Aesthetic Fillers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

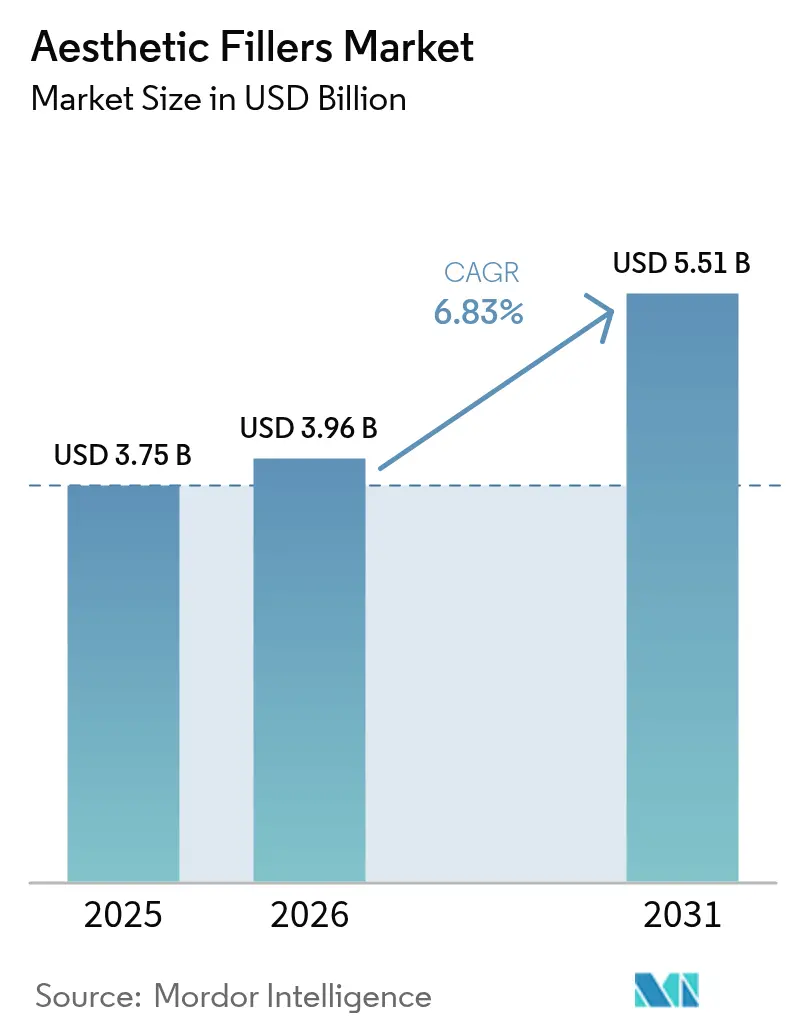

| Market Size (2026) | USD 3.96 Billion |

| Market Size (2031) | USD 5.51 Billion |

| Growth Rate (2026 - 2031) | 6.83% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aesthetic Fillers Market Analysis by Mordor Intelligence

The Aesthetic Fillers Market size is expected to grow from USD 3.75 billion in 2025 to USD 3.96 billion in 2026 and is forecast to reach USD 5.51 billion by 2031 at 6.83% CAGR over 2026-2031.

Accelerated consumer pivot toward minimally invasive rejuvenation, a surge in AI-guided injection planning, and fast-rising male participation are expanding the addressable base and shortening treatment cycles. U.S. physicians now perform 5.3 million hyaluronic-acid filler sessions annually, signaling that injectables have moved from episodic cosmetic events to routine self-care.[1]American Society of Plastic Surgeons, “Plastic Surgery Statistics Report 2024,” American Society of Plastic Surgeons, plasticsurgery.org Regenerative formulations blending stem-cell exosomes with traditional polymers promise longer-lasting volume and higher patient lifetime value, while the FDA’s vigilance on adverse-event clusters is elevating compliance costs for manufacturers.[2]U.S. Food and Drug Administration, “Safety Communication: FDA Warns About Rare but Serious Complications of Dermal Fillers,” U.S. Food and Drug Administration, fda.gov Competitive dynamics are intensifying as Asian entrants deploy low-cost fermentation-derived HA and direct-to-clinic logistics to undercut Western brands, even as gray-market proliferation threatens patient safety and premium pricing.

Key Report Takeaways

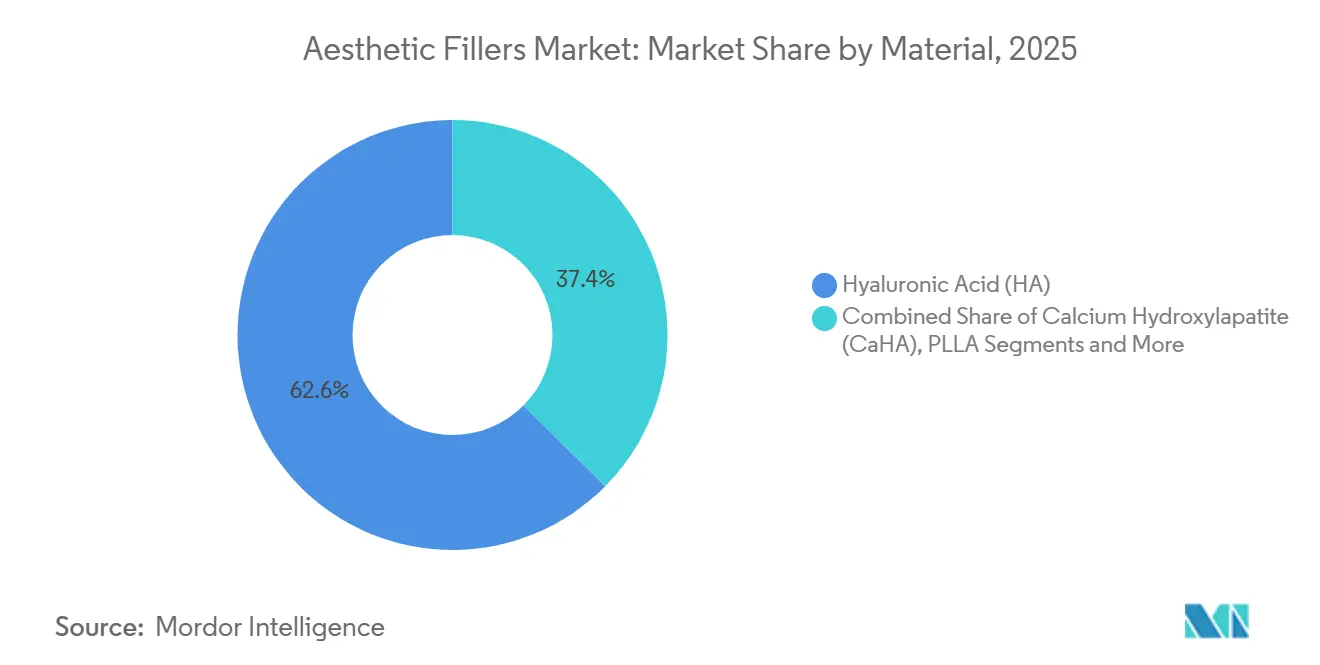

- By material, hyaluronic acid led with 62.57% of the aesthetic filler market share in 2025, while poly-L-lactic acid is projected to post a 10.53% CAGR through 2031.

- By application, facial line correction held 44.72% of revenue in 2025; facial contouring and volume restoration is advancing at a 9.25% CAGR to 2031.

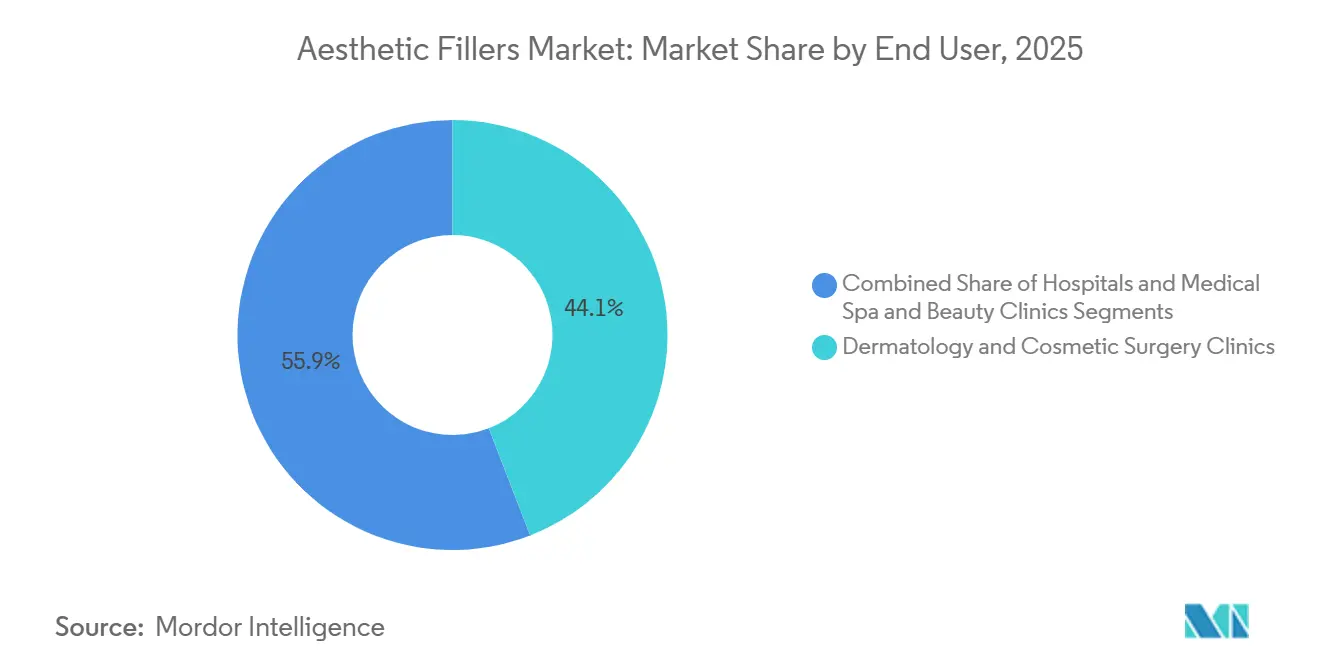

- By end user, dermatology and cosmetic surgery clinics captured 44.11% of 2025 sales, whereas medical spas and beauty clinics are expected to expand at an 8.62% CAGR over the forecast period.

- By gender, female patients accounted for 81.46% of injections in 2025, and male demand is rising at an 8.24% CAGR through 2031.

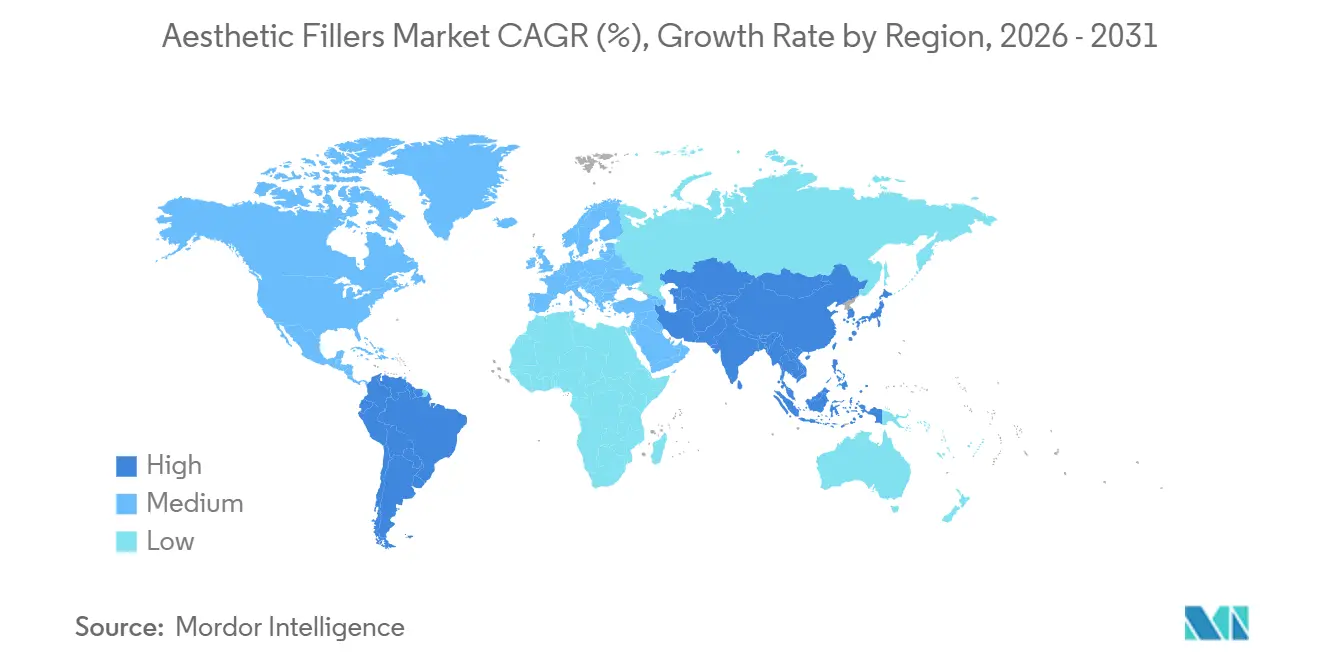

- By geography, North America generated 34.83% of global revenue in 2025; Asia-Pacific is forecast to grow fastest at a 9.04% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aesthetic Fillers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Minimally Invasive Cosmetic Procedures | +1.8% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Aging Population Seeking Anti-Ageing Solutions | +1.5% | Japan, South Korea, Western Europe, North America | Long term (≥ 4 years) |

| Growing Disposable Incomes in Emerging Economies | +1.2% | China, India, Southeast Asia, GCC, Brazil, Mexico | Medium term (2-4 years) |

| Regenerative-Medicine Fillers with Stem-Cell Matrices | +0.9% | North America, Europe, South Korea, Japan | Long term (≥ 4 years) |

| Male-Focused Aesthetic Marketing | +0.7% | United States, United Kingdom, South Korea, urban China | Medium term (2-4 years) |

| AI-Assisted Injection Planning & 3D Analytics | +0.6% | North America, Europe, South Korea, Japan, Singapore | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Minimally Invasive Cosmetic Procedures

Practitioners and patients favor fillers over surgical facelifts because downtime drops from weeks to hours, a trade-off that resonates when work and social calendars leave little recovery space. Millennials and Gen Z seek preventive volumization in their late twenties, expanding lifetime treatment cycles and smoothing clinic revenue. FDA pre-market approvals create a quality floor, yet enforcement gaps allow gray-market syringes to persist online. Technology-driven consultation tools reduce chair time and help practices scale volume without proportionate labor increases. Collectively, these forces keep the aesthetic filler market on a double-digit procedure-growth trajectory even when macroeconomics soften discretionary budgets.

Aging Population Seeking Anti-Ageing Solutions

Japan’s health ministry projects that 31% of its residents will be 65 or older by 2030, and similar demographic inversion is unfolding in Western Europe. Older consumers use facial fillers to align appearance with extended careers and active retirement lifestyles. Poly-L-lactic acid attracts this cohort because it triggers collagen synthesis lasting up to 24 months, outpacing HA’s durability.[3]Roberta Signori, “Poly-L-Lactic Acid for Facial Rejuvenation: A Systematic Review,” Journal of Cosmetic Dermatology, onlinelibrary.wiley.com Pension assets cushion out-of-pocket spending, while social acceptance of “aging well” lowers stigma. Clinics exploit this demand with bundled annual maintenance plans that lock in repeat visits and stable cash flow.

Growing Disposable Incomes in Emerging Economies

The Chinese regulator approved multiple domestic HA brands in 2025, cutting syringe prices by roughly 30% and widening access. India and Southeast Asia see similar middle-class expansions, although supply bottlenecks and uneven enforcement slow market maturity. Saudi Arabia and the UAE court medical tourists with luxury filler-and-spa packages, knitting injectables into broader hospitality revenue. Latin America, led by Brazil, benefits from cultural acceptance of cosmetic enhancement and a dense dermatologist network, even as currency swings periodically dent volume. Combined, these regions inject momentum into the global aesthetic filler market.

Regenerative-Medicine Fillers with Stem-Cell Matrices Gaining Traction

A 2024 trial showed that exosome-enriched HA raised dermal thickness by 18% at six months versus HA-only controls, catalyzing Phase II studies at Revance and peer biotechs. By recruiting the body’s repair pathways, regenerative fillers aim to stretch treatment intervals to two years, a consumer value proposition that could reset pricing power. Regulatory hurdles remain steep because the FDA treats cell-derived components as biologics, demanding GMP-grade manufacturing proof. Early adopters in South Korea and Japan bundle these fillers with autologous fat transfer, positioning the service as both aesthetic and anti-ageing therapy. Commercial scale will hinge on consistent cell-processing protocols and payer attitudes toward biologic pricing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse Events & Stricter Regulatory Scrutiny | -0.9% | North America, Europe, select Asia-Pacific markets | Short term (≤ 2 years) |

| High Procedure Costs in Price-Sensitive Markets | -0.6% | India, Southeast Asia, Latin America (ex-Brazil), Sub-Saharan Africa | Medium term (2-4 years) |

| Supply-Chain Risk for HA Raw Materials | -0.5% | North America, Europe | Medium term (2-4 years) |

| Proliferation of Counterfeit & Gray-Market Fillers | -0.7% | Global e-commerce, tourism hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Adverse Events & Stricter Regulatory Scrutiny

Vascular occlusion remains the gravest filler complication; 58% of affected patients lose vision permanently, prompting FDA safety communications and EU annual safety-report mandates. National seizures of counterfeit vials reached 4,700 in the United Kingdom by August 2025. Compliance costs escalate as manufacturers submit real-world performance data and fund practitioner-training grants. Small brands without regulatory teams face margin compression, nudging market consolidation.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety concerns and adverse event reports | -0.8% | North America, Europe, Global online patient communities | Short term (≤ 2 years) |

| Regulatory variability and approval delays | -0.6% | China, India, Latin America, Other emerging markets | Medium term (2-4 years) |

| High procedure costs in price-sensitive markets | -0.5% | Africa, South & Southeast Asia, Latin America | Long term (≥ 4 years) |

| Presence of counterfeit and low-quality products | -0.4% | Unregulated channels in Asia-Pacific, Eastern Europe, Latin America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Procedure Costs in Price-Sensitive Markets

A single HA syringe costs USD 500-1,200 in developed economies, far above average monthly wages in India and parts of Latin America. Financing plans exist but carry double-digit interest, deterring younger clients. Domestic Chinese and Korean brands shave costs but fight perception that low price equals low safety. Economic slowdowns produce immediate volume drops because insurance rarely covers cosmetic injectables.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: HA Dominance Meets Biostimulatory Innovation

Hyaluronic acid captured 62.57% of the aesthetic filler market share in 2025 owing to reversibility and broad indications. Poly-L-lactic acid leads growth at a 10.53% CAGR, buoyed by Galderma’s 2024 Sculptra acquisition and clinical proof of 24-month collagen stimulation. Calcium hydroxylapatite enjoys renewed interest in hyper-dilute protocols for skin quality, while PMMA remains niche due to permanence risks.

Regenerative blends that add stem-cell exosomes to HA promise to extend the aesthetic filler market size for premium biostimulatory offerings. FDA biologic classification hikes regulatory hurdles, yet early South Korean adopters report higher patient retention. Self-cross-linked HA removes BDDE but requires rigorous batch control. Material-choice diversity widens practitioner toolkits and cushions market growth against any single polymer’s regulatory shock.

By Application: Contouring Overtakes Line Correction

Facial line correction held 44.72% of 2025 revenue, but contouring and volume restoration is growing at 9.25% CAGR as millennials seek preventive structure in the aesthetic filler market. Lip enhancement remains visible, although subtle reshaping replaces earlier dramatic trends.

Liquid facelift protocols that deploy multiple syringes across cheeks, jawline, and temples raise per-visit spend, pushing up the aesthetic filler market size per patient episode. FDA approval of under-eye formulas opened a challenging yet lucrative anatomical niche. Off-label nose and chin sculpting expands use cases but demands advanced anatomy skills to avoid vascular events.

By End User: Medical Spas Disrupt Traditional Clinics

Dermatology and cosmetic surgery clinics owned 44.11% of 2025 sales, yet medical spas and beauty clinics are advancing at an 8.62% CAGR, leveraging hospitality aesthetics and retail convenience. Variable physician-supervision laws in the United States let some facilities operate with remote oversight, cutting overhead.

Hospitals play a marginal role outside reconstructive indications, so the aesthetic filler market shifts toward boutique, experience-driven settings. Rising adverse events in loosely regulated spas have spurred professional societies to demand standardized injector credentials. Nonetheless, consumer appetite for comfort and flexibility keeps the channel on a steep climb.

By Gender: Male Segment Closes the Gap

Women represented 81.46% of procedures in 2025, but male uptake is climbing at 8.24% CAGR, narrowing the gap. Executive wellness programs, influencer normalization, and performance-oriented marketing reshape perceptions. Men prioritize subtle jaw and tear-trough corrections and prefer lower-viscosity gels.

Cultural resistance persists in conservative regions, yet urban professionals under 40 treat fillers like fitness or tailored suits. Manufacturers tailor viscosity and packaging aesthetics to masculine preferences, reinforcing growth and contributing incremental gains to the aesthetic filler market size.

Geography Analysis

North America generated 34.83% of global revenue in 2025, underpinned by robust per-capita spend, broad FDA approvals, and 5.3 million HA sessions logged in 2024. Canada mirrors U.S. pathways but varies injector scope by province. Mexico draws cost-conscious U.S. tourists, although counterfeit risks temper volumes. Ongoing FDA e-commerce crackdowns highlight enforcement gaps in cross-border sales.

Asia-Pacific is projected to grow at 9.04% CAGR, led by China’s domestic-brand approvals that slice syringe prices by 30%. South Korea funnels medical tourists into AI-enabled 3D scanning clinics, while Japan’s aging demographics sustain premium collagen-induction demand despite cultural caution. India’s Central Drugs Standard Control Organisation is modernizing trials, yet income disparity limits conversion rates. Australia’s tight post-market surveillance positions it as a regional quality gatekeeper.

Europe shows steady but slower growth as the EMA intensifies post-market reporting. Germany, France, and the United Kingdom anchor demand, backed by partial reimbursement for reconstructive uses. The UK regulator seized 4,700 counterfeit vials by August 2025, illustrating the region’s vigilance. In the Middle East, Saudi Arabia and the UAE leverage Vision 2030 tourism strategies to bundle fillers with luxury services. Latin America remains dominated by Brazil’s culturally normalized filler culture, while Argentina and Chile face macro-volatility headwinds.

Competitive Landscape

AbbVie’s Allergan Aesthetics, Galderma, and Merz Pharma collectively control major share of revenue, positioning the aesthetic filler market as moderately concentrated. Galderma’s CHF 2.2 billion IPO in 2024 funds geographic expansion and product acquisitions like Sculptra. Allergan’s Juvéderm portfolio spans eight SKUs, fortified by loyalty programs that offer rebates and certified-training modules. Merz differentiates with Radiesse hyper-dilute protocols and a double-purified neurotoxin.

Asian entrants such as Bloomage, Huons, and Croma-Pharma lean on cost advantage and direct-to-clinic distribution, appealing to price-sensitive spas. Revance’s 2024 Opul buyout signals a push toward bundled neuromodulator-and-filler packages. Technology adoption now separates leaders from laggards: AI planning tools and blockchain traceability win clinic mindshare and reduce counterfeit risk, yet uptake varies by capital availability.

Aesthetic Fillers Industry Leaders

Galderma

AbbVie Inc.

Merz Pharma

Ipsen

Revance Therapeutics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Galderma announced FDA acceptance of its BLA resubmission for RelabotulinumtoxinA to treat glabellar and canthal lines.

- February 2026: Merz Aesthetics marked 15 years of XEOMIN approval and launched a year-of-treatments giveaway via the Xperience+ loyalty platform.

- January 2026: Huons Biopharma’s partner IMeik secured Chinese NMPA registration for Hutox, expanding neurotoxin options in China.

- September 2025: Allergan Aesthetics debuted “The One & Only” multichannel campaign to reinforce BOTOX Cosmetic’s category leadership.

Global Aesthetic Fillers Market Report Scope

Dermal fillers, or aesthetic fillers, are gel-like injectables made of hyaluronic acid, used to restore volume, smooth lines, and enhance facial contours, with effects lasting 6 to 18 months.

The Aesthetic Filler Market Report is segmented by Material, Application, End User, Gender, and Geography. By Material, the market is segmented into Hyaluronic Acid, Calcium Hydroxylapatite, Poly‑L‑lactic Acid, Polymethyl‑methacrylate, Collagen, and Others. By Application, the market is segmented into Facial Line Correction, Lip Enhancement, Facial Contouring/Volume Restoration, Scar & Acne Mark Revision, and Others. By End User, the market is segmented into Dermatology & Cosmetic Surgery Clinics, Hospitals, and Medical Spa & Beauty Clinics. By Gender, the market is segmented into Female and Male. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Hyaluronic Acid (HA) |

| Calcium Hydroxylapatite (CaHA) |

| Poly-L-lactic Acid (PLLA) |

| Polymethyl-methacrylate (PMMA) |

| Collagen & Others |

| Facial Line Correction |

| Lip Enhancement |

| Facial Contouring / Volume Restoration |

| Scar & Acne Mark Revision |

| Others |

| Dermatology & Cosmetic Surgery Clinics |

| Hospitals |

| Medical Spa & Beauty Clinics |

| Female |

| Male |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material | Hyaluronic Acid (HA) | |

| Calcium Hydroxylapatite (CaHA) | ||

| Poly-L-lactic Acid (PLLA) | ||

| Polymethyl-methacrylate (PMMA) | ||

| Collagen & Others | ||

| By Application | Facial Line Correction | |

| Lip Enhancement | ||

| Facial Contouring / Volume Restoration | ||

| Scar & Acne Mark Revision | ||

| Others | ||

| By End User | Dermatology & Cosmetic Surgery Clinics | |

| Hospitals | ||

| Medical Spa & Beauty Clinics | ||

| By Gender | Female | |

| Male | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is global demand for dermal injectables growing through 2031?

Global procedure volume is projected to rise at a 6.83% CAGR, lifting the aesthetic filler market size from USD 3.96 billion in 2026 to USD 5.51 billion by 2031.

Which material currently dominates filler usage worldwide?

Hyaluronic acid leads, holding 62.57% of 2025 revenue because clinicians value its reversibility and wide FDA-approved indications.

What geography is expanding fastest?

Asia-Pacific is forecast to log a 9.04% CAGR through 2031, driven by China’s domestic approvals and South Korea’s medical-tourism ecosystem.

Why are regenerative fillers gaining attention?

Early trials show stem-cell exosome–enriched fillers can extend dermal thickness for 18-24 months, potentially halving the frequency of repeat injections.

Are male patients a significant growth vector?

Yes. Male procedures are advancing at an 8.24% CAGR as workplace video calls and performance-oriented marketing normalize subtle contouring.

What is the biggest regulatory challenge right now?

Counterfeit and gray-market injectables are prompting global crackdowns that raise compliance costs and threaten patient safety.

Page last updated on: