Automotive Brake Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 78.49 Billion |

| Market Size (2031) | USD 101.47 Billion |

| Growth Rate (2026 - 2031) | 5.57% CAGR |

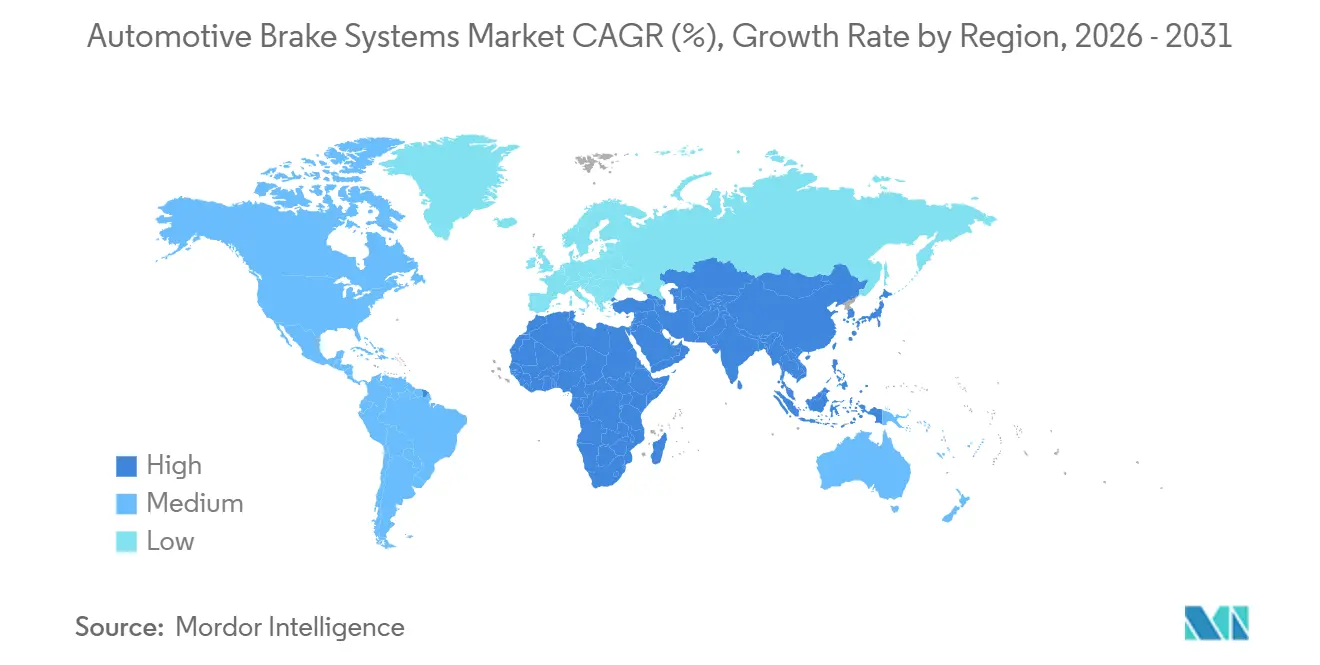

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

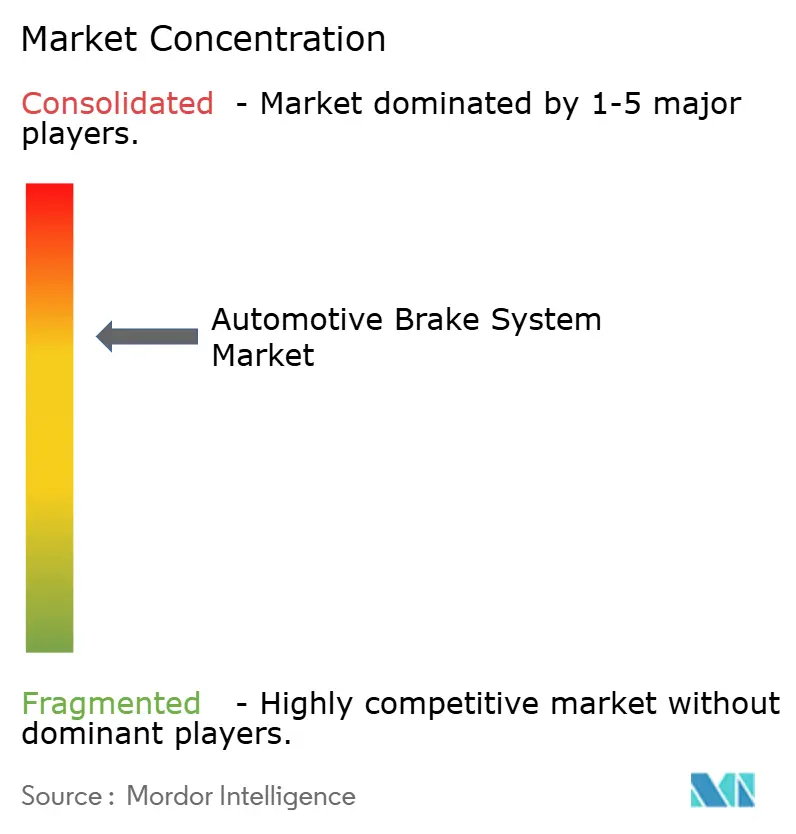

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Brake Systems Market Analysis by Mordor Intelligence

The automotive brake system market size is expected to increase from USD 74.94 billion in 2025 to USD 78.49 billion in 2026 and reach USD 101.47 billion by 2031, growing at a CAGR of 5.57% over 2026-2031. Demand gains stem from the rollouts of battery-electric vehicles (BEVs) that retool friction hardware for regenerative deceleration, the growing adoption of brake-by-wire modules that satisfy automatic emergency braking mandates, and OEM efforts to align copper-free pads with tightening particulate limits. Disc brakes dominate fitment, yet regenerative sub-assemblies post the fastest gains as blended-braking algorithms migrate from premium to mass-market nameplates. Tier-one suppliers integrate sensors, actuators, and domain control units to deliver one-box solutions that shorten vehicle-development cycles while protecting intellectual property. Regional momentum remains strongest in Asia-Pacific, where localized BEV platforms are driving annual revenue share gains and prompting capacity additions for electronic stability control modules.

Key Report Takeaways

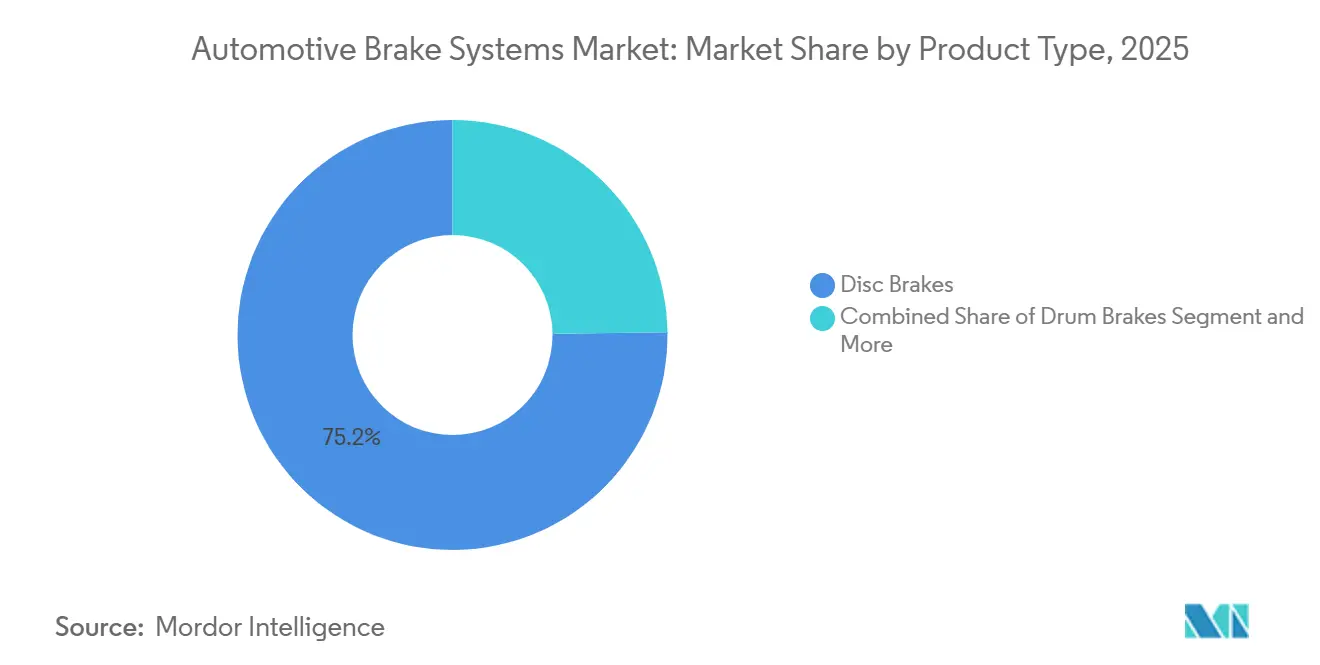

- By product type, disc brakes accounted for 75.21% of the automotive brake system market in 2025; regenerative modules are forecast to expand at a 7.77% CAGR through 2031.

- By technology, anti-lock braking systems captured 45.65% of the automotive brake system market share in 2025, whereas electronic stability control is projected to show the highest 6.34% CAGR to 2031.

- By actuation mechanism, hydraulic systems accounted for 84.02% of the automotive brake system market size in 2025, while electromagnetic and brake-by-wire solutions are set to grow at a 9.69% CAGR.

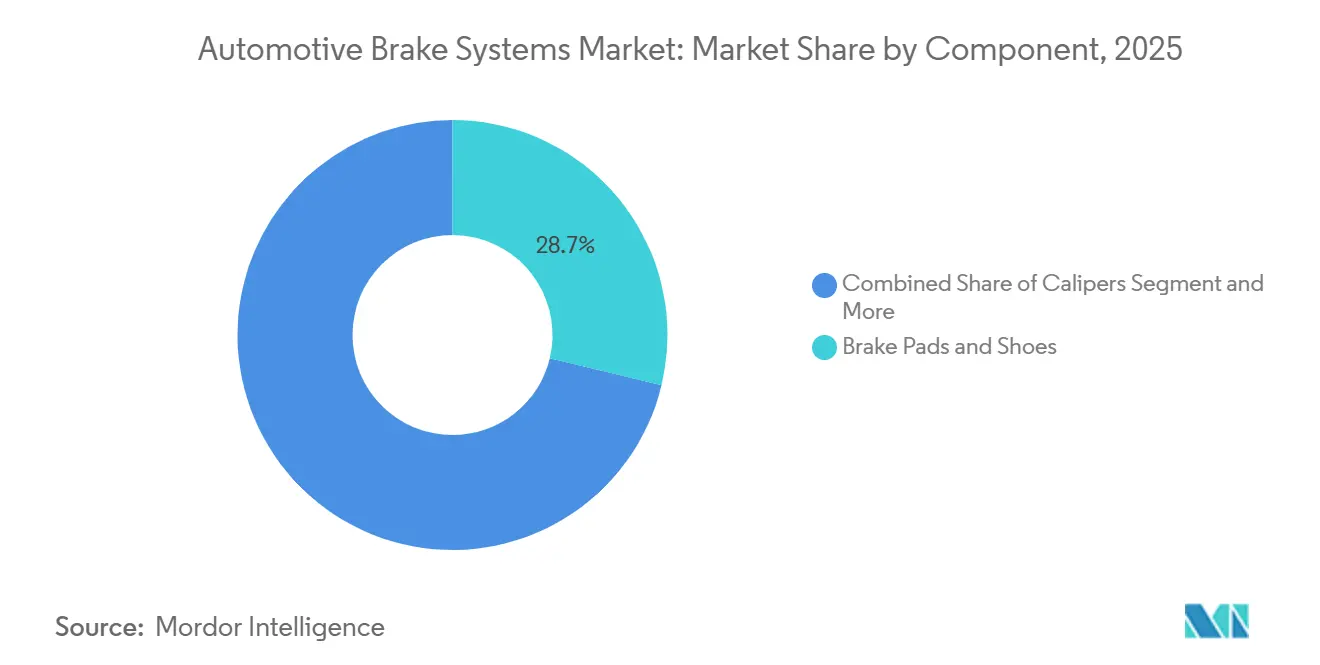

- By component, pads and shoes led with 28.75% share in 2025; electronic control units record the fastest 8.31% CAGR during 2026–2031.

- By pad material, semi-metallic formulas dominated at 42.31% in 2025; ceramic pads are advancing at a 7.77% CAGR driven by regulatory and warranty factors.

- By sales channel, OEM contracts accounted for 69.03% of total revenue in 2025, while aftermarket e-commerce is growing at a 7.54% CAGR.

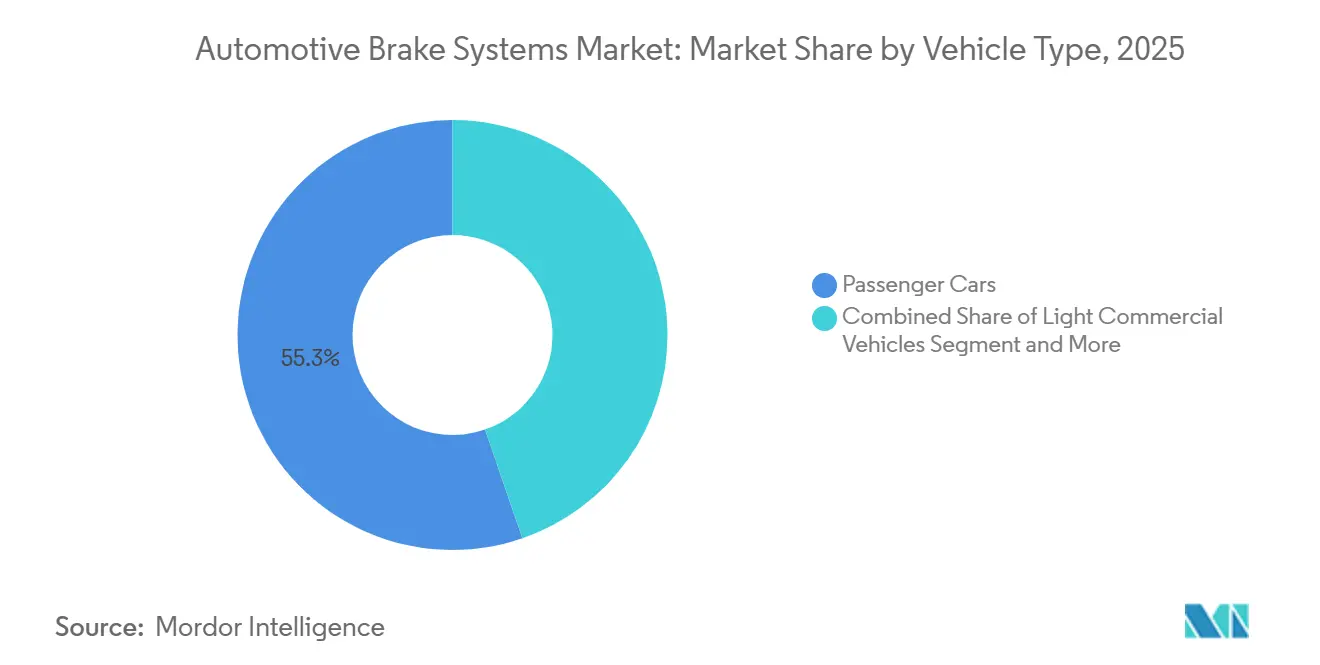

- By vehicle type, passenger cars accounted for 55.27% of the 2025 market size; light commercial vehicles registered the strongest 7.33% CAGR as e-commerce fleets expand.

- By propulsion, internal-combustion platforms held an 83.71% share in 2025, but battery-electric vehicles posted a leading 12.55% CAGR through 2031.

- By geography, Asia Pacific led with 42.41% revenue share in 2025, and is projected to register the fastest 6.88% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Brake Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Electrification | +1.8% | Global, APAC core with spill-over to EU & NA | Medium term (2–4 years) |

| Accelerating Global BEV Production | +1.2% | Global, early gains in China, California, EU | Medium term (2–4 years) |

| Heightened ADAS Penetration | +1.0% | North America & EU, premium segments in APAC | Long term (≥ 4 years) |

| U.S. FMVSS 126 and UNECE R140 Mandates | +0.7% | Global, phased compliance in emerging markets | Short term (≤ 2 years) |

| Post-COVID E-commerce Surge | +0.5% | North America, Western Europe, urban APAC | Short term (≤ 2 years) |

| OEM Warranty Extensions | +0.4% | Global, concentrated in premium OEM segments | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rapid Electrification Driving Regenerative-Compatible Brake Hardware

Growing BEV production is compelling suppliers to redesign calipers, rotors, and software for blended braking that maximizes energy recovery. Polestar and Tesla have demonstrated one-pedal modes that cut pad contact in urban duty cycles, extending service intervals beyond 100,000 kilometers. These requirements push tier ones toward integrated control units that can communicate battery-state data in real-time. China’s GB 21670-2025 updates passenger-car braking system requirements and is expected to influence regenerative-braking/one-pedal calibration strategies in NEVs.[1]Beiwan Nanxiang, "Interpretation of the new national standard GB 21670-2025," Technical Requirements and Test Methods for Passenger Car Braking Systems", EEWORLD Inc., en.eeworld.com.cn Joint engineering programs between OEMs and suppliers are replacing the traditional black-box sourcing model, ensuring software ownership and compliance with cybersecurity standards.

Accelerating Global BEV Production Necessitating Low-Dust, Copper-Free Friction Materials

California’s Safer Consumer Products rule and equivalent Washington legislation cap pad copper content at 0.5% by weight beginning in 2025, forcing a shift toward ceramic fibers and aramid pulp[2]"Washington's toxics in products laws", Washington State Department of Ecology, ecology.wa.gov. Bosch rolled out an ECE R90-certified low-metallic pad that meets proposed Euro 7 particulate limits, while Akebono’s ProACT line claims over 60% dust reduction relative to semi-metallic analogs. The European Union’s draft Euro 7 framework adds a 7 mg/km brake-dust ceiling, further tightening qualification tests. Because regenerative braking reduces contact frequency, any residual dust becomes more visible, intensifying OEMs' preference for clean-brake chemistries that protect brand image and air quality.

Heightened ADAS Penetration Raising Demand for Brake-by-Wire Architectures

The U.S. National Highway Traffic Safety Administration finalized an automatic emergency-braking rule in 2024 that requires collision-avoidance performance up to 62 mph by 2029, effectively standardizing high-bandwidth brake-by-wire hardware on future platforms. Euro NCAP’s 2025 five-star protocol mirrors this expectation at highway speeds. ZF secured a 5-million-unit production award for electromechanical brakes, and Bosch’s Integrated Brake Control eliminates the vacuum booster, cutting mass by 30%. Continental's dry, fluid-free caliper targets software-defined chassis that enable over-the-air updates and sub-100-millisecond response times.

Stricter U.S. FMVSS 126 and UNECE R140 Mandates Boosting ABS/ESC Installations

Electronic stability control, already universal across the United States since 2012, continues to expand globally as developing regions phase in UNECE-aligned rules. India’s ESC requirement accelerated localization by Bosch and Mando, while China’s GB 21670 update broadened coverage to all new passenger models. ABS remains the foundational layer upon which traction control, electronic brake-force distribution, and hill-hold assist are enabled, amplifying unit value even in mature markets.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reduced Wear in Regenerative Braking | -0.6% | Global, concentrated in BEV-dense urban markets | Medium term (2–4 years) |

| Volatility in Rare-earth Prices | -0.4% | Global, supply-chain exposure in APAC & NA | Short term (≤ 2 years) |

| Supply-chain Bottlenecks | -0.3% | Europe, secondary effects in NA | Short term (≤ 2 years) |

| Declining Diesel CV Production | -0.2% | Europe, limited impact in APAC & NA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Reduced Wear in Regenerative Braking Curtailing Aftermarket Pad Revenues

Service data indicates that BEVs can double the pad-replacement interval compared with comparable ICE models, trimming independent workshop revenue and encouraging consolidation among distributors. Fleet operators welcome the lower total cost of ownership, yet suppliers reliant on high-volume pad sales face declining unit sales and must pivot toward premium composites or embedded sensor services to restore value capture.

Volatility in Rare-Earth Prices Inflating Electronic Brake Actuator Costs

Neodymium oxide climbed from USD 56 to over USD 65 per kilogram between mid-2024 and early-2025, driving up costs for permanent-magnet motors inside electromechanical calipers. Continental estimates a EUR 15 headwind per integrated control unit and seeks relief through long-term contracts with non-Chinese refiners. Research into ferrite motors presents an eventual workaround but currently sacrifices torque density, limiting near-term substitution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Disc Brakes Retain Scale as Electric Park Brakes Accelerate

Disc brakes captured 75.21% of the 2025 market size, underpinning the automotive brake system market through proven heat management, consistent pedal feel, and rapid pressure modulation. Their extensive supply networks and backward compatibility with ABS and ESC help defend their position even as blended-braking strategies proliferate. Drum brakes remain cost-effective for rear axles in entry-level cars and light vans, yet mandatory stability control erodes their relevance. Regenerative modules, although smaller in absolute terms, are projected to advance at a 7.77% CAGR as OEMs seek every watt of energy recovery to extend the driving range of BEVs. Lightweight carbon-ceramic discs from Brembo illustrate convergence between traditional friction materials and electrification requirements.

Continental’s modular regenerative controller showcases how software-centric architectures are redefining product roadmaps across tier-one suppliers. The controller is designed to communicate the battery's state of charge in real-time, enabling seamless transitions between motor torque and hydraulic pressure. Such integration shortens validation cycles and lowers calibration costs for global platforms. In parallel, electric parking brakes are gaining popularity by freeing cabin space and facilitating automated parking functions. Together, these developments reinforce the long-term pivot from purely hydraulic hardware toward hybrid energy-recovery topologies.

By Technology: ESC Integration with ADAS Drives Fastest Growth Amid ABS Maturity

Anti-lock braking systems accounted for 45.65% of 2025 revenue, anchoring stability performance and satisfying legacy mandates across most major markets. Nonetheless, their forecasted CAGR trails electronic stability control, which benefits from a tight regulatory link with automatic emergency braking and lane-keeping assist. ESC leverages shared wheel-speed and yaw-rate sensors, allowing tier-one manufacturers to package multiple functions inside a single domain controller and reduce wiring weight. Bosch’s Vehicle Motion Management, already scheduled for a volume launch, unifies ESC, torque vectoring, and adaptive cruise control to reduce stopping distance by over 8%. This bundling trend elevates software value while flattening hardware cost curves.

Traction control and electronic brake-force distribution are integrated into the same silicon, further reducing incremental component costs. Euro NCAP’s 2025 five-star protocol and the U.S. AEB rule both list ESC as a prerequisite for high-speed collision-avoidance certification, thereby accelerating its penetration in entry-level trims. ZF’s cubiX platform links the ESC to electric power steering and active suspension, enabling predictive wheel-torque commands that stabilize the vehicle before the driver reacts. In emerging economies, India’s AIS-145 mandate has spurred local module production, trimmed import duties, and secured supply. Collectively, these triggers position ESC as the new baseline for software-defined chassis control.

By Actuation Mechanism : Electromagnetic Systems Surge as Hydraulic Retains Installed Base

Hydraulic actuation commands 84.02% of the 2025 market size, supported by decades of engineering refinement, low unit cost, and pervasive tooling across regional assembly plants. Even so, its CAGR lags behind electromagnetic and brake-by-wire solutions, which post a 9.69% CAGR as BEV and autonomous programs mature. Pneumatic systems remain essential for heavy trucks but face headwinds from Europe’s declining diesel registrations and tightening noise regulations. Brake-by-wire eliminates the vacuum booster, shortens pedal travel, and enables sub-100-millisecond response, a key specification for ADAS collision-avoidance maneuvers. Continental’s fluid-free MK C2 system highlights the shift toward dry calipers that reduce mass by 25% and simplify thermal management in electric SUVs.

ZF’s record order for 5 million electro-mechanical units demonstrates mainstream acceptance beyond luxury nameplates. Nexteer’s steer-by-wire and brake-by-wire prototype shows how independent wheel-torque control can enhance automated parking, lane centering, and low-speed maneuvering. ISO 26262 functional-safety rules enforce redundant actuation paths, raising the engineering bar and favoring tier-ones with deep validation budgets. Suppliers are therefore partnering with semiconductor houses to co-design safety-certified microcontrollers that lower latency. As the cost differential narrows, OEMs see value in over-the-air upgradability that hydraulic lines can never match.

By Component: Electronic Control Units Lead Growth as Pads Dominate Revenue

Pads and shoes accounted for 28.75% of component revenue in 2025, making them the most significant slice of the automotive brake system market, despite modest CAGR projections. Their volume is protected by routine maintenance cycles, but regenerative braking and longer OEM warranties temper unit demand. Cast-iron rotors in particular face lightweight substitution from aluminum-matrix or carbon-ceramic designs. Brake boosters transition from vacuum to electro-hydraulic formats as ICE manifold suction is eliminated on turbo-downsized and electric powertrains.

Electronic control units, however, expand at an 8.31% CAGR as brake-by-wire and integrated ESC-ADAS stacks gain content per vehicle. Bosch’s Integrated Brake Control reduces part count by 40% by fusing master cylinder, hydraulic modulator, and pedal simulator into one 4.5-kilogram box. Continental’s 48-volt booster works seamlessly with mild hybrids, illustrating how component design now assumes dual-voltage architectures. Suppliers are embedding cybersecurity modules to meet UNECE R155 requirements, turning the ECU into both a braking brain and a network firewall. These features command higher average selling prices and justify capital investment in new ASICs.

By Pad Material: Ceramic Formulations Gain Traction as Semi-Metallic Holds Volume Share

Semi-metallic pads accounted for 42.31% of the 2025 revenue, striking a balance between cost efficiency, thermal stability, and broad vehicle compatibility. Yet their projected growth outlook pales in comparison to ceramic formulations, which rise 7.77% annually, driven by copper bans and OEM warranty extensions to 160,000 kilometers. Organic non-asbestos pads are shrinking as fleet buyers demand superior fade resistance, while metallic pads remain a niche for heavy-duty rigs that can tolerate higher noise levels. Akebono’s latest ceramic line replaces copper with aramid fibers and graphite, cutting dust by over 50% and meeting California’s 0.5% copper limit.

The draft Euro 7 rules introduce a 7 mg/km brake particulate ceiling, effectively mandating low-wear materials across the European fleet. Suppliers test closed-loop calipers that capture airborne debris inside replaceable cartridges, opening a fresh revenue stream. Consumers appreciate the quieter operation and cleaner wheels of ceramic pads, which strengthens pull-through in the aftermarket e-commerce channel. Bosch and Ferodo market ECE R90-certified kits online, offering vehicle-fitment guarantees that mitigate installation risk for DIY buyers. The combined effect is a gradual pivot toward premium chemistry even in price-sensitive segments.

By Sales Channel: OEM Dominates but Aftermarket E-Commerce Expands Rapidly

OEM contracts secured 69.03% of 2025 sales due to locked-in sourcing during the seven-year platform cycle and deep co-development ties between automakers and tier-ones. However, the aftermarket posts a 7.54% CAGR as digital storefronts disrupt traditional distributor models, allowing enthusiasts to order pads, rotors, and fluid directly to their garage. Amazon Automotive and RockAuto integrate VIN decoders that slash fitment errors, raising consumer confidence in online transactions. Fleet operators leverage bulk e-commerce purchases to manage brake inventory for last-mile delivery vans, squeezing regional jobbers on price.

Regenerative braking lengthens replacement intervals in BEVs, pressuring unit volumes; yet, suppliers offset this by offering premium ceramic and carbon-composite kits that lift average selling prices. Continental’s direct-to-consumer launch bundles wear sensors and mobile diagnostics to capture data for predictive maintenance analytics. EU Block Exemption rules compel OEMs to share repair manuals, ensuring independent shops can install advanced brake-by-wire modules without proprietary tools. Global distributors respond by stocking higher-value SKUs and offering training webinars that monetize expertise. Collectively, these shifts redraw value pools across the channel landscape.

By Vehicle Type: Passenger Cars Lead Volume While LCVs Benefit from E-Commerce Fleets

Passenger cars delivered 55.27% of the 2025 market size; however, their growth trails the overall automotive brake system market CAGR, as plateauing demand in mature economies offsets incremental ADAS content. BEV trims within the passenger segment command higher bill-of-materials, raising revenue per vehicle even when volumes flatten. Light commercial vehicles are gaining momentum and are projected to grow at a 7.33% CAGR driven by e-commerce and urban logistics, requiring durable pads and anti-corrosion coatings to withstand high stop-start cycles. Heavy commercial vehicles use electro-pneumatic blends that reduce compressor use by prioritizing regenerative deceleration, thereby lowering the total cost of ownership.

Volvo’s electric heavy-duty platform and Daimler’s eActros demonstrate how brake-system redesign is closely tied to battery pack packaging and chassis electrification. Municipal bus tenders are increasingly specifying regenerative-compatible hardware, spurring local suppliers across India and South America to license technology from global tier-one companies. Insurance premiums now reward fleets that incorporate ESC and collision-mitigation braking, as well as add pull-through for electronics. Meanwhile, passenger-car OEMs market ceramic pads as a luxury comfort upgrade, tapping noise reduction to differentiate trim levels. These parallel trends diversify growth vectors by vehicle class.

By Propulsion: BEVs Drive Fastest Growth as ICE Retains Installed Base

Internal-combustion vehicles still accounted for 83.71% of the 2025 market size, primarily due to legacy refueling infrastructure and lower sticker prices in many emerging markets. Yet their CAGR lags BEVs, which are growing at a 12.55% CAGR, driven by stricter emissions caps and falling battery costs. Hybrid electric vehicles are increasing as an interim step, familiarizing drivers with regenerative braking and electrified accessories—fuel-cell prototypes in long-haul trucking test high-pressure pneumatic circuits integrated with electro-mechanical calipers to manage hydrogen tank placement.

CATL’s battery-to-brake communication protocol sends state-of-charge data directly to the controller, optimizing regenerative torque and extending pad life, an innovation soon to be copied by peer cell suppliers. Tesla’s adaptive regen update modulates motor braking based on ambient temperature, demonstrating how software can compensate for physical constraints without hardware swaps. China’s dual-credit program ties OEM profitability to zero-emission volumes, accelerating the shift in vehicle mix toward BEVs, which inherently require blended-brake logic. This propulsion transition thus defines the future revenue cadence for both friction and electronics suppliers.

Geography Analysis

Asia-Pacific produced 42.41% of global 2025 revenue and is projected to grow at a 6.88% CAGR through 2031, the fastest among all regions. China’s dual-credit policy rewards new-energy vehicle output, pushing BYD, Geely, and NIO to specify regenerative-ready brake modules on every fresh platform. India’s production-linked incentives lure Bosch and ZF into local ESC and electronic parking brake plants, reducing reliance on imports and shortening lead times. Japan’s Akebono, Nissin, and Hitachi Astemo leverage precision manufacturing to hold a premium share even as domestic volumes plateau.

North America advances with mature ABS penetration, yet is invigorated by the U.S. automatic emergency braking rule that mandates compliant hardware by 2029. ZF’s order for 5 million electromechanical calipers from a Detroit automaker underscores the rapid migration toward software-defined braking. Canada’s zero-emission sales mandate accelerates demand for copper-free pads and regenerative control software, while Mexico’s cost advantage encourages near-shoring of cast-iron rotor machining. Aftermarket revenue benefits from e-commerce, although longer pad life in BEVs moderates sales cycles, nudging distributors toward premium kits and value-added diagnostics.

Europe grows at a comparatively modest rate as declining diesel van production and steel-rotor shortages offset incremental ADAS content. Euro NCAP’s 2025 assessment and pending Euro 7 dust limits nonetheless sustain investment in brake-by-wire, ceramic pads, and particulate-capture calipers. Germany hosts Continental, Bosch, and ZF, which together channel R&D into fluid-free actuators that meet ISO 26262 while lowering mass. Supply-chain tension eased somewhat after ArcelorMittal shifted volumes to Spain, but high-grade sheet remains tight, nudging suppliers toward aluminum and composite rotors. Southern European ports explore shore-power requirements that may extend to logistics trucks, implying future demand for regenerative-compatible commercial-vehicle brakes.

Competitive Landscape

The automotive brake-system market exhibits moderate concentration, with Continental, Bosch, and ZF Friedrichshafen collectively commanding a majority of global revenue through vertical integration of sensors, actuators, electronic control units, and software platforms that enable one-box solutions for OEMs seeking to reduce supplier count and simplify vehicle integration. Their vertical scope and functional-safety credentials satisfy OEM risk criteria and discourage multi-sourcing.

Brembo secures its market share through carbon-ceramic discs and lightweight calipers, catering to performance and EV segments that reward reductions in unsprung mass. Akebono leverages its ceramic pad expertise and localized North American capacity to maintain market share. Price-led pressure comes from Chinese entrants offering brake-by-wire modules at approximately 20% lower prices, prompting incumbents to automate and regionalize supply.

White-space innovation revolves around predictive maintenance analytics and V2X-enabled cooperative braking. Bosch’s Vehicle Motion Management domain controller and Continental’s dry caliper exemplify convergent hardware-software platforms positioned for software-defined vehicle rollouts. Start-ups focusing on solid-state actuators remain niche until they pass ISO 26262 audits and secure volume contracts.

Automotive Brake Systems Industry Leaders

-

Continental AG

-

Hitachi Astemo Ltd.

-

Brembo S.p.A

-

Akebono Brake Industry Co., Ltd

-

Robert Bosch GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Nexteer Automotive launched an electro-mechanical brake-by-wire system designed for modular, software-defined chassis integration.

- March 2025: Brembo unveiled an electro-mechanical caliper, targeting series production in 2026.

- January 2025: ZF agreed on a high-volume brake-by-wire supply for a North American model line, pairing electro-mechanical rear brakes with integrated front hydraulics.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the global automotive brake system market as the value of factory-built braking assemblies, including disc, drum, electric parking, and brake-by-wire modules, supplied to passenger and commercial vehicles at OEM and authorized aftermarket points. Systems designed strictly for rolling stock, bicycles, or two-wheelers fall outside this scope.

Scope exclusion: retro-fit kits for off-road racing conversions are not considered.

Segmentation Overview

-

By Product Type

- Disc Brakes

- Drum Brakes

- Electric Parking Brakes

- Regenerative Braking Modules

-

By Technology

- Anti-lock Braking System (ABS)

- Electronic Stability Control (ESC)

- Traction Control System (TCS)

- Electronic Brake-force Distribution (EBD)

-

By Actuation Mechanism

- Hydraulic

- Pneumatic

- Electromagnetic / Brake-by-Wire

- Mechanical (Cable)

-

By Component

- Brake Pads and Shoes

- Calipers

- Rotors and Drums

- Brake Boosters and Master Cylinders

- Electronic Control Units and Actuators

-

By Pad Material

- Organic (Non-Asbestos)

- Semi-Metallic

- Metallic

- Ceramic

-

By Sales Channel

- Original Equipment Manufacturers (OEM)

- Aftermarket

-

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles and Buses

-

By Propulsion

- Internal Combustion Engine (ICE) Vehicles

- Hybrid Electric Vehicles (HEV/PHEV)

- Battery Electric Vehicles (BEV)

- Fuel-Cell Electric Vehicles (FCEV)

-

By Geography

-

North America

- United States

- Canada

- Rest of North America

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

To refine assumptions, we interview OEM purchasing managers, tier-1 engineering leads, regional brake distributors, and road-safety regulators across Asia-Pacific, North America, and Europe. Their inputs clarify average selling prices, new-model take-rates for ABS, ESC, and regenerative modules, and regional warranty replacement cycles, enabling us to close gaps left by desk work.

Desk Research

Mordor analysts begin with trusted open datasets such as OICA vehicle output, UN/ECE safety regulations, NHTSA Federal Motor Vehicle Standards, International Trade Center HS 870830 trade flows, and technical papers hosted on SAE Mobilus. Financial disclosures and investor decks from leading tier-1 brake suppliers add cost and mix insights, while D&B Hoovers and Dow Jones Factiva provide corroborative company revenue splits. These publicly available sources supply baseline production, technology penetration, and price corridors. The list is illustrative; many additional references guide data checks throughout the process.

Market-Sizing & Forecasting

The model opens with a top-down reconstruction of global light and heavy vehicle production, adjusted by brake-system fitment rates and OEM-aftermarket mix. Select bottom-up cross-checks, sampled supplier shipments and channel checks, validate volumes before average price layering. Key variables include: 1) mandated ABS/ESC adoption timelines, 2) battery-electric vehicle share (impacts regenerative braking demand), 3) regional miles-driven trends, 4) raw-material index for cast iron and ceramics, and 5) average disc-to-drum mix shift. A multivariate regression, stress-tested through scenario analysis, projects 2025-2030 values, with expert consensus guiding variable trajectories where public data lag.

Data Validation & Update Cycle

Outputs undergo variance scans versus historical trade, recall, and accident-rate data; anomalies trigger iterative fixes. A senior reviewer signs off after peer audit. Reports refresh yearly, with interim revisions when safety mandates or major capacity announcements materially alter forecasts.

Why Mordor's Automotive Brake System Baseline Commands Reliability

Published figures often diverge because firms pick differing component sets, price points, and refresh rhythms. By anchoring totals to verified vehicle builds and regulation-driven fitment ratios, we provide a consistent yardstick that decision-makers can trace.

Key gap drivers include narrower component baskets used by some publishers, currency conversions frozen at older rates, or single-region sampling extrapolated globally, which inflate or deflate totals relative to Mordor's blended approach and annual refresh.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 77.21 B (2025) | Mordor Intelligence | - |

| USD 24 B (2023) | Global Consultancy A | Excludes aftermarket discs and brake-by-wire units; 2022 FX base |

| USD 23.45 B (2023) | Global Consultancy B | Counts only on-highway vehicles; limited Asia primary checks |

| USD 48.22 B (2024) | Trade Journal C | Aggregates disc and drum parts but omits electronic control units |

Taken together, the comparison shows that Mordor's disciplined scope, dual-path modeling, and timely updates yield a balanced, transparent baseline that clients can replicate and stress-test with confidence.

Key Questions Answered in the Report

How large is the automotive brake system market in 2026 and what growth is expected?

The market stands at USD 78.49 billion in 2026 and is forecasted to reach USD 101.47 billion by 2031, reflecting a 5.57% CAGR.

Which brake technology segment is expanding fastest?

Electronic stability control is the fastest-growing sub-segment, advancing at a 6.34% CAGR due to ADAS and AEB mandates.

What regional market leads growth through 2031?

Asia-Pacific registers the highest 6.88% CAGR, driven by Chinese and Indian BEV platform expansion and localized tier-one investments.

How are rare-earth prices affecting brake-by-wire adoption?

Volatile neodymium and dysprosium costs increase electro-mechanical caliper pricing, prompting long-term sourcing contracts and R&D into ferrite motors.

Why are ceramic pads gaining popularity?

Copper bans, warranty extensions, and lower dust emissions push OEMs toward ceramic formulations growing at a 7.77% CAGR.

Page last updated on: