Automotive Pump Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 12.35 Billion |

| Market Size (2030) | USD 14.85 Billion |

| Growth Rate (2025 - 2030) | 3.76% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Pump Market Analysis by Mordor Intelligence

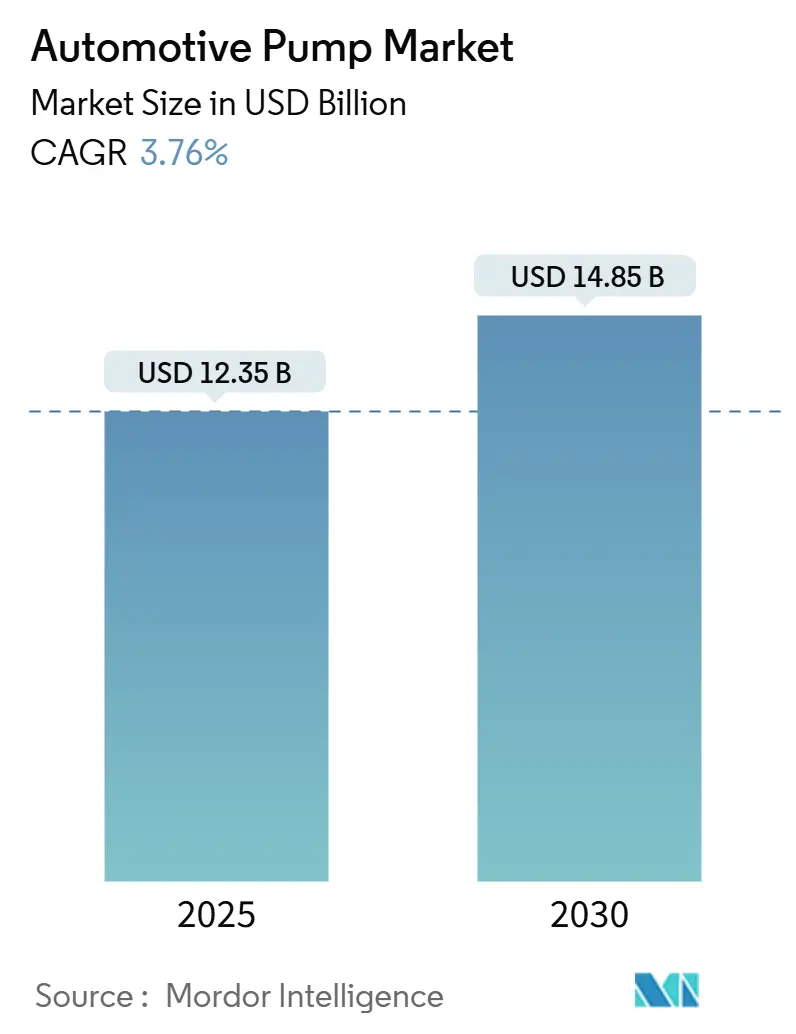

The automotive pump market size stands at USD 12.35 billion in 2025 and is forecast to reach USD 14.85 billion by 2030, translating into a 3.76% CAGR for the assessment period. This steady advance captures the industry’s migration from mechanically driven to electrically controlled pumps, a shift propelled by tightening global emissions regulations, electrified powertrains, and rising vehicle software content. Suppliers that master electric-pump integration into vehicle thermal networks are gaining pricing power, even as mechanical pumps remain entrenched in cost-sensitive segments. The Asia-Pacific production surge, expanding turbo-hybrid powertrains, and OEM demand for modular thermal packages will keep the automotive pump market on a predictable upward trajectory. System consolidation, predictive diagnostics, and new hydrogen internal-combustion pilots add incremental opportunity layers that temper the industry’s otherwise moderate growth pace.

Key Report Takeaways

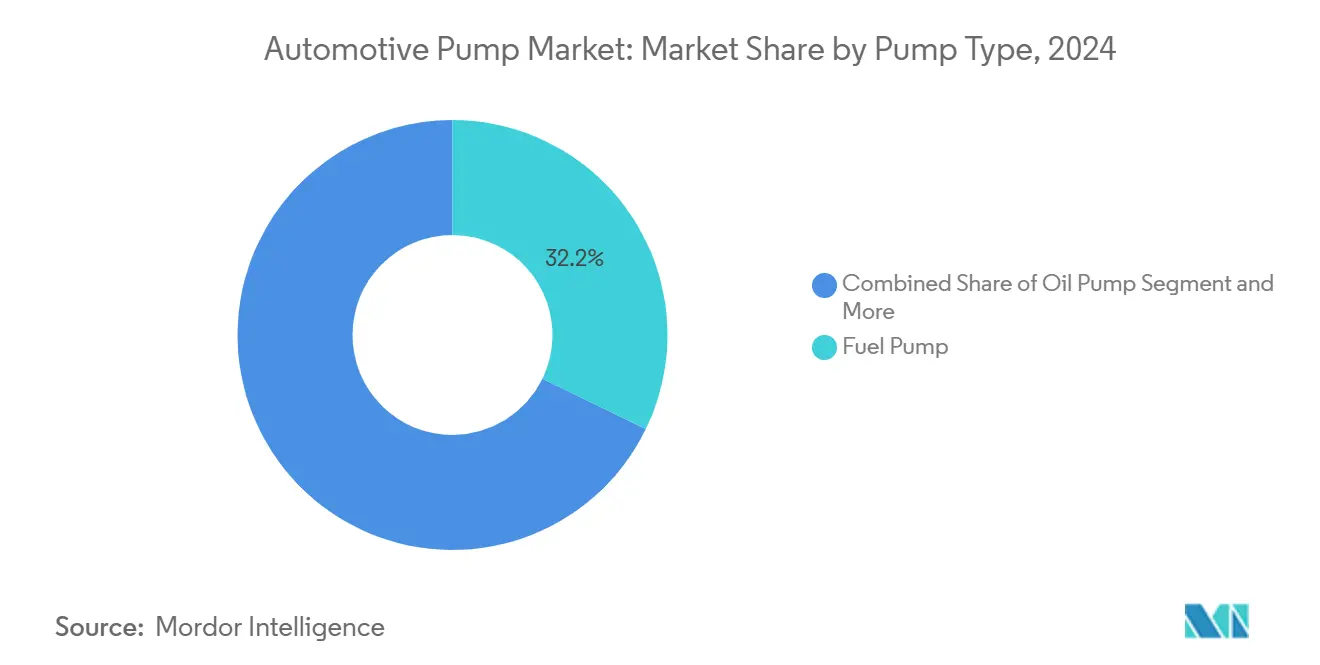

- By pump type, fuel pumps led with a 32.15% of the automotive pump market share in 2024; water pumps are projected to expand at a 4.62% CAGR through 2030.

- By technology, mechanical pumps held 69.33% of the automotive pump market share in 2024, while electric pumps are on course for a 6.14% CAGR to 2030.

- By vehicle type, passenger cars accounted for 49.55% of the automotive pump market share in 2024, and medium and heavy commercial vehicles are set to advance at a 5.25% CAGR through 2030.

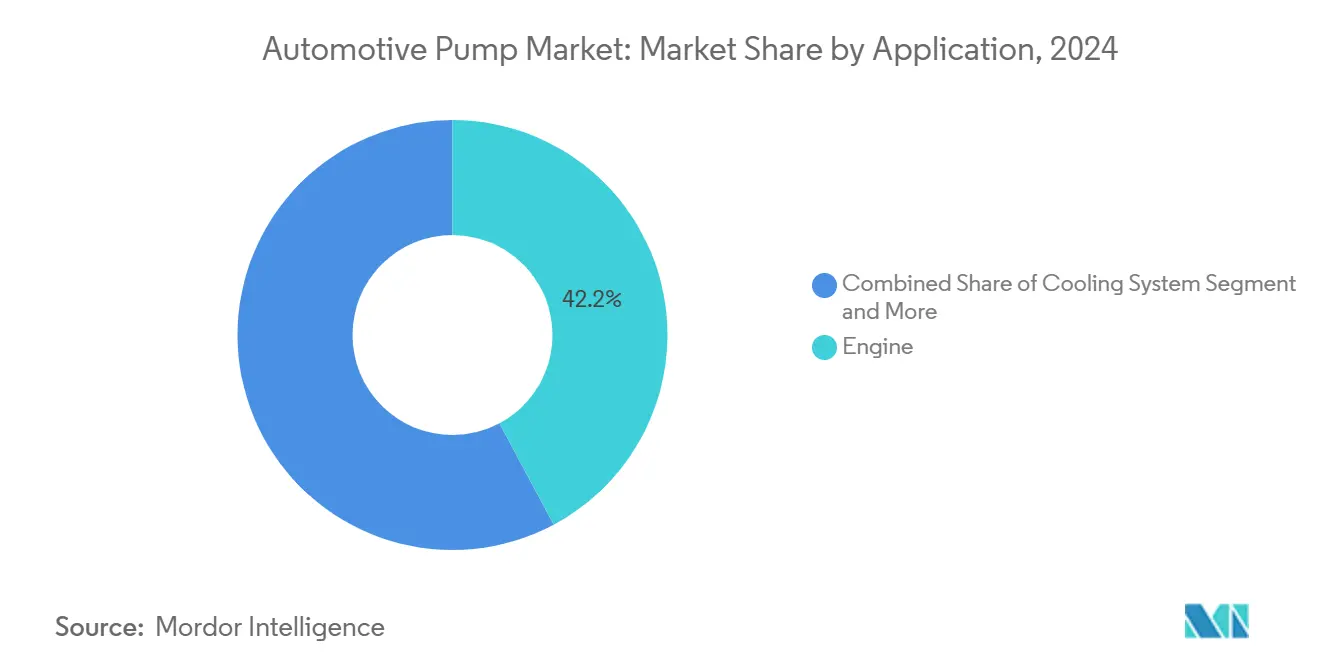

- By application, engine applications captured 42.17% of the automotive pump market share in 2024; cooling systems are forecast to grow at a 5.73% CAGR to 2030.

- By sales channel, the OEM channel dominated with 74.26% of the automotive pump market share in 2024 while growing at a 3.95% CAGR toward 2030.

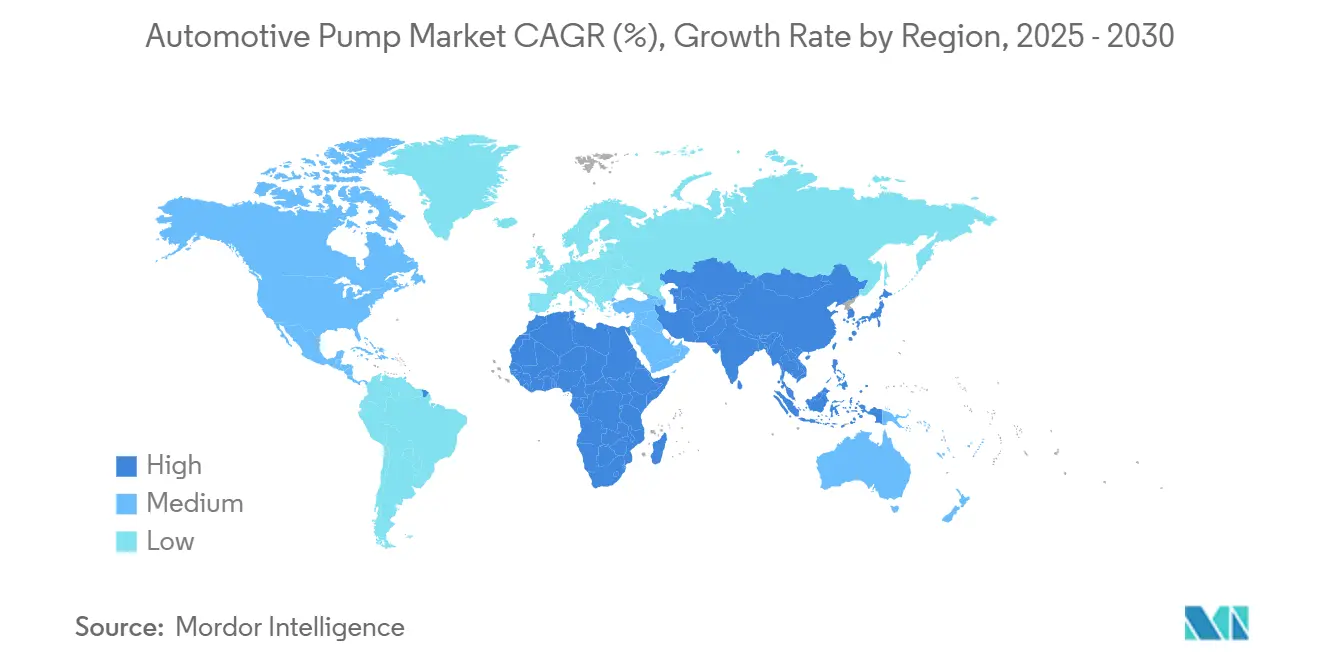

- By geography, Asia-Pacific led with a 45.11% of the automotive pump market share in 2024 and is positioned to expand at a 4.15% CAGR through 2030.

Global Automotive Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global CO₂ / CAFÉ Norms Tighten | +1.2% | Global, strongest in EU and North America | Medium term (2-4 years) |

| Asia-Pacific Production Ramps Up | +0.9% | Asia-Pacific core, global spill-over | Short term (≤ 2 years) |

| Turbo-Hybrid Engines Demand High-Pressure Pumps | +0.8% | Global, notably Asia-Pacific and North America | Medium term (2-4 years) |

| OEMs Prefer Integrated Pump Packages | +0.6% | Global, led by Europe and North America | Long term (≥ 4 years) |

| Smart Sensor Integration Enables Maintenance | +0.4% | Global, early uptake in premium segments | Long term (≥ 4 years) |

| Hydrogen Pilots Drive Ultra-High-Pressure Pumps | +0.2% | Europe and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tightening Global CO₂ / CAFÉ Norms Accelerating E-Pump Adoption

Regulators in the United States and European Union continue to ratchet down fleet-average CO₂ targets, compelling OEMs to harvest every reliable gram of emissions reduction[1]“Multi-Pollutant Emissions Standards for Model Years 2027 and Later,” Environmental Protection Agency, federalregister.gov. Electric pumps enable on-demand fluid delivery, reduce parasitic losses, and extend stop-start engine dwell times, yielding measurable fuel-economy gains inside test cycles. With legacy “off-cycle” credits being phased out in the early 2030s, compliance now hinges on hardware that proves its worth during certification runs instead of spreadsheet accounting. As global vehicle platforms converge, e-pump specifications validated for one jurisdiction increasingly cascade worldwide, creating a multiplier effect for suppliers already with high-efficiency electric offerings.

Rapid Ramp-Up of Asia-Pacific ICE and EV Production Capacity

In December 2024, retail sales of passenger vehicles (PVs) in China hit 2.635 million units, marking a 12% increase from the previous year and an 8.7% rise from the prior month, as reported by the China Passenger Car Association (CPCA), and ASEAN’s infusion of Chinese OEM investments underpins Asia-Pacific’s market share leadership. New factories are being designed with dual-architecture flexibility, enabling seamless switching between internal-combustion and battery-electric models. This volume expansion compresses development calendars and incentivizes local sourcing of high-value pump modules, benefiting suppliers that can stand up green-field lines quickly while meeting stringent PPAP and software-integration requirements.

Shift Toward Power-Dense Turbo-Hybrid Engines Demanding High-Pressure Fuel and Oil Pumps

Engine downsizing, turbocharging, and hybrid assist elevate fuel-injection pressures above 350 bar and mandate rapid oil circulation during frequent start-stop events. Bosch has fielded pump families rated up to 500 bar, while Toyota’s 2.4 L turbo-hybrid program underscores how robust lubrication and cooling solutions must now coexist inside tighter engine bays[2]“Flexible Thermal Unit: Integrated Thermal Management for Passenger Cars,” Bosch Mobility, bosch-mobility.com. The thermal loads generated by turbo-hybrid architectures also accelerate demand for variable-speed coolant pumps that adapt flow rates in milliseconds, mitigating hotspots and safeguarding turbocharger bearings throughout aggressive duty cycles.

OEM Preference for Integrated, Modular Pump Packages

Vehicle manufacturers increasingly seek plug-and-play thermal modules integrating pumps, valves, heat exchangers, and control systems into compact, efficient units. Solutions like Bosch’s and Tuopu’s modular assemblies reflect this trend, helping reduce assembly time and minimize the risk of fluid leaks. This system-level integration enables more innovative thermal management, lighter wiring, and streamlined inventory. However, it also raises the bar for suppliers; those lacking expertise in electronics or fluid systems may struggle to compete, as contracts increasingly favor single-source providers capable of delivering complete, integrated thermal solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Upfront Cost Delta Of Electric Pumps | -0.7% | Global | Short term (≤ 2 years) |

| Aluminum Volatility Inflating Pump Costs | -0.5% | Global | Short term (≤ 2 years) |

| Decline In European Diesel Vehicles | -0.4% | Europe | Medium term (2-4 years) |

| Counterfeit Parts Increase Recall Exposure | -0.3% | Global, concentration in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Upfront Cost Delta of Electric Versus Mechanical Pumps

Electric pumps with advanced components like brushless motors, controllers, and sensors cost more than traditional mechanical systems. This added cost poses challenges for entry-level vehicles, potentially straining budget targets and hindering adoption. However, benefits such as emissions credits or diminished warranty expenses might mitigate these challenges. Service channels face resistance, as vehicle owners often shy away from high replacement costs, leading them to favor simpler mechanical assemblies in the aftermarket. Yet, with the declining costs of power electronics and mounting regulatory pressures on emissions, the economic rationale for electric pumps is poised to strengthen, even as affordability presents a short-term hurdle.

Global Aluminum Price Volatility Inflating Pump Housing Costs

Pump suppliers face significant vulnerabilities due to aluminum's dominant role in material costs. Unpredictable fluctuations in aluminum prices can drastically squeeze margins, compelling die-casting operations to hedge or renegotiate contracts, mid-cycle actions that come with their own financial and scheduling risks. During supply shortages, engineering teams frequently scramble to validate alternative alloys, which can incur expensive retooling and testing expenses. Such volatility underscores the strategic importance of multi-material designs and additive manufacturing pilots, providing enhanced flexibility and resilience against supply chain disruptions while maintaining structural performance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pump Type: Fuel Dominance Meets Water-Pump Momentum

Fuel pumps retained the lead with 32.15% revenue share in 2024 as direct-injection systems multiplied across turbo-hybrid programs. The automotive pump market size attributed to water pumps is narrowing the gap, expanding at a 4.62% CAGR due to battery thermal loops and electric turbocharger cooling circuits. In emerging economies, carbureted two-wheelers still demand low-pressure fuel pumps, sustaining baseline volume even as global electrification advances. Water-pump suppliers are responding with brushless DC designs rated for 30,000-plus hours of fault-free service, a metric crucial for warranty alignment in EV platforms.

Oil pumps leverage variable-displacement architectures that curtail parasitic losses during idle phases and high-vacuum conditions. Vacuum pumps, once tied to diesel brake-boost assist, now find renewed purpose in gasoline hybrids that lack manifold vacuum at shut-off. Specialty niches like hydrogen-injection pumps and e-axle coolant loops are small today but signal technical pathways for next-generation offerings. The diversification compels portfolio breadth, positioning multi-technology vendors to capitalize on the full automotive pump market opportunity.

By Technology: Mechanical Stronghold Faces Electric Surge

Mechanical solutions still command 69.33% share, anchored by cost effectiveness and minimal electrical-architecture dependence. Yet electric pumps are advancing at a 6.14% CAGR, a trajectory that will erode the mechanical advantage over the forecast horizon. Brushless motors coupled with micro-controller units deliver fine-grained flow control, enabling thermal management efficiencies unachievable with belt-driven designs.

Safety protocols for high-voltage environments now embed ISO 26262 diagnostics directly into pump firmware, broadening the addressable scope of electric units for both coolant and oil circulation. Conversely, mechanical pumps endure in commercial diesel programs where durability under severe duty cycles remains paramount. Over time, hybrid architectures will retain select mechanical pumps for fail-safe redundancy, ensuring a measured rather than abrupt technology crossover inside the automotive pump market.

By Vehicle Type: Passenger Car Scale Meets Commercial-Vehicle Acceleration

Passenger cars dominated 2024 volume at 49.55%, buoyed by strong compact-SUV demand in China, India, and the United States. Medium and heavy commercial vehicles register the fastest 5.25% CAGR, driven by stringent 2027 U.S. heavy-duty emissions rules that require high-efficiency thermal subsystems. Battery-electric delivery vans present unprecedented cooling loads, requiring dual-circuit coolant pumps capable of servicing battery packs and inverters.

Off-highway equipment such as agricultural tractors and mining haulers adds ruggedized pump demand that values corrosion-resistant castings and extended seal life. Two-wheeler programs, though less revenue-intensive, reward compact form factors and cost-optimized brushless designs. Collectively, diverse vehicle categories keep the automotive pump market resilient to any single powertrain trajectory.

By Application: Engine Share Holds While Cooling Systems Outpace

Engine-mounted pumps delivered 42.17% of 2024 turnover, encompassing fuel, oil, and hybrid vacuum functions. Cooling systems logged the highest 5.73% CAGR because lithium-ion battery packs, power electronics, and turbo-compressors each require dedicated coolant circuits. Transmission pumps benefit from growing dual-clutch and planetary-automatic adoption, particularly in Asia-Pacific mid-size SUVs.

HVAC heat-pump modules for electric cars introduce new low-temperature coolant loops, spawning incremental pump volume that augments traditional refrigerant circulation. Emerging applications such as hydrogen fuel-cell stack cooling contribute small but strategically significant orders that seed expertise for future product lines, broadening the automotive pump market footprint in thermal innovation.

By Sales Channel: OEM Integration Sustains Dominance

The OEM channel captured 74.26% of 2024 revenue and expected to witness growth of 3.95% CAGR, reflecting automakers’ tighter control over supplier ecosystems and preference for pre-validated modules during platform design. Automotive pump market share held by aftermarket distributors remains in decline as component reliability lengthens replacement intervals. Counterfeit part exposure further redirects repair traffic to OEM-branded pumps with verified lineage and software compatibility.

Tier-1 suppliers leverage digital twins and co-simulation with OEM engineering hubs, cementing early-stage design-in advantages that the aftermarket cannot replicate. Forward-looking vendors pursue service revenue through predictive-maintenance analytics, yet these initiatives still route data through OEM telematics backbones, reinforcing original-equipment primacy.

Geography Analysis

Asia-Pacific held a 45.11% share in 2024 and is advancing at a 4.15% CAGR through 2030, powered by China’s quarterly output above 2.7 million units and India’s plan for 3 million additional annual capacity. Large-scale battery and engine programs across Thailand and Indonesia amplify demand for both electric and mechanical pumps, making local sourcing indispensable for cost and logistics control. Suppliers that combine flexible manufacturing with region-specific validation protocols are best positioned to ride this volume wave.

North America commands premium margins on the back of light-truck and SUV popularity, segments that require multiple high-capacity pumps for transmission, torque-converter, and auxiliary cooling tasks. The EPA’s 2027 emissions framework is accelerating electric-pump uptake in gasoline and diesel models, adding technology upside even as overall vehicle output grows at a modest pace. Europe is pivoting rapidly from diesel to electrified architectures, increasing per-vehicle pump counts despite flat registrations, while real-world driving-emission rules keep electric coolant pumps in sharp focus.

South America and the Middle East & Africa together contribute a smaller but rising slice of global demand. Brazil’s auto-sector rebound and Saudi Arabia’s green-field assembly projects stimulate early-cycle orders dominated by cost-optimized mechanical pumps. Currency volatility and supply-chain complexity remain challenges, yet gradual alignment with global emissions standards should pave the way for higher-value electric and smart-pump solutions over the forecast horizon.

Competitive Landscape

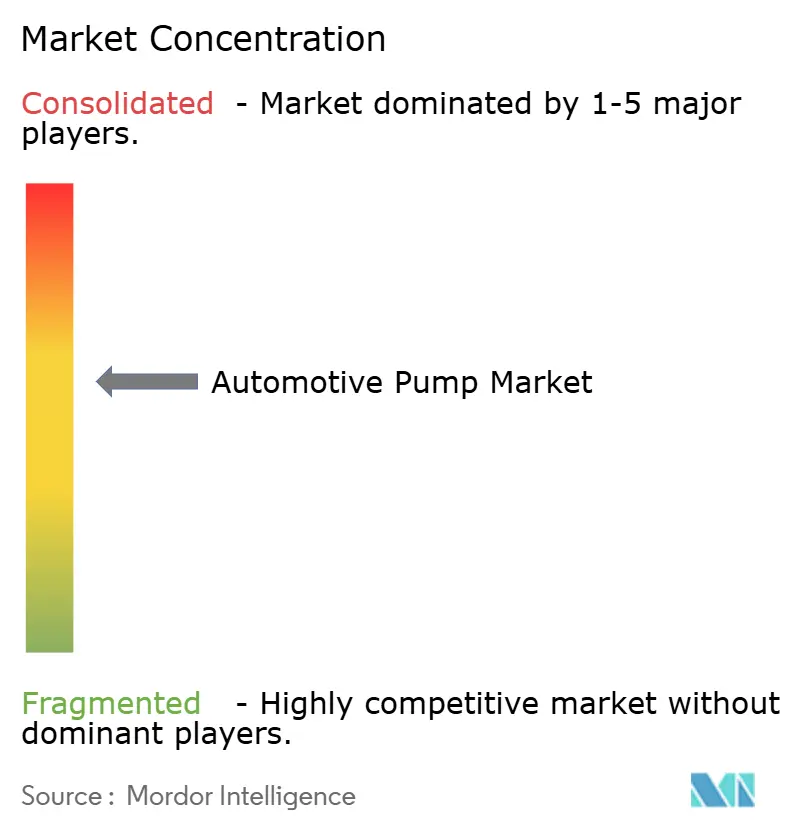

The automotive pump market exhibits moderate fragmentation that rewards scale, breadth, and software acumen. Bosch, Denso, and Continental anchor the leadership tier by bundling pumps into integrated thermal blocks, reducing OEM procurement complexity. Denso’s smart-factory rollout in India exemplifies how automation and in-line data analytics shorten product-validation loops while maintaining Six-Sigma quality.

Mid-tier contenders such as BorgWarner and Rheinmetall pursue adjacency expansion through acquisitions and long-term pump-supply contracts for hybrid platforms[3]“Advanced Coolant Pump Contract Award,” Rheinmetall AG, rheinmetall.com. Their investments in high-pressure fuel-injection and e-coolant technologies reflect the market’s pivot toward electrically actuated, smart-sensor equipment. System-integration capabilities, rather than single-component excellence, increasingly dictate RFQ success as OEMs demand turnkey thermal-management modules.

New entrants focus on niche breakthroughs such as solid-state pump drives, high-temperature ceramic bearings, or hydrogen-specific sealing solutions. However, scaling to automotive-grade volumes remains a formidable barrier. Intellectual property filings cluster around rotor-stator geometry, advanced coatings, and embedded cyber-security for over-the-air update channels. Over the forecast window, strategic alliances between semiconductor firms and mechanical pump specialists will influence how quickly digital diagnostics diffuse through the automotive pump industry.

Automotive Pump Industry Leaders

Robert Bosch GmbH

Denso Corporation

Aisin Seiki Co. Ltd.

Continental AG

Magna International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Setco Automotive Limited unveiled an engine-cooling water pump tailored for LCVs and MHCVs.

- February 2025: TIF Fluid Systems launched the eCP electric coolant pump series featuring integrated flow sensors and predictive-maintenance firmware.

- October 2024: Honda Cars India Limited initiated a preventive fuel-pump replacement campaign covering 90,468 vehicles manufactured in earlier years.

- June 2024: Rheinmetall secured a multi-million-unit order for electric coolant pumps supplying a global hybrid-vehicle platform.

Global Automotive Pump Market Report Scope

| Fuel Pump |

| Fuel Injection Pump |

| Oil Pump |

| Water Pump |

| Steering Pump |

| Windshield Washer Pump |

| Vacuum Pump |

| Others |

| Mechanical Pumps |

| Electric Pumps |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Two-Wheelers |

| Off-Highway Vehicles |

| Engine |

| Transmission |

| Cooling System |

| Lubrication |

| Windshield |

| HVAC |

| Others |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Pump Type | Fuel Pump | |

| Fuel Injection Pump | ||

| Oil Pump | ||

| Water Pump | ||

| Steering Pump | ||

| Windshield Washer Pump | ||

| Vacuum Pump | ||

| Others | ||

| By Technology | Mechanical Pumps | |

| Electric Pumps | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| Two-Wheelers | ||

| Off-Highway Vehicles | ||

| By Application | Engine | |

| Transmission | ||

| Cooling System | ||

| Lubrication | ||

| Windshield | ||

| HVAC | ||

| Others | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the automotive pump market by 2030?

The market is forecast to reach USD 14.85 billion by 2030 based on a 3.76% CAGR.

Which pump type is growing fastest through 2030?

Water pumps lead growth with a 4.62% CAGR driven by battery and turbocharger cooling needs.

Why does Asia-Pacific dominate automotive pump demand?

The region combines massive vehicle production scale with aggressive expansion of both ICE and EV capacity, giving it 45.11% share in 2024 and the fastest 4.15% CAGR.

Which vehicle segment is projected to post the quickest pump-demand rise?

Medium and Heavy commercial vehicles, expanding at a 5.25% CAGR, owing to new thermal-management needs in electrified trucks and buses.

Page last updated on: