Automotive Voice Recognition System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.08 Billion |

| Market Size (2031) | USD 9.86 Billion |

| Growth Rate (2026 - 2031) | 14.17% CAGR |

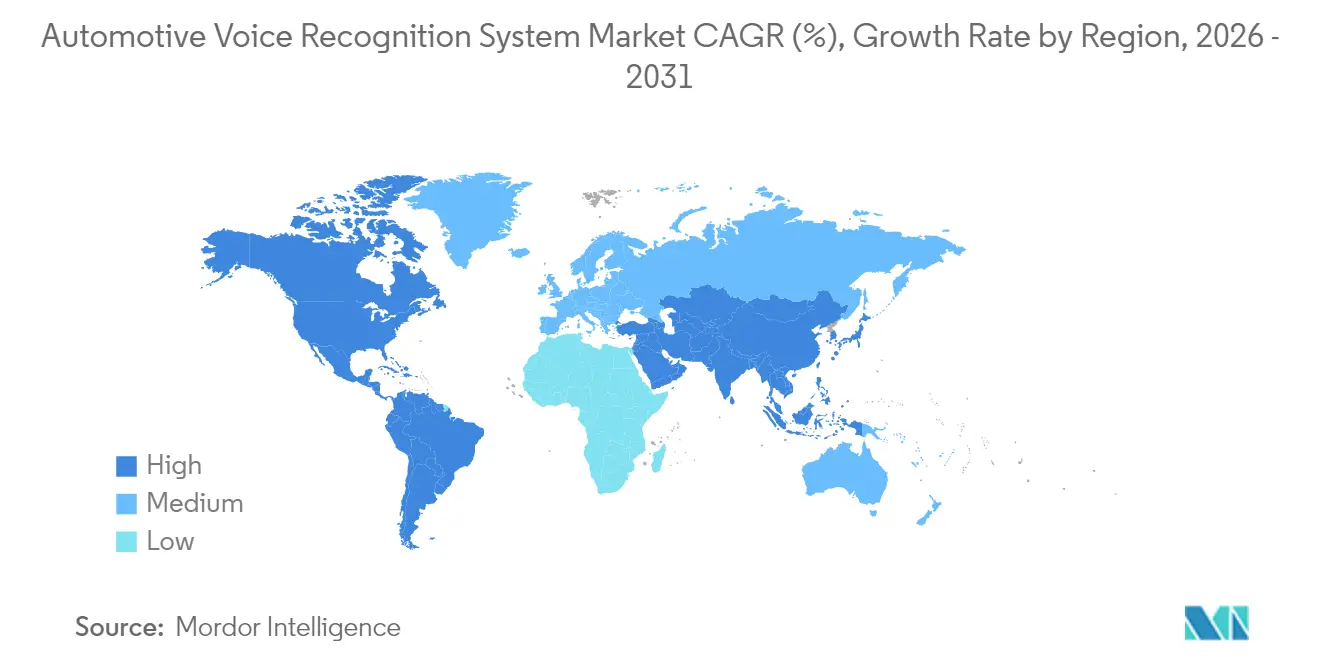

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

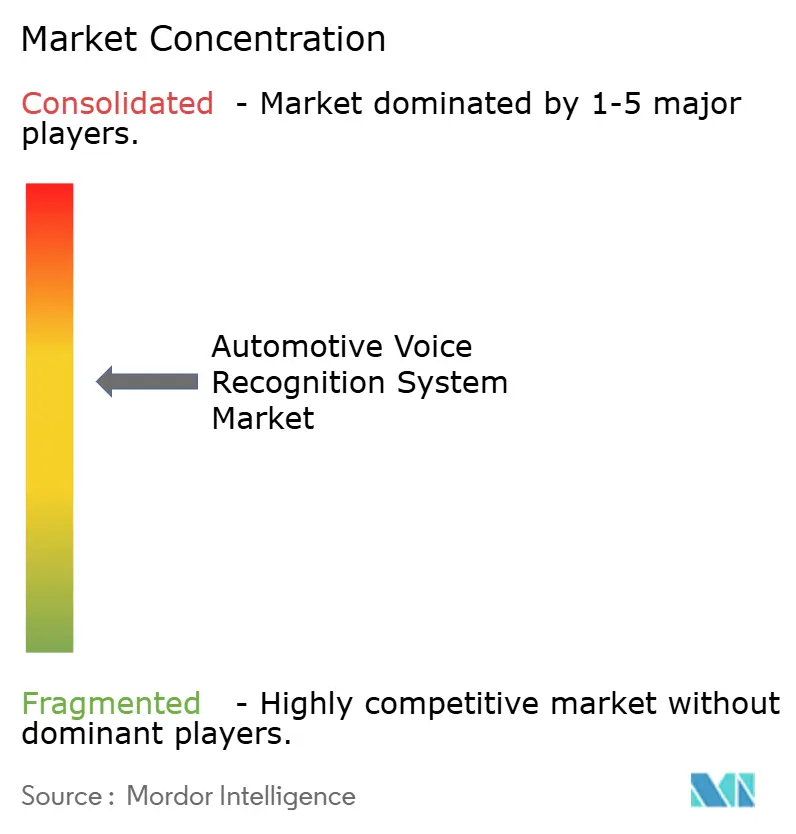

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Voice Recognition System Market Analysis by Mordor Intelligence

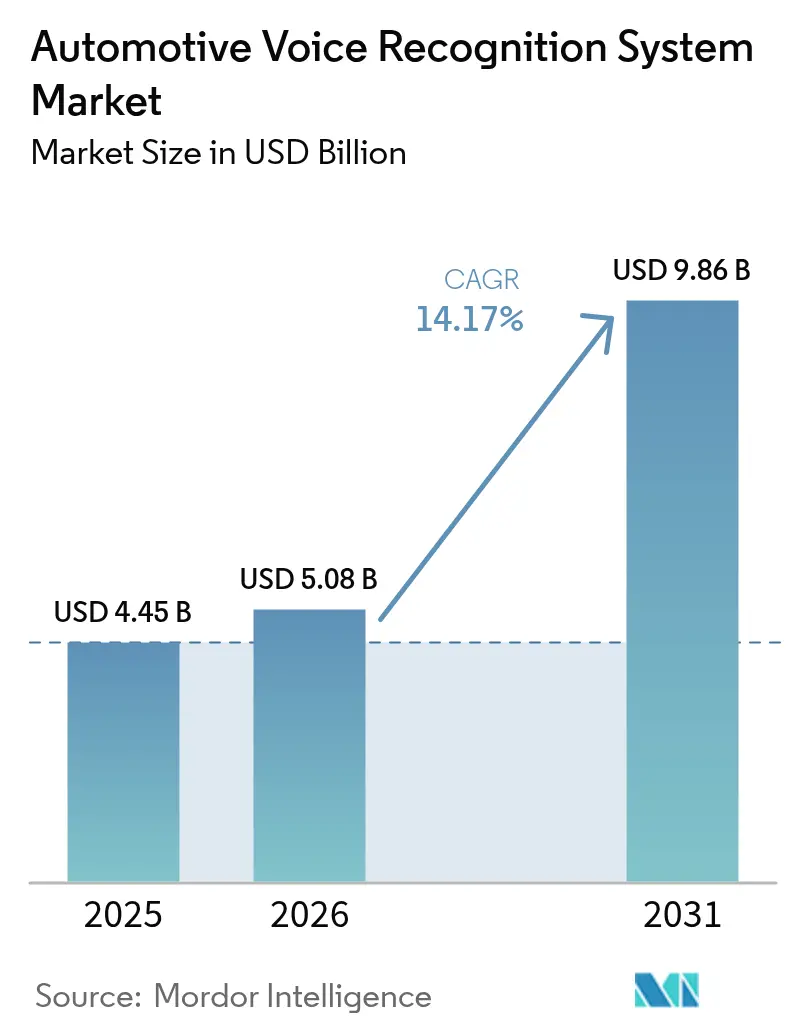

The Automotive Voice Recognition System market size was valued at USD 4.45 billion in 2025 and estimated to grow from USD 5.08 billion in 2026 to reach USD 9.86 billion by 2031, at a CAGR of 14.17% during the forecast period (2026-2031). Accelerating growth stems from three converging shifts: connected-car ecosystems now treat voice as the primary user interface, edge-AI chips slash on-device processing costs, and regulators tighten rules on distraction-free driving. Automakers have begun treating voice as a revenue engine, bundling subscription services and in-vehicle commerce that extend well beyond simple command execution.

Key Report Takeaways

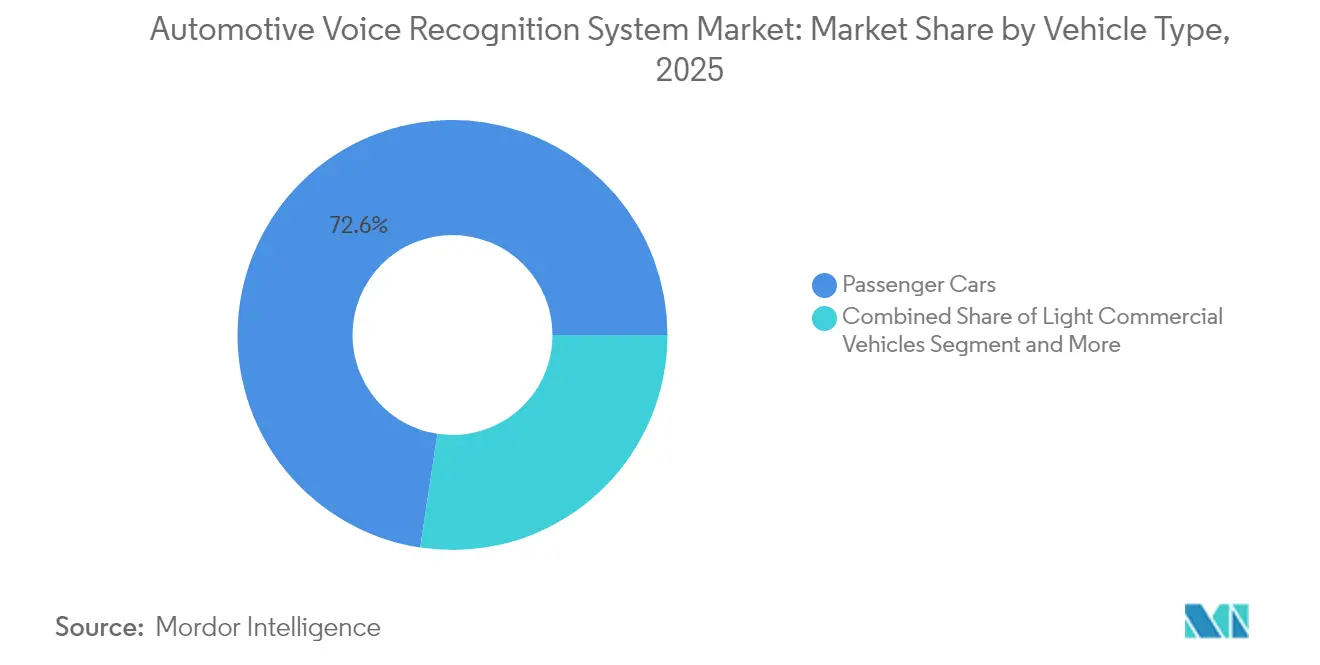

- By vehicle type, passenger cars led with 72.60% of the Automotive Voice Recognition System market share in 2025, while Commercial Vehicles are projected to expand at 14.62% CAGR through 2031.

- By technology, embedded solutions accounted for 53.80% of the Automotive Voice Recognition System market size in 2025; the Cloud-based segment is on track for the fastest 14.65% CAGR to 2031.

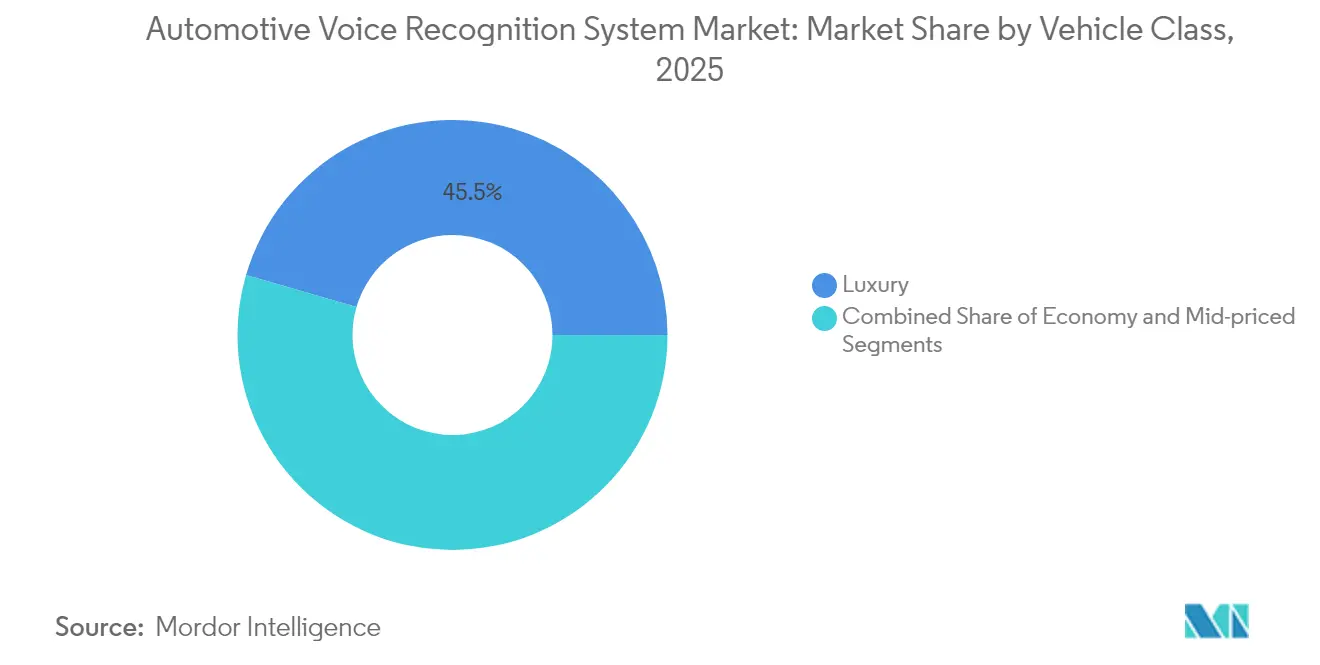

- By vehicle class, luxury models captured 45.50% revenue share in 2025, yet Economy vehicles are forecast to climb at 14.32% CAGR.

- By microphone array design, single-microphone layouts held a 31.70% share in 2025, whereas beam-forming arrays will post a 13.72% CAGR through 2031.

- By geography, North America maintained a 37.10% share in 2025; Asia Pacific is the high-growth region with a 14.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Voice Recognition System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Connected-Car Ecosystems | +3.2% | Global (North America, Europe early) | Medium term (2-4 years) |

| Luxury and Premium Vehicle Penetration | +2.8% | North America, Europe, China | Short term (≤ 2 years) |

| In-Cabin Distraction Regulations | +2.1% | Europe, North America, APAC spillover | Long term (≥ 4 years) |

| Edge-AI Chip Cost | +1.9% | Global (manufacturing in APAC) | Medium term (2-4 years) |

| OEM Monetisation | +1.7% | North America, Europe, APAC expansion | Long term (≥ 4 years) |

| Driver-Health Monitoring Integration | +1.4% | Global (focus Europe, North America) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Connected-Car Ecosystems

Connected-car platforms now link vehicle functions, smart-home devices, and third-party apps through a unified voice layer. Volkswagen’s rollout of Cerence Chat Pro enables conversational control over navigation, weather, and commerce from a single interface.[1]Cerence, “Cerence launches Chat Pro for Volkswagen Group vehicles,” cerence.com Over-the-air updates continually sharpen recognition accuracy and add new skills, helping brands keep pace with user expectations. Partnerships such as SoundHound AI with Tencent extend these benefits into mobility super-apps that bridge in-car and mobile experiences.[2]SoundHound AI, “SoundHound partners with Tencent for in-vehicle voice commerce,” soundhound.com As ecosystems mature, authenticated voice commerce unlocks new revenue streams for automakers, further reinforcing voice as the default human-machine channel.

Surge in Luxury & Premium Vehicle Penetration

Premium marques deploy voice as a signature experience to justify higher sticker prices. The 2025 Mercedes-Benz S-Class introduced AI-powered assistants able to recognise individual occupants and anticipate preferences. Jaguar Land Rover’s collaboration with Cerence adds emotion detection and multilingual support to bolster brand differentiation. Such luxury rollouts absorb early cost premiums, allow software refinement in low-volume settings and pave the way for cost-down migration to mid-segment vehicles. Subscription add-ons in premium segments also validate monetisation models that mainstream brands later replicate.

Tighter In-Cabin Distraction Regulations

Regulatory frameworks increasingly mandate hands-free interaction capabilities, positioning voice recognition as essential safety technology rather than optional convenience features. In the United States, NHTSA’s Section 24220 mandate for driver-impairment detection from 2026 further boosts demand for speech-based monitoring capable of spotting drowsiness through vocal biomarkers. These rules lock voice into vehicle roadmaps regardless of consumer tastes. Further, the UN Economic Commission for Europe's new regulations for additional driver assistance systems further emphasize voice interaction as a key component of connected and automated mobility frameworks.[3]UNECE, "New UN regulation paves the way for the roll-out of additional driver assistance systems", unece.org

Edge-AI Chip Cost Declines

Dramatic reductions in edge-AI chip costs are enabling on-device voice processing that addresses privacy concerns while improving response times and reducing connectivity dependencies. Syntiant's achievement of 100% acceleration in large language model performance for edge devices demonstrates how specialized processors make sophisticated voice recognition economically viable for mass-market vehicles. SoundHound AI's collaboration with NVIDIA to develop on-device voice assistants that operate without cloud connectivity illustrates how edge processing enables real-time responses while maintaining user privacy. These advances solve privacy and coverage gaps, letting OEMs run core commands locally and reserve the cloud for generative tasks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hardware Retrofit Costs | -2.3% | Global, with higher impact in price-sensitive markets | Short term (≤ 2 years) |

| Accent and Dialect Accuracy Gaps | -1.8% | APAC, South America, Africa, Middle East | Medium term (2-4 years) |

| Data-Privacy Compliance Burden | -1.5% | Europe and China core, expanding globally | Long term (≥ 4 years) |

| RF Interference from Multi-Sensor Cockpits | -1.2% | Global, with higher impact in premium vehicles | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Up-Front Hardware Retrofit Costs

Substantial upfront investments required for voice recognition hardware integration create significant barriers for automakers operating in price-sensitive markets and existing vehicle retrofitting scenarios. These costs are compounded by the need for electromagnetic compatibility solutions to address RF interference, requiring additional shielding and filtering components that further increase implementation expenses. Cerence Link's OBD-port solution represents one approach to retrofit challenges, but such aftermarket solutions typically offer limited functionality compared to integrated systems. The cost burden is particularly acute for commercial vehicle operators who must balance voice system benefits against fleet acquisition costs, though emerging evidence suggests voice technology's operational efficiency gains can justify the investment over time.

Accent and Dialect Accuracy Gaps in Emerging Markets

Voice error rates remain 2–3× higher for Indian English or African dialects than for standard American English, frustrating users and denting brand perception. The challenge is compounded in markets like India, where multiple languages and regional dialects create complex recognition requirements that current systems struggle to address effectively. Until accent coverage improves, uptake in multilingual markets will lag headline growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Fleets Drive Voice Adoption

Passenger Cars still command 72.60% of 2025 shipments, yet their growth curve will plateau relative to fleet-driven demand. Learnings from round-the-clock commercial duty cycles feed refinements back into consumer interfaces, raising reliability expectations. As regulatory thresholds tighten for distraction metrics, passenger models increasingly inherit fleet-proven microphone arrays and edge-processing chips, ensuring consistency across brand portfolios.

Commercial Vehicles, although contributing a smaller base, will outpace the broader Automotive Voice Recognition System market at a 14.62% CAGR through 2031. Fleet operators quantify return on investment via reduced distraction-related incidents and faster dispatch communications. Light commercial vans increasingly ship with voice-activated work-order logging, while heavy trucks pair assistants with telematics to vocalise predictive-maintenance alerts. These tangible savings persuade fleet owners to specify voice as standard spec, reinforcing unit volumes that, in turn, dilute per-vehicle costs for passenger cars.

By Technology: Cloud-Based Solutions Accelerate Despite Privacy Concerns

Embedded processing remains the workhorse, anchoring 53.80% of 2025 revenue because it satisfies GDPR-centred privacy norms and guarantees service in low-coverage zones. However, cloud-centric architectures are scaling fastest at 14.65% CAGR, propelled by generative-AI services impossible to host on 16-bit microcontrollers. Volkswagen’s ChatGPT integration shows how on-demand cloud reasoning augments local command sets while retaining sub-second response times.

Hybrid topologies now blend the two, running wake-word and HVAC commands on the device while routing knowledge queries to remote GPUs. This split satisfies data-protection regulators yet unleashes richer experiences, making hybrid likely to dominate the Automotive Voice Recognition System market share beyond 2028. Suppliers that orchestrate seamless hand-offs between edge and cloud thus occupy pivotal positions in OEM roadmaps.

By Vehicle Class: Economy Segment Democratises Voice Technology

Luxury cars captured 45.50% of 2025 spend because early adopters valued premium assistants with mood sensing and personalised lighting scripts. Yet the economy segment will post the sharpest 14.32% CAGR as microphone and DSP costs slide beneath USD 30 per vehicle. Manufacturers now pre-pack basic speech control for navigation, music, and calls in entry variants, mirroring the earlier diffusion path of touchscreen head-units.

Mid-segment sedans serve as a technology bridge, offering hybrid processing and over-the-air vocabulary expansions that acclimate mass-market buyers to voice. The democratisation loop is self-reinforcing: rising economy volumes widen data capture for accent fine-tuning, which then improves recognition further and unlocks additional use cases such as micro-commerce even in budget cars.

By Microphone Array Design: Beam-Forming Technology Emerges

Single-mic solutions remain prevalent in small cars owing to minimal hardware and calibration needs. Dual-mic arrays gain share in midsize vehicles where cabin length demands directionality. The most dynamic segment is beam-forming arrays projected to grow at 13.72% CAGR. Suppliers such as Kardome squeeze six-speaker separation into one compact array, eliminating wiring complexity while isolating voice signals in noisy cabins.

HARMAN’s exterior beam-forming mics extend interaction to outside the vehicle, enabling drivers to open trunks or summon parking maneuvers verbally. As price points drop, beam-forming will shift from premium line-ups into mainstream, improving accuracy for occupants in all seat rows and supporting hands-free compliance for legislation targeting rear-seat distraction.

Geography Analysis

North America accounted for 37.10% of 2025 revenue, underpinned by ubiquitous smartphone assistant usage and early embrace of in-car voice commerce. US OEMs bundle food-ordering, fuel-payment, and subscription media inside voice dashboards that expand recurring revenue streams beyond the original sale. Canada accentuates bilingual English-French processing, compelling suppliers to optimise language-switching algorithms. While regional growth cools from earlier highs, upcoming NHTSA driver-impairment mandates create a fresh floor for demand by 2026.

Asia Pacific is the fastest climber, with a 14.78% CAGR that will lift its Automotive Voice Recognition System market share materially by 2031. China’s domestic automakers embed Baidu and Tencent assistants as default user interfaces, leaning on 5G networks to serve generative AI queries. Great Wall Motor’s global expansion program relies on Cerence for multilingual rollout across right-hand and left-hand drive markets. India’s push for regional-language recognition fuels model training runs that raise system robustness worldwide. Japan emphasises elder-friendly features such as medication reminders, shaping inclusive design frameworks exported globally.

Europe maintains steady adoption, driven less by gadget enthusiasm than by safety and privacy regulation. GDPR steers OEMs toward on-device processing or consent-controlled cloud hand-offs, while Euro NCAP’s 2026 rating updates make hands-free control indispensable for touchscreen-heavy interiors. Volkswagen Group’s pan-brand ChatGPT upgrade demonstrates how European players reconcile privacy with AI capability through anonymised, opt-in data flows. Growing demand for multi-language support across 24 official EU tongues also pushes suppliers to invest in accent coverage.

Competitive Landscape

Competition blends consumer-tech titans, automotive Tier-1s, and focused AI startups. Players like Cerence lead with supply deals covering a significant portion of light-vehicle production, leveraging domain-specific acoustic models and OEM toolkits. Tech conglomerates Microsoft, Amazon, and Google enter via Android Automotive OS and Alexa Auto integrations, offering cloud heft but limited car-grade acoustics. Continental, Bosch and HARMAN defend share by fusing microphones, amplifiers and software into turnkey cockpit modules, easing OEM validation cycles.

Strategic mergers intensify: Gentex bought VOXX to marry premium Klipsch audio with its mirror-based electronics, bolstering cabin acoustics critical for high-accuracy voice. SoundHound AI acquired Amelia to deepen natural-language reasoning and cross-sell solutions to automotive and enterprise clients. Startups such as Syntiant and Kardome carve niches in ultra-low-power silicon and beam-forming, respectively, pressuring incumbents to innovate or partner.

As OEMs pivot to software-as-a-service, revenue shifts to post-sale subscriptions. Suppliers able to furnish commerce APIs, OTA upgrade pipelines and data analytics gain long-term contracts. Consequently, the market rewards companies offering both deep acoustic science and cloud-scale monetisation platforms.

Automotive Voice Recognition System Industry Leaders

-

Alphabet Inc.

-

Amazon.com, Inc.

-

Cerence Inc.

-

Harman International (Samsung)

-

Nuance Communications (Microsoft)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: SoundHound AI partnered with Tencent Intelligent Mobility to embed voice commerce and natural-language functions in vehicles across the globe.

- April 2025: Gentex Corporation completed the USD 7.50-per-share acquisition of VOXX International, integrating Klipsch and Onkyo audio with Gentex electronics.

- April 2025: Kia launched a generative-AI voice assistant across Europe, delivering natural conversation and OTA feature drops.

- January 2025: Cerence AI expanded its collaboration with NVIDIA to accelerate CaLLM language-model optimisation using the NVIDIA AI Enterprise stack.

Global Automotive Voice Recognition System Market Report Scope

Automotive voice recognition systems are computer programs and hardware devices used in an automobile to decode the human voice in order to offer a hands-free communication experience to avoid or minimize the driver's distraction while driving the vehicle in the interest of enhanced safety.

The automotive voice recognition system market is segmented by vehicle type, technology, vehicle class, and geography. By vehicle type, the market is segmented into passenger cars and commercial vehicles. By technology, the market is segmented into embedded, cloud-based, and hybrid. By vehicle class, the market is segmented into economy, mid-priced, and luxury. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World.

The report offers size and forecasts for the automotive voice recognition system market in value (USD) for all the above segments.

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Embedded |

| Cloud-based |

| Hybrid |

| Economy |

| Mid-priced |

| Luxury |

| Single-mic |

| Dual-mic |

| Beam-forming mic |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East and Africa | Turkey |

| Saudi Arabia | |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Heavy Commercial Vehicles | ||

| By Technology | Embedded | |

| Cloud-based | ||

| Hybrid | ||

| By Vehicle Class | Economy | |

| Mid-priced | ||

| Luxury | ||

| By Microphone Array Design | Single-mic | |

| Dual-mic | ||

| Beam-forming mic | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Turkey | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Automotive Voice Recognition System market?

The Automotive Voice Recognition System market size stood at USD 5.08 billion in 2026 and is forecast to reach roughly USD 9.86 billion by 2031.

Which vehicle segment is growing the fastest?

Commercial Vehicles are expanding at a 14.62% CAGR as fleet owners adopt voice to cut distraction and streamline dispatch.

How will upcoming Euro NCAP rules affect adoption?

Euro NCAP’s 2026 mandate for physical buttons elevates voice as the safest way to manage secondary tasks, ensuring continued deployment across new models.

What technology architecture is likely to dominate?

Hybrid systems that process simple commands on-device while sending complex queries to the cloud are expected to command the majority share post-2028.

Why are edge-AI chips important for voice?

Falling silicon costs allow large language models to run locally, boosting privacy, lowering latency and enabling reliable service even where connectivity is poor.

Page last updated on: