Automotive Body-in-White Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 146.92 Billion |

| Market Size (2031) | USD 174.67 Billion |

| Growth Rate (2026 - 2031) | 3.52% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Body-in-White Market Analysis by Mordor Intelligence

The automotive body-in-white market size in 2026 is estimated at USD 146.92 billion, growing from 2025 value of USD 141.92 billion with 2031 projections showing USD 174.67 billion, growing at 3.52% CAGR over 2026-2031. Momentum stems from regulatory pressure for lighter vehicles, rapid electrification, and the spread of giga-casting that cuts part count while boosting torsional rigidity. Automakers favor third-generation advanced high-strength steel for cost-effective weight reduction, even as aluminum, composite, and magnesium solutions gain ground. Tier-1 suppliers are responding with integrated multi-material offerings and localized production footprints that shorten supply chains and align with carbon-border policies. Meanwhile, Chinese OEMs’ pioneering of structural battery packs and giga-castings is reshaping global competitive dynamics, forcing incumbents to accelerate capital spending on next-generation body shops.

Key Report Takeaways

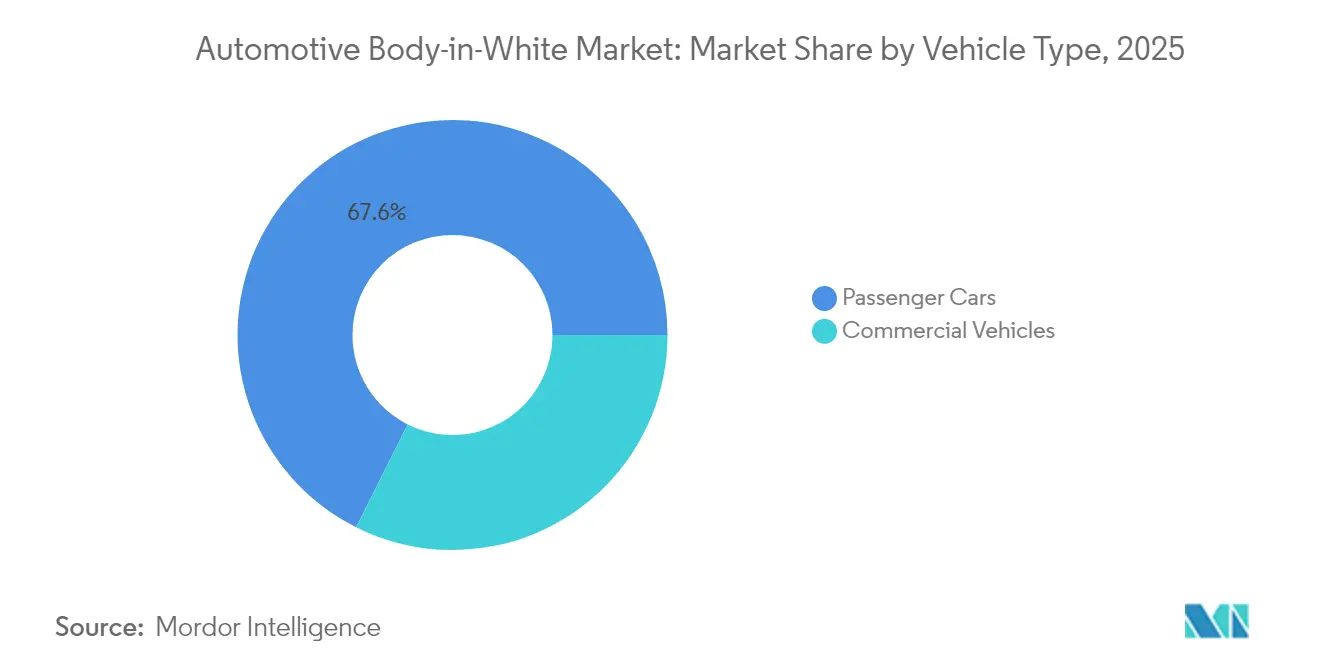

- By vehicle class, passenger cars captured 67.60% of the automotive body-in-white market size in 2025, yet commercial vehicles are expected to lead growth with a 4.43% CAGR through 2031.

- By propulsion, internal-combustion engines accounted for 62.70% of the automotive body-in-white market share in 2025, whereas electric vehicles are set to post an 10.84% CAGR up to 2031.

- By material type, steel commanded 62.80% of the automotive body-in-white market size in 2025; aluminum is forecast to register the fastest 6.07% CAGR during 2026-2031.

- By material joining technique, resistance spot welding retained 57.20% of the automotive body-in-white market share in 2025, while adhesive and hybrid bonding solutions are advancing at a 3.76% CAGR over 2026-2031.

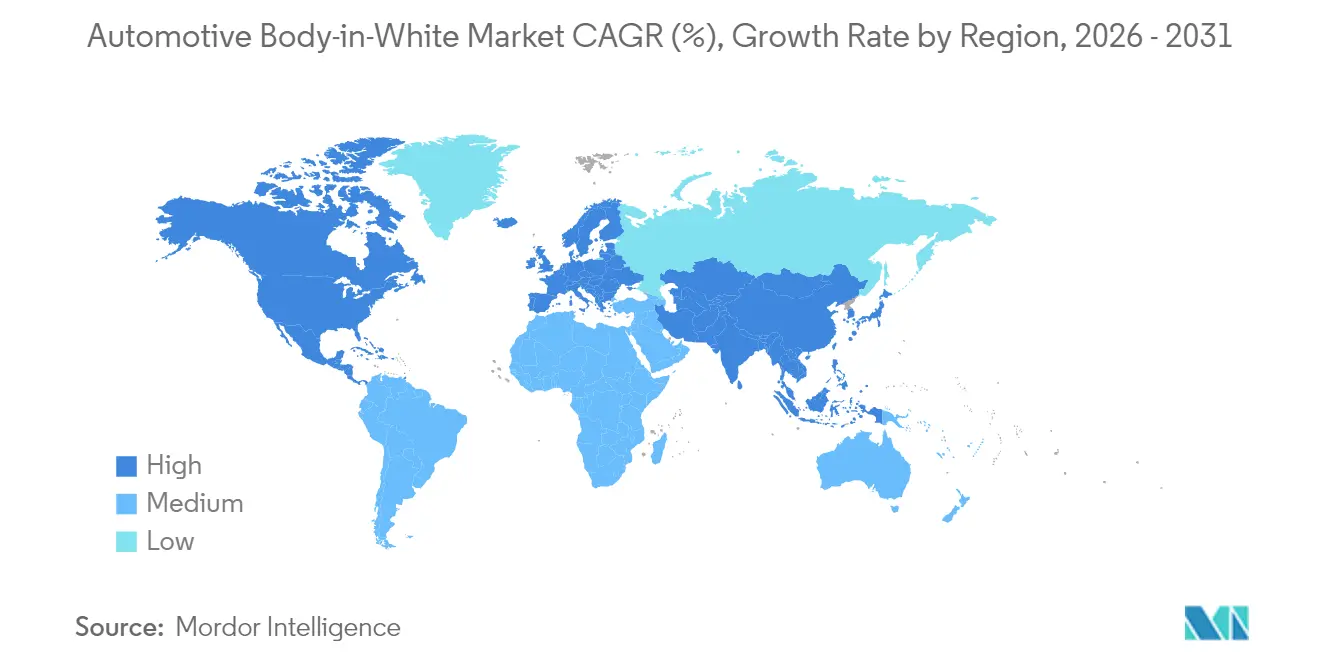

- By geography, Asia-Pacific held 45.60% of the automotive body-in-white market share in 2025, while the region is projected to expand at a 4.69% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Body-in-White Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Lightweight Vehicles | +1.2% | Global, with early adoption in Europe and North America | Medium term (2-4 years) |

| Rapid Scaling of EV Production Platforms | +1.1% | China, Europe, North America core; expanding to ASEAN | Short term (≤ 2 years) |

| Stringent Global CO₂ and Fuel-Economy Regulations | +0.9% | Europe, North America, China leading; spillover to emerging markets | Long term (≥ 4 years) |

| Advances In High-Strength Steel and Aluminum Alloys | +0.8% | Global, with R&D concentration in Germany, Japan, South Korea | Medium term (2-4 years) |

| Adoption of Giga-Cast Structures by Chinese EV OEMs | +0.7% | China leading, spreading to global EV manufacturers | Short term (≤ 2 years) |

| Greenfield ASEAN EV Plants Boosting Local BIW Capacity | +0.6% | ASEAN core, serving regional and export markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Lightweight Vehicles

As global markets tighten regulatory standards, the automotive industry is increasingly turning to lightweighting. Automakers are now embracing advanced materials and innovative design strategies to shed vehicle weight, all while upholding safety and performance standards. Next-generation high-strength steels are at the forefront, delivering notable weight reductions without sacrificing structural integrity or crash safety. Concurrently, as electric vehicle adoption surges, there's a heightened emphasis on lighter body structures; even slight weight cuts can lead to substantial improvements in driving range.

Though aluminum space frames have gained traction in premium segments, their elevated production costs hinder broader acceptance in the mass market. Consequently, manufacturers are meticulously weighing performance, cost, and manufacturability in their material selections.

Rapid Scaling of EV Production Platforms

Dedicated EV platforms slash part counts and enable structural battery packs that double as load paths. Tesla’s Austin plant reports a 30-40% component reduction after shifting to integrated front and rear giga-castings[1]Tesla Inc., “2025 Impact Report,” Tesla, tesla.com. BYD and NIO employ cell-to-pack architecture requiring new bonding and thermal-barrier solutions. The demand for enhanced electrical isolation surges as premium electric vehicles embrace high-voltage architectures, leading to a growing reliance on composite inserts in structural components. The heft of sizable battery packs amplifies the necessity for ultra-strong materials and refined structural designs. In response, automakers are turning to advanced steels and employing topology optimization to harmonize safety, performance, and efficiency in their next-gen vehicle platforms.

Stringent Global CO₂ and Fuel-Economy Regulations

EU Fit for 55 targets full zero-emission new-car sales by 2035, embedding weight reduction into program budgets. China’s dual-credit scheme incentivizes lightweighting to unlock favorable NEV scores[2]China Association of Automobile Manufacturers, “NEV Monthly Data,” CAAM, caam.org.cn. United States CAFE rules seek 40.4 mpg fleet averages in 2026, pushing multi-material designs once limited to luxury segments. Vehicle developers are increasingly feeling the pinch of compliance costs, which consume a significant chunk of their program budgets. Many are optimizing the body-in-white structure as a savvy, cost-effective strategy to navigate regulatory demands. Meanwhile, introducing carbon border adjustment mechanisms (CBAM) will reshape material sourcing. By penalizing imports of carbon-heavy steel, CBAM is nudging the industry towards greener, low-emission feedstocks. Such shifts underscore the importance of lightweighting and material efficiency in automotive design and procurement.

Greenfield ASEAN EV Plants Boosting Local BIW Capacity

To lure electric vehicle (EV) assemblers, Thailand, Indonesia, and Vietnam are rolling out extended tax holidays. These incentives aim to position the countries as competitive hubs for EV manufacturing in the region. The newly established plants boast modular body shops, tailored for versatile multi-material lines. These advanced facilities are designed to accommodate evolving manufacturing needs, ensuring a steady demand for adhesives, laser welding, and high-strength steels in the future. Additionally, the focus on modularity and flexibility highlights the region's commitment to fostering innovation and meeting the growing global demand for EVs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Advanced BIW Materials | -0.8% | Global, most acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Complex Joining and Repair of Multi-Material Structures | -0.6% | Developed markets with established service networks | Medium term (2-4 years) |

| Scarcity of Low-Carbon Steel/Aluminum Supply | -0.5% | EU and North America leading green material adoption | Long term (≥ 4 years) |

| Insurance and Repair-Cost Risks for Giga-Cast Bodies | -0.4% | Markets with advanced EV adoption and giga-casting | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced BIW Materials

Lightweight materials are pivotal to automotive innovation, yet their adoption hinges on a web of cost, infrastructure, and supply chain dynamics. Aluminum, celebrated for its weight-saving advantages, commands a notable premium over conventional steel. This price disparity renders aluminum more suited for premium vehicle segments, sidelining it from mass-market applications. Meanwhile, carbon fiber-reinforced plastics (CFRP) boast an outstanding strength-to-weight ratio, yet their high material and processing costs restrict their use predominantly to ultra-luxury vehicles.

Moreover, while metals benefit from established recycling infrastructures, composites lag significantly, inflating ownership costs and curtailing the potential for a circular economy. Aluminum is a prime example. The unpredictability of raw material prices further muddies sourcing strategies, posing challenges for manufacturers' long-term planning.

Complex Joining and Repair of Multi-Material Structures

Immaculate surface preparation and oven curing are essential for adhesive-bonded joints, leading to heightened capital expenditure and risks associated with takt time. These processes ensure the durability and reliability of the joints, which are critical in various applications. To avert galvanic attacks, aluminum-steel interfaces require isolation layers; overlooking these process steps can lead to latent warranty exposures, potentially impacting long-term performance[3]Gestamp Automoción, “Multi-Material Joining Guidelines,” Gestamp, gestamp.com. In collision repairs, replacing entire sections can elevate claim values by as much as 60%, significantly increasing repair costs for insurers and customers. Diverse proprietary systems necessitate extended training hours and a broader parts inventory for body shops, adding complexity to operations and rising operational expenses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Vehicles Drive Structural Innovation

Passenger cars represented 67.60% of the automotive body-in-white market size in 2025, whereas commercial vehicles are forecast to compound at 4.43% through 2031. Fleet operators prioritize lifetime operating savings, accepting the material premiums of aluminum space frames that cut mass and extend electric range. Electric vans carrying 100 kWh packs need 20-30% extra reinforcement, spawning demand for ultra-high-strength steel cross-members. Over the forecast, modular ladder-frame concepts will let truck OEMs mix cargo boxes, cabins, and fuel-cell mounts on one chassis, rewarding BIW suppliers that design standardized joining flanges.

Longer product cycles in commercial platforms—up to 10 years—provide volume stability for capital-intensive hot-stamping lines. Regulatory layers, such as the EU’s General Safety Regulation mandating driver-assistance sensors, push BIW designs to embed protected electronics cavities. The 2027 U.S. Phase 2 greenhouse-gas rules for heavy trucks will further widen demand for lightweight beams and cross-members, supporting steady growth in the automotive body-in-white market.

By Propulsion Type: Electric Vehicles Reshape Structural Requirements

Internal combustion engines hold a 62.70% share of the automotive body-in-white market 2025. Electric cars and trucks are rising quickly with an 10.84% CAGR through 2031. Structural battery packs eliminate separate floor pans and raise torsional stiffness by 15-20%, letting automakers delete cross rails and simplify crash-load paths. The shift to 800 V electrics ups insulation mandates, steering engineers toward composite or coated aluminum enclosures. Internal-combustion models still dominate unit volumes, preserving baseline demand for hydro-formed steel side sills optimized for crash energy absorption. Over 2026-2031, dual body architectures will coexist, compelling suppliers to maintain parallel welding and bonding competencies in the automotive body-in-white market.

Range anxiety also sustains lightweighting budgets because each kilogram trimmed from the body returns 2-3 km of driving distance. Finally, EU battery regulations require design-for-disassembly, so OEMs are replacing welded brackets with bolt-on or rivet systems that enable pack removal without structural damage.

By Material Type: Aluminum Gains Despite Steel Dominance

Steel commanded 62.80% of the automotive body-in-white market share in 2025, bolstered by low cost and mature supply chains. Yet aluminum is set to outpace steel with a 6.07% CAGR as producers roll out 7000-series sheets that hit steel-like strength at a 40% weight saving. Third-generation AHSS still expands, reaching >1,500 MPa tensile strength and supporting 25-30% gauge reductions on roof rails. Composite and magnesium content will inch upward but remain niche until recycling and cost hurdles fall.

Europe’s CBAM favors low-carbon metals, advantaging Nordic aluminum smelters powered by hydroelectricity. Regional discrepancies in scrap collection impede uniform adoption; Europe already recycles 95% of automotive aluminum, while emerging markets hover near 70%. Over time, supply security and decarbonization pressure make aluminum the principal challenger to steel in the automotive body-in-white market.

By Material Joining Technique: Adhesives Challenge Welding Dominance

Resistance spot welding still held 57.20% of the automotive body-in-white market share in 2025, underpinned by global line saturation and standardized electrode tooling. Adhesive and hybrid bonding will post a 3.76% CAGR to 2031, propelled by multi-material bodies where weld nuggets risk brittle failures. Structural adhesives excel at load distribution and electrical insulation, vital for 800 V EV architectures. Laser welding adoption picks up in premium segments for its narrow heat-affected zones that protect thin-gauge aluminum. Friction stir welding enables hermetic battery enclosures, and self-piercing rivets satisfy circular-economy policies that mandate reversibility. Line operators now earn certification across up to six joining processes, a sharp rise from two a decade ago, underscoring skills complexity within the automotive body-in-white market.

Geography Analysis

Asia-Pacific commanded 45.60% of the automotive body-in-white market share in 2025 and is tracking a 4.69% CAGR to 2031. China drives volume via New Energy Vehicle quotas, while BYD and NIO champion structural battery packs that reshape load-path design. Japanese steelmakers advance 1,500 MPa AHSS, supplying domestic and ASEAN factories. South Korea clusters BIW, battery, and module suppliers, accelerating vertical integration.

Europe retains technological leadership in multi-material joining and decarbonized production. German toolmakers ship hot-stamping lines with localized quench zones. Nordic aluminum producers are now supplying feedstock with a markedly reduced carbon footprint, outpacing traditional coal-based smelters in the automotive manufacturing sector. With the introduction of carbon border adjustment mechanisms (CBAM) imposing taxes on high-emission imports, the advantages of these Nordic producers are becoming more sharply focused. Automakers are pivoting towards low-carbon materials and body-in-white optimization, coupled with escalating compliance costs, frequently taking up a significant portion of vehicle program budgets. These strategies align with regulatory demands and serve as prudent measures to sidestep potential penalties.

North America grows steadily due to USMCA content rules and EV investments. United States factories reinvest in aluminum-ready presses, while Mexican plants supply cost-competitive stampings under regional-content thresholds. Canadian smelters leverage hydroelectric power to attract OEMs seeking low-carbon aluminum. Labor cost differentials versus Asia remain a headwind, but onshoring incentives and logistical resilience keep capacity expansion on track for the automotive body-in-white market.

Regulatory Landscape

Regulation affecting body-in-white (BIW) design is tightening around emissions compliance, safety performance, and trade measures, pushing OEMs and suppliers to re-optimize structures for mass reduction without sacrificing crashworthiness. In the United States, the EPA finalized multipollutant emissions standards for light-duty and medium-duty vehicles in April 2024, phasing in for model years 2027 through 2032, which strengthens the business case for lightweight BIW architectures and multi-material strategies.

Safety and market-access rules are also moving forward through harmonized frameworks. UNECE WP.29 continues to update global safety requirements, including amendments tied to occupant protection such as the 06 series of amendments to UN Regulation No. 95 on lateral collision occupant protection, while ongoing WP.29 work on automated driving safety provisions increases cross-functional compliance needs for BIW programs that must package sensors and protected electronics cavities. Trade policy remains a material variable for BIW inputs and subassemblies, with US Section 232 actions including an April 2025 proclamation imposing 25% tariffs on imported automobiles and certain auto parts, and a March 2026 Federal Register notice opening an April 2026 inclusions window for automobile parts under the Section 232 tariff inclusions process. This reinforces localization and sourcing diversification for stampings, castings, and joining consumables.

Value Chain Analysis

The BIW value chain starts upstream with primary and low-carbon feedstocks and semi-finished products, led by steel and aluminum producers such as Nippon Steel, ArcelorMittal, and Hyundai Steel, before moving into coil service, blanking, and forming into stampings, extrusions, and castings. Midstream, Tier-1 and Tier-2 specialists handle die engineering, hot stamping, welding and adhesive bonding, hemming, and sub-assembly of closures and underbodies, then sequence modules to OEM body shops located near paint operations. Logistics constraints favor local-for-local manufacturing of large structural assemblies in these cases.

Downstream value creation increasingly comes from co-engineering and process validation rather than part-by-part supply, as OEMs adopt multi-material architectures and higher automation in body shops. ArcelorMittal’s Multi Part Integration (MPI) approach, for example, consolidates BIW parts, while Novelis has worked with Li Auto on aluminum-intensive BIW applications (Li MEGA using Advanz 6HS-s650 aluminum for an 11% weight reduction). Capacity localization is also visible through stampers such as Gestamp, which inaugurated a new hot-stamping plant in Piracicaba, Brazil (June 2026). Bottlenecks still tend to cluster around long die-design and tool lead times (often 12 to 18 months) and the complexity of validating mixed joining routes, including spot and laser welding combined with structural adhesives, for durability, corrosion management, and repairability.

Competitive Landscape

The automotive body-in-white market is seeing a shift in competitive dynamics. Companies are now prioritizing cross-material expertise and establishing proximity to OEM EV hubs. Magna expanded its giga-casting capabilities in a strategic move with a 2025 acquisition of a German aluminum caster, directly challenging Tesla's in-house approach. Meanwhile, Gestamp's intensified focus on hot-stamped steel components for Volkswagen's EV platform highlights the enduring relevance of steel, even as aluminum gains traction. Thyssenkrupp's collaboration with a Chinese battery manufacturer points to a strategic shift towards integrated body-battery modules catering to local OEMs. While regional supply chain localization offers opportunities for emerging suppliers from ASEAN and India, challenges like high capital expenditure and the need for specialized process knowledge hinder the swift displacement of established players.

Automotive Body-in-White Industry Leaders

Magna International Inc.

Gestamp Automocion SA

Autokiniton US Holdings, Inc (Tower International)

Benteler International AG

KIRCHHOFF Automotive GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Automaker and supplier investment in North American and Latin American manufacturing footprints is creating near-term whitespace for BIW stamping, hot forming, joining automation, and line-retrofitting services that support multi-model flexibility and EV-specific underbody structures. In 2026, multiple OEM announcements highlighted body shop and press-shop modernization needs, including Mercedes-Benz outlining a USD 4 billion investment plan at its Alabama facility through 2030 with body shop enhancements, and Hyundai Motor Group detailing a USD 485 million press-shop expansion at its Metaplant America campus in Georgia. These programs point to sustained demand for advanced dies, hot-stamping capacity, robotic joining cells, and process engineering that can handle higher-strength steels, aluminum-intensive designs, and faster model changeovers.

Process digitization and advanced joining are also shaping where suppliers can differentiate as BIW architectures incorporate structural battery packs, mixed-metal joints, and tighter dimensional control needs. Production planning is moving toward simulation-led commissioning and digital-twin-based BIW line design to manage complexity across welding, laser joining, riveting, and adhesive or hybrid bonding. Laser-based joining adoption is gaining traction for aluminum-intensive EV structures, while plants running high robot densities in BIW lines are raising demand for integrators and suppliers that can deliver in-line quality monitoring, seam tracking, and joining specifications aligned with IATF 16949 and OEM weld standards.

Recent Industry Developments

- June 2026: Gestamp inaugurated its seventh factory in Brazil in Piracicaba, Sao Paulo, supported by an investment of R$200 million and an initial footprint designed to scale headcount significantly. The site focuses on lightweight metal body and chassis components, adding hot-stamping capacity closer to regional OEM production. This strengthens localized BIW supply for South America and reduces the logistics burden associated with shipping bulky structural assemblies.

- February 2026: Autokiniton announced a USD 313 million expansion of its Bellevue, Ohio, manufacturing facility, adding 215,000 square feet along with new production lines and assembly equipment, with completion targeted over about 18 months. The upgrade expands North American capacity for structural components supplied into OEM programs that require tighter tolerances and flexible manufacturing. It also supports localization strategies shaped by tariff exposure and regional-content requirements.

- December 2024: Magna International announced a USD 200 million investment to build a new 625,000-square-foot factory and expand an existing site in Piedmont, South Carolina, creating around 200 jobs. The added footprint increases regional capability to support OEM production hubs in the US Southeast with faster delivery of large structural parts and assemblies. Expanded local capacity also helps shorten supply chains for BIW-related stampings and subassemblies where transport costs are high relative to value density.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the automotive body in white market is defined as the value of the vehicle body structure up to the pre-paint stage, where stamped or formed parts are joined into a welded and bonded shell.

Scope exclusions: The sizing excludes paint shop processes, trim and final assembly, and most exterior add-ons that are not part of the core BIW shell.

Segmentation Overview

- By Vehicle Type

- Passenger Cars

- Commercial Vehicles

- By Propulsion Type

- Internal Combustion Engine

- Electric Vehicles

- By Material Type

- Aluminum

- Steel (Mild, HSS, AHSS, UHSS)

- Composites (CFRP, GFRP, SMC)

- Magnesium and Other Metals

- By Material Joining Technique

- Welding (RSW, Laser, FSW)

- Self-Piercing and Plasma-Assisted Riveting

- Clinching and Mechanical Fastening

- Adhesive and Hybrid Bonding

- Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the demand pool and the key conversion factors that connect vehicle output to BIW value. We relied on public production and sales signals, plus technical references that explain how materials and joining choices are changing BIW content per vehicle.

Typical sources included OICA vehicle production statistics, US DOT and NHTSA publications, Eurostat manufacturing and trade series, International Energy Agency updates on EV adoption, and SAE technical papers on BIW lightweighting and joining. We also reviewed company annual reports, investor presentations, and trade association websites to cross-check capacity additions, new platform launches, and material substitution trends. Paid subscriptions were then used for company financials, shipment-level trade checks, and patent screening where it clarified open questions. The desk source list is illustrative only, and many other public sources were also used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on confirming BIW content per vehicle and the pace of change in materials and joining methods, since these two items can move totals quickly. We interviewed a mix of OEM engineering and purchasing contacts, BIW tooling and stamping experts, and material and joining solution specialists across APAC, EMEA, and the Americas. The intent was to correct assumptions from desk research and then apply the same content-per-vehicle logic across regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 12% | APAC: 46% |

| Mid tier: 51% | Functional/Unit leaders: 39% | EMEA: 33% |

| Smaller Players: 20% | Managers: 49% | Americas: 21% |

Market-Sizing & Forecasting

The core sizing logic follows a top-down approach where vehicle production by region is reconstructed and then converted into BIW value using BIW content assumptions per vehicle. Those content assumptions are built from a practical mix of material mix (steel, aluminum, composites), joining method intensity (welding, bonding, clinching, laser brazing), and the share of EV platforms where BIW architectures can differ from ICE platforms.

To keep the model grounded, totals were corroborated with selective bottom-up approximations, such as sampled BIW system pricing ranges discussed in interviews, checks on stamping and BIW line utilization trends, and cross-checks against reported revenues for relevant body structure activities where disclosure allowed reasonable filtering. When bottom-up signals were incomplete, for example where suppliers report combined structures, we applied conservative allocation factors validated through follow-up calls, and we documented the reason for each adjustment.

Forecasting was built using scenario analysis tied to vehicle production outlooks and platform cycle timing, then refined using expert views on the speed of lightweighting and the expected pace of EV mix change. Short-term changes were treated carefully because BIW demand can shift with production shocks, model changeovers, and localized supply constraints, so the forecast was reviewed region by region before consolidation.

Data Validation & Update Cycle

Model outputs were checked against independent signals, including regional vehicle build trends, major platform launch timing, and observed shifts in material usage, so the final market value stays tied to real production conditions. Any large variance across regions or a sudden jump in implied BIW value per vehicle triggers an anomaly review, followed by targeted re-checks with interviewees and a second-pass review by another analyst.

Reports refresh annually, and interim updates are done when major events materially affect demand assumptions, such as sharp production revisions, major capacity changes, or significant regulatory actions related to lightweighting and safety. Before delivery, we run a final data pass to capture the most recent public releases and to ensure the numbers remain consistent across the model, charts, and narrative.

Mordor Intelligence's White Automotive Body Market Estimate Compared With Other Published Estimates

Published numbers for automotive body in white often differ because the counted cost items are not the same, and because vehicle production and content assumptions are refreshed on different timelines. Currency conversion timing and the treatment of EV platforms versus ICE platforms also play a real role in where the final value lands.

The table shows a visible spread in 2025 to 2026 values, and in Mordor Intelligence's model the market is counted as the BIW shell up to the pre-paint stage, then tied to vehicle production by region and BIW content per vehicle. This tends to diverge from studies that extend into paint shop or adjacent body systems.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 146.92 B (2026) | |

| Industry Research Publisher A | USD 90.19 B (2025) | Uses an earlier base year and a narrower value capture in some cases, and it can also blend construction and manufacturing method cuts that shift the implied BIW content per vehicle downward across regions. |

| Industry Research Publisher B | USD 68.69 B (2025) | Reports a smaller starting value that is consistent with tighter component inclusion and a different product-type split, which can undercount joining-intensive BIW assemblies when content per vehicle is averaged across platforms. |

Across the three values, the main takeaway is that scope boundaries and the content-per-vehicle assumption explain most of the difference, more than simple growth rates do. By keeping the steps traceable, from vehicle builds to BIW material and joining intensity and then to regional aggregation, the estimate can be repeated and stress-tested when a client wants to adjust a key input.

Key Questions Answered in the Report

How big is the Automotive Body-in-White Market?

The Automotive Body-in-White Market size is expected to reach USD 146.92 billion in 2026 and grow at a CAGR of 3.52% to reach USD 174.67 billion by 2031.

Which region leads demand for body-in-white structures?

Asia-Pacific held 45.60% of 2025 revenue, driven by China’s EV boom and ASEAN greenfield investments.

What is the fastest-growing propulsion segment for BIW suppliers?

Electric vehicles are forecast to grow at an 10.84% CAGR, reshaping battery integration and material choices.

Which region has the biggest share in Automotive Body-in-White Market?

In 2025, the Asia-Pacific accounts for the largest market share in Automotive Body-in-White Market.

Why are adhesives gaining traction over traditional welding?

Adhesive and hybrid bonding support multi-material bodies, distribute loads evenly, and improve electrical insulation for 800 V EV platforms.

Which joining technologies are critical for giga-cast bodies?

Large aluminum castings rely on hybrid bonding, laser welding of sub-frames, and reinforced adhesive seams to handle crash loads while minimizing distortion.

Page last updated on: