Body Control Module Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 34.51 Billion |

| Market Size (2030) | USD 41.03 Billion |

| Growth Rate (2025 - 2030) | 3.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Body Control Module Market Analysis by Mordor Intelligence

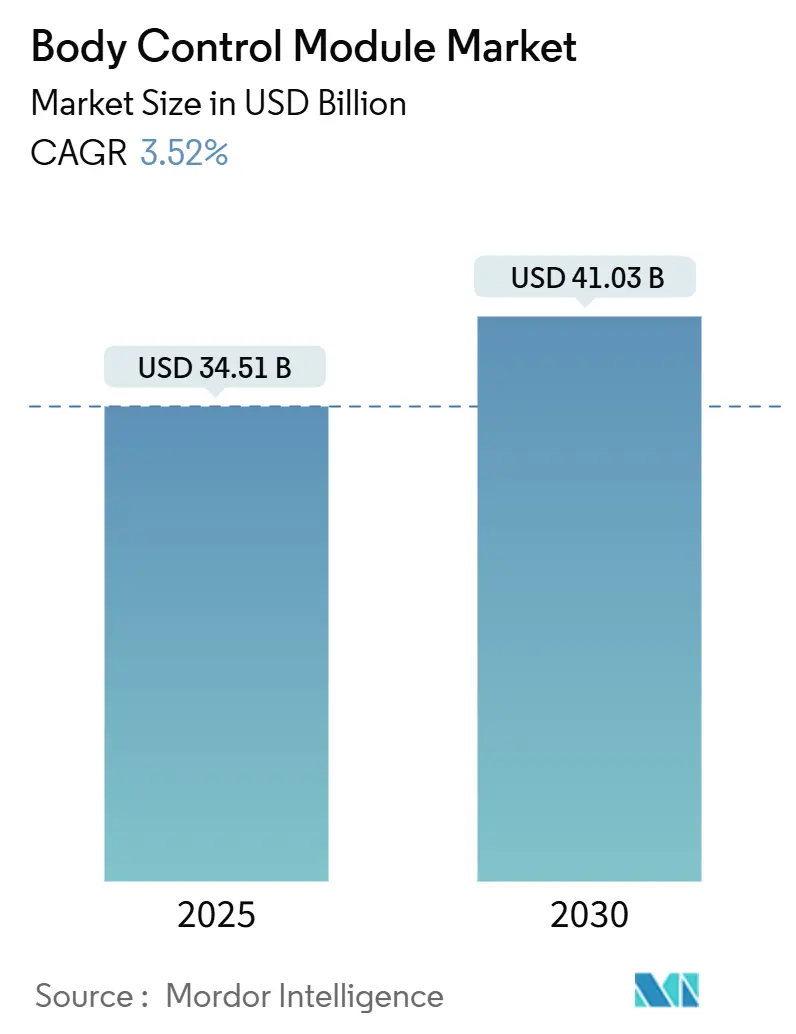

The Body Control Module Market size is estimated at USD 34.51 billion in 2025, and is expected to reach USD 41.03 billion by 2030, at a CAGR of 3.52% during the forecast period (2025-2030).

This steady trajectory is underpinned by the migration to software-defined electrical architectures, tighter cybersecurity mandates, and the electrification wave that raises low-voltage system complexity. Hardware continues to supply the backbone of control logic, but demand is tilting toward software-upgradeable platforms as over-the-air (OTA) regulations become global. Zonal designs are reshaping supplier strategies by collapsing dozens of legacy electronic control units (ECUs) into a handful of high-compute controllers, elevating the role of body modules as secure gateways for lighting, comfort, and diagnostics. At the same time, semiconductor supply disruption, UNECE-R155/156 homologation costs, and communication-bus redesign cycles temper the growth outlook and favor well-capitalized Tier-1s that can subsidize compliance engineering.

Key Report Takeaways

- By component, hardware commanded 70.37% of the automotive body control module market share in 2024, whereas the software segment is projected to deliver the strongest 5.18% CAGR through 2030.

- By functionality, low-end body control modules secured a 62.22% share of the automotive body control module market in 2024, while high-end platforms are advancing at a 4.76% CAGR to 2030.

- By application, lighting control led with 23.28% of the automotive body control module market share in 2024, and driver assistance systems are on track for the fastest 5.48% CAGR through 2030.

- By bit size, 32-bit processors held 40.72% of the automotive body control module market share in 2024 and posted the highest 4.66% CAGR over the forecast period.

- By communication interface, CAN retained a 60.43% share of the automotive body control module market in 2024, while FlexRay registered the quickest 4.86% CAGR to 2030.

- By vehicle type, passenger cars dominated, with 64.32% of the automotive body control module market share in 2024, and the market is forecast to grow at a 4.12% CAGR through 2030.

- By sales channel, OEM deliveries represented 79.78% of the automotive body control module market share in 2024, whereas the aftermarket channel expanded at the highest 4.82% CAGR to 2030.

- By region, Asia-Pacific captured a 34.51% of the automotive body control module market share in 2024, while South America posted the fastest 5.01% CAGR through 2030.

Global Body Control Module Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Zonal-Controller E-Architecture Shift | +0.8% | Asia-Pacific and Europe | Medium term (2-4 years) |

| Software-Defined Vehicle Investments | +0.6% | North America and EU; rising in Asia-Pacific | Long term (≥4 years) |

| 48 V Low-Voltage Battery Downsizing | +0.4% | Global EV hubs | Short term (≤2 years) |

| Adaptive Ambient-Lighting Demand | +0.3% | North America and Europe luxury segments | Medium term (2-4 years) |

| Fleet-Wide OTA Mandates | +0.2% | China first; global later | Short term (≤2 years) |

| Right-To-Repair Aftermarket Pull | +0.1% | United States and EU | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Vehicle E-Architecture Shift Toward Zonal Controllers

Electronic control systems in the automotive industry are undergoing a significant redesign and integration overhaul. In the past, vehicles operated on a distributed architecture, deploying dozens, and at times, over a hundred Electronic Control Units (ECUs). Each ECU was dedicated to specific functions, from braking and lighting to infotainment. However, as vehicles increasingly embrace software-driven features, this once-effective approach has become a complex, costly, and challenging system to scale.

This shift brings forth new technical challenges. While traditional CAN and LIN communication protocols are still utilized for specific functions, they've found a new partner in Ethernet backbones. These backbones facilitate higher data throughput and real-time communication. Navigating this hybrid landscape demands flexible transceivers and robust multilayer cybersecurity frameworks, ensuring every vehicle system operates securely and reliably.

Premium OEM Demand for Adaptive Ambient Lighting

BMW’s iX integrates 200 addressable LEDs orchestrated via BCM-embedded algorithms for color, brightness, and music synchronization[1]"iX Lighting Innovation,”, BMW Group, bmwgroup.com. Mainstream brands increasingly adopt these experience features. Consequently, BCMs embed graphical processors and lightweight machine-learning kernels to deliver real-time personalization, boosting silicon content and reinforcing the case for high-end variants.

Fleet-wide OTA Update Mandates

China’s Ministry of Industry and Information Technology requires OTA-capable electric vehicles as of January 2024[2]“EV OTA Regulation 2024,”, Ministry of Industry and Information Technology, miit.gov.cn. Europe and California are drafting similar rules. BCMs now need encrypted channels, rollback logic, and secure diagnostics, adding cost and firmware complexity. Vendors with proven OTA stacks and public-cloud partnerships capture design wins, while hardware-only firms scramble to license software.

Right-to-repair Legislation Boosting Aftermarket BCM Upgrades

The U.S. REPAIR Act, reintroduced in February 2025, obliges automakers to share diagnostic data with independent workshops, unlocking retrofit demand for older vehicles[3]“REPAIR Act 2025,”, U.S. Congress, congress.gov. Aftermarket suppliers can market plug-compatible BCMs that add connectivity or lighting upgrades. Cybersecurity liability remains a hurdle, but regulatory momentum favors broader access, potentially extending module lifecycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor Supply Volatility | -0.7% | Global, acute in Asia-Pacific fabs | Short term (≤2 years) |

| UNECE-R155/R156 Cybersecurity Costs | -0.5% | Mandatory in Europe; spreading worldwide | Medium term (2-4 years) |

| CAN/LIN-To-Ethernet Redesign Risk | -0.3% | Global OEMs in transition | Medium term (2-4 years) |

| Tier-1 Consolidation Curbs Low-End Sourcing | -0.2% | Cost-sensitive regions | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Persistent Semiconductor Supply Volatility

Extended lead times for key microcontrollers are putting significant pressure on the automotive electronics supply chain. Once predictable and manageable procurement cycles have turned into prolonged and volatile processes. This shift strains production schedules and working capital, especially for modules like Body Control Modules (BCMs), which are pivotal in modern vehicle architectures.

Larger Tier-1 suppliers, wielding greater purchasing power and boasting established relationships, are in a prime position to secure allocations from semiconductor manufacturers. Their scale not only buffers them against supply disruptions but also ensures continuity in production. On the other hand, smaller firms grapple with competition for limited inventory, resulting in production gaps and a heightened dependence on the unpredictable and often inflated spot market.

Transition Risk From CAN/LIN to Ethernet

As Automotive Ethernet evolves to support higher data rates, it significantly boosts in-vehicle communication capabilities. Yet, this advancement brings new technical demands: updated physical layer components, enhanced shielding, and rigorous validation processes. Such complexities often lengthen development timelines for vehicle platforms, particularly for manufacturers with constrained engineering resources. Midsized automotive brands, feeling the urgency to adapt, might face postponed vehicle launches or hasty redesigns, which inject unpredictability into the demand for Body Control Modules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Resilience Amid Software Acceleration

Hardware generated 70.37% of the automotive body control module market size in 2024, anchored by microcontrollers, power-management ICs, and rugged housings that withstand –40 °C to +125 °C temperature exposure. Despite the hardware skew, the software segment is climbing at a 5.18% CAGR thanks to OTA-ready frameworks that extend feature roadmaps after vehicle sale. The hardware footprint must also expand to host richer firmware, prompting vendors to integrate larger flash arrays and crypto accelerators.

A symbiotic trajectory emerges rather than zero-sum competition. Software relies on steadily more capable silicon, while new silicon wins hinge on demonstrable software value. Suppliers coupling both layers lock in multiyear platforms and higher average selling prices.

By Functionality: Low-end Predominance With High-end Traction

Low-end modules retained a 62.22% share in 2024 by delivering lighting and window control at razor-thin cost targets. However, premium modules integrating adaptive lighting, zonal communication, and cybersecurity are advancing at a 4.76% CAGR. Rising regulatory overhead nudges even entry-segments toward richer processors, slowly eroding the low-end value gap.

The blurring boundary lets high-end suppliers repurpose architectures downstream, pressuring legacy low-cost players to upskill or exit. Over time, value migrates to software-upgradeable modules able to monetize features throughout the vehicle life.

By Application: Lighting Control Leads while ADAS Surges

Lighting held 23.28% revenue share in 2024 as every vehicle demands exterior and interior illumination management. Driver assistance control is scaling fastest at 5.48% CAGR, reflecting mandates for lane-keeping and automated braking. Window and door electronics remain staple content, whereas climate and powertrain functions pivot toward energy-efficient algorithms in EVs.

The convergence of lighting with human-machine interface design elevates BCM's importance: color palettes now sync with driving modes and safety alerts. Similarly, ADAS integration embeds sensor-fusion pre-processing at the body-domain layer, intensifying compute requirements.

By Bit Size: 32-Bit Dominance Guiding Performance Uplift

32-bit architectures accounted for 40.72% of automotive body control module market share in 2024 and are growing 4.66% annually as cybersecurity and OTA tasks exceed 16-bit capacity. Although 8-bit cores linger in legacy switching roles, OEMs favor unified 32-bit software frameworks to cut validation costs.

Growth will accelerate when zonal controllers consolidate dozens of small ECUs into a few high-compute nodes, incentivizing platform reuse and firmware portability—advantages native to 32-bit ecosystems.

By Communication Interface: CAN Legacy Meets Flexray Emergence

CAN still moves 60.43% of BCM traffic, given its low cost and deterministic reliability. FlexRay, with built-in redundancy and 10 Mbps bandwidth, leads growth at 4.86% CAGR as time-critical chassis functions migrate to higher bus rates. LIN persists for low-speed peripherals where sub-cost thresholds trump performance.

Over the forecast window, Ethernet will eat into both CAN and FlexRay once 100 Mbps single-pair variants reach cost parity. BCM vendors hedge by offering multiplexed PHYs that auto-detect legacy topologies.

By Vehicle Type: Passenger-Car Volume, Commercial-Vehicle Upside

Passenger cars delivered 64.32% volume in 2024 and will post a 4.12% CAGR as electronics per vehicle rise under safety rules. Light commercial vans benefit from e-commerce delivery growth, demanding telematics and predictive maintenance that elevate BCM attach rates. Heavy trucks and buses electrify slowly but require robust thermal and charging control, yielding premium ASPs.

Autonomous-ready commercial platforms require triple-redundant electronics, turning BCMs into safety-critical gatekeepers and widening margins for specialized suppliers.

By Sales Channel: OEM scale vs aftermarket opening

OEM channels controlled a 79.78% share in 2024 because in-line validation and software pairing make BCMs integral to vehicle launch. Still, aftermarket demand climbs 4.82% CAGR courtesy of right-to-repair statutes and longer service lives. Independent shops are investing in secure flashing tools to replace or upgrade BCMs, though rising software protection injects complexity.

Tier-1s reluctant to cannibalize OEM contracts may license older designs to third-party distributors, creating a stratified aftermarket tier with mixed cybersecurity assurances.

Geography Analysis

Asia-Pacific captured 34.51% of the automotive body control module market in 2024, leveraging China’s 40% new-energy-vehicle sales quota for 2030, India’s 30 million-unit vehicle output, and the semiconductor clusters of Japan and South Korea. Government incentives and labor-cost advantages sustain BCM capacity expansion from Shanghai to Bangkok.

North America and Europe represent mature yet technologically intensive arenas. The United States emphasizes cybersecurity compliance and OTA frameworks, while the European Union enforces UNECE’s R155/R156 rules, inflating development overhead but enabling premium pricing. Both regions favor adaptive ambient lighting, predictive diagnostics, and cloud-based remote updates, magnifying content per vehicle despite plateauing volumes.

South America is the fastest riser at 5.01% CAGR through 2030, driven by Brazil’s production rebound and Argentina’s EV-charging build-out. Currency volatility and limited wafer fabs remain obstacles, but local content mandates and rising safety regulations unlock opportunities for suppliers able to localize assembly. The Middle East and Africa offer niche plays centered on smart-city fleets in the United Arab Emirates and South African premium imports.

Competitive Landscape

Leading companies dominate the revenue landscape in this moderately consolidated sector. Yet, this concentration hasn't shut the door on specialized entrants, paving the way for innovation and niche expertise. Bosch, Continental, and Denso extract advantage from global manufacturing footprints, vertical integration, and multidecade OEM ties. Yet the shift to software-centric architectures invites challengers such as Aptiv, which couples cloud analytics with hardware gateways.

There's a noticeable shift towards vertical integration in the automotive electronics arena. Concurrently, a notable surge in patent filings—specifically in automotive cybersecurity has been observed, with numbers more than tripling over just two years. This trend underscores the growing importance of intellectual property protection, positioning it on par with manufacturing scale when carving out a competitive edge.

Partnership ecosystems blossom around semiconductor roadmaps. NXP’s S32G4 processors embed hardware security modules tailored to BCM workloads; Tier-1s integrate these chips with in-house firmware to offer turnkey zonal nodes. OEMs respond by co-developing interfaces to hedge against supply shortages and lock in shared software stacks for vehicle generations extending to 2035.

Body Control Module Industry Leaders

-

Continental AG

-

Robert Bosch GmbH

-

Denso Corporation

-

Aptiv PLC

-

HELLA GmbH & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: HIRAIN's Body Control Module Makes European Debut, Expanding Its Market Footprint. As vehicles evolve to be more intelligent and interconnected, the appetite for high-performance Body Control Modules surges. HIRAIN's Body Control Module played a pivotal role in helping Foton Piaggio's NP6 light truck navigate stringent European cybersecurity regulations, paving the way for its mass production.

- September 2024: NOVOSENSE Microelectronics, a semiconductor firm known for its high-performance analog and mixed-signal chips, has unveiled a series of high-side switches. These switches are designed to drive traditional resistive, inductive, and halogen lamp loads in automotive body control modules (BCM). Additionally, they cater to large capacitive loads typically seen in first and second-level power distribution within zone control units (ZCU).

Global Body Control Module Market Report Scope

| Hardware |

| Software |

| Low-End BCMs |

| High-End BCMs |

| Lighting Control |

| Window & Door Control |

| Climate Control |

| Security & Safety |

| Powertrain Control |

| Infotainment |

| Driver Assistance Systems |

| Others |

| 8-bit |

| 16-bit |

| 32-bit |

| Controller Area Network (CAN) |

| Local Interconnect Network (LIN) |

| FlexRay |

| Passenger Cars |

| Light Commercial Vehicles (LCVs) |

| Heavy Commercial Vehicles (HCVs) |

| Buses and Coaches |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Component | Hardware | |

| Software | ||

| By Functionality | Low-End BCMs | |

| High-End BCMs | ||

| By Application | Lighting Control | |

| Window & Door Control | ||

| Climate Control | ||

| Security & Safety | ||

| Powertrain Control | ||

| Infotainment | ||

| Driver Assistance Systems | ||

| Others | ||

| By Bit Size | 8-bit | |

| 16-bit | ||

| 32-bit | ||

| By Communication Interface | Controller Area Network (CAN) | |

| Local Interconnect Network (LIN) | ||

| FlexRay | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCVs) | ||

| Heavy Commercial Vehicles (HCVs) | ||

| Buses and Coaches | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How big is the automotive body control module market in 2025?

It was valued at USD 34.51 billion in 2025 and is projected to reach USD 41.03 billion by 2030.

Which component segment is growing fastest?

Software posts the highest 5.18% CAGR, driven by over-the-air update requirements.

Why are 32-bit processors gaining share in BCMs?

Regulatory cybersecurity demands and richer firmware workloads are pushing OEMs toward 32-bit cores that support encryption and secure-boot functions.

How are zonal architectures affecting BCM suppliers?

Zonal layouts consolidate multiple ECUs into high-compute nodes, raising module content per vehicle but requiring integrated hardware-software expertise.

What is the main restraint on near-term BCM growth?

Persistent semiconductor supply volatility keeps microcontroller lead times high, limiting production scalability.

Page last updated on: