Europe Automotive LED Package Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

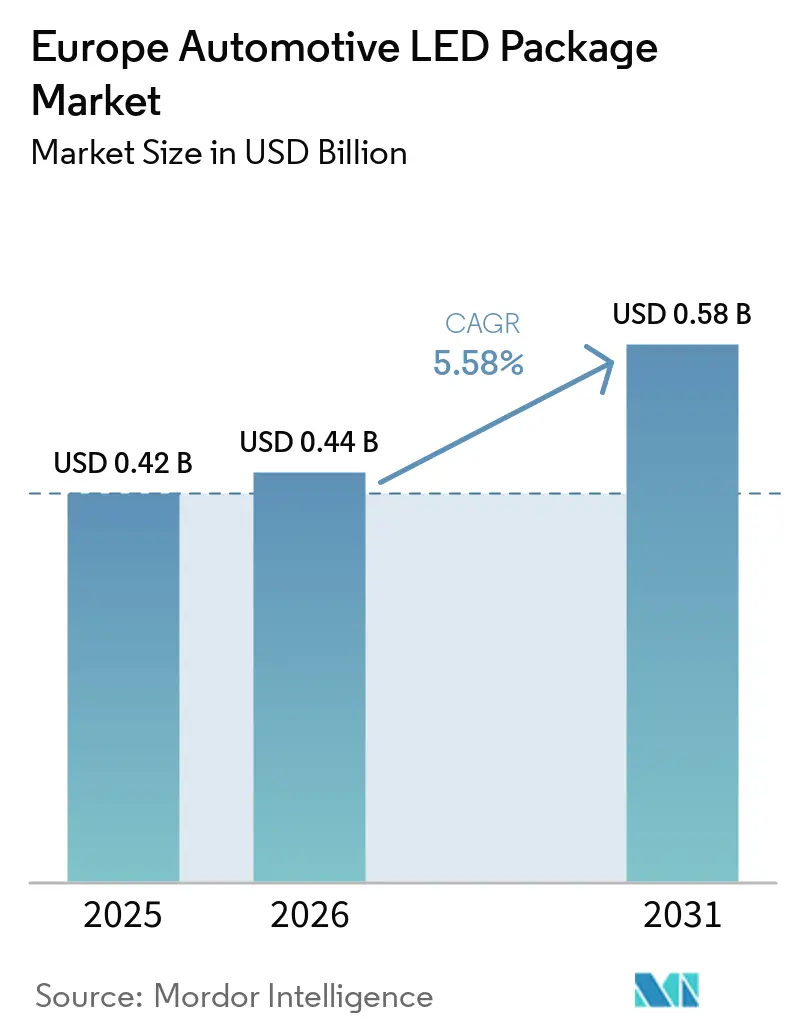

| Base Year Market Size (2025) | USD 0.42 Billion |

| Market Size (2026) | USD 0.44 Billion |

| Market Size (2031) | USD 0.58 Billion |

| Growth Rate (2026 - 2031) | 5.58% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Automotive LED Package Market Analysis by Mordor Intelligence

The Automotive LED package market size is expected to increase from USD 0.42 billion in 2025 to USD 0.44 billion in 2026 and reach USD 0.58 billion by 2031, growing at a CAGR of 5.58% over 2026-2031. A mature halogen-to-LED replacement cycle now limits unit growth, so value creation depends on high-pixel adaptive systems, interior ambient innovations, and regulatory pushes for energy efficiency. European passenger car output edged up only 1.4% in 2025, confirming that volume alone will not accelerate demand; instead, premium lighting content per vehicle is rising as OEMs adopt chip-scale packages, micro-LED arrays, and driver-IC integration. Germany’s premium brands continue to seed early technology adoption, yet France shows the strongest growth momentum thanks to incentives that boosted battery electric vehicle (BEV) registrations and stimulated new adaptive lighting programs. Thermal breakthroughs, software-defined architectures, and localized supply chains in Eastern Europe are reshaping procurement logic, while impending carbon-related import fees pressure Asian suppliers to shift fabrication closer to the region.

Key Report Takeaways

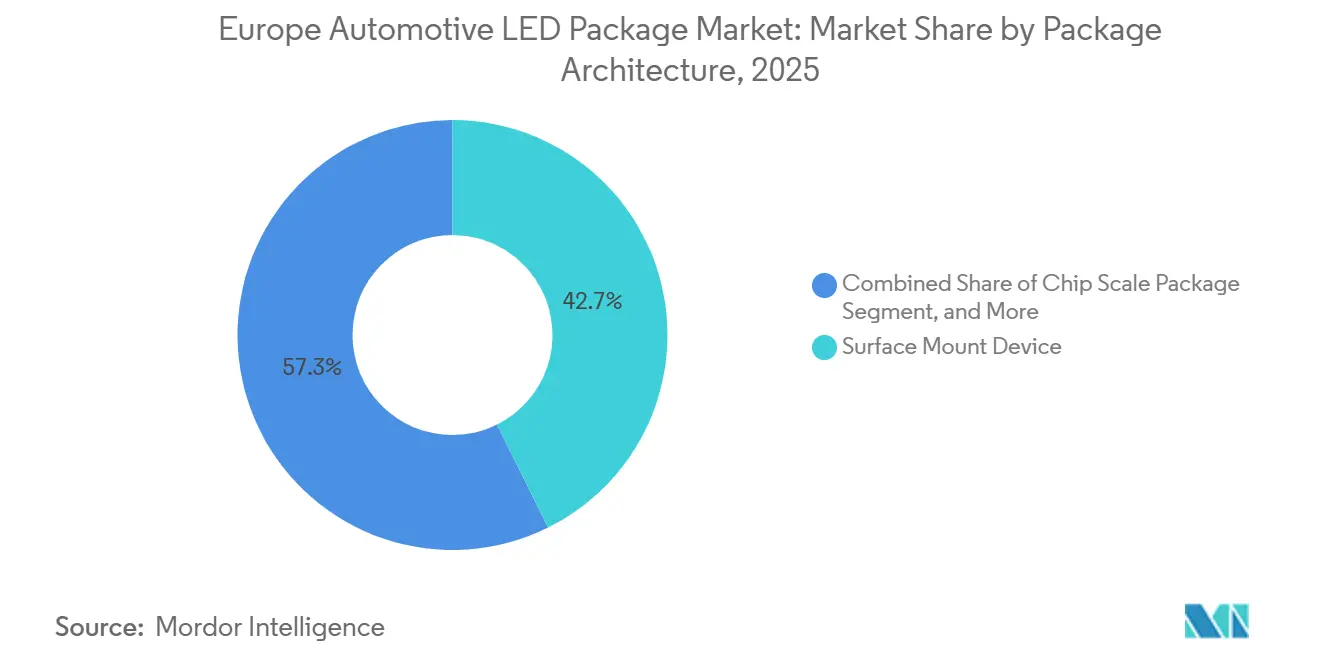

- By package architecture, surface-mount device packages held 42.67% revenue share in 2025; chip-scale packages are forecast to expand at a 6.01% CAGR to 2031.

- By power class, high-power packages above 1 W captured 59.68% of 2025 revenue and will grow at 5.94% through 2031.

- By application, exterior lighting represented 51.29% of 2025 demand, yet interior lighting is expected to post the fastest 6.11% CAGR into 2031.

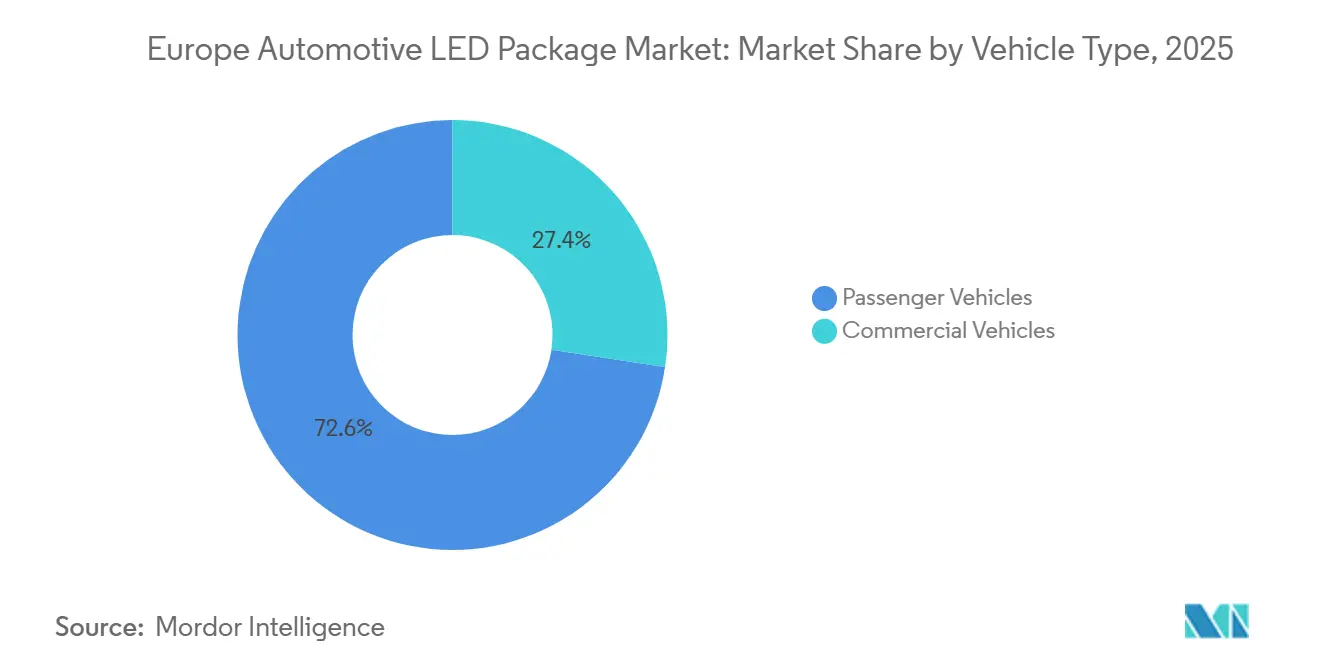

- By vehicle type, passenger vehicles accounted for 72.63% of the Automotive LED package market size in 2025 and are set to progress at a 6.16% CAGR during 2026-2031.

- By geography, Germany led with 27.44% of Automotive LED package market share in 2025, while France is projected to advance at a 5.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Automotive LED Package Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Shift From Halogen to LED Headlamps | +1.2% | Germany, France, UK, Rest of Europe | Medium term (2–4 years) |

| Growing Demand for Adaptive Front-Lighting | +1.5% | Germany, France, premium segments Europe-wide | Long term (≥ 4 years) |

| Stringent EU CO₂ Regulations | +0.9% | EU-wide, strongest in Germany and France | Short term (≤ 2 years) |

| Mini-LED and Micro-LED Integration | +0.8% | Germany, UK, premium OEM platforms | Long term (≥ 4 years) |

| Supply Chain Localization Incentives | +0.5% | Poland, Czech Republic, Slovakia, Hungary | Medium term (2–4 years) |

| Automotive Cyber-Security IR LED Demand | +0.4% | EU-wide, driven by UN R155 compliance | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Shift From Halogen to LED Headlamps

UN Regulation 37 amendments in 2022 cleared the legal path for certified LED retrofit bulbs in halogen positions. In May 2025, ams OSRAM shipped the first ECE-approved H11 LED replacements, promising fivefold energy savings and six times longer life. A phased roadmap runs through 2028 to address the full halogen bulb family, opening a multiyear retrofit opportunity across Europe’s 252 million-unit passenger fleet. Concurrently, OEMs like Stellantis have showcased compact Bi-LED modules that meet halogen photometry at lower cost and power, signaling parallel demand for cost-optimized LEDs in new entry vehicles. Package suppliers must therefore split portfolios between thermally robust retrofit formats and ultra-compact OEM solutions, each requiring different impedance and driver-IC strategies.

Growing Demand for Adaptive Front-Lighting Systems

UN Regulation 123 harmonization lowered homologation barriers for adaptive driving beam (ADB), shifting the feature from luxury to mass-market trims. Audi’s 2026 Q3 debuts a micro-LED matrix with 25,600 pixels, while Nichia’s three-tier Pixelated Light Source family lets OEMs scale from entry to premium ADB without new housings. Integrated Infineon LITIX drivers cut idle power by 50% during city cycles, meeting BEV efficiency targets. These architectures favor suppliers that combine LED epitaxy with ASIC co-design, accelerating a “winner-take-most” dynamic in high-pixel modules.

Stringent EU CO₂ Regulations Driving Energy-Efficient Lighting

The EU fleet target of 93 g CO₂ per km for 2025-2027 pushes OEMs to harvest every watt. Lighting redesigns such as the NALYSES project reduced headlamp power from 26 W to 10 W and cut life-cycle emissions by 52%. In BEVs, a 10 W load reduction can add up to 2 km of range, a spec already promoted in marketing. Package builders are moving to higher luminous efficacy, synchronous buck drivers hitting 92% efficiency, and advanced phosphors that satisfy UN Regulation 112 flux minima without breaching thermal limits.[1]International Council on Clean Transportation, “EU Fleet Average CO₂ Performance 2025,” theicct.org

Mini-LED and Micro-LED Integration in Premium Models

Premium brands now treat exterior lighting as a communication canvas. Mercedes-Benz’s GLC concept employed over 900 grille dots plus rear fluid light panels, while Porsche rolled HD matrix micro-LEDs across multiple lines. LG Innotek’s Nexlide Pixel shrinks modules to 3 mm thick, boosts efficiency 30%, and supports grille and badge integration. The thermal load of >10 W per square centimeter pushes suppliers toward vapor chambers and high-conductivity graphite, a capability that only vertically integrated players presently master.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Automotive Production Volumes | -0.6% | EU-wide, acute in Germany and UK | Short term (≤ 2 years) |

| Thermal Management Challenges at >1 W | -0.4% | Germany, France, premium OEM platforms | Medium term (2–4 years) |

| Patent Cliffs and LED IP Litigations | -0.3% | EU-wide, focus in Germany, Netherlands | Medium term (2–4 years) |

| Import Duties After CBAM Roll-out | -0.5% | EU-wide, impacting Asian suppliers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility in Automotive Production Volumes Post-2025

European builds remain 3 million units below pre-pandemic peaks, with 100,000+ supplier jobs lost since 2024. UK output fell 15.5% in 2025 amid cyberattacks and tariff woes, and van plus truck registrations slid 8.8% and 6.2% respectively. Energy inflation, labor shortages, and just-in-time disruptions raise working-capital costs for LED makers, forcing those without diversified end markets to operate under-utilized cleanrooms that erode margins.

Thermal Management Challenges at Power Classes Above 1 W

High-power LEDs generate junction temperatures that double failure rates every 10 °C unless advanced heat paths are deployed. Infrared thermography confirms that radiative self-heating inside lamp optics is often under-modeled. Compliance with UN Regulation 112 stability tests obliges suppliers to adopt copper-embedded boards, heat pipes, or graphite sheets, raising bill-of-materials costs. Mid-tier vendors lacking materials science partnerships face reliability cliffs that block entry into adaptive headlamps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Package Architecture: Chip-Scale Packages Accelerate

Chip-scale packages accounted for a rising slice of the Automotive LED package market size in 2025 and will out-grow legacy surface-mount devices through 2031. CSP attaches the die directly to the substrate, cutting thermal resistance and enabling pixel pitches fit for adaptive beams. Suppliers leverage CSP in micro-LED arrays where each die is <100 µm, limiting crosstalk while supporting >25,000-pixel matrices. Flip-chip variants offer superior current spreading for >10,000-candela headlamp beams yet demand void-free bonding, driving tighter process controls. Traditional SMD packages still dominate cost-sensitive daytime running lamps, but their share erodes as OEMs pivot to system-integrated solutions that combine LEDs and drivers on a single board. Chip-on-board remains the low-cost choice for entry reflectors, though its non-replaceability conflicts with EU circularity debates, a potential headwind to wide adoption.

The Automotive LED package market share leader in 2025 remained SMD, yet CSP’s 6.01% CAGR gives it the steepest trajectory. High-pixel adaptive lighting, digital signage, and grille illumination all benefit from CSP’s lower Z-height and thermal path, allowing thinner lamp profiles that improve aerodynamics. Suppliers that bundle CSP dies with Infineon or NXP driver ASICs gain system stickiness, while those limited to commodity SMD risk compression. EU discussions around replaceable LED sources may even tilt volume back to modular formats, creating a three-way contest among SMD, CSP, and emerging plug-in LED engine standards.

By Power Class: High-Power Packages Anchor Premium Content

High-power packages above 1 W contributed nearly 60% of Automotive LED package market revenue in 2025 as UN Regulation 112 flux thresholds lock headlamps into high-luminous systems.[2]European Commission, “Official Journal of the European Union, UN Regulation 112 Amendments,” eur-lex.europa.eu Premium ADB modules routinely exceed 2,000 lumens and thus require cleaning and leveling, activities best met by single high-power dies rather than many mid-power chips, simplifying optics and wiring. Mid-power LEDs fill cornering and signal niches where intensity demands are moderate, but their unit volumes cannot offset falling prices. Low-power LEDs remain vital for ambient interiors and cluster backlighting; however, ISELED smart RGB devices blur the line by embedding drivers, which shifts value from discrete packages to semiconductor-integrated lights.

High-power dominance will persist, with a 5.94% CAGR driven by projection headlamps and micro-LED arrays, yet thermal ceilings are real. Suppliers integrate vapor chambers or graphite sheets to keep junctions under 125 °C, a requirement for L70 lifetime beyond 25,000 hours. Vendors unable to manage >10 W per square centimeter risk exclusion from next-gen headlamps. Conversely, low-power interior LEDs thrive on BEV demand for customizable cabins and energy savings, with addressable RGB strips enabling over-the-air themes that synchronize with infotainment.

By Application: Interior Lighting Leads Growth

Exterior functions accounted for 51.29% of 2025 spending, covering headlamps, stop lights, and DRLs, yet cabin illumination is the fastest climber. Electric vehicles emphasize minimalist dashboards and mood lighting, making thin, flexible light guides a brand differentiator. Valeo’s 2026 IMSE launch inserts LEDs into molded panels, shrinking part counts and enabling three-dimensional gradients. LG Innotek’s Nexlide Air reduces module thickness by half, easing fit behind trim. OEM adoption of ISELED and ILaS protocols lowers harness complexity, letting software call dynamic color scenes.

Exterior spend remains anchored by safety mandates and styling refreshes. Adaptive beams, sequential turn signals, and animated welcome patterns all rely on high-output LEDs and precise drivers. Yet lamp volumes fall when production slows, whereas interior options attach to every trim regardless of sales slump, cushioning suppliers. Infrared LEDs for driver monitoring and gesture control add another demand vector, strengthened by UN R155 cybersecurity rules mandating secure cabin sensors.

By Vehicle Type: Passenger Cars Outperform Commercial Fleets

Passenger vehicles accounted for 72.63% of Automotive LED package market share in 2025 and are projected to expand at a 6.16% CAGR through 2031, benefiting from faster battery-electric uptake and higher lighting content per unit. Battery electric vehicles reached 19% of European passenger car registrations in 2025, four points above the prior year, intensifying the focus on energy-efficient LEDs that minimize range loss. Adaptive front-lighting and immersive RGB ambient systems now cascade from luxury to C-segment models, lifting package value even when overall vehicle production is flat. Suppliers that integrate chip-scale dies with Infineon or NXP drivers tout quiescent currents below 100 µA, a metric OEMs highlight in BEV marketing materials.

Commercial vehicles vans, trucks, and buses generated the remaining 27.37% of the Automotive LED package market size in 2025 but face weaker fundamentals. Van registrations fell 8.8% and truck registrations declined 6.2% in 2025, delaying retrofit cycles that would otherwise swap halogens for LEDs. BEV penetration in vans lags at roughly 10%, and heavy-duty electrification remains niche outside urban delivery fleets. Municipal bus programs in Denmark, Luxembourg, and the Netherlands have pushed e-bus fleet share past 10%, creating small spikes in demand for ruggedized high-power LEDs with replaceable modules. Nonetheless, the average European truck age of 14 years stretches halogen dominance, so most near-term LED growth stems from passenger cars rather than commercial platforms.

Geography Analysis

Germany captured the largest share of the Automotive LED package market size with 27.44% in 2025, reflecting its cluster of premium OEMs that spearhead micro-LED and adaptive headlamp adoption. The country’s 21% slice of EU production supports a dense supplier base and R&D ecosystem, yet high energy prices and labor gaps constrain output. Chinese entrants held 7% of EU sales in 2025, pressuring German brands on cost, so suppliers emphasize innovation and sustainability, exemplified by Hella’s 70% recyclable headlamp prototypes presented in March 2026.

France shows the fastest 5.91% CAGR to 2031, fueled by Stellantis electrification roadmaps and Renault’s software-centric lighting. Valeo’s January 2026 IMSE win plus its April 2025 laser projection partnership underline a pivot toward integrated hardware-software lighting solutions. Government BEV incentives lifted French and Spanish electric registrations, boosting demand for energy-efficient LED packages along the supply chain.

The United Kingdom saw a 15.5% production drop in 2025 after cyber disruptions at JLR and post-Brexit tariff friction, dampening near-term LED orders. Eastern European nations such as Poland, Czech Republic, and Slovakia attract localization incentives but battle port delays of up to 72 hours and acute logistics staffing shortages. Their lower labor costs lure Asian LED firms considering CBAM-induced reshoring, yet infrastructure gaps temper those moves.

Across the rest of Europe, Spain, Italy, and the Nordics balance the market with mixed signals. Spain’s 77% surge in BEV registrations created incremental demand for cabin ambient solutions, while Italy’s slower EV uptake held back adaptive headlamp volumes. Nordic bus electrification stimulates rugged LED modules for transit fleets. Collectively, these sub-regions keep the Automotive LED package market diversified and shield suppliers from any single-country shock.

Competitive Landscape

Competition remains moderately fragmented. OSRAM, Nichia, and Lumileds command premium headlamp LEDs and driver IC co-designs, collectively holding a dominant high-power slice. Asian players such as Seoul Semiconductor, Samsung, and LG Innotek expand aggressively in mid-power and mini-LED niches, often leveraging domestic fabs to offset CBAM fees. March 2024 saw Seoul Semiconductor sue Amazon Services Europe under the new Unified Patent Court, signaling a more litigious arena that smaller suppliers struggle to navigate.

Tier-1 integrators Valeo, Hella, and ZKW pursue vertical strategies, embedding LED engines into full lamp assemblies and monetizing software features like road projections. Valeo’s January 2026 IMSE program win and its Appotronics laser venture highlight how integrators bundle optics, heat sinks, and code to capture value beyond chips. Lumileds counters with modular LUXEON Go systems that anticipate future UN replaceable LED rules, positioning for circular-economy gains.

White-space lies in thermal-integrated packages and replaceable LED engines. Suppliers combining heat pipes or graphite sheets with LEDs secure premium pricing. Disruptors such as Ennostar and Refond push micro-LED epitaxy paired with in-house pick-and-place, challenging incumbents in grille and signal displays. Inova Semiconductors’ ISELED ecosystem has shipped 500 million smart RGB drivers since 2021, underpinning interior ambient explosions and giving semiconductor firms a stronger voice in lighting architecture.[3]Inova Semiconductors, “ISELED Ecosystem Shipments,” dvn-munich.com

Europe Automotive LED Package Industry Leaders

ams OSRAM AG

Nichia Corporation

Lumileds Holding B.V.

Seoul Semiconductor Co., Ltd.

Samsung Electronics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Audi launched micro-LED digital matrix headlights on the Q3, bringing 25,600-pixel adaptive projection to the compact segment.

- January 2026: Valeo secured a high-volume interior lighting program using TactoTek IMSE technology for a premium automaker.

- July 2025: LG Innotek partnered with Aeva, committing USD 50 million to supply ultra-slim 4D FMCW LiDAR modules for mobility applications.

- May 2025: ams OSRAM introduced the first ECE-approved H11 LED retrofit bulb, with a staged roadmap for the remaining halogen portfolio through 2028.

Europe Automotive LED Package Market Report Scope

The Europe Automotive LED Package Market is witnessing significant growth due to the increasing adoption of advanced lighting technologies in vehicles. Factors such as rising demand for energy-efficient lighting solutions, advancements in LED technology, and stringent government regulations on vehicle lighting standards are driving the market. The growing focus on enhancing vehicle aesthetics and safety further drives market expansion.

The Europe Automotive LED Package Market Report is Segmented by Package Architecture (SMD, CSP, Flip-Chip LED Packages, COB), Power Class (Low Power <0.5 W, Mid Power 0.5-1 W, High Power >1 W), Application (Exterior Lighting, Interior Lighting, Sensing/IR Applications, Other Applications), Vehicle Type (Passenger Vehicles, Commercial Vehicles), and Geography (United Kingdom, Germany, France, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| SMD (Surface Mount Device) |

| CSP (Chip Scale Package) |

| Flip-Chip LED Packages |

| COB (Chip-on-Board) |

| Low Power (<0.5 W) |

| Mid Power (0.5–1 W) |

| High Power (>1 W) |

| Exterior Lighting |

| Interior Lighting |

| Sensing / IR Applications |

| Other Applications (Signaling, minor) |

| Passenger Vehicles |

| Commercial Vehicles |

| United Kingdom |

| Germany |

| France |

| Rest of Europe |

| By Package Architecture | SMD (Surface Mount Device) |

| CSP (Chip Scale Package) | |

| Flip-Chip LED Packages | |

| COB (Chip-on-Board) | |

| By Power Class | Low Power (<0.5 W) |

| Mid Power (0.5–1 W) | |

| High Power (>1 W) | |

| By Application | Exterior Lighting |

| Interior Lighting | |

| Sensing / IR Applications | |

| Other Applications (Signaling, minor) | |

| By Vehicle Type | Passenger Vehicles |

| Commercial Vehicles | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Rest of Europe |

Key Questions Answered in the Report

How large will lighting content per BEV become by 2031?

Rising adoption of adaptive front lighting and immersive cabin ambient solutions is set to lift per-vehicle LED package content well above 2025 levels as OEMs shift toward software-defined lighting features.

Which LED package architecture is gaining traction fastest in Europe?

Chip-scale packages show the steepest growth thanks to their low thermal resistance and compact footprints that suit high-pixel adaptive beams.

What is the biggest hurdle for high-power headlamp LEDs?

Managing junction temperatures above 1 W power class remains critical because every 10 °C rise can double failure rates and jeopardize UN Regulation 112 compliance.

Why is France the fastest-growing market in this segment?

Government incentives, Stellantis electrification, and Valeo’s integrated lighting programs give France a 5.91% CAGR outlook through 2031.

How does the EU Carbon Border Adjustment Mechanism affect suppliers?

CBAM imposes embedded-carbon certificates on imported materials, increasing landed costs for Asian LED package makers and encouraging regional production shifts.

Which companies benefit most from replaceable LED source discussions?

Lumileds and other firms promoting modular LED engines stand to gain if UN regulations formalize field-serviceable lighting categories.

How large is the Europe automotive LED package market today?

It is valued at USD 0.44 billion in 2026 and is projected to reach USD 0.58 billion by 2031 at a 5.58% CAGR.

Page last updated on: