Asia-Pacific Engineering Research And Development Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

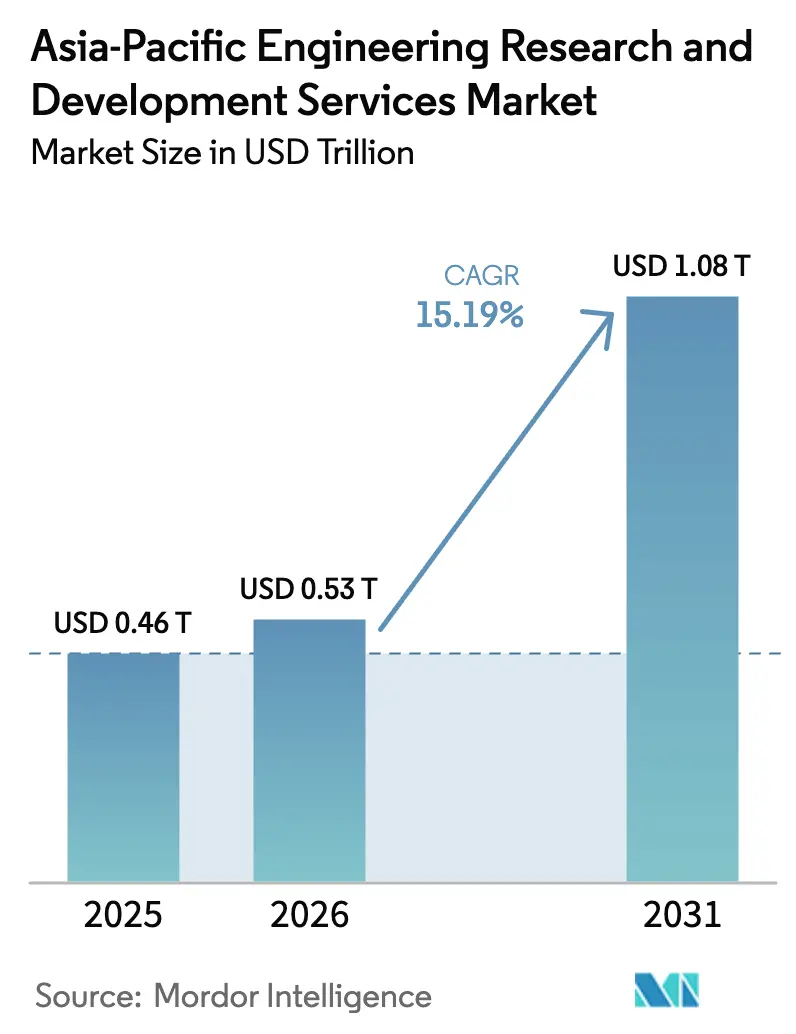

| Base Year Market Size (2025) | USD 0.46 Trillion |

| Market Size (2026) | USD 0.53 Trillion |

| Market Size (2031) | USD 1.08 Trillion |

| Growth Rate (2026 - 2031) | 15.19% CAGR |

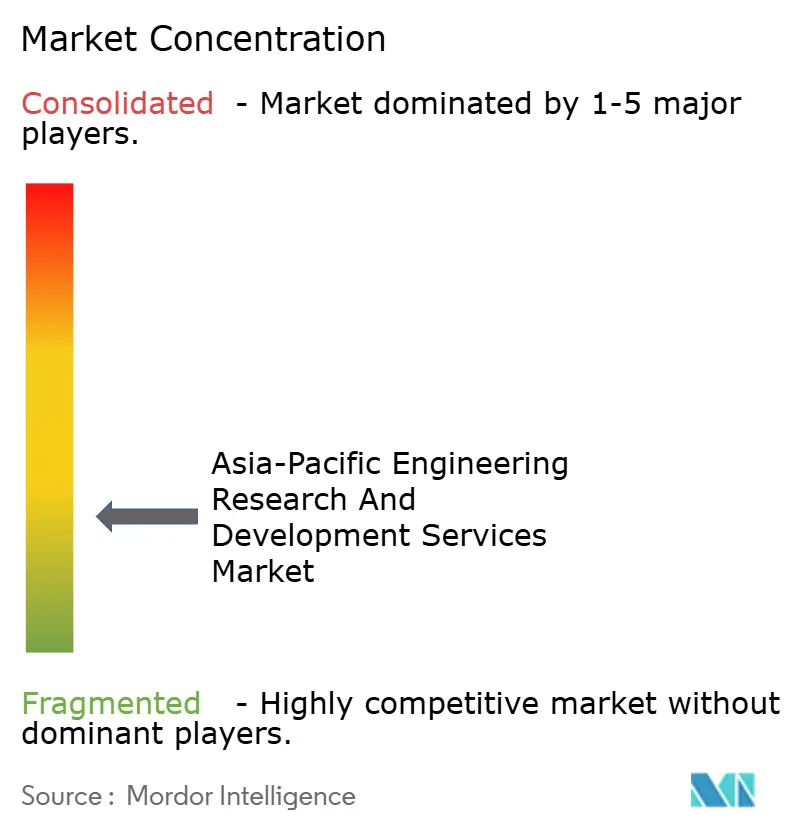

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Engineering Research And Development Services Market Analysis by Mordor Intelligence

The Asia-Pacific engineering research and development services market size is expected to grow from USD 462.96 billion in 2025 to USD 533.28 billion in 2026 and is forecast to reach USD 1,081.51 billion by 2031 at 15.19% CAGR over 2026-2031. Cost advantages of 50-70% versus Western peers, sovereign-AI mandates that keep inference engineering onshore, and government-funded 5G-6G test beds combine to pull core product-development cycles into the region. India remains the single largest revenue hub, while China and Japan diversify the vendor base with indigenous-innovation and Beyond-5G programs. Engineering service providers and global capability centers intensify competition for AI-ready talent, nudging both groups toward tier-2 city micro-hubs that lower attrition and real-estate costs. Heightened export-control scrutiny since 2025 is reinforcing a structural pivot toward in-house engineering models and hybrid delivery architectures.

Key Report Takeaways

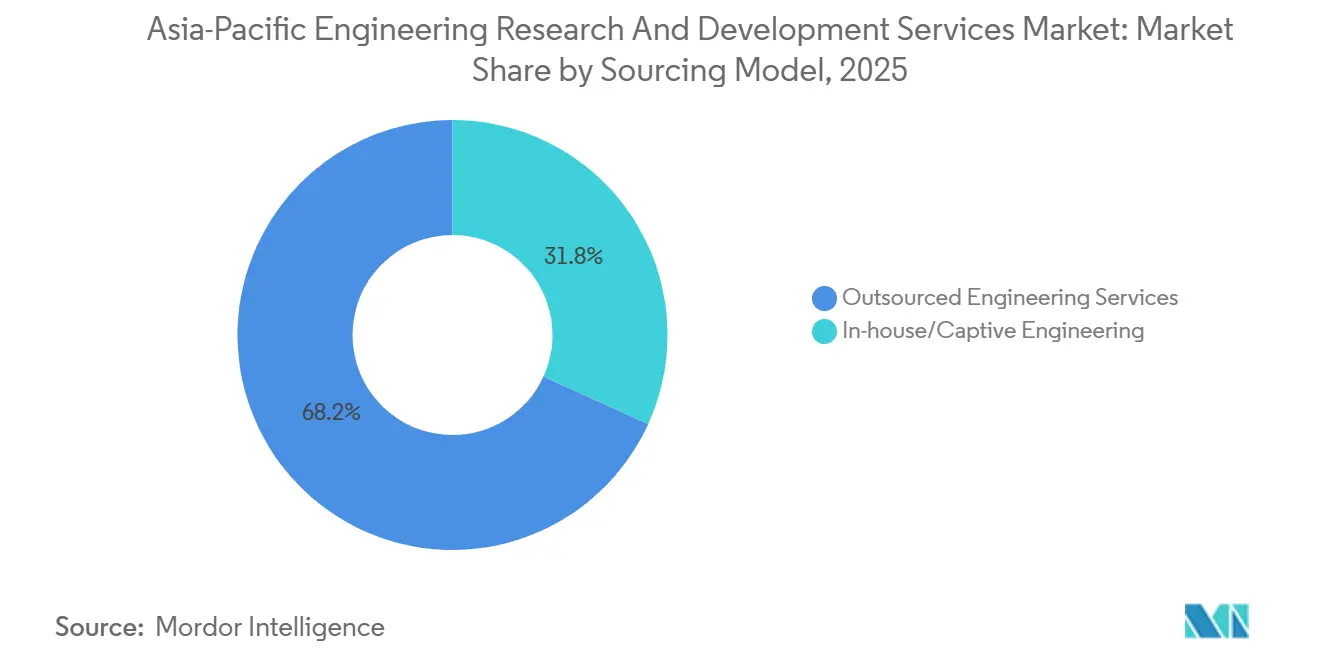

- By sourcing model, outsourced engineering held 68.21% of the Asia-Pacific engineering research and development services market share in 2025, while in-house captive engineering is projected to expand at a 15.53% CAGR through 2031.

- By service provider type, engineering service providers accounted for 54.12% of the Asia-Pacific engineering research and development services market in 2025, yet global capability centers recorded the fastest trajectory at a 15.59% CAGR to 2031.

- By industry vertical, automotive accounted for 22.19% of the Asia-Pacific engineering research and development services market revenue in 2025, whereas healthcare engineering is set to advance at a 17.12% CAGR through 2031.

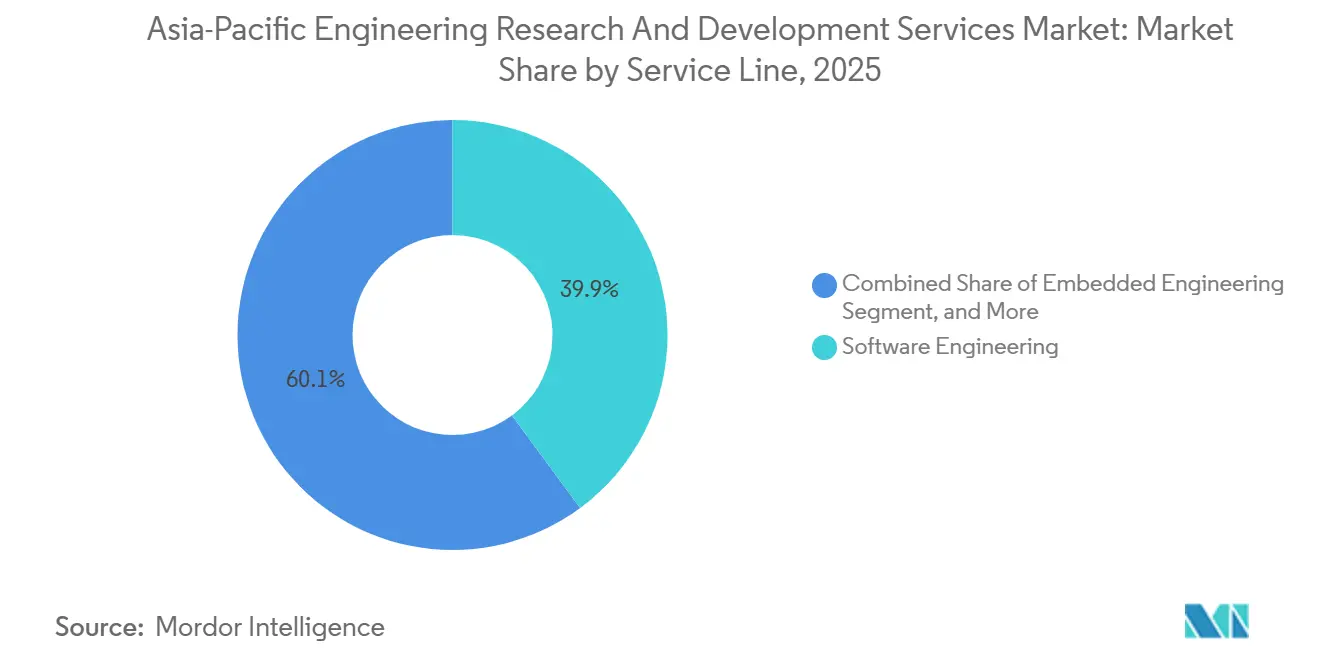

- By service line, software engineering accounted for 39.87% of the Asia-Pacific engineering research and development services market in 2025, and embedded engineering is poised for future growth at a 15.72% CAGR through 2031.

- By delivery model, offshore delivery captured 46.17% share of Asia-Pacific engineering research and development services market in 2025, although near-shore operations are poised for a 15.96% CAGR through 2031.

- By geography, India commanded 32.44% of Asia-Pacific engineering research and development services market share in 2025, while Indonesia is projected to register the fastest expansion among tracked nations at 16.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Engineering Research And Development Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to Digital-First Product Life-Cycles | +3.2% | Japan, South Korea, Singapore | Medium Term (2–4 Years) |

| Outsourcing-Friendly Cost Differentials in Asia-Pacific | +2.8% | India, Vietnam, Malaysia, Indonesia | Short Term (≤2 Years) |

| Accelerated Electric Vehicle and Autonomous Platform Programs | +3.5% | China, Japan, South Korea, India | Medium Term (2–4 Years) |

| Government-Funded 5G–6G Test-Beds | +2.1% | Japan, South Korea, China, Singapore | Long Term (≥4 Years) |

| Tier-2 City Micro-Hubs and Tax-Holiday Parks | +1.9% | India, Malaysia, Indonesia | Short Term (≤2 Years) |

| Generative-AI-Assisted Design-for-Manufacture | +2.4% | India, China, Japan | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Shift to Digital-First Product Life-Cycles

Digital twins, model-based systems engineering, and simulation-driven validation have slashed the number of physical-prototype loops and redirected workload to Asia-Pacific centers equipped with cloud-native product lifecycle management stacks. Japan’s 2025 Integrated Innovation Strategy earmarks more than USD 200 billion for HPC-enabled design.[1]EY, “India GCC Report 2024,” ey.com Firms adopting generative AI tooling report 25% shorter time-to-market but face skill shortages; only 1 in 5 self-identified AI professionals in India deploys models in production [2]Cabinet Office Japan, “Integrated Innovation Strategy 2025,” cao.go.jp. ISO 15288 and IEC 62443 certifications are, therefore, becoming table stakes for regional vendors that must demonstrate the secure handling of digital engineering threads.

Outsourcing-Friendly Cost Differentials in Asia-Pacific

Engineering wages in Vietnam equal roughly 30% of U.S. rates and 50% of Western European levels, preserving gross margins above 40% for projects shifted offshore.[3]A*STAR, “Research, Innovation and Enterprise 2025,” a-star.edu.sg Singapore-Vietnam delivery splits combine client-facing architecture in Singapore with volume execution in Ho Chi Minh City, leveraging Vietnam’s streamlined STEM work-permit regime. However, rising real estate and salary inflation in tier-1 Indian cities is fueling a drift toward second-tier hubs such as Coimbatore and Visakhapatnam, where operating expenses are 20-30% lower and local governments co-invest in plug-and-play campuses.

Accelerated Electric Vehicle and Autonomous Platform Programs

Shanghai’s Level 4 roadmap targets mass production by 2027, creating demand for sensor fusion, path-planning, and V2X stack validation. China granted Level 3 public-road approvals in 2025, intensifying spend on digital-twin test grounds that Asia-Pacific vendors monetize through outcome-based contracts pegged to miles-per-disengagement. Japan and South Korea channel hundreds of millions of U.S. dollars into 5G-connected intersections and HD-map upkeep, compressing vehicle platform cycles from 48 to 30 months as 800-volt systems and silicon-carbide inverters standardize. Compliance with UN ECE R155 cybersecurity and R156 software-update rules elevates demand for embedded engineering accredited to ISO 26262 and ASPICE Level 3.

Government-Funded 5G-6G Test-Beds

Regional telecom regulators bankroll terahertz, optical-wireless, and distributed-MIMO pilots that underpin envisioned 100 Gbps 6G networks by 2030. Subsidized test-beds give device makers pre-certified reference designs, truncating interoperability cycles but also imposing adherence to 3GPP Releases 18-19. Engineering centers in Bangalore, Shenzhen, Seoul, and Tokyo thus need deep RF and protocol-stack skill pools that remain scarce, extending onboarding timelines yet promising premium billing rates for certified talent.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Engineering-Talent Attrition | −1.8% | India, China, Malaysia | Short Term (≤2 Years) |

| IP-Protection and Export-Control Compliance Costs | −1.5% | Semiconductor and Aerospace Hubs | Medium Term (2–4 Years) |

| Rising Project-Based Billing Price Pressure | −1.2% | India, China, Malaysia | Short Term (≤2 Years) |

| Data-Localization Laws Limiting Code Transfer | −1.1% | China, India, Indonesia, Vietnam | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Persistent Engineering-Talent Attrition

Annual churn of 25–30% in semiconductor and embedded design roles erodes productivity and forces premium hiring bonuses. A 2024 EY survey showed that only 43% of engineers felt organizational belonging, signaling retention risk. Compensation inflation above 15% in tier-1 Indian cities narrows the cost gap versus Eastern Europe. Providers now allocate a growing share of operating budgets to reskilling academies and wellness initiatives, which depress short-term margins yet remain essential for sustaining delivery velocity in the Asia-Pacific engineering research and development services market.

IP-Protection and Export-Control Compliance Costs

Penalties for mishandling restricted design tools can exceed USD 100 million, as evidenced by a USD 140 million settlement in 2025 for unlicensed EDA transfers to China. New U.S. rules curtail sub-16 nm tools, advanced AI weights, and high-bandwidth memory, obligating Asia-Pacific centers to install technology-protection plans that add 3-5% overhead. Enhanced inspections in Singapore and Malaysia further delay shipments of semiconductor equipment, prolonging design timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sourcing Model: Captive Expansion Counters Compliance Risk

Outsourced services controlled 68.21% of Asia-Pacific engineering research and development services market share in 2025. Captive centers, however, are projected to clock a 15.53% growth pace as export rules tighten. Multinationals like Sanofi expanded Hyderabad headcount to 4,500 in 2026, centralizing clinical and regulatory workflows once spread across three continents. That shift cuts investigational new drug filing cycles by nearly one-fifth. Captives also dovetail with India’s GENESIS incentives, while allowing sensitive code to remain behind corporate firewalls, limiting third-party licensing friction.

Near-term, variable-cost flexibility keeps outsourcing relevant for platform migrations such as ICE-to-EV powertrain redesigns where providers spin up multidisciplinary squads inside 12 weeks. Yet data-localization in China and Indonesia is nudging hybrid models that reserve protected algorithms for in-house teams and farm out validation. Tax-holiday parks in Johor and Penang amplify the appeal of owned facilities by dropping corporate levies to 5% and personal taxes to 15% for knowledge staff.

By Service Provider Type: GCC Velocity Surpasses ESP Scale

Engineering service providers held 54.12% of Asia-Pacific engineering research and development services market size in 2025, but global capability centers are accelerating faster at a 15.59% CAGR. India hosts more than 1,700 GCCs generating USD 64.6 billion in fiscal 2024, and that figure could surpass USD 105 billion by 2030 as firms chase ISO 13485 and AS9100 compliance. GCC internal control of intellectual property also eases navigation of new export-control layers.

Despite the swing, scale advantages keep large ESPs center-stage for mega deals. L&T Technology Services landed a USD 100 million semiconductor program in 2025, evidencing provider agility. Private-equity interest remains strong, as a USD 4.5 billion Hillhouse stake in Quest Global showed in 2026. Still, both GCCs and ESPs confront a ferocious talent war that inflates wage premiums in second-tier cities once tapped for cost savings.

By Industry Vertical: Healthcare Emerges as High-Velocity Niche

Automotive generated 22.19% of the Asia-Pacific engineering research and development services market revenue in 2025, powered by demand for consolidated domain controllers and Level 4 autonomy pilots. Yet healthcare engineering outpaces every vertical with a 17.12% CAGR, as medical-device firms seek ISO 13485-compliant prototyping hubs that can juggle FDA, EU MDR, and China NMPA dossiers in parallel. South Korean startups such as KAIROS Medtech leverage triple-market alignment to shave 12-18 months off launch windows.

Industrial and semiconductor programs also expand, driven by Industry 4.0 retrofits and India’s design-linked incentive push to build a USD 103 billion local chip market by 2030. Aerospace engagement is capped by tightened ITAR and BIS controls, but Australia’s new USD 330 million fund is lifting regional unmanned-system engineering. Consumer electronics continues its drift toward Vietnam and Malaysia as diversified supply footprints take hold.

By Service Line: Embedded Engineering Narrows Gap With Software

Software engineering represented 39.87% share in 2025, mirroring cloud migration of embedded stacks and microservices adoption. The embedded segment, however, is catching up fast, forecast at a 15.72% CAGR as EV platforms collapse 100 ECUs into sub-10 compute modules. Providers must straddle AUTOSAR Classic for deterministic tasks and AUTOSAR Adaptive for high-bandwidth domains, maintaining dual toolchains and safety cases.

Mechanical and electrical niches gain a lift from generative-AI tools that shave 25% off design-cycle time and cut component mass 15-20% through topology optimization. L&T Technology Services’ Altair Digital Twin hub couples multiphysics simulation with real-time field telemetry, cutting physical prototypes by up to 40%. Demand for DevSecOps pipelines integrating static and dynamic security scans is expanding across both software and embedded workstreams.

By Delivery Model: Near-Shore Uptick Reflects Data Sovereignty

Offshore delivery held a 46.17% share in 2025, but near-shore configuration is racing ahead at a 15.96% CAGR as China, India, and Vietnam enact data-localization statutes with multimillion-dollar penalty teeth. Corporations answer by cloning engineering pods inside each jurisdiction to keep “important industrial data” onshore, while shipping regression testing to lower-cost offshore sites. Johor-Singapore SEZ exemplifies the model, with weekly cross-border reviews replacing long-haul travel and slashing associated expense by 60%.

Onshore teams remain relevant for safety-critical aerospace and medical firmware that regulators require to be co-developed with client engineers. Hybrid splits now partition source code by sensitivity level, holding machine-learning training loops in captive repositories and assigning documentation or UI work to providers in Vietnam or Malaysia. The arrangement cushions attrition while respecting national security clauses embedded in the latest export-control guidance.

Geography Analysis

India captured 32.44% of the Asia-Pacific engineering research and development services market share in 2025, supported by more than 1,700 global capability centers that employed 1.9 million engineers and generated USD 64.6 billion in fiscal 2024. Engineering and R&D centers are scaling 1.3 times faster than the broader GCC landscape as firms pursue ISO 26262 and ASPICE Level 3 credentials. Government programs deepen this momentum, with the GENESIS scheme offering single-window permits and the India Semiconductor Mission earmarking INR 1,000 crore (USD 120 million) in design-linked incentives that underpin a USD 103 billion chip-revenue goal for 2030. Tier-2 cities such as Coimbatore, Visakhapatnam, and Jaipur run 20-30% below metro operating costs, cutting attrition below 15% and broadening the talent funnel. Data-localization rules issued by the Reserve Bank of India and sector regulators force providers to add in-country infrastructure for finance and healthcare clients, lifting capital budgets by as much as 15%.

Indonesia is projected to grow at a 16.92% CAGR to 2031, the region’s quickest pace, as the National Innovation System targets R&D spending equal to 2% of GDP and the Batam Free Trade Zone grants 10-year zero corporate tax holidays. Regulation 71 compels public-sector data to stay onshore, prompting multinationals to locate engineering hubs in Jakarta and Surabaya, where universities now graduate about 150,000 STEM students each year. Decree 219/2025 trims foreign work-permit processing to seven business days, enabling hybrid delivery models that pair local execution with Singapore-based architecture support. Neighboring Malaysia leverages a 5% corporate tax and 15% personal tax in the Johor-Singapore Special Economic Zone, luring Infineon’s planned USD 7 billion silicon-carbide fab and a 500-acre Penang engineering park focused on semiconductor, aerospace, and MedTech tenants. Singapore complements this corridor with a SGD 1 billion (USD 740 million) advanced-manufacturing fund that sits alongside its SGD 25 billion RIE 2025 program for deep-tech ventures.

China channels USD 47.5 billion through the Big Fund III to chase semiconductor self-reliance, yet U.S. export controls on sub-16 nm tools push local firms toward alternative design flows. Shanghai’s Level 4 autonomous-vehicle roadmap aims for mass production by 2027 and six million annual passenger trips, intensifying demand for sensor-fusion and digital-twin testing. Cybersecurity Law amendments that take effect in 2026 levy fines up to RMB 10 million (USD 1.4 million) for unauthorized cross-border data transfers, steering foreign OEMs toward in-country engineering mirrors. Japan invests JPY 30 trillion (USD 207 billion) under its Integrated Innovation Strategy and saw Rapidus unveil a 2 nm prototype in early 2026, reinforcing a Beyond-5G and quantum-computing roadmap. South Korea commits more than USD 670 million to 6G cores and autonomous-mobility infrastructure, while Australia’s USD 330 million Advanced Manufacturing Fund seeds Adelaide-based aerospace and space-launch programs that require AS9100-aligned engineering talent.

Competitive Landscape

Market power is diffused; the top 10 providers capture only about 35-40% of regional revenue, reflecting vertical-specific certification hurdles that limit cross-sector economies of scale. Engineering service providers such as L&T Technology Services, Tata Technologies, and Quest Global increasingly push outcome-based deals tied to defect density or miles per disengagement, shifting execution risk onto vendor balance sheets. GCCs run by Sanofi, Bosch, and Siemens internalize design IP to sidestep licensing headaches and export-control risk, yet must swallow sustained hiring premiums as AI-competent talent scarcity worsens.

Second-tier city clusters such as Penang and Visakhapatnam help smaller challengers undercut large incumbents while maintaining ASPICE Level 3 and ISO 26262 ASIL-D maturity. Generative-AI design assistants surface as a disruptive equalizer; L&T Technology Services’ FusionWorld.ai cuts mechanical cycle time by a quarter, opening doors to fixed-bid arrangements previously deemed too risky. Strategic moves in the past 18 months range from Tata Technologies’ USD 85 million ES-Tec acquisition to Quest Global’s USD 4.5 billion valuation financing, underscoring investor appetite for scalable IP portfolios within the Asia-Pacific engineering research and development services market.

Hyperscalers and telecom vendors are emerging as influential ecosystem partners, wiring service providers into co-innovation alliances that bundle cloud credits, AI accelerators, and 5G test-bed access. Wipro’s Siemens-powered Xcelerator labs offer integrated PLM, digital twin, and edge analytics packages for automotive and industrial clients, while Tech Mahindra’s Qualcomm Open RAN program embeds AI-driven network optimization modules that reduce latency below 10 milliseconds for factory-automation workloads. These alliances deepen vertical specialization and raise switching costs, yet they also bind participants to multiyear roadmap synchronizations that can strain smaller vendors’ capital budgets when hyperscaler standards pivot.

Asia-Pacific Engineering Research And Development Services Industry Leaders

L&T Technology Services Limited

Tata Technologies Limited

QuEST Global Services Pte. Ltd.

Wipro Limited

Tech Mahindra Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Sanofi expanded its Hyderabad GCC to 4,500 employees, consolidating global R&D and trimming investigational new drug submission cycles by 18%.

- February 2025: Quest Global secured minority investment from Hillhouse at a USD 4.5 billion valuation, reinforcing capital availability for ESP scale-ups.

- February 2026: Australia launched a USD 330 million Advanced Manufacturing Fund to nurture domestic unmanned-system engineering and space-launch capacity.

- January 2026: L&T Technology Services signed a multi-year R&D pact with a global OEM for 800-volt EV platforms compliant with UN ECE R155 and R156.

Asia-Pacific Engineering Research And Development Services Market Report Scope

The Asia-Pacific Engineering Research and Development Services Market Report is Segmented by Sourcing Model (In-house/Captive Engineering, Outsourced Engineering Services), Service Provider Type (Global Capability Centres, Engineering Service Providers), Industry Vertical (Automotive, Industrial, Aerospace and Defence, Consumer Electronics, Semiconductor, BFSI, Retail, Healthcare, IT and Telecom, Rest of Industry Verticals), Service Line (Mechanical and Electrical Engineering, Embedded Engineering, Software Engineering), Delivery Model (Onshore, Offshore, Near-shore, Hybrid), and Geography (China, India, Japan, South Korea, Australia, Singapore, Malaysia, Indonesia, Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| In-house/Captive Engineering |

| Outsourced Engineering Services |

| Global Capability Centres (GCCs) |

| Engineering Service Providers (ESPs) |

| Automotive |

| Industrial |

| Aerospace and Defence |

| Consumer Electronics |

| Semiconductor |

| BFSI |

| Retail |

| Healthcare |

| IT and Telecom |

| Rest of Industry Verticals |

| Mechanical and Electrical Engineering |

| Embedded Engineering |

| Software Engineering |

| Onshore |

| Offshore |

| Near-shore |

| Hybrid |

| China |

| India |

| Japan |

| South Korea |

| Australia |

| Singapore |

| Malaysia |

| Indonesia |

| Rest of Asia-Pacific |

| By Sourcing Model | In-house/Captive Engineering |

| Outsourced Engineering Services | |

| By Service Provider Type | Global Capability Centres (GCCs) |

| Engineering Service Providers (ESPs) | |

| By Industry Vertical | Automotive |

| Industrial | |

| Aerospace and Defence | |

| Consumer Electronics | |

| Semiconductor | |

| BFSI | |

| Retail | |

| Healthcare | |

| IT and Telecom | |

| Rest of Industry Verticals | |

| By Service Line | Mechanical and Electrical Engineering |

| Embedded Engineering | |

| Software Engineering | |

| By Delivery Model | Onshore |

| Offshore | |

| Near-shore | |

| Hybrid | |

| By Country | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Singapore | |

| Malaysia | |

| Indonesia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How fast is spending on ER&D services in Asia-Pacific expanding?

Regional spend is forecast to climb from USD 533.28 billion in 2026 to USD 1,081.51 billion by 2031, reflecting a 15.19% CAGR.

Which country commands the largest share of Asia-Pacific ER&D revenue?

India holds the lead with 32.44% of regional revenue, sustained by more than 1,700 global capability centers and expansive STEM talent pools.

What vertical offers the quickest growth opportunity?

Healthcare engineering is projected to advance at 17.12% a year to 2031, outpacing automotive and semiconductor workstreams.

Why are captives gaining on traditional outsourcing?

Stricter export-control rules and data-localization laws push multinationals to internalize IP within owned global capability centers that meet compliance mandates.

How are data-sovereignty rules reshaping delivery models?

New localization laws in China, India, and Vietnam spur near-shore and onshore setups that keep sensitive code inside national borders while routing test and UI work offshore.

What technological trend most influences engineering workloads?

The move toward digital-first product life-cycles using digital twins and generative-AI design tools is compressing development schedules and reallocating spend to high-compute Asia-Pacific hubs.

Page last updated on: