Fixed Asset Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

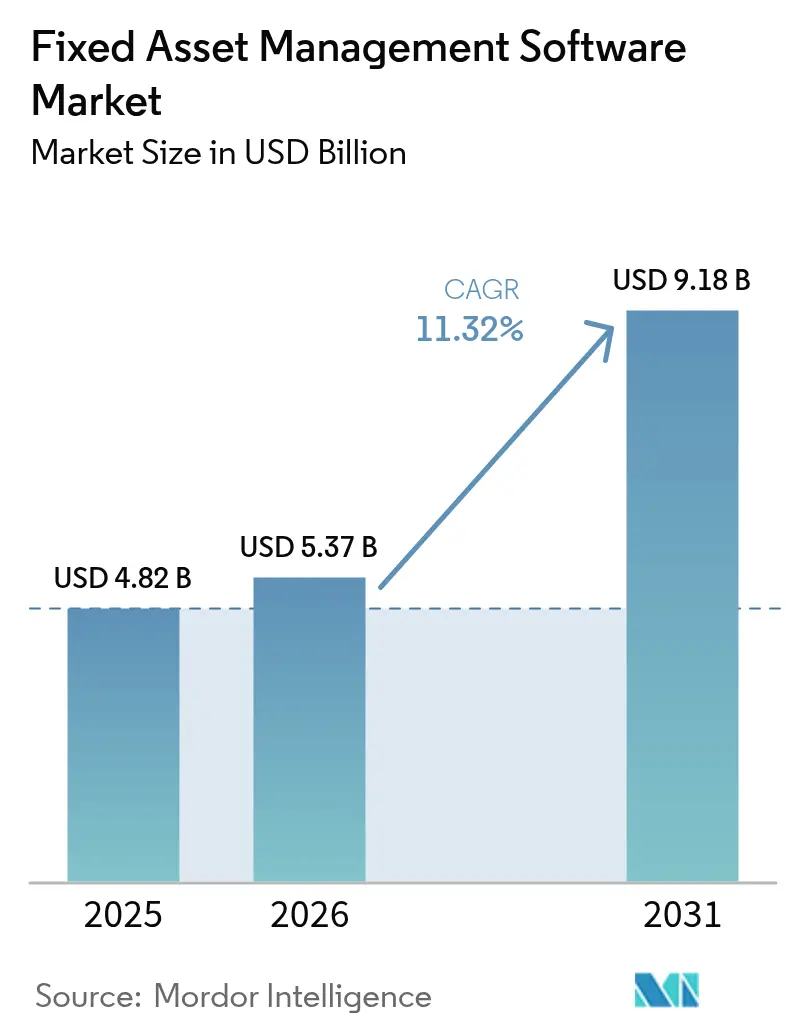

| Market Size (2026) | USD 5.37 Billion |

| Market Size (2031) | USD 9.18 Billion |

| Growth Rate (2026 - 2031) | 11.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fixed Asset Management Software Market Analysis by Mordor Intelligence

The fixed asset management software market size was valued at USD 4.82 billion in 2025 and estimated to grow from USD 5.37 billion in 2026 to reach USD 9.18 billion by 2031, at a CAGR of 11.32% during the forecast period (2026-2031). Surging investment in real-time tracking, predictive maintenance, and cloud-native architectures is elevating software from a record-keeping tool to a strategic operations platform, especially in manufacturing, transportation, and healthcare. North America continues to anchor global demand, yet sustained double-digit growth in Asia-Pacific is shifting the competitive focus toward localized regulatory support and lower-cost SaaS deployments. Vendors are sharpening value propositions around ESG reporting, AI-driven cost savings, and risk-based maintenance, while acquisitions by Siemens and Prometheus Group demonstrate rising consolidation momentum among platform providers. Despite persistent concerns over multi-tenant cloud security and SME budget constraints, low-code configuration, subscription pricing, and government digitalization incentives are expanding addressable demand and tightening payback cycles for buyers.

Key Report Takeaways

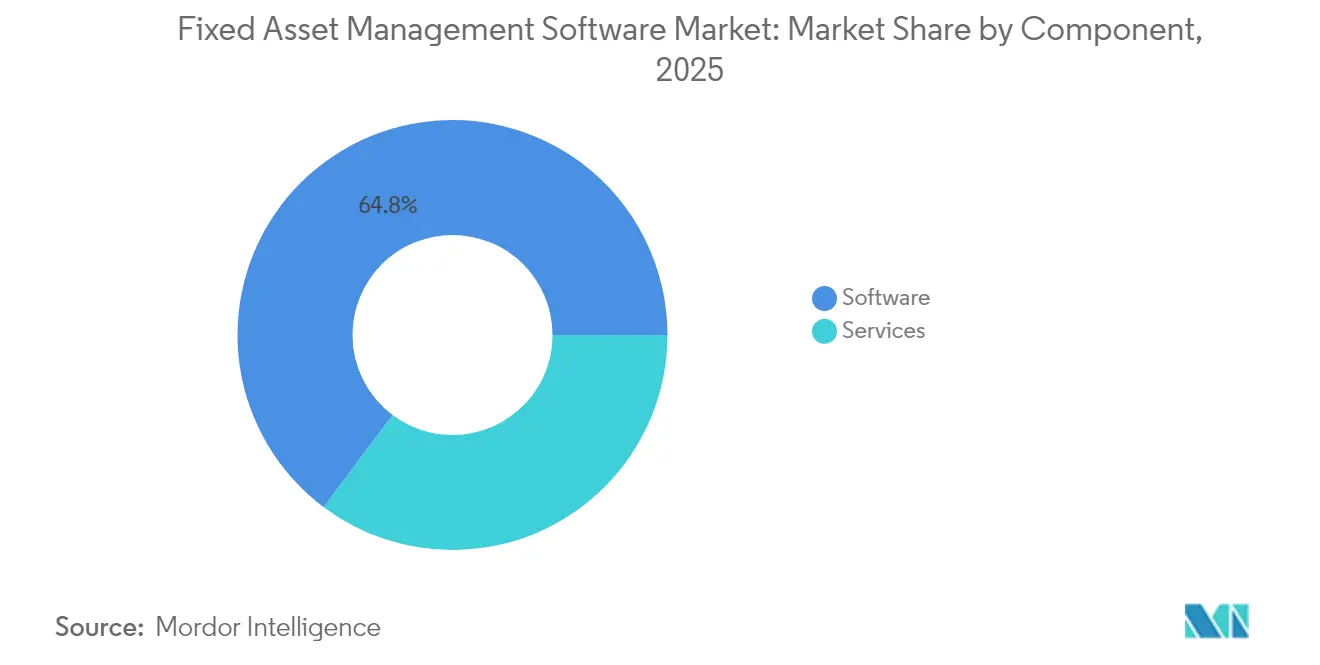

- By component, the software category led with 64.78% of fixed asset management software market share in 2025, while services are advancing at a 13.22% CAGR through 2031.

- By deployment model, on-premise systems held 62.95% of the fixed asset management software market size in 2025, yet cloud solutions are projected to grow at a 13.26% CAGR.

- By enterprise size, large enterprises commanded 71.25% of fixed asset management software market size in 2025; SMEs represent the fastest growth at 12.57% CAGR.

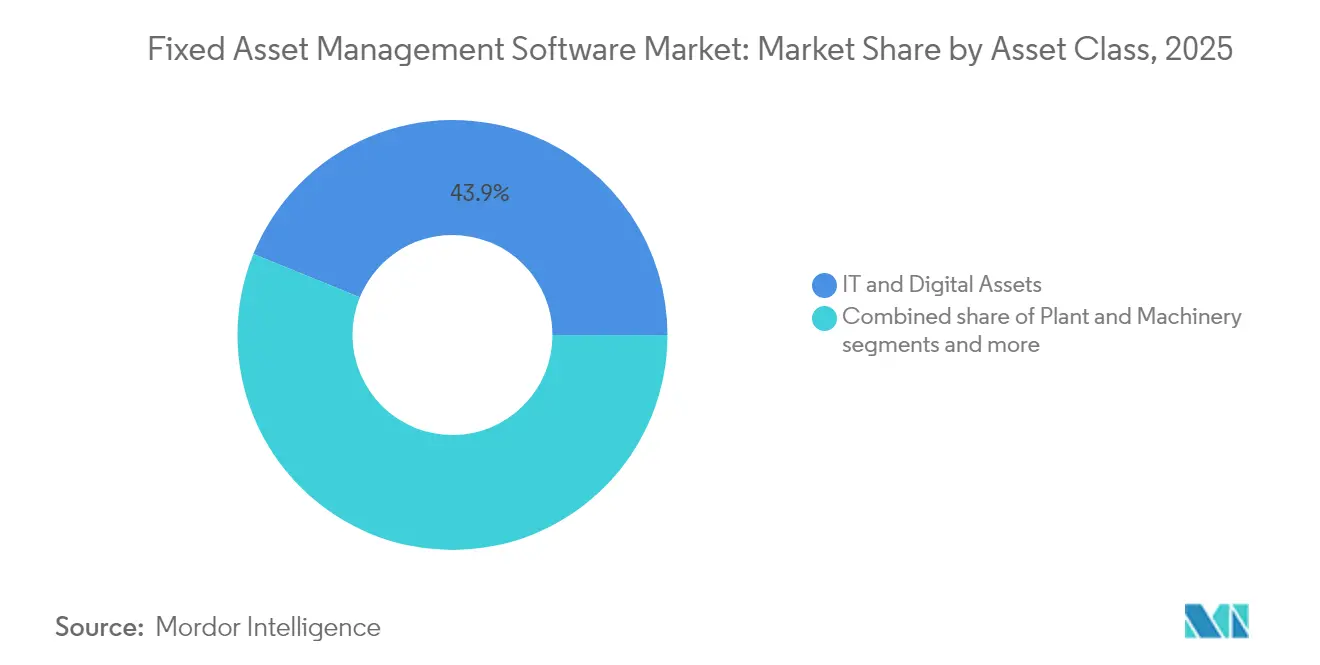

- By asset class, IT and digital assets held 43.85% share of the fixed asset management software market size in 2025, while fleet and mobile equipment is projected to expand at a 12.34% CAGR through 2031.

- By end-user industry, industrial manufacturing accounted for 21.72% fixed asset management software market share in 2025, whereas transportation and logistics are expanding at an 11.63% CAGR.

- By geography, North America led with 36.88% revenue share in 2025; Asia-Pacific is poised for a 12.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Fixed Asset Management Software Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost barrier for SMEs | −0.8% | Global, acute in developing economies | Short term (≤ 2 years) |

| Data-security and privacy concerns | −0.6% | EU and North America, expanding globally | Medium term (2-4 years) |

| Legacy-equipment integration complexity | −0.5% | North America & Europe | Medium term (2-4 years) |

| Vendor-lock and limited interoperability | −0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Focus on Optimizing Operational Cost

Cost containment tops CIO agendas as inflation and supply chain volatility pressure margins. IFS recorded a 33% surge in software revenue and a 46% jump in cloud revenue during 2024, evidence that buyers prioritize rapid payback and operating-expense models over capital-heavy deployments[1]IFS, “IFS Generates Continued Strong Momentum in 2024,” ifs.com. AI-enhanced modules identify underutilized equipment, predict part failures, and rebalance maintenance schedules to lower unplanned downtime. Manufacturing SMEs illustrate the benefit: peer-reviewed studies confirm Industrial IoT systems deliver statistically significant cost reductions that exceed installation spend, accelerating adoption beyond large multinationals. Vendors now embed ROI dashboards and savings guarantees in proposals to shorten decision cycles and neutralize budget objections.

Growing Adoption of IoT-enabled Real-time Asset Tracking

Sensor miniaturization and affordable connectivity underpin a dramatic leap in asset visibility. Hospitals deploy RFID and Bluetooth tags to slash equipment search time, curbing rental fees and asset loss. The hospital asset tracking market itself is advancing at 16.8% CAGR, reinforcing healthcare’s status as an early adopter. Transportation platforms integrate telematics, route optimization, and condition monitoring, propelling sector software revenue to USD 72 billion at an expected 19.8% CAGR. Real-time datasets also enhance regulatory audits, producing immutable trails that satisfy ISO and safety mandates while feeding predictive models that shift maintenance from reactive to proactive.

Regulatory and Financial-audit Compliance Pressures

Governments are tightening asset stewardship rules that mandate detailed lifecycle documentation. The U.S. General Services Administration requires executive agencies to operate Joint Financial Management Improvement Program-compliant systems, converting compliance into a non-discretionary budget line[2]U.S. General Services Administration, “Asset Management Systems Requirements,” gsa.gov. The IRS formalized IT asset controls in 2024, signaling an enterprise-grade discipline now expected across federal departments. Healthcare providers confront FDA equipment tracking mandates that feed demand for specialized modules integrating with hospital information systems. These directives insulate the fixed asset management software market from macro-economic cycles by codifying asset management into governance frameworks.

Rapid Shift Toward Cloud-native SaaS EAM Suites

Cloud uptake has moved past lift-and-shift toward composable, AI-ready architectures. GE Vernova’s migration to a cloud-based Asset Performance Management environment documented faster upgrade cycles and enhanced cybersecurity versus on-premise estates. PwC reported that 92% of high-performing firms will lift cloud spending in 2025 to gain elastic compute for AI workloads. Subscription models lower entry barriers for SMEs, while zero-touch updates cut overhead for large enterprises. Cloud platforms also enable digital twin visualizations and augmented-reality workflows that field technicians access via tablets and smart glasses.

Restraints Impact Analysis of Fixed Asset Management Software Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost barrier for SMEs | −0.8% | Global, acute in developing economies | Short term (≤ 2 years) |

| Data-security and privacy concerns | −0.6% | EU and North America, expanding globally | Medium term (2-4 years) |

| Legacy-equipment integration complexity | −0.5% | North America and Europe | Medium term (2-4 years) |

| Vendor-lock and limited interoperability | −0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost Barrier for SMEs

Comprehensive platforms can require USD 200,000–250,000 for custom deployments in healthcare, sums that deter smaller firms. Surveys of 4,500 SMEs confirm financial limitations and skills shortages remain the largest drag on digital uptake. OECD analyses underscore that SMEs lag larger rivals in advanced software adoption, widening productivity gaps. Vendors counter with tiered SaaS packages, phased rollouts, and government-backed grants that distribute expenditure over subscription cycles, although budget hesitancy persists in emerging economies.

Data-security and Privacy Concerns in Multi-tenant Clouds

Critical asset telemetry traverses public clouds, raising fears of industrial espionage and non-compliance with data sovereignty laws. The U.S. Chief Information Officers Council cautions that agencies remain responsible for security even when workloads sit on third-party infrastructure. Manufacturers guarding intellectual property often favor hybrid architectures that keep sensitive analytics on-premise, yet hyperscalers now tout zero-trust frameworks, customer-managed keys, and sector-specific certifications to mitigate risk perception. Progress is steady but the trust gap still subtracts from the overall growth rate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Fixed Asset Management Software Market Segment Analysis

By Component:

Services Accelerate Implementation SuccessSoftware modules retained 64.78% of the fixed asset management software market share in 2025 as enterprises demanded integrated tracking, depreciation, and compliance functionality. Growth now centers on services, which are expanding at 13.22% CAGR through 2031 because migrations from legacy databases, data cleansing, and change-management programs require external expertise. Implementation partners design IoT sensor layouts, map maintenance hierarchies, and train users in predictive workflows, activities that internal teams struggle to resource. Managed services appeal to SMEs lacking 24/7 IT support, offering end-to-end monitoring, patching, and reporting under pay-as-you-go terms.

The asset tracking and bar-coding sub-segment benefits directly from the IoT surge, while AI-infused predictive maintenance modules help organizations avoid catastrophic downtime. Accounting teams rely on depreciation calculators to align with evolving tax schedules, especially in jurisdictions rolling out accelerated write-off rules. Compliance modules now embed ESG metrics such as energy intensity and emissions intensity, allowing automated export into sustainability reports. Collectively, the breadth of functionality reinforces the fixed asset management software market as the foundational layer for enterprise performance data.

By Deployment Model:

Cloud Transformation AcceleratesOn-premise systems commanded 62.95% of the fixed asset management software market size in 2025, a legacy function of earlier capital-expense cycles and tight security postures in sectors like defense. Yet cloud platforms are scaling at 13.26% CAGR as CIOs pursue elastic resources that handle sensor streams and AI workloads. Early adopters cite automatic versioning, lower hardware refresh outlays, and anytime mobile access for distributed technicians. Hybrid patterns persist: sensitive process controls remain on-site while analytics dashboards reside in regional clouds for latency-tolerant use cases.

Edge computing augments both models by pre-processing vibration or thermal imagery at gateways before sending summaries to the cloud, reducing bandwidth and cost. Vendors such as IFS indicated cloud revenue rising 46% in 2024 as license customers transition to usage-based contracts. The direction is unequivocal. By 2030, the fixed asset management software market narrative will center on SaaS consumption, AI copilots, and click-configured workflows rather than server counts.

By Enterprise Size:

SME Adoption Democratizes TechnologyLarge corporations still dominate spending, with a 71.25% fixed asset management software market size in 2025, because they manage extensive plant footprints, aircraft fleets, or national logistics networks. These firms integrate asset suites with ERP, supply chain, and financial consolidation tools to produce a single system of record. However, SMEs represent the fastest expansion at 12.57% CAGR. Subscription pricing, template libraries, and low-code configurators eliminate many historical barriers. Mobile-first interfaces empower frontline workers without lengthy classroom sessions, which is critical for firms lacking dedicated IT trainers.

Government subsidies and fintech leasing programs further soften upfront costs. The OECD credits pandemic-era remote work mandates with accelerating cloud adoption among smaller factories and field-service businesses. As SMEs scale digital maturity, they unlock predictive scheduling, inventory rationalization, and warranty recovery benefits once reserved for Fortune 500 peers. This democratization widens the overall fixed asset management software industry revenue stream and diversifies vendor go-to-market channels.

By Asset Class:

Digital Assets Lead Enterprise PriorityIT and digital assets formed the largest share at 43.85% in 2025. Cybersecurity regulations, software-license audits, and remote work flexibility forced organizations to inventory servers, network gear, and SaaS seats with granular precision. Plant and machinery assets follow closely, reflecting the continual drive for throughput and energy efficiency on production lines. Fleet equipment is the breakout category, recording a 12.34% CAGR, as telematics-enabled vehicles deliver data that feeds into consolidated dashboards for dispatchers and finance teams.

Real-estate and infrastructure assets add momentum thanks to smart-building retrofits and corporate sustainability targets. As asset classes converge in dashboards, management teams gain a panoramic view that supports cross-asset investment decisions. Interdependency mapping flags how an HVAC failure could jeopardize a data center or how poor truck maintenance inflates carbon footprints, weaving ESG priorities back into everyday operations inside the fixed asset management software market.

By End-user Industry:

Manufacturing Leads While Transportation AcceleratesIndustrial manufacturing commanded 21.72% of fixed asset management software market share in 2025, propelled by Industry 4.0 programs that combine condition sensors with MES and ERP data for closed-loop optimization. Predictive analytics minimize stoppages on high-cost machinery, and quality modules link asset performance to final product defects. Transportation and logistics achieve the swiftest growth at 11.63% CAGR through 2031. E-commerce demand, last-mile delivery complexity, and green fleet regulations drive carriers to instrument vehicles, warehouses, and containers.

Healthcare institutions deploy specialized systems for surgical instrument tracking, infusion pump utilization, and FDA reporting requirements, matching the hospital asset tracking surge documented earlier. Utilities digitize substations and meters to coordinate renewable inputs with aging infrastructure. Construction and real estate players track heavy equipment across multiple sites while complying with BIM mandates. The breadth of vertical use cases underscores why the fixed asset management software market maintains double-digit expansion even as individual segments mature.

Geography Analysis

North America Fixed Asset Management Software Market

North America maintained a 36.88% revenue share in 2025, fueled by early enterprise adoption, federal compliance mandates, and robust partner ecosystems. United States agencies must operate JFMIP-aligned asset systems, embedding stable funding into annual budgets. Canada scales investment in energy and healthcare modernization, while Mexican maquiladora plants adopt SaaS asset suites to support export supply chains. Market maturity does temper growth, yet vendor competition intensifies around AI add-ons and subscription renewals.

APAC Fixed Asset Management Software Market

Asia-Pacific delivers the fastest trajectory at 12.05% CAGR through 2031, reflecting aggressive manufacturing upgrades, infrastructure build-outs, and SME cloud adoption across China, India, and ASEAN. Beijing’s Industry 4.0 incentives, New Delhi’s digital-SEZ expansion, and cross-border e-commerce logistics all demand unified asset visibility. Oracle’s localized language packs, multi-currency billing, and region-specific compliance templates accelerate rollouts. Japan and South Korea leverage advanced robotics integration, while Indonesia and Vietnam install fleet telematics to manage archipelagic logistics.

Europe Fixed Asset Management Software Market

Europe combines stable growth with differentiated demand drivers. The EU Corporate Sustainability Reporting Directive obligates more than 50,000 firms to disclose asset performance and climate impact, reinforcing software conversions. Germany’s Mittelstand manufacturers deploy AI maintenance to hedge energy costs, the United Kingdom expands NHS equipment tracking, and France integrates asset tools into nuclear and rail modernization. Data-sovereignty laws open space for regional cloud providers to challenge hyperscalers, framing compliance as a competitive advantage.

Competitive Landscape

The fixed asset management software market shows moderate fragmentation yet clear consolidation vectors. Enterprise heavyweights IBM, SAP, and Oracle leverage entrenched ERP installs to upsell integrated asset modules, reinforcing stickiness via single-vendor roadmaps. Siemens’ USD 1.6 billion pickup of Brightly Software in 2022 signaled entry by industrial automation giants eager to fuse operational technology with maintenance workflows. Hexagon’s 2025 acquisition of CAD Service bolsters 3D visualization, enabling augmented-reality maintenance guides in high-complexity environments.

IFS, AssetWorks, and Prometheus Group differentiate through industry-specific depth and rapid cloud innovation. IFS portrays itself as an AI-first industrial suite, evidenced by 46% cloud revenue growth in 2024. Prometheus Group’s six acquisitions since 2019 sharpen mobile EAM capabilities and Oracle integration. UpKeep, MaintainX, and Fleetio disrupt from below with mobile-first interfaces and subscription contracts that resonate with resource-tight SMEs. Patent filings proliferate around machine-learning anomaly detection and digital-twin syncing, while open APIs become decisive for ecosystem partnerships.

Strategic alliances expand platform scope. Fleetio’s 2024 partnership with Razor Tracking integrates agricultural telematics, courting heavy-equipment OEMs. GE Vernova collaborates with utilities to embed predictive modules into renewable assets. Insurance carriers pilot risk-based maintenance bundles with software vendors, offering premium discounts that reinforce a value chain spanning operations and finance. Competitive intensity nudges pricing toward tiered bundles rather than monolithic licenses, further democratizing access across enterprise sizes.

Fixed Asset Management Software Industry Leaders

Infor Inc.

IBM Corporation

SAP SE

FMIS Ltd.

Asset Panda, LLC

- *Disclaimer: Major Players sorted in no particular order

Fixed Asset Management Software Market Companies Covered in this Report

- IBM Corporation

- SAP SE

- Infor Inc.

- Oracle Corporation

- Hexagon AB (HxGN EAM)

- IFS AB

- AssetWorks LLC

- Asset Panda LLC

- FMIS Ltd.

- Ramco Systems

- UpKeep Technologies

- Sage Group plc

- MRI Software LLC

- Fiix Software

- Wasp Barcode Technologies (AssetCloud)

- Tracet (Adaequare Info Pvt Ltd.)

- RCS Technologies

- Mynd Integrated Solutions

- Osource Global

- EZ Web Enterprises

- InfoFort LLC

Recent Industry Developments in Fixed Asset Management Software Market

- March 2025: Houlihan Lokey’s Transportation Technology review highlighted renewed Mergers and Acquisitions in AI-centric asset platforms.

- February 2025: Oracle launched Database 23ai with SAP-optimized extensions, extending Database 19c support until 2032 and adding in-memory acceleration for large-scale asset queries.

- February 2025: ISG ranked SAP, IBM, and GE Vernova as leaders in its Power and Utilities Enterprise Asset Management guide.

- January 2025: Hexagon acquired CAD Service to integrate 3D modeling and augmented-reality visualization into its Enterprise Asset Management suite.

- November 2024: Prometheus Group closed the acquisition of Ventureforth, boosting its mobile-first EAM capabilities across Oracle environments.

Fixed Asset Management Software Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the fixed asset management software market as all packaged or cloud-native solutions that let organizations record, track, depreciate, and audit tangible fixed assets throughout their economic life, including related mobile apps and reporting modules. Hardware trackers, professional implementation, and managed support services are covered only when they are sold as part of the core software contract, which keeps the value chain comparable across geographies.

Scope exclusion: stand-alone RFID readers, generic enterprise resource planning suites, and facilities maintenance platforms are left out because they serve markedly wider purposes and would inflate the software-only baseline.

Segments Covered in This Report

- By Component

- Software

- Asset Tracking and Bar-coding Module

- Preventive and Predictive Maintenance Module

- Depreciation and Tax Management Module

- Risk and Compliance Module

- Services

- Professional and Implementation

- Managed Services

- Software

- By Deployment Model

- Cloud-based

- On-premise

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By Asset Class

- IT and Digital Assets

- Plant and Machinery

- Fleet and Mobile Equipment

- Real-Estate and Infrastructure

- By End-user Industry

- Industrial Manufacturing

- Transportation and Logistics

- Healthcare and Life Sciences

- Energy and Utilities

- Construction and Real Estate

- Government and Public Sector

- IT and Telecom

- Other Industries (Media, Education, BFSI, Retail)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- UAE

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed finance controllers, IT procurement heads, and asset-audit specialists across North America, Europe, and Asia-Pacific. Conversations explored average user seats per site, typical depreciation schedule configurations, and switching barriers, while short web surveys with software integrators validated upgrade cycles and cloud price points. These dialogues filled gaps left by public sources and confirmed early findings.

Desk Research

We first mapped the demand pool using public datasets from bodies such as the International Accounting Standards Board, the U.S. Bureau of Economic Analysis, Eurostat, and China's National Bureau of Statistics, which quantify asset intensity and capital-stock growth. Supplementary insight came from industry associations like the Construction Industry Institute and the Healthcare Financial Management Association, which publish asset turnover ratios, plus company 10-Ks and investor decks that disclose fixed-asset values and software budgets. Subscription databases including D&B Hoovers and Dow Jones Factiva helped cross-check vendor revenues and recent contract awards. These sources illustrate typical license fees, regional adoption curves, and regulatory triggers for digital record-keeping. The list is illustrative, not exhaustive, and many other outlets informed data checks and clarifications.

A second pass filtered press releases, patent filings retrieved through Questel, and customs shipment records from Volza to validate the pace at which barcode scanners and handheld terminals, key complements, are entering each region. This triangulation grounded our base-year penetration assumptions.

Market-Sizing & Forecasting

We began with a top-down reconstruction of the global fixed-asset software spend by applying modeled license penetration rates to the net fixed-asset stock maintained by enterprises in 29 countries, followed by selective bottom-up checks using vendor revenue breakouts and sampled average selling price times active-user calculations. Key variables include corporate capital-expenditure growth, the number of auditable assets per enterprise, cloud adoption share, median annual maintenance fee, and regional compliance deadlines. Forecasts through 2030 rely on multivariate regression blended with scenario analysis, where capital-spending outlooks, SaaS migration velocity, and tightening audit norms drive CAGR differentials. Gaps in vendor roll-ups, when encountered, were bridged using conservative midpoint estimates validated with senior interviewees.

Data Validation & Update Cycle

Before sign-off, every model passes variance checks versus historical software revenue series and peer adoption surveys; anomalies prompt re-contact of at least one source. Reports refresh yearly, with interim updates if material events, such as a major accounting rule change, shift baseline drivers. A final analyst review guarantees clients receive the most current view.

How Mordor Intelligence's Fixed Asset Management Software Market Size Compares to Other Published Estimates

Published estimates frequently diverge because firms pick different functional scopes, apply distinct ASP trajectories, and refresh at uneven intervals.

The largest gaps stem from whether hardware trackers and broad ERP modules are included, how aggressively cloud discounts are projected, and how currency conversions are timed. Mordor's disciplined scope, annual license price audit, and mid-year refresh keep our 2025 baseline tightly linked to observable spend, which rivals often miss when they model broader asset-management ecosystems or lean solely on historical vendor filings.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.82 B (2025) | Mordor Intelligence | |

| USD 8.14 B (2024) | Global Consultancy A | Bundles hardware readers and implementation fees, inflating value |

| USD 4.15 B (2024) | Research Firm B | Counts only SaaS subscriptions, excludes perpetual licenses |

The comparison shows that figures swing widely when scope or price curves shift. By centering on clearly defined software components, validating prices with users, and revisiting variables every twelve months, Mordor Intelligence offers a balanced, transparent baseline that decision-makers can replicate and trust.

Key Questions Answered in the Report

What is the current size of the fixed asset management software market?

The market is valued at USD 5.37 billion in 2026 and is projected to reach USD 9.18 billion by 2031 at an 11.32% CAGR.

Which region is growing the fastest for fixed asset management solutions?

Asia-Pacific leads growth with a 12.05% CAGR through 2031, driven by manufacturing expansion, regulatory adoption, and cloud-native deployments.

How quickly are cloud deployments expanding compared with on-premise systems?

Cloud solutions are increasing at a 13.26% CAGR, outpacing on-premise growth as enterprises prioritize scalability, AI readiness, and reduced capital expenditure.

Which industry holds the largest share of market spending?

Industrial manufacturing controls 21.72% of 2025 revenue, reflecting complex equipment portfolios and high downtime-avoidance priorities.

What are the key drivers behind market expansion?

Cost optimization, IoT-enabled real-time tracking, compliance mandates, cloud adoption, ESG reporting, and insurtech-linked maintenance models collectively bolster demand.

How do SMEs overcome high implementation costs?

Subscription-based SaaS pricing, government grants, and phased rollouts reduce upfront expenditure, enabling SMEs to access the same predictive capabilities as large enterprises.

Page last updated on: