Asia-Pacific Enterprise Resource Planning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

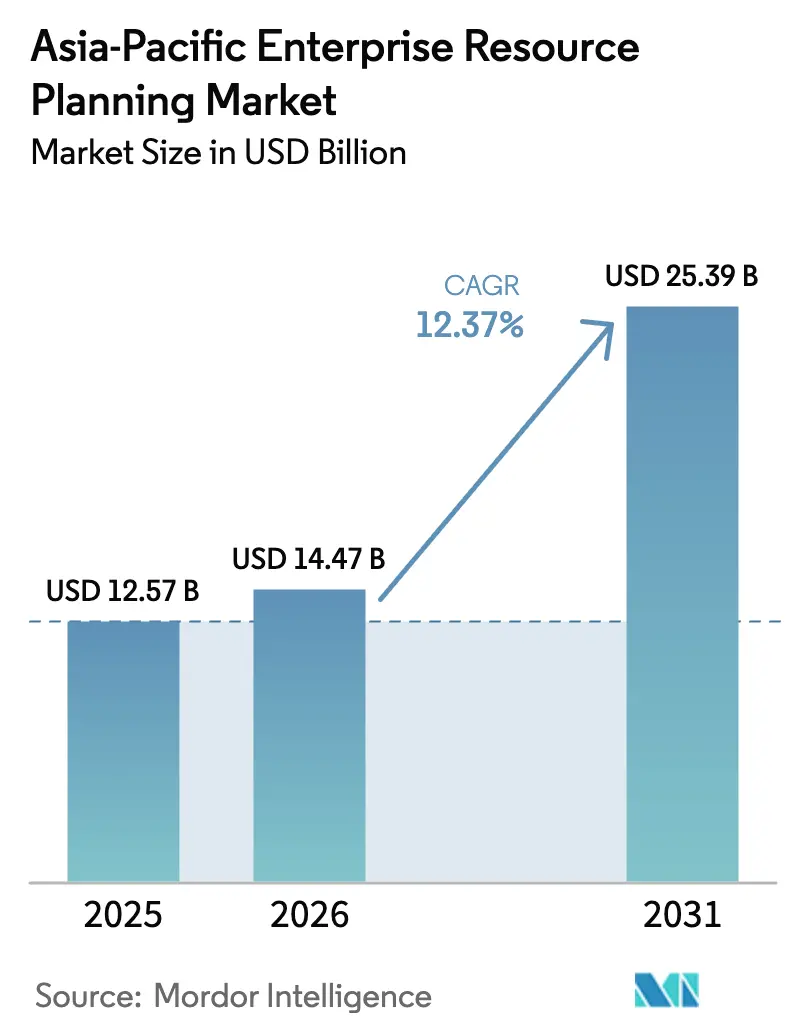

| Base Year Market Size (2025) | USD 12.57 Billion |

| Market Size (2026) | USD 14.47 Billion |

| Market Size (2031) | USD 25.39 Billion |

| Growth Rate (2026 - 2031) | 12.37% CAGR |

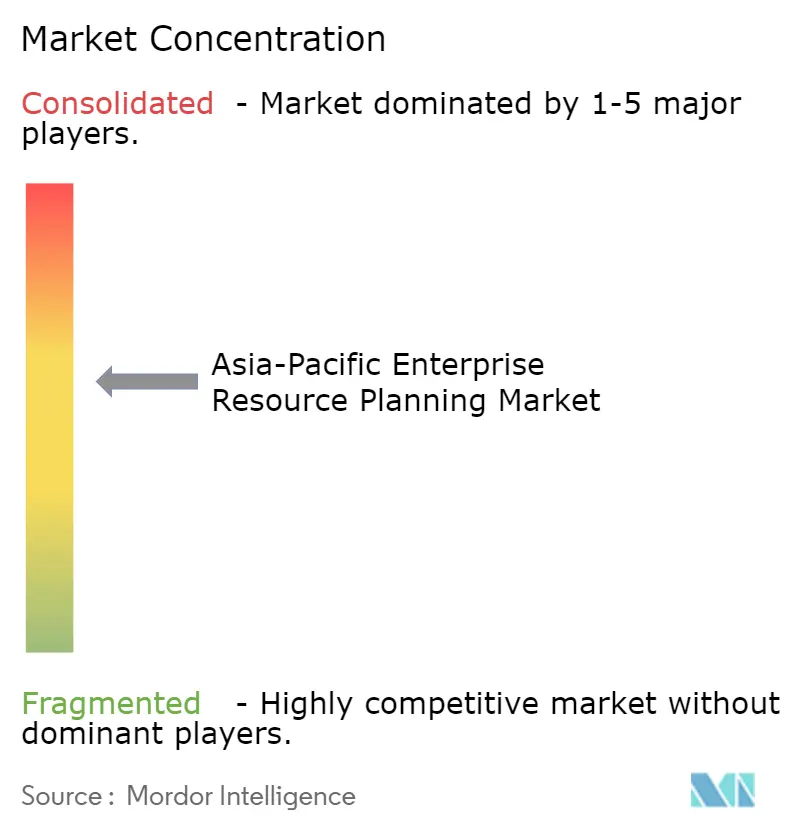

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Enterprise Resource Planning Market Analysis by Mordor Intelligence

The Asia-Pacific Enterprise Resource Planning Market size is expected to grow from USD 12.57 billion in 2025 to USD 14.47 billion in 2026 and is forecast to reach USD 25.39 billion by 2031 at a 12.37% CAGR over 2026-2031. Rapid uptake of cloud-native suites, formal cloud-first policies, and the embedding of artificial intelligence into core workflows are widening the addressable base beyond large manufacturers into highly regulated public-sector agencies and small retailers. Government frameworks that mandate e-invoicing, unified data registries, and sovereign cloud hosting have shortened decision cycles and redirected information-technology budgets toward modern enterprise resource planning platforms. Vendors are racing to certify local data centers, pre-integrate with national identity wallets, and expose application programming interfaces that enable start-ups to build vertical extensions, intensifying the competitive landscape. The convergence of demographic pressures, mobile-first workstyles, and low-code configuration tools is further lowering adoption barriers for resource-constrained small and medium enterprises.

Key Report Takeaways

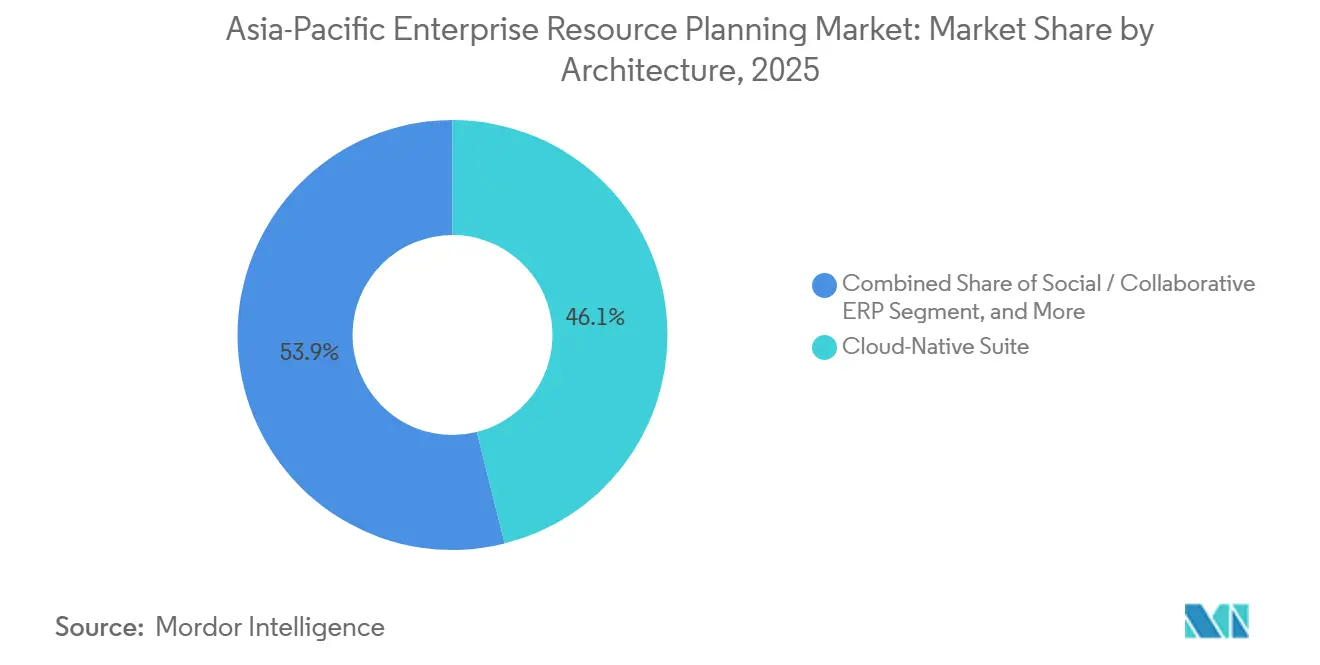

- By architecture, cloud-native suite architecture led the Asia-Pacific enterprise resource planning market with a 46.1% share in 2025. Mobile-first ERP is projected to advance at a 12.7% CAGR through 2031.

- By business function, finance and accounting commanded 31.5% of 2025 revenue of the APAC ERP Market, while human capital management is poised for a 12.9% CAGR through 2031.

- By deployment model, cloud captured 63.4% of 2025 revenue of the Asia-Pacific ERP Market and is forecast to expand at a 12.3% CAGR through 2031.

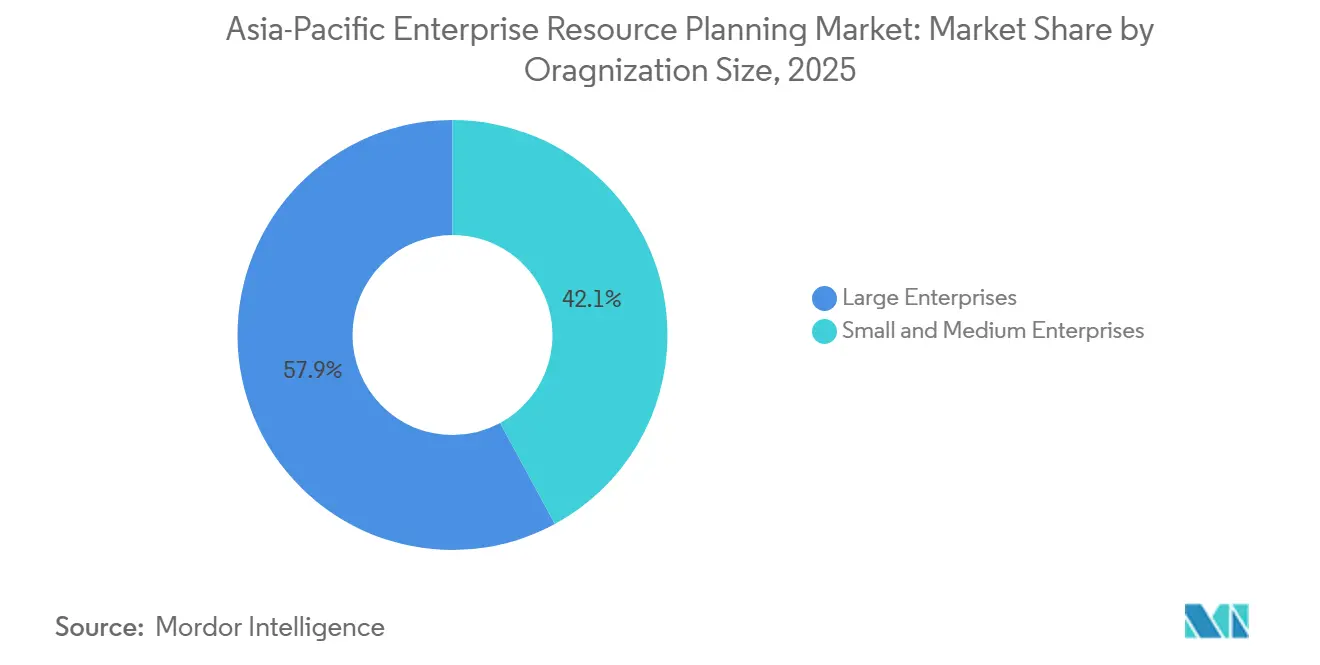

- By organization size, large enterprises held 57.9% share of the APAC enterprise resource planning market value in 2025; small and medium enterprises are projected to grow at a 12.7% CAGR through 2031.

- By industry vertical, manufacturing led with 28.7% revenue share in 2025, whereas retail and e-commerce are expected to post a 13.3% CAGR through 2031.

- By geography, China accounted for 38.5% revenue share in 2025, while India is forecast to grow at a 13.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Enterprise Resource Planning Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption Of Cloud-Native Architectures | +2.8% | China, India, Japan, Singapore, Australia | Medium Term (2-4 Years) |

| Government-Led Digital Transformation | +2.5% | China, India, Japan, Singapore, Malaysia, Vietnam | Short Term (≤ 2 Years) |

| Remote Work And Mobile-First Workflows | +1.9% | Urban Centers In China, India, Southeast Asia | Short Term (≤ 2 Years) |

| Local ISV Ecosystems For Industry Extensions | +1.6% | China, India, Japan, South Korea, ASEAN | Medium Term (2-4 Years) |

| AI-Driven Analytics Integration | +2.1% | Japan, Singapore, Australia, China | Medium Term (2-4 Years) |

| Venture Capital Funding For Vertical SaaS | +1.2% | India, Singapore, China, Australia, Indonesia, Vietnam | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Cloud-Native Architectures Among Asia-Pacific Enterprises

Public-sector mandates are cascading into private procurement cycles. Japan’s government cloud portfolio expanded from 671 to 2,918 systems between 2024 and 2025, a 335% surge, after centralized deadlines required agencies to vacate legacy data centers. Australia activated a whole-of-government cloud policy in 2026 that compels agencies to embed cloud economics in every new digital investment, driving hyperscaler partner certifications.[1]Source: Digital Transformation Agency, “New Cloud Policy,” dta.gov.au Singapore migrated 213 systems to commercial clouds across 41 agencies, pushing more than 80% of eligible workloads off the government's private cloud. These exemplars demonstrate measurable reductions in release cycles and operating costs, persuading financial institutions and retailers to follow similar modernization blueprints in the APAC enterprise resource planning market.

Government-Led Digital Transformation Initiatives Across Emerging Asian Economies

National blueprints now tie gross domestic product targets to digital economy output, ensuring sustained budget allocations for unified data backbones and artificial intelligence-ready enterprise resource planning foundations. Beijing’s Digital China 2025 Action Plan aims for core digital industries to exceed 10% of GDP while expanding compute capacity beyond 300 exaflops, creating predictable demand for domestically hosted, standards-based platforms. The India-Japan Digital Partnership 2.0, signed in 2025, codifies collaboration on interoperability of digital public infrastructure, artificial intelligence governance, and semiconductor value chains, accelerating cross-border system integration projects. Singapore’s Smart Nation 2.0 recorded a 11.2% compound annual growth rate over the past five years in its digital economy, with 9 in 10 firms adopting at least one digital tool in 2024. Such policies compress adoption timelines for modern suites and favor vendors able to certify local data residency while integrating with e-procurement platforms and digital-identity rails in the Asia-Pacific ERP market.

Accelerated Post-Pandemic Push Toward Remote Work and Mobile-First Workflows

Distributed teams now expect full transactional parity between desktop and handheld devices. Japan’s Digital Infrastructure Development Plan for 2030 funds all-optical networks and non-terrestrial backhaul to guarantee latency-sensitive access in remote prefectures. Malaysia ties smart-factory grants to readiness assessments that emphasize mobile dashboards for predictive maintenance. Singapore’s Singpass identity wallet underpins more than 2,700 public services, normalizing biometric login for approvals and expense claims on smartphones.[2]Source: Government Technology Agency of Singapore, “Annual Report 2024/2025,” govtech.gov.sg These factors elevate vendor road-maps that prioritize responsive design, push notifications, and offline synchronization for field-force scenarios in the APAC enterprise resource planning market.

AI-Driven Analytics Driving Demand for Modern ERP Suites

Consultants stress that artificial intelligence generates sustainable value only after data harmonization is achieved inside the core system of record. McKinsey finds that fewer than 40% of enterprises report any earnings before interest and taxes benefit from artificial intelligence because foundational resource-planning layers remain fragmented. EY, SAP, and Microsoft now jointly migrate legacy workloads to SAP S/4HANA Cloud Private Edition on Azure to position autonomous agents that reconcile invoices or predict cash-flow variances. Infor’s collaboration with Amazon Web Services logged a 900% jump in marketplace revenue after embedding generative tools inside healthcare and manufacturing suites. The shift reframes enterprise resource planning from a transaction engine into an insight generator, creating peer pressure for late adopters.

Restraint Impact Analysis*

| Restraint | (~) % Impact On CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage Of Skilled Implementation Partners | -1.4% | Tier-2 Cities In India, China, Indonesia, Vietnam | Medium Term (2-4 Years) |

| Data Sovereignty Regulations | -1.8% | China, India, Vietnam, Indonesia, Malaysia, Thailand | Short Term (≤ 2 Years) |

| Fragmented SME Market And Low IT Budgets | -1.6% | Rural ASEAN, India, Inland China | Long Term (≥ 4 Years) |

| Complex Legacy Customizations Inflating Migration Risk | -1.3% | Japan, Australia, South Korea, China, India | Medium Term (2-4 Years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled ERP Implementation Partners in Tier-2 Asian Cities

Consultancy talent remains concentrated in metro hubs, leaving manufacturers in provincial clusters with long wait times and premium travel charges. A survey of 605 Vietnamese small and medium enterprises showed sustained usage plunged to 35% after 18 months without an internal champion.[3]Source: World Bank, “Challenges with Digital Technology Adoption by SMEs,” worldbank.org Malaysia’s New Industrial Master Plan flags the same skills gap as a barrier to smart-factory ambitions, prompting the government to earmark intervention funds for training. Vendors offer remote configuration portals and templated rollouts, yet these often limit deep customization in the Asia-Pacific ERP market.

Data Sovereignty Regulations Limiting Cross-Border Cloud Deployments

Divergent localization rules lead to increased infrastructure duplication. China caps foreign equity in many value-added services at 50% and requires critical operators to localize all personally identifiable data. Vietnam’s Data Law 2024 introduces Important and Core classifications that force pre-transfer impact reviews. Multinationals now juggle multiple regional instances and reconcile ledgers offline, inflating the total cost of ownership and delaying analytics projects that rely on aggregated datasets in the Asia-Pacific ERP market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Architecture: Modular Suites Outpace Monolithic Platforms

Cloud-native suites owned 46.1% of the Asia-Pacific enterprise resource planning market share in 2025. Mobile-first architectures are forecast to post a 12.7% CAGR through 2031 as distributed workforces demand smartphone parity. The market for cloud-native modules is expanding as public agencies migrate from on-premises SAP ECC and Oracle E-Business Suite before their support sunsets. Enterprises value microservices that allow phased cutovers, avoiding risky big-bang switches. Mobile-first design reduces end-user training overhead and accelerates approval cycles, a boon for retailers reconciling omnichannel inventory.

Vendor strategies illustrate the shift. Japan’s Digital Agency slashed release cycles from six months to 48 hours by adopting scaled agile frameworks and automated quality gates.[4]Source: The Asian Banker, “Japan Digital Agency SAFe Impact,” theasianbanker.com Microsoft and SAP target 40,000 mid-market firms for ECC migrations that bundle built-in artificial intelligence co-pilots. Workday’s December 2025 purchases of Sana and Pipedream deliver 3,000 pre-built connectors, enabling enterprises to embed conversational agents without heavy custom code.

By Business Function: Finance Dominance Gives Way to Human Capital Management Velocity

Finance and accounting retained 31.5% of the Asia-Pacific enterprise resource planning market share in 2025, yet human capital management is on track for a 12.9% CAGR. Mandatory e-invoicing and real-time tax remittance keep finance at the core, but demographic headwinds make workforce intelligence equally strategic. The Asia-Pacific enterprise resource planning market for payroll and talent modules is growing as Japan’s My Number Card and Singapore’s Singpass APIs enable systems to pull verified identity and benefits data in real time.

Government deployments set precedents. Singapore’s VISION platform, spanning 100,000 public officers, cut processing time by 30% after automating hire-to-retire workflows. Infosys applies its Topaz artificial intelligence methodology to Workday rollouts, claiming measurable gains in close rates and retention. These examples reinforce that talent analytics and predictive attrition models are now board-level priorities. Additionally, integrating AI-driven insights into ERP systems enables organizations to make more informed, strategic decisions.

By Deployment Model: Cloud Ascendancy Reshapes Infrastructure Economics

Cloud accounted for 63.4% of the 2025 value and is projected to add a 12.3% CAGR through 2031, underscoring irreversible momentum toward subscription economics. Asia-Pacific ERP market share for on-premise editions is eroding as vendors throttle feature parity and raise support fees. Public-sector frameworks such as Australia’s AUD 152 million (USD 109 million) whole-of-government SAP agreement grant agencies pre-vetted pricing and security wrappers, making procurement frictionless.

Private firms exhibit similar trends to those observed in the public sector. For instance, New South Wales successfully migrated a significant number of users to RISE with SAP, enabling the harmonization of numerous agencies under a unified ledger system. This migration highlights the potential for streamlined operations and improved efficiency across various departments. Similarly, New Zealand has implemented a framework contract that allows ministries to leverage a unified master agreement. This approach simplifies legal reviews and reduces administrative complexities, making it easier for ministries to adopt cloud-based solutions. These examples provide strong validation of the economic benefits and operational efficiencies that cloud solutions can deliver, even in highly regulated industries.

By Organization Size: Small and Medium Enterprises Close the Adoption Gap

Large enterprises still account for 57.9% of 2025 revenue, but small and medium enterprises will deliver outsized growth at a 12.7% CAGR. Subsidies anchored in Singapore’s Digital Enterprise Blueprint and China’s small-business digital-transformation vouchers reduce upfront cost. Low-code templates bundled with managed services mean owners can deploy invoicing, payroll, and inventory within weeks instead of quarters. The Asia-Pacific ERP market for small and medium enterprises remains modest today, yet rapid growth could shift vendor roadmaps toward multi-tenant, consumption-based pricing.

Field evidence suggests retention hinges on quick wins. World Bank trials in Vietnam revealed that firms focused on paperwork reduction persisted, whereas those lacking internal champions churned quickly. Vendors now bundle adoption coaches and gamified learning modules to preserve engagement. Furthermore, these initiatives are increasingly being integrated with real-time performance tracking to ensure sustained adoption success in the APAC enterprise eesource planning market.

By Industry Vertical: Manufacturing Leadership Meets Retail Velocity

Manufacturing generated 28.7% of 2025 revenue and remains the anchor vertical, but retail and e-commerce are racing ahead at a 13.3% CAGR. The market size expansion in retail is fueled by omnichannel orchestration, last-mile delivery optimization, and unified promotions across social and physical storefronts. Factories invest in predictive maintenance and digital thread traceability to meet export compliance requirements and decarbonization audit standards.

Case studies abound. Malaysia plans to certify 3,000 smart factories by 2030, linking grant access to ERP-connected sensors. Vietnamese bank VPBank migrated 77 terabytes to a containerized core in one weekend, doubling peak capacity and demonstrating that even regulated finance can execute big-bang data moves when orchestration is automated. These vignettes highlight divergent, industry-specific payoffs, in the APAC enterprise resource planning market, that modern suites enable.

Geography Analysis

China accounted for 38.5% of 2025 revenue, reflecting the scale of state-owned enterprises and rigid localization mandates that favor domestic cloud partners. Government objectives to raise digital-economy output above 10% of GDP and accrue 300 exaflops of compute by 2025 guarantee sustained license demand, although foreign vendors must joint-venture to comply with equity caps. India, in contrast, offers rapid growth: with a significant compound annual growth rate, Goods and Services Tax integration deadlines, and the India-Japan Digital Partnership, demand is increasing for interoperable, cloud-hosted suites that integrate with Aadhaar and the Unified Payments Interface. Japan’s substantial rise in government cloud workloads between 2024 and 2025 underscores the policy-driven urgency and serves as a model for municipalities to emulate.

South Korea’s Distributed Energy Act nudges data center operators toward renewable energy, subtly affecting the total cost of ownership for hosted ERP. Australia and New Zealand provide regulatory certainty, evidenced by multi-year, whole-of-government SAP accords that standardize service-level agreements and cost baselines. Rest-of-Asia-Pacific remains heterogeneous. Vietnam’s Data Law imposes impact assessments before cross-border replication, while Malaysia’s master plan couples factory grants to digital-readiness scores.

These nuances dictate deployment choice: multinationals often adopt hub-and-spoke architectures with localized edge instances and centrally governed finance cores. Localized language packs, tax engines, and statutory reporting embedded in modern suites reduce ongoing compliance spend. Vendors that can flex licensing metrics, such as per-transaction billing for start-ups, will capture greenfield opportunities in Indonesia and the Philippines, where formal enterprise resource planning penetration is below 20%.

Competitive Landscape

The Asia-Pacific enterprise resource planning market is moderately fragmented. Global incumbents such as SAP, Oracle, Microsoft, and Workday dominate federal and blue-chip contracts through accredited data centers and vast partner ecosystems, yet regional specialists like Yonyou, Kingdee, and Pronto carve out a share by localizing payroll, Unicode support, and fiscal calendars. Generative artificial intelligence road maps are a new battleground. Workday’s acquisition of Sana and Pipedream layers retrieval-augmented generation atop 3,000 connectors, enabling chat-based workflows that write back into finance and human-capital ledgers.

System integrators integrate offensively. EY’s three-way alliance with SAP and Microsoft promises autonomous, general-ledger-closing, while Infosys Topaz automates configuration sprints, claiming double-digit reductions in person-weeks per rollout. Infor leans on Amazon Web Services marketplaces to tap mid-tier hospitals and discrete manufacturers, reporting a 400% lift in co-sell deals.

White-space remains in agriculture, construction, and hospitality, where workflow depth lags. Low-code disruptors backed by venture capital prototype vertical micro-services, yet scale depends on assembling certified implementers across dozens of second-tier cities. These sectors present untapped opportunities for growth, provided companies address the challenges of scalability and localized implementation. Compliance scaffolding, sovereign-cloud options, and transparent cost analytics will decide the next wave of share shifts.

Asia-Pacific Enterprise Resource Planning Industry Leaders

SAP SE

Oracle Corporation

Microsoft Corporation

Yonyou Network Technology

Infor Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: SAP opened a Public Sector Centre of Excellence in Canberra to accelerate federal cloud migration and claims to achieve 20-30% efficiency gains through automation.

- December 2025: Workday completed its Sana acquisition and agreed to buy Pipedream, embedding knowledge retrieval and 3,000 connectors in ChannelLife Australia.

- December 2025: China’s Cyberspace Administration unveiled a China-ASEAN digital-governance initiative focused on threat information sharing.

- August 2025: India and Japan signed the Digital Partnership 2.0 memorandum covering digital public infrastructure and artificial intelligence governance, with METI Japan and MeitY India.

- March 2025: EY, SAP, and Microsoft launched a joint program to migrate to an autonomous ERP.

Asia-Pacific Enterprise Resource Planning Market Report Scope

The Asia-Pacific Enterprise Resource Planning Report is Segmented by Architecture (Cloud-Native Suite, Mobile-First ERP, Social and Collaborative ERP, and Two-Tier and Edge ERP), Business Function (Finance and Accounting, Supply-Chain and Operations, Human Capital Management, Customer Relationship and Commerce, and Manufacturing Execution and Quality), Deployment Model (On-Premise, and Cloud), Organization Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (Manufacturing, Retail and E-commerce, BFSI, Government and Public Sector, IT and Telecom, Healthcare and Life Sciences, and Other Industry Verticals), and Geography (China, India, Japan, South Korea, Australia and New Zealand, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Native Suite |

| Mobile-First ERP |

| Social / Collaborative ERP |

| Two-Tier / Edge ERP |

| Finance and Accounting |

| Supply-Chain and Operations |

| Human Capital Management |

| Customer Relationship and Commerce |

| Manufacturing Execution and Quality |

| On-Premise |

| Cloud |

| Large Enterprises |

| Small and Medium Enterprises |

| Manufacturing |

| Retail and E-commerce |

| BFSI |

| Government and Public Sector |

| IT and Telecom |

| Healthcare and Life Sciences |

| Other Industry Verticals |

| China |

| India |

| Japan |

| South Korea |

| Australia and New Zealand |

| Rest of Asia-Pacific |

| By Architecture | Cloud-Native Suite |

| Mobile-First ERP | |

| Social / Collaborative ERP | |

| Two-Tier / Edge ERP | |

| By Business Function | Finance and Accounting |

| Supply-Chain and Operations | |

| Human Capital Management | |

| Customer Relationship and Commerce | |

| Manufacturing Execution and Quality | |

| By Deployment Model | On-Premise |

| Cloud | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Industry Vertical | Manufacturing |

| Retail and E-commerce | |

| BFSI | |

| Government and Public Sector | |

| IT and Telecom | |

| Healthcare and Life Sciences | |

| Other Industry Verticals | |

| By Geography | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large will Asia-Pacific enterprise software spending for resource planning be by 2031?

It is projected to reach USD 25.39 billion, rising from USD 14.47 billion in 2026 on an 12.37% CAGR.

Which deployment option is expanding fastest across government agencies?

Cloud deployments, already 63.4% of 2025 revenue, are expected to grow at a 12.3% CAGR as whole-of-government agreements streamline procurement.

Why are human-capital modules gaining momentum?

Demographic pressures and regulatory payroll transparency rules push firms to adopt analytics-driven talent suites growing at a 12.9% CAGR.

What limits adoption in smaller cities?

A shortage of certified consultants inflates project costs and delays go-lives, reducing sustained usage in tier-2 clusters.

How does data sovereignty shape vendor strategy?

Divergent localization mandates force providers to maintain multiple in-country instances and offer hybrid architectures with assured residency.

Which industry vertical shows the quickest expansion?

Retail and e-commerce, driven by omnichannel inventory synchronization needs, is forecast to log a 13.3% CAGR through 2031.

Page last updated on: