Austria Container Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

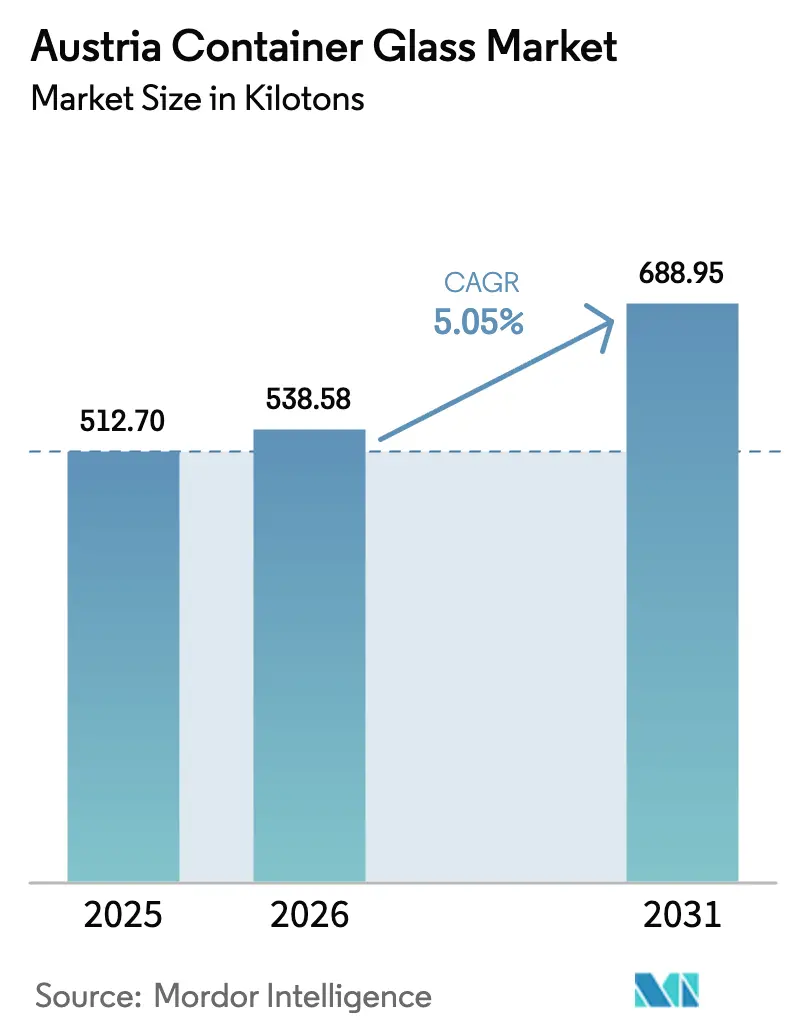

| Base Year Market Size (2025) | 512.70 kilotons |

| Market Volume (2026) | 538.58 kilotons |

| Market Volume (2031) | 688.95 kilotons |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Austria Container Glass Market Analysis by Mordor Intelligence

Austria container glass market size in 2026 is estimated at 538.58 kilotons, growing from 2025 value of 512.70 kilotons with 2031 projections showing 688.95 kilotons, growing at 5.05% CAGR over 2026-2031. Robust domestic beverage production, favorable deposit regulations that exclude glass, and high recycling efficiencies underpin this growth. The Austria container glass market benefits from the nation’s 9,000-plus vineyards and 347 breweries that collectively maintain elevated demand for premium, reusable bottles. Yet producers face persistently high energy tariffs that rank among Europe’s costliest, a condition expected to prevail through 2028. Energy-saving investments, such as Vetropack’s 8 MWh solar array in Kremsmünster, illustrate how manufacturers balance sustainability mandates with cost containment.[1]Glass International, “Vetropack to install solar power system at Austrian plant,” glass-international.com Competitive pressures from PET and metal packaging persist, but glass retains an advantage in premium positioning, health safety, and exemption from Austria’s January 2025 deposit on single-use plastic and metal containers.

Key Report Takeaways

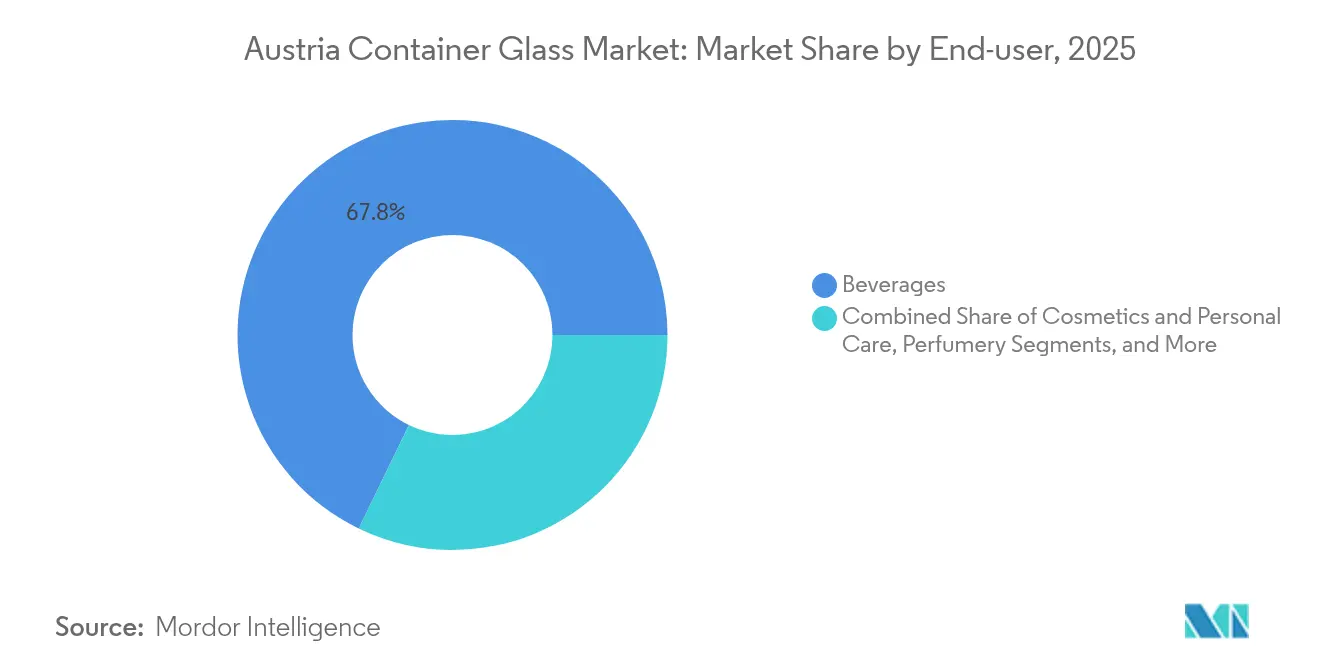

- By end-user, beverages captured 67.82% of the Austria container glass market share in 2025.

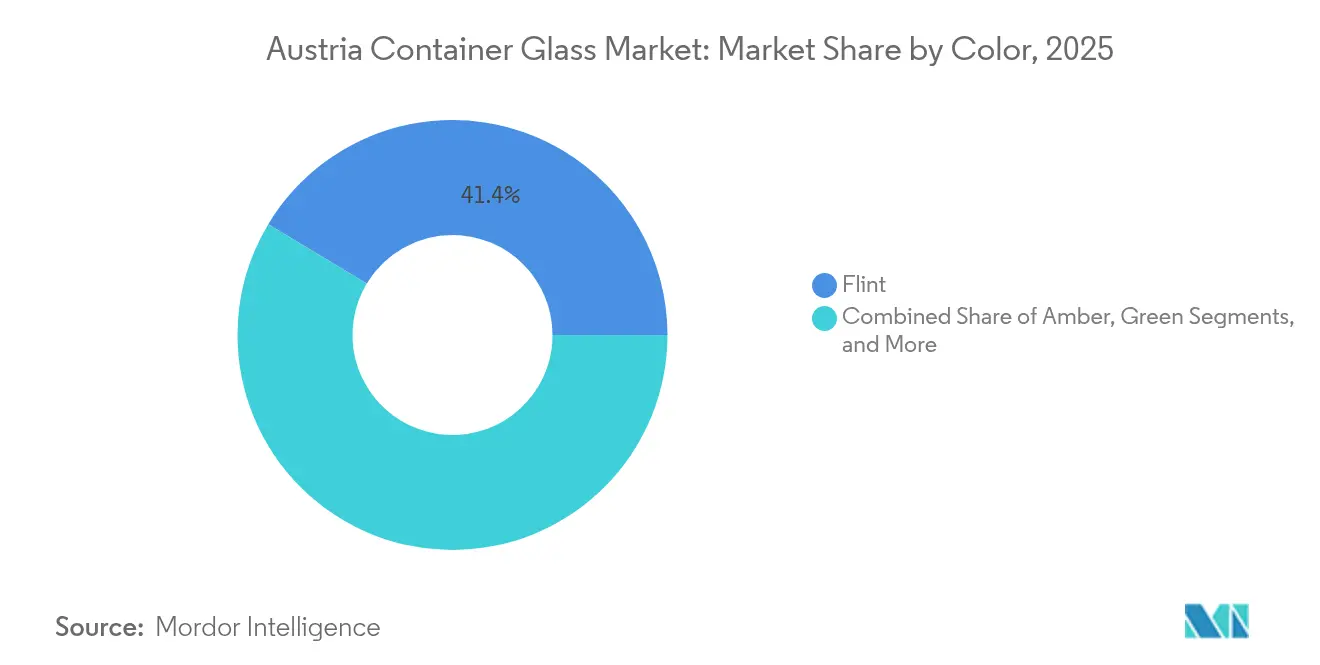

- By color, the Austria container glass market for amber glass is projected to grow at a 6.46% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Austria Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising environmental awareness and preference for sustainable packaging | +1.2% | Global, strong EU support | Medium term (2-4 years) |

| Health consciousness and food-safety perception of glass | +0.8% | Austria and wider DACH | Long term (≥ 4 years) |

| Government recycling targets driving cullet usage | +1.0% | Austria aligned with EU | Short term (≤ 2 years) |

| Premium beverage exports boosting value-added bottles | +0.6% | Austria to Germany, USA | Medium term (2-4 years) |

| Craft spirits boom demanding bespoke bottles | +0.9% | Vienna, Graz, Waldviertel | Short term (≤ 2 years) |

| Local soda-ash self-sufficiency | +0.3% | Austria production base | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising environmental awareness and preference for sustainable packaging

Austria's container glass market growth accelerates as consumers favor infinitely recyclable packaging that avoids quality loss. The federal circular economy roadmap aims for 18% material circularity by 2030 and already mandates 70% glass recycling by 2025, giving glass a regulatory edge. Municipal systems achieve high capture rates. Lower Austria alone recovered 44,100 tons of waste glass in 2022, ensuring a reliable supply of cullet.[2]Lower Austrian Government, “Waste Management Plan 2024,” noe.gv.at Austria also participates in the Close the Glass Loop program that aims for 90% EU-wide glass collection by 2030, a target reinforced by landfill bans for glass. Producers are responding with greater recycled content; Vetropack plans to achieve 70% cullet in melts by 2030, resulting in a 2.5% reduction in energy and a 5% reduction in CO₂ emissions per 10% increase in cullet added. Altogether, sustainability imperatives translate into demand expansion for the Austria container glass market.

Health consciousness and food-safety perception of glass

Glass remains chemically inert, eliminating migration of additives that concern health-minded buyers. This positions it as the preferred container for Austria’s premium wines, craft beers, and organic spirits, where purity narratives dominate branding. Pharmaceutical fillers utilize glass’s barrier against oxygen and moisture, and Austrian suppliers, such as Stoelzle, maintain ISO 15378 certification to meet stringent drug standards. Growing organic vineyard acreage now accounts for 20% of the national total, amplifying consumer scrutiny of packaging and reinforcing glass’s clean-label appeal. Given these attributes, the Austria container glass market continues to capture high-value applications even as lighter PET gains ground elsewhere.

Government recycling targets driving cullet usage

Mandatory Austrian quotas escalate from 70% glass recycling in 2025 to 75% in 2030, ensuring a robust cullet pipeline. Household collection must reach 85% by 2030, while large producers that exceed 300 tons of glass waste annually are required to deploy separate streams. Such regulation stabilizes the raw material supply and reduces the furnace energy load by approximately 3% for every 10% substitution of cullet. Vetropack processes about 895,000 tons of cullet company-wide, and local operations integrate proprietary sorting plants to maintain batch purity. Clear labeling codes GL 70, GL 71, GL 72 guarantee recyclate color segregation, an essential quality factor for the Austria container glass market.

Premium beverage exports boosting value-added bottles

Despite a 6% decline in 2024 wine export value, Austria still shipped EUR 233.3 million (USD 257.0 million) in bottled wine, with a focus on glass-heavy formats. Beer exports increased by 9% to 1.56 million hectoliters, sustaining steady demand for bottles. Craft spirit distillers, such as Aeijst and Kaiser Gin, choose bespoke, thick-flint bottles that elevate shelf appeal in foreign markets. Export geographies are increasingly insisting on sustainable packaging, and glass’s infinite recyclability becomes a key marketing differentiator. The resulting demand for high-end bottles drives the Austrian container glass market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High energy and production costs | -1.8% | Austria and Europe | Short term (≤ 2 years) |

| Substitution threat from PET and metal packaging | -1.2% | Global with Austrian wine exposure | Medium term (2-4 years) |

| Skilled furnace-operator shortage | -0.7% | Austria and Central Europe | Long term (≥ 4 years) |

| Rising energy prices and gas-diversion policies | -1.1% | Austria integrated into EU market | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High energy and production costs

Wholesale electricity prices averaged EUR 79.49/MWh in April 2025, 33% higher than the prior year, while gas prices reached EUR 43.49/MWh, 56% higher. With container furnaces running at 1,600 °C around the clock, such tariffs erode margins and encourage capacity relocation to lower-cost regions. Vetropack and Stoelzle counteract energy consumption through solar arrays and batch pre-heater retrofits, which reduce annual usage by up to 4,000 MWh per furnace. Austria’s EUR 55/t carbon price in 2025 adds further strain, though partial rebates for energy-intensive sectors mitigate leakage risk. Still, cost inflation remains a material drag on the Austria container glass market.

Substitution threat from PET and metal packaging

Wegenstein Winery’s PET bottle, which delivers a 38% smaller carbon footprint, underscores the rising competition from lightweight plastics. The January 2025 deposit on PET and cans may tilt retail choices, but the 25-cent charge could equally deter consumers, giving refillable glass a pricing edge. Weight disadvantages also surface in cosmetics, where glass jars achieve only 60.23% packaging efficiency against lighter laminates. Combined, these factors cap upside for the Austria container glass market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-user: Beverages Drive Reusable Innovation

In 2025, beverages accounted for 67.82% of Austria's container glass market share, driven by 10.09 million hectoliters of beer output and robust domestic wine bottlings. Updated deposits boosted returns on the ubiquitous 0.5 L bottle, while the new 0.33 L Vetropack reusable variant adds 20% more refill loops, reinforcing sustainability economics. Spirit brands leverage heavy flint for premium cues, and customized embossing differentiates craft gins exported to Germany and the United States. Cosmetics and personal care, although smaller, are projected to post a 6.08% CAGR to 2031 as recyclable glass dispensers meet the rising demand for eco-luxury positioning. Pharmaceuticals are packaged in glass vials for their inertness and regulatory compliance, ensuring a steady baseline volume. These trends solidify the beverage's core while broadening downstream applications for the Austria container glass market.

Austrians consumed 105 L of beer per capita in 2024, a top-five global rank, and 67% of domestic beer was moved in refillable containers, underpinning closed-loop bottle demand. Wine exporters are pivoting toward bulk to manage logistics costs, tempering bottle growth; yet, premium segments cling to branded glass for shelf differentiation. Food processors utilize glass’s impermeability for sauces and spreads, while baby food manufacturers maintain glass jars for safety concerns. Across end-uses, deposit-free status keeps glass cost-competitive at checkout, defending share against PET and metal rivals.

By Color: Flint Dominates While Amber Accelerates

Flint constituted 41.38% of Austria's container glass market size in 2025, favored for its clarity in beer and white wine, as well as for pharmaceutical transparency. Vetropack’s Pöchlarn furnace rebuild in 2025 aims to increase high-capacity flint output, positioning the firm to achieve 30% lighter, hard-tempered bottles by 2026. Green glass serves heritage wine aesthetics, but amber registers the fastest 6.46% CAGR through 2031, propelled by UV-sensitive spirits and medicine vials.

Stoelzle’s amber furnace upgrade in Köflach utilizes batch pre-heating to save 8% energy, an innovation aligned with decarbonization targets. Specialty cosmetic houses demand limited-run feeder colors to align with brand identity, adding value despite modest tonnage. Color-coded cullet segregation remains mandatory, safeguarding melt consistency for the Austria container glass market.

Geography Analysis

Austria sits inside a European container glass landscape that contracted after mid-2023, yet local production endured thanks to regulatory exemption from the 2025 deposit on plastic and metal. Upper Austria hosts energy-intensive furnaces and approximately 36,800 industrial jobs, prompting industry calls for further energy price relief. Lower Austria excels in recycling, with municipal systems achieving a 63% waste-glass diversion rate and only 5.9 kg of glass per capita ending up in residual waste, outperforming EU averages.

Vienna and Graz spearhead craft-spirit demand, while Waldviertel’s whisky distillery galvanizes boutique bottle orders. Access to export channels remains pivotal. Germany absorbs 60.2% of Austrian wine shipments; thus, currency swings and German consumer sentiment ripple through the Austria container glass market.

Beer flows to Italy and the United States rose in 2024, adding geographic diversification. EU transport corridors benefit from short haul distances that temper freight penalties associated with heavier glass, yet rising fuel costs threaten this advantage. Cross-border waste-glass transfers operate under the 2023 Federal Waste Management Plan, which spells out end-of-waste criteria, ensuring a stable cullet trade that underpins domestic melting operations.

Competitive Landscape

The market remains moderately concentrated. Vetropack Austria delivers 1.574 billion containers annually across its plants in Kremsmünster and Pöchlarn, translating into EUR 181 million (USD 199.1 million) in sales for 2024. Stoelzle Glass Group brings an additional 3.4 billion units globally with 90% export orientation, leveraging Austrian R&D for pharmaceutical and prestige spirits packaging.

New lightweight bottle patents from Vetropack promise 30% mass reduction, cutting logistics costs and carbon footprints. Stoelzle installed rapid-prototyping 3D printers, which shrink customer development cycles from weeks to hours, thereby enhancing design agility. Niche player Cristallo positions itself in bespoke, short-run production for craft gins and whiskies.

Market entry remains difficult, as evidenced by the competition authority's scrutiny of the Gerresheimer-Bormioli deal, due to high barriers in the soda-lime pharmaceutical glass market. Energy relief schemes and investment grants influence site selection, yet domestic players still weigh offshoring against reputational gains from “Made in Austria” branding. Substitution risk compels glass makers to aggressively market their sustainability credentials to defend the Austrian container glass market.

Austria Container Glass Industry Leaders

Vetropack Austria GmbH

Stoelzle Oberglas GmbH

Cristallo Glas GmbH

Etivera Verpackungstechnik GmbH

Ardagh Group S.A

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Vetropack approved industrial-scale output of thermally hardened lightweight bottles at Pöchlarn, with production slated for summer 2026.

- May 2025: Stoelzle installed UV-cured acrylate 3D printers in Köflach to speed sample bottle delivery.

- March 2025: Deposit on 0.5 L reusable beer bottles increased from EUR 9 to EUR 20, raising return incentives for glass containers.

- January 2025: Austria’s deposit regulation took effect, imposing EUR 0.25 on PET bottles and cans while exempting glass, establishing a competitive moat for the Austria container glass market.

Austria Container Glass Market Report Scope

Container glass is used in the alcoholic and non-alcoholic beverage industries due to its ability to maintain chemical inertness, sterility, and non-permeability. Glass packaging is valued for its unique properties, including its transparency, inertness, and ability to preserve the quality and integrity of its contents. It is often chosen for products where purity, safety, and environmental sustainability are paramount concerns.

Austria container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery), by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

How large is Austria’s container glass sector today?

The Austria container glass market size reached 538.58 kilotons in 2026 and is forecast to hit 688.95 kilotons by 2031.

What CAGR is expected for Austrian container glass through 2031?

The industry is projected to post a 5.05% CAGR between 2026 and 2031.

Which end-use category dominates demand?

Beverages led with a 67.82% share in 2025, reflecting Austria’s strong brewing and wine traditions.

What is the fastest-growing segment within the market?

Cosmetics and personal care packaging registers the highest growth, advancing at a 6.08% CAGR through 2031.

How are energy costs affecting producers?

Electricity and gas prices remain around twice pre-crisis levels, prompting firms to deploy solar, cullet, and furnace upgrades to mitigate expense spikes.

Why is glass still favored despite PET competition?

Glass offers infinite recyclability, chemical inertness, and exemption from Austria’s 2025 deposit on plastic and metal containers, preserving its premium position.

Page last updated on: