Micro-pumps Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

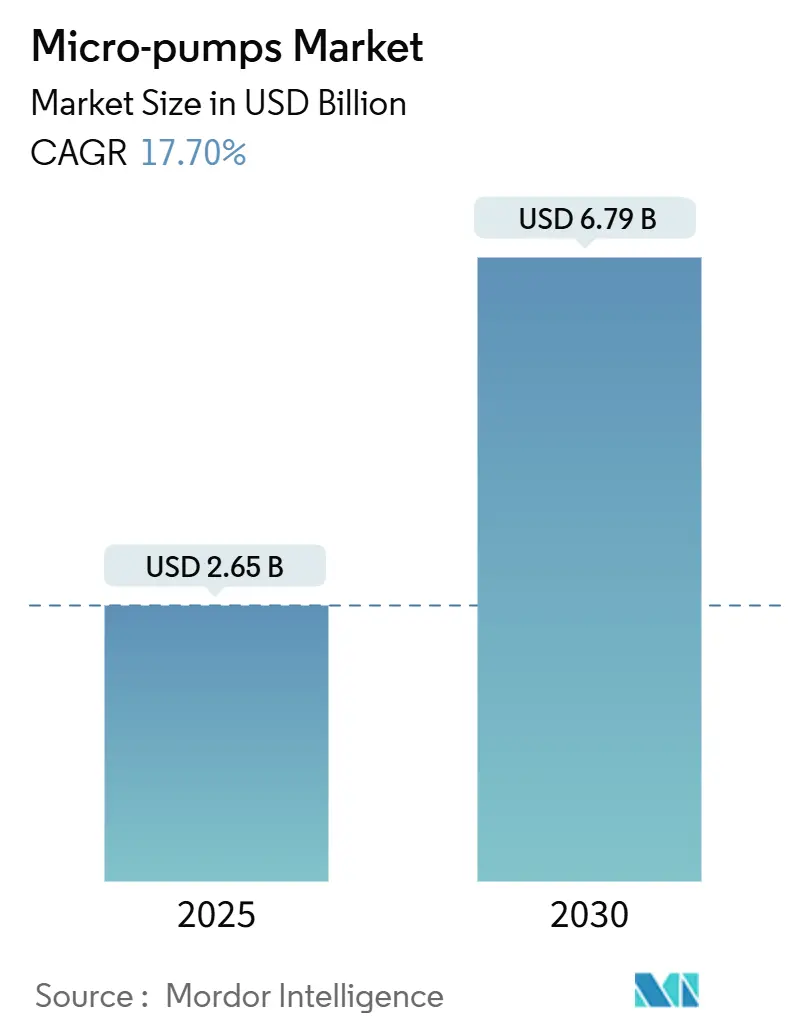

| Market Size (2025) | USD 2.65 Billion |

| Market Size (2030) | USD 6.79 Billion |

| Growth Rate (2025 - 2030) | 17.70% CAGR |

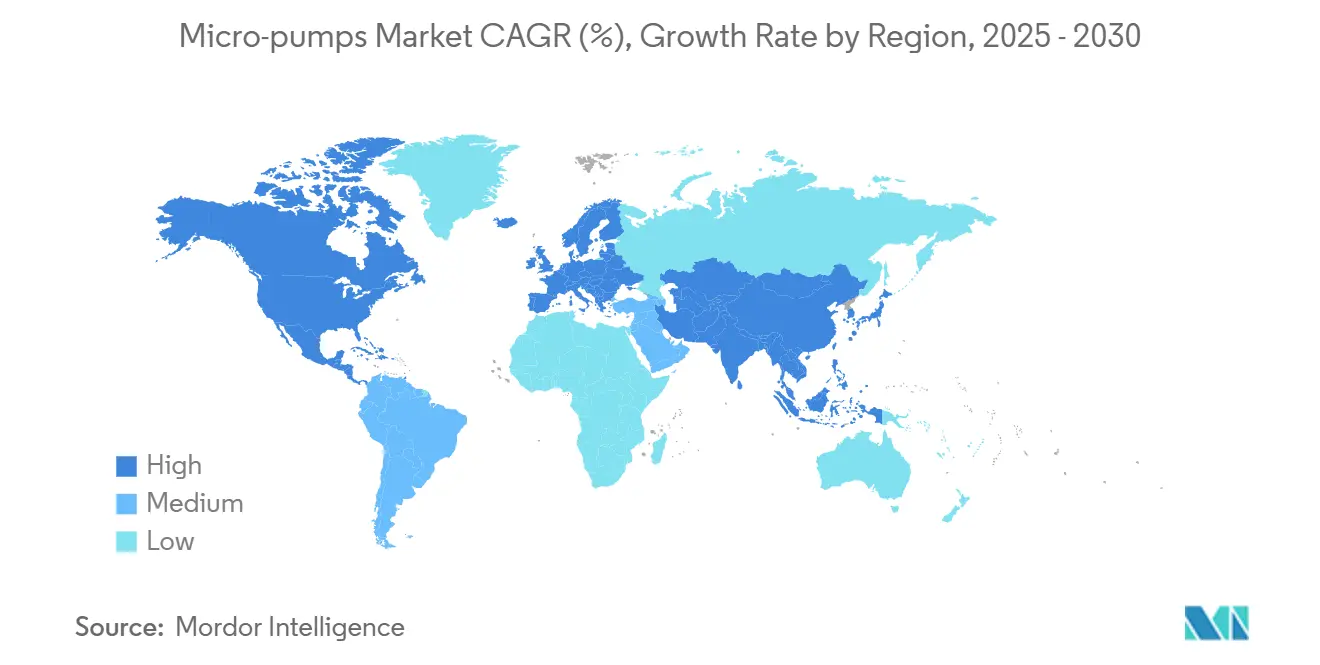

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Micro-pumps Market Analysis by Mordor Intelligence

The micropumps market size reached USD 2.65 billion in 2025 and is forecast to climb to USD 6.79 billion in 2030, registering a 17.7% CAGR across the period. Progress is underpinned by the simultaneous push for miniaturization in healthcare, electronics, and precision industrial processes, all of which depend on tighter fluid-handling tolerances than macro-scale pumps can achieve. The U.S. Food and Drug Administration (FDA) clarified development pathways for drug-delivery hardware in 2024, easing regulatory uncertainty for active implantable and wearable infusion systems. At the same time, the broader micro-electromechanical systems (MEMS) supply chain keeps chip-level integration on a steep cost-down trajectory, even though packaging still absorbs more than 80% of device production budgets. Healthcare maintains revenue leadership on the back of chronic-condition management programs that increasingly embed microfluidic drug reservoirs. In contrast, thermal management uses in high-performance computing now represent the fastest-scaling opportunity as processors cross the 700 W thermal-design threshold. Regionally, North America captures the largest revenue share owing to deep clinical-trial infrastructure and reimbursement frameworks, while Asia-Pacific is growing the quickest due to sovereign funding for semiconductor self-sufficiency and large-scale contract manufacturing.

Key Report Takeaways

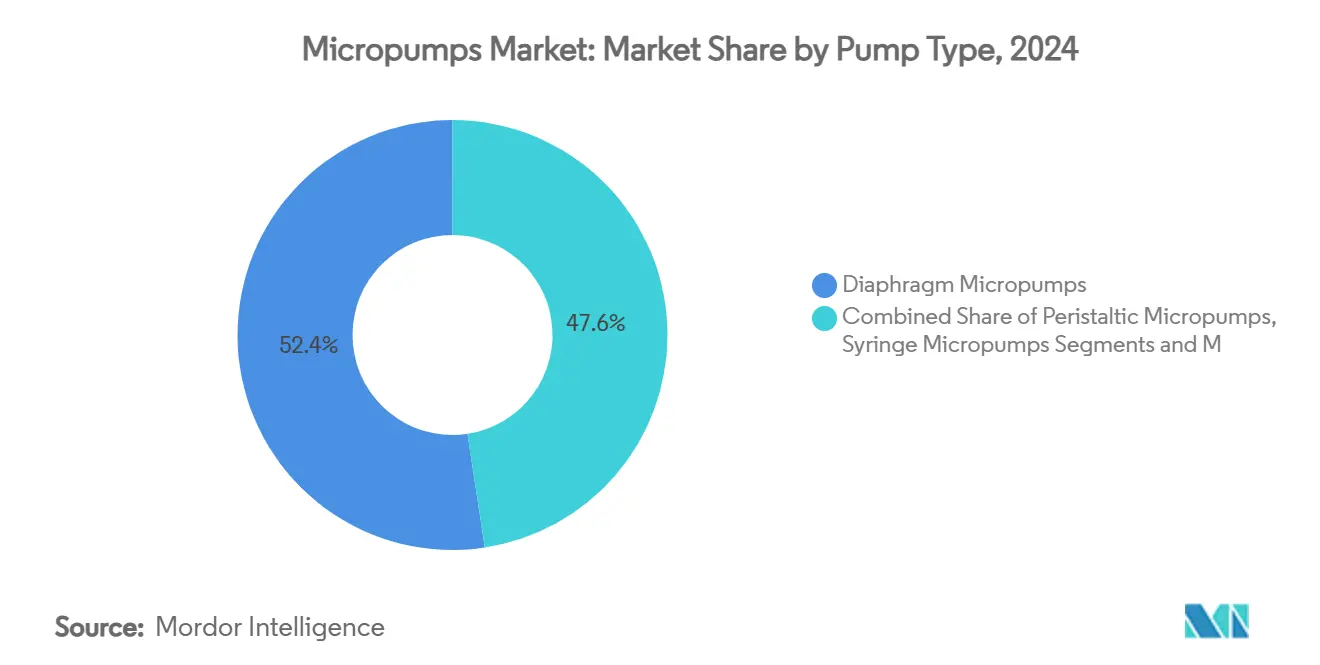

- By pump type, diaphragm micropumps captured 46.2% of the micropumps market share in 2024; piezoelectric micropumps are projected to lead growth at 18.2% CAGR through 2030.

- By actuation principle, mechanically driven devices held 52.4% revenue share in 2024, while electrostatic variants are forecast to advance at 16.2% CAGR to 2030.

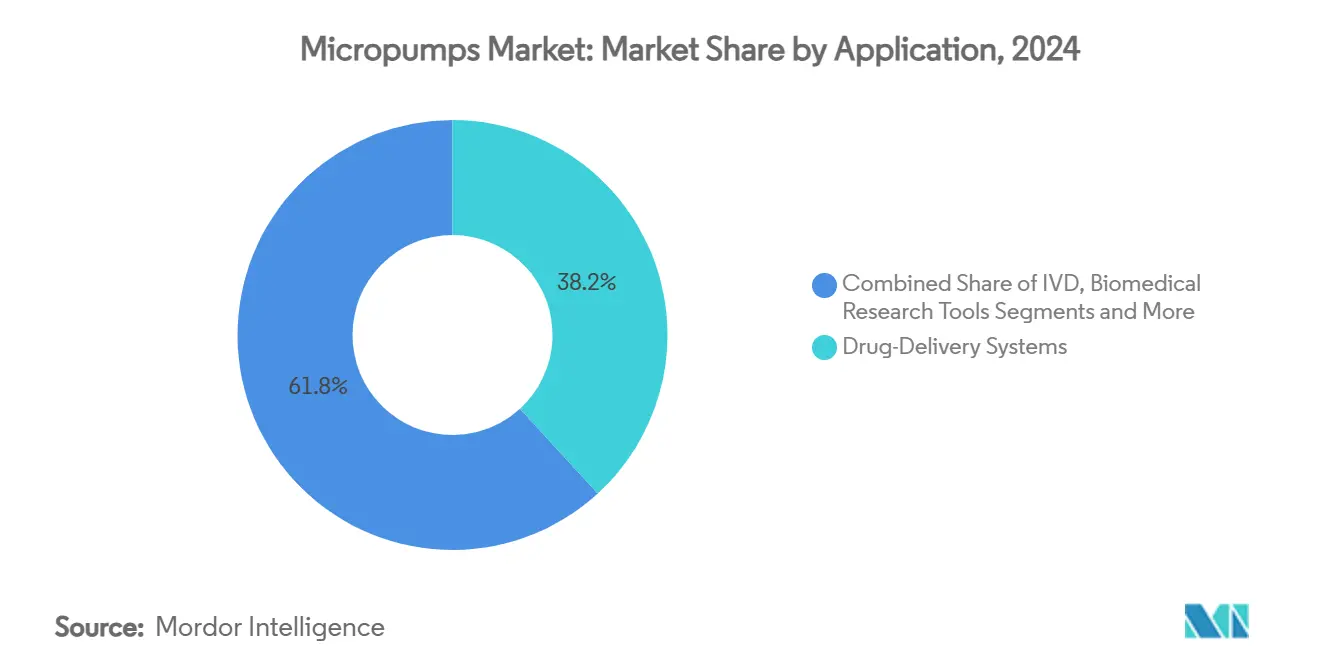

- By application, drug-delivery systems accounted for a 38.2% share of the micropumps market size in 2024 and are expanding at a 17.4% CAGR through 2030, driven by insulin and oncology infusion platforms.

- By end-user industry, healthcare and life sciences led with 42.7% of the micropumps market share in 2024; electronics and semiconductors are on track for the highest segment CAGR of 15.3% to 2030.

- By geography, North America controlled 35.8% of 2024 revenue, while Asia-Pacific is expected to post the strongest regional CAGR at 16.9% over the outlook period.

Global Micro-pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Miniaturization Of Wearable & Implantable Devices | +3.20% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Growing Demand For POC & IVD Microfluidics | +2.80% | Global, strongest in APAC and North America | Short term (≤ 2 years) |

| Chronic-Disease-Led Uptake Of Precision Drug Delivery | +2.10% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Government R&D Funding For Lab-On-Chip Platforms | +1.90% | APAC core, spill-over to North America & EU | Medium term (2-4 years) |

| MEMS-Based Thermal Management In Semiconductors | +2.40% | APAC manufacturing hubs, global deployment | Short term (≤ 2 years) |

| Adoption Of Cuff-Less BP Monitors With Integrated Micropumps | +1.80% | Global, led by North America consumer markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Miniaturization of Wearable & Implantable Devices

BioMEMS revenue is projected to reach USD 24.5 billion by 2030, with piezo-actuated micropumps serving as the de facto fluid drivers for subcutaneous insulin algorithms, leadless pacemakers, and pulmonary pressure sensors.[1]Vibhor Kumar, “Advancements in Wearable and Implantable BioMEMS Devices,” mdpi.com Conductive polymers and bio-degradable substrates slim down board area and open new form factors, while embedded Bluetooth Low Energy radios relay dosage data to cloud dashboards for clinicians. Leadless pacing platforms such as Micra have reported low complication scores and obviate the lead-extraction risk seen in conventional pacemakers. Wireless pulmonary artery monitors like CardioMEMS further demonstrate how battery-less telemetry meshes well with passive fluid chambers, cutting heart-failure readmissions for eligible patients. Remaining hurdles include energy harvesting for chronic implants and multi-jurisdiction regulatory audits. Yet, the overall cost-benefit calculus favors micropump adoption as hospitals migrate from episodic to continuous care models.

Growing Demand for POC & IVD Microfluidics

Point-of-care diagnostic brands commercialized during the COVID-19 emergency have set new user-expectation baselines for assay speed, sample volume, and portability.[2]Abdul Raffay Khan, “Point-of-Care Testing: Market and Future Trends,” frontiersin.org Micro-chambers capable of moving sub-microliter samples via piezo diaphragms now achieve sensitivity parity with central-lab immunoassays, shortening sepsis identification to under 60 minutes. In Asia-Pacific, government procurement programs for community clinics prioritize devices with inbuilt calibration routines that tolerate local humidity swings. Industry leaders Abbott and Siemens now bundle cloud dashboards, enabling epidemiology officers to map outbreaks in near-real-time. Obstacles remain around reagent shelf life and cartridge waste streams. Still, field evidence shows that micro-scale pumping can double analyte hit rates by reducing dead volume compared with capillary-driven strips.

Chronic-Disease-Led Uptake of Precision Drug Delivery

Osmotically triggered cartridges and piezo-pumped T-pipes converge in the SUSTAIN modular patch, offering week-long basal infusions followed by clinician-triggered bolus events for oncology and endocrinology protocols.[3]Wei Chen, “Sequentially Triggerable Implantable Nozzle System,” science.org Gerresheimer’s alliance with Adamant Health layers machine-learning tremor scores onto Parkinson’s infusion profiles, creating a closed-loop system that modifies apomorphine doses every 30 minutes, an upgrade over static titration calendars. In diabetology, pump-sensor convergence has cut time-in-range metrics below the 70 mg/dL hypo wall in multi-country trials, incentivizing payers to underwrite automated insulin delivery. Biocompatibility and immune encapsulation issues still challenge device longevity, but early design-for-disassembly approaches hint at circular-economy take-back schemes that could unlock reimbursement credits.

Government R&D Funding for Lab-On-Chip Platforms

Chinese and South Korean ministries collectively earmarked more than USD 1.9 billion for lab-on-chip consortia between 2024 and 2025, spurring university spin-outs focused on SlipChip gas-gradient generation and lipid-nanoparticle fabrication. Subsidized wafer runs in 200 mm MEMS lines allow start-ups to iterate channels and pump chambers without committing to six-figure pilot lots. In India and Singapore, funding calls emphasize point-source environmental analyzers that can attach to drones or disposable water probes. The influx of public capital lowers time-to-functional-prototype metrics and creates de-risked licensing opportunities for multinational device firms that prefer late-stage acquisitions over internal blue-sky R&D.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Fabrication & Packaging Costs | -2.90% | Global, most acute in North America & EU | Short term (≤ 2 years) |

| Regulatory Validation Cycles For Active Implantables | -1.70% | North America & EU regulatory jurisdictions | Long term (≥ 4 years) |

| Volatility In Specialty Piezo-Ceramic Supply Chain | -1.40% | Global, with critical exposure in APAC manufacturing hubs | Medium term (2-4 years) |

| Heat-Dissipation Limits In High-Flow Micro-Viscous Pumping | -0.80% | Global, particularly affecting high-performance applications | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Fabrication & Packaging Costs

Packaging remains the single largest cost driver because MEMS structures diverge from pure silicon logic, forcing bespoke cap bonding and fluidic port alignment steps that standard CMOS lines cannot accommodate. Cleanroom yield risk increases whenever bio-compatible coatings enter the stack, pushing defect-density budgets beyond typical IC tolerances. As a result, cost curves flatten only when annualized production tops 5 million units—an output level fewer than ten suppliers currently achieve. Industry alliances are exploring glass-frit caps and through-silicon-vias to trim assembly station counts, but breakthrough economics will likely wait for hybrid wafer-level-packaging cells now under trial in Taiwan.

Regulatory Validation Cycles for Active Implantables

Postmarket surveillance databases logged 1.7 million injuries tied to medical devices in the United States, prompting the FDA to intensify sample-level safety tracking.[4]U.S. Government Accountability Office, “FDA Postmarket Surveillance System,” gao.gov Active implantables require rigorous bench-to-human biocompatibility evidence, stretching 510(k) and PMA timelines. The VIVISTIM neuro-stimulator journey from dossier submission to market approval spanned 2,719 days, spotlighting the headwinds that fluidic implants also face. The 2024 draft Essential Drug Delivery Outputs guidance now demands design-history-file documentation that tracks pump accuracy over battery life, adding lab time upfront but promising smoother inspections later. Smaller innovators often lack the capital cushion for such extended cycles, slowing market entry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pump Type: Piezoelectric Leadership Sustains Momentum

diaphragm micropumps contributed 46.2% of 2024 revenue, making them the single largest component of the Micropumps market size. Valveless Coriolis-effect variants now exceed 1.7 mL/min under optimized voltage waveforms, validating their transfer to ambulatory infusion pens. Diaphragm architectures stay relevant where back-pressure is unpredictable, particularly in veterinary anesthesia vaporizers. Syringe-format pumps remain a lab staple due to their absolute volumetric accuracy, yet their discrete footprint disqualifies them from wrist-worn wearables. Emerging research that couples piezo stacks to hollow microneedles promises high-precision intradermal vaccination with sub-second transients, augmenting public-health campaigns that must vaccinate in non-clinical settings.

Piezoelectric materials science is evolving alongside form factors. Commercial PZT ceramics now benefit from DC poling treatments that lift d₃₃ coefficients 12% and elevate Curie points, allowing continuous duty at 150 °C—critical for semiconductor cooling modules. Single-use pump cassettes such as Dover’s Quattroflow QB2-SD address cGMP contamination concerns in biologics production and accelerate batch changeovers in cell-therapy plants. Studies on active lubrication show piezoelectric micropumps can meter 0.8 μL shots of oil into micro-gears, opening an adjacent revenue stream in precision-mechanical subassemblies.

By Actuation Principle: Mechanical Reliability vs. Electrostatic Precision

Mechanical schemes, including piezoelectric diaphragms and gear-based micro-engines, delivered 52.4% of top-line value in 2024, reinforcing their role in moderate-cost, high-wear applications such as ambulatory drug pumps. Electrostatic actuation, while accounting for a smaller installed base, is projected to expand at a 16.2% CAGR thanks to low-power consumption and CMOS-friendly fabrication. Silicon microfluidic chips using V-shaped electro-thermal actuators demonstrate sub-40 ms response times, illustrative of the speed edge over solenoid valves.

Magneto-hydrodynamic and electro-osmotic approaches are carving niche opportunities where ion-free flows or non-mechanical chambers are mandatory, as in optogenetics perfusion. However, they face higher drive-voltage requirements and fluid-conductivity constraints. Meanwhile, research on stacked MEMS resonators opens the door to hybrid electrostatic-piezoelectric arrays that could combine force density with nanoliter accuracy. The technology split suggests a coexistence strategy: mechanical pumps tackle high-flow macrodosing, while electrostatic modules finesse micro-dosing stages in the same device.

By Application: Drug-Delivery Dominance, Electronics Cooling Acceleration

Drug-delivery systems represented 38.2% of the Micropumps market share in 2024, anchored by insulin, oncology, and neuro-stimulation infusions. Regulatory clarity after the Essential Drug Delivery Outputs guidance gave OEMs a predictable design-verification checklist, quickening time-to-clearance for connected autoinjectors. Patch pumps now store multi-drug cartridges and auto-switch based on wearable glucose sensor feedback, reducing user intervention.

Electronics cooling is climbing fastest at 17.4% CAGR, as liquid-based cold plates migrate from hyperscale data halls into thin-and-light consumer electronics. SiC vapor chambers paired with micro-pumps slashed thermal-resistance values to one-third of fin-stack equivalents, sustaining 4 K die-to-lid gradients in field tests. Parallel momentum is visible in rapid bacterial-detection cassettes for in-vitro diagnostics (IVD). Spiral microfluidic chips generate lipid-nanoparticle libraries at 960 mL/h, a scale adequate for seasonal vaccine campaigns. Environmental monitoring applications exploit surface-acoustic-wave mixers to detect nitrate spikes in irrigation runoff within 90 seconds, promising a new revenue avenue tied to climate-regulation compliance.

By End-User Industry: Healthcare Primacy, Electronics Upswing

Healthcare and life sciences retained 42.7% of 2024 turnover, reflecting ongoing demand for chronic-disease management tools that prioritize patient convenience. Remote patient-monitoring kits now embed micro-reservoirs that autonomously dispatch rescue medications when AI detects arrhythmia or asthma onset. Pharmaceutical continuous manufacturing uses pump arrays to modulate reagent stoichiometry, ensuring real-time release quality.

The electronics & semiconductors cohort forecasts the steepest trajectory at 15.3% CAGR through 2030 as mobile devices integrate on-device generative AI and need superior heat evacuation solutions. High-bandwidth memory stacks in graphics cards rely on piezo-centric micro-loops to cap junction temperatures. Chemical-process sectors adopt robust peristaltic microsystems for inline pH correction, while aerospace engineers test ultra-light pumps in cryogenic fuel conditioning. Agricultural-tech pilots mount piezo pumps on sensor drones to dispense micro-liter doses of nutrient solutions, illustrating cross-sectoral innovation.

Geography Analysis

North America held 35.8% of 2024 revenue on the strength of FDA-aligned quality systems, academic research pipelines, and reimbursements that encourage at-home therapies. Venture capital access speeds proof-of-concept to pivotal trials, but tight labor markets and higher cleanroom lease rates raise the cost per die. Government initiatives such as ARPA-H underwrite microfluidic cancer-screening prototypes, aligning public health goals with commercial interests.

Asia-Pacific is projected to post a 16.9% CAGR, the fastest of any region, underpinned by sovereign semiconductor policies in China, Japan, and South Korea. Contract manufacturers leverage existing MEMS fabs to spin up microfluidic lines with minimal CapEx. Regional ministries co-fund SlipChip and lipid-nanoparticle projects that answer both biopharma and defense bio-protection agendas. Rising incomes and an aging demographic broaden the addressable base for point-of-care diagnostics. Supply-chain shocks still lurk in specialty ceramics and silver paste, but multi-source frameworks partially mitigate concentration risks.

Europe maintains steady uptake backed by MDR harmonization and high per-capita healthcare spending. Automotive and aerospace incumbents pioneer micro-pump cooled avionics, tapping EU Horizon funds. Sustainability codes incentivize micropump integration into water-quality probes for smart-city rollouts. Middle East & Africa and South America register nascent but growing demand, particularly as regional oncology centers adopt portable infusion devices to serve rural populations. Currency volatility and divergent regulatory regimes extend time-to-market, though multilateral health programs gradually improve procurement transparency.

Competitive Landscape

The micropumps arena is moderately fragmented. The top five suppliers together account for an estimated 38% of global revenue, leaving room for specialist entrants targeting high-margin sub-niches. Players differentiate by proprietary actuation physics, sterile single-use kits, and embedded sensor integration. Sensirion’s February 2025 collaboration with TTP Ventus marries ultra-low-flow pumps with CMOS flow sensors to create closed-loop drivers capable of ±2% flow accuracy at 100 μL/min, a specification valued in cell-therapy media exchanges. IDEX’s 2024 divestment of Micropump Inc. signals a shift toward platform rationalization, concentrating resources on high-pressure metering valves.

M&A appetite remains high. AMETEK’s acquisition of Kern Microtechnik brings sub-micron machining that translates directly into tighter pump-chamber geometries, giving AMETEK a supply-side edge. Dover, through its Quattroflow line, capitalizes on the single-use bioprocessing boom by offering plug-and-play cassettes validated to 50 psi back-pressure. Meanwhile, ceramic-based start-ups tout PZT-free thin-film stacks to lure customers worried about toxicity regulations. Cloud-ready pumps equipped with Wi-Fi/BLE modules accumulate real-world duty-cycle data, letting vendors pivot to service-as-a-software subscription models that add annuity revenue.

White-space opportunities remain in environmental sensing, lunar in-situ resource utilization, and micro-propulsion for CubeSats. Barriers center on funding long validation cycles and certifying pumps for extreme temperatures or radiation. Suppliers that master cross-disciplinary collaborations with AI algorithm houses and bio-polymer labs are positioned to outpace mechanical-integration-focused competitors.

Micro-pumps Industry Leaders

Takasago Electric Inc.

TTP Ventus (The Lee Company)

KNF Neuberger

Bartels Mikrotechnik

Fluigent SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Sensirion AG partnered with TTP Ventus to bundle the SLF3x liquid-flow sensor with Disc Pump kits, achieving closed-loop flow regulation for R&D microfluidics.

- February 2025: Dover Corporation’s PSG Biotech unveiled the Quattroflow QB2-SD single-use micropump targeting contamination-sensitive biopharma batches.

- August 2024: IDEX Corporation finalized the sale of Micropump Inc., sharpening its focus on core metering technologies

Global Micro-pumps Market Report Scope

| Diaphragm Micropumps |

| Peristaltic Micropumps |

| Syringe Micropumps |

| Piezoelectric Micropumps |

| Others |

| Mechanical |

| Piezoelectric |

| Electrostatic |

| Magneto/EHD |

| Others |

| Drug-Delivery Systems |

| In-Vitro Diagnostics |

| Biomedical Research Tools |

| Micro-electronics Cooling |

| Industrial Ink-jet Printing |

| Healthcare & Life Sciences |

| Electronics & Semiconductors |

| Chemical & Process |

| Environmental Monitoring |

| Automotive & Aerospace |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Pump Type | Diaphragm Micropumps | |

| Peristaltic Micropumps | ||

| Syringe Micropumps | ||

| Piezoelectric Micropumps | ||

| Others | ||

| By Actuation Principle | Mechanical | |

| Piezoelectric | ||

| Electrostatic | ||

| Magneto/EHD | ||

| Others | ||

| By Application | Drug-Delivery Systems | |

| In-Vitro Diagnostics | ||

| Biomedical Research Tools | ||

| Micro-electronics Cooling | ||

| Industrial Ink-jet Printing | ||

| By End-user Industry | Healthcare & Life Sciences | |

| Electronics & Semiconductors | ||

| Chemical & Process | ||

| Environmental Monitoring | ||

| Automotive & Aerospace | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the Micropumps market in 2030?

The sector is forecast to reach USD 6.79 billion in 2030 on the back of a 17.7% CAGR.

Which pump type currently generates the highest revenue?

Piezoelectric designs lead with 52.4% of 2024 turnover due to broad applicability in medical and cooling tasks.

Why is Asia-Pacific expected to grow faster than other regions?

Sovereign semiconductor policies, large-scale manufacturing capacity, and expanding healthcare access combine to produce a 16.9% regional CAGR.

Which application is expanding most quickly?

Electronics cooling is advancing at 17.4% CAGR as liquid loops displace air cooling in data centers and mobile devices.

How do regulatory cycles affect active implantable micropumps?

Extended validation periods, sometimes exceeding 2,700 days, raise development costs and delay time-to-market, although new FDA guidance aims to streamline verification steps.

What material challenges face piezoelectric micropump producers?

Supply volatility in lead zirconate titanate powders prompts dual-sourcing and research into alternative thin-film materials with comparable energy densities.

Page last updated on: