Automotive Switch Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 46.42 Billion |

| Market Size (2031) | USD 60.09 Billion |

| Growth Rate (2026 - 2031) | 5.31% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

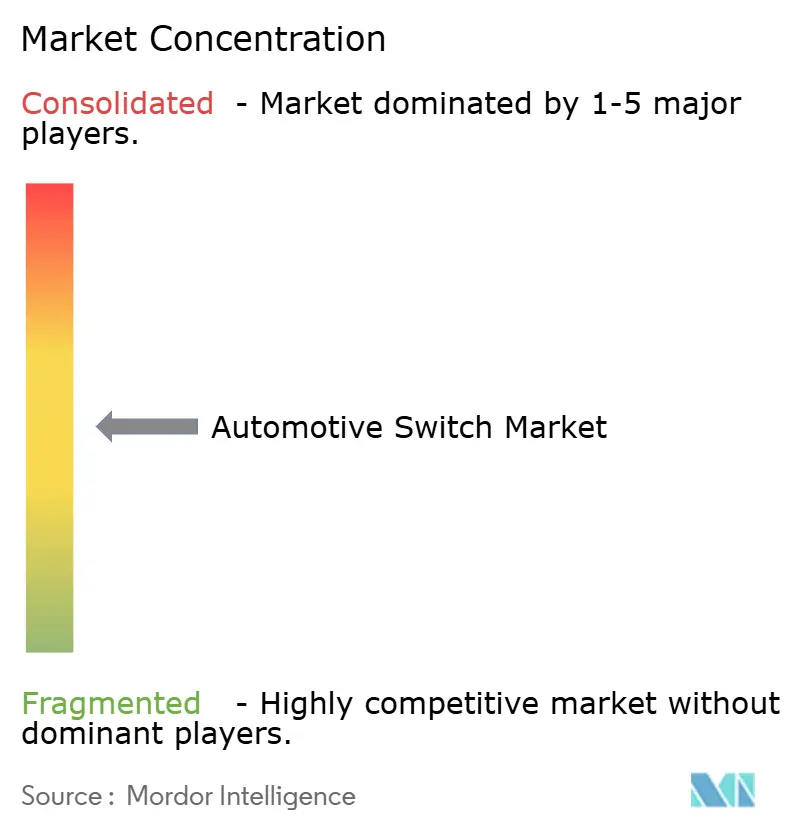

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Switch Market Analysis by Mordor Intelligence

The automotive switch market size was valued at USD 44.08 billion in 2025 and estimated to grow from USD 46.42 billion in 2026 to reach USD 60.09 billion by 2031, at a CAGR of 5.31% during the forecast period (2026-2031). The upswing reflects a wider transition to software-defined vehicles where switches act as frontline human-machine interfaces that connect mechanical feel with electronic intelligence. Electrification now shapes material demand and cost structures, as each battery-electric vehicle needs far more copper and high-voltage circuitry than its combustion counterpart. Greater infotainment and ADAS content, the push for luxurious illuminated cabins, and stricter ISO 26262 safety rules all raise the functional expectations placed on every switch. Competitive rivalry intensifies as haptic and capacitive technologies challenge the mechanical status quo, while supply-chain shocks surrounding copper and rare-earths force manufacturers to rethink sourcing, cost hedging, and regional production footprints.

Key Report Takeaways

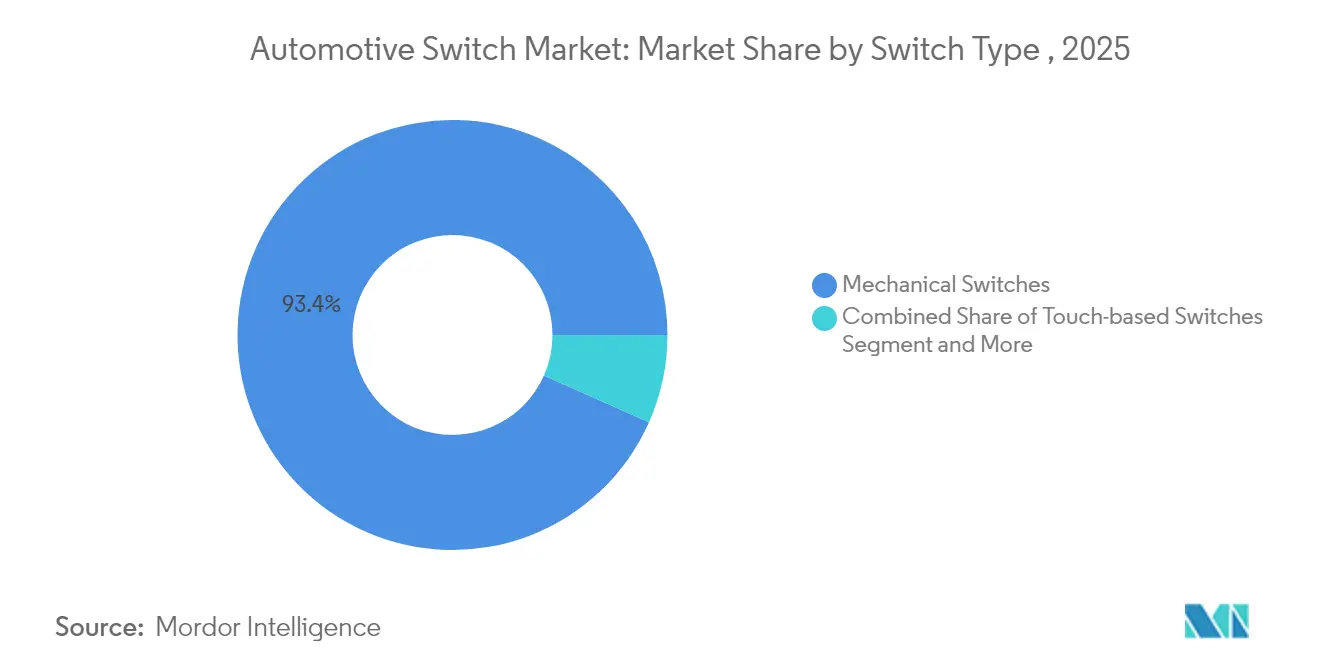

- By switch type, mechanical designs led with 93.35% revenue share in 2025, whereas touch-based interfaces are set to expand at an 8.03% CAGR to 2031.

- By application, indicator systems captured 24.80% of 2025 revenue; HVAC controls are projected to rise at a 5.53% CAGR through 2031.

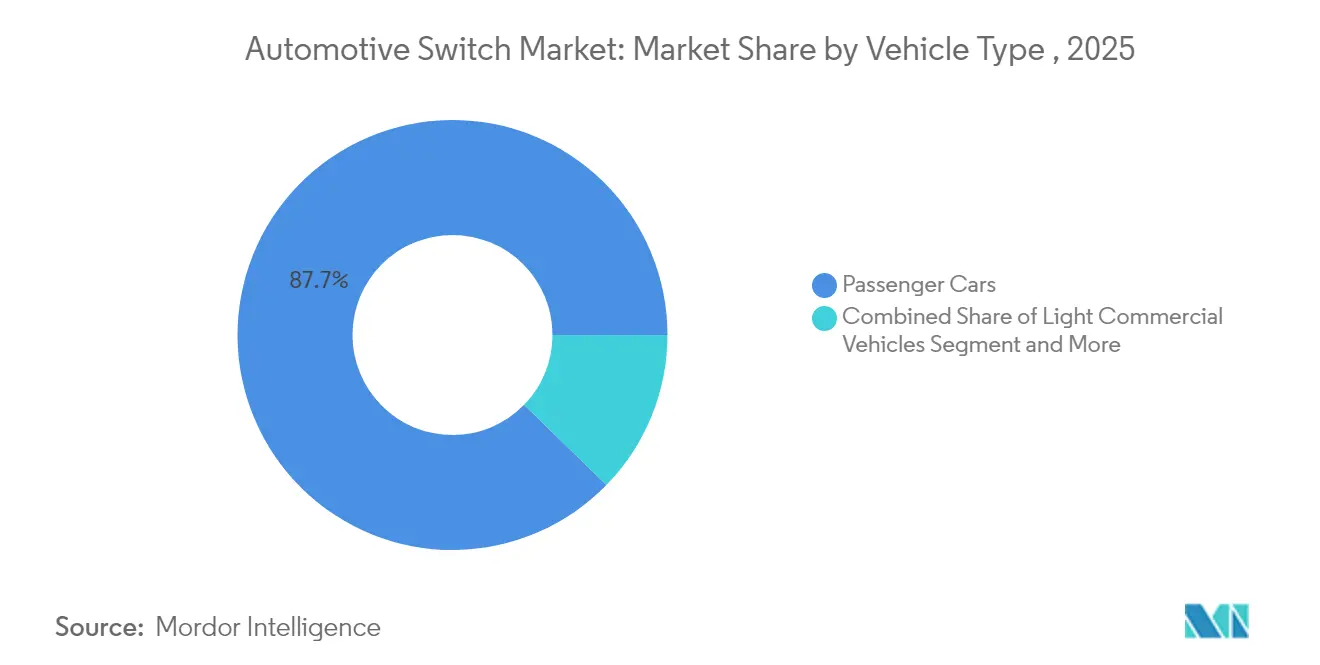

- By vehicle type, passenger cars held 87.70% of the automotive switch market share in 2025 and will also post the fastest 5.44% CAGR to 2031.

- By sales channel, OEMs controlled 85.60% of revenue in 2025, yet the aftermarket is growing at a 7.11% CAGR as global fleets age.

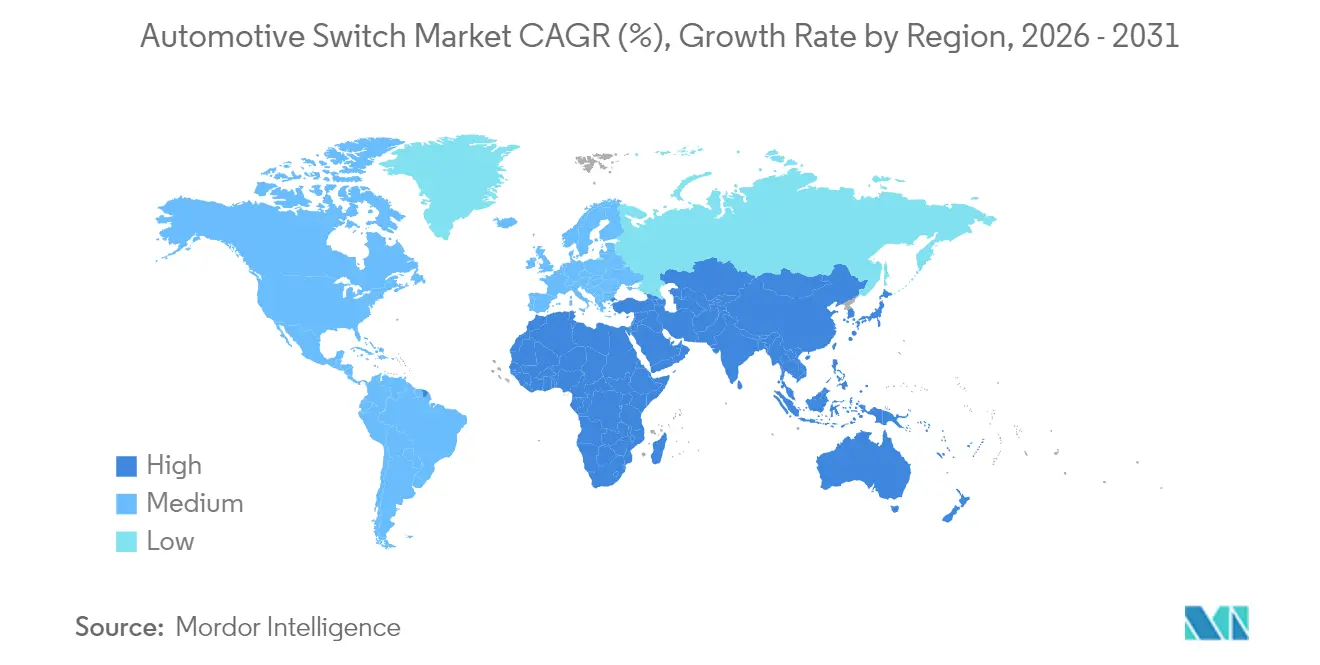

- By geography, Asia Pacific commanded 49.40% of revenue in 2025, whereas the Middle East & Africa segment exhibits the strongest 7.43% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Switch Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vehicle Electrification Surge | +1.2% | APAC & Europe | Medium term (2-4 years) |

| Expansion of Advanced Infotainment & ADAS | +0.9% | North America & EU | Short term (≤ 2 years) |

| Rising Vehicle Output in Emerging Economies | +0.8% | APAC › MEA › South America | Long term (≥ 4 years) |

| Premium-interior Demand for Illuminated & Capacitive Units | +0.6% | North America & EU luxury | Medium term (2-4 years) |

| Adoption of Haptic/Force-touch Technology | +0.4% | Global premium tiers | Long term (≥ 4 years) |

| Functional-safety Need for Redundant Designs | +0.3% | Global regulations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rise in Vehicle Electrification

Electric powertrains introduce unique control needs—battery management, regenerative braking, and thermal optimization all require purpose-built switches that tolerate higher voltage while preserving tactile response. Panasonic Automotive’s centralized ECU architecture shows how electronics content balloons once combustion hardware is removed. Brazil’s plug-in sales jumped 90% in 2024 to 177,360 units, underscoring how quickly demand patterns shift. China’s plan to launch cars using 100% domestically sourced chips by 2026 will further reshape component procurement paths [1]“China Aims to Produce Cars with 100% Domestic Chips by 2026,” Asia Nikkei, nikkei.com. These forces collectively lift the automotive switch market by broadening both unit volumes and the variety of switch functions.

Growth of Advanced Infotainment & ADAS Features

Cloud-linked cockpits built on Qualcomm’s Snapdragon platforms require multifunction controllers able to talk to exterior sensors, voice assistants, and over-the-air update back-ends. Continental’s programmable haptic knob enables a single dial to mimic many different detents, satisfying space and styling goals in next-generation dashboards [2]“Variable Haptic Feedback Control Device Patent,” Continental Automotive, continental-automotive.com. Safety-critical ADAS layers demand switches certified to ISO 26262, ensuring redundant actuation for features such as lane-keeping. The retrofit ADAS aftermarket, approaching USD 1 billion, expands addressable demand among older vehicles seeking new safety functions.

Rising Vehicle Output in Emerging Economies

Thailand and Indonesia are fast becoming EV manufacturing hubs as Japanese, Chinese, and South Korean suppliers invest to shorten supply chains. Brazil remains a global top-ten producer, with Stellantis deploying R$30 billion (USD 6.0 billion) to cement regional leadership [3]“Stellantis Commits R$30 Billion to Latin America,” Valor Econômico International, valorinternational.globo.com . Localized production lowers logistics costs and allows switch makers to tune products for region-specific regulations, thereby sustaining the automotive switch market momentum over the long run.

Premium-Interior Demand for Illuminated & Capacitive Switches

A growing share of luxury trims now includes back-lit capacitive surfaces that adapt color and iconography to driving mode. Ford’s multi-light illuminated switch patent exemplifies how styling merges with user feedback. Schurter’s IP67-rated ceramic capacitive models meet IATF 16949 compliance while offering multicolor options. Consumer expectations forged by smartphones make reconfigurable cabin lighting a differentiator even in mass-market upper trims, widening adoption horizons within the automotive switch market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Copper & Rare-earth Prices | -0.8% | Global cost-sensitive tiers | Short term (≤ 2 years) |

| Shift toward Display-centric Cabins | -0.6% | North America & EU premium first | Medium term (2-4 years) |

| Supply Bottlenecks in Tactile-dome Sub-components | -0.4% | Asia Pacific manufacturing hubs | Short term (≤ 2 years) |

| Tighter EMC Limits Raising Validation Costs | -0.3% | Global compliance | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Prices of Copper & Rare-Earth Inputs

Copper prices climbed nearly 20% after February 2024 and are on track to top USD 15,000 per ton in 2025, inflating the bill-of-materials for every mechanical switch that uses high-purity contacts. Parallel restrictions on Chinese rare-earth exports have already forced short production pauses at OEMs, including Suzuki and Ford. Switch makers are hedging material costs, redesigning contact layouts, and evaluating lower-mass alloys to protect margins inside the automotive switch market.

Shift Toward Display-Based Touch Interfaces

Tesla-style, screen-only dashboards inspire rivals to replace discrete controls with virtual buttons, trimming switch counts per vehicle. Yet regulators may still insist on physical interfaces for safety-critical tasks, preserving core volumes. Continental’s rebranding to Aumovio underscores a supplier pivot toward software and large displays. For switch producers, the lesson is clear: hybrid approaches—thin, haptic overlays embedded on glass—will be key to defending share.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Switch Type: Mechanical Dominance Faces Digital Disruption

Mechanical designs retained 93.35% of 2025 revenue, proving their reliability in temperature, dust, and vibration extremes. Buttons handle high-frequency user tasks, rocker units govern binary functions, and paddles manage steering-mounted commands. The automotive switch market size for mechanical variants is projected to expand steadily even as displays grow, because safety codes continue to demand tactile backup controls.

Touch-based switches hold modest volume today but carry an 8.03% CAGR to 2031 as luxury and mass-premium trims migrate to flush lit panels. Continental’s electrostatic feedback knob reproduces mechanical detents without gears, and Snaptron’s solderable tactile domes can double annual output capacity. This convergence blurs the line: hybrid modules bundle capacitive sensing beneath a thin plastic cap yet still generate a click, giving OEMs styling freedom while maintaining the legacy feel expected in the automotive switch market.

By Application: Indicator Systems Lead While HVAC Accelerates

Indicator controls owned 24.80% of 2025 revenue because every jurisdiction mandates robust signaling for turn, hazard, and warning functions. The automotive switch market size for indicator applications remains secure even in fully digital cockpits, as external lighting commands must work when screens fail.

HVAC interfaces earn the fastest 5.53% CAGR thanks to range-sensitive thermal logic in electric cars. Tokai Rika’s in-mold-painting process, already used on Toyota’s Hiace, slashes energy use during manufacturing while delivering scratch-resistant fascias. Climate controls cannot disappear into touchscreens entirely; users need immediate tactile access to demist or defrost, sustaining demand across the automotive switch market.

By Vehicle Type: Passenger Cars Sustain Growth Leadership

Passenger cars generated 87.70% of 2025 revenue and share the highest 5.44% CAGR through 2031, powered by rising middle-class ownership and richer electronic feature sets. The automotive switch market share for passenger cars benefits from sheer unit scale, plus the move toward personalized cabin lighting schemes.

Commercial vehicles follow a durability-first approach. ZF’s chassis division is refocusing on truck electrification even as it reports EUR 22 billion H1 2024 sales. That segment values rugged sealed toggles and oversized push buttons able to withstand gloved operation, keeping distinct requirements stream inside the broader automotive switch market.

By Sales Channel: OEM Dominance Meets Aftermarket Acceleration

OEMs wielded 85.60% of 2025 revenue because switches must integrate tightly with wiring harnesses and in-vehicle networks at the factory. Safety documentation and firmware calibration further lock in Tier 1 supply agreements.

Yet the aftermarket now posts a 7.11% CAGR. Fleet owners hold vehicles for 12.6 years on average, spurring replacement demand for high-cycle components. Continental’s addition of ADAS sensor switches to its spare-parts catalog shows how mainstream Tier 1 suppliers pivot to e-commerce and distributor channels, a trend enlarging the automotive switch market opportunity outside production lines.

Geography Analysis

Asia Pacific spearheads the automotive switch market with 49.40% revenue in 2025, making it the largest market today. Entrenched supply clusters in China, Japan, South Korea, and India, plus robust EV incentives, keep the region in front as global OEMs scale local production. Thailand’s first electric pickup program and Indonesia’s nickel-rich battery corridor reinforce APAC’s leadership.

The Middle East & Africa, while smaller, posts the fastest 7.43% CAGR through 2031. Saudi Arabia’s USD 2.9 billion pipeline of automotive projects, including Ceer’s USD 1.3 billion EV complex, alongside 50,000 public chargers planned by 2025, accelerates switch demand across Gulf economies. Dubai’s target of 42,000 EVs by 2030 further widens the growth gap.

North America and Europe retain strong positions by marrying premium nameplates with high-content ADAS and infotainment systems. South America gains steady ground as Brazil’s R$30 billion (USD 6.0 billion) Stellantis program secures regional manufacturing. Suppliers able to locate production close to final assembly sites remain best placed to navigate evolving trade and compliance pressures.

Regulatory Landscape

Automotive switches fall under vehicle functional-safety, driver-distraction, identification, and type-approval frameworks that shape control layouts, illumination, and the supporting validation evidence. UNECE UN Regulation No. 121 covers location and identification of hand controls, tell-tales, and indicators, while ISO 2575:2021 standardizes symbols and colors for controls and indicators. In the United States, NHTSA requirements under 49 CFR Part 571 (FMVSS) set mandatory performance, visibility, and control-related requirements that influence design choices for safety-critical functions.

As cockpits move toward more software-defined architectures, compliance expectations are widening from ergonomics and reliability into software and system integrity. UNECE UN Regulation No. 155 (cybersecurity management system) and UN Regulation No. 156 (software update management system) introduce type-approval expectations that push switch modules and body controllers toward secured communication, traceability, and controlled update processes. For commercial vehicle categories, UNECE UN Regulation No. 169 (effective June 19, 2024) on event data recorders raises the bar for diagnostic robustness and survivability in the broader electrical and electronic architecture that switches connect to, while IATF 16949 remains a common quality-management baseline for switch manufacturing, traceability, and end-of-line testing.

Value Chain Analysis

The automotive switch value chain runs from raw materials and electronics inputs through precision manufacturing and tiered distribution into OEM integration and the growing aftermarket. Upstream inputs include copper-based contacts and springs, rare-earth-related materials in certain magnetic sensing designs, plastics and resins for housings, LEDs and light guides for illuminated units, and electronics such as microcontrollers, Hall-effect sensors, and capacitive-sensing ICs that enable smart and touch-based interfaces. Midstream, suppliers manufacture mechanical switches, mechatronic modules, and increasingly CAN and LIN-integrated smart switch assemblies, with production built around IATF 16949 controls, high automation, and rigorous end-of-line functional testing.

Downstream, Tier 1s and specialized switch makers supply OEM programs where integration with wiring harnesses, body control modules, and zonal architectures is validated alongside EMC and functional-safety requirements. Distribution also includes replacement and upgrade demand via aftermarket channels as fleets age, with high-cycle parts such as window, HVAC, stalk, and steering-wheel controls driving ongoing replacement. Recent product activity reflects the technology shift in the chain: Infineon introduced the Power PROFET + 24/48V smart power switch family (April 2025) supporting migration to 48V architectures, and Sensata launched the FaultBreak high-voltage switching and protection contactor (March 2026) aimed at EV safety needs, reinforcing the move toward higher-voltage, software-aware, electronics-heavy switching content.

Competitive Landscape

Global competition is intense yet fragmented. Alps Alpine, Continental and Bosch hold entrenched Tier 1 status owing to extensive validation records and global footprint. Continental’s decision to spin off its automotive division as Aumovio and list it on the Frankfurt exchange in September 2025 signals a strategic pivot to software-centric cockpit electronics. Schaeffler’s October 2024 merger with Vitesco creates a EUR 25 billion powertrain and electronics heavyweight focused on e-mobility synergies.

Scale economies matter: Snaptron now fabricates over 100 million tactile domes annually, and a forthcoming solderable-dome line may double throughput. Patent activity surges around haptic, illuminated, and force-feedback designs that help automakers reduce part counts while elevating perceived quality. Regional challengers in China and India exploit local-content rules to gain bids on new EV programs, pulling the automotive switch market toward dual sourcing models that balance cost with geopolitical resilience.

Winning suppliers blend cost-optimized mechanical units for mass-volume programs with premium capacitive offerings for luxury trims—all while meeting ISO 26262 redundancy mandates. Those that fortify raw-material hedges and cultivate multi-continent manufacturing sites will best offset copper and rare-earth volatility, sustaining margins amid the rapid re-architecture of vehicle interiors driven by the automotive switch market evolution.

Automotive Switch Industry Leaders

Alps Alpine Co. Ltd

Valeo SA

Robert Bosch GmbH

Continental AG

Leopold Kostal GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities concentrate around hybrid HMI architectures that preserve tactile, safety-critical controls while delivering the styling and packaging benefits associated with display-centric cockpits. Euro NCAPs January 2026 safety testing updates, which connect top five-star ratings to physical controls for key functions (direction indicators, hazard lights, horn, wipers, and SOS), create a clearer requirement set that supports demand for dedicated switch hardware and tactile surfaces integrated into cockpit modules. This also increases pull for illuminated and clearly identifiable controls aligned with ISO 2575 and UN Regulation No. 121 conventions, as OEMs harmonize designs across global platforms.

A second whitespace area is material and architecture innovation that reduces part count while increasing reconfigurability and tactile feedback. SAE International published a 2026 technical paper (2026-26-0596) on selectively elevated fabric switch concepts with tactile actuation, which highlights R&D pathways for thin, surface-integrated switches that can replace conventional mechanical assemblies in selected interior zones. With the industry shift toward 48V subsystems and smarter power distribution, including smart power switches for 24/48V, switch suppliers that can bundle sensing, illumination, haptics, and secured in-vehicle networking into modular assemblies have clearer entry points into next-generation cockpit and zonal electrical architectures.

Recent Industry Developments

- May 2026: Alps Alpine demonstrated 48V-compatible detection switches and advanced haptic interior technologies at the Automotive Engineering Exposition 2026 in Yokohama. The exhibit highlighted a push toward higher-voltage architectures and richer tactile user interfaces within software-defined cockpits.

- June 2025: Minda Corporation collaborated with Toyodenso Co. to develop and manufacture advanced automotive switches for the Indian market, spanning two-wheelers and passenger vehicles. The tie-up includes plans for a new manufacturing facility in Noida, expanding localization and supply assurance for domestic OEM programs.

- November 2024: NOVOSENSE Microelectronics introduced a suite of automotive high-side switches designed for body control modules and zonal control unit power distribution. The launch broadens semiconductor options for smarter load driving and protection, aligning with the shift toward electronics-heavy switch and control architectures.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the automotive switch market covers switches used inside and on vehicles to control electrical and electronic functions, and the sizing is captured as revenue generated from the sale of these switches across passenger and commercial vehicles.

Scope exclusions: We exclude broader electronic control units, wiring harnesses, and sensor modules, and we also exclude services and software that do not represent switch hardware revenue.

Segmentation Overview

- By Switch Type

- Mechanical Switches

- Knob

- Button

- Rocker

- Toggle/Paddle

- Touch-based Switches

- Capacitive Touchpad

- Haptic-feedback Surface

- Multifunction / Combination Modules

- Mechanical Switches

- By Application

- Indicator System Switches

- HVAC Controls

- Power Window and Door-Lock Switches

- Steering-Wheel Control Switches

- Seat and Interior Comfort Switches

- Lighting and Wiper Switches

- Engine-Management (EMS) Switches

- By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Medium and Heavy Commercial Vehicles

- By Sales Channel

- OEM

- Aftermarket

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Egypt

- Turkey

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research helped us map the industry structure and set realistic ranges for demand and pricing before we moved into interviews. We relied on public sources such as vehicle production and registration series from government transport departments, trade and customs statistics, and trade association publications related to automotive components and safety.

We also reviewed company annual reports, investor presentations, product catalogs, and reputable news coverage to understand switch adoption in key vehicle functions (for example, steering wheel controls and HVAC panels). Patent databases were used to sense technology shifts like touch and capacitive switching, and a paid subscription for company financials and news supported quick cross-checks on revenue exposure and end market mentions. These desk sources are illustrative, and many other public references were also used to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work was used to confirm what is actually shipped and priced in the market, especially where public data is broad or delayed. We spoke with a mix of component manufacturers, vehicle OEM and Tier supplier functions, and distribution side contacts across major auto producing regions so that adoption assumptions could be tested across different vehicle platforms and price points.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 14% | APAC: 44% |

| Mid tier: 61% | Functional/Unit leaders: 30% | EMEA: 30% |

| Smaller Players: 14% | Managers: 56% | Americas: 26% |

Market-Sizing & Forecasting

The core sizing was built using a top-down approach where vehicle production by region and vehicle type was reconstructed into an install-base demand pool, and then translated into switch value using penetration and content assumptions by application. To keep the totals realistic, we corroborated the result with selective bottom-up checks, including sampled average selling price ranges, channel feedback on mix, and supplier revenue exposure where it was clearly stated.

Inputs that mattered most included passenger versus commercial production trends, the shift in feature content per vehicle (more steering wheel and infotainment controls), electrification related content changes, typical switch counts by cabin and body functions, and price differences between mechanical and touch style switches. For forecasting, scenario analysis was used to reflect different adoption speeds for touch interfaces and comfort features, and then the scenarios were aligned to expert views gathered in interviews. When bottom-up signals were incomplete for smaller applications, gaps were handled through conservative share allocations tied back to vehicle build mix and validated price bands.

Data Validation & Update Cycle

Outputs were checked against independent signals like regional vehicle output, import and export patterns for related components, and the direction of quoted price ranges from interviews. Any large variances were reworked by revisiting assumptions, and then the model went through a second analyst review before sign-off.

The report is refreshed on an annual cycle, and interim updates are made when material events change production outlooks or pricing assumptions. Before delivery, a final freshness pass is completed so the latest public statistics and recent interview feedback are reflected in the numbers clients receive.

Mordor Intelligence's Automotive Switch Market Size Measured Against Other Published Estimates

Published market values for automotive switches can look far apart because the scope and counting rules are not consistent across publishers, even when the titles sound similar. Differences usually come from what is counted as a switch, whether OEM and aftermarket revenues are both included, and how pricing is converted and projected over time.

In practice, the biggest gaps come from whether adjacent cockpit modules are bundled into the switch value, how touch and multifunction controls are priced (separating the switch element from the surrounding trim and electronics), and whether the base year is aligned to the same production cycle across regions. Some sources also use older currency conversion points, which can inflate or deflate the same physical demand when reported in USD, and their refresh cadence can miss a year of model changeovers.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 46.42 B (2026) | |

| Global Consultancy A | USD 50.73 B (2026) | This estimate appears to apply a broader value capture around cockpit and comfort controls, which can pull in non-switch electronics and higher blended pricing, and this widens totals versus a switch-only revenue view. |

| Regional Consultancy B | USD 18.10 B (2023) | The lower figure is consistent with a narrower product definition or partial channel coverage, and it also uses an earlier base year that can understate the current feature-content uplift seen in newer vehicle programs. |

The spread across the table is mostly explained by what gets bundled into the switch value and how base-year pricing is carried forward. By tying demand to vehicle production, application level switch content, and interview-tested price bands, the scope stays focused on switch revenue rather than broader cockpit electronics, a modeling choice applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the current size of the automotive switch market?

The automotive switch market stands at USD 46.42 billion in 2026 and is projected to grow to USD 60.09 billion by 2031.

Which switch type holds the largest market share today?

Mechanical designs dominate with 93.35% revenue share in 2025 because of their proven tactile reliability.

Why are HVAC controls the fastest-growing application?

Electric vehicles rely on precise thermal management to protect driving range, so OEMs integrate more sophisticated HVAC interfaces.

Which region is expanding most quickly?

The Middle East and Africa segment records a 7.43% CAGR through 2031, supported by large-scale EV manufacturing and charging-infrastructure programs in Saudi Arabia and the UAE.

Page last updated on: