Automotive Front End Module Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 140.01 Billion |

| Market Size (2031) | USD 188.25 Billion |

| Growth Rate (2026 - 2031) | 6.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Front End Module Market Analysis by Mordor Intelligence

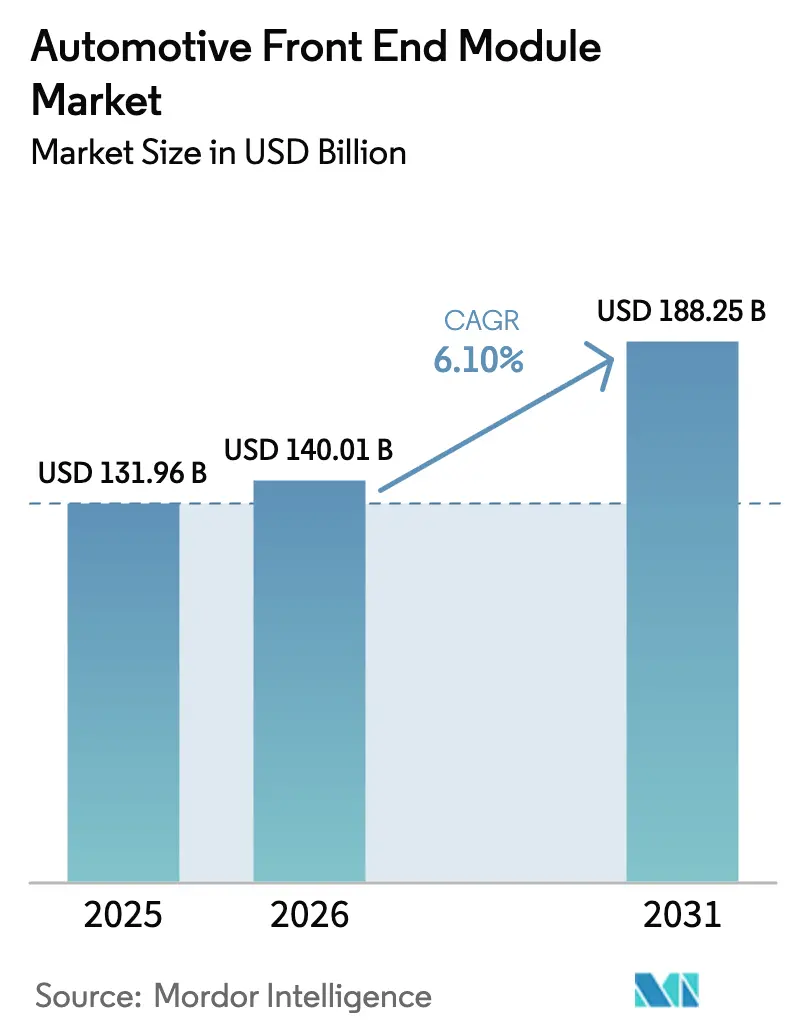

The automotive front-end module market size is expected to grow from USD 131.96 billion in 2025 to USD 140.01 billion in 2026 and is forecast to reach USD 188.25 billion by 2031, growing at a CAGR of 6.10% during the forecast period (2026-2031). Final-assembly outsourcing to tier-1 integrators that deliver complete bolt-on carriers is cutting plant labor by 20-30%, intensifying OEM demand for turnkey systems. Closed-grille architectures optimized for battery-electric thermal loops are spreading from premium EVs into volume segments, while precision mounts for radar, LiDAR, and camera sensors are transforming the module from a commodity bracket into a software-defined sensing hub. Heightened crash-test rigor under Euro NCAP and IIHS is driving a rebound in high-strength steel-aluminum hybrids that absorb energy while remaining light enough to meet CO₂ rules. Near-shoring in North America and tariff-sensitive EU-UK corridors is re-shaping the supplier footprint as OEMs seek modules that meet significant regional-value thresholds under USMCA.

Key Report Takeaways

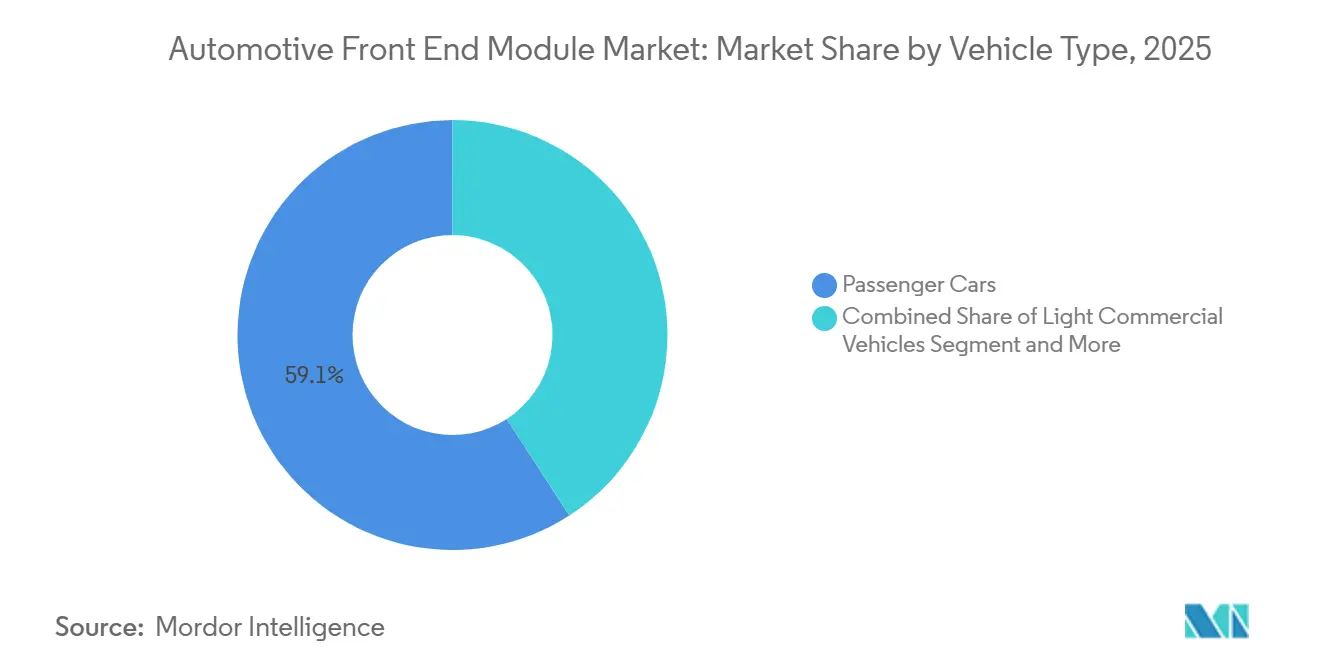

- By vehicle type, passenger cars led with 59.13% of the automotive front-end module market share in 2025, while medium and heavy commercial vehicles are projected to expand at an 8.71% CAGR through 2031.

- By raw material, composite frames captured 44.25% of the automotive front-end module market size in 2025, while metal frames are forecast to register a 7.12% CAGR between 2026 and 2031.

- By product type, hybrid frames accounted for 47.11% of the automotive front-end module market size in 2025, and will continue their growth trajectory at a 9.12% CAGR through 2031.

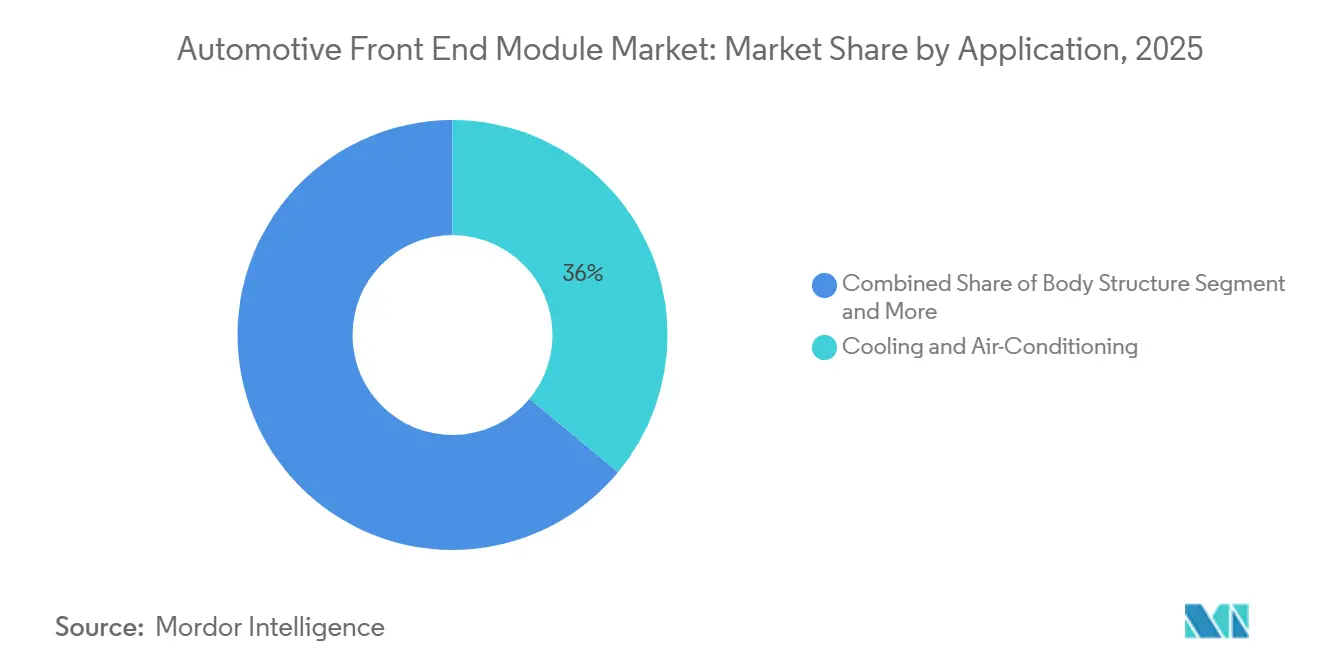

- By application, cooling and air-conditioning accounted for 36.02% of the automotive front-end module market size in 2025, whereas sensor integration is advancing at a 7.86% CAGR through 2031.

- By end use, the OEM segment accounted for 92.15% of the automotive front-end module market size in 2025, while the aftermarket is projected to grow at an 8.25% CAGR through 2031.

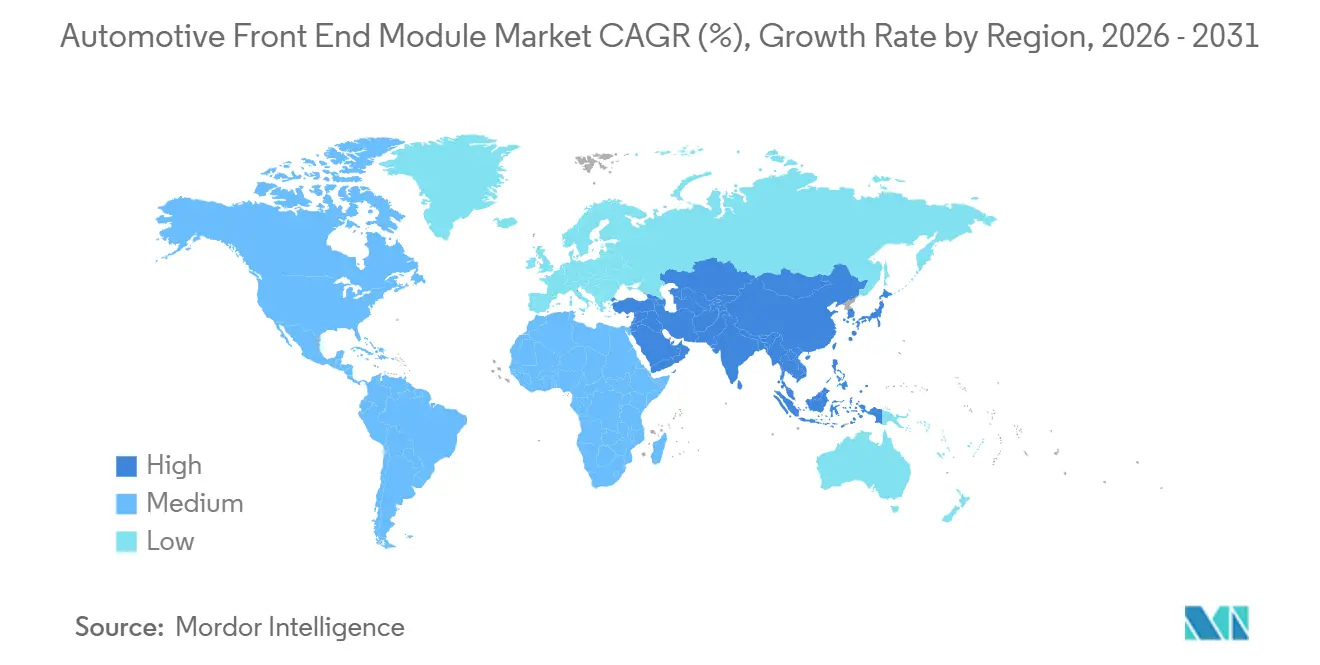

- By geography, Asia-Pacific accounted for 46.34% of the automotive front-end module market size in 2025 and will retain its dominance with a 7.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Front End Module Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Thermal-Management | +1.4% | Asia-Pacific and North America (EV hubs) | Long term (≥ 4 years) |

| Lightweighting and Fuel-Economy Regulations | +1.2% | Global (EU and China lead) | Long term (≥ 4 years) |

| ADAS Sensor-Mounting Demand | +1.0% | Global (early EU, Japan, North America) | Long term (≥ 4 years) |

| Outsourcing of Modular FEMs | +0.9% | North America and EU (expanding to Asia-Pacific) | Medium term (2-4 years) |

| Grille-Shutter / Adaptive-Aero Adoption | +0.8% | North America and EU (premium), Asia-Pacific spill-over | Medium term (2-4 years) |

| Near-Shoring of FEM Production | +0.6% | North America (USMCA), select EU-UK | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EV Thermal-Management Need for Integrated, Closed-Grille FEMs

Battery-electric vehicles swap open radiator grills for sealed fascias that route air through chillers and condensers hidden behind the bumper beam, demanding carriers that package heat exchangers, coolant manifolds, and ducts in a single structure. Tesla achieved a significant drag reduction on its 2025 Model 3 refresh, while BYD’s Blade Battery platform extends life by maintaining a ±2 °C band using Yinlun-supplied liquid-cooled carriers. In hot climates across Asia-Pacific and the United States Sunbelt, thermal integration is quickly becoming a gating item for range certification. Rivian has locked in a five-year contract with Valeo for dual-loop carriers consolidating battery and drive-unit cooling, illustrating the deep co-development ties now required. Long-term, EV-specific modules will underpin 50% of the automotive front-end module market revenue as BEV share breaches 50% of global sales in the early 2030s.

Lightweighting and Stricter CO₂ / Fuel-Economy Regulations

Global emissions policies are driving automakers to reduce the weight of traditional steel carriers, accelerating the adoption of materials such as aluminum extrusions, carbon-fiber-reinforced thermoplastics, and magnesium die-casts. These materials are critical for meeting the EU's fleet-average emissions targets by 2030. In China, regulatory frameworks are pushing OEMs to adopt hybrid-frame modules that maintain crash energy absorption while significantly reducing weight. In the United States, updated CAFE rules finalized in 2024 are prompting automakers like Ford and GM to transition to multi-material carriers. These carriers integrate essential components such as crash rails, cooling packs, and sensor plates within a lightweight design. ISO 14040 life-cycle reporting is increasing the demand for recycled aluminum and bio-based resins, encouraging suppliers to qualify low-carbon materials and tap into new revenue opportunities tied to ESG credits. These regulatory trends are embedding lightweighting into every vehicle program from 2026 onward, establishing it as the most significant value-creation driver for suppliers in the automotive front-end module market.

ADAS Sensor-Mounting Demand Elevates Structural Precision Requirements

Radar, LiDAR, and multi-camera stacks require mounting-surface flatness within ±0.3 mm, so suppliers are adopting laser-tracker verification and closed-loop injection molding, which boost per-unit cost. BMW’s 2026 5 Series features five sensors on a Magna carrier with IP6K9K-sealed connectors to ensure calibration during splash tests. Euro NCAP now requires five-star ratings only if autonomous emergency braking operates at up to 80 km/h, forcing mass-market cars to adopt precision sensor mounts by default. Long-term, sensor integration is the highest-value growth lever inside the automotive front-end module market, locking suppliers into co-validation loops with chipmakers and software teams.

OEM Outsourcing of Modular FEMs to Cut 20-30% Assembly Cost

Automakers are increasingly relying on tier-1 suppliers for complete carrier build-up. At General Motors plants, this approach has significantly reduced line-side labor per vehicle and lowered tooling amortization costs across multiple programs. Volkswagen has optimized its MEB platform by adopting an HBPO one-piece front-end, drastically shortening installation times compared to legacy processes. This improvement not only accelerates production but also creates additional space in body-shop floors for battery-pack installations. Labor-intensive factories in regions such as North America and Europe are seeing the most significant benefits. At the same time, Hyundai has achieved substantial working-capital savings by transferring carrier inventory management to Mobis. By 2028, a majority of new passenger-car platforms are expected to utilize fully integrated modules. This transition is anticipated to consolidate purchase volumes with fewer suppliers, boosting market margins for those proficient in just-in-sequence logistics within the automotive front-end module market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Steel, Polymer, and Energy Prices | −0.7% | Global (acute EU and North America) | Short term (≤ 2 years) |

| High R&D / Tooling Spend | −0.5% | North America and EU, emerging Asia-Pacific | Medium term (2-4 years) |

| Cyber-Security and Homologation Hurdles | −0.4% | Global (EU and North America lead) | Long term (≥ 4 years) |

| Radar-Signal Attenuation Issues | −0.3% | EU, Japan, North America premium | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Steel, Polymer and Energy Prices Inflate BOM Cost

In 2025, hot-rolled coil prices increased compared to the previous year, driven by EU energy surcharges that raised electric-arc-furnace overheads. During the same year, a force majeure on the Gulf Coast led to a significant rise in polypropylene prices, negatively impacting tier-1 gross margins. Higher European gas prices led to a notable increase in molding energy costs, adding to the production expenses for hybrid frames. Aluminum extrusion premiums rose due to Section 232 tariffs, intensifying spot-buy exposure. Suppliers with fixed-price contracts for the year faced profitability challenges, leading to more frequent renegotiations that strained relationships with OEMs and potentially affected investments in module innovation.

High R&D / Tooling Spend for Multi-Material Sensor-Ready Frames

Next-generation carriers require significant investment for validation, involving advanced technologies such as laser-weld cells, automated fiber placement, and climatic chambers. Magna has planned substantial funding for multiple electric vehicle (EV) programs in 2025. The development of multi-cavity molds demands considerable financial and time resources, creating challenges for smaller suppliers. Additional complexities arise from sensor EMC testing and LiDAR rigidity checks, which have driven mergers and acquisitions, such as Samvardhana Motherson’s recent composite-focused acquisition. As a result, the supply chain has become divided, favoring larger, capital-intensive integrators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Fleets Accelerate Module Adoption

Passenger Cars still account for the bulk of volume, with a 59.13% of the automotive front-end module market size in 2025, and adopt standardized carriers across hatchback, sedan, and CUV body styles. Medium- and heavy-duty commercial vehicles will post an 8.71% CAGR, expanding the automotive front-end module market faster than any other vehicle class as fleet owners electrify last-mile vans and long-haul tractors that rely on integrated thermal loops and precision sensor mounts. Daimler Truck’s eCascadia specifies an aluminum carrier that trims assembly by 45 minutes and shortens overhang, highlighting value for depot maneuverability [1]“eCascadia Technical Press Statement,” Daimler Truck AG, daimlertruck.com.

Fleet electrification policies in Europe and China, alongside U.S. tax incentives, are driving commercial OEMs toward sealed-grille modules that protect battery thermal systems from road debris while enabling quick sensor calibration for collision avoidance. Light commercial vehicles such as Ford Transit and Ram ProMaster are embedding forward-collision and lane-keep sensors into the carrier, ensuring compliance with 2026 NHTSA mandates. Hybrid-frame assemblies deliver 18-22% mass savings, essential for offsetting battery weight and retaining payload capacity, cementing their role across logistics fleets over the forecast horizon.

By Raw Material: Metal Rebounds On Crash-Test Rigor

Composites controlled 44.25% of the automotive front-end module market in 2025, yet renewed Euro NCAP and IIHS protocols are boosting metal demand, pushing high-strength steel and aluminum hybrids toward a 7.12% CAGR and expanding their share of the automotive front-end module market through 2031. Euro NCAP’s more challenging 64 km/h offset test penalizes brittle composite rails, prompting German OEMs to reinstate specific steel grades in crash rails [2]“2025 Protocol Update,” Euro NCAP, euroncap.com.

Composite uptake plateaus in sensor zones where radar transparency is critical; instead, suppliers use metal subframes topped with thermoplastic facias to blend impact energy absorption with styling freedom. Plastic carriers dominate cost-sensitive emerging markets, but their growth is constrained by thermal degradation risks under high-ambient EV duty cycles. Regulations now require embodied-carbon disclosure, positioning recycled aluminum as a favored middle ground that balances weight, crash performance, and ESG credits.

By Product Type: Hybrid Frames Dominate Platform Standardization

Hybrid frames accounted for 47.11% of the automotive front-end module market in 2025. They will grow at a 9.12% CAGR as OEMs standardize attachment points across ICE, hybrid, and BEV derivatives, driving unit economies and larger automotive front-end module market share. Volkswagen’s single hybrid design for ID.-family crossovers saves engineering costs per derivative.

All-metal frames persist in entry-level and commercial vehicles where simplicity and low tooling cost outweigh aerodynamics, while pure plastic rails remain limited to microcars. Hybrid sandwiched structures enable laser-weld seams joining steel, aluminum, and glass-fiber PP, hitting five-star ratings while shedding 16 kg versus monosteel baselines. SAE J3016 Level 3 autonomy mount-point standards further lock in hybrid relevance by requiring positional repeatability that injection-molded thermoplastics alone cannot always guarantee.

By Application: Sensor Integration Surges With ADAS Proliferation

Cooling and HVAC remain the largest segment at 36.02% of the automotive front-end module market in 2025, but their growth is EV-linked, requiring closed ducting and stackable heat exchangers. Sensor integration is forecast to outpace all other uses, with a 7.86% CAGR through 2031, expanding its share of the automotive front-end module market as Level 2+ functions reach a significant share of global new-car sales by 2028.

Body-structure rails continue steady growth to meet stricter pedestrian-protection and small-overlap rules, while adaptive LED headlamps packaged on the carrier evolve into software-controlled projection units, increasing wiring and thermal loads. Continental’s ARS540 radar mount's ±0.3 mm tolerance requires laser-tracker verification for every airline, converting a former stamped plate into a mechatronic sub-system. Such value escalation cements sensor mounts as the most lucrative application segment.

By End Use: Aftermarket Gains On Modular Replacement Protocols

OEM channels accounted for 92.15% of the automotive front-end module market in 2025. Yet, the aftermarket will compound at an 8.25% CAGR as insurers dictate certified bolt-on replacements that cut repair times by 3.2 days and reduce total-loss decisions. North America leads, with modular carriers accounting for a notable share of front-end collision repairs in 2025, driven by insurer mandates and technician shortages.

State Farm now specifies certified modules on 18 high-volume models to trim claim severity. At the same time, Forvia’s 2025 launch of aftermarket SKUs offers pre-calibrated radar brackets that plug straight into ADAS service tools. Europe lags due to OEM software lock-outs on sensor calibration, but regulatory pressure for fair repair access could unlock growth beyond 2028. By 2030, modular replacements may capture a significant portion of mature-market repairs, forming a steady annuity stream for integrators.

Geography Analysis

Asia-Pacific accounted for 46.34% of the automotive front-end module market in 2025. It will grow at a 7.44% CAGR through 2031. China’s passenger output now specifies closed-grille carriers with battery chillers as standard on high-volume BYD and SAIC models. India’s industry attracts Marelli and Aisin hybrid-frame lines under PLI incentives. Japan’s precision molders embed 77 GHz radar mounts for Toyota bZ and Honda e: N families, exporting to U.S. plants as yen depreciation improves cost competitiveness. South Korea’s Hyundai Mobis grew export module revenue in 2025 due to contracts for the Genesis GV60 and Kia EV9. Cybersecurity regulation GB/T 40861 and Bharat NCAP crash test rules jointly raise barriers, cementing the adoption of sensor-ready modules.

In 2025, North America emerged as a significant contributor to revenue, with the USMCA's rules driving a major expansion for Magna and HBPO. This expansion, spanning Tennessee and Michigan, significantly increased annual production capacity. Meanwhile, Mexico's robust production levels are fostering growth in Flex-N-Gate's tool room in Guanajuato. In Canada, efforts to meet the ZEV mandate by 2030 are accelerating the adoption of sealed grilles to enhance battery-pack thermal efficiency. The aftermarket is witnessing growth led by collision repair, with modular carriers improving cycle times to align with insurer benchmarks, further strengthening North America's position in global service revenue.

Europe, a key player in 2025 revenue, is led by Germany, France, Spain, and Italy. Decarbonization initiatives are driving the development of sensor-ready hybrid carriers with active shutters integrated behind composite facias. In 2024, Germany introduced updated crash tests, including a new side-pole scenario, which is expediting the use of high-strength steel rails. Post-Brexit, HBPO's Sunderland site has maintained the UK's export competitiveness by avoiding tariffs. Forvia's acquisition of a French composite firm is supporting Renault and Stellantis's EV production. Additionally, Spain and Italy are leveraging their proximity to North African plants for logistical advantages. Turkey and South Africa are central to module production for the Middle East & Africa, though currency volatility is limiting their capital investments. In South America, Brazil's substantial production volumes are driving demand, supported by local biofuel policies that are encouraging hybrid adoption.

Competitive Landscape

In 2025, HBPO, Magna, Forvia, Hyundai Mobis, and DENSO collectively accounted for a significant share of industry revenue, indicating moderate concentration. This scenario opens opportunities for regional contenders such as China's Yinlun and South Korea's SL Corporation. Magna, making a strategic move, invested heavily in multiple EV platforms, integrating advanced laser-weld and fiber-placement assets, achieving notable weight reductions compared to traditional monosteel baselines [3]“2025 Investor Day Presentation,” Magna International, magna.com.

There's untapped potential in thermal-integrated carriers tailored for commercial BEVs and aftermarket modules backed by insurers. Yinlun, in a strategic collaboration with BYD, co-engineered blade-battery cooling, capturing a substantial share of China's EV thermal market and outpacing global competitors. Meanwhile, SL Corporation, leveraging its expertise in plastics, provides hybrid-frame modules to premium EVs from Genesis and Kia, ensuring radar-transparent facias.

The competitive landscape is increasingly favoring suppliers that can certify to ISO/SAE 21434 cybersecurity standards, integrate over-the-air shutter firmware, and invest in high-value tooling packages. Forvia, recognizing the importance of cybersecurity, allocated a significant portion of its 2025 FEM engineering budget to cyber initiatives. Concurrently, patent filings for sensor-bracket designs increased notably year-on-year, with Continental, Valeo, and Marelli at the forefront. Amidst raw-material volatility and escalating R&D challenges, consolidation becomes imperative; regional stampers emerge as prime acquisition targets as global integrators rush to bolster capacity ahead of the anticipated surge in Level 3 autonomy volumes post-2028.

Automotive Front End Module Industry Leaders

HBPO GmbH

Magna International Inc.

Forvia SE

Hyundai Mobis Co., Ltd.

OPMOBILITY SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: LFT-G® Global partnered with a tier-1 supplier to redesign a C-segment SUV module, reducing weight, costs, and assembly time through the substitution of long-fiber thermoplastic.

- May 2024: Hyundai Mobis unveiled a front-face integration module for EVs that consolidates grille aesthetics with aerodynamic shutters, reshaping design and manufacturing paradigms.

Global Automotive Front End Module Market Report Scope

The scope includes segmentation by vehicle type (passenger cars, light commercial vehicles, and medium and heavy commercial vehicles), raw material (metal, plastic, composite, and hybrid), product type (metal frame, plastic frame, and hybrid frame), application (body structure, cooling and air-conditioning, sensor integration, and lighting systems), and end use (OEM and aftermarket). The analysis also covers regional-level segmentation, including North America, South America, Europe, Asia-Pacific, and the Middle East and Africa. Market size and growth forecasts are presented by value in USD.

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Metal |

| Plastic |

| Composite |

| Hybrid |

| Metal Frame |

| Plastic Frame |

| Hybrid Frame |

| Body Structure |

| Cooling and Air-Conditioning |

| Sensor Integration |

| Lighting Systems |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Turkey | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Raw Material | Metal | |

| Plastic | ||

| Composite | ||

| Hybrid | ||

| By Product Type | Metal Frame | |

| Plastic Frame | ||

| Hybrid Frame | ||

| By Application | Body Structure | |

| Cooling and Air-Conditioning | ||

| Sensor Integration | ||

| Lighting Systems | ||

| By End Use | Original Equipment Manufacturer (OEM) | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will automotive front-end module market size be by 2031?

It is projected to reach USD 188.25 billion by 2031 on a 6.10% CAGR from 2026-2031.

Which vehicle class is growing fastest in front-end modules?

Medium and heavy commercial vehicles are set to post an 8.71% CAGR as fleets electrify and demand integrated thermal carriers.

Why are hybrid-frame modules becoming the industry default?

They balance crash energy absorption, lightweighting, and sensor-mount precision, while letting OEMs reuse tooling across multiple ICE and EV platforms.

How are insurers influencing aftermarket demand?

Certified pre-assembled modules reduce repair times by over three days and lower total-loss frequency, leading insurers to mandate their use on newer models.

Page last updated on: