Automotive Parking Sensors Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

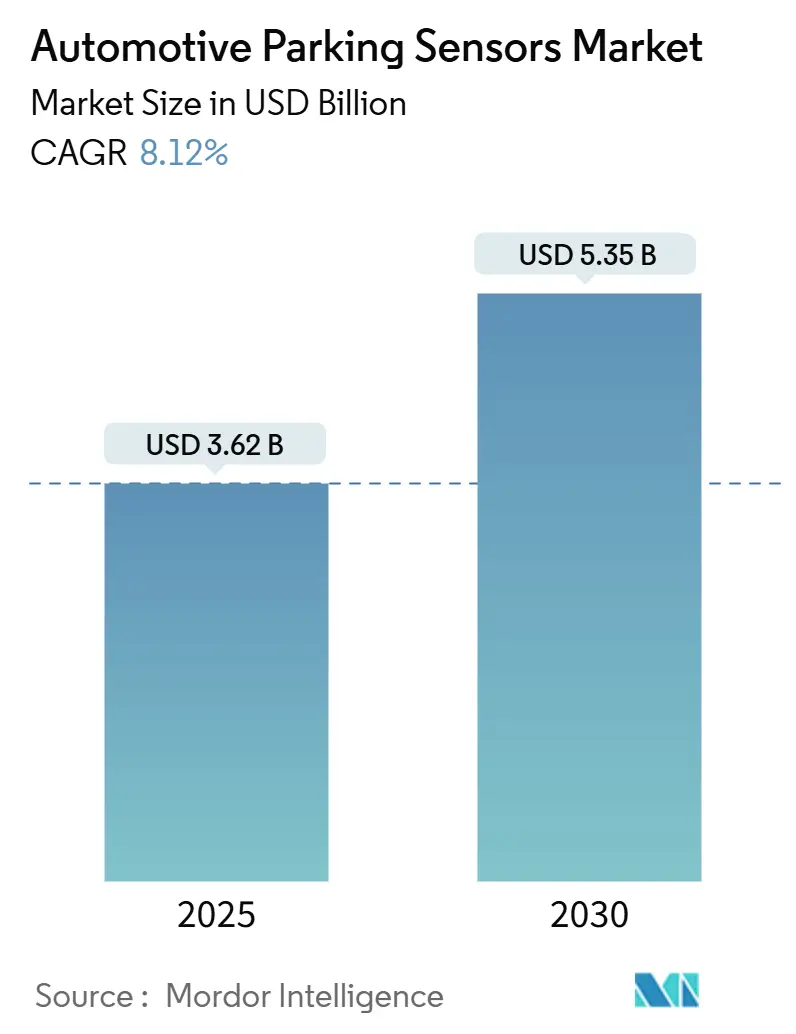

| Market Size (2025) | USD 3.62 Billion |

| Market Size (2030) | USD 5.35 Billion |

| Growth Rate (2025 - 2030) | 8.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

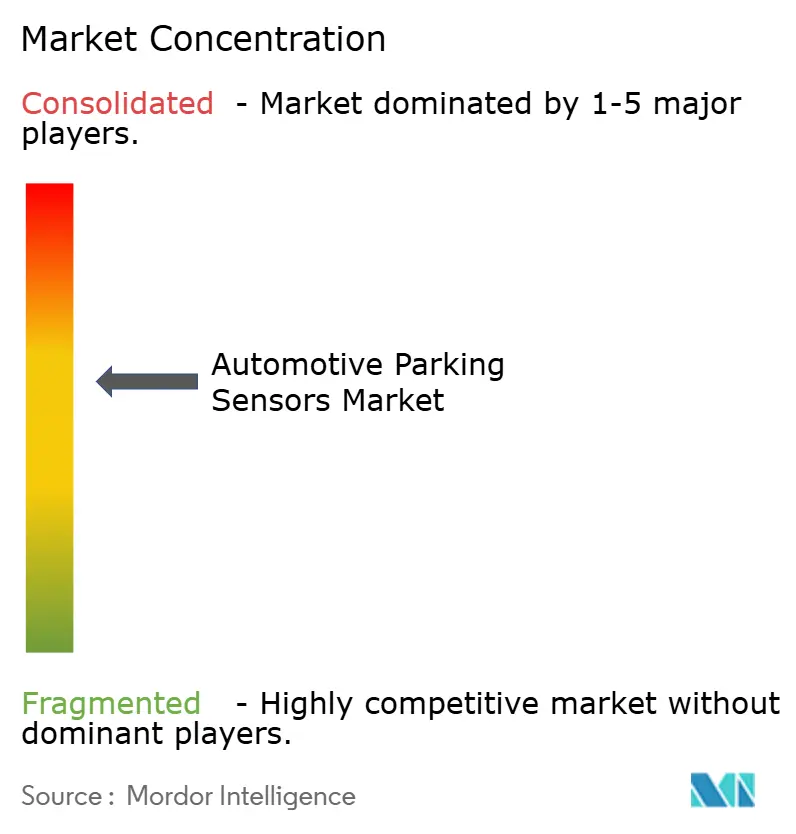

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Parking Sensors Market Analysis by Mordor Intelligence

The automotive parking sensors market stood at USD 3.62 billion in 2025 and is forecast to reach USD 5.35 billion by 2030, translating into an 8.12% CAGR during the forecast period. A convergence of safety‐driven regulations, sensor miniaturization, and software‐defined vehicle architectures is shifting parking sensors from optional accessories to core safety elements inside new-build vehicles. Regulatory mandates in the EU, China, and the United States require sensor-rich advanced driver-assistance systems. At the same time, digital MEMS ultrasonic arrays slash noise floors and simplify wiring harnesses, trimming total system cost. Electric-platform layouts free up bumper real estate, encouraging modular multi-sensor arrays. Scale purchasing by consolidated Tier-1 suppliers compresses unit prices even as insurance telematics reward vehicles that provide park-assist data feeds. These forces collectively reinforce sustained demand growth across the automotive parking sensors market[1]“General Safety Regulation,”, European Commission, europa.eu.

Key Report Takeaways

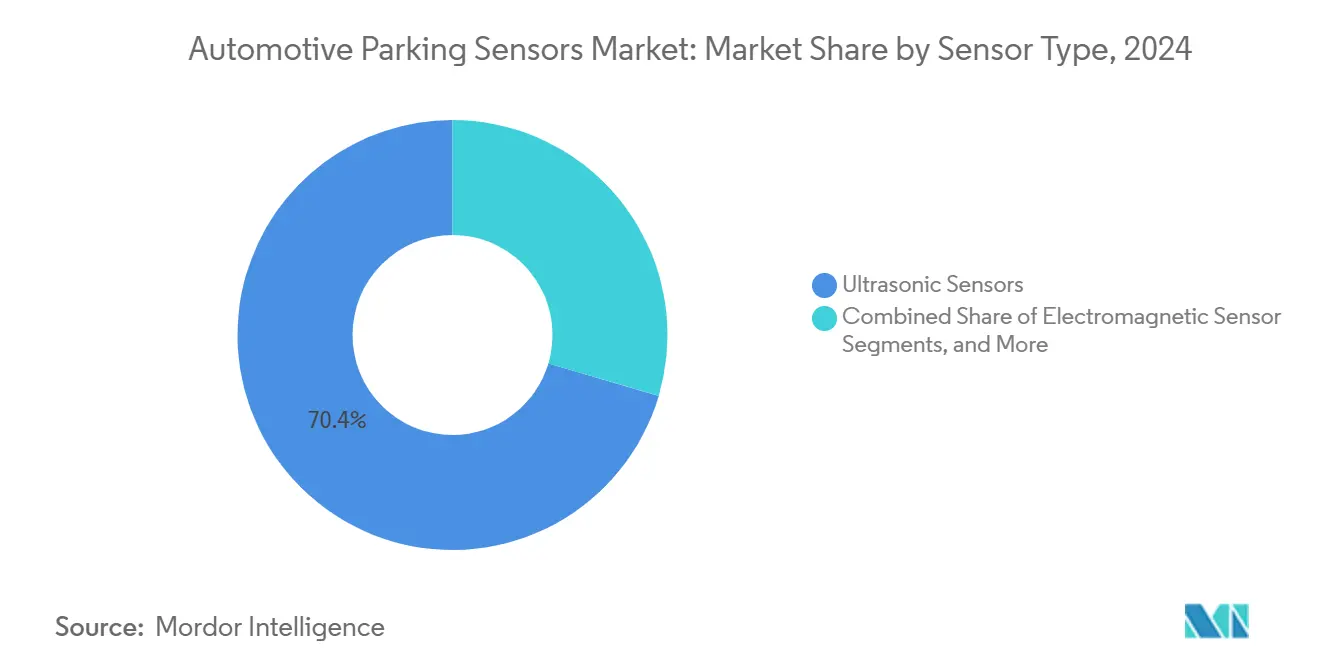

- By sensor type, ultrasonic held 70.42% of the automotive parking sensors market share in 2024, while infrared sensors are forecast to expand at a 10.26% CAGR through 2030.

- By vehicle type, passenger cars dominated with 82.32% of the automotive parking sensors market share in 2024, yet light commercial vehicles are projected to grow at a 9.41% CAGR during the forecast period.

- By product type, rear sensors accounted for 63.72% of the automotive parking sensors market share in 2024, whereas front sensors are tracking an 8.88% CAGR to 2030.

- By distribution channel, OEM installations captured 83.23% of the automotive parking sensors market share in 2024, but the aftermarket is advancing at a 9.12% CAGR across the forecast window.

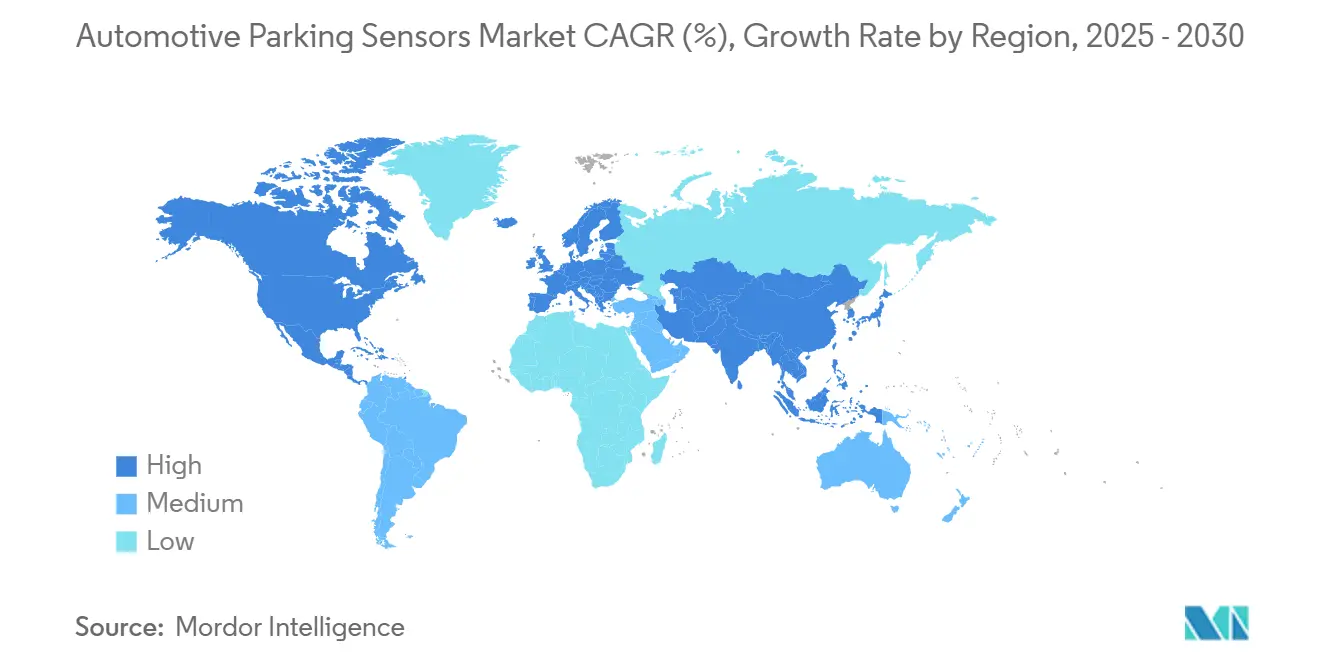

- By geography, Europe led with a 34.28% of the automotive parking sensors market share in 2024, while Asia Pacific is poised for a 9.87% CAGR through 2030.

Market Trends and Insights

Drivers Impact Analysis of Automotive Parking Sensors Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ADAS Mandates Rising in China, Europe and United States | +2.1% | Global, with early adoption in China and Europe | Medium term (2-4 years) |

| OEMs Moving to Digital MEMS Ultrasonic Arrays | +1.8% | Global, led by German and Japanese OEMs | Short term (≤ 2 years) |

| EV Redesigns Free Bumper Space for Modular Sensors | +1.4% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Tier-1 Consolidation Driving Cost Efficiency | +1.2% | Global, concentrated in automotive hubs | Long term (≥ 4 years) |

| Insurance Telematics Favoring Park-Assist Scores | +0.9% | North America and Europe, pilot programs in Asia-Pacific | Medium term (2-4 years) |

| Smart-Curb Laws Requiring Curb-Side Detection | +0.7% | Urban centers globally, led by smart cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging ADAS mandates in China, Europe and Unites States

China’s GB/T 44156-2024 rear-crossing alert rule, the EU General Safety Regulation, and an expected 2025 NHTSA ruling on automatic emergency braking tighten the safety baseline for all new cars. To meet the prescribed performance envelopes, OEMs must integrate multi-sensor fusion setups, including ultrasonic, radar, camera, and infrared. Roughly two-thirds of light vehicles sold in 2024 have already entered markets where at least one of these mandates applied, pushing procurement forecasts upward for the automotive parking sensors market[2]“GB/T 44156-2024,”, Standardization Administration of China, cnis.gov.cn.

Rapid OEM Shift from Analog to Digital MEMS Ultrasonic Arrays

Infineon’s capacitive MEMS ultrasonic transducer shows a 20 × noise reduction and 1,000 × signal-to-noise improvement over legacy piezo-ceramics, enabling detection ranges above 7 meters at centimeter-grade precision. Digital output removes the need for analog shielding, slots neatly into zonal Ethernet backbones, and supports over-the-air firmware updates. OEMs benefit through lighter harnesses, faster assembly, and enhanced self-diagnostics, propelling near-term volume gains for MEMS-based parking sensors[3]“Capacitive MEMS Ultrasonic Transducers,”, Infineon Technologies AG, infineon.com.

Insurance Telematics Rewarding Vehicles with Park-Assist Scores

Usage-based insurance programs in the United States and Europe now factor low-speed collision data and park-assist activation frequencies into premium calculations. Fleet owners gain measurable savings when vehicles carry multi-sensor park-assist suites documenting near-miss events, nudging replacement cycles toward sensor-rich trims. The incentive loops into OEM option-take rates, bolstering the automotive parking sensors market.

Emerging Smart-Curb Regulations Requiring Curb-Side Object Detection

Smart-city ordinances in Tokyo, Barcelona, and Los Angeles pilot curb-side object detection schemes that alert municipal platforms to illegal parking or delivery-zone misuse. Vehicles gain compliance credits when onboard parking sensors wirelessly transmit available curb data, encouraging the installation of lateral-facing ultrasonic and infrared modules. Long-term adoption may broaden regulatory pull across dense urban centers worldwide.

Restraints Impact Analysis of Automotive Parking Sensors Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Auto-Grade Piezo Shortages Persist | -1.9% | Global, acute in Asia-Pacific supply chains | Short term (≤ 2 years) |

| Tariff Swings Inflate Sensor BOM Costs | -1.4% | North America, with spillover to global supply chains | Short term (≤ 2 years) |

| Ultrasonic Degrades in Ice and Heavy Rain | -1.2% | Northern regions, monsoon-affected areas | Medium term (2-4 years) |

| Cyber-Hardening Adds OTA ECU Costs | -0.8% | Developed markets with connected vehicle adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Semiconductor Shortages in Automotive-Grade Piezo Ceramics

Specialized piezo-electric powders and ceramic substrates remain capacity-constrained because only a handful of Asian fabs meet AEC-Q200 temperature and vibration limits. Lead times stretch to 36 weeks for ultrasonic front-end chips, forcing OEMs to lengthen demand forecasts and carry buffer inventory. Qualification of alternative suppliers is slow due to mandatory 2-year reliability cycles, dampening short-term availability for the automotive parking sensors market.

Cyber-Hardening Costs for OTA-Updatable Parking ECUs

Over-the-air calibration unlocks lifecycle revenue but exposes parking ECUs to network attack surfaces that must meet ISO 21434 and UNECE R155 security directives. Extra microcontroller flash, secure boot, and hardware root-of-trust raise bill-of-material cost by roughly USD 1.25 per sensor node, squeezing margins in entry-level segments until volumes scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Automotive Parking Sensors Market Segment Analysis

By Sensor Type:

Digital MEMS Anchors Ultrasonic LeadershipUltrasonic sensors retained a 70.42% share of the automotive parking sensors market in 2024, thanks to proven robustness, low unit cost, and standardized CAN messaging. Introducing MEMS-based capacitive designs accelerates performance gains, pushing detection ranges to 7 meters while shrinking package footprint to 6 × 4 millimeters. The segment’s broad adoption ensures economies of scale that defend pricing even under raw-material inflation. Over the forecast period, the market size of the ultrasonic modules' automotive parking sensors will expand alongside heightened fitment rates in compact and mid-size cars.

Infrared technology is small today, yet it logged a 10.26% CAGR trajectory that outpaces other modalities. Price erosion in long-wave infrared imagers and tighter low-light detection mandates form the springboard for growth. Tier-1 suppliers now bundle thermopile arrays with standard ultrasonic to create dual-mode front and corner modules, easing OEM integration. Electromagnetic sensing remains niche but finds loyal aftermarket followers because magnetic kits can be installed without drilling painted bumpers. Technology convergence drives renewed interest in mixed-sensor pods that pool redundant data through zonal controllers, reinforcing demand breadth across the automotive parking sensors market.

By Vehicle Type:

Commercial Electrification Accelerates LCV UptakePassenger cars controlled an 82.32% share of the automotive parking sensors market in 2024, driven by the rising standardization of rear sensors on entry models and 360-degree suites on premium trims. Nevertheless, light commercial vehicles post the fastest 9.41% CAGR through 2030, as parcel fleets electrify under European CO₂ caps and United States incentives. Electric last-mile vans require precise curb detection and automated park-lock to comply with dense urban delivery norms, lifting sensor count per vehicle.

Medium and heavy trucks display steady adoption as safety regulators mandate blind-spot coverage, yet their absolute volumes lag car segments. Forward-facing ultrasonic pods mounted in bumper steps, coupled with side radar, reduce low-speed dock collisions, trimming downtime costs for fleet managers. Ride-hail robo-taxi pilots also call for high-reliability sensor arrays that endure 20-hour duty cycles, widening the vehicle-type footprint for the automotive parking sensors market.

By Product Type:

Front Sensors Gain MomentumRear sensors held a 63.72% share of the automotive parking sensors market in 2024 because reversing collisions remain among the most frequent insurance claims. Standard inclusion on A- and B-segment hatchbacks cements volume leadership. Front sensors, however, carry the highest 8.88% CAGR through 2030 as urban congestion compels tighter curb maneuvers and automated valet parking features migrate downmarket. New models increasingly link front ultrasonics with forward camera fusion for curb height estimation, preventing wheel-rim damage.

Corner and side sensors emerge as discrete SKUs in electric pickup designs with wide fender flares and tall ride heights. Aptiv’s Parking Cube, which merges radar and camera in a single fascia pod, exemplifies product innovation that may redirect share away from stand-alone ultrasonic sets and expand the overall automotive parking sensors market size.

By Distribution Channel:

Aftermarket Proves ResilientOEM channels commanded 83.23% share of the automotive parking sensors market in 2024 because regulatory compliance drives factory-fit sensor adoption across nearly all trim levels. Automakers prefer integrated solutions validated under full-vehicle duty cycles, locking in Tier-1 suppliers for years. Still, the aftermarket grew at a CAGR of 9.12% through 2030, as aged vehicles require collision-damage replacement or retrofit upgrades to maintain resale value.

Independent repair shops leverage plug-and-play harness adapters and mobile programming tools, lowering labor barriers. Rising electronic complexity does cap do-it-yourself replacements, yet professional installers capture the gap, ensuring a durable aftermarket revenue channel within the automotive parking sensors market.

Geography Analysis

Europe Automotive Parking Sensors Market

Europe led the automotive parking sensors market in 2024 with a 34.28% revenue share, reflecting strict EU General Safety rules and premium vehicle concentration. German OEMs spearhead sensor fusion R&D, issuing paint-thickness bulletins for optimal ultrasonic performance, while France and Italy push smart-curb pilot zones in city centers. National subsidies for electric vans propel sensor counts upward because urban low-emission zones require automated parking aids for delivery vehicles. Rising retrofit demand for twelve-year-old vehicle fleets further sustains aftermarket sales in the region.

APAC Automotive Parking Sensors Market

Asia-Pacific is the fastest-growing cluster at a 9.87% CAGR to 2030, primarily due to China’s ambition to have 30% of 2025 new cars reach Level 3 automation. Domestic makers such as AUDIOWELL ramp up the capacity of ultrasonic pieces for local assembly plants. Japanese and Korean suppliers contribute semiconductor and packaging expertise, enabling cost-competitive exports to ASEAN production hubs. Government incentives for domestic semiconductor fabrication mitigate part of the global shortage risk, supporting smoother shipment schedules.

North America Automotive Parking Sensors Market

North America presents a mixed outlook. Consumers favor pickup trucks and SUVs that necessitate higher sensor density for elevated ride heights, boosting average selling prices. However, tariff volatility on imports from Asia threatens bill-of-material predictability. Manufacturers leverage the USMCA framework to localize final assembly in Mexico, sidestepping select duties but incurring re-qualification costs. Large vehicle parc volumes and high collision repair rates ensure replacement-cycle demand underpins the automotive parking sensors market even during tariff turbulence.

Competitive Landscape

The market exhibits moderate concentration. Continental pairs ultrasonic transducers with model-based parking algorithms capable of over-the-air updates, tightening OEM lock-in. Bosch exploits in-house semiconductor fabs for vertical integration, trimming sourcing risks when global chip supply tightens.

New entrants seek differentiation through fusion modules. Aptiv’s Parking Cube unites radar and camera in one component that competes with multi-ultrasonic arrays, addressing bumper-space constraints in EVs. Waymo’s granted patent for street-parking detection injects intellectual-property barriers that can be licensed to automakers deploying robo-taxi services, nudging the landscape toward software royalty models.

Supplier alliances continue to grow. Continental’s 2024 partnership with NOVOSENSE broadens ASIC sourcing while meeting ASIL-B functional safety, demonstrating how cross-border cooperation tempers geopolitical supply risks. Hyundai, Infineon, and Valeo each opened regional innovation labs during 2025 to co-create diagnostic standards for sensor health reporting, deepening ecosystem interdependence, and fortifying entry barriers for latecomers.

Automotive Parking Sensors Industry Leaders

Robert Bosch GmbH

Continental AG

Valeo SA

Denso Corporation

ZF Friedrichshafen AG

- *Disclaimer: Major Players sorted in no particular order

Automotive Parking Sensors Market Companies Covered in this Report

- Robert Bosch GmbH

- Continental AG

- Valeo SA

- Denso Corporation

- ZF Friedrichshafen AG

- Aptiv PLC

- HELLA GmbH & Co. KGaA

- Texas Instruments Inc.

- NXP Semiconductors N.V.

- Infineon Technologies AG

- Sensata Technologies Inc.

- TE Connectivity Ltd.

- Murata Manufacturing Co., Ltd.

- Panasonic Holdings Corp.

- Magna International Inc.

- Autoliv Inc.

- Hitachi Astemo Ltd.

- OMRON Corporation

- TDK Corporation

- Elmos Semiconductor SE

Recent Industry Developments in Automotive Parking Sensors Market

- June 2025: Valeo Group will begin supplying its Valeo Smart Safety 360 (VSS360) ADAS solution to a European premium OEM in 2026. The system includes radars, cameras, ultrasonic sensors, and computer vision technology, with radar fused into the front camera and a Parking ECU enabling hands-free parking.

- January 2025: Texas Instruments (TI) launched integrated automotive chips that enhance driving safety across all vehicle segments. The company's AWRL6844 60GHz mmWave radar sensor performs occupancy monitoring, including seat belt reminders, child presence detection, and intrusion detection. The single-chip solution incorporates edge AI algorithms to improve vehicle safety features.

Global Automotive Parking Sensors Market Report Scope

Segmentation Overview

| Ultrasonic Sensors |

| Electromagnetic Sensors |

| Infrared Sensors |

| Passenger Car |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Front Parking Sensors |

| Rear Parking Sensors |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Sensor Type | Ultrasonic Sensors | |

| Electromagnetic Sensors | ||

| Infrared Sensors | ||

| By Vehicle Type | Passenger Car | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Product Type | Front Parking Sensors | |

| Rear Parking Sensors | ||

| By Distribution Channel | Original Equipment Manufacturer (OEM) | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the automotive parking sensors market by 2030?

The market is forecast to reach USD 5.35 billion by 2030, reflecting an 8.12% CAGR from 2025.

Which sensor technology leads current installations?

Ultrasonic sensors command 70.42% of total 2024 shipments due to proven reliability and low cost.

Why are light commercial vehicles a high-growth opportunity?

Fleet electrification mandates and last-mile delivery optimization push LCV parking sensor demand at a 9.41% CAGR through 2030.

How do tariffs affect North American sensor costs?

Import duties of up to 25% on assemblies and 50% on certain semiconductors inflate landed costs, encouraging production shifts to USMCA-compliant plants.

How does MEMS technology improve parking sensors?

Digital capacitive MEMS ultrasonic transducers cut noise floors by 20 × and enable Ethernet connectivity, reducing wiring and boosting diagnostic capabilities.

Page last updated on: