Asia-Pacific Frontline Worker Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

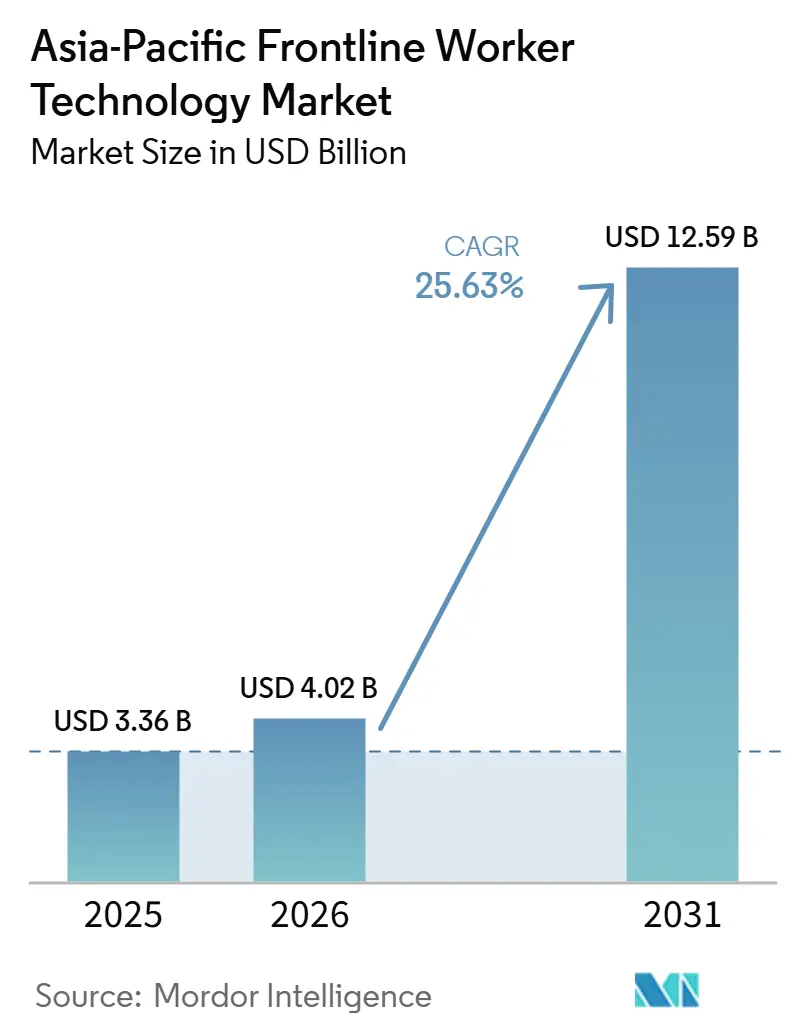

| Base Year Market Size (2025) | USD 3.36 Billion |

| Market Size (2026) | USD 4.02 Billion |

| Market Size (2031) | USD 12.59 Billion |

| Growth Rate (2026 - 2031) | 25.63% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Frontline Worker Technology Market Analysis by Mordor Intelligence

The Asia-Pacific frontline worker technology market size is expected to grow from USD 3.36 billion in 2025 to USD 4.02 billion in 2026 and is forecast to reach USD 12.59 billion by 2031 at 25.63% CAGR over 2026-2031. The Asia-Pacific frontline worker technology market is expanding as employers move frontline processes away from paper and fragmented tools toward connected mobile workflows that support daily execution at scale. Demand is also being reinforced by aging industrial workforces in Japan and South Korea, where companies need digital systems that help less-experienced workers complete tasks with greater consistency. Industrial connectivity is improving across the region, enabling real-time coordination, monitoring, and guided work in factories, logistics sites, and field locations. The Asia-Pacific frontline worker technology market is also benefiting from the shift toward cloud delivery, which reduces deployment friction for both large enterprises and smaller firms. Competitive activity is increasingly centered on software depth, AI-enabled guidance, and service capability, because buyers now expect platforms to support adoption, integration, and compliance rather than just communication.

Key Report Takeaways

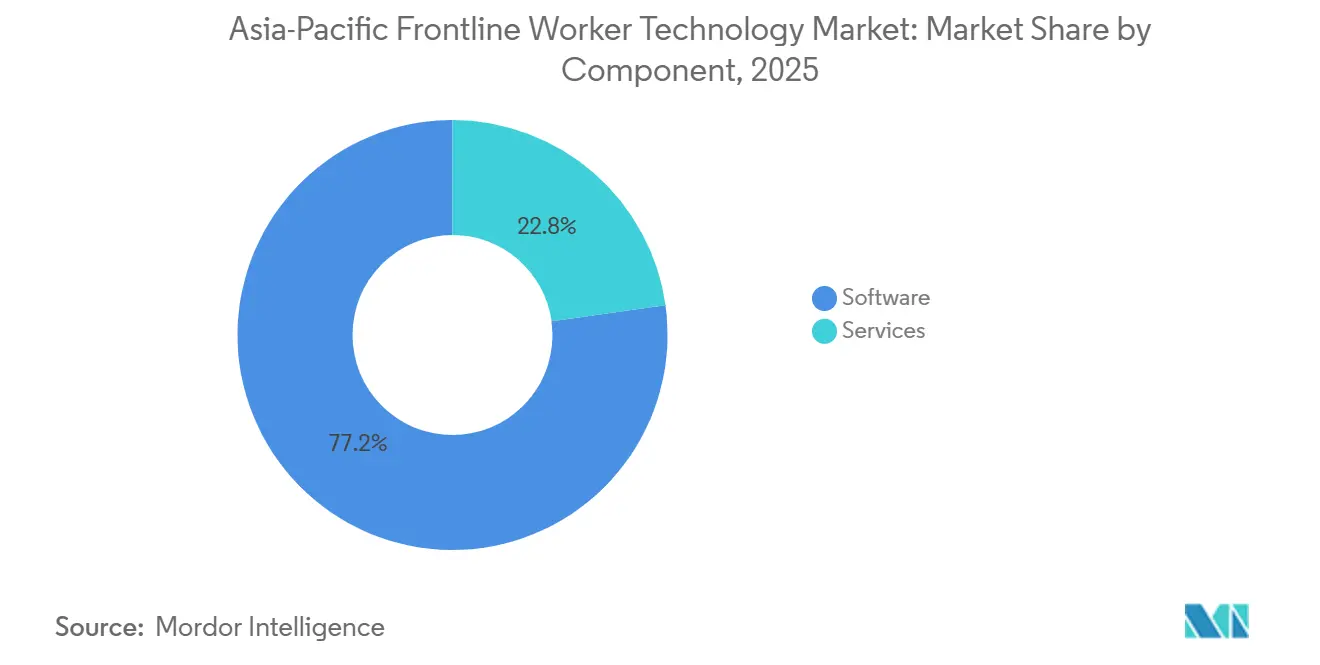

- By component, software held 77.21% of the Asia-Pacific frontline worker technology market revenue in 2025, while services are projected to expand at a 28.41% CAGR through 2031.

- By deployment, cloud-based deployment accounted for 70.23% of the Asia-Pacific frontline worker technology market revenue in 2025, and is projected to expand at a 28.05% CAGR through 2031.

- By organization size, large enterprises held 69.12% of the Asia-Pacific frontline worker technology market revenue in 2025, while small and medium enterprises are projected to expand at a 28.73% CAGR through 2031.

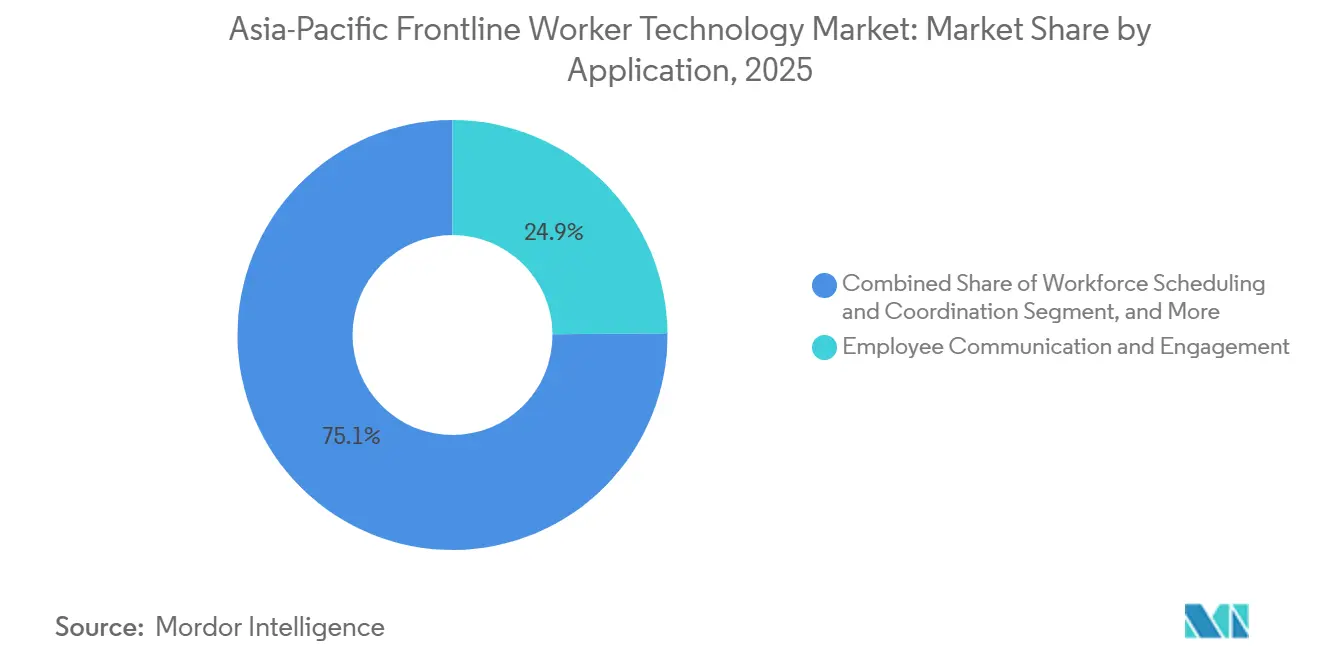

- By application, employee communication and engagement accounted for 24.87% share of the Asia-Pacific frontline worker technology market size in 2025, while workforce analytics and performance management are projected to expand at a 27.33% CAGR through 2031.

- By end-user industry, industrial manufacturing held 26.03% of revenue in 2025, while transportation and logistics is projected to expand at a 27.04% CAGR through 2031.

- By geography, China held 33.41% of the Asia-Pacific frontline worker technology market share in 2025, while India is projected to expand at a 27.69% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Frontline Worker Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Safety Documentation Requirements in Regulated Worksites | +5.2% | APAC core, concentrated impact in Japan, South Korea, Australia, and India | Short term (≤ 2 years) |

| Labor Shortages Increasing Reliance on Workflow Automation | +4.8% | Global, with acute pressure in Japan, South Korea, and Southeast Asia | Medium term (2-4 years) |

| Expansion of Private 5G and Industrial Connectivity at the Edge | +4.2% | China, Japan, South Korea, India, and Australia | Medium term (2-4 years) |

| Faster Adoption of AI-Enabled Task Routing and Coaching | +3.7% | Global, with early gains in China, India, and Southeast Asia | Short term (≤ 2 years) |

| Digital Traceability Demands Across Frontline Operations | +2.4% | China, Vietnam, Southeast Asia, and Australia | Medium term (2-4 years) |

| Workforce Retention Pressure in High-Turnover Service Industries | +1.8% | APAC core, concentrated impact in Southeast Asia, retail, and hospitality | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Safety Documentation Requirements in Regulated Worksites

Safety documentation is becoming a core operating requirement on regulated worksites across the region, driving the Asia-Pacific frontline worker technology market toward broader digital adoption. When compliance records must be timely, searchable, and easy to verify, paper-based frontline processes become harder to sustain. The same mobile interface used for safety checks can also support task handovers, checklists, and incident logging, extending technology use beyond a single compliance function. This dynamic raises demand for platforms that are easy to deploy across dispersed worker groups and multiple shifts. It also strengthens the case for integrated communication and workflow tools, because disconnected systems create avoidable gaps in reporting and accountability. Singapore’s workplace safety framework reflects this regulatory direction and reinforces the shift toward more structured frontline risk management workflows.

Labor Shortages Increasing Reliance on Workflow Automation

Persistent labor pressure is creating a durable growth base for the Asia-Pacific frontline worker technology market, especially in sectors that depend on shift-based and field-based labor. Companies are not only trying to reduce vacancies but also to make each available worker more productive during every shift. That is why demand is moving beyond simple scheduling tools and toward guided workflows, digital standard operating procedures, and AI-supported coaching. The value of these systems increases when experienced workers retire, because employers then need faster ways to transfer knowledge to newer staff. Hitachi’s July 2025 launch of its Frontline Coordinator, Naivy, shows how vendors are addressing this need by embedding expert guidance into operational workflows. As this pattern spreads, buyers are likely to place more value on platforms that help protect institutional knowledge than on tools that only manage attendance or messaging.

Expansion of Private 5G and Industrial Connectivity at the Edge

The expansion of private 5G is improving the operating conditions for the Asia-Pacific frontline worker technology market in environments where reliable wireless coverage was once difficult or costly. This matters because many frontline use cases require constant connectivity, low latency, and stable performance across large or physically complex sites. When those conditions improve, companies can support more connected devices, more real-time alerts, and more guided actions on the shop floor or in the field. NTT Group’s April 2026 announcement on remote operation and automated control at Japan’s Mizushima Industrial Complex shows how local 5G and advanced network architecture are being tested in demanding industrial settings.[1]NTT Group, “NTT Group and TAISEI CORPORATION Successfully Demonstrate Remote Operation and Automated Control of Multiple Pieces of Heavy Machinery Using the IOWN APN, Local 5G, and 60 GHz-Band Wireless LAN,” NTT Group, group.ntt As connectivity becomes more dependable, competition shifts away from hardware lock-in and toward software, analytics, and workflow intelligence. That change supports broader adoption because buyers can focus more on business outcomes and less on basic network feasibility.

Faster Adoption of AI-Enabled Task Routing and Coaching

AI is making the Asia-Pacific frontline worker technology market more relevant to daily operations by helping route tasks, interpret context, and reduce manual planning time. This shifts frontline systems from static communication layers to active execution tools. In manufacturing, CIMC’s AI routing project with the University of Hong Kong Centre for AI and Robotics in Manufacturing Operations showed that blueprint reading, workstation assignment, and schedule generation can be automated into a draft that still allows human validation. In office and field productivity, Microsoft’s June 2026 Work Trend Index pointed to a sharp rise in advanced AI use among Indonesian workers, which indicates that worker familiarity with AI is spreading faster in parts of Asia than many enterprise software cycles would suggest. As a result, buyers are more willing to test frontline platforms that offer contextual guidance, faster decision support, and simpler execution for less-experienced workers. The commercial effect is stronger for vendors that can embed AI into operational moments rather than treating it as a separate productivity feature.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy Concerns around Worker Monitoring | -2.8% | China (PIPL), Japan (APPI), Singapore (PDPA), India (DPDPA), South Korea (PIPA) | Medium term (2-4 years) |

| Integration Complexity With Legacy OT and ERP Systems | -2.1% | APAC core, concentrated in industrial hubs in China, Japan, and South Korea | Long term (≥ 4 years) |

| Uneven Device Durability in Harsh Industrial Environments | -1.0% | Southeast Asia, South Asia, and Australia | Medium term (2-4 years) |

| Budget Sensitivity Among Small and Medium Enterprises | -0.8% | Southeast Asia and India | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data Privacy Concerns around Worker Monitoring

Data privacy remains a meaningful brake on the Asia-Pacific frontline worker technology market because many frontline systems collect worker location, task behavior, communication activity, or device usage patterns. These tools can improve coordination, but they also raise questions around consent, retention, disclosure, and cross-border transfer. The challenge becomes harder for employers that operate across multiple APAC jurisdictions, as they often need different data-handling practices in different countries. That makes implementation more expensive for buyers without large compliance teams or mature governance processes. Vendors that offer built-in privacy controls, clear administrative settings, and flexible data policies are in a stronger position than those that compete solely on functionality. This restraint does not stop adoption, but it does lengthen review cycles and pushes buyers toward vendors that can reduce legal and operational uncertainty.

Integration Complexity with Legacy OT and ERP Systems

Integration with legacy OT and ERP systems continues to slow parts of the Asia-Pacific frontline worker technology market, especially in older industrial environments with mixed technology estates. Many large plants still rely on proprietary control systems, aging manufacturing execution systems, and long-standing on-premises ERP environments. Frontline platforms can deliver value quickly at the user level, but scaling that value across sites usually requires data links into scheduling, maintenance, inventory, and production systems. That adds cost, extends deployment schedules, and increases the need for technical services. The restraint is especially visible among large enterprises, because they have the budget to invest but also the heaviest system complexity to resolve. Vendors that bring pre-built connectors and practical integration support can convert this barrier into a competitive advantage within the Asia-Pacific frontline worker technology market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services are Accelerating as Implementation Complexity Grows

Software remained the largest component in 2025, with 77.21% of revenue, while services are projected to expand at a 28.41% CAGR through 2031. This mix shows that the Asia-Pacific frontline worker technology market still leans heavily toward platforms that manage communication, scheduling, analytics, and guided work at scale. Software benefits from strong repeatability across buyer groups, especially when vendors can deliver the same core product across manufacturing, logistics, healthcare, and service environments. Cloud delivery has also helped accelerate software adoption, enabling buyers to get started sooner and reducing the burden on local IT teams. As more companies move core frontline workflows onto digital platforms, software remains the anchor for user engagement, data capture, and process standardization.

Services are growing faster because implementation is becoming harder, not easier, as the market matures. Buyers increasingly expect localization, workflow redesign, worker training, integration support, and managed services that can help adoption continue after launch. In the Asia-Pacific frontline worker technology industry, those needs are intensified by language diversity, regulatory variation, and uneven digital maturity across sites. A platform may be technically ready on day 1, but performance gains often depend on how well the vendor aligns the tool with site-specific work routines. That creates a larger role for advisory and operational support inside total contract value. Over time, this should make services a more meaningful differentiator even when software remains the largest revenue pool.

By Deployment: Cloud-Based Delivery Reflects a more Practical Buying Model

Cloud-based deployment accounted for 70.23% of revenue in 2025, indicating that buyers have clearly favored lower-friction delivery models across the region. This lead reflects a practical decision by employers who want faster setup, lower upfront spending, and easier multi-site management. Cloud delivery also matches the needs of frontline use cases, because new locations, contractors, or seasonal labor can often be onboarded without major infrastructure work. In the Asia-Pacific frontline worker technology market, that advantage is especially relevant where companies operate across wide geographies and varied labor pools. The result is a buying pattern that rewards platforms with strong mobile usability and straightforward administration.

Hybrid and on-premises models still hold a place in the market because not every buyer can shift fully to the cloud. Industrial operators often have data control requirements, site connectivity limits, or legacy architectures that make a full migration less practical in the near term. Government-linked, utility, and heavy-industry users may also prefer tighter control over operational information. Even so, the share held by cloud-based delivery shows that the center of gravity has already shifted. Cloud deployments also shorten implementation timelines, which matters for mid-sized buyers that cannot support long enterprise rollouts. This balance suggests that cloud will remain dominant, while hybrid and on-premises options will remain relevant in more regulated or technically constrained environments.

By Organization Size: SME Adoption is Broadening the Customer Base

Large enterprises accounted for 69.12% of revenue in 2025, reflecting their larger budgets, higher frontline headcounts, and greater need for structured execution across multiple sites. These buyers have been the early anchor for the Asia-Pacific frontline worker technology market because they can fund complex rollouts and absorb longer decision cycles. They also gain more from central oversight, stronger compliance tracking, and standardized communication across distributed operations. Large organizations often have the deepest operational pain points, especially where staffing gaps, turnover, and process variation can hurt productivity. Their spending has helped establish the commercial base for enterprise-grade frontline platforms across the region.

Small and medium enterprises are projected to grow faster, at a 28.73% CAGR through 2031, and that changes the demand map in a meaningful way. Cloud-native vendors have reduced several barriers that once limited smaller buyers, including high setup costs, complex configuration, and reliance on internal IT teams. In the Asia-Pacific frontline worker technology market, this is especially important in Southeast Asia and India, where many frontline workers are employed by smaller firms in retail, food service, and logistics. Simpler onboarding and modular pricing allow these employers to adopt practical tools without committing to a full enterprise transformation. The SME opportunity also supports a more diverse vendor field, because smaller buyers often value speed, ease of use, and local relevance over large suite breadth. That is likely to keep market growth broad-based rather than concentrated only in enterprise accounts.

By Application: Communication Leads While Analytics Gains Strategic Weight

Employee communication and engagement accounted for 24.87% share of the Asia-Pacific frontline worker technology market size in 2025, making it the largest application area. This position makes sense because most employers begin by solving everyday coordination problems between managers and deskless staff. Communication tools are easier to justify early, since they improve message delivery, shift clarity, and workforce visibility without requiring a deep process redesign. They also create the user layer on which other applications can later be added. Once workers are active on one platform, companies can more easily expand into scheduling, learning, safety, and performance tracking. That makes communication not just the entry point, but also the foundation for wider platform retention.

Workforce analytics and performance management are projected to expand at a 27.33% CAGR through 2031, signaling a shift in what buyers want from frontline systems. Employers are no longer satisfied with visibility alone; they increasingly want tools that can interpret operational data and support action in real time. As more tasks, responses, and coaching moments are recorded digitally, analytics becomes more useful for identifying bottlenecks, coverage gaps, and recurring deviations. In the Asia-Pacific frontline worker technology industry, that shift raises the strategic value of applications that connect data capture to better execution. It also lifts the importance of AI features that can move from reporting to intervention. Over time, analytics is likely to become one of the clearest markers of platform maturity and pricing power.

By End-User Industry: Manufacturing Remains the Base While Logistics Expands Fast

Industrial manufacturing accounted for 26.03% of end-user revenue in 2025, making it the largest vertical in the market. This reflects the dense concentration of frontline labor across automotive, electronics, and process manufacturing operations in major APAC economies. Manufacturing buyers often have clear use cases for guided work, digital standard operating procedures, shift coordination, compliance capture, and issue escalation. They also tend to feel labor quality and productivity pressures quickly, which strengthens the business case for frontline tools. The segment’s lead, therefore, reflects both worker density and the practical need for better daily execution.

Transportation and logistics are projected to grow at a 27.04% CAGR through 2031, highlighting where operational urgency is building fastest. E-commerce growth, delivery pressure, warehouse throughput demands, and last-mile labor shortages are all increasing the need for better task orchestration. Frontline systems are useful in this vertical because they can shorten response times, improve dispatch clarity, and support more consistent handling of variable workloads. The same environment also raises interest in traceability, visibility into worker productivity, and simpler onboarding for new staff. Within the Asia-Pacific frontline worker technology market, logistics stands out as a segment where technology is becoming part of operational continuity rather than a discretionary upgrade. That supports sustained adoption even when budgets remain under scrutiny.

Geography Analysis

China held 33.41% of the Asia-Pacific frontline worker technology market share in 2025, making it the regional leader by revenue. The country’s position reflects the scale of its frontline manufacturing workforce and the continued push toward industrial digitalization across production environments. Demand is supported by the need to coordinate large labor pools more effectively while improving execution consistency across complex facilities. The rise of more technically skilled frontline roles in smart manufacturing also increases the need for training, guided work, and knowledge-enablement tools.

India is projected to expand at a 27.69% CAGR through 2031, making it the fastest-growing country market in the region. Growth is supported by manufacturing expansion, digital infrastructure investment, and a large, mobile-first workforce receptive to app-based workflows. The Asia-Pacific frontline worker technology market is also seeing strong growth in India, as onboarding, retention, and training needs remain high across logistics, commerce, and industrial operations. Southeast Asia adds another important layer of demand because retail, hospitality, logistics, and manufacturing together employ very large frontline populations across the subregion. High turnover in service sectors makes communication, scheduling, and training tools particularly relevant for employers that need faster workforce stabilization.

Japan remains a bellwether for advanced adoption because labor aging and skill transfer needs push companies toward guided work and embedded knowledge systems. Hitachi’s Naivy example shows how the focus is shifting toward helping less-experienced workers perform more effectively in operational settings.[2]Hitachi, “Hitachi Develops ‘Frontline Coordinator - Naivy’ as a Next-Generation AI Agent That Helps Alleviate the Psychological Burden on Frontline Workers and Enhance Work Efficiency,” Hitachi, hitachi.com South Korea combines industrial intensity with a growing need to sustain output through better workforce-support tools rather than relying solely on labor expansion. The rest of Asia-Pacific, including Australia, New Zealand, and selected emerging markets, contributes a mix of logistics, retail, port, and field-service demand, broadening the addressable base. Across these geographies, the Asia-Pacific frontline worker technology market follows a common pattern: employers want faster execution, better worker support, and more resilient operations, but they pursue those goals through different combinations of compliance, labor, and connectivity priorities.

Competitive Landscape

The Asia-Pacific frontline worker technology market has a two-layer competitive structure, with large global vendors at the top and specialist providers below, competing on use-case depth and regional fit. Microsoft, Honeywell International, and Zebra Technologies benefit from scale, broad product portfolios, and established enterprise relationships. Their advantage is strongest where buyers want integrated programs that combine software, devices, analytics, and support across many sites. This gives them a clear position in large industrial, logistics, and enterprise accounts where deployment complexity is high.

Competition is now moving beyond rugged hardware and basic workforce messaging toward workflow intelligence and AI-linked decision support. Zebra Technologies highlighted that shift in June 2026 when it introduced Zebra Nucleus and Workcloud Business Intelligence to connect frontline workflow management with real-time analytics. ServiceNow made a similar move in May 2026 with Autonomous Workforce and ServiceNow Otto, extending enterprise workflow automation into employee execution use cases. Honeywell also expanded its connected workforce offering in January 2026 with Performance+ for Guided Work, which supported multilingual frontline environments across warehousing, retail, and logistics.[3]Honeywell, “Honeywell Launches New Performance+ for Guided Work to Enable Faster, Smarter Supply Chain Operations,” Honeywell, honeywell.com These moves show that the market is rewarding vendors that can turn frontline data into guided action rather than just digitized observation.

Specialist providers remain important because many buyers need local language support, easier deployment, and focused functionality that large suites do not always deliver cleanly. WorkJam’s January 2026 release added offline task completion and strengthened compliance credentials, which directly addressed connectivity gaps and procurement scrutiny in regulated environments. LumApps also strengthened its frontline position after the Beekeeper combination, and in May 2026, it launched Beekeeper’s AI-Powered Frontline Intelligence platform to deepen analytics for frontline managers. This leaves room for continued competition around vertical specialization, ASEAN language support, and mobile-first operating models. The Asia-Pacific frontline worker technology market, therefore, remains led by scaled vendors at the top, but it is not closed to challengers that solve local execution problems better than broader platforms.

Asia-Pacific Frontline Worker Technology Industry Leaders

Zebra Technologies Corporation

Honeywell International Inc.

Microsoft Corporation

SAP SE

RealWear, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Zebra Technologies unveiled the Machine Vision Ecosystem at Automate 2026, including the CV70 high-performance machine vision camera, which integrates physical-world sensing with frontline workflow automation across manufacturing and supply chain operations. This extends Zebra's frontline AI portfolio into fixed industrial scanning, creating a broader hardware-to-software upsell pathway for industrial buyers.

- June 2026: Zebra Technologies launched Zebra Nucleus and Workcloud Business Intelligence (Workcloud BI) at its ZONE 2026 customer conference, embedding real-time data analytics directly into frontline task management and enabling IT leaders to convert operational data into immediate workforce decisions, marking Zebra's pivot from device-led to data-led platform competition.

- May 2026: ServiceNow launched Autonomous Workforce and ServiceNow Otto at Knowledge 2026, combining the Moveworks conversational AI acquisition with the Now Platform to deliver agentic, end-to-end workflow execution for frontline and enterprise employees; ISG's April 2026 APAC report had already identified ServiceNow as the primary platform APAC enterprises are using to build AI operational readiness, underlining the commercial significance of this release for the region.

- January 2026: Honeywell launched Performance+ for Guided Work, a voice-driven, connected workforce solution that combines Guided Work Solutions with advanced analytics across warehousing, retail, and logistics. The solution supports more than 48 languages using AI, directly addressing APAC's multilingual frontline workforce complexity across markets, including Japan, India, South Korea, and Australia.

Asia-Pacific Frontline Worker Technology Market Report Scope

The Asia-Pacific Frontline Worker Technology Market includes digital solutions and workforce enablement platforms that help frontline employees perform operational, customer-facing, and field-based activities across industries such as manufacturing, retail, healthcare, logistics, construction, hospitality, and government. These technologies support communication, workforce scheduling, task management, learning, safety compliance, and workforce analytics. Rapid digital transformation, expanding industrialization, increasing adoption of the mobile workforce, and rising demand for operational visibility and productivity improvements drive the market. The market enables organizations to connect frontline workers with enterprise systems and real-time operational data to enhance efficiency, safety, and workforce performance.

The Asia-Pacific Frontline Worker Technology Market Report is Segmented by Component (Software, and Services), Deployment (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Employee Communication and Engagement, Workforce Execution and Task Management, Workforce Scheduling and Coordination, Learning and Knowledge Enablement, Workforce Analytics and Performance Management, Safety and Compliance Management, and Other Applications), End-User Industry (Retail and E-Commerce, Industrial Manufacturing, Healthcare and Life Sciences, Transportation and Logistics, Hospitality, Construction, Government and Public Administration, and Other End-User Industries), and Geography (China, Japan, India, South Korea, Southeast Asia, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Employee Communication and Engagement |

| Workforce Execution and Task Management |

| Workforce Scheduling and Coordination |

| Learning and Knowledge Enablement |

| Workforce Analytics and Performance Management |

| Safety and Compliance Management |

| Other Applications |

| Retail and E-Commerce |

| Industrial Manufacturing |

| Healthcare and Life Sciences |

| Transportation and Logistics |

| Hospitality |

| Construction |

| Government and Public Administration |

| Other End-User Industries |

| China |

| Japan |

| India |

| South Korea |

| Southeast Asia |

| Rest of Asia-Pacific |

| By Component | Software |

| Services | |

| By Deployment | Cloud-Based |

| Hybrid | |

| On-Premises | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Employee Communication and Engagement |

| Workforce Execution and Task Management | |

| Workforce Scheduling and Coordination | |

| Learning and Knowledge Enablement | |

| Workforce Analytics and Performance Management | |

| Safety and Compliance Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Industrial Manufacturing | |

| Healthcare and Life Sciences | |

| Transportation and Logistics | |

| Hospitality | |

| Construction | |

| Government and Public Administration | |

| Other End-User Industries | |

| By Geography | China |

| Japan | |

| India | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current and forecast value of the Asia-Pacific frontline worker technology market?

The Asia-Pacific frontline worker technology market was valued at USD 3.36 billion in 2025, stands at USD 4.02 billion in 2026, and is forecast to reach USD 12.59 billion by 2031 at a 25.63% CAGR.

Which component leads revenue in frontline worker technology across Asia-Pacific?

Software led the market with 77.21% of revenue in 2025, while services are growing faster as buyers need integration, training, and deployment support.

Why is cloud-based deployment so important for frontline technology adoption?

Cloud-based deployment held 70.23% of revenue in 2025 because it allows faster rollout, lower upfront cost, and easier multi-site management for deskless workforces.

Which application area is growing fastest in frontline worker platforms?

Workforce analytics and performance management is projected to expand at a 27.33% CAGR through 2031, reflecting demand for real-time visibility and action from frontline data.

Which end-user sector is creating the strongest near-term opportunity?

Industrial manufacturing remained the largest end-user segment in 2025 with 26.03% share, while transportation and logistics is projected to grow fastest at a 27.04% CAGR.

Which country offers the strongest growth outlook in Asia-Pacific?

China led revenue with 33.41% share in 2025, but India is projected to post the fastest growth through 2031 with a 27.69% CAGR due to manufacturing and digital expansion.

Page last updated on: