses across varied occupant sizes. Regulators increasingly test small-female and large-male dummies, demanding broader performance envelopes that non-energy-absorbing designs cannot meet. Insurance bodies highlight lower thoracic and femur loads in vehicles equipped with adaptive columns, reinforcing OEM preference for these systems.

Non-energy-absorbing columns persist in low-cost regions where frontal-impact speeds average below 45 km/h and where side-impact structures absorb most kinetic energy. They employ shear-pin collapses that are easy to machine but offer limited tuning flexibility. As global safety mandates converge, these basic designs will retreat to low-volume commercial or off-road applications. Suppliers focus R&D on variable-resistance mechanisms that alter collapse force in real time using magneto-rheological dampers. The next innovation wave could therefore blur the line between passive energy absorption and active safety actuation.

By Vehicle Type: Passenger Cars Drive Volume Growth

Passenger cars represented 69.52% of the automotive collapsible steering column market size in 2024 and are projected to grow at a 7.97% CAGR through 2030, buoyed by continuous styling refreshes that embed new safety tech. Family sedans and compact SUVs account for most unit volume, and their platform commonality simplifies column reuse across badges. Electrification further boosts column content per vehicle as EPS motors integrate torque feedback and vibration-cancellation features. Fleet operators prefer models with adjustable columns that improve driver comfort across multiple shifts, adding aftermarket revenue potential.

Light commercial vehicles trail but log faster installation of collapsible designs as urban delivery fleets value higher crash-worthiness scores. Medium and heavy trucks rely on bulkier hydraulic systems, yet still require controlled collapse to protect drivers in frontal jack-knife events. Upcoming U.S. regulations will likely extend small-overlap crash tests to Class 3 trucks, forcing heavier platforms to adopt passenger-car-level energy management. The combined effect broadens the customer base and sustains steady growth in the automotive collapsible steering column market.

By Distribution Channel: OEM Dominance Shapes Market Structure

OEM channels owned an 82.85% share of the automotive collapsible steering column market size in 2024, reflecting the safety-critical nature of steering columns and the need for bespoke calibration within each vehicle’s crash envelope. Direct sourcing also aligns with just-in-sequence assembly processes that minimize plant inventory. As columns evolve into steer-by-wire nodes, OEMs require deep software integration that favors tier-one suppliers embedded in early design phases. Warranty considerations further reinforce the preference for factory-installed units.

The aftermarket segment, however, is projected to grow at 8.27% CAGR as vehicle age rises in North America and Europe. Digital catalogs, VIN-level fit-guides, and remote programming tools lower the replacement barrier for independent garages. Continental’s recent range expansion shows that OE-quality columns can be profitably sold outside dealer networks once patents expire. Collision repair drives most volume, but tuner segments also buy adjustable columns to customize driving ergonomics. This incremental demand builds a secondary revenue pillar for suppliers already entrenched in OEM programs.

Geography Analysis

Asia-Pacific accounted for 43.96% of global market revenue in 2024 and is forecasted to grow at a 7.39% CAGR through 2030. Expansion stems from high-volume manufacturing clusters in China, India, and Japan, each scaling EV production that inherently demands EPS-compatible, lightweight columns. Government incentives for domestic battery-electric vehicles push automakers to integrate next-generation safety modules early in product cycles. Localization agendas drive capital inflows into regional column plants, tightening supplier-OEM collaboration and shortening design-for-manufacture loops.

North America ranks second by value, supported by aggressive Insurance Institute for Highway Safety (IIHS) protocols that compel adoption of multi-stage energy-absorbing columns across car and light-truck lineups. While the region trails Asia-Pacific in unit growth, premium vehicle concentration elevates average column content per vehicle, bolstering revenue. Investments in localized specialty steel production mitigate tariff risks and reinforce supply security, positioning domestic suppliers to serve electrified pickup and SUV programs launching from 2026.

Europe retains a technology leadership role thanks to GSR II and NCAP harmonization, although unit demand plateaus in mature markets. Regulatory emphasis on advanced driver-assistance compatibility pushes European OEMs to leverage steer-by-wire-ready columns as differentiators in premium platforms. Suppliers respond with modular designs that blend electronic strain sensors and deployable crash-stroke adjusters, future-proofing columns for Level 3 autonomy. Emerging demand in Eastern European assembly hubs introduces cost-and-performance balancing challenges that global suppliers must navigate to safeguard margins.

Competitive Landscape

Competition remains moderately concentrated as the top five suppliers collectively hold a majority share, yet preserving room for tier-two specialists that excel in niche mechanisms or regional fulfillment. JTEKT command stems from tight Toyota group linkages and a breadth of hydraulic-to-electric offerings that appeal across powertrain spectrums. ZF follows, leveraging systems-integration know-how to bundle columns with steer-by-wire actuators, reinforcing platform-level pull-through.

Bosch differentiates through holistic vehicle-motion management that synchronizes steering, braking, and suspension controllers, allowing its columns to act as an integral node in the software-defined chassis. NSK and Nexteer round out the leading quintet, each emphasizing localized engineering centers and adaptive energy-absorbing strap patents. New entrants concentrate on composite-tube technology and electronic redundancy but face capital and homologation hurdles that lengthen time-to-market.

Strategic moves through 2025 revolve around capacity expansion in emerging manufacturing corridors and joint development agreements targeting steer-by-wire readiness. Plant announcements in Mexico, Morocco, and Southeast Asia illustrate the race to align with OEM localization mandates. Concurrently, patent filings for adaptive deformation zones signal an IP arms race poised to intensify as autonomous driving milestones near. The competitive outlook favors suppliers that blend mechanical crash expertise with functional-safety certified electronics while sustaining cost disciplines in volatile commodity environments.

Automotive Collapsible Steering Column Industry Leaders

-

JTEKT Corporation

-

ZF Friedrichshafen AG

-

Robert Bosch GmbH

-

NSK Ltd.

-

Nexteer Automotive

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: ZF LIFETEC unveiled an electric folding steering wheel that retracts into the dashboard within two seconds, opening cabin space for automated driving modes.

- April 2025: The Alvis Car Company premiered the 2025 Lancefield continuation car in Japan, featuring a collapsible steering column alongside modern emissions components.

- March 2025: Maruti Suzuki updated the Alto K10 with standard collapsible steering column, ESP, and multiple occupant-safety upgrades.

- October 2024: Isuzu Motors India launched the D-MAX Ambulance with a collapsible steering column and side-impact protection beams for enhanced pedestrian safety.

Global Automotive Collapsible Steering Column Market Report Scope

| Manual Collapsible Steering Column |

| Electric Collapsible Steering Column |

| Hydraulic Collapsible Steering Column |

| Steel |

| Aluminum |

| Composite Materials |

| Plastic |

| Energy Absorbing |

| Non-Energy Absorbing |

| Passenger Vehicles |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Manual Collapsible Steering Column | |

| Electric Collapsible Steering Column | ||

| Hydraulic Collapsible Steering Column | ||

| By Material | Steel | |

| Aluminum | ||

| Composite Materials | ||

| Plastic | ||

| By Mechanism Type | Energy Absorbing | |

| Non-Energy Absorbing | ||

| By Vehicle Type | Passenger Vehicles | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the automotive collapsible steering column market by 2030?

The market is forecasted to reach USD 4.91 billion by 2030, growing at a 6.17% CAGR from 2025.

Which product type leads global demand?

Electric collapsible steering columns hold the largest 53.16% share and record the fastest 8.78% CAGR through 2030.

Why are composite materials gaining traction?

Glass-fiber-reinforced composites offer superior energy absorption per kilogram, driving an 8.07% CAGR despite higher production complexity.

Which region offers the highest growth potential?

Asia-Pacific combines the largest 43.96% share with the quickest 7.39% CAGR, propelled by expanding EV production.

Page last updated on: