Injection Pen Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

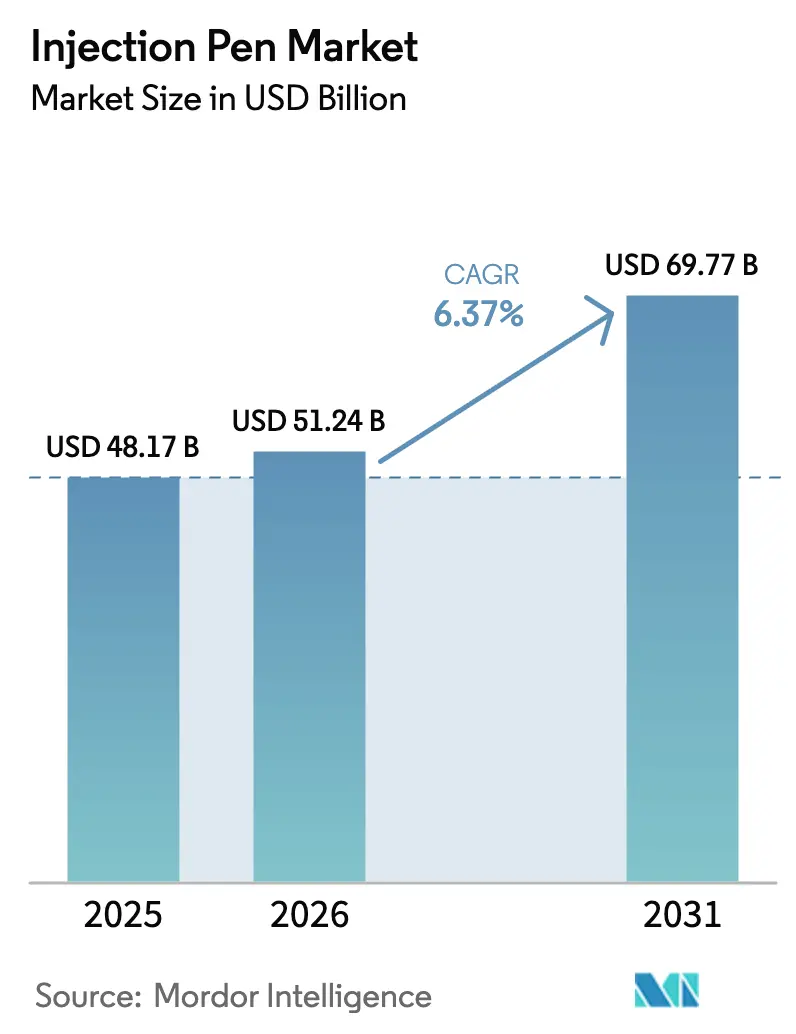

| Market Size (2026) | USD 51.24 Billion |

| Market Size (2031) | USD 69.77 Billion |

| Growth Rate (2026 - 2031) | 6.37% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

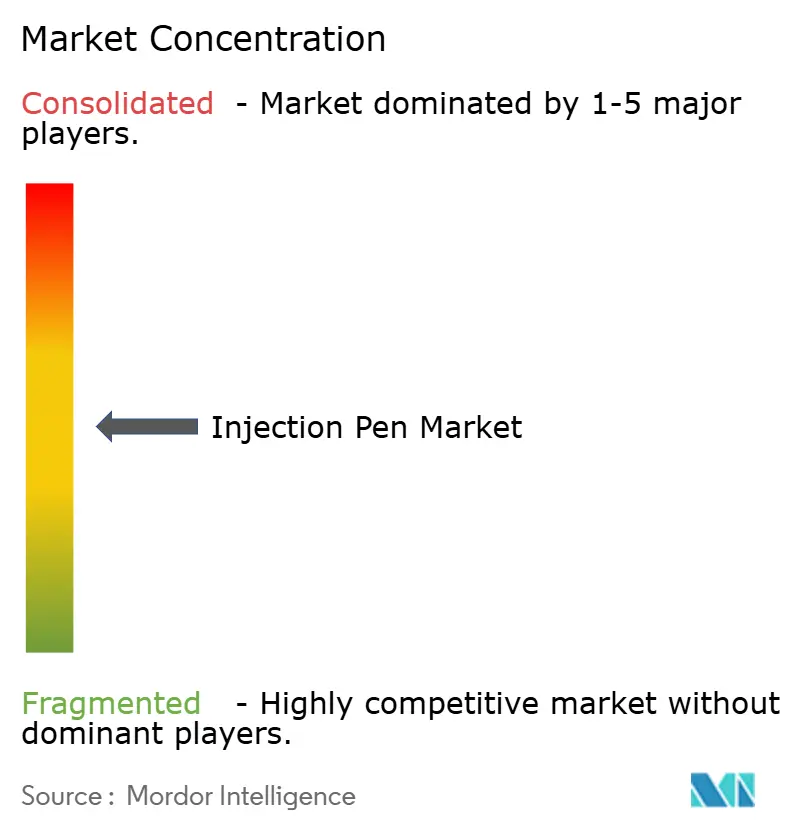

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Injection Pen Market Analysis by Mordor Intelligence

The Injection Pen Market size was valued at USD 48.17 billion in 2025 and estimated to grow from USD 51.24 billion in 2026 to reach USD 69.77 billion by 2031, at a CAGR of 6.37% during the forecast period (2026-2031).

Demand is accelerating as diabetes prevalence rises, high-viscosity biologics fill late-stage pipelines, and connected health ecosystems embed self-administration into chronic-care pathways. Smart, reusable formats gain momentum because they enable payer-mandated outcome tracking, mitigate sustainability concerns, and lower per-dose costs. Competitive intensity is building around GLP-1 and GIP drug classes, where injection pen compatibility remains critical despite exploratory moves toward oral alternatives. Supply-chain pressure on pharmaceutical-grade polymers and strict cybersecurity rules under FDA Section 524B elevate barriers to entry, steering market power toward vertically integrated manufacturers capable of global regulatory compliance.

Key Report Takeaways

- By product type, disposable pens accounted for 64.12% of injection pen market share in 2025, while smart/connected devices are expanding at an 10.83% CAGR through 2031.

- By indication, diabetes held 70.68% share of the injection pen market size in 2025, whereas autoimmune diseases are forecast to record a 9.82% CAGR to 2031.

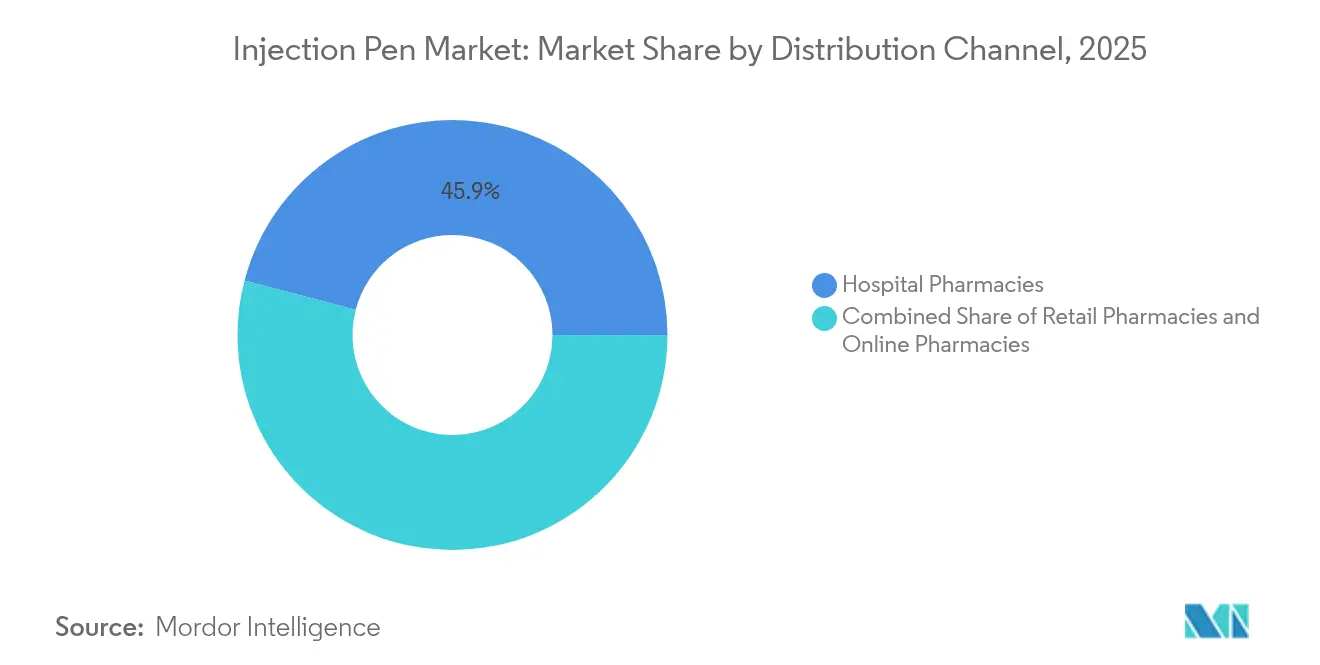

- By distribution channel, hospital pharmacies captured 45.92% of the injection pen market size in 2025, yet online pharmacies are projected to rise at a 13.02% CAGR through 2031.

- By geography, North America maintained 35.98% market share in 2025; Asia-Pacific is on track for a 11.35% CAGR, fueled by rapid diabetes incidence growth and health-system modernization.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Injection Pen Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Prevalence of Diabetes & Preference for Self-Administration | +1.8% | Global, with highest impact in North America & Asia-Pacific | Long term (≥ 4 years) |

| Expanding GLP-1/GIP Agonist Pipeline Requiring Pen Formats | +1.5% | North America & EU primary, expanding to APAC | Medium term (2-4 years) |

| Shift To Value-Based Care Favouring Home-Use Devices | +1.2% | North America & EU core markets | Medium term (2-4 years) |

| Growth Of Tele-Pharmacy & E-Commerce for Rx Refills | +0.9% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| Sustainability Mandates Pushing Reusable/Eco Pens | +0.6% | EU leading, expanding to North America | Long term (≥ 4 years) |

| Connectivity & Data-Sharing Demand from Payers | +0.7% | North America & EU, emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Prevalence of Diabetes & Preference for Self-Administration

Diabetes affects about 500 million people worldwide, and these patients increasingly favor devices that enable safe self-injection outside clinical settings.[1]Jane Doe, “Smart Insulin Pens and Glucose Monitoring,” Diabetes Therapy, springer.com In China, 92% of insulin users rely on injection pens, illustrating the strong preference for pen-based delivery when needles are short and injection steps are simple. Insurance gaps elevate total care costs for patients who must pay out-of-pocket for pen needles, yet payer interest in preventive approaches is spurring broader coverage in high-burden markets. Smart pens that synchronize with continuous glucose monitors provide time-stamped dose data, helping clinicians correlate insulin administration with glycemic trends and reinforcing adherence. The combination of patient convenience, clinical insight, and cost containment cements injection pens as a central element of diabetes management frameworks.

Expanding GLP-1/GIP Agonist Pipeline Requiring Pen Formats

GLP-1 patient counts are projected to quadruple to more than 60 million by 2035, intensifying demand for pens engineered to deliver viscous formulations at high concentrations.[2]Ypsomed AG, “Annual Report 2025,” ypsomed.com Tirzepatide has demonstrated 20.2% average weight reduction versus 13.7% for semaglutide, strengthening competitive positioning for pen-compatible obesity and diabetes drugs. Manufacturers are shifting from disposable to high-capacity, reloadable designs to accommodate fill-finish constraints and sustainability targets. Patent filings now exceed 200 for GLP-1 delivery devices, underscoring proprietary races to refine pen ergonomics and dose accuracy. Although oral GLP-1 candidates could moderate injectable demand after 2030, near-term revenue pipelines remain tethered to pen formats, sustaining robust component and systems orders across OEM supply chains.

Shift to Value-Based Care Favoring Home-Use Devices

Payers link reimbursement to demonstrable outcome gains, driving preference for injection pens that log usage data and cut clinic visits.[3]American Journal of Managed Care, “On-Body Delivery Devices and Payer Value,” ajmc.com Smart autoinjectors push adherence above 80% in multiple sclerosis therapy, doubling treatment persistence versus legacy devices. Skilled-nursing facilities reduced insulin costs from USD 10.29 to USD 4.08 per patient-day after switching to pens, validating tangible savings for institutional providers. Such evidence encourages adoption in accountable-care organizations tasked with lowering readmissions. Device complexity and caregiver training remain obstacles; however, integrated onboarding platforms and visual tutorials shorten learning curves and boost patient confidence.

Growth of Tele-Pharmacy & E-Commerce for Rx Refills

Specialty pharmacies handled nearly USD 243 billion in U.S. prescription revenues during 2023, exploiting cold-chain know-how vital for temperature-sensitive pens . Online channels post a 13.76% CAGR because home delivery eliminates travel friction for chronic disease patients while preserving product integrity through insulated packaging. Leading networks such as CVS Specialty, Accredo, and Optum leverage analytics to automate prior approvals, accelerating time-to-therapy for GLP-1 starts. Compounded alternatives surfaced amid branded shortages but remain limited by FDA oversight, which reinforces reliance on compliant pen-based biologics. Integration of connected pens with tele-health dashboards allows pharmacists to trigger interventions when dose misses appear, aligning service models with outcome-based contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited HCP Training in Low-Income Countries | -0.8% | APAC emerging markets, MEA, Latin America | Long term (≥ 4 years) |

| Stringent EU MDR & ISO 11608 Compliance Costs | -1.1% | EU primary, global spillover effects | Medium term (2-4 years) |

| Device Cybersecurity & Data-Privacy Concerns | -0.7% | North America & EU, emerging in APAC | Short term (≤ 2 years) |

| Supply-Chain Pressure on Medical-Grade Polymers | -0.9% | Global, with acute impact in North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent EU MDR & ISO 11608 Compliance Costs

European MDR directives and ISO 11608 revisions demand exhaustive validation of cap-removal, dose-dialing, and injection-time metrics, often extending launch timelines by 12-18 months. Notified-body fees vary widely, but cumulative regulatory expenses can exceed USD 1 million per product line, discouraging smaller entrants from participating. Connected devices shoulder additional FDA Section 524B obligations, including software bills of material and vulnerability monitoring protocols, escalating design-control overhead. Established manufacturers with enterprise-level QA resources absorb these burdens more readily, which accelerates consolidation and limits diversity of ecosystem participants.

Limited HCP Training in Low-Income Countries

In low-income regions, clinicians often lack formal instruction in pen operation and troubleshooting, constraining patient onboarding. Insufficient cold-chain capacity hampers biologic stability in remote clinics, where power outages compromise storage. Cultural inclination toward provider-administered injections further slows adoption, necessitating labor-intensive education programs. Multilingual labeling and pictogram guides raise manufacturing costs and regulatory complexity. Limited broadband penetration curtails smart-pen functionality, reducing value propositions that hinge on data connectivity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smart Connectivity Drives Premium Growth

Smart and connected pens lead the injection pen market with an 10.83% CAGR and are rapidly converting technology-savvy patient cohorts. Disposable formats still command 64.12% of 2025 revenue because of physician familiarity and low upfront cost. Sustainability mandates in the EU and forthcoming U.S. regulations are nudging users toward reusable architectures that shrink plastic waste and simplify sharps recovery. Smart variants integrate dose capture, reminder alerts, and Bluetooth-enabled data uploads, aligning with payer demand for measurable adherence. Novo Nordisk’s ReMed program, which collects used pens for recycling in seven countries, mitigates environmental critiques leveled at disposables.

Reusable platforms occupy a pragmatic middle ground, delivering cost economy for daily injectors without imposing app dependence on technology-averse populations. As cloud integration becomes standard, smart formats are displacing basic disposables in high-income markets; however, hybrid solutions that retrofit disposable pens with clip-on sensors are gaining traction as affordability bridges. OEM collaborations with digital-health start-ups are shortening development cycles, while contract manufacturers scale modular electronics sub-assemblies to meet volume surges tied to GLP-1 launches. These patterns underpin a steady migration toward intelligent delivery ecosystems anchored by user-friendly human-factors engineering.

By Indication: Autoimmune Surge Challenges Diabetes Dominance

Diabetes maintained a 70.68% foothold in 2025, but autoimmune therapies are on course for a 9.82% CAGR, riding a wave of monoclonal antibody approvals that require frequent at-home dosing. Biologics for rheumatoid arthritis, inflammatory bowel disease, and psoriasis increasingly rely on pen devices capable of handling high-viscosity formulations without requiring patient priming. Growth-hormone deficiency therapies reinforce acceptance of electronic pens, with 98% of surveyed users rating modern designs easy to learn and largely pain-free.

Oncology supportive-care pens such as pegfilgrastim on-body injectors reduced febrile neutropenia to 1.4%, marginally outperforming prefilled syringes and eliminating infusion-center visits. Osteoporosis regimens benefit from enlarged actuator buttons and color-coded guidance that shorten nursing-time training and improve long-term compliance. Fertility and rare-disease segments add volume diversity, prompting manufacturers to develop variable-dose dialers and concentration-specific cartridges. The evolving indication mix broadens revenue streams and spurs iterative innovations in pen ergonomics, drug stability, and user feedback mechanisms.

By Distribution Channel: Digital Transformation Reshapes Access

Hospital pharmacies held 45.92% of 2025 transactions, but e-commerce channels are expanding at 13.02% CAGR and progressively capturing refill volumes for chronic injectables. Specialty networks leverage refrigerated last-mile logistics and embedded nurse help lines that traditional brick-and-mortar outlets find hard to replicate. Retail pharmacies preserve relevance through convenient pickup and in-store counseling, although margin pressure intensifies as online platforms negotiate direct-to-manufacturer discounts.

The shift to tele-pharmacy is furthered by smart-pen telemetry, which alerts pharmacists to missed doses and triggers automated adherence coaching. Cold-chain compliance remains a gatekeeper; platforms able to track temperature excursions in real time differentiate themselves to biotech partners. Channel consolidation is under way as large networks acquire regional players to expand geographic reach and fortify negotiating leverage with payers. As value-based agreements proliferate, distributors able to furnish adherence analytics will command preferred-provider status.

Geography Analysis

North America anchored 35.98% of 2025 revenue, reflecting early GLP-1 adoption, broad reimbursement of electronic devices, and robust cybersecurity frameworks that accelerate smart-pen approvals. The region continues to absorb capacity as incumbents reorganize supply chains to navigate medical-grade polymer shortages and FDA cyber-resilience mandates. Investment incentives in the United States have spawned domestic autoinjector plants that cut freight risk and shorten lead times for blockbuster launches. Canada mirrors these trends through provincial tender programs that encourage adherence and reduce hospital admissions linked to poorly managed diabetes.

Europe remains a second revenue pillar, buoyed by integrated health systems that reimburse reusable pen kits and favor eco-friendly designs aligned with circular-economy directives. However, EU MDR recertification bottlenecks elevate compliance costs and delay product rollouts, prompting some smaller manufacturers to exit certain markets. The United Kingdom’s National Health Service is piloting smart-pen linked remote-monitoring services to support community-pharmacy diabetes clinics, providing a template for outcome-based payment models.

Asia-Pacific is the fastest-growing region at 11.35% CAGR, driven by China, India, and Southeast Asian countries wrestling with steep diabetes incidence. Manufacturers partner with national academic centers to localize training materials and adapt pens for region-specific dosage regimens. Government insurance expansion and Tier 2 city hospital upgrades improve patient access to advanced delivery devices. Japanese demand skews toward premium smart formats supported by an aging, tech-literate population, whereas cost-sensitive markets in South Asia favor reusable platforms with minimal electronic components.

Latin America exhibits steady uptake as social-security systems integrate biosimilar insulin aspart and liraglutide into formularies alongside generic needles. Distribution hurdles persist in remote Andean and Amazonian regions, but tele-pharmacy pilots signal gradual progress. The Middle East and Africa hold nascent penetration levels; oil-exporting Gulf states invest in public-private partnerships to deploy closed-loop diabetes management, yet sub-Saharan areas grapple with training shortages and unreliable cold chains, limiting mass deployment until infrastructure improves.

Competitive Landscape

The injection pen market is moderately concentrated. Novo Nordisk produces half of global insulin supply and exceeds 600 million pen units annually, leveraging integrated cartridge molding and custom robotics to maintain low unit costs. The USD 16.5 billion Catalent acquisition secures fill-finish throughput for GLP-1 expansion, exemplifying vertical integration as a risk-mitigation tactic. Eli Lilly exploits head-to-head clinical superiority in weight-management trials to capture share and partners with Antares for QuickShot autoinjectors aimed at high-dose biologics.

Ypsomed, BD, and SHL Medical dominate the contract manufacturing tier. Ypsomed recorded 37.9% revenue growth in 2024/25 and is scaling facilities across Switzerland, Germany, China, and the United States to meet OEM demand for both disposable and reusable systems. SHL’s new U.S. autoinjector plant supports large-volume biologics that require higher injection forces, reflecting a pivot toward oncology and autoimmune molecules. Aptar and Gerresheimer enrich portfolios with digital add-ons, including NFC-enabled caps that feed real-world adherence data to cloud dashboards.

Patent activity remains intense, particularly in torsion-spring energy storage, lead-screw drive systems, and multi-dose dial-back mechanisms. Sustainability and circularity spur innovation in bio-resin housings and modular designs that eliminate metal components for easier recycling. Needle-free jet-injector entrants occupy specialized niches but face muscle-ache side-effects and higher regulatory scrutiny, limiting immediate threat to needle-based incumbents. Overall, competitive dynamics revolve around supply assurance, connected-device ecosystems, and regulatory fluency rather than traditional price wars.

Injection Pen Industry Leaders

Novo Nordisk

medac GmbH

Gerresheimer AG

Owen Mumford

Eli Lilly and Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Biocon Biologics Ltd. (BBL), a global biosimilars subsidiary of Biocon Ltd., has received U.S. FDA approval for KIRSTY (Insulin Aspart-xjhz), 100 units/mL, marking a significant milestone as the first and only interchangeable biosimilar to NovoLog (Insulin Aspart). This approval reinforces BBL’s position in the global insulin biosimilars market and expands its footprint in the U.S. diabetes care segment.

- April 2025: Meitheal Pharmaceuticals, Inc., a fully integrated biopharmaceutical company headquartered in Chicago, has announced a significant regulatory and commercial milestone with the U.S. FDA approval and launch of liraglutide injection (18mg/3mL) the generic equivalent of Victoza in the United States.Meitheal has introduced liraglutide injection in a three-pack configuration, with plans to expand availability through additional pack sizes later in 2025, enhancing flexibility for prescribers and patients.

- April 2025: SHL Medical opened a new autoinjector manufacturing facility in the United States, enhancing production capabilities for large-volume and high-viscosity formulations while supporting pharmaceutical partners' geographic expansion strategies

- April 2024: Eisai Co. Ltd and nippon medac Co. Ltd obtained marketing and manufacturing approvals for Metoject Subcutaneous Injection, an injection pen that contains methotrexate drugs to treat rheumatoid arthritis patients in Japan.

Global Injection Pen Market Report Scope

An injection pen is a device that is used to deliver drugs. It typically consists of a cartridge or prefilled drug reservoir, a disposable needle, and a pen-like device that holds and delivers the medication. Injector pens are designed to make injectable medication more accessible and convenient, thus increasing patient adherence. This industry combines innovative, advanced technologies to offer personalized, accessible, and effective solutions for individuals seeking support for drug delivery.

The injection pen market is segmented by product, indication, and geography. By product, the market is segmented into disposable and reusable. By indication, the market is segmented into diabetes, autoimmune diseases, and other indications. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report offers market sizes and forecasts in terms of value (USD) for all the above segments.

| Disposable |

| Reusable |

| Smart/Connected |

| Diabetes |

| Autoimmune Diseases |

| Growth Hormone Deficiency |

| Oncology Supportive Care |

| Osteoporosis |

| Other Indications |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Disposable | |

| Reusable | ||

| Smart/Connected | ||

| By Indication | Diabetes | |

| Autoimmune Diseases | ||

| Growth Hormone Deficiency | ||

| Oncology Supportive Care | ||

| Osteoporosis | ||

| Other Indications | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the injection pen market be by 2031?

Forecasts place the injection pen market size at USD 69.77 billion by 2031, representing a 6.37% CAGR from 2026.

Which product category is growing fastest?

Smart and connected pens are projected to expand at 10.83% CAGR, the highest among all product types.

What therapeutic area offers the greatest near-term growth upside?

Autoimmune diseases are expected to post a 9.82% CAGR as biologic approvals accelerate.

Which region shows the strongest growth momentum?

Asia-Pacific leads with an anticipated 11.35% CAGR through 2031, driven by soaring diabetes prevalence and infrastructure upgrades.

How are sustainability concerns being addressed?

Manufacturers are rolling out reusable housings, recycling initiatives such as Novo Nordisk’s ReMed program, and bio-resin components to curb single-use plastic waste.

What is the biggest regulatory hurdle for new entrants?

Compliance with EU MDR and ISO 11608 testing adds substantial cost and time, often requiring more than USD 1 million per product line and extending launch timelines up to 18 months.

Page last updated on: