Aseptic Filling Machine Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

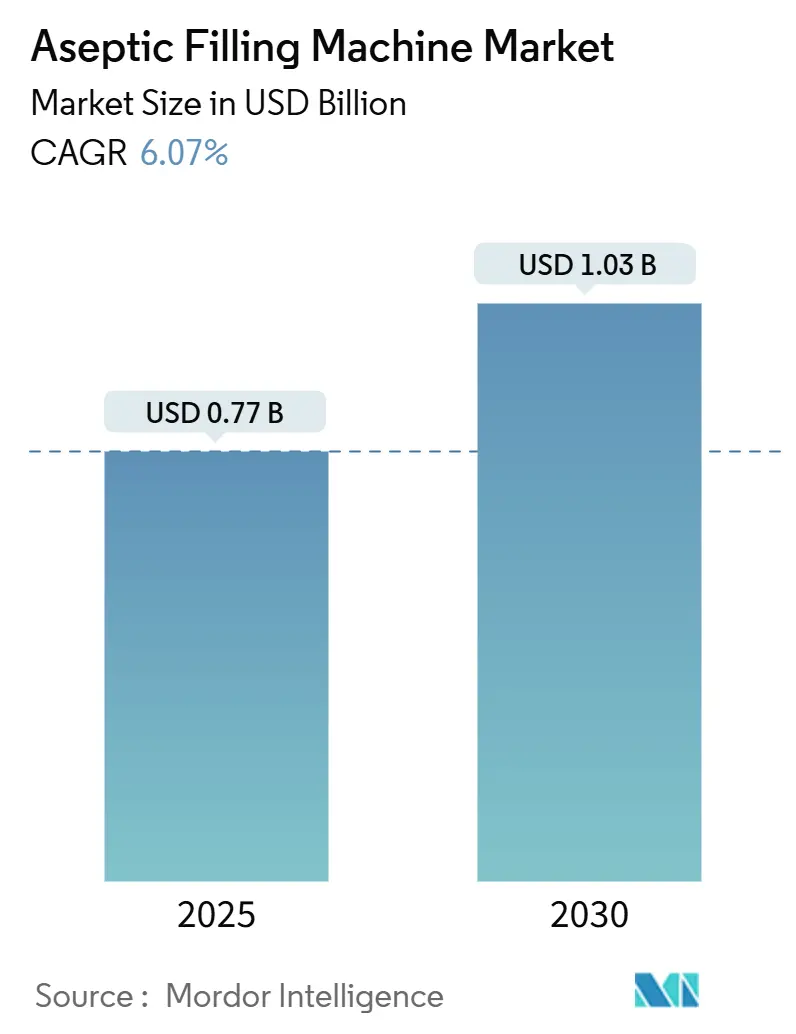

| Market Size (2025) | USD 0.77 Billion |

| Market Size (2030) | USD 1.03 Billion |

| Growth Rate (2025 - 2030) | 6.07% CAGR |

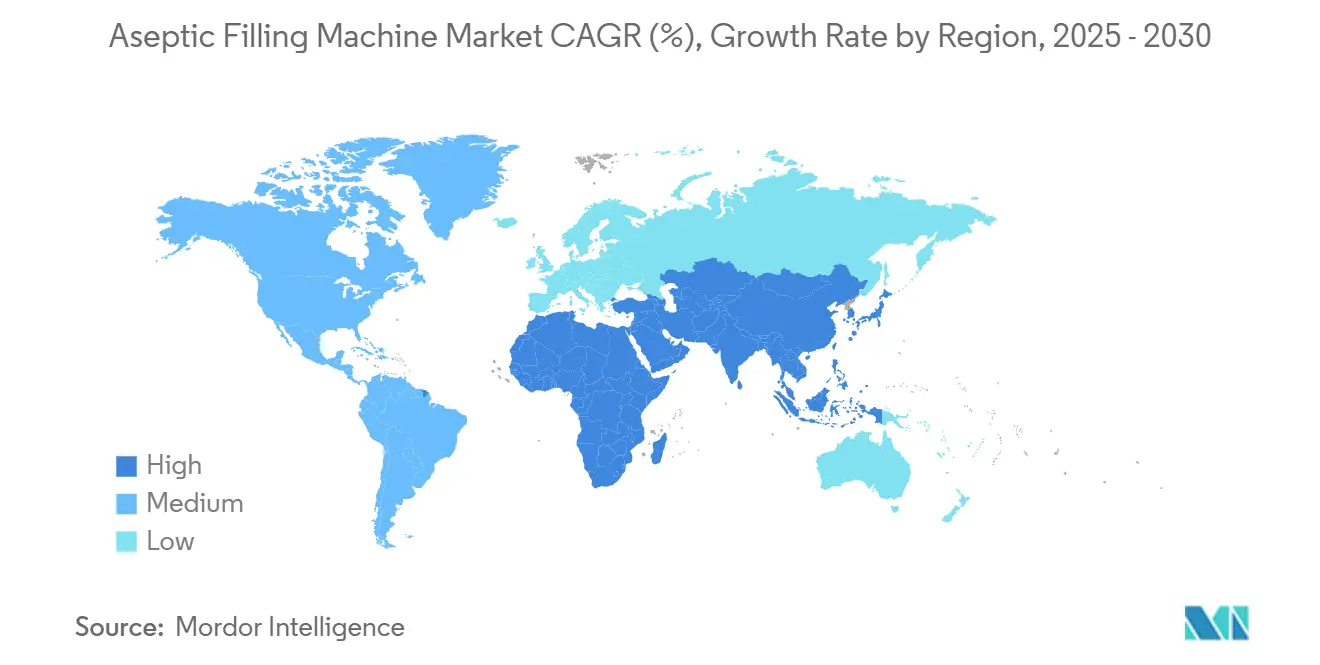

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

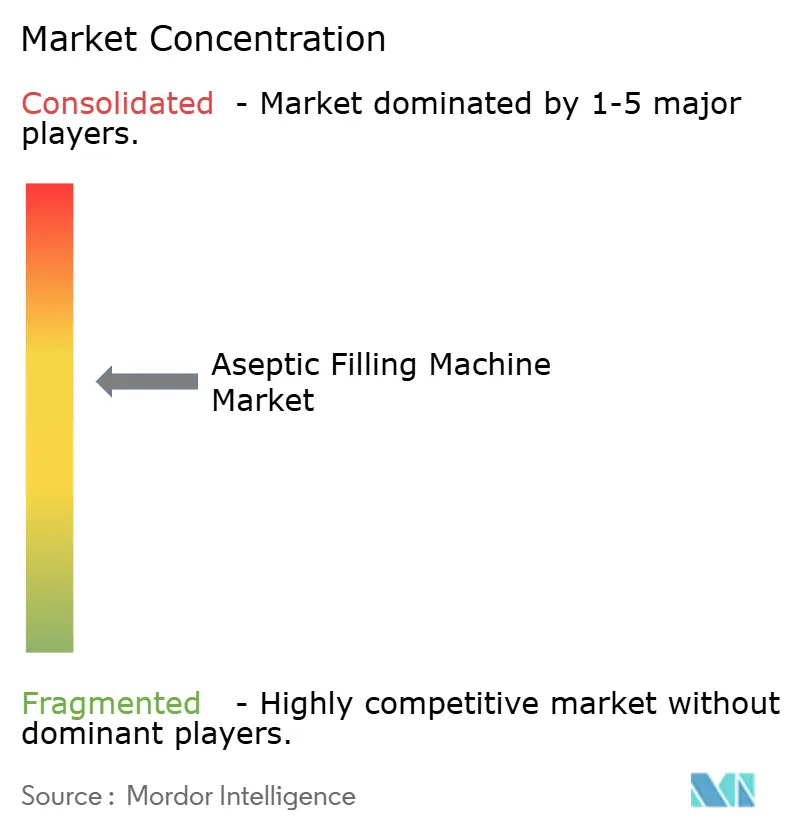

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aseptic Filling Machine Market Analysis by Mordor Intelligence

The aseptic filling machine market size reached USD 0.77 billion in 2025 and is forecast to climb to USD 1.03 billion by 2030, advancing at a 6.07% CAGR over the period. Continued adoption of biologics and mRNA-based vaccines, the pivot toward personalized medicine, and stricter global sterility rules keep capital flowing into next-generation barrier technologies. Equipment suppliers benefit from Annex 1’s wider scope, which pushes drug makers toward isolator lines and robotic workcells that cut human intervention to near zero. North American and European expansions, together with fast-growing Asia-Pacific capacity build-outs, channel demand toward versatile systems able to switch quickly between formats, volumes, and products. Competitive intensity remains moderate because high validation expertise and multimillion-dollar cleanroom outlays deter new entrants, yet specialized firms still capture niches such as micro-fill gene-therapy applications.

Key Report Takeaways

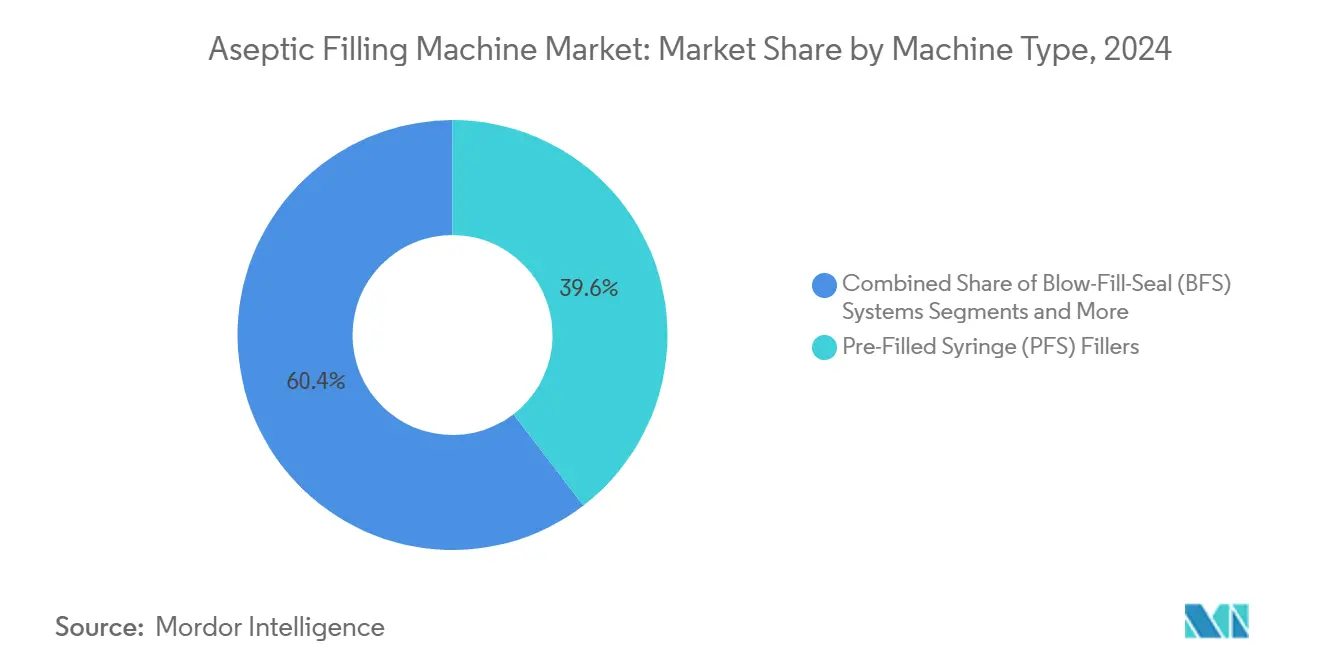

- By machine type, pre-filled syringe fillers held 39.57% of aseptic filling machine market share in 2024, whereas blow-fill-seal equipment is projected to grow at a 10.38% CAGR through 2030.

- By sterilization technology, isolator-based systems dominated with 46.59% share in 2024, while gloveless robotic isolators are on track for a 10.47% CAGR to 2030.

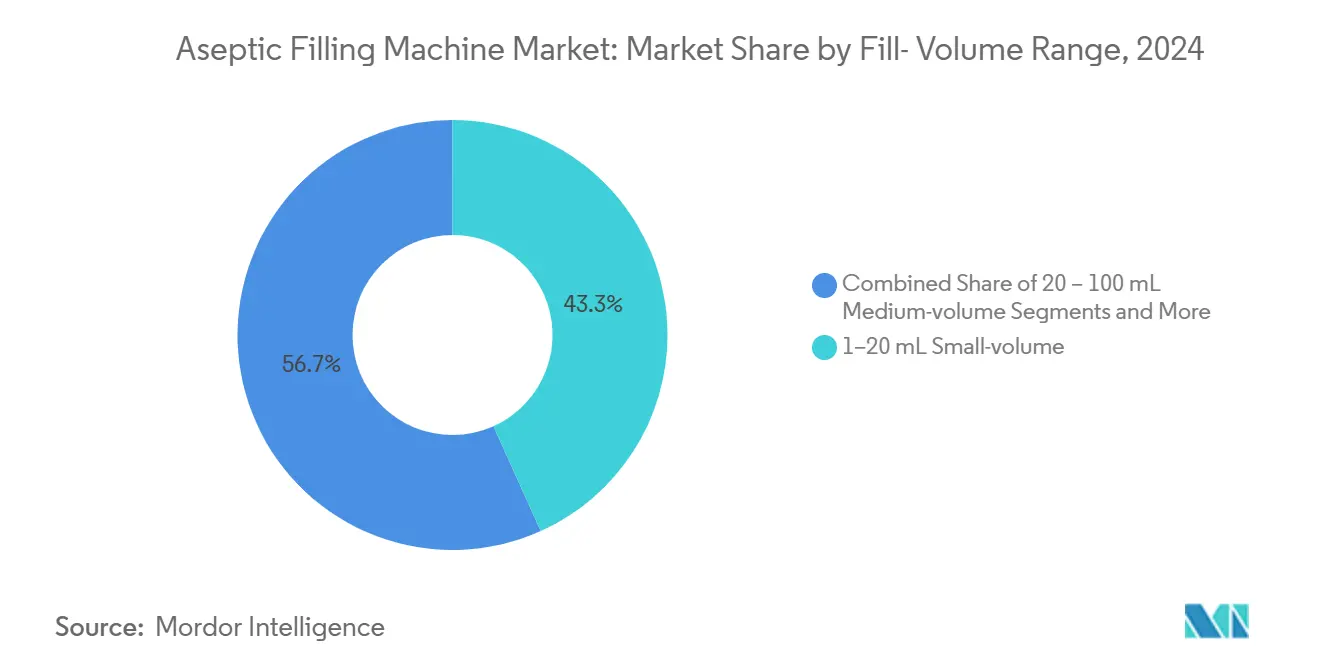

- By fill-volume range, 1-20 mL captured 43.26% of aseptic filling machine market size in 2024, but ≤1 mL micro-fills will expand at a 9.17% CAGR to the end of the decade.

- By end-user, CDMOs led with 34.72% share in 2024, and vaccine producers represent the fastest-growing customer group at 9.75% CAGR through 2030.

- North America commanded 37.33% of 2024 revenues, whereas Asia-Pacific is projected to post the highest regional CAGR at 8.36% to 2030.

Global Aseptic Filling Machine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Biologics & mRNA vaccine pipeline expansion | +1.8% | Global, strongest in North America & Europe | Medium term (2-4 years) |

| Oncology shift to ready-to-administer parenterals | +1.2% | North America & EU, spreading to Asia-Pacific | Medium term (2-4 years) |

| Outsourcing boom to CDMOs for fill-finish | +1.5% | Global, led by North America & Asia-Pacific | Short term (≤ 2 years) |

| Annex 1 sterility revisions tighten compliance | +0.9% | Primarily EU, global influence | Short term (≤ 2 years) |

| Robotic isolator lines cut contamination risk | +0.7% | Global, advanced economies first | Long term (≥ 4 years) |

| Personalized medicine needs flexible small-batch fillers | +0.6% | North America & EU, emerging Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Biologics & mRNA vaccine pipeline expansion

A once-in-a-generation biologics wave reshapes capacity planning, and every major mRNA site coming online now specifies closed robotic fillers designed for lipid nanoparticle suspensions.[1]Dan Stanton, “Moderna eyes mRNA manufacturing efficiencies as 3 plants set to come online in 2025,” BioProcess Insider, bioprocessinsider.comMolecules that denature quickly outside tight temperature bands need systems that eliminate manual touchpoints, so the aseptic filling machine market pivots toward isolator workcells with cryogenic compatibility. Cell and gene therapies intensify the push, calling for ultra-small batch runs measured in hundreds of vials rather than tens of thousands. Container suppliers respond by standardizing ready-to-use vials and cartridges that drop directly into robotic nests, further accelerating adoption. These structural shifts lock in steady multi-year demand for precision, low-volume solutions.

Oncology shift to ready-to-administer parenterals

Cancer care teams now prefer delivery formats that arrive pre-dosed and sterile, minimizing infusion-center preparation time and staff exposure.[2]Cytiva Life Sciences, “Cytotoxic Drug Filling – Cytiva,”, cytivalifesciences.com Antibody-drug conjugates and checkpoint inhibitors therefore move to pre-filled syringes and cartridges, boosting throughput requirements for dedicated PFS lines. The technology must also handle potent payloads safely, which drives investment in gloveless isolators combined with high-resolution inline inspection. As home-based treatment models emerge, patient-friendly device formats reinforce this path, keeping the aseptic filling machine market aligned with high-value small-volume assets.

Outsourcing boom to CDMOs for fill-finish capacity

Drug sponsors increasingly partner with contract developers to dodge nine-figure capital hurdles and tap specialist skill sets. CDMOs correspondingly upgrade to multi-format robotic suites able to swap between syringes, vials, and cartridges in hours rather than days. Standardized line architectures grant regulators clear validation dossiers across multiple clients, while shared utilities help amortize isolator costs. The outsourcing tide therefore sustains equipment orders even when individual pharma pipelines ebb and flow.

Annex 1 sterility revisions tighten compliance

Europe’s 2023 Annex 1 update extends risk-based sterility rules worldwide, effectively making barrier technology compulsory for new facilities. Manufacturers now document contamination-control strategies in detail, proving first-air integrity at the exact fill point. Legacy RABS set-ups and conventional cleanrooms thus face retrofit projects or full replacement, funneling procurement toward isolator platforms with automated decontamination cycles. The directive also favors inline analytics and data-rich electronic batch records, entwining equipment upgrades with digital systems integration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High isolator / Grade A cleanroom capital cost | -1.3% | Global, hardest on small manufacturers | Short term (≤ 2 years) |

| Skill shortage in aseptic validation & QA | -0.8% | North America & Europe, rising Asia-Pacific | Medium term (2-4 years) |

| Complex multi-format changeovers drive downtime | -0.6% | Global multi-product facilities | Medium term (2-4 years) |

| Cold-chain alternative technologies | -0.4% | Developed markets first | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High isolator / Grade A cleanroom capital cost

New isolator lines typically run USD 10-15 million each and require extensive building upgrades, a financial wall that many early-stage biotechs cannot climb. Even after installation, yearly validation and maintenance fees consume sizeable operating budgets. Companies with limited portfolios often turn to CDMOs to sidestep the burden, reinforcing outsourcing cycles yet slowing direct equipment purchases from smaller license holders. Vendors respond with modular skid offerings, but sticker shock remains a headwind for broad deployment.

Skill shortage in aseptic validation & QA

Four out of five manufacturers report gaps in automation and sterility-assurance know-how, lengthening project schedules and driving salary inflation for scarce talent.[3]Rana Faqihi, “A Methodology for Identifying Current and Future Skills Gaps,” BioProcess International, bioprocessinternational.comAs lines become more robotic and data-driven, expertise now spans software, analytics, and traditional microbiology. Training pipelines struggle to catch up, and knowledge drain through retirements compounds the shortfall. Without seasoned specialists, firms delay tech transfers and slow capitalization decisions, weighing on aseptic filling machine market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Precision syringes remain dominant while BFS accelerates

Pre-filled syringe fillers captured 39.57% of 2024 revenues, reflecting healthcare’s pivot to ready-to-inject therapies that cut dosing errors and speed administration. Capacity additions such as Syntegon’s MLD Advanced platform, capable of 400 units per minute, reinforce this leadership. Many biologics sponsors now standardize on nested tub formats that simplify sterilization logistics. In contrast, blow-fill-seal lines post a 10.38% CAGR because their one-step container formation and filling lowers contamination risk and cost per dose, a critical factor for high-volume generics. High-output BFS modules process up to 33,000 containers hourly while occupying smaller cleanroom footprints, appealing to cost-sensitive vaccine and saline producers.

Aseptic filling machine market size for vial and cartridge equipment stays resilient, especially in clinical trial supply where format versatility outweighs mass-production efficiency. Lyophilization-integrated fillers carve a niche in products needing freeze-dried stability, and IV-bag lines remain staples for inpatient fluid therapy. Yet the pace of investment tilts toward platforms that can scale from pilot to commercial runs without major retrofits, supporting continued BFS share gains.

By Sterilization Technology: Isolator security with robotic momentum

Isolator-based systems held 46.59% of 2024 spend, anchored by regulators’ preference for closed barriers that guarantee Grade A conditions at the critical zone. Robust decontamination cycles and integrated particle monitoring satisfy Annex 1’s stringent documentation demands. This dominance underpins the aseptic filling machine market share for suppliers offering turnkey isolator suites paired with line-side environmental data analytics.

Gloveless robotic isolators, though a smaller installed base, grow at 10.47% CAGR as manufacturers chase zero-touch production. Platforms such as Cytiva’s SA25 consistently meet 99.5% quality-acceptance thresholds while freeing operators from cumbersome glove-port workflows. RABS provide an intermediate step for refurbishing legacy plants, but forward-looking projects increasingly budget for full isolator containment to future-proof assets.

By Fill-Volume Range: Small volumes dominate, micro-fills surge

The 1-20 mL bracket accounts for 43.26% of aseptic filling machine market size, a testament to the prevalence of monoclonal antibodies, insulin, and specialty injectables that fall within this range. Versatile nests handle syringes and vials interchangeably, letting firms align presentation with therapy-area norms. Medium-volume and large-volume parenteral fillers continue serving critical-care infusions, yet capital intensity has shifted toward precision dosing systems.

Micro-fills of ≤ 1 mL expand at 9.17% CAGR, propelled by gene-editing vectors and autologous cell doses that require only tens of microliters per patient. Accurate dispense down to ±1 % becomes essential, pushing machine builders to adopt high-resolution peristaltic pumps and inline weigh-check algorithms. These projects often pair with cryogenic tunnels, intertwining filling technology choices with supply-chain temperature strategies.

By End-User: CDMOs anchor growth; vaccine players accelerate

CDMOs booked 34.72% of 2024 equipment outlays as brand-name drug sponsors pursued asset-light models while retaining rapid access to qualified capacity. Multi-tenant facilities demand format-flexible lines plus digital batch records that segregate client data securely. In turn, vendors embed recipe-driven control layers that slash changeover times and simplify audit trails, reinforcing outsourcing appeal.

Vaccine producers post the sharpest rise at 9.75% CAGR because governments fund pandemic preparedness and routine immunization drives. End-to-end biologics clusters in India and China now order complete fill-finish suites to pair with upstream bioreactors, expanding the geographic footprint of high-grade isolator technology. Big pharma maintains sizeable internal networks for flagship brands, while hospital compounding centers invest selectively in tabletop micro-batch fillers for personalized dosing needs.

Geography Analysis

North America retained 37.33% of 2024 revenue, sustained by headline projects such as Novo Nordisk’s USD 4.1 billion Clayton build-out and Eli Lilly’s parallel investments in advanced injectable lines. Robust FDA oversight and ready access to skilled engineers shorten validation cycles, encouraging sustained domestic manufacturing despite wage inflation. Canada leverages government co-funding to entice biologics expansions, and Mexico offers cost-competitive packaging hubs that feed the continental supply chain.

Europe stands as the second-largest contributor, buoyed by Annex 1’s regulatory clarity and Germany’s emergence as a fill-finish hotspot. Investments from Sanofi, Boehringer Ingelheim, and Stevanato drive localized equipment demand, while Italy and Switzerland anchor contract manufacturing clusters. The aseptic filling machine market there benefits from deep engineering talent and cross-border logistical networks, even as Brexit introduces customs frictions that firms counter by duplicating capacity.

Asia-Pacific records the fastest trajectory at 8.36% CAGR, where China’s biopharma stimulus packages and India’s production-linked incentives spark a wave of isolator-based green-fields. Local CDMOs raise standards to win multinational projects, importing Western robotics yet pricing competitively. Japan and South Korea invest in precision automation to safeguard quality reputations, and Australia positions itself as an mRNA hub serving Southeast Asia. Overall, diversified sourcing strategies amplify capital deployment across the region, underpinning global uptake of aseptic filling technology.

Competitive Landscape

The aseptic filling machine industry exhibits moderate consolidation. Market leaders such as Syntegon, IMA, and Rommelag capitalize on decades-old validation libraries and multiple service centers, assuring clients of post-installation uptime. Syntegon posted an 11% jump in 2024 order intake and broadened its robotics offer through targeted acquisitions, illustrating how scale and specialization blend to widen moats. Yet private-equity activity, highlighted by Novo Holdings’ USD 11 billion Catalent buyout, signals outside capital’s confidence in the sector’s growth visibility.

Differentiation now hinges on digital twins, predictive maintenance, and modular designs that trim installation windows. Emerging challengers focus on cell-therapy micro-batch lines and decentralized production carts, carving footholds that larger firms may eventually absorb. Regional expansions continue: European incumbents open U.S. demo labs, and Asian players license Western IP to ride domestic demand. Customer loyalty skews toward suppliers capable of long-term lifecycle support, cementing a competitive field where service quality rivals mechanical innovation.

Aseptic Filling Machine Industry Leaders

Syntegon Technology

Bausch + Ströbel

IMA Group

Groninger

Optima Pharma

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Syntegon introduced the Pharmatag 2025 line, integrating advanced liquid-handling modules aimed at precision biologics filling.

- April 2025: Syntegon rolled out the MLD Advanced RTU syringe filler, achieving 400-unit-per-minute throughput with enhanced inline controls.

- May 2024: Stevanato Group inaugurated a Cisterna di Latina facility to expand EZ-fill syringe output.

- March 2024: Argonaut Manufacturing Services invested USD 45 million in isolator-based syringe and cartridge capacity in California.

Global Aseptic Filling Machine Market Report Scope

| Vial & Cartridge Fill-Finish Lines |

| Pre-Filled Syringe (PFS) Fillers |

| Blow-Fill-Seal (BFS) Systems |

| IV-Bag / Large-Volume Parenteral Fillers |

| Lyophilization-Integrated Fillers |

| Isolator-Based Systems |

| RABS (Restricted Access Barrier System) |

| Gloveless Robotic Isolators |

| Conventional Cleanroom Lines |

| Less Than and Equal To 1 mL Micro-fills |

| 1 – 20 mL Small-volume |

| 20 – 100 mL Medium-volume |

| More Than 100 mL Large-volume Parenteral |

| Big Pharma Manufacturers |

| Contract Development & Manufacturing Organizations (CDMOs) |

| Vaccine Producers |

| Biotechnology & Start-ups |

| Hospital/Compounding Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Machine Type | Vial & Cartridge Fill-Finish Lines | |

| Pre-Filled Syringe (PFS) Fillers | ||

| Blow-Fill-Seal (BFS) Systems | ||

| IV-Bag / Large-Volume Parenteral Fillers | ||

| Lyophilization-Integrated Fillers | ||

| By Sterilization/Barriering Technology | Isolator-Based Systems | |

| RABS (Restricted Access Barrier System) | ||

| Gloveless Robotic Isolators | ||

| Conventional Cleanroom Lines | ||

| By Fill Volume Range | Less Than and Equal To 1 mL Micro-fills | |

| 1 – 20 mL Small-volume | ||

| 20 – 100 mL Medium-volume | ||

| More Than 100 mL Large-volume Parenteral | ||

| By End-user | Big Pharma Manufacturers | |

| Contract Development & Manufacturing Organizations (CDMOs) | ||

| Vaccine Producers | ||

| Biotechnology & Start-ups | ||

| Hospital/Compounding Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the aseptic filling machine market in 2025?

The aseptic filling machine market size reached USD 0.77 billion in 2025.

What is the forecast CAGR for aseptic filling equipment through 2030?

The market is projected to post a 6.07% CAGR from 2025 to 2030.

Which machine type leads current sales?

Pre-filled syringe fillers command 39.57% of 2024 revenue thanks to ready-to-inject biologics.

Which region grows fastest over the forecast period?

Asia-Pacific shows the highest growth, advancing at an expected 8.36% CAGR to 2030.

Why are CDMOs important buyers of aseptic fillers?

CDMOs captured 34.72% share in 2024 as drug sponsors outsource fill-finish to avoid large capital spends and tap specialist expertise.

What technology trend is reshaping sterility assurance?

Gloveless robotic isolators are rising quickly, projected at a 10.47% CAGR, because they eliminate direct human contact and cut contamination risk.

Page last updated on: