North America Automotive Collision Repair Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

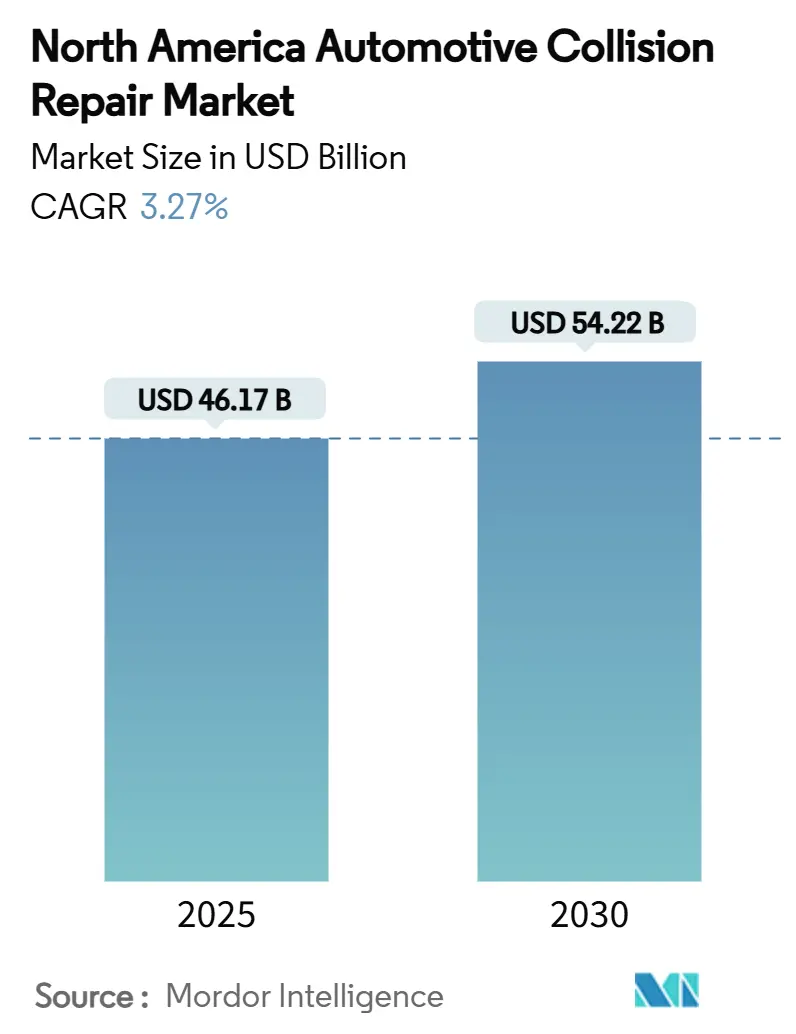

| Market Size (2025) | USD 46.17 Billion |

| Market Size (2030) | USD 54.22 Billion |

| Growth Rate (2025 - 2030) | 3.27% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Automotive Collision Repair Market Analysis by Mordor Intelligence

The North America Automotive Collision Repair Market size is estimated at USD 46.17 billion in 2025, and is expected to reach USD 54.22 billion by 2030, at a CAGR of 3.27% during the forecast period (2025-2030). Private-equity investment worth more than USD 9 billion since late 2023 underscores investor confidence in the sector’s predictable cash flow profile as well as its resilience to economic cycles.[1]“Private Equity Investment Trends 2025,” PitchBook Data, pitchbook.com Stricter safety regulations, especially NHTSA’s mandate for automatic emergency braking on all light vehicles by September 2029, are reshaping repair complexity and elevating average ticket values through mandatory ADAS calibrations.[2]“Automatic Emergency Braking Final Rule,” National Highway Traffic Safety Administration, nhtsa.gov The average vehicle age rose to 12.7 years in 2024 and is expected to reach 13 years by 2026, keeping repair volumes steady even as unit collision frequency declines. Digitally enabled insurance workflows are streamlining claims while favoring shops equipped with integrated management platforms, reinforcing the shift toward multi-shop operator (MSO) consolidation.

Key Report Takeaways

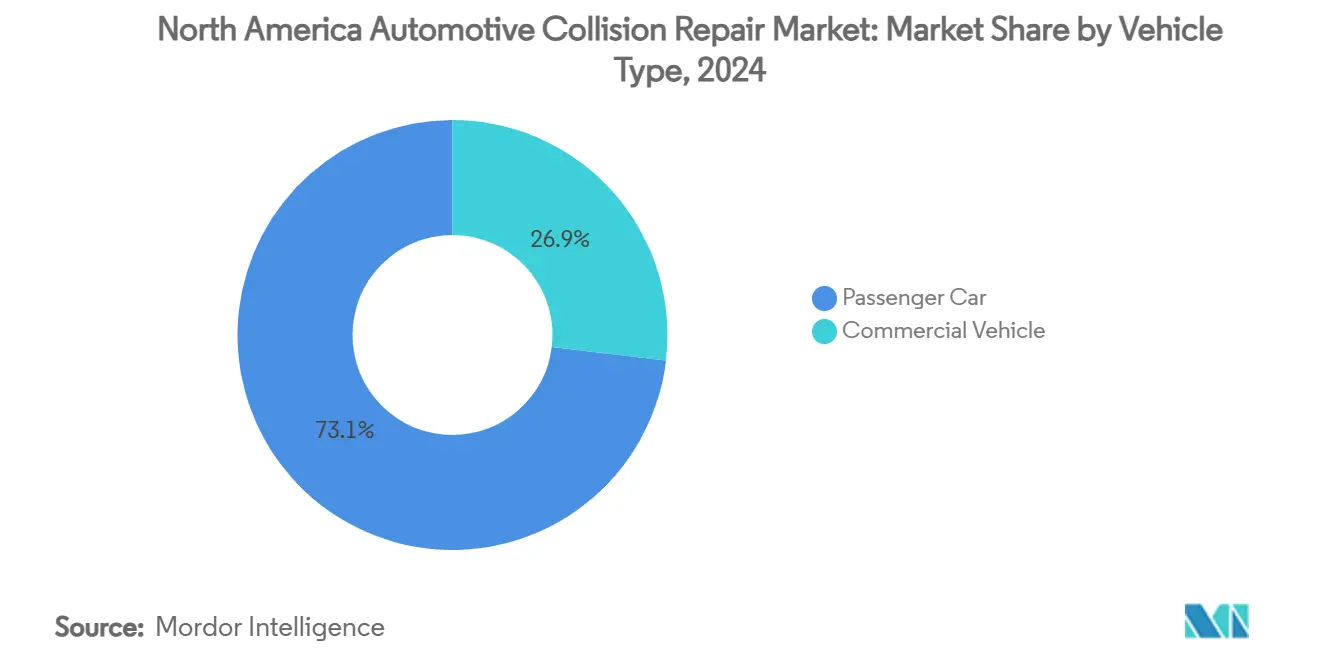

- By vehicle type, passenger cars commanded 73.14% of the North America automotive collision repair market size in 2024, while commercial vehicles recorded the highest projected CAGR at 3.34% through 2030.

- By product, paints & coatings led with 43.11% revenue share in 2024, and spare parts are poised to grow at a 3.41% CAGR to 2030.

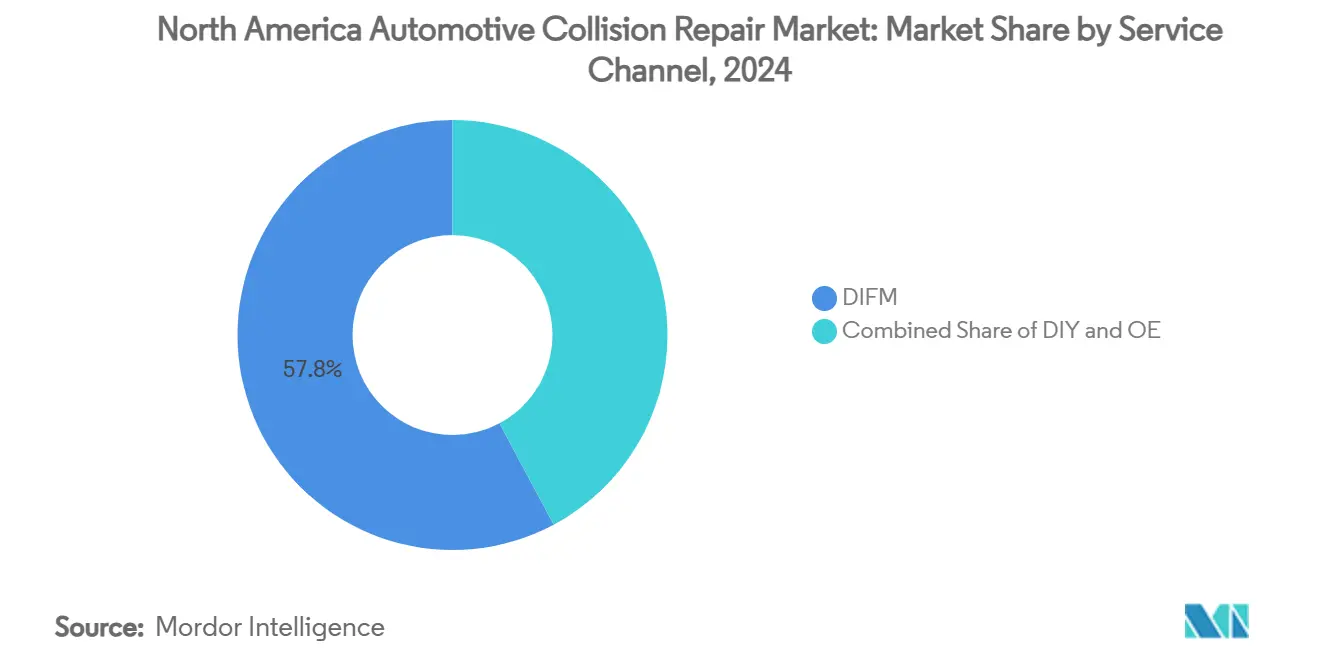

- By service channel, DIFM services accounted for 57.81% share of the North America automotive collision repair market size in 2024, whereas OE services are advancing at a 3.64% CAGR through 2030.

- By damage type, cosmetic & paint repairs captured 46.21% share in 2024 and glass & ADAS calibration is progressing at a 3.45% CAGR to 2030.

- By geography, the United States held 83.63% of the North America automotive collision repair market share in 2024, while Rest of North America is forecast to expand at a 3.51% CAGR through 2030.

Worldwide, activity is shaped by contributions from multiple regions, with North america representing one of the more structurally developed among them. The global report on automotive collision repair market by Mordor Intelligence reflects how these regional layers combine into a single system.

North America Automotive Collision Repair Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing fleet extending repair | +0.7% | North America | Long term (≥ 4 years) |

| Stringent U.S. and Canada safety regulations | +0.6% | United States and Canada | Medium term (2-4 years) |

| ADAS calibration boosting repair ticket size | +0.4% | United States and Canada | Medium term (2-4 years) |

| Growing vehicle parc and VMT | +0.3% | United States, Canada, Mexico | Long term (≥ 4 years) |

| Digital-first insurance workflows | +0.3% | United States and Canada | Short term (≤ 2 years) |

| PE-backed MSO | +0.2% | United States, spill-over to Canada | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ageing Fleet Extending Repair Demand

The average North American passenger vehicle age rose to 14.5 years, while light trucks averaged 11.9 years. Vehicles older than seven years now account for 45% of repairable claims, nine points higher than in 2019. Older units increase demand for aftermarket or recycled parts, whereas newer models require OEM components and ADAS calibrations, producing a bifurcated sourcing landscape. Total-loss frequency reached 22% of claims in 2024, enlarging salvage supply chains operated by recyclers capable of rapid dismantling and e-commerce distribution. Shops with diverse sourcing and mixed-technology expertise are better positioned to monetize both ends of this age spectrum. The trend establishes a floor under collision repair volumes despite technology-driven frequency reductions.

Stringent U.S. & Canada Safety Regulations

Harmonized safety standards between NHTSA and Transport Canada introduce complex compliance obligations that smaller independents struggle to absorb. The automatic emergency braking requirement effective September 2029 stimulates near-term demand because older vehicles without AEB remain more collision-prone. Larger MSOs with OEM certifications gain a regulatory advantage, as manufacturers increasingly dictate specialized tools and training for warranty-compliant repairs. FMVSS No. 305a covering electric-vehicle safety, effective December 2025, pushes operators to invest in high-voltage protocols that raise capital barriers for new entrants. The dynamic encourages consolidation as compliance costs climb and scale efficiencies become critical to profitability.

Growing Vehicle Parc & VMT in North America

Vehicle miles traveled climbed from 2.77 trillion miles in 2021 to 3.26 trillion miles in 2023, increasing exposure to collision risk even as per-vehicle frequency trends downward. The region’s light-duty fleet reached 197 million units, while average annual miles per vehicle rose from 10,775 to 11,408. E-commerce growth propels commercial-vehicle utilization, compelling fleet owners to prioritize uptime and speed of repair. Labor markets responded as Canadian automotive repair employment expanded to 112,166 workers in 2022. Urban corridors face capacity constraints, giving multi-location brands an edge in negotiating insurer-preferred status. Rural markets lean toward mobile repair models due to longer travel distances and parts logistics challenges.

Digital-First Insurance Workflows

Artificial-intelligence damage assessment platforms now trim initial inspection times by as much as 40%. Insurers rely on data-rich photo estimates, reducing adjuster site visits and compressing claim cycles. MSOs equipped with end-to-end management systems integrate seamlessly with carrier platforms, earning higher referral volumes. Photo-based estimating obliges shops to invest in imaging infrastructure and staff training, raising operational standards. Predictive analytics embedded in claims systems facilitate proactive maintenance outreach, creating incremental revenue opportunities. Smaller independents without IT resources risk exclusion from insurer direct-repair programs, accelerating consolidation momentum within the North America automotive collision repair market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ADAS and active-safety lowering collision | -0.5% | United States and Canada | Medium term (2-4 years) |

| Certified-technician shortage | -0.4% | North America | Long term (≥ 4 years) |

| Parts-supply | -0.3% | North America | Short term (≤ 2 years) |

| VOC limits on refinish coatings | -0.2% | United States and Canada | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

ADAS & Active-Safety Lowering Collision Frequency

Mandatory automatic emergency braking could prevent at least 24,000 injuries and at least 360 deaths annually once fully adopted. Rear-end crash frequency is already decreasing, chipping away at lower-severity job volume. However, ADAS components inflate severity when accidents occur because damaged sensors and wiring harnesses are expensive. Shops unable to handle calibrations lose work to equipped competitors. Insurers are recalibrating actuarial models, potentially reducing premium inflows that fund repairs. The net effect is fewer repairable events but higher revenue per incident across the North American automotive collision repair market.

Certified-Technician Shortage

Collision-repair technician employment fell drastically over the year, while annual demand for new technicians increases exponentially through 2025. Vehicle electrification and lightweight materials require specialized training that traditional vocational programs are slow to deliver. Caliber Collision’s apprenticeship initiative graduated more than 1,000 technicians in 2024, leaving a sizable deficit. Wage inflation elevates operating costs and extends cycle times as shops queue work behind limited labor availability. The shortage restricts output capacity, tempering growth in the North American automotive collision repair market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial-Vehicle Uptick Outpaces Overall Growth

In 2024 passenger cars retained 73.14% of the North America automotive collision repair market share, yet their growth rate lags as private ownership plateaus and safety technology proliferates. Commercial vehicles represent the fastest-expanding slice of the North America automotive collision repair market, advancing at a 3.34% CAGR through 2030. Fleet units demand rapid turnaround to maintain logistics schedules, and operators often negotiate national contracts that funnel volume to MSOs equipped with uniform processes. Fleet operators prolong asset life amid high interest rates, raising collision exposure over extended service cycles. Electric vans introduce battery-pack safety checks and insulated tool requirements, heightening labor specialization needs.

Tighter delivery windows mean fleets prioritize shop capacity and reliability over cost, creating pricing power for consolidators. Data-rich telematics platforms facilitate proactive damage triage, enabling parts-ordering before the vehicle arrives. Commercial-vehicle growth therefore buffers aggregate demand even as private-vehicle frequency softens. The segment’s rising revenue share strengthens the long-term outlook for the North America automotive collision repair market.

By Product: Spare-Parts Revenue Accelerates on Aging Fleet

Paints & coatings accounts for 43.11% of the North America automotive collision repair market share in 2024, whereas spare parts revenue is forecast to climb at a 3.41% CAGR. Rising average vehicle age and higher ADAS component density compel more component replacements, boosting parts turnover. Supply-chain disruptions elevate inventory-carrying costs, favoring distributors that integrate coatings, consumables, and mechanical items under one umbrella, as illustrated by LKQ Refinish’s 2024 formation.

Glass parts are evolving from simple windshields into sensor-housing structures needing precise fit and calibration. Consumables remain stable but see product-mix shifts toward low-VOC materials. Integrated distribution networks improve fill rates, reduce cycle times, and enhance supplier leverage across the North America automotive collision repair market.

By Service Channel: OE-Certified Shops Extend Reach

In 2024 DIFM captured 57.81% of the North America automotive collision repair market size, reflecting consumers’ preference for professional repairs on increasingly sophisticated vehicles. OE services are projected to expand at a 3.64% CAGR as automakers deepen involvement in post-sale touchpoints. Certified OE programs steer warranty repairs to authorized facilities, raising hardware and training standards.

Insurers appreciate OE-certified quality control and channel more volume to such networks, reinforcing their growth. DIY participation continues to shrink because ADAS and electrification elevate technical barriers. Technology adoption in scheduling and estimate transparency improves customer satisfaction and loyalty, supporting the ongoing shift toward professionalized channels.

By Damage Type: Glass & ADAS Blend Drives Ticket Growth

In 2024 cosmetic & paint work still accounted for 46.21% of revenue, yet rising sensor integration forces windscreen replacements to include camera and radar alignment. Glass & ADAS calibration services are set to grow 3.45% annually through 2030, outpacing other damage categories.

Calibration mistakes can disable safety systems, exposing shops to liability, which in turn pushes insurers to prefer facilities with documented calibration capability. Electric vehicles contribute more complex damage regimes, including battery isolation and thermographic imaging post-impact. These factors raise average repair severity, bolstering top-line growth within the North America automotive collision repair market.

Geography Analysis

The United States dominates the North American automotive collision repair market with an 83.63% revenue share in 2024, supported by the highest number of registered light-vehicle fleet. Private-equity capital concentrates on dense metropolitan corridors where repair volumes justify multi-location footprints, while rural areas remain less consolidated and dependent on independent shops. Insurance regulatory frameworks favor standardized repair protocols that MSOs can meet at scale.

Canada contributes unique dynamics to the North American automotive collision repair industry. EV collision claims averaged CAD 6,534, exceeding comparable U.S. repairs. Cross-border operators such as Boyd Group deploy shared procurement and training models that leverage exchange-rate arbitrage and harmonized safety standards.

Rest of North America—chiefly Mexico—anchors future expansion potential as vehicle ownership rises and domestic manufacturing capacity grows. The region is forecast to achieve a 3.51% CAGR to 2030. USMCA provisions simplify parts movement, yet variability in local regulations and fragmented market structure necessitate partnerships with established Mexican service networks. Operators equipped with bilingual customer interfaces and localized supply chains stand to capture incremental share in this high-growth corridor of the North America automotive collision repair market.

Mordor Intelligence provides coverage of the automotive collision repair market across other key regional markets, including Europe and Asia, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The market remains moderately fragmented. Approximately 40,000 repair shops operate in the United States. Still, the five largest MSOs together controlled the largest number of locations and a significant chunk of 2024 revenue.[4]“Company Fact Sheet 2025,” Caliber Collision, calibercollision.com MSOs leverage shared services hubs, centralized parts procurement, and proprietary training academies to widen the operational gap over independents.

Strategic initiatives concentrate on technology adoption. Crash Champions’ integration with Service King to create more than 550 shops allows investment in AI-based estimating and ADAS calibration bays. Gerber, part of Boyd Group, deploys a single enterprise resource platform across all 985 North American sites to standardize cycle-time metrics and insurer reporting. Classic Collision employs geographic clustering to decrease parts-delivery latency and improve labor utilization within high-density urban markets.

White-space opportunities exist in mobile services and dedicated ADAS centers. Several consolidators pilot on-site calibration vans that travel to satellite shops lacking equipment. Equipment manufacturers collaborate with MSOs to validate new alignment targets and software, forging co-development agreements. Competitive advantage increasingly hinges on data integration, with leading operators analyzing telematics and claims datasets to forecast parts demand and optimize staffing. These shifts fortify the long-term performance of the North America automotive collision repair market.

North America Automotive Collision Repair Industry Leaders

Caliber Collision

Boyd Group Services

Crash Champions

Classic Collision

Joe Hudson’s Collision Centers

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: CollisionRight reached 100 collision-repair shops after acquiring Tripp’s Collision in Michigan, positioning it as the sixth-largest MSO and outlining plans to triple its footprint within five years.

- June 2024: LKQ Corporation merged its PBE and FinishMaster businesses to establish LKQ Refinish, offering integrated coatings and parts distribution to more than 40,000 collision-repair customers across North America.

- January 2024: Summit Partners committed growth capital to CollisionRight to support continued acquisition of high-quality regional collision-repair shops in the Central United States and Mid-Atlantic.

North America Automotive Collision Repair Market Report Scope

| Passenger Car |

| Commercial Vehicle |

| Paints & Coatings |

| Consumables |

| Spare Parts |

| Glass |

| Other Product |

| DIY |

| DIFM |

| OE |

| Structural Repair |

| Cosmetic & Paint |

| Glass & ADAS Calibration |

| United States |

| Canada |

| Rest of North America |

| By Vehicle Type | Passenger Car |

| Commercial Vehicle | |

| By Product | Paints & Coatings |

| Consumables | |

| Spare Parts | |

| Glass | |

| Other Product | |

| By Service Channel | DIY |

| DIFM | |

| OE | |

| By Damage Type | Structural Repair |

| Cosmetic & Paint | |

| Glass & ADAS Calibration | |

| By Geography | United States |

| Canada | |

| Rest of North America |

Key Questions Answered in the Report

What is the current size of the North America automotive collision repair market?

The North America automotive collision repair market size reached USD 46.17 billion in 2025 and is projected to grow to USD 54.22 billion by 2030.

Which geographic segment leads the market?

The United States dominates with an 83.63% revenue share, supported by a 289 million-unit light-vehicle fleet and mature insurance infrastructure.

How are ADAS systems affecting repair costs?

ADAS calibration adds USD 250–600 to each repair order and raises tooling requirements, lifting average repair severity even as collision frequency gradually declines.

Why is private-equity interest increasing in collision repair?

Defensive cash flows, rising labor rates, and scalable consolidation opportunities have driven more than USD 9 billion of private-equity investment since 2023.

Which service channel is expanding fastest?

OE-certified repair networks are projected to grow at a 3.64% CAGR to 2030 as automakers strengthen post-sale engagement and insurers favor certified facilities.

What is the biggest operational challenge facing repair shops?

A certified-technician shortage is constraining capacity, driving wage inflation, and lengthening cycle times, especially for complex ADAS and electric-vehicle repairs.

Page last updated on: