Asset Management Enterprise Resource Planning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

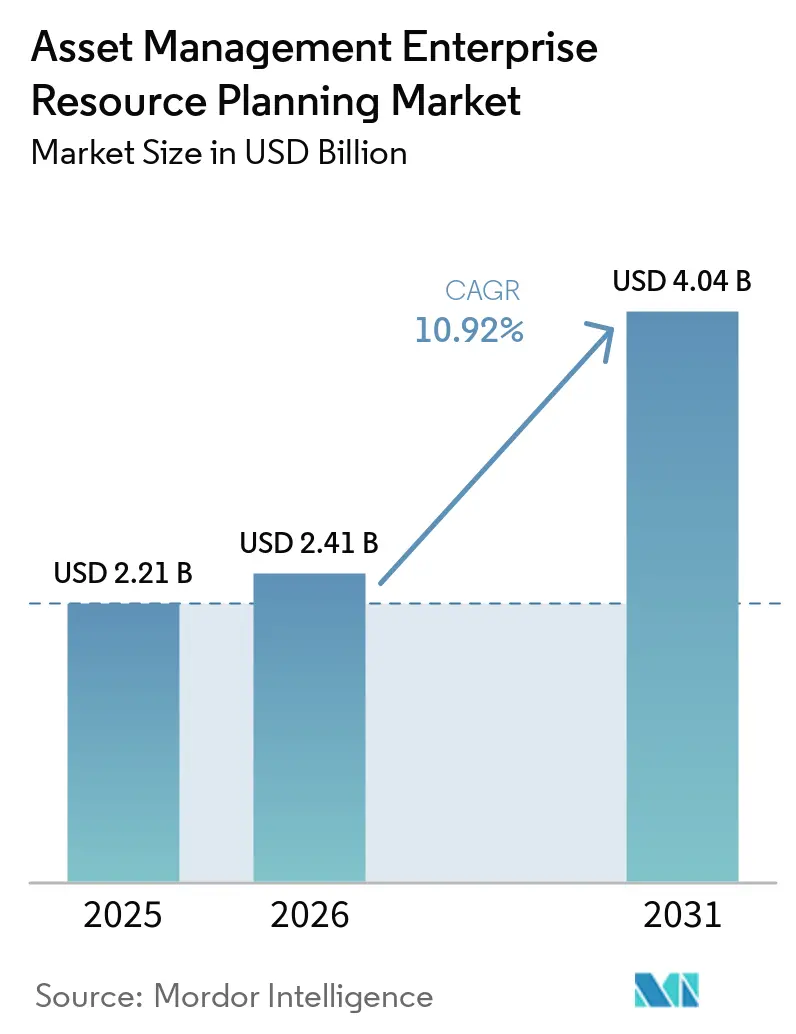

| Market Size (2026) | USD 2.41 Billion |

| Market Size (2031) | USD 4.04 Billion |

| Growth Rate (2026 - 2031) | 10.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asset Management Enterprise Resource Planning Market Analysis by Mordor Intelligence

The Asset Management Enterprise Resource Planning (ERP) market size is expected to grow from USD 2.21 billion in 2025 to USD 2.41 billion in 2026 and is forecast to reach USD 4.04 billion by 2031 at 10.92% CAGR over 2026-2031. The migration from fragmented legacy systems to cloud-native suites is reshaping asset-intensive sectors, giving enterprises real-time lifecycle visibility and predictive maintenance that trims downtime and supports capital efficiency. Vendor focus on embedded artificial intelligence, industrial IoT telemetry, and automated Scope 3 emissions reporting is widening the addressable base across manufacturing, energy, transportation, and the public sector. Subscription pricing and containerized microservices are lowering upfront barriers, though data integration complexity and cybersecurity obligations are adding implementation friction. Strategic acquisitions that bundle warehouse execution, field inspection, and security analytics into unified platforms are intensifying competition while creating richer ecosystems for partners and developers.

Key Report Takeaways

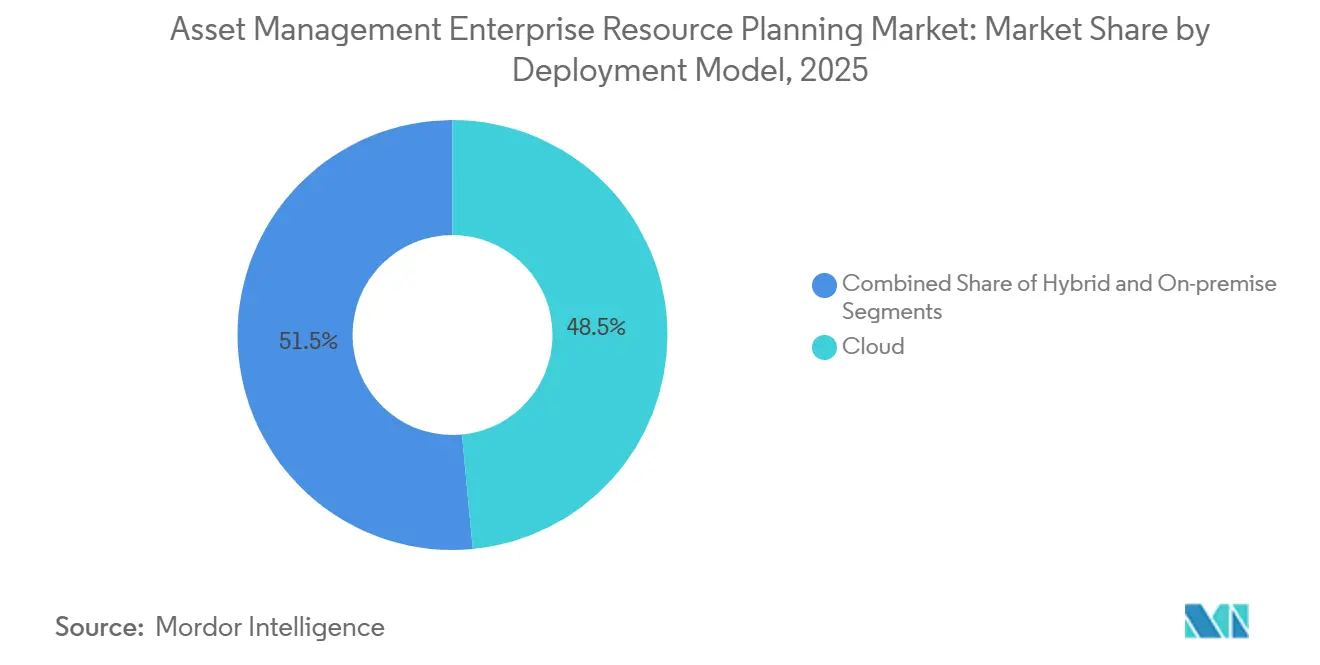

- Cloud deployment led the Asset Management Enterprise Resource Planning (ERP) market with 48.50% market share in 2025 and is widening its lead at a 12.30% CAGR through 2031.

- Large enterprises accounted for 60.30% of 2025 revenue, while small and medium enterprises are advancing at a 11.60% CAGR on the back of usage-based pricing.

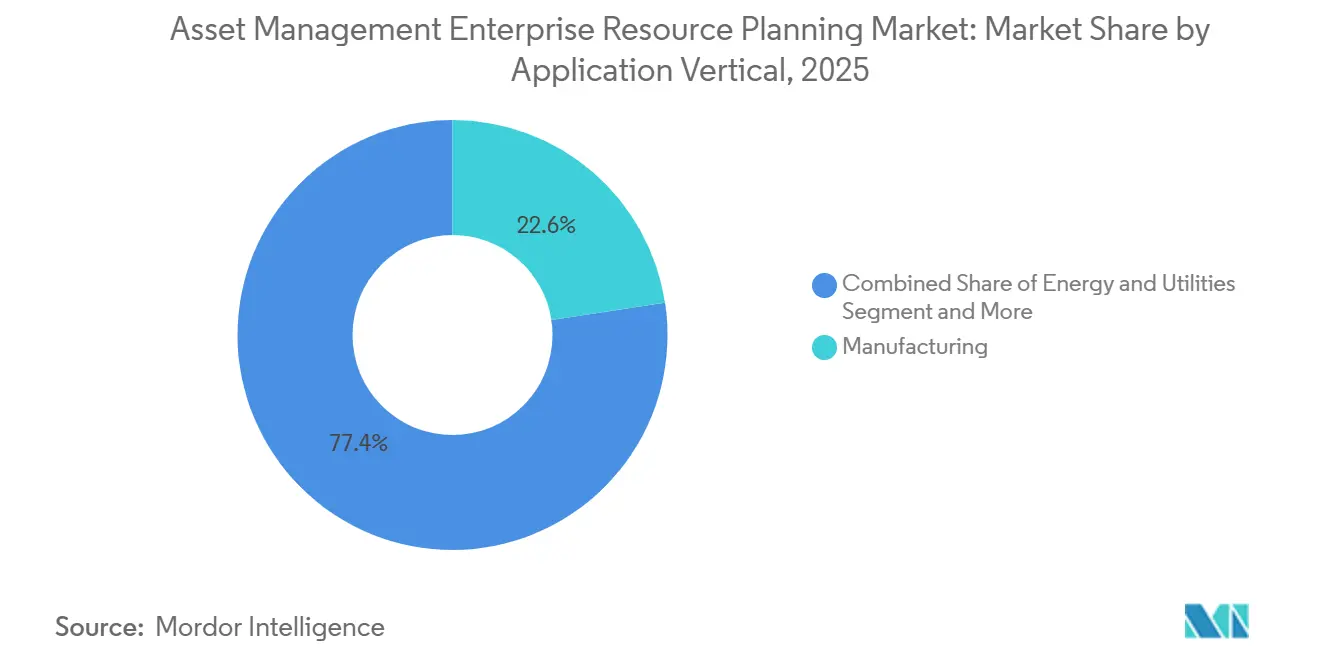

- Manufacturing accounted for 22.60% of 2025 spending, whereas transportation and logistics are expanding at a 13.80% CAGR as fleet electrification accelerates.

- Asset lifecycle management controlled 19.40% of 2025 revenue, yet predictive maintenance is scaling fastest at a 14.90% CAGR as AI models mature.

- North America captured 33.40% of 2025 revenue, but Asia-Pacific is the growth engine with an 11.40% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Asset Management Enterprise Resource Planning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Migration to Cloud-Based Deployment Models | +2.1% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Growing Adoption of IoT Sensors Enabling Predictive Maintenance | +1.8% | Global, APAC manufacturing hubs and North America utilities | Long term (≥ 4 years) |

| Rising Demand to Reduce Unplanned Downtime in Asset-Intensive Industries | +1.5% | Global, led by manufacturing, energy, transportation | Medium term (2-4 years) |

| Convergence of EAM and Sustainability Reporting for Scope 3 Compliance | +1.3% | Europe, North America, expanding to APAC | Long term (≥ 4 years) |

| Uptake of AI-Driven Master-Data Cleansing Tools | +0.9% | Global, early in North America and Europe | Short term (≤ 2 years) |

| Availability of Usage-Based Subscription Pricing for Mid-Tier Manufacturers | +0.7% | Global, high in APAC and South America SME segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Migration to Cloud-Based Deployment Models

Cloud-native suites let enterprises offload infrastructure, accelerate feature delivery, and align expenses with consumption. Cloud ERP spending will shift toward AI-enabled solutions by 2027, highlighting a pivot toward platforms that embed machine learning into valuation and depreciation workflows. According to NetSuite, Hybrid architectures remain prevalent, with 88% of organizations retaining sensitive ledgers on private clouds while scaling analytics in the public cloud. Containerization has been adopted in significant production environments, making asset modules portable across clouds and simplifying disaster recovery. However, several percent of enterprises have repatriated workloads amid unforeseen costs, underscoring the need for FinOps governance and automated cost controls. Overall, cloud acceleration is unlocking rapid IoT integration and predictive analytics, making it the largest single growth lever for the Asset Management Enterprise Resource Planning (ERP) market.

Growing Adoption of IoT Sensors Enabling Predictive Maintenance

IEEE case studies confirm that sensor-to-ERP integration automates maintenance request processing and failure threshold alerts, reducing manual entry and enabling predictive workflows. Utilities are early adopters: DNV’s Cascade links SCADA historians to asset scores, while SAS analytics detect turbine anomalies to enable proactive scheduling. Security remains a hurdle because most IoT devices lack agents and ship with default credentials, forcing enterprises to rely on micro-segmentation and network detection to safeguard ERP interfaces. As coverage gaps close, predictive maintenance will continue to outpace other modules within the Asset Management Enterprise Resource Planning (ERP) market.

Rising Demand to Reduce Unplanned Downtime in Asset-Intensive Industries

Downtime erodes throughput and drives regulatory penalties, prompting a shift to condition-based maintenance. IBM Maximo Condition Insight embeds watsonx agents that parse work orders, time-series data, and failure modes to deliver prescriptive recommendations within seconds. Schneider Electric reports 40% shorter outages by fusing weather forecasts with grid analytics. Agentic AI automates the full loop: monitoring detects wear, AI triggers part requisition and technician scheduling, and human oversight approves high-risk tasks. These autonomous workflows reposition maintenance from a cost center to a performance driver, expanding the value proposition for the Asset Management Enterprise Resource Planning (ERP) market.

Convergence of EAM and Sustainability Reporting for Scope 3 Compliance

Regulators now require quantification of Scope 3 emissions, which often make up the majority of corporate footprints. SAP Sustainability Data Exchange enables enterprises to share product carbon data with suppliers and customers, replacing estimates with verified figures.[1]Amit Tandon, “Tracking Scope 3 Emissions Using SAP SDX,” SAP Community, sap.com The GHG Protocol mandates coverage of 15 categories, compelling ERPs to ingest procurement, travel, fuel, and investment data while managing emission factors and allocation logic. The EU Cyber Resilience Act tightens timelines by requiring 24-hour breach reporting, causing vendors to unify cybersecurity telemetry with carbon accounting so both can leverage common data pipelines. Integrating sustainability into asset workflows expands ERP relevance to finance and ESG teams, boosting demand across the Asset Management Enterprise Resource Planning (ERP) market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Integration Cost with Legacy ERP Systems | -1.4% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Cybersecurity and Data-Privacy Concerns in Connected Asset Ecosystems | -1.1% | Global, regulatory pressure highest in Europe, rising in North America | Medium term (2-4 years) |

| Shortage of Certified Asset Management ERP Implementation Specialists | -0.8% | Global, intense in APAC and emerging markets | Medium term (2-4 years) |

| Vendor Lock-In Risk Due to Proprietary Data Models | -0.6% | Global, complicates multi-cloud and hybrid strategies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Integration Cost with Legacy ERP Systems

Decades of custom code and undocumented interfaces make modernization expensive. Process-mining tools reveal hidden inefficiencies: production often lags records by two days, and BOMs misstate changeover rules, underscoring the need for master-data remediation before go-live. Organizations that neglect this step risk automating poor workflows and eroding the ROI of the Asset Management Enterprise Resource Planning (ERP) market rollout.

Cybersecurity and Data-Privacy Concerns in Connected Asset Ecosystems

Forescout tracked 2,155 industrial CVEs in 2025, 82% of which were rated high or critical, highlighting the attack surface that arises when ERP links IT, OT, and IoT layers.[2]Rob Hulsebos, “ICS Vulnerabilities and the Path Forward,” Forescout Blog, forescout.com Many devices ship with default credentials and see infrequent patching; 60% of IoT breaches originate in outdated firmware. The EU Cyber Resilience Act imposes 24-hour reporting and fines of up to EUR 15 million, forcing vendors to adopt secure-by-design practices and to publish software bills of materials. Compliance demands network segmentation, identity-aware gateways, and digital twin testbeds, adding costs and complexity that may delay projects in the Asset Management Enterprise Resource Planning (ERP) market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Dominance Accelerates as Hybrid Architectures Mature

Cloud deployments accounted for 48.50% of the Asset Management Enterprise Resource Planning (ERP) market share in 2025, and the segment is forecast to grow at a 12.30% CAGR through 2031. Organizations prefer vendor-managed infrastructure and rapid feature releases, while containerized microservices improve portability for hybrid strategies. The Asset Management Enterprise Resource Planning (ERP) market size attached to cloud deployments will expand as AI-enabled services move maintenance analytics and carbon accounting closer to compute power.

On-premise solutions persist where latency and data-sovereignty mandates prevail, especially in defense and heavily regulated utilities. Hybrid models, now embraced by 88% of enterprises, balance these constraints by keeping sensitive ledgers on private clouds and using public regions for scaling analytics. FinOps guardrails are becoming standard because 54% of enterprises cannot accurately track cloud spend, threatening to offset savings from hardware avoidance. Overall, the deployment choice now hinges more on regulatory and latency considerations than on technical capability differentials.

By Organization Size: SME Adoption Surges on Usage-Based Pricing

Large enterprises accounted for 60.30% of 2025 revenue, but small and medium enterprises are expanding at a 11.60% CAGR as vendors roll out consumption-based pricing, low-code templates, and managed services. The Asset Management Enterprise Resource Planning (ERP) market size accruing to SMEs will benefit from easier onboarding and reduced capital expenditure.

Resource constraints still challenge SMEs, yet SaaS suites that bundle finance, supply chain, and asset modules with automated master-data cleansing narrow the capability gap. In APAC and South America, cloud-first government incentives and currency-hedged subscription offers further lower adoption barriers. As usage-based pricing matures, SMEs are expected to drive a larger share of incremental demand over the forecast period.

By Application Vertical: Transportation and Logistics Leads Growth Amid Electrification

Manufacturing accounted for 22.60% of 2025 revenue, attributable to early ERP adoption, though its growth is steadier than that of faster-moving service industries. The Asset Management Enterprise Resource Planning (ERP) market share within transportation and logistics will surge as electrification mandates pressure operators to digitize fleet maintenance and route optimization.

Energy and utilities are integrating real-time grid analytics, DER orchestration, and compliance workflows, relying on predictive modules to extend the lifespan of aging infrastructure. Public-sector agencies are modernizing to improve citizen services and meet transparency mandates, while healthcare facilities need asset-tracking systems for regulatory and quality-assurance purposes. The unifying thread is the demand for data-driven maintenance that aligns uptime, safety, and sustainability metrics.

By Module and Functionality: Predictive Maintenance Surges as AI Capabilities Mature

In 2025, asset lifecycle management accounted for 19.40% of total spending, emphasizing the management of work orders, inventories, and depreciation ledgers. At the same time, predictive maintenance is witnessing significant growth, with a compound annual growth rate (CAGR) of 14.90%, making it the fastest-growing revenue stream within the Asset Management Enterprise Resource Planning (ERP) market.

Advanced features such as voice-enabled mobile applications, automated work-order creation, and explainable artificial intelligence are driving increased user adoption, extending usage beyond traditional reliability engineers. Moreover, financial accounting modules now integrate depreciation data with asset health insights, enabling CFOs to make more accurate, strategic decisions about the timing of capital replacements. Additionally, sustainability-focused add-ons that calculate Scope 3 carbon footprints are embedding environmental data into core asset records. This integration provides boards with a centralized, reliable source of information for both financial reporting and Environmental, Social, and Governance (ESG) disclosures, enhancing transparency and decision-making.

Geography Analysis

North America accounted for 33.40% of 2025 revenue, supported by mature cloud infrastructure and early adoption of AI-driven analytics. Migration from SAP ECC to S/4HANA before the 2027 deadline is accelerating deals, though data-cleansing complexity is stretching timelines. The extraterritorial reach of the EU Cyber Resilience Act is prompting U.S. vendors to harden their products preemptively, embedding vulnerability-reporting and SBOM features to maintain European market access.

Asia-Pacific, the fastest-growing region at 11.40% CAGR, benefits from large-scale infrastructure investment in China and India and semiconductor capacity expansion backed by private commitments exceeding USD 500 billion. SMEs across Southeast Asia are leveraging subscription licensing to access enterprise-grade functionality without capital strain, further lifting regional demand.

Europe faces stringent cybersecurity and sustainability requirements, making integrated compliance features a must-have. The Middle East and Africa and South America remain nascent but promising. UAE conglomerates rolling out Infor M3 and Brazilian mid-market manufacturers adopting NetSuite SaaS platforms reflect rising interest where cloud regions and foreign-exchange-hedged pricing mitigate macro risks. Government cloud-first mandates, such as Kenya’s trusted data zone projects, illustrate how sovereign-cloud provisions unlock adoption among state-owned utilities and transportation agencies.[3]Microsoft News Center Staff, “Microsoft and G42 Announce USD 1 Billion Kenya Cloud Investment,” microsoft.com Absent major economic shocks, regional uptake is expected to broaden steadily through 2031.

Competitive Landscape

Market concentration is moderate, with SAP, Oracle, IBM, Infor, and IFS anchoring global share through full-suite offerings and extensive partner ecosystems. These incumbents are acquiring niche vendors to plug functionality gaps: IFS merged with Softeon to blend warehouse execution and Industrial AI, processing millions of monthly orders across 30 countries. ServiceNow’s planned USD 7.75 billion purchase of Armis will embed real-time asset discovery into its platform, tripling security revenue and extending reach into OT environments.

Bentley Systems is expanding AI-driven inspection services via Talon Aerolytics and Pointivo, pushing asset analytics as a consumption-based service.[4]Anthony Davis, “Bentley Systems Expands Asset Analytics,” highways.today Smaller players differentiate through open-source stacks, vertical templates, or low-code extensibility, appealing to SMEs and greenfield adopters. Regulatory overhead, especially the EU Cyber Resilience Act, raises switching costs, favoring vendors with mature security postures and coordinated vulnerability disclosure.

White-space opportunities lie at the intersection of asset intelligence and sustainability reporting, where unified carbon and maintenance datasets drive board-level insights. Vendors embedding agentic AI to autonomously resolve supply disruptions or automate warranty claims are redefining competitive baselines. Buyers now evaluate not just feature breadth but explainability of AI outputs, cross-cloud portability, and evidence of secure-by-design practices.

Asset Management Enterprise Resource Planning Industry Leaders

IBM Corporation

SAP SE

Oracle Corporation

Infor, Inc.

IFS AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: SAP released Cloud ERP Private 2025 FPS01, adding AI-enabled Change Record Management Agents and industry data products for asset services.

- March 2026: IFS closed its Softeon acquisition, forming IFS Softeon to blend warehouse management, robotics orchestration, and Industrial AI.

- February 2026: SAP launched Cloud ERP 2602 updates with a new Asset Overview app, Permit to Work processes, and Joule AI copilot integration.

- January 2026: Bentley completed Talon Aerolytics and Pointivo acquisitions to expand AI-driven analytics for telecom and utilities.

Global Asset Management Enterprise Resource Planning Market Report Scope

The Asset Management Enterprise Resource Planning (ERP) market comprises integrated software solutions that manage, monitor, and optimize the lifecycle of physical and financial assets across an organization. These systems support asset-intensive industries by enabling efficient asset tracking, maintenance planning, utilization optimization, and compliance management, while improving operational reliability and reducing total cost of ownership.

The Asset Management Enterprise Resource Planning (ERP) Market Report is Segmented by Deployment Model (Cloud, On-Premise, Hybrid), Organization Size (Large Enterprises, Small and Medium Enterprises), Application Vertical (Manufacturing, Energy and Utilities, Transportation and Logistics, Government and Public Sector, Healthcare, Other Application Verticals), Module and Functionality (Asset Lifecycle Management, Work Order Management, Inventory and Spare Parts Management, Predictive Maintenance, Financial Asset Accounting, Other Modules), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa).

| Cloud |

| On-Premise |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Manufacturing |

| Energy and Utilities |

| Transportation and Logistics |

| Government and Public Sector |

| Healthcare |

| Other Application Verticals |

| Asset Lifecycle Management |

| Work Order Management |

| Inventory and Spare Parts Management |

| Predictive Maintenance |

| Financial Asset Accounting |

| Other Modules |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Deployment Model | Cloud | |

| On-Premise | ||

| Hybrid | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Application Vertical | Manufacturing | |

| Energy and Utilities | ||

| Transportation and Logistics | ||

| Government and Public Sector | ||

| Healthcare | ||

| Other Application Verticals | ||

| By Module | Asset Lifecycle Management | |

| Work Order Management | ||

| Inventory and Spare Parts Management | ||

| Predictive Maintenance | ||

| Financial Asset Accounting | ||

| Other Modules | ||

| BY GEOGRAPHY | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What growth rate is forecast for the Asset Management Enterprise Resource Planning (ERP) market through 2031?

The market is projected to expand at a 10.92% CAGR between 2026 and 2031, rising from USD 2.41 billion in 2026 to USD 4.04 billion by 2031.

Which deployment model is growing fastest in Asset Management ERP?

Cloud deployment is outpacing alternatives, holding 48.50% share in 2025 and expanding at a 12.30% CAGR through 2031.

Why are transportation and logistics companies investing in Asset Management ERP now?

Fleet electrification mandates and real-time telematics integration are pushing the vertical to adopt predictive maintenance, driving a 13.80% CAGR for the period.

How are small and medium enterprises adopting Asset Management ERP?

Usage-based subscription pricing and low-code templates lower upfront costs, helping SMEs achieve an 11.60% CAGR in adoption.

What regulatory trend is shaping ERP cybersecurity requirements?

The EU Cyber Resilience Act mandates 24-hour reporting of exploited vulnerabilities beginning in 2026, driving vendors to embed secure-by-design and SBOM capabilities.

Which module is moving fastest within Asset Management ERP suites?

Predictive maintenance is the fastest-growing module, registering a 14.90% CAGR as AI models mature and IoT sensor data proliferates.

Page last updated on: