Biometric Vehicle Access System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.49 Billion |

| Market Size (2030) | USD 2.55 Billion |

| Growth Rate (2025 - 2030) | 11.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Biometric Vehicle Access System Market Analysis by Mordor Intelligence

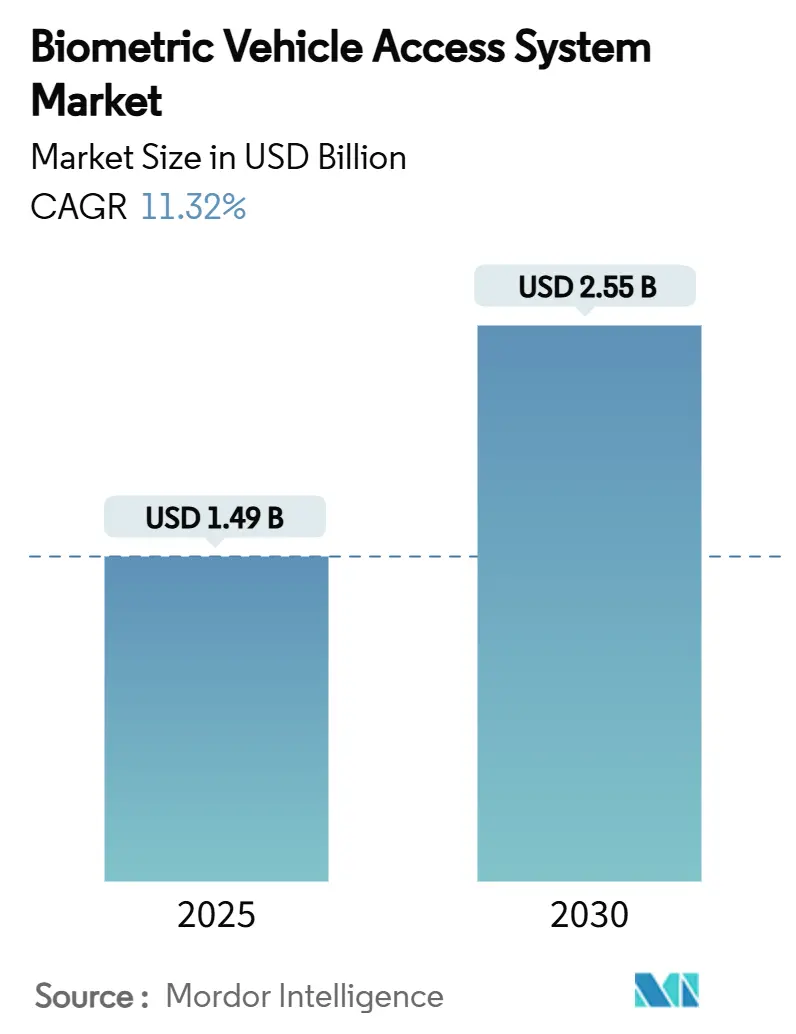

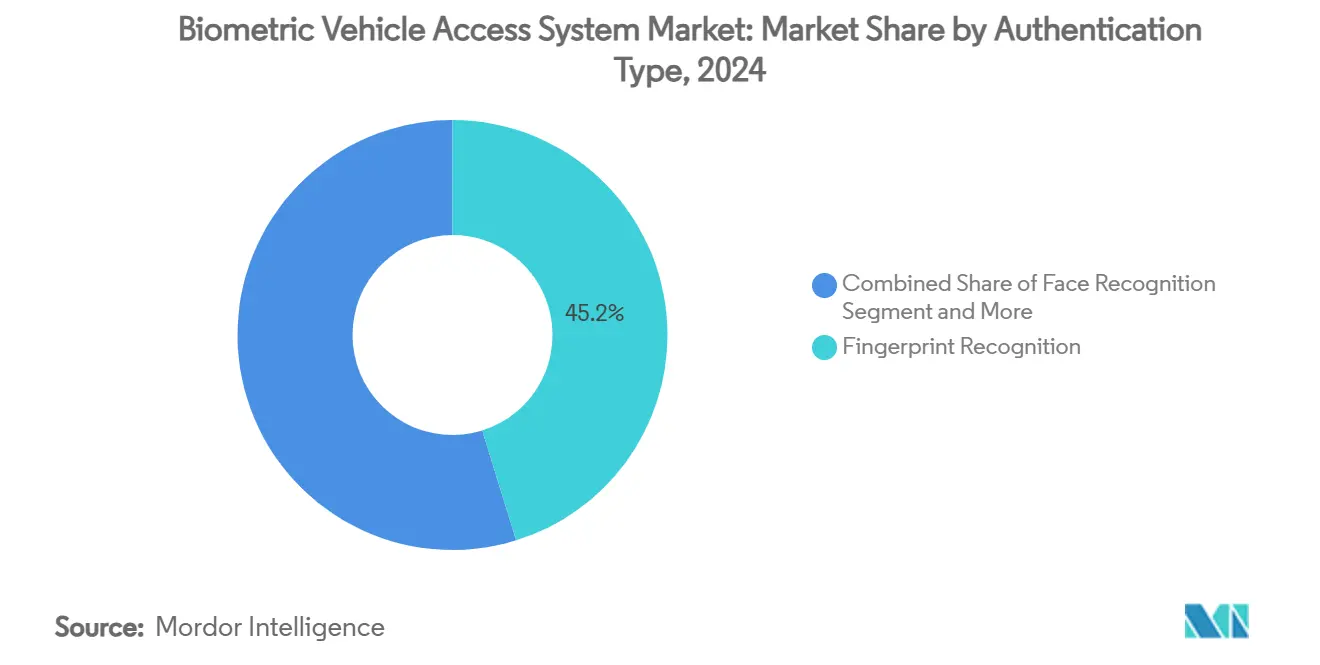

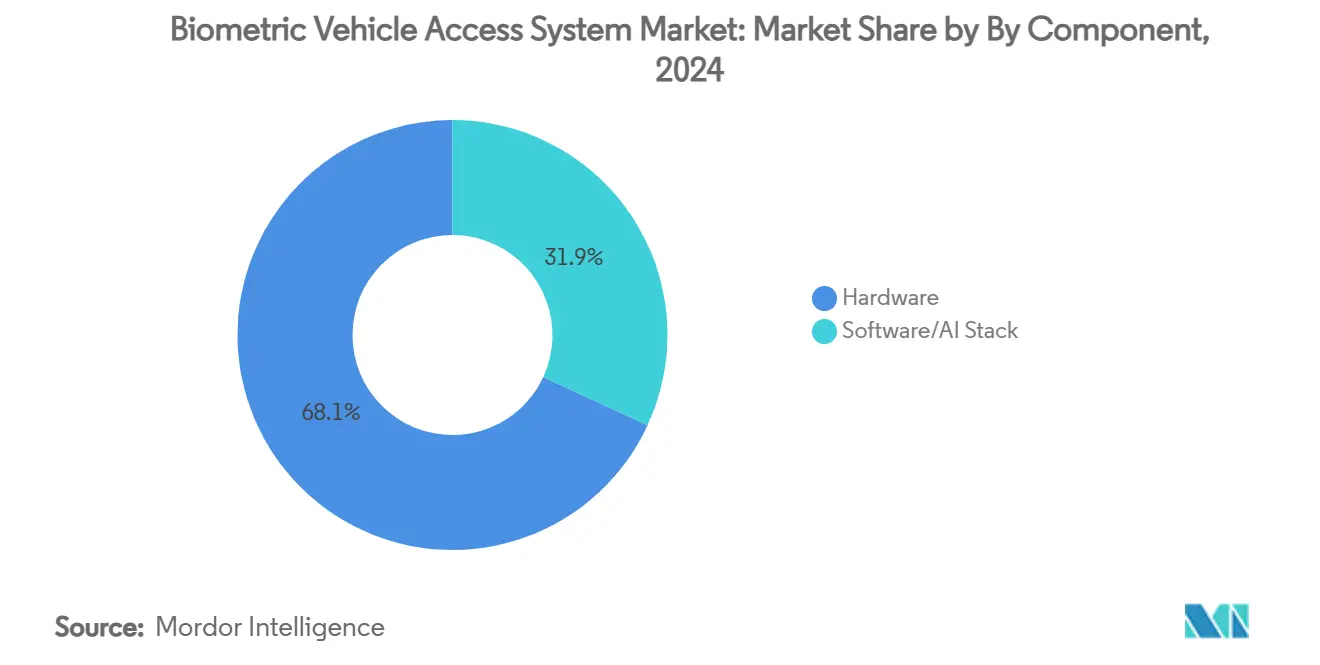

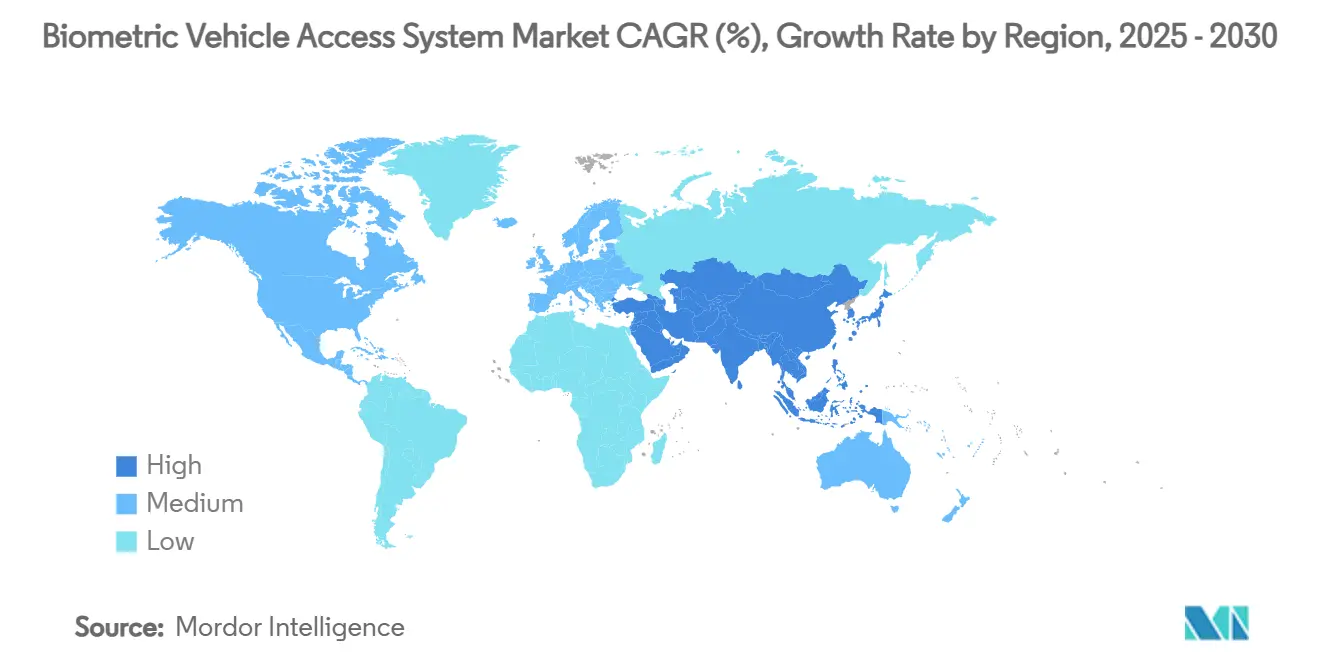

The biometric vehicle access system market size is poised to reach USD 1.49 billion in 2025 and is forecast to register an 11.32% CAGR to USD 2.55 billion by 2030, reflecting rapid adoption of multimodal authentication, falling sensor costs, and the first full model-year subject to ISO/SAE 21434 cybersecurity compliance requirements. Smartphone-class fingerprint and facial sensors, now qualified for −40 °C to +105 °C duty cycles, let automakers migrate from keys to native biometric entry without a price premium, while the same hardware underpins in-car payments and subscription services. Asia-Pacific leads the biometric vehicle access system market with 30.47% revenue share in 2024 and shows the fastest 18.61% CAGR because Chinese OEMs such as BYD and Changan deploy palm-key and facial recognition across mid-tier trims well ahead of Western rivals. Fingerprint recognition retains a 45.23% authentication share; however, iris recognition is gaining the steepest 27.58% CAGR, a signal that premium and commercial fleets are shifting toward higher-security modalities. Hardware modules still deliver 68.08% of 2024 revenues but software and AI stacks expand at 19.76% CAGR as suppliers pivot to over-the-air algorithm upgrades and subscription models.

Key Report Takeaways

- By authentication type, fingerprint recognition led with 45.23% revenue share in 2024; iris recognition is projected to expand at 27.58% CAGR to 2030.

- By vehicle type, passenger cars held 63.14% share of the biometric vehicle access system market size in 2024, while commercial vehicles are advancing at 21.43% CAGR through 2030.

- By component, hardware commanded 68.08% of biometric vehicle access system market share in 2024; the software and AI stack is forecast to grow at 19.76% CAGR up to 2030.

- By sales channel, OEM factory-fit installations accounted for 84.31% share of the biometric vehicle access system market size in 2024, whereas aftermarket retrofit solutions are set to rise at 18.64% CAGR between 2025 and 2030.

- By geography, Asia-Pacific captured 30.47% share in 2024 and is progressing at 18.61% CAGR until 2030.

Global Biometric Vehicle Access System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fingerprint Sensors Common in Mid-Price Cars | +2.8% | Global, with APAC leading adoption | Medium term (2-4 years) |

| OEM Push for Password-Free Payments | +2.1% | North America and EU premium segments | Short term (≤ 2 years) |

| ISO/SAE 21434 Cybersecurity Mandate | +1.9% | Global, mandatory compliance | Short term (≤ 2 years) |

| Tier-1 Biometrics-as-a-Service Models | +1.4% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Multi-Factor Access Pilots in Robotaxis | +0.8% | Urban centers in US, China, EU | Long term (≥ 4 years) |

| Insurance Discounts for MFA Systems | +0.6% | North America and EU markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ubiquity of Smartphone-Class Fingerprint Sensors in Mid-Price Cars

The democratization of capacitive fingerprint sensors from premium smartphones to mid-market vehicles accelerates biometric adoption across price segments previously dominated by traditional key systems. Infineon's October 2024 launch of automotive-qualified fingerprint sensor ICs (CYFP10020A00 and CYFP10020S00) operating from -40°C to +105°C demonstrates the technical maturation required for mass-market deployment[1]"Infineon introduces new fingerprint sensor ICs for identification and authentication in automotive applications," infineon.com. . These sensors integrate with existing microcontroller architectures while providing trackpad functionality, reducing implementation complexity for OEMs targeting cost-sensitive segments. The convergence of consumer electronics supply chains with automotive requirements creates economies of scale that drive sensor costs below USD 5 per unit, making biometric access economically viable for vehicles priced under USD 30,000. This cost trajectory enables mainstream adoption beyond luxury segments, fundamentally expanding the addressable market for biometric vehicle access systems.

OEM Push for Password-Free In-Car Payments

Automotive manufacturers increasingly view biometric authentication as the gateway to recurring revenue streams from in-vehicle commerce, transforming cars into payment platforms that rival smartphone ecosystems. Continental's CoSmA digital key system and Remote Cloud Key solutions demonstrate how biometric verification enables seamless transactions for fuel, parking, and drive-through purchases without requiring physical wallets or mobile device interactions. This strategic shift reflects OEMs' recognition that vehicle access represents the first touchpoint in a broader digital services ecosystem, with biometric authentication providing the security foundation for high-value transactions. Ford's patent filings for facial recognition vehicle entry systems that integrate with payment processing indicate the convergence of access control and financial services within automotive platforms. The revenue potential from transaction fees and data monetization justifies the upfront investment in biometric infrastructure, creating compelling business cases for OEM adoption.

ISO/SAE 21434 Cybersecurity Mandates (2025)

The enforcement of ISO/SAE 21434 cybersecurity engineering standards in 2025 mandates comprehensive risk management frameworks that position biometric authentication as a critical security control for connected vehicles. This regulation requires Cyber Security Management Systems (CSMS) for all new vehicle types, with biometric systems providing multi-factor authentication that addresses both physical access and digital identity verification requirements. The standard's emphasis on lifecycle security management aligns with biometric systems' ability to provide continuous authentication and behavioral monitoring throughout vehicle operation. UN R155 regulation adoption across major automotive markets creates regulatory convergence that eliminates regional compliance variations, accelerating global deployment of standardized biometric solutions. The compliance timeline creates urgency for OEMs to implement biometric systems in 2025 model years, driving immediate market demand and establishing biometric authentication as a baseline security requirement rather than a premium feature.

Tier-1 Suppliers' "Biometrics-as-a-Service" Revenue Models

Traditional automotive suppliers transform from component vendors to service providers through biometric-as-a-service models that generate recurring revenue from software updates, algorithm improvements, and cloud-based authentication services. Bosch's Fleet Management Xtended Access system exemplifies this transition, offering subscription-based vehicle access management that scales across commercial fleets while providing continuous security updates and feature enhancements. This model shift addresses the automotive industry's challenge of capturing value from software-defined vehicle features while providing OEMs with predictable cost structures and suppliers with stable revenue streams. Continental's demonstration of invisible biometrics sensing displays at CES 2025 indicates the evolution toward comprehensive biometric monitoring services that extend beyond access control to include health monitoring and personalization features. The service model enables continuous algorithm refinement and security updates that traditional hardware-only approaches cannot provide, creating competitive advantages for suppliers that successfully transition to software-centric business models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cold-Weather Issues with Budget Fingerprint Readers | -1.2% | Northern regions, Canada, Nordic countries | Short term (≤ 2 years) |

| GDPR & CCPA Data-Privacy Litigation Risk | -0.9% | EU, California, expanding globally | Medium term (2-4 years) |

| No Global Spoof-Testing Standards | -0.7% | Global, affecting premium segments | Medium term (2-4 years) |

| VCSEL Supply-Chain Vulnerability | -0.5% | Global, concentrated in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cold-Weather Reliability Issues for Low-Cost Fingerprint Readers

Temperature-induced performance degradation in capacitive fingerprint sensors creates adoption barriers in cold-climate markets where sensor accuracy drops below acceptable thresholds during winter months. While Infineon's automotive-qualified sensors address this challenge through extended temperature ranges, cost-optimized solutions deployed in mid-market vehicles often lack the thermal compensation required for reliable operation below -20°C. This technical limitation forces OEMs to implement backup authentication methods or restrict biometric functionality during extreme weather conditions, undermining user confidence and adoption rates. The issue particularly affects markets like Canada, Nordic countries, and northern US states where winter temperatures regularly exceed sensor operating limits, creating regional variations in biometric system reliability. Resolution requires either premium sensor components that increase system costs or algorithmic adaptations that maintain accuracy across temperature extremes, both of which impact the economic viability of biometric systems in price-sensitive segments.

Data-Privacy Litigation Risk Under GDPR and CCPA

Biometric data classification as sensitive personal information under GDPR and CCPA creates significant legal exposure for automotive manufacturers, with potential fines reaching 4% of global revenue for non-compliance violations. The trucking industry's experience with biometric privacy litigation under Illinois' Biometric Information Privacy Act (BIPA) demonstrates the financial risks, with recent amendments limiting penalties while requiring explicit written consent for data collection[2]Pamella De Leon, "Mitigating legal risks against collecting truck drivers' biometric data," Commercial Carrier Journal, ccjdigital.com.. Automotive applications face additional complexity due to cross-border data transfers and varying national privacy frameworks, requiring comprehensive data governance systems that increase implementation costs and operational complexity. The litigation risk particularly affects European and California markets where privacy enforcement is most aggressive, potentially creating regional variations in biometric feature availability and functionality. OEMs must balance biometric system capabilities with privacy compliance requirements, often resulting in reduced functionality or increased legal and technical overhead that impacts system economics and user experience.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Authentication Type: Multimodal Integration Drives Premium Adoption

Fingerprint recognition maintains a 45.23% market share in 2024, reflecting the industry's evolution toward higher-security modalities for premium applications. Iris recognition emerges as the fastest-growing authentication segment at 27.58% CAGR through 2030. The growth disparity indicates market bifurcation between cost-optimized fingerprint solutions for mainstream vehicles and sophisticated multimodal systems for luxury and commercial applications where security requirements justify higher implementation costs. Face recognition and voice recognition segments capture smaller but strategically important market shares, particularly in applications requiring hands-free operation or integration with existing infotainment systems. Multimodal and multi-factor authentication (MFA) systems represent the emerging premium segment, combining multiple biometric modalities to achieve security levels suitable for high-value transactions and regulatory compliance requirements.

Continental's CES 2025 demonstration of invisible biometrics sensing displays illustrates the convergence toward integrated multimodal systems that combine facial recognition with vital sign monitoring, creating comprehensive authentication and safety platforms. This integration approach addresses the fundamental limitation of single-modality systems while providing additional functionality that justifies premium pricing. The authentication type segmentation reflects broader automotive trends toward software-defined vehicles where biometric capabilities can be upgraded through over-the-air updates, enabling OEMs to introduce new authentication modalities without hardware changes.

By Vehicle Type: Commercial Fleets Lead Security Innovation

Passenger cars commanded a 63.14% market share in 2024, reflecting fleet operators' prioritization of security, regulatory compliance, and operational efficiency over cost considerations. Commercial vehicles drive the fastest segment growth at 21.43% CAGR. The FMCSA's implementation of biometric identity verification for trucking registrations in 2025 creates mandatory adoption drivers that accelerate commercial vehicle biometric deployment ahead of consumer applications. Fleet applications benefit from centralized procurement decisions and higher vehicle utilization rates that improve biometric system return on investment compared to personal vehicle use cases. Commercial vehicle biometric systems often integrate with fleet management platforms, providing operators with comprehensive access control, driver monitoring, and compliance reporting capabilities that extend beyond simple vehicle access.

The commercial vehicle segment's growth trajectory indicates potential technology spillover to passenger vehicles as biometric systems mature and costs decline through volume production. Bosch's Fleet Management Xtended Access system demonstrates how commercial applications drive technical innovation in areas like remote access management and multi-vehicle authentication that subsequently influence consumer vehicle development. This technology transfer pattern suggests commercial vehicles serve as proving grounds for biometric innovations that eventually reach mainstream passenger car applications.

By Component: Software Intelligence Transforms Hardware Value

Hardware components maintain 68.08% market share in 2024, yet software and AI stack segments achieve the fastest growth at 19.76% CAGR, signaling the industry's transition toward intelligence-driven biometric systems where algorithms create differentiation and value. This growth pattern reflects the commoditization of biometric sensors and the increasing importance of machine learning algorithms for multimodal fusion, spoof detection, and continuous authentication. Software-centric approaches enable over-the-air updates that improve system performance and add new capabilities without hardware modifications, creating ongoing revenue opportunities for suppliers and enhanced functionality for users. The component segmentation evolution mirrors broader automotive industry trends toward software-defined vehicles, where hardware provides the platform for software-delivered features and services.

Infineon's integration of fingerprint sensors with trackpad functionality demonstrates how hardware vendors add software-enabled features to maintain differentiation in increasingly commoditized sensor markets. The software segment's growth trajectory indicates successful biometric implementations will depend more on algorithmic sophistication than sensor hardware specifications, shifting competitive dynamics toward companies with strong AI and machine learning capabilities. This transition creates opportunities for technology companies and software specialists to capture value in traditionally hardware-dominated automotive supply chains.

By Sales Channel: Aftermarket Retrofit Captures Legacy Value

OEM factory-fit installations dominate with 84.31% market share in 2024, while aftermarket and retrofit solutions achieve the fastest growth at 18.64% CAGR, creating parallel market opportunities for integrated and retrofit biometric systems. The aftermarket growth reflects the substantial installed vehicle base that cannot access factory biometric systems but can benefit from retrofit solutions, particularly in commercial fleet applications where security upgrades justify retrofit investments. Retrofit solutions face technical challenges, including integration with existing vehicle electronics and limited access to vehicle data networks, requiring specialized approaches that differ significantly from factory-integrated systems. The sales channel bifurcation suggests distinct market segments with different value propositions, technical requirements, and competitive dynamics.

Continental's Remote Cloud Key system exemplifies retrofit-friendly approaches that provide biometric-enabled access without requiring deep vehicle integration, using Bluetooth and battery power to minimize installation complexity. The aftermarket segment's growth indicates significant pent-up demand for biometric vehicle access among existing vehicle owners, creating market opportunities for suppliers that can develop cost-effective retrofit solutions. This dynamic enables market expansion beyond new vehicle sales to include the much larger population of existing vehicles, substantially increasing the total addressable market for biometric access systems.

Geography Analysis

Asia-Pacific leads both market share at 30.47% in 2024 and growth rate at 18.61% CAGR through 2030 driven by Chinese automakers' aggressive biometric integration and supportive government policies for intelligent vehicle development[3]Jack Shaw, "Biometrics rolling towards relevance for automakers and drivers," Biometric Update, biometricupdate.com.. Government roadmaps for intelligent connected vehicles reference multimodal driver ID as a base layer, so supplier orders ramp quickly when local authorities count the feature toward Level-3 autonomy scoring. Taiwan’s Lextar started volume VCSEL production under AEC-Q102, stabilizing supply for domestic and export builds. The consequence is a reinforcing loop: stronger local supply cuts cost, encouraging wider fit-rates that in turn entice even more capacity.

North America ranks second by revenue, boosted by the FMCSA rule mandating biometric validation on commercial motor-carrier license renewals in 2025, a direct spark for fleet retrofit programs. Detroit OEMs also chase subscription revenues arranged around digital wallets, and US consumers accept pay-at-pump by face because the reference experience already exists on phones. Cold-weather reliability remains a headwind for entry-level trims in the Midwest and Canada, restraining penetration until next-gen sensors work reliably at −30 °C.

Europe advances at a steady clip under twin pressures: ISO/SAE 21434 compliance and premium-segment competition among German marques. GDPR forces local data storage with encryption at rest, steering architecture toward edge AI chips inside the driver-monitoring camera. Tier-1s such as Bosch and Valeo highlight privacy-by-design in marketing, turning what once was a compliance cost into a perceived brand advantage. While overall volumes trail Asia, European unit ASPs sit at the top of the curve because buyers expect seamless MFA tied to digital key sharing with valet or ride-share guests.

Competitive Landscape

The biometric vehicle access system market features mid-level concentration. Continental, Bosch, and Denso each bundle sensors, ECUs, and credential services under long-term nomination contracts. Specialized players like Fingerprint Cards ship capacitive silicon at scale, while Synaptics and Omnitron push photonic ICs aimed at next-gen 3-D imaging. Software-first entrants like Cerence lend voice biometrics that complement physical traits, creating coopetition because Tier-1s license these stacks to fill portfolio gaps.

Strategic plays increasingly revolve around service models rather than hardware cost. Bosch’s Xtended Access sells as a per-vehicle SaaS license that fleets renew annually; Continental’s Invisible Biometrics Sensing Display embeds cameras behind OLED layers, enabling later software unlock of medical-grade vital monitoring. Patent activity intensifies: Ford received new grants for keypad-integrated fingerprint arrays, and GM’s Cruise unit filed claims on gesture-based authentication for driverless pods. M&A tallies up as ASSA ABLOY buys niche badge-reader firms to cross-sell into automotive, while suppliers enter multi-year VCSEL wafer deals with IQE and Lumentum to secure optical inventory.

White-space opportunities include AI-driven liveness detection certified by independent labs, and turnkey retrofit bundles for light-duty fleets that bypass OEM CAN policies. Firms able to scale both cloud credential orchestration and AEC-Q100 hardware stand best placed to consolidate share during the 2027–2028 platform refresh cycle, when most global OEMs launch software-defined architectures.

Biometric Vehicle Access System Industry Leaders

-

Robert Bosch GmbH

-

Continental AG

-

Valeo SA

-

Synaptics Inc.

-

LG Electronics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Continental showcased its Invisible Biometrics Sensing Display at CES 2025, demonstrating advanced in-cabin monitoring capabilities that combine biometric authentication with health monitoring through hidden cameras and laser projectors. The technology represents a significant advancement in integrated biometric systems for vehicles.

- October 2024: Infineon Technologies launched automotive-qualified fingerprint sensor ICs (CYFP10020A00 and CYFP10020S00) with extended temperature ranges from -40°C to +105°C, addressing cold-weather reliability challenges in automotive biometric applications. The sensors meet AEC-Q100 automotive standards and integrate with Infineon's TRAVEO™ T2G microcontroller family.

Global Biometric Vehicle Access System Market Report Scope

| Fingerprint Recognition |

| Face Recognition |

| Iris Recognition |

| Voice Recognition |

| Multimodal/MFA |

| Passenger Cars |

| Commercial Vehicles |

| Hardware |

| Software/AI Stack |

| OEM Factory-Fit |

| Aftermarket/Retrofit |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Authentication Type | Fingerprint Recognition | |

| Face Recognition | ||

| Iris Recognition | ||

| Voice Recognition | ||

| Multimodal/MFA | ||

| By Vehicle Type | Passenger Cars | |

| Commercial Vehicles | ||

| By Component | Hardware | |

| Software/AI Stack | ||

| By Sales Channel | OEM Factory-Fit | |

| Aftermarket/Retrofit | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving the rapid growth of the biometric vehicle access system market?

Heightened cybersecurity regulations, falling sensor costs, and OEM strategies to monetize in-car payments are combining to lift global demand, resulting in an 11.32% CAGR through 2030.

Which region leads the biometric vehicle access system market?

Asia-Pacific commands 30.47% of 2024 revenue and posts the fastest 18.61% CAGR thanks to aggressive deployments by Chinese automakers and supportive policy frameworks.

Why are commercial vehicles adopting biometrics faster than passenger cars?

FMCSA identity-verification rules and fleet insurance discounts create immediate ROI, driving a 21.43% CAGR for commercial vehicle installations.

What challenges could restrain future adoption?

Cold-weather sensor reliability, strict privacy regulations like GDPR and CCPA, and periodic VCSEL supply shortages each exert downward pressure on overall CAGR forecasts.

Are retrofit solutions a viable opportunity?

Yes; aftermarket kits growing at 18.64% CAGR allow fleet operators and used-car dealers to add biometric entry to existing vehicles without OEM support.

Page last updated on: