Aseptic Transfer System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

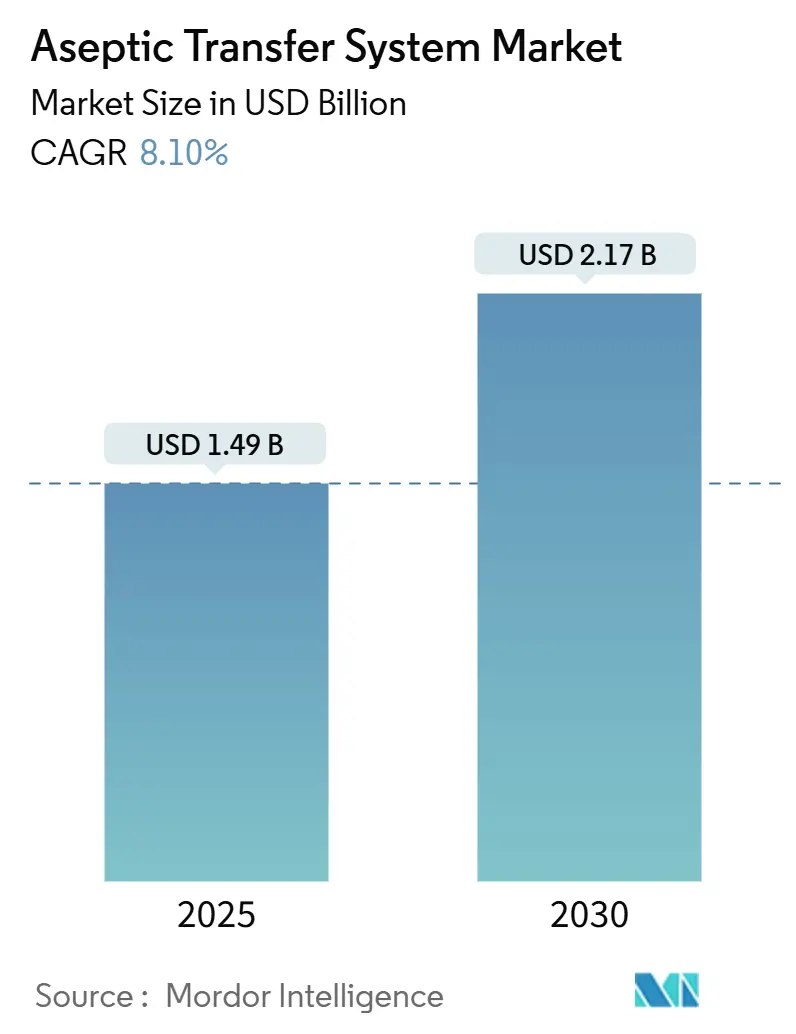

| Market Size (2025) | USD 1.49 Billion |

| Market Size (2030) | USD 2.17 Billion |

| Growth Rate (2025 - 2030) | 8.10% CAGR |

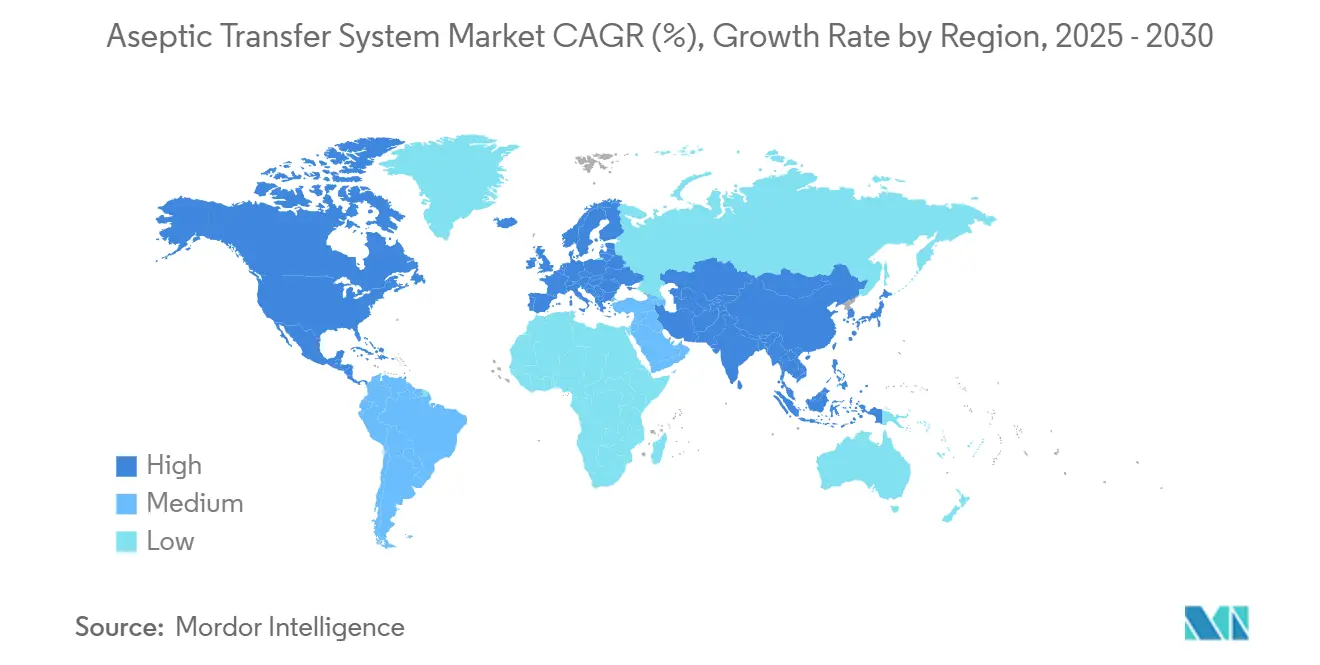

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aseptic Transfer System Market Analysis by Mordor Intelligence

The Aseptic Transfer System market size stood at USD 1.49 billion in 2025 and is forecast to reach USD 2.17 billion by 2030, registering an 8.1% CAGR over the period as pharmaceutical manufacturers adopt closed, contamination-free handling platforms that satisfy tightened regulatory expectations. Elevated spending on biologics fill-finish lines, the 2025 revision of EU GMP Annex 1, and parallel FDA guidance updates have transformed aseptic transfer from a routine operational safeguard into a board-level investment priority. North America remains the technology bellwether, yet fast-growing Asia Pacific production hubs are scaling capacity to serve both regional demand and global supply-chain diversification agendas. Across plants worldwide, single-use flow paths, modular cleanroom PODs, and robotics are converging to reduce human interventions, strengthen documentation, and shorten batch changeovers. Suppliers that combine hardware innovation with software connectivity and validation expertise are gaining pricing power, even though the competitive field is still moderately fragmented.

Key Report Takeaways

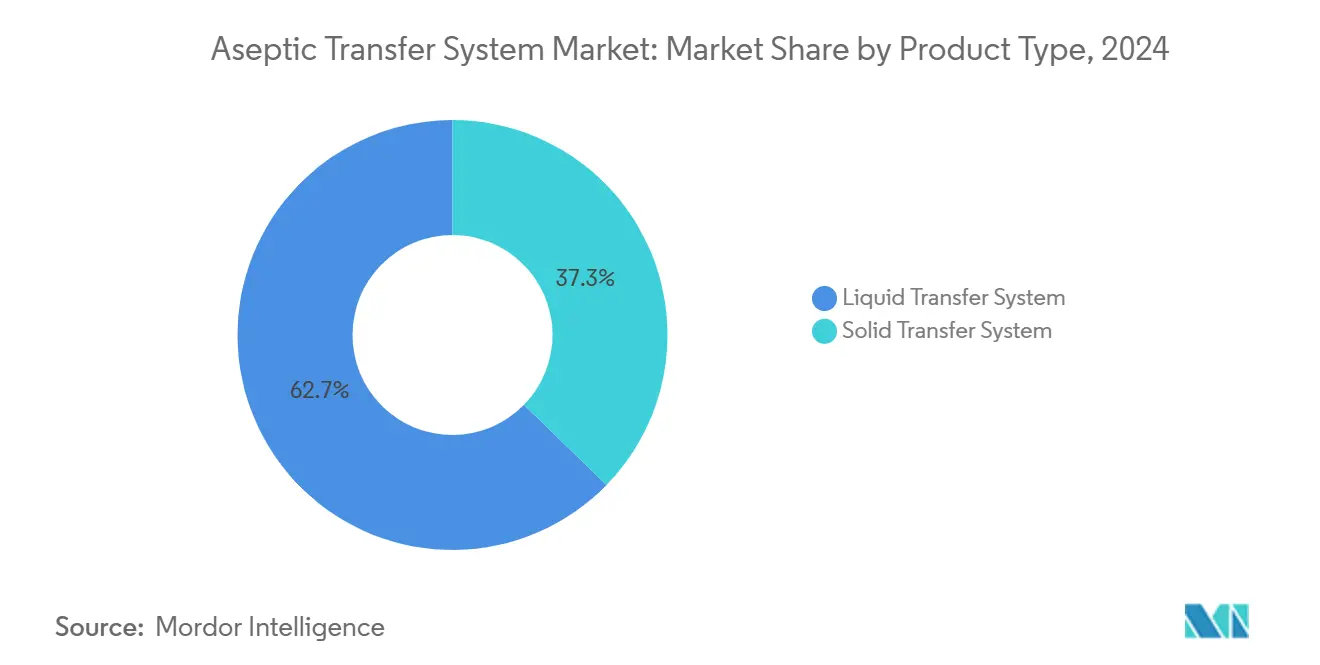

- By product type, Liquid Transfer Systems led with 62.7% revenue share in 2024, whereas Solid Transfer Systems are projected to expand at a 10.2% CAGR through 2030.

- By usability, multi-use platforms accounted for 58.3% of the Aseptic Transfer System market share in 2024, yet single-use variants are set to grow at a 12.5% CAGR to 2030.

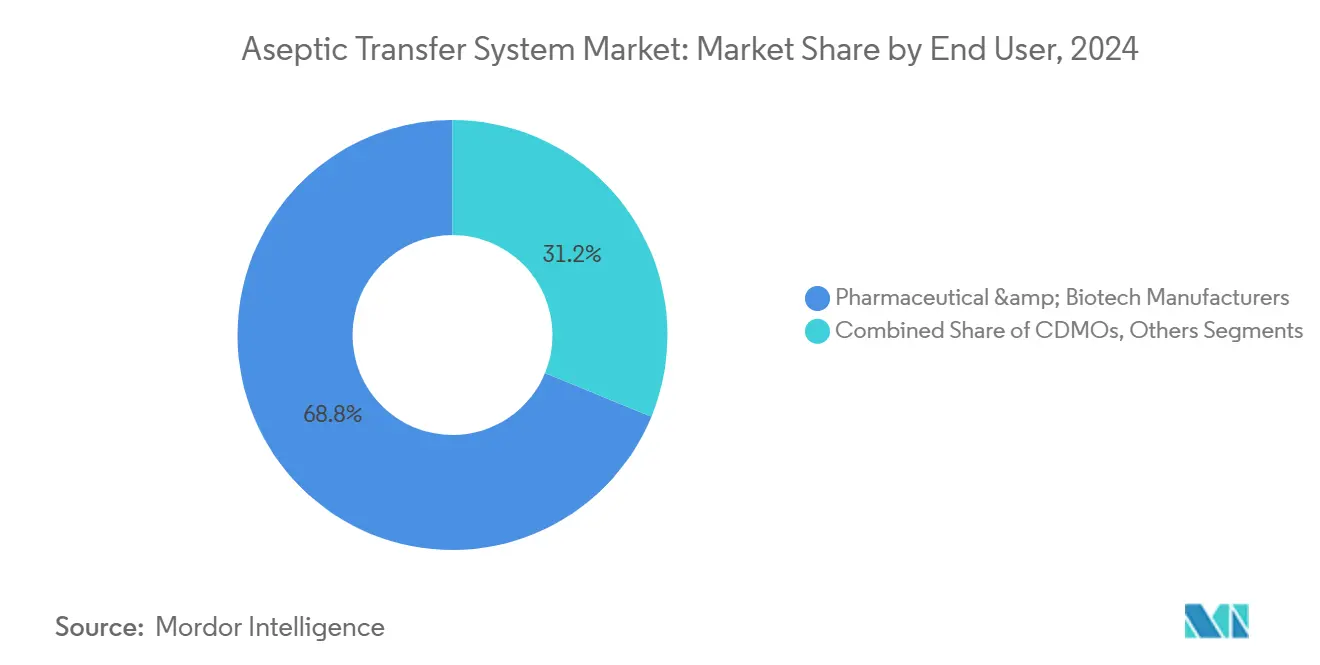

- By end user, Pharmaceutical & Biotech Manufacturers retained 68.8% share in 2024, while CDMOs are forecast to register the highest CAGR at 11.3% through 2030.

- Geographically, North America commanded a 34.2% share of the Aseptic Transfer System market in 2024, whereas Asia Pacific is advancing at an 11.8% CAGR to 2030.

Global Aseptic Transfer System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Global Demand For Sterile Pharmaceutical And Biologic Products | +1.80% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Intensifying Regulatory Focus On Contamination Control And Sterility Assurance | +1.50% | Global, led by EU and FDA jurisdictions | Short term (≤ 2 years) |

| Proliferation Of Single-Use And Modular Manufacturing Facilities | +1.20% | North America & APAC core, spill-over to Europe | Medium term (2-4 years) |

| Growing Outsourcing Of Fill-Finish Operations To CDMOs And CMOs | +1.00% | Global, with early gains in Asia Pacific | Long term (≥ 4 years) |

| Expansion Of High-Value Therapies Requiring High-Containment Handling | +0.90% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Digitalisation And Automation Of Aseptic Manufacturing Environments | +0.70% | Developed markets, gradual adoption in emerging regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Global Demand for Sterile Pharmaceutical and Biologic Products

Rising approvals of complex biologics—half of FDA’s 2024 new drug approvals—require closed transfer technology capable of maintaining sterility across intricate, temperature-sensitive workflow.[1]US Food and Drug Administration, “Novel Drug Approvals 2024,” fda.gov Manufacturers building capacity for cell- and gene-based medicines now specify modular, operator-free transfer nodes as standard, pushing the Aseptic Transfer System market toward integrated robotic solutions. Small-batch orphan drug pipelines further intensify the need for flexible systems that switch products without costly cleaning validation, solidifying demand for single-use assemblies. Across major hubs, procurement teams increasingly weigh contamination control metrics above unit throughput when selecting new lines, a change that supports sustained equipment premium pricing.

Intensifying Regulatory Focus on Contamination Control and Sterility Assurance

EU GMP Annex 1 now obliges sites to implement end-to-end Contamination Control Strategies, while FDA’s updated sterile processing guidance endorses risk-based, fully documented barrier technologies.[2]European Commission, “EudraLex Volume 4 – Annex 1 Manufacture of Sterile Medicinal Products,” ec.europa.eu Inspections show a jump in production-record-review observations, spotlighting transfer breaches as a recurrent root cause. To avoid warning letters and import alerts, operators are investing in automated, closed systems with integrated environmental monitoring that cut direct human contact points by up to 90%. The regulatory clock is short, driving near-term capex surges and propelling the Aseptic Transfer System market.

Proliferation of Single-Use and Modular Manufacturing Facilities

Single-use flow paths demonstrate double-digit utility savings and eliminate cleaning agents, aligning with both environmental targets and faster facility start-ups. When combined with prefabricated cleanroom PODs, build times shrink from years to months, helping companies hedge against regional supply disruptions. This structural flexibility explains why emerging APAC biotech clusters leapfrog legacy stainless-steel builds, fuelling regional demand and reinforcing the Aseptic Transfer System market’s evolution toward disposable, plug-and-play architectures.

Growing Outsourcing of Fill-Finish Operations to CDMOs and CMOs

Global drug sponsors outsource aseptic fill-finish to de-risk capital exposure and tap specialist expertise. CDMOs respond by constructing large-scale Grade A/B modules with high-throughput isolators and fully integrated transfer tunnels, thereby deepening their pull on the Aseptic Transfer System market. Long-term service contracts embed next-generation transfer hardware as part of turnkey packages, accelerating technology refresh cycles industry-wide.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital And Validation Costs Of Implementing Advanced Transfer Systems | -1.30% | Global, particularly impacting smaller manufacturers | Short term (≤ 2 years) |

| Supply Chain Vulnerabilities For Critical Sterile Barrier Materials | -0.80% | Global, with acute impact in Asia Pacific | Medium term (2-4 years) |

| Technical Integration Challenges With Legacy Equipment And Processes | -0.60% | North America & Europe legacy facilities | Medium term (2-4 years) |

| Limited Skilled Workforce In Aseptic Processing Across Emerging Markets | -0.50% | Asia Pacific & Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital and Validation Costs of Implementing Advanced Transfer Systems

Top-tier barrier systems raise facility budgets by hundreds of USD per square foot, and full qualification can extend timelines by 18 months, straining cash flows of mid-tier manufacturers. Validation documentation now spans thousands of pages, often requiring external consultants. These expenses push some firms to delay upgrades, tempering the immediate expansion pace of the Aseptic Transfer System market.

Supply-Chain Vulnerabilities for Critical Sterile Barrier Materials

Single-use assemblies rely on specialized polymers and sterilization services concentrated in a handful of regions. Pandemic-era freight bottlenecks exposed this fragility and triggered component shortages that caused drug-product delays. Manufacturers are diversifying suppliers and stockpiling consumables, but extended lead times and dual-sourcing validations still curb the Aseptic Transfer System market’s near-term momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Liquid Systems Maintain Leadership, Solid Systems Accelerate

Liquid Transfer Systems commanded 62.7% share of the Aseptic Transfer System market in 2024, anchored by pervasive use of pre-filled syringes and parenteral biologics. Automation upgrades such as robotic filling workcells reduce bubble formation and enable ISO 5 compliance without laminar hoods. Yet Solid Transfer Systems, though smaller in absolute terms, are projected to grow at a 10.2% CAGR, catalyzed by potent oral oncology actives requiring high-containment vacuum or pressure-assisted transfer. The evolution toward oncology powders, personalized capsules, and continuous tableting widens the addressable base for solid-phase transfer equipment, translating to incremental revenue streams for suppliers.

Ongoing R&D focuses on hybrid platforms capable of handling both phases within a unified isolator, a shift that could blur segment boundaries while deepening customer stickiness. Meanwhile, innovators such as Dec Group promote contained powder systems that abolish gravity-feed constraints, enabling multi-storey plant retrofits without structural overhauls. These advances underpin sustained demand and reinforce the Aseptic Transfer System market’s strategic relevance in next-generation OSD and biologic facilities alike.

By Usability: Single-Use Revolution Gains Ground

Although multi-use stainless assemblies continue to dominate installed bases, single-use solutions are set to outpace them at a 12.5% CAGR through 2030 as sponsors prioritize agile, multi-product pipelines. Disposable bags, connectors, and ports almost eliminate cleaning validation, enabling rapid line changeovers critical for low-volume advanced therapies. Vendors now certify gamma-stable films and helium-tested surge bags to assure integrity under cold-chain conditions, broadening single-use applicability to vaccines and lipid nanoparticles.

Capital-intensive high-volume producers still opt for multi-use equipment to leverage depreciation, but rising water-for-injection and energy costs erode this economic edge. Regulatory shifts that scrutinize cross-contamination add strategic impetus toward disposables, sustaining the Aseptic Transfer System market momentum across greenfield and retrofit projects.

By End User: CDMOs Emerge as Catalysts

Pharmaceutical & Biotech Manufacturers accounted for 68.8% revenue in 2024, reflecting entrenched capacity at big-pharma campuses. Yet CDMOs show the strongest growth trajectory, clocking an 11.3% CAGR as innovators outsource complex fill-finish to specialists operating state-of-the-art modules. CDMOs amortize isolator costs across multiple clients, permitting continuous upgrades and accelerating technology diffusion across the wider Aseptic Transfer System market.

Industry partnerships reveal a trend toward bundled offerings: advanced transfer hardware, digital batch records, and end-to-end validation under single contracts. Smaller biotech firms value this integrated approach, freeing resources for discovery while ensuring compliance from first-in-human to commercial scale.

Geography Analysis

North America retains leadership with 34.2% revenue share, driven by stringent FDA oversight and fresh capital allocations aimed at reshoring critical drug production. Federal incentives encourage the build-out of biologic and mRNA capacity, compelling sites to specify higher-grade barrier isolation and automated transfer nodes that conform to Annex 1 and FDA guidance simultaneously.

Europe remains a mature yet technologically progressive market. Annex 1’s 2025 compliance deadline spurs retrofit campaigns across Germany, France, and Italy, favoring isolator-integrated transfer solutions that simplify Contamination Control Strategy documentation. Investment programmes by players such as Vetter reinforce regional demand while fostering cross-Atlantic equipment standardization.

Asia Pacific is the fastest-growing arena, expanding at an 11.8% CAGR. China and India leverage cost advantages and public funding to become global contract-manufacturing hubs. Plants designed from scratch adopt single-use, robot-ready transfer infrastructure, sidestepping legacy integration hurdles that slow Western retrofits. Southeast Asian nations, from Malaysia to Singapore, market themselves as alternative supply bases, further widening the regional Aseptic Transfer System market footprint.[3]International Society for Pharmaceutical Engineering, “Navigating the Asia-Pacific Pharmaceutical Landscape,” ispe.org

Competitive Landscape

The aseptic transfer system market remains moderately fragmented. Leaders such as Sartorius and Getinge exploit scale to supply complete isolation suites with consumable tie-ins, securing recurring revenue and customer lock-in. Sartorius generated EUR 3.4 billion in 2023, with 75% from sterile single-use products, underscoring the pull of disposables. Getinge, despite logistics disruptions, reported robust order intake in 2024 as hospitals and pharma sites upgraded containment.

Mid-tier innovators, including Syntegon-Telstar, capitalize on robotics, while regional specialists offer custom retrofits for legacy plants. Technological moats now centre on automation algorithms, integrated environmental monitoring, and software-defined maintenance rather than mechanical prowess alone. Partnerships between equipment OEMs and digital-platform providers signal an industry shift toward data-rich, predictive environments that reinforce client dependency and discourage price-led competition.

White-space remains in emerging regions where cost-conscious buyers seek performance at lower price points. Suppliers that adapt high-spec designs into modular, scalable packages stand to penetrate these segments without cannibalizing premium Western offerings, ensuring sustained inflows into the global Aseptic Transfer System market.

Aseptic Transfer System Industry Leaders

Sartorius AG

Getinge

ChargePoint Technology

ABC Transfer

Central Research Laboratories (CRL)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Thermo Fisher Scientific agreed to acquire Solventum’s purification and filtration business for USD 4.1 billion, strengthening its single-use bioprocessing portfolio

- February 2025: Jabil purchased Pharmaceutics International Inc., adding 360,000 sq ft of aseptic capacity to enter the CDMO arena

- October 2024: Recipharm and Exela Pharma Sciences formed a US-focused alliance capable of 100 million sterile units annually

- September 2024: SCHOTT Pharma, Gerresheimer, and Stevanato launched the Alliance for RTU to standardize ready-to-use containers

Global Aseptic Transfer System Market Report Scope

| Liquid Transfer System |

| Solid Transfer System |

| Single-Use |

| Multi-Use |

| Pharmaceutical & Biotech Manufacturers |

| Contract Development & Manufacturing Organisations (CDMOs) |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Liquid Transfer System | |

| Solid Transfer System | ||

| By Usability | Single-Use | |

| Multi-Use | ||

| By End-User | Pharmaceutical & Biotech Manufacturers | |

| Contract Development & Manufacturing Organisations (CDMOs) | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What factors are driving demand for modern aseptic transfer equipment?

Tightened FDA and EU Annex 1 rules, the rise of biologics and growing reliance on CDMOs are prompting rapid adoption of closed, automated transfer technologies.

Which product category leads global sales?

Liquid Transfer Systems hold 62.7% of 2024 revenue, reflecting the dominance of injectable biologics production.

How fast will single-use transfer assemblies grow?

Single-use solutions are projected to advance at a 12.5% CAGR through 2030 as manufacturers prioritise flexibility and lower cleaning validation costs.

Why are CDMOs important to future growth?

CDMOs spread equipment costs across multiple sponsors and continually invest in state-of-the-art modules, making them the fastest-growing end-user group at 11.3% CAGR.

Which region offers the highest growth potential?

Asia Pacific is expanding at an 11.8% CAGR due to cost-advantaged facilities, government incentives and improving regulatory alignment.

What is the role of digitalisation in this market?

AI-enabled environmental monitoring, mobile ISO 5 robots and digital twins are enhancing sterility assurance and uptime, adding new value layers to each equipment sale.

Page last updated on: