Asia-Pacific Communication Platform-as-a-Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

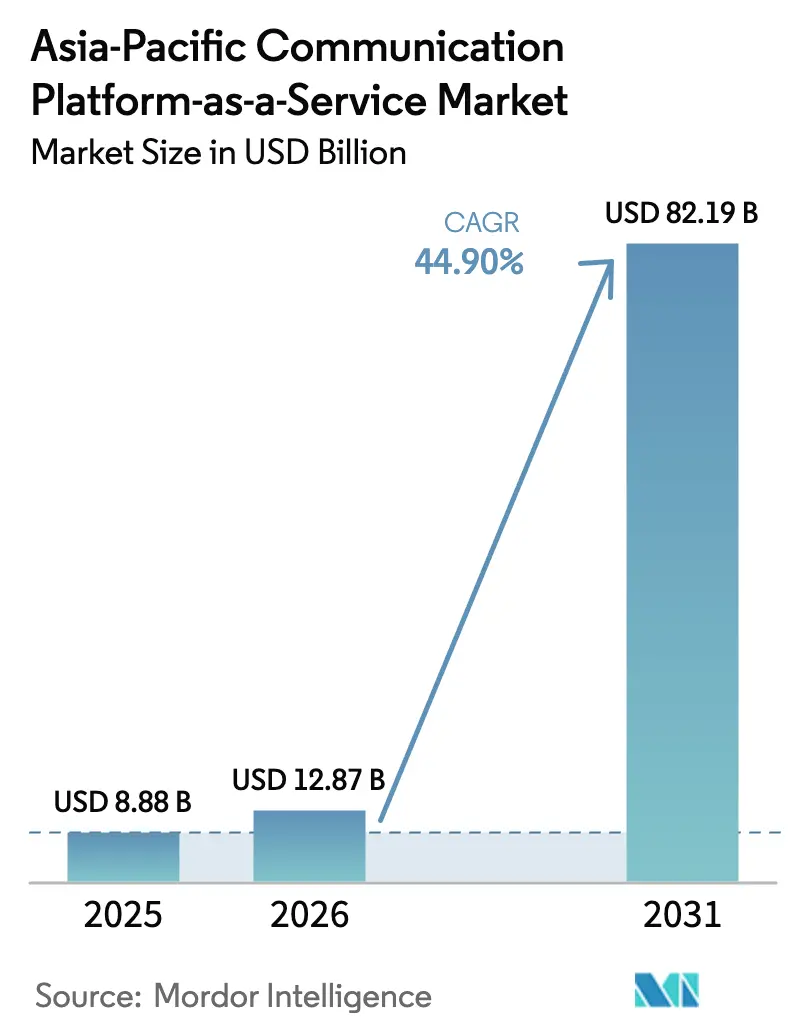

| Base Year Market Size (2025) | USD 8.88 Billion |

| Market Size (2026) | USD 12.87 Billion |

| Market Size (2031) | USD 82.19 Billion |

| Growth Rate (2026 - 2031) | 44.90% CAGR |

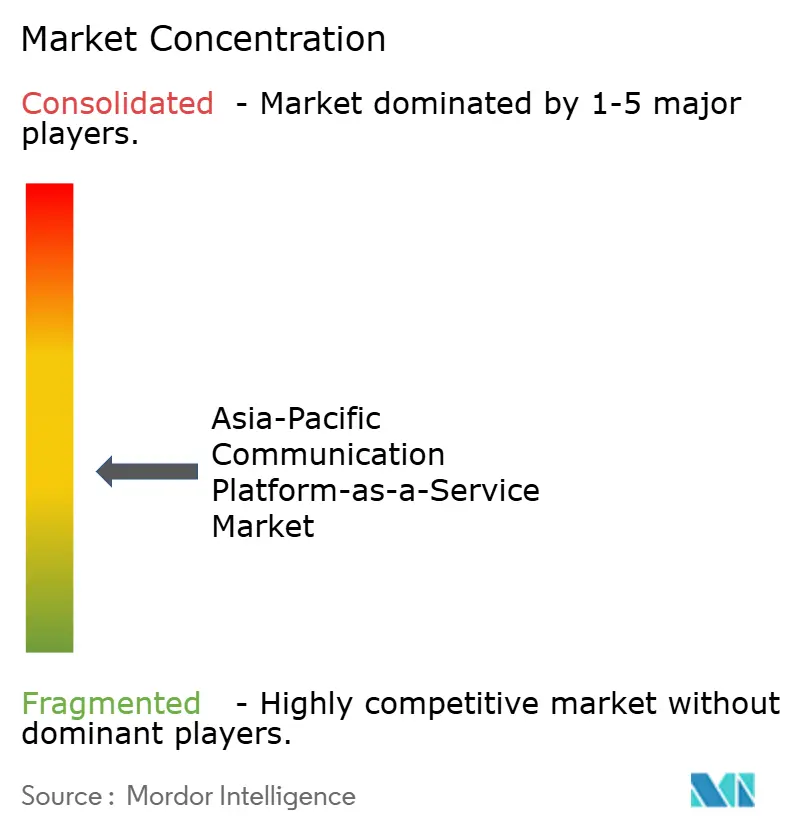

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Communication Platform-as-a-Service Market Analysis by Mordor Intelligence

The Asia-Pacific CPaaS market size in 2026 is estimated at USD 12.87 billion, growing from 2025 value of USD 8.88 billion with 2031 projections showing USD 82.19 billion, growing at 44.90% CAGR over 2026-2031. These growth dynamics stem from accelerated digital transformation programs, the proliferation of cloud-native communication stacks, and a decisive enterprise shift toward API-driven messaging, voice, and video workflows. China’s 5G-enabled cloud infrastructure, India’s fintech-centric super-apps, and Southeast Asia’s mobile-first commerce collectively reinforce adoption momentum. Large enterprises keep spending high, yet simplified low-code interfaces now allow SMEs to embed real-time communications without specialist talent, widening the addressable base. Providers differentiate through multi-channel orchestration, AI-powered analytics, and partnerships that bundle telco network APIs with advanced security and compliance. As a result, the Asia-Pacific CPaaS market is evolving from point-solution messaging toward integrated customer-experience platforms that unify channels, data, and automation.

Key Report Takeaways

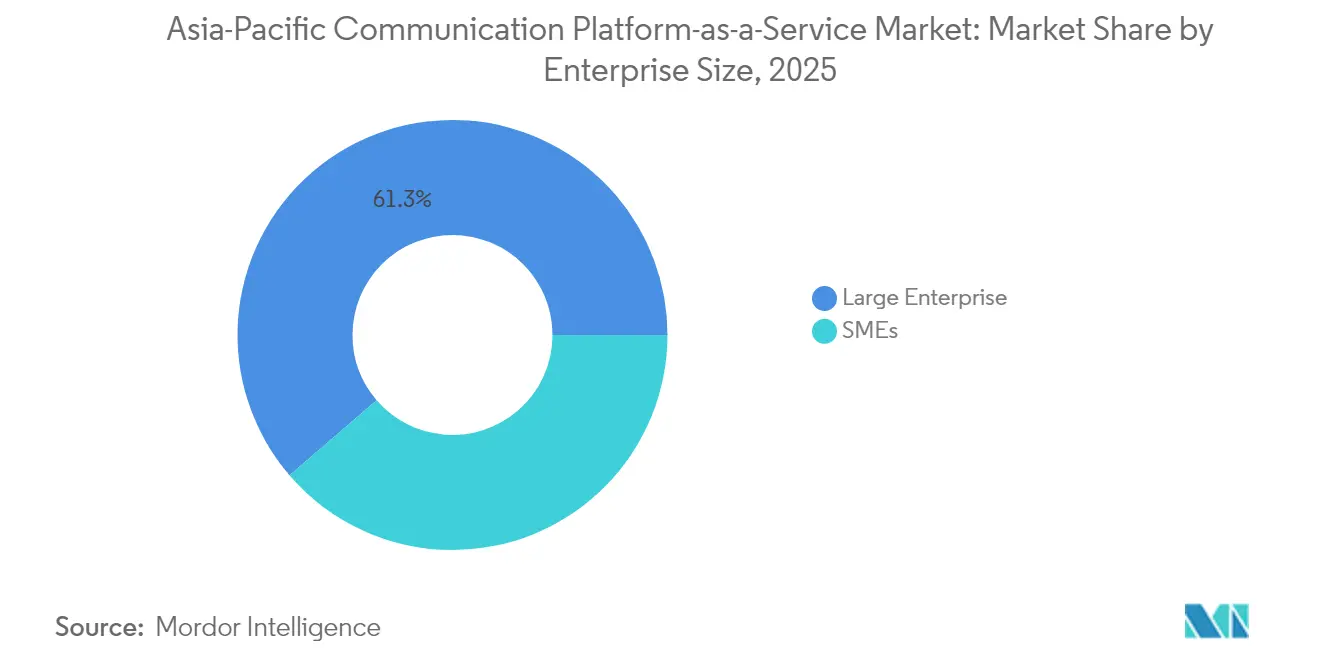

- By organization size, large enterprises contributed 61.30% revenue in 2025, whereas SMEs are poised to compound at 45.10% CAGR to 2031, the fastest among all segments.

- By end-user industry, BFSI accounted for a 25.10% share of the Asia-Pacific CPaaS market size in 2025 and e-commerce and logistics is advancing at a 44.80% CAGR during 2026-2031.

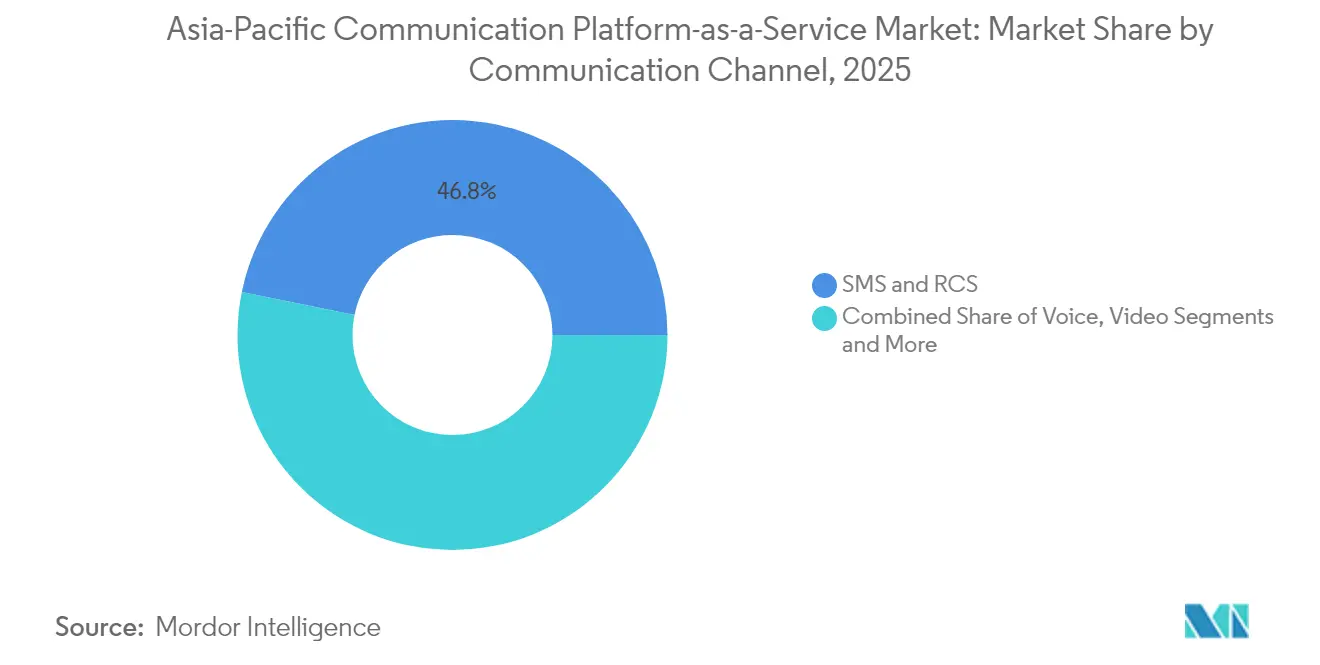

- By communication channel, SMS and RCS retained 46.80% share in 2025, whereas video APIs are forecast to grow at a 45.90% CAGR through 2031.

- By component, messaging APIs held 42.60% revenue in 2025; multi-channel workflow orchestration platforms deliver the highest projected CAGR at 46.40% to 2031.

- By geography, China led with 31.40% of Asia-Pacific CPaaS market share in 2025, while India is projected to expand at a 45.60% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Communication Platform-as-a-Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid cloud-led digital transformation across SMEs and large enterprises | +8.2% | Global, with concentration in China, India, Southeast Asia | Medium term (2-4 years) |

| Mobile-first population and 5G rollout accelerating A2P traffic | +7.8% | APAC core, particularly South Korea, Japan, Australia | Short term (≤ 2 years) |

| Growing omnichannel CX and CPaaS-based CX modernization wave | +6.9% | Global, with early adoption in Singapore, Hong Kong, Japan | Medium term (2-4 years) |

| Telco-backed Open-Gateway APIs unlocking network programmability | +5.4% | Regional, with focus on developed APAC markets | Long term (≥ 4 years) |

| Embedded-finance integrations driving CPaaS uptake in fintech and super-apps | +4.7% | Southeast Asia, India, China | Medium term (2-4 years) |

| Generative-AI infused APIs expanding CPaaS service mix and ARPU | +6.1% | Global, with innovation centers in China, Singapore, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Cloud-Led Digital Transformation Across SMEs and Large Enterprises

Enterprises have migrated 85% of applications to cloud platforms by 2025, and this lift in cloud workloads directly fuels demand for flexible communication APIs that plug into SaaS back-ends.[1]Huawei, “Cloud and Network Synergy for B2B Services,” huawei.com China’s cloud spending is rising 15% in 2025, with Alibaba Cloud, Huawei Cloud, and Tencent Cloud jointly delivering 71% domestic share, each embedding CPaaS add-ons into their marketplace portfolios. SMEs now regard communications as code rather than infrastructure, using pay-as-you-go APIs to send alerts, authenticate users, and orchestrate contact-center tasks. These low-barrier entry points democratize enterprise-grade communications, erasing the CapEx hurdle that historically limited adoption. The structural shift positions API communications as a core pillar of digital-experience architecture, not an auxiliary bolt-on.

Mobile-First Population and 5G Rollout Accelerating A2P Traffic

Asia-Pacific’s smartphone penetration surpasses 78% in 2025, and 5G subscriptions in Southeast Asia and Oceania are on course to exceed 570 million by 2027, reinforcing mobile-first engagement habits.[2]ICT Business, “5G to Top 570 Million Subscriptions in Southeast Asia and Oceania in 2027,” ictbusiness.biz Although international one-time-password traffic is set to decline as authentication alternatives emerge, operators counter by commercializing Rich Communication Services and advanced messaging formats. Sinch and Singtel’s 2024 launch of Singapore’s first RCS Business Messaging service showcases how richer media will offset plain-text erosion. As bandwidth improves, enterprises pivot from static SMS to video snippets, conversational commerce, and in-app chat, unlocking new monetization streams for CPaaS vendors.

Growing Omnichannel CX and CPaaS-Based CX Modernization Wave

Companies that deploy integrated messaging, voice, and social channels achieve 89% customer-retention rates, more than doubling single-channel strategies.[3]IntelePeer, “Demand for Better CX Is Here to Stay,” intelepeer.ai The healthcare super-app Apollo 24/7 raised average order revenue 72% after combining WhatsApp, RCS, and voice flows via Infobip, validating omnichannel ROI. Operators extend the concept: Thailand’s TrueBusiness launched “True CPaaS,” pairing AI-based personalization with multi-channel delivery to streamline commerce and support. These examples illustrate a region-wide pivot toward outcome-oriented communications in marketing automation, sales enablement, and post-purchase support—feeding continuous demand for orchestration and analytics modules.

Telco-Backed Open-Gateway APIs Unlocking Network Programmability

GSMA-aligned Open Gateway initiatives let developers access carrier functions—location, quality-on-demand, number verification—through standardized APIs. Ericsson and 12 operators formed the Aduna joint venture in 2025 to aggregate such capabilities, ensuring single-point exposure for the developer ecosystem. In Korea, mobile carriers jointly standardize network APIs to accelerate 5G monetization. TrueBusiness and EASY BUY introduced Thailand’s first commercial number-verification API, proving the commercial viability of this model. As these APIs blend with CPaaS platforms, enterprises gain programmable network attributes that elevate reliability and security, driving incremental spend per user.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy integration and migration complexity | -4.3% | Global, with higher impact in Japan, South Korea, Australia | Medium term (2-4 years) |

| Fragmented data-privacy and cross-border compliance landscape | -3.8% | Regional, particularly affecting cross-border operations | Long term (≥ 4 years) |

| Volatile regional SMS termination pricing and carrier consolidation | -2.9% | Asia-Pacific core, with concentration in Indonesia, Thailand, Philippines | Short term (≤ 2 years) |

| Rising AIT/SMS-fraud prompting aggressive traffic filtering | -2.7% | Global, with particular focus on India, China, Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy Integration and Migration Complexity

Two-thirds of communication-service providers cite legacy system entanglement as a top barrier to rolling out modern APIs, and technology debt reached 56% of IT budgets in 2024. Japanese and Korean enterprises that accrued proprietary systems over decades face complex data-mapping and security-governance tasks before activating CPaaS modules. In Singapore, 81% of companies seek vendors capable of managing multi-cloud migration and legacy coexistence The resulting preference is for end-to-end platforms that bundle pre-built connectors, secure edge nodes, and consulting services.

Fragmented Data-Privacy and Cross-Border Compliance Landscape

Asia-Pacific lacks a uniform data-protection regime, forcing providers to navigate divergent rules such as Hong Kong’s PDPO, Singapore’s PDPA, and India’s Digital Personal Data Protection Act. Each mandates distinct consent, residency, and breach-notification processes, inflating compliance overhead. Smaller CPaaS firms often lack the legal resources to customize architectures per jurisdiction, leading to service limitations or market exits. MVNO and net-neutrality directives add another layer of complexity, particularly where cross-border routing of SMS or voice may breach domestic carriage rules. The burden skews competitive advantage toward larger providers with dedicated governance teams, accelerating market consolidation and potentially throttling innovation in underserved markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: SMEs Drive Democratization

Large enterprises captured 61.30% of Asia-Pacific CPaaS market share in 2025, leveraging complex integrations, heavy security layers, and multi-country footprints. SMEs, however, are growing at a 45.10% CAGR to 2031, narrowing the historical adoption gap. Coca-Cola Europacific Partners Indonesia’s use of 8x8 SMS APIs within its Klik Toko app underscores how even blue-chip brands rely on CPaaS to streamline B2B distribution. The falling cost of programmable communications and the availability of low-code builders let smaller retailers embed chatbots, payment alerts, and click-to-video support in days rather than months. Providers now launch tiered packages that scale from starter kits to enterprise clusters, ensuring that entry-level customers do not churn as usage expands. This democratization both enlarges the total addressable base and intensifies competition for price-sensitive SME contracts.

By End-User Industry: BFSI Leadership Faces E-Commerce Challenge

BFSI held 25.10% of the Asia-Pacific CPaaS market size in 2025, reflecting widespread use of OTP, transaction alerts, and regulatory notices. Yet e-commerce and logistics is forecast to accelerate at a 44.80% CAGR through 2031 as super-apps embed conversational checkout, order tracking, and returns automation. Financial institutions prioritize reliability and compliance, driving uptake of number-verification APIs and encrypted messaging. In contrast, online marketplaces demand personalization and rapid experimentation, favoring platforms that expose A/B testing hooks and AI-powered chat composition. This divergence compels CPaaS vendors to segment roadmaps: highly secure, audit-ready modules for regulated sectors and agile CX toolkits for digital commerce.

Logistics operators adopt video chat for driver support and warehouse troubleshooting, while insurers test voice-biometric authentication to speed claims processing. Healthcare extends CPaaS into tele-consultation and prescription reminders, leveraging video SDKs compliant with patient-data laws. These diversified use cases emphasize that verticalized templates, not generic APIs, now determine vendor differentiation. Providers able to package regulatory accelerators—PCI-DSS, HIPAA equivalence, local e-signature—capture stickier revenue as industries converge on omnichannel engagement norms

By Communication Channel: Video APIs Surge Despite SMS Dominance

SMS and RCS delivered 46.80% of revenue in 2025, benefiting from device ubiquity and carrier-grade reach. Yet video APIs exhibit the fastest 45.90% CAGR as 5G bandwidth and browser-native WebRTC enable frictionless calls within mobile apps. Enterprises blend asynchronous SMS with live video to create guided support flows—the customer receives a text containing a one-time video link that escalates to a product specialist. Rich media’s ascent also manifests in banking, where advisors host secure video KYC sessions initiated from a verified SMS thread. While voice remains indispensable for IVR and agent assist, its growth plateaus as messaging channels absorb simple queries.

In-app chat gains traction inside super-apps, where transport, food delivery, and financial services co-exist. Push notifications and email maintain roles for account statements and regulatory disclosures, but younger demographics gravitate to real-time chat. Consequently, CPaaS vendors pivot to channel-agnostic orchestration that selects the optimal path based on user preference, cost, and compliance. Feature roadmaps now prioritize advanced codecs, AI camera effects, and screen-share functions to keep video engagement sticky, cementing its status as the next revenue unlock within the Asia-Pacific CPaaS market.

By Component: Multi-Channel Platforms Lead Innovation

Messaging APIs still contribute 42.60% of 2025 revenue, serving as the entry point for bulk alerts and transactional traffic. However, multi-channel workflow orchestration is expanding at a 46.40% CAGR as enterprises demand single-pane-of-glass control over SMS, voice, chat, and email journeys. Builders such as 8x8 Automation Builder illustrate how drag-and-drop flows democratize complex logic, letting marketers launch campaigns without engineering tickets. Voice APIs hold steady, augmented by speech-to-text, sentiment, and voice-biometric extensions that elevate caller experience. Video SDKs and in-call widgets accelerate tele-health, e-learning, and remote-inspection scenarios, reinforcing the channel mix thesis.

Professional and managed services gain relevance as enterprises seek advisory support on compliance, architecture, and ROI tracking. Providers that bundle consultative blueprints with platform licenses secure multi-year contracts and higher net revenue retention rates. The Asia-Pacific CPaaS market therefore tilts toward platform-plus-services propositions, with orchestration engines as the anchoring layer around which ancillary modules—AI bots, campaign analytics, payment gateways—cluster.

Geography Analysis

China commanded 31.40% of regional revenue in 2025, underpinned by expansive 5G roll-outs, cloud price wars, and government-backed “Eastern Data Western Computing” policies that balance data-center load and renewable energy sourcing. The Big Three telcos—China Mobile, China Unicom, China Telecom—each reported rising enterprise service lines, and Alibaba Cloud’s 59% international price cut signals aggressive scale economics to onboard more CPaaS workloads. Domestic providers embed messaging and video APIs directly into SaaS suites, streamlining procurement for state-owned banks, logistics conglomerates, and retail chains. As Chinese vendors expand into Southeast Asia, they carry bilateral cloud agreements that promote data-residency compliance, accelerating cross-border CPaaS expansion.

India is the growth pacesetter, clocking a 45.60% CAGR to 2031 as fintech apps, digital public-infrastructure projects, and affordable 5G devices unlock mass messaging and verification traffic. Tanla Platforms holds 35% share of the local CPaaS ecosystem and posted 29% year-on-year profit growth by scaling WhatsApp Business and RCS campaigns for banking and commerce clients.

Competitive Landscape

The Asia-Pacific CPaaS market sits in a consolidation cycle, yet remains moderately fragmented. Global leaders Twilio, Sinch, and Vonage scale via hyperscale cloud nodes and AI feature roadmaps, while regional specialists Tanla Platforms and Route Mobile leverage in-country carrier contracts and compliance accelerators. Proximus Global fused BICS, Telesign, and Route Mobile in January 2025, forming a cross-continent powerhouse that bundles wholesale messaging with enterprise APIs. At the network layer, the USD 6.5 billion XL Axiata-Smartfren merger strengthens Indonesian termination routes, indirectly benefiting CPaaS providers reliant on domestic reach.

Strategic differentiation increasingly hinges on AI integration. Alibaba Cloud pledged USD 52.9 billion toward Model-as-a-Service platforms, positioning to expose generative-AI functions directly through CPaaS endpoints. Twilio’s multi-year alliance with Microsoft Azure layers voice analytics and large-language-model capabilities atop existing communications workflows. Regional champions follow suit: Infobip joined forces with NTT Com Online to provide omnichannel services in Japan, pairing local sales muscle with global platform depth.

Asia-Pacific Communication Platform-as-a-Service Industry Leaders

Twilio Inc.

Vonage Holdings Corp

Tanla Platforms Limited

Route Mobile

VCloudX PTE Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Alibaba Cloud committed USD 52.9 billion to expand AI infrastructure and open-source tooling, reinforcing its CPaaS stack.

- May 2025: Twilio entered a multi-year partnership with Microsoft to deepen CPaaS integration with Azure services.

- January 2025: Proximus Global completed the merger of BICS, Telesign, and Route Mobile, forming a large-scale CPaaS entity.

- January 2025: Infobip partnered with NTT Com Online to broaden omnichannel delivery in Japan

Asia-Pacific Communication Platform-as-a-Service Market Report Scope

CPaaS, or communication platform-as-a-service, is a cloud-based platform that embeds voice, video, chat, and messaging applications within an organization’s business applications.CPaaS is a middleware offering wherein companies (vendors) build and distribute real-time communication software. It suggests that agents can communicate within the CRM application or contact center software platform in the contact center context.

The Asia-Pacific communication platform-as-a-service (CPaaS) market is segmented by organization size (SME and large-scale enterprise), end-user vertical (IT and Telecom, BFSI, retail, and consumer goods, consumer goods, and other end-user verticals), and country (China, India, Japan, South Korea, South East Asia, and rest of Asia-Pacific).

The market sizes and forecasts are provided in value in USD for all the above segments.

| Small and Medium-sized Enterprises (SMEs) |

| Large Enterprises |

| IT and Telecom |

| BFSI |

| Retail and Consumer Goods |

| Healthcare and Life Sciences |

| E-commerce and Logistics |

| Others |

| SMS and RCS |

| Voice |

| Video |

| Email and Push |

| In-app / OTT Chat |

| Messaging APIs |

| Voice APIs |

| Video APIs and SDKs |

| Multi-channel and Workflow Orchestration Platforms |

| Professional and Managed Services |

| China |

| India |

| Japan |

| South Korea |

| Southeast Asia |

| Australia and New Zealand |

| Rest of Asia-Pacific |

| By Organization Size | Small and Medium-sized Enterprises (SMEs) |

| Large Enterprises | |

| By End-User Industry | IT and Telecom |

| BFSI | |

| Retail and Consumer Goods | |

| Healthcare and Life Sciences | |

| E-commerce and Logistics | |

| Others | |

| By Communication Channel | SMS and RCS |

| Voice | |

| Video | |

| Email and Push | |

| In-app / OTT Chat | |

| By Component / Service Type | Messaging APIs |

| Voice APIs | |

| Video APIs and SDKs | |

| Multi-channel and Workflow Orchestration Platforms | |

| Professional and Managed Services | |

| By Geography | China |

| India | |

| Japan | |

| South Korea | |

| Southeast Asia | |

| Australia and New Zealand | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current size and growth outlook for the Asia-Pacific CPaaS market?

The market stands at USD 12.87 billion in 2026 and is projected to reach USD 82.19 billion by 2031, reflecting a 44.90% CAGR.

Which country generates the highest CPaaS revenue in Asia-Pacific?

China leads the region with 31.40% share in 2025, boosted by large-scale 5G roll-outs and extensive cloud infrastructure.

Which industry segment holds the largest share of CPaaS spending?

BFSI commands 25.10% of regional revenue, mainly through transaction notifications, number verification, and secure customer communications.

Which communication channel is expanding the fastest?

Video APIs record the strongest momentum, advancing at a 45.90% CAGR through 2031 as enterprises embed real-time video into mobile and web apps.

Page last updated on: