Asia-Pacific Benefits Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

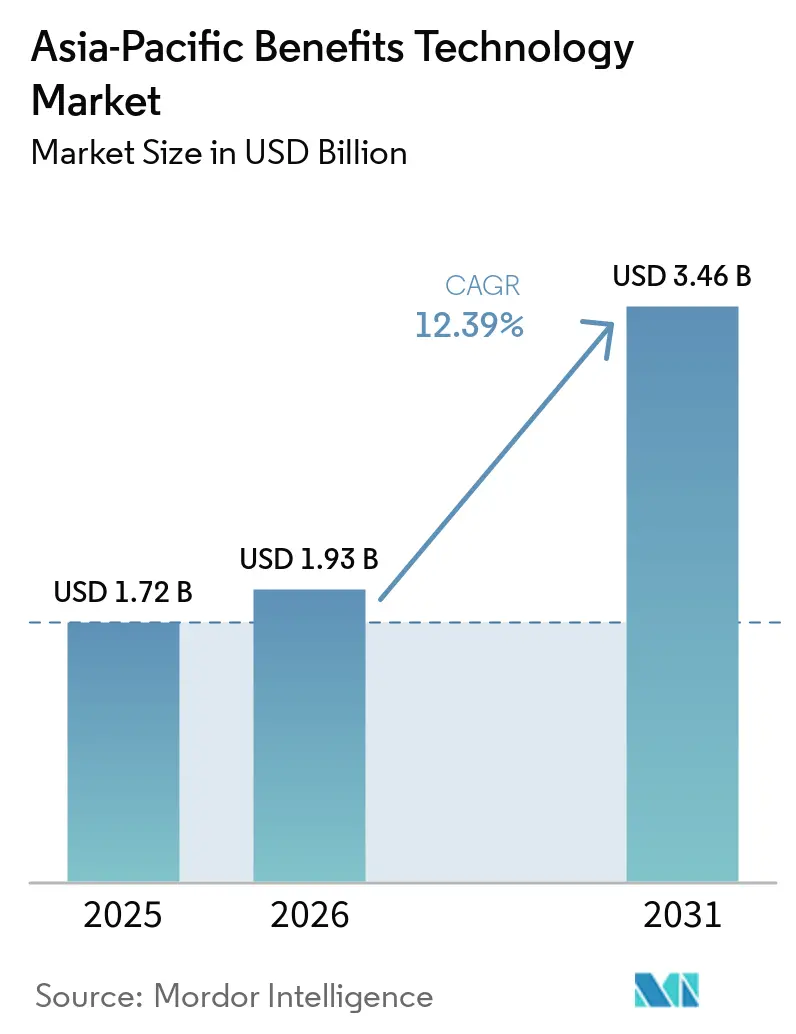

| Base Year Market Size (2025) | USD 1.72 Billion |

| Market Size (2026) | USD 1.93 Billion |

| Market Size (2031) | USD 3.46 Billion |

| Growth Rate (2026 - 2031) | 12.39% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Benefits Technology Market Analysis by Mordor Intelligence

The Asia-Pacific benefits technology market size is expected to grow from USD 1.72 billion in 2025 to USD 1.93 billion in 2026 and is forecast to reach USD 3.46 billion by 2031 at 12.39% CAGR over 2026-2031. The Asia-Pacific benefits technology market is expanding as employers across the region shift how they manage, deliver, and measure workforce benefits through digital systems that connect benefits, payroll, and compliance in a single environment. Many organizations in the region are moving directly to SaaS platforms rather than carrying legacy on-premises stacks forward, which makes the replacement cycle faster than in more mature Western HR technology environments. Demand is also rising because employers are under pressure to control healthcare costs, respond to a mobile-first workforce, and offer more personalized benefit choices without adding administrative burden. Budget priorities are shifting toward high-value programs, which is increasing interest in analytics-capable platforms that can show utilization patterns and support better benefit design decisions. The competitive setting remains moderately fragmented, and the clearest commercial openings are in cloud migration, payroll-benefit integration, flexible plan design, and services that can localize deployments across very different statutory systems.

Key Report Takeaways

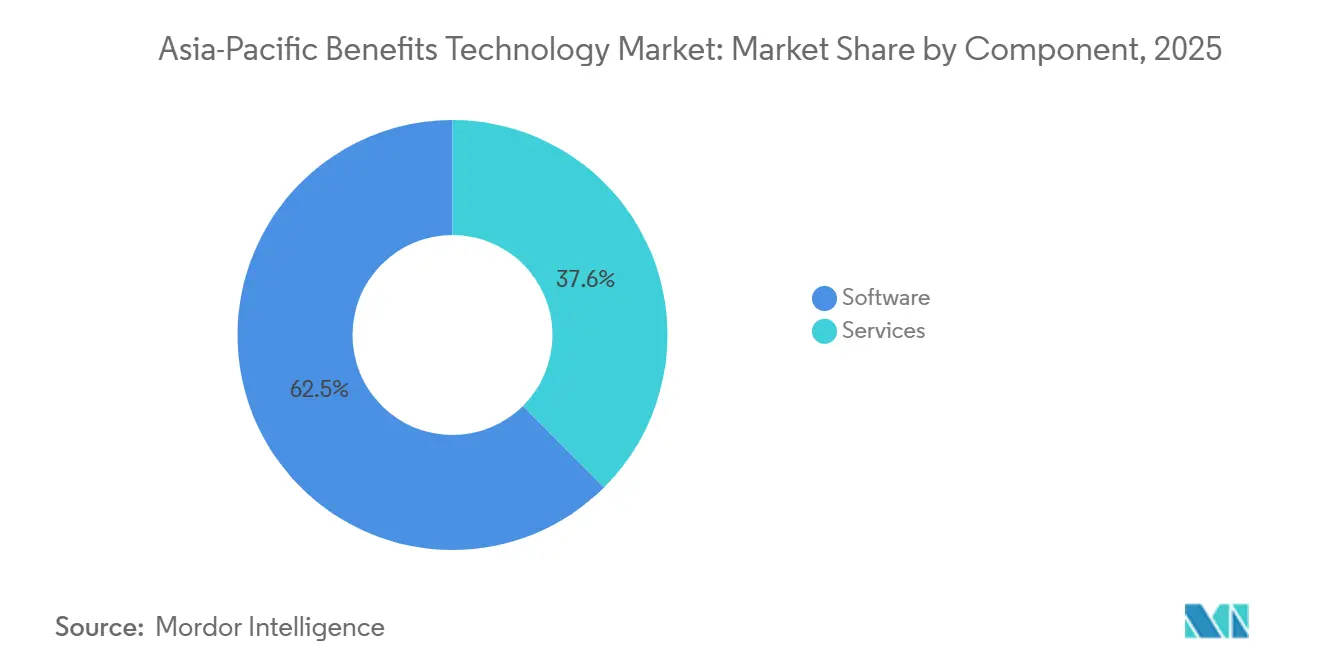

- By component, software held 62.45% share in the Asia-Pacific benefits technology market in 2025, while services are projected to expand at a 15.02% CAGR through 2031.

- By application, benefits administration accounted for 28.16% share in 2025, while flexible benefits and personalization platforms are projected to grow at a 14.28% CAGR through 2031.

- By deployment mode, on-premises held 58.12% share of the Asia-Pacific benefits technology market in 2025, while cloud-based deployment is projected to record the fastest growth at a 14.67% CAGR through 2031.

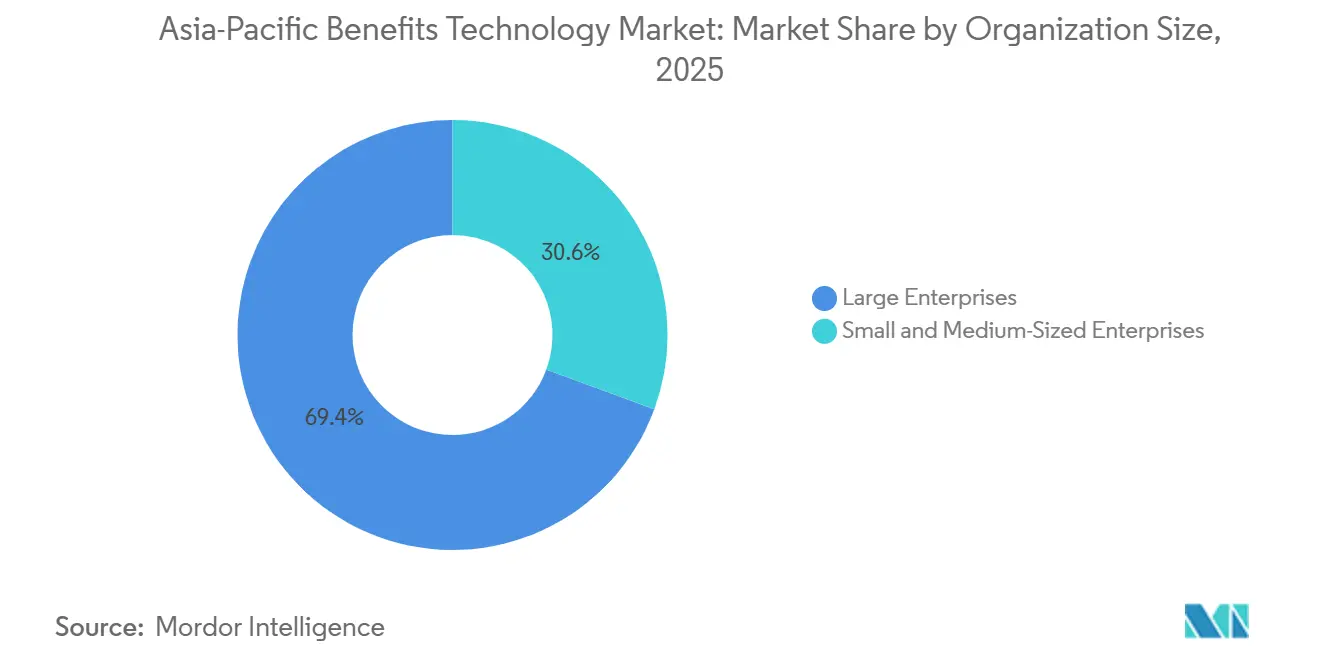

- By organization size, large enterprises held a 69.38% share of the Asia-Pacific benefits technology market in 2025, while SMEs are projected to grow at a 15.36% CAGR through 2031.

- By end-user industry, IT and telecommunications led with 31.29% share in 2025, while healthcare and life sciences are projected to expand at a 13.56% CAGR through 2031.

- By geography, China held 29.41% share in the Asia-Pacific benefits technology market in 2025, while India is projected to grow at a 13.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Benefits Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-Based HR and Benefits Stack Modernization | +3.2% | Global, with concentrated impact in China, Japan, and India | Medium term (2-4 years) |

| Automation of Enrollment, Compliance, and Payroll Connectivity | +2.8% | APAC core, Indonesia, Vietnam, Philippines, with spillover to India and Malaysia | Medium term (2-4 years) |

| Mobile-First Self-Service and Benefits Experience Demand | +2.3% | Southeast Asia, India, South Korea | Short term (≤ 2 years) |

| SME Adoption of Low-Cost SaaS Benefits Platforms | +1.9% | India, Southeast Asia, Australia and New Zealand | Medium term (2-4 years) |

| Medical Inflation-Led Benefits Cost Optimization | +1.2% | Global, with highest urgency in Malaysia, Indonesia, Philippines, Singapore | Short term (≤ 2 years) |

| Cross-Border Statutory Benefits Fragmentation Across Asia-Pacific | +0.8% | APAC core, concentrated in multinational employer corridors through Singapore, Hong Kong, and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-Based HR and Benefits Stack Modernization

Cloud migration has moved from a long-range plan to an operating need for many employers in the Asia-Pacific benefits technology market. Employers are trying to bring HR, payroll, and benefits functions onto unified systems that can support multi-country configurations without repeated custom builds. That shift matters because cloud platforms give benefit teams a single view of usage patterns, plan uptake, and administrative exceptions across different markets. The Asia-Pacific benefits technology market is also moving faster than older HR software cycles because many mobile-native workforces are accessing benefits digitally as their main channel rather than as a secondary desktop option. A clear example came when Sumitomo Metal Mining selected Works Human Intelligence's integrated COMPANY platform to unify around 7,000 group employees on a single HR foundation, replacing fragmented legacy arrangements.

Automation of Enrollment, Compliance, and Payroll Connectivity

Automation has become a major growth engine for the Asia-Pacific benefits technology market because statutory rules differ widely across the region and change on separate timelines. Employers often need one connected process for enrollment, eligibility, payroll calculation, and reporting, but many still run those tasks through disconnected systems or manual handoffs. That operating model becomes difficult when wage ceilings, contribution rules, and local filing requirements differ by country and are updated at different times of year. The Asia-Pacific benefits technology market is therefore seeing stronger demand for platforms that embed local statutory logic into the product, rather than leaving reconciliation work to internal teams. Ramco Systems highlighted that multi-country payroll operations and AI-supported verification are becoming more important as employers try to reduce manual effort and move toward connected payroll and benefits workflows.[1]Ramco Systems, “2025 APAC Payroll Recap Multi-Country Payroll and AI,” Ramco Systems, ramco.com The market is expected to continue evolving as organizations increasingly prioritize automation and efficiency in compliance.

Mobile-First Self-Service and Benefits Experience Demand

Employee expectations are pushing the Asia-Pacific benefits technology market toward mobile-first design, simpler self-service, and more personalized benefit selection. Large employers increasingly use technology to personalize benefits, and many APAC employers are also planning to deploy AI to support benefit choice and wellbeing delivery. The demand gap is clear: employee interest in personalized benefits remains much higher than actual access, creating room for platforms that guide choices and surface relevant options at the right time. In practical terms, that means the user experience is now part of the product value, not just a front-end feature. Japan's April 2026 expansion of the non-taxable meal subsidy allowance helped create immediate momentum for digital meal benefit cards and automated tax-processing integrations from platforms such as Benesmart and Miive.

SME Adoption of Low-Cost SaaS Benefits Platforms

SMEs are the fastest-growing segment in the Asia-Pacific benefits technology market because SaaS pricing has lowered the entry threshold for digital benefits administration. Low-cost platforms are making enrollment, configuration, and basic compliance functions available to companies that previously lacked the budget or internal support to deploy them. The commercial effect is larger than the price change alone because payroll connectivity and standardized compliance logic are now being packaged for businesses with very small employee counts. Employment Hero said its platform supported more than 350,000 businesses globally as of early 2026, while maintaining growth above 30%, underscoring the strong scale of the SME opportunity in this part of the market. As these platforms gain deeper sector presence, provider networks and workflow familiarity start to create switching costs that go beyond product features.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy and Cybersecurity Exposure in Health and Payroll Data | -2.4% | India, Vietnam, Indonesia, Philippines, high regulatory exposure markets | Medium term (2-4 years) |

| Legacy HRIS and Payroll Integration Complexity | -1.8% | Japan, China, South Korea, large-enterprise on-premises installed base | Long term (≥ 4 years) |

| Budget Rebalancing Delaying Net-New Module Purchases | -1.0% | Global, concentrated in Singapore, Hong Kong, Australia | Medium term (2-4 years) |

| Low Utilization Signal Quality in Wellbeing and Mental Health Benefits | -0.7% | APAC core, strongest signal in Japan and South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Privacy and Cybersecurity Exposure in Health and Payroll Data

Data privacy is a meaningful drag on the Asia-Pacific benefits technology market because health and payroll data move through systems that are often shared across employers, insurers, and payroll operators. The region does not operate under a single privacy framework, so vendors must adjust their data-handling, storage, notification, and transfer practices country by country. That raises the minimum product standard for encryption, access control, residency design, and audit readiness before a platform can scale across borders. Smaller SaaS vendors face a harder path because localization and security investment rise before revenue reaches regional scale. For multinational employers, the result is a slower buying cycle because privacy reviews now affect architectural decisions as much as contract terms.

Legacy HRIS and Payroll Integration Complexity

Integration complexity remains a structural restraint in the Asia-Pacific benefits technology market, especially among large employers with long-established HR and payroll estates. Many organizations still operate payroll on one system, core HR on another, benefits on a third, and finance on a fourth, with years of manual exports or custom connectors sitting between them. That makes migration harder because the challenge is not limited to replacing a user interface; it often requires rebuilding country-specific rules and event flows inside a new platform. The issue is especially visible in markets with deep on-premises customization, where statutory logic and year-end processing rules are tightly embedded in older systems. Even when the business case for replacement is strong, implementation risk can stretch decision cycles and delay full deployment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Emerge as the Critical Value Layer

Software held 62.45% of the Asia-Pacific benefits technology market share in 2025, indicating that platform licenses still accounted for the largest revenue base in the region. That leadership reflects the strong role of software-led delivery models for enrollment, compliance management, employee access, and payroll connectivity. At the same time, the commercial center of gravity is shifting as customers increasingly need platforms that can be implemented and localized without lengthy internal projects. The Asia-Pacific benefits technology market is now rewarding vendors that can pair software with deployment depth across languages, currencies, and statutory frameworks.

Services are projected to expand at a 15.02% CAGR through 2031, faster than the software component, underscoring the value now in implementation, integration, advisory, and support work. The shift does not reflect weak software demand; it reflects the fact that many employers already have product options and instead struggle with execution across multiple countries. That is why implementation and integration services have become a core demand driver for the Asia-Pacific benefits technology industry, especially where payroll and benefits data must be reconciled across separate systems. Regional changes to statutory rules have added urgency, as employers have had to update payroll-benefit logic rather than leave older links in place. Ramco Systems' work around multi-country payroll and AI-based verification reflects this broader service demand, where the product alone is not enough without strong integration capability.

By Application: Flexible Benefits Outpace Conventional Administration Models

Benefits administration accounted for 28.16% of the Asia-Pacific benefits technology market in 2025, making it the largest application layer. That position is logical because enrollment, eligibility checks, and carrier or provider connectivity remain the foundation for every employer deployment. Employers usually digitize those workflows before they move into more specialized modules. This gives the administration layer a broad installed base, even when employers are still early in wider benefits modernization.

Flexible benefits and personalization platforms are projected to grow at a 14.28% CAGR through 2031 as employers move away from one-size-fits-all programs and toward employee-choice models. The shift is being reinforced by rising demand for decision support, health navigation, and more targeted benefit communication. A 2025 Aon research study found that many employees in multinational firms would trade their current arrangements for greater personalization, which helps explain why choice architecture is moving to the center of platform roadmaps. The Asia-Pacific benefits technology market is also seeing convergence among benefits selection, wellbeing, and communication tools, which is why many vendors now bundle recognition and engagement functions rather than sell isolated modules. CDP Group's C-Benefits platform exemplifies this direction by combining commercial insurance, health management, flexible benefits, and recognition services for more than 1,000 enterprises and 800,000 employees in 2025.[2]CDP Group, “C-Benefits Platform,” CDP Group, cdpgroupltd.com The growing emphasis on personalization and integration is expected to drive further innovation in the benefits technology market.

By Deployment Mode: On-Premises Installed Base Declines as Cloud Migration Accelerates

On-premises accounted for 58.12% of the Asia-Pacific benefits technology market in 2025, reflecting the weight of long replacement cycles in China, Japan, and South Korea. Many large employers in those markets still operate customized HR environments with local statutory rules deeply embedded in their systems. That gives on-premises deployments significant staying power in the near term. It also means that the current share does not fully describe where new demand is moving.

Cloud-based deployment is projected to expand at a 14.67% CAGR through 2031 and is clearly the fastest-moving deployment model in the Asia-Pacific benefits technology market. The reason is not only lower infrastructure burden, but it is also the need for faster updates, easier scaling, and more consistent access across countries and devices. Hybrid models remain important in transition cases, especially where data sovereignty or internal control rules slow full migration. Even so, the direction of travel is clear because AI-supported payroll review, anomaly detection, and centralized analytics work best in cloud-hosted architectures. Ramco Systems noted that its anomaly and reasoning capabilities can compress payroll verification from a multi-day process into a short review window, which underlines why cloud migration is becoming a functional requirement rather than a hosting preference.

By Organization Size: SME Platforms Threaten Enterprise Incumbents at the Mid-Market

Large enterprises accounted for 69.38% of the Asia-Pacific benefits technology market in 2025, supported by larger contract values, broader module adoption, and the demands of multi-country benefit administration. Those employers still represent the most established customer base for full-suite vendors. They also carry more legacy complexity, which makes implementation-heavy engagements common. That combination kept large enterprises in the lead even as the buyer mix started to widen.

SMEs are projected to grow at a 15.36% CAGR through 2031, making them the fastest-growing organization-size segment in the Asia-Pacific benefits technology market. The core change is that compliance logic and payroll connectivity are now being delivered at a cost point that smaller firms can absorb. This is giving SME-focused vendors room to move upmarket into the mid-market, where customers need more sophistication but remain price-sensitive. Darwinbox is a strong example of that pattern because it offered a full HCM stack, including benefits capability, at a lower cost position and scaled to 4 million employees across 130 countries after its USD 140 million round in March 2025 and its additional USD 40 million investment in August 2025. The Asia-Pacific benefits technology industry is therefore facing a mid-market erosion risk for traditional incumbents, not only an SME expansion story.

By End-User Industry: Healthcare Demand Accelerates as Medical Costs Drive Benefits Re-Engineering

IT and telecommunications held a 31.29% share in 2025, making it the largest end-user vertical in the Asia-Pacific benefits technology market. The sector adopted digital HR and benefits tools earlier than many others, which helped it build a durable installed base. Large knowledge workforces and strong digital operating models also made the transition easier. That early lead explains why the sector remained the largest even as adoption spread into other industries.

Healthcare and life sciences are projected to grow at a 13.56% CAGR through 2031, driven by rising medical cost pressures, more complex data-handling needs, and stronger retention pressure on skilled employees. Medical inflation in APAC reached 14% gross in 2026, which created a strong urgency for employers to identify high-cost conditions, adjust plan design, and optimize benefit spending. Manufacturing is also becoming more relevant because factory-floor employees in Indonesia, Vietnam, and China increasingly access benefits through mobile-first interfaces rather than desktop systems. BFSI, retail, public sector, and education remain meaningful adopter groups, but their requirements increasingly center on compliance control, communication, and support for mixed workforce models. As a result, the Asia-Pacific benefits technology market is broadening beyond its early digital-heavy customer base and moving into sectors where workforce access, healthcare cost control, and regulatory oversight all matter simultaneously.

Geography Analysis

China held 29.41% of Asia-Pacific benefits technology market share in 2025, which made it the largest country market in the region. Its position rests on a deep corporate benefits ecosystem that links state-backed welfare structures, broker networks, and digital platforms with domestic workplace ecosystems such as WeChat Work and DingTalk. In China, benefit technology adoption is often tied to tax optimization and compliant welfare structuring, not only to employee experience goals. Japan is also an important market because aging demographics, workforce disclosure requirements, and broad digital transformation spending are encouraging employers to modernize benefit administration. Japan's April 2026 tax reform that lifted the non-taxable meal subsidy allowance to JPY 7,500 per month (USD 49) created immediate demand for platforms that could automate tax treatment inside benefit delivery.

India is projected to expand at a 13.91% CAGR through 2031, making it the fastest-growing geography in the Asia-Pacific benefits technology market. Growth there is being supported by SME digitization, stronger domestic insurtech participation, multinational expansion, and a rising compliance threshold for handling employee data. Plum Benefits Insurance Brokers said it covered around 600,000 employees across 6,000 organizations and raised INR 193 crore (USD 22.5 million) in March 2026 to scale AI-based claims operations and deepen HR and payroll integrations. Australia and New Zealand form a more mature but still attractive zone in the Asia-Pacific benefits technology market because enterprise digitization and compliance-led upgrades remain active, especially around payroll and superannuation workflows.

Southeast Asia is becoming one of the most dynamic subregions in the Asia-Pacific benefits technology market because many employers are skipping legacy infrastructure and deploying cloud-native systems directly. Compliance requirements remain difficult across Vietnam, Indonesia, the Philippines, and neighboring markets, which raises the value of software that can localize statutory logic and payroll connectivity. Singapore continues to serve as the region's main deployment hub because it combines regulatory maturity, vendor density, and access to cross-border employer demand. The rest of Asia-Pacific remains at an earlier stage, but mobile-first platforms with lightweight onboarding are well placed because they fit markets where desktop-heavy HR deployment models were never deeply established.

Competitive Landscape

The Asia-Pacific benefits technology market is moderately fragmented, with competition spanning global HCM suites, regional specialist vendors, domestic platform leaders, and insurtech-driven challengers. No single company holds a dominant regional position, and country-level share patterns vary because localization depth matters more than broad branding in many benefit workflows. That structure keeps pricing, service design, and integration capability at the center of competition. One clear strategic pattern is consolidation for scale, shown by Benefex Limited's February 2025 merger with Benify to form Benifex, which created a platform serving more than 3,000 organizations across 100 countries.[3]Benifex, “Benefex Plus Benify Equals Benifex, A New Era for Employee Experience,” Benifex, benifex.com Benifex extended that logic in May 2025 through a partnership with bswift to support connected benefits administration for employees outside the United States under a broader global delivery model.

The main white space sits in the mid-market segment across Southeast Asia, where firms with 300 to 2,000 employees are often priced out of full-suite platforms but need more compliance depth than lightweight SME tools can offer. A second gap persists in deskless and factory-floor use cases, where offline capabilities, low-bandwidth performance, and local-language support still lag real-world workforce conditions. A third gap is the analytics layer, because many employers still cannot clearly link benefits spend with retention, health outcomes, or workforce productivity. In that setting, the Asia-Pacific benefits technology market favors vendors that can turn operational workflows into measurable employer outcomes rather than only adding more front-end modules.

Strategic moves by growth vendors show how the market is being contested from several directions at once. Employment Hero pushed its compliance-led model further in 2026 and continued to scale after surpassing AUD 300 million in annual recurring revenue, equivalent to USD 189 million, which signaled that SME-focused HR platforms can build meaningful regional weight. Mednefits took a different route by building depth in Singapore and Malaysia, where its flexible benefits marketplace and network of more than 7,000 medical and wellness providers created defensible local relevance. The Asia-Pacific benefits technology market, therefore, remains open, but the winners are increasingly those that combine localization, deep integration, provider networks, and capital support rather than relying solely on a generic regional product story.

Asia-Pacific Benefits Technology Industry Leaders

Benefitfocus.com, Inc.

PlanSource Benefits Administration, Inc.

PeopleKeep, Inc.

ThrivePass, Inc.

Nayya Health, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: SmartHR, Japan's leading cloud HR software provider with 80,000-plus registered company tenants, and Finatext began co-developing a digital insurance marketplace inside SmartHR's "Money Portal" benefits service. The integration enables automatic employee data pre-filling from SmartHR and will launch with a pregnancy and childbirth insurance product in summer 2026, with plans to expand to life and non-life insurance, as well as personalized insurance recommendations by life stage.

- May 2026: Employment Hero launched HeroForce in Australia, New Zealand, and the United Kingdom, a co-employment model in which the company assumes legal employer status and uses AI to interpret complex award structures, automate payroll, and manage compliance obligations, targeting AUD 12.6 billion (USD 7.9 billion) in duplicated compliance expenditure across Australian SMEs.

- April 2026: MIXI, a Japanese technology company, launched its "MIXI Cafeteria Plan" powered by HQ's Cafeteria HQ platform, providing 240,000 points annually to 1,390 eligible employees, with 44% adoption within the first month.

- March 2026: Plum Benefits Insurance Brokers Pvt Ltd raised INR 193 crore (USD 22.5 million) in a Series B round led by Peak XV Partners, with Tanglin Venture Partners and GMO Venture Partners participating, to scale AI-driven claims operations, deepen HR and payroll integrations, and expand its healthcare stack to cover 10 million employees.

Asia-Pacific Benefits Technology Market Report Scope

The Asia-Pacific Benefits Technology Market encompasses software and service platforms that help manage and deliver a range of employee benefits, from health and insurance to retirement and wellness programs. By centralizing benefits administration and communication, these platforms cater to a distributed workforce. Growth in this market is fueled by a surge in the adoption of cloud-based HR tools and a heightened emphasis on enhancing the employee experience. Moreover, these solutions play a pivotal role in ensuring regulatory compliance and managing benefits across diverse regional markets.

The Asia-Pacific Benefits Technology Market Report is Segmented by Component (Software, and Services), Application (Benefits Administration, Compensation and Rewards Management, Employee Recognition and Engagement Platforms, Benefits Communication and Employee Portals, Flexible Benefits / Personalization Platforms, and Other Applications), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (Banking, Financial Services, and Insurance, IT and Telecommunications, Healthcare and Life Sciences, Manufacturing, Retail and E-Commerce, Public Sector and Education, and Other End-User Industries), and Geography (China, Japan, India, South Korea, Australia and New Zealand, Southeast Asia, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| Software | |

| Services | Implementation and Integration Services |

| Consulting and Advisory Services | |

| Support and Maintenance Services |

| Benefits Administration |

| Compensation and Rewards Management |

| Employee Recognition and Engagement Platforms |

| Benefits Communication and Employee Portals |

| Flexible Benefits / Personalization Platforms |

| Other Applications |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Banking, Financial Services, and Insurance |

| IT and Telecommunications |

| Healthcare and Life Sciences |

| Manufacturing |

| Retail and E-Commerce |

| Public Sector and Education |

| Other End-User Industries |

| China |

| Japan |

| India |

| South Korea |

| Australia and New Zealand |

| Southeast Asia |

| Rest of Asia-Pacific |

| By Component | Software | |

| Services | Implementation and Integration Services | |

| Consulting and Advisory Services | ||

| Support and Maintenance Services | ||

| By Application | Benefits Administration | |

| Compensation and Rewards Management | ||

| Employee Recognition and Engagement Platforms | ||

| Benefits Communication and Employee Portals | ||

| Flexible Benefits / Personalization Platforms | ||

| Other Applications | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By End-User Industry | Banking, Financial Services, and Insurance | |

| IT and Telecommunications | ||

| Healthcare and Life Sciences | ||

| Manufacturing | ||

| Retail and E-Commerce | ||

| Public Sector and Education | ||

| Other End-User Industries | ||

| By Geography | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

How large is the Asia-Pacific benefits technology market in 2026 and what is the 2031 outlook?

The Asia-Pacific benefits technology market was projected at USD 1.93 billion in 2026 and is forecast to reach USD 3.46 billion by 2031, growing at a 12.39% CAGR over 2026-2031.

Which application area is growing the fastest across the region?

Flexible benefits and personalization platforms are projected to grow the fastest, with a 14.28% CAGR through 2031, as employers move toward employee-choice models and digital decision support.

Why are SMEs becoming a more important customer group?

SMEs are projected to expand at a 15.36% CAGR because low-cost SaaS platforms now package enrollment, compliance, and payroll-linked benefits in formats that smaller firms can deploy more easily.

Which country leads regional demand and which one is expanding the fastest?

China held the largest share at 29.41% in 2025, while India is expected to grow the fastest at a 13.91% CAGR through 2031.

What is driving demand from healthcare and life sciences employers?

Healthcare and life sciences is forecast to grow at a 13.56% CAGR as employers respond to medical inflation, tighter data handling requirements, and stronger pressure to use benefits as a retention tool.

What is the main deployment shift taking place across employers?

On-premises still led with 58.12% share in 2025, but cloud deployment is projected to grow faster at a 14.67% CAGR because employers need quicker updates, stronger analytics, and easier scaling across countries.

Page last updated on: