Infusion Pump Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

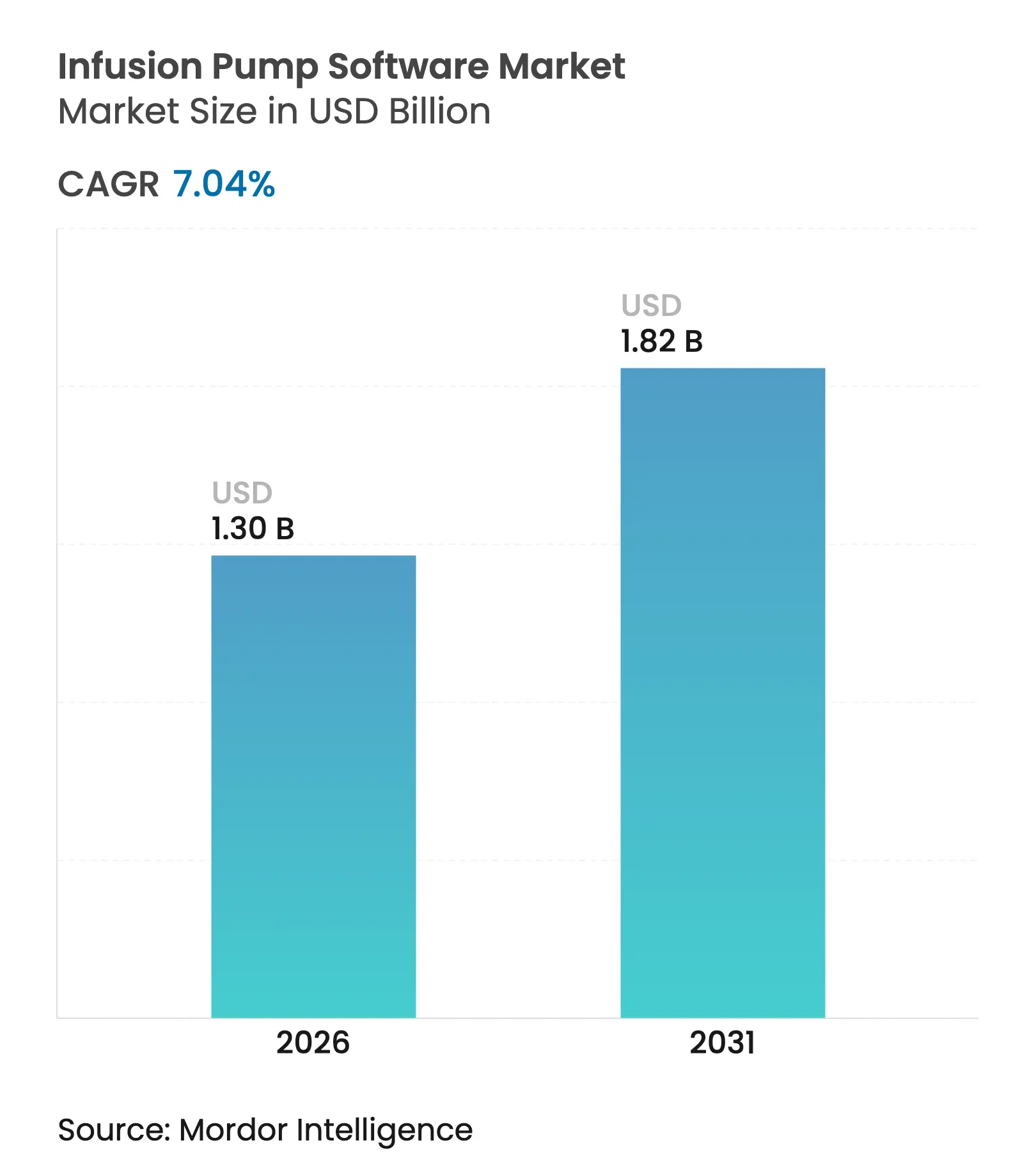

| Market Size (2026) | USD 1.3 Billion |

| Market Size (2031) | USD 1.82 Billion |

| Growth Rate (2026 - 2031) | 7.04 % CAGR |

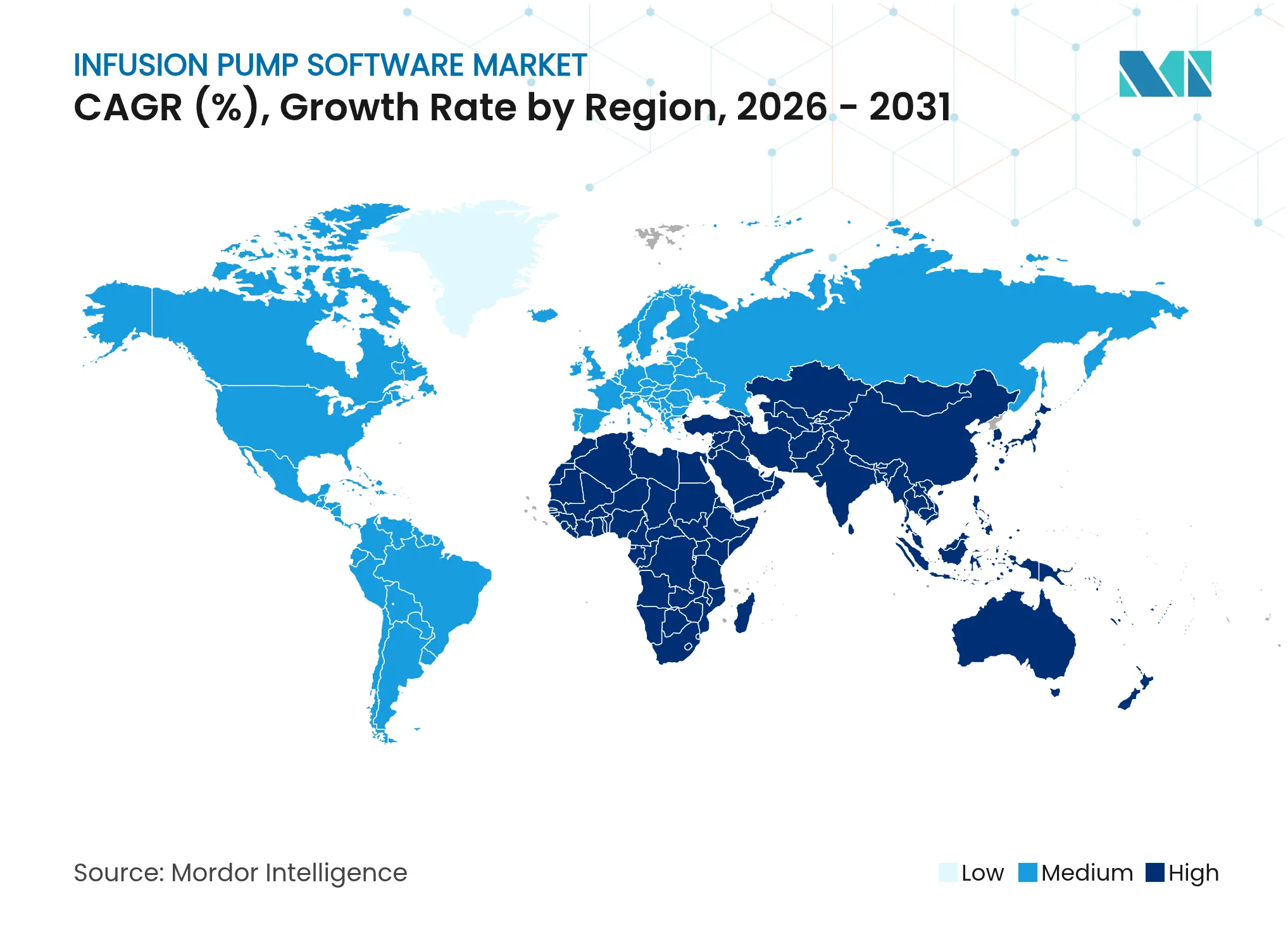

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

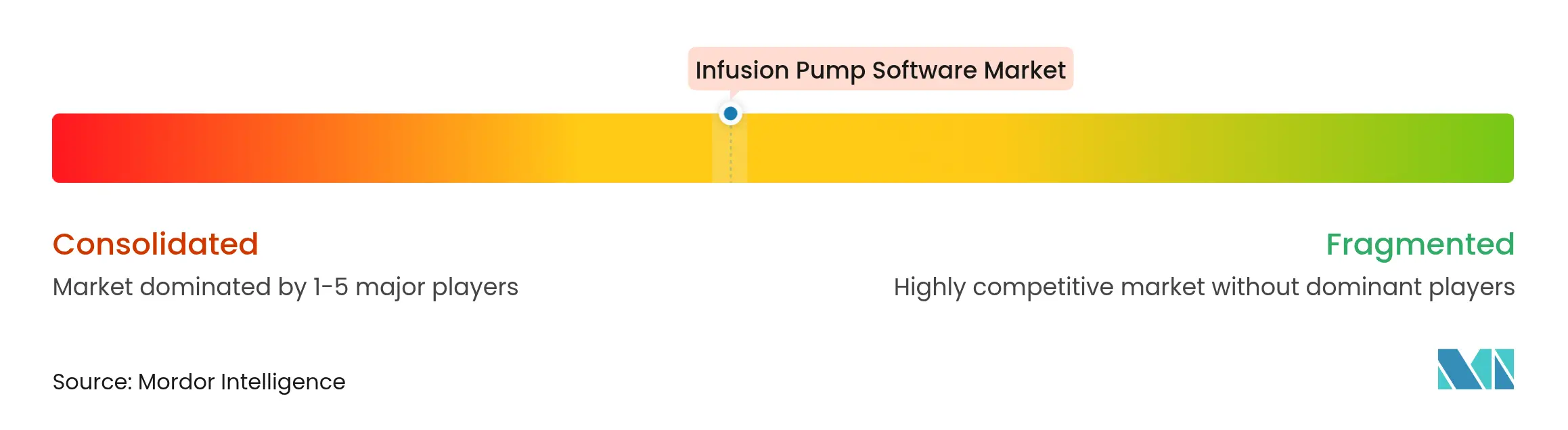

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Infusion Pump Software Market Analysis by Mordor Intelligence

Vendors benefit from mandatory cybersecurity filings, rising AI integration, and a shift toward outpatient care, all of which elevate the strategic importance of medication-delivery software. Regulatory scrutiny has intensified since the United States Food and Drug Administration (FDA) began rejecting premarket submissions that omit cybersecurity documentation, while the European Union Medical Device Regulation (EU-MDR) adds parallel pressure. Hospital digitalization, home-care expansion, and strong demand for predictive analytics together reinforce a stable mid-single-digit growth profile. North America remains the revenue anchor, yet Asia-Pacific is accelerating fastest as governments invest in connected medical devices and societies age. Competitive intensity now centers on software differentiation rather than pump hardware, and platforms that pair AI with drug-library updates gain pricing power and stickiness.

Key Report Takeaways

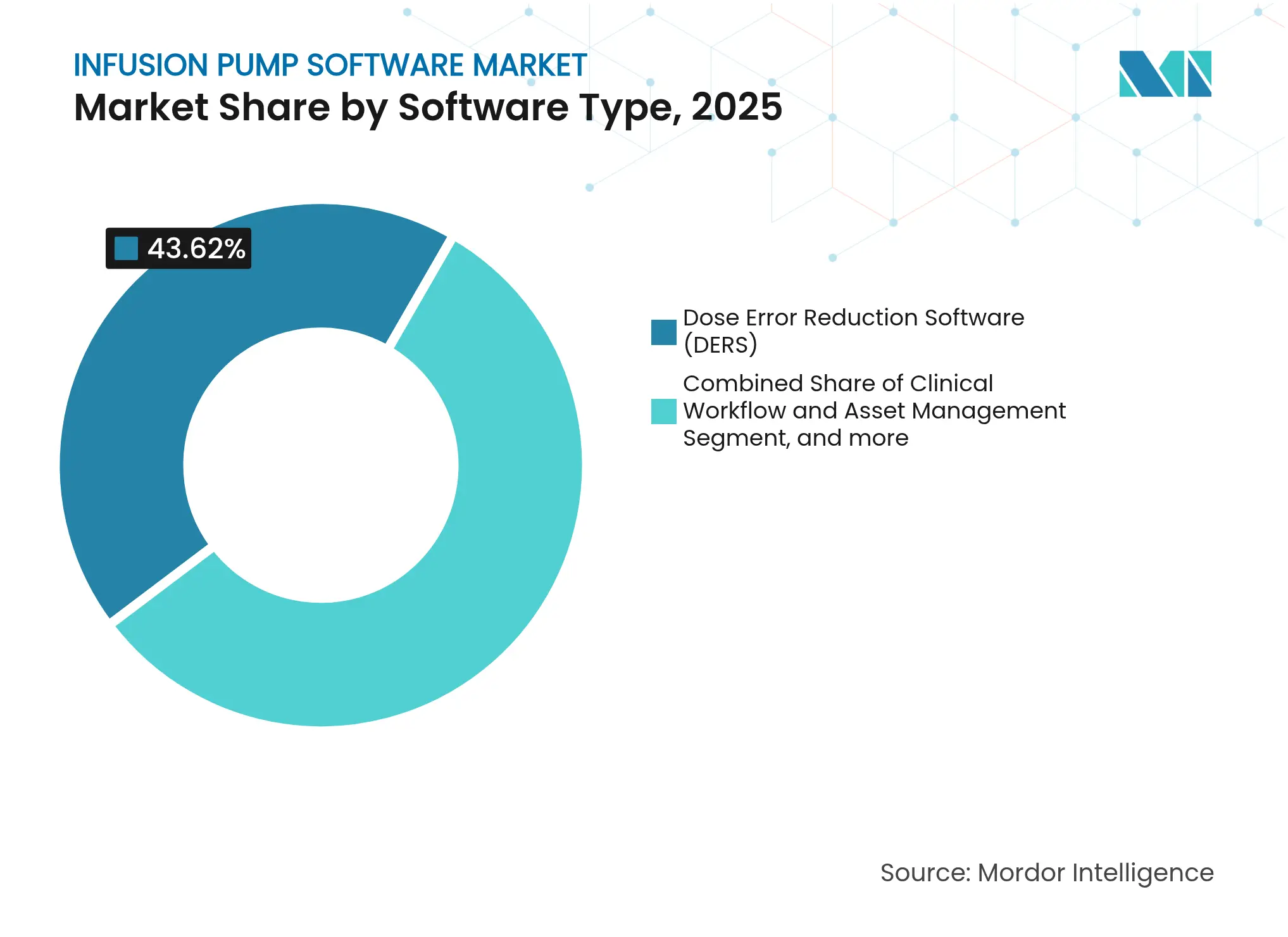

- By software type, dose-error-reduction programs led with 43.62% of infusion pump software market share in 2025, while AI-driven closed-loop control is projected to post an 8.63% CAGR through 2031.

- By application, pain and anesthesia management captured 32.41% of the infusion pump software market size in 2025, whereas insulin infusion software is expected to expand at a 9.66% CAGR up to 2031.

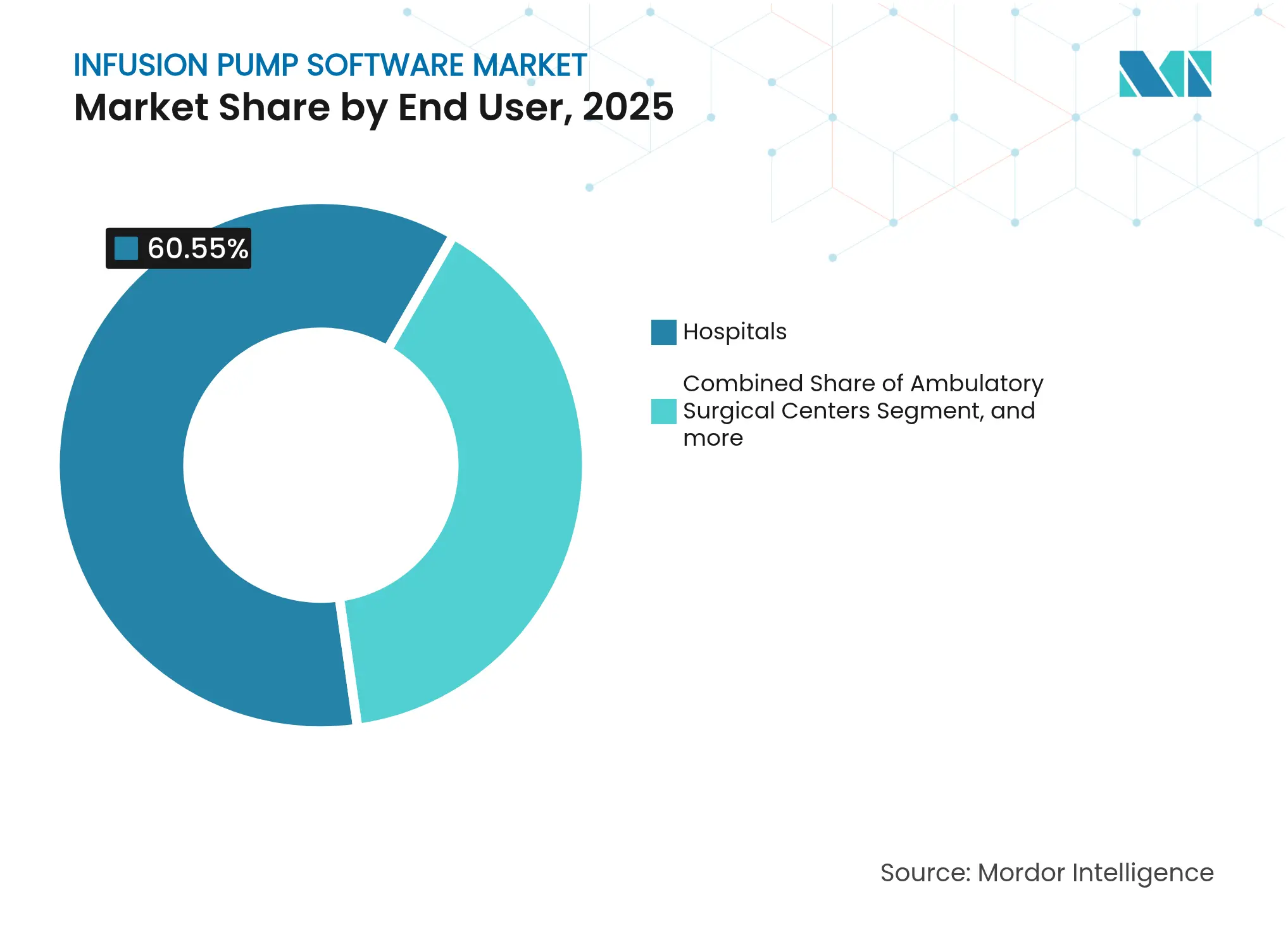

- By end user, hospitals held 60.55% share of the infusion pump software market in 2025, yet home-care settings are forecast to grow 11.79% annually to 2031.

- By geography, North America accounted for 41.12% of infusion pump software market revenue in 2025, while Asia-Pacific is on track for an 11.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Infusion Pump Software Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Increasing

Prevalence of Chronic Diseases

Increasing

Prevalence of Chronic Diseases

| +1.8% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

(~) %

Impact on CAGR Forecast

:

+1.8%

|

Geographic

Relevance

:

Global, with

concentration in North America & Europe

|

Impact

Timeline

:

Long term (≥

4 years)

|

Rising Demand

for Ambulatory & Home-Care Infusion Pumps

Rising Demand

for Ambulatory & Home-Care Infusion Pumps

| +1.5% | Global, led by North America and APAC | Medium term (2-4 years) | |||

Surge In

Global Surgical Volume

Surge In

Global Surgical Volume

| +1.2% | Global, with emerging market acceleration | Medium term (2-4 years) | |||

Enforcement

of FDA / EU-MDR Interoperability Mandates

Enforcement

of FDA / EU-MDR Interoperability Mandates

| +1.0% | North America & EU primarily | Short term (≤ 2 years) | |||

AI-Driven

Closed-Loop Infusion Algorithms

AI-Driven

Closed-Loop Infusion Algorithms

| +0.9% | North America & EU early adoption, APAC following | Long term (≥ 4 years) | |||

Escalating

Cybersecurity Requirements for Networked Devices

Escalating

Cybersecurity Requirements for Networked Devices

| +0.8% | Global, regulatory-driven in developed markets | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Increasing Prevalence of Chronic Diseases

Chronic conditions such as diabetes, cancer, and heart disease require continuous or recurrent medication delivery. Health systems therefore favor platforms that combine infusion accuracy with remote titration features. Medtronic’s MiniMed 780G insulin system, which logged 11.8% revenue growth in 2024, demonstrates how closed-loop algorithms satisfy this need.[1]Medtronic plc, “Fiscal 2024 Annual Report,” medtronic.com Continuous monitoring lowers complication rates and reduces long hospital stays, creating a tangible return on investment for providers. Multiple payers now reimburse automated insulin delivery, further lifting adoption. As chronic-care caseloads rise through 2030, software that integrates wearables, drug libraries, and predictive dosing remains vital to provider workflow. This dynamic keeps the infusion pump software market on a structurally higher growth path.

Rising Demand for Ambulatory & Home-Care Infusion Pumps

Home-based treatment surged during the COVID-19 period and is now an accepted care norm. Patients prefer therapy in familiar surroundings, while payers see cost savings. Software interfaces must therefore be intuitive, secure, and compatible with consumer-grade networks. Remote dashboards alert nurses to occlusions or dose deviations, enabling early intervention. Vendors that layer AI on top of connectivity stand out by predicting adverse events before they escalate. As outpatient reimbursement widens, more chemotherapy, antibiotic, and hydration regimens shift into residences, feeding additional demand for feature-rich software suites. The infusion pump software market gains long tail growth as each new therapy class moves outside the hospital.

Surge in Global Surgical Volume

Elective and minimally invasive procedures have rebounded, and enhanced recovery protocols need precise anesthetic and fluid control. Target-controlled infusion pumps, now exceeding 60,000 units worldwide, run pharmacokinetic models to match dosage with patient physiology.[2]Journal of Anaesthesiology Clinical Pharmacology, “Worldwide Utilization of Target-Controlled Infusion Pumps,” jAnaesthClinPharm.org Real-time analytics shorten extubation times and cut drug wastage. Robotic surgery platforms are also integrating infusion control loops, adding incremental software revenue per procedure. Hospitals that adopt these solutions document lower postoperative complications, feeding a virtuous cycle of investment. Consequently, the infusion pump software market secures a resilient revenue stream from perioperative care.

Enforcement of FDA / EU-MDR Interoperability Mandates

Since October 2023, the FDA has required cybersecurity specifications under Section 524B for every networked medical device submission. Hospitals must upgrade or replace legacy pumps lacking authenticated patches or encrypted communication. Parallel EU-MDR rules cause approval bottlenecks, with only 43 notified bodies reviewing roughly 500,000 device files. Vendors with mature quality-management systems, therefore, win share as smaller firms struggle to certify products. Clinical studies show a 15.4% to 90.5% error reduction when pumps link to electronic health records, reinforce the regulatory push.[3]Dove Medical Press, “Smart Infusion Pump Interoperability Impact on Medication Errors,” dovepress.com Compliance costs rise in the near term, but reward manufacturers that build secure, interoperable ecosystems.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Frequent

Product Recalls & Safety Alerts

Frequent

Product Recalls & Safety Alerts

| -1.2% | Global, with higher impact in regulated markets | Short term (≤ 2 years) |

(~) %

Impact on CAGR Forecast

:

-1.2%

|

Geographic

Relevance

:

Global, with

higher impact in regulated markets

|

Impact

Timeline

:

Short term (≤

2 years)

|

Limited

Wireless Connectivity in Low-Resource Settings

Limited

Wireless Connectivity in Low-Resource Settings

| -0.8% | APAC emerging markets, Sub-Saharan Africa | Medium term (2-4 years) | |||

High

EHR-Integration & Validation Costs

High

EHR-Integration & Validation Costs

| -1.0% | North America & EU primarily | Medium term (2-4 years) | |||

Needle-Free

& Subcutaneous Delivery Alternatives

Needle-Free

& Subcutaneous Delivery Alternatives

| -0.7% | Global, with early adoption in developed markets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Frequent Product Recalls & Safety Alerts

High-profile recalls erode provider confidence. In 2024 the FDA issued a Class I recall covering 50,743 Medfusion syringe pumps due to software faults that could delay therapy. Fresenius Kabi later pushed corrective patches for its Ivenix platform to resolve under-infusion risks. Hospitals respond by demanding longer warranties, live patch verification, and reference installations. These steps lengthen sales cycles and raise customer-acquisition costs. Vendors must now balance rapid feature releases with exhaustive validation, and those unable to prove reliability risk exclusion from tender lists.

Limited Wireless Connectivity in Low-Resource Settings

Many rural clinics in emerging economies lack stable broadband coverage. Cloud dashboards and over-the-air updates therefore stall or perform inconsistently. Manufacturers develop hybrid modes that store logs locally and synchronize when networks recover, but the extra coding inflates project timelines. Feature parity across regions also suffers, pressuring price points and limiting upgrades. Consequently, the infusion pump software market progresses unevenly, with advanced functions restricted to bandwidth-rich locales while basic safety software dominates low-resource segments.

Segment Analysis

By Software Type: DERS Dominance Faces AI Disruption

Dose-error-reduction software has long served as the cornerstone of hospital medication safety and held 43.62% of the infusion pump software market in 2025. Widespread formulary libraries flag concentration and rate mismatches before therapy starts, helping hospitals meet Joint Commission guidelines. Yet closed-loop control algorithms are scaling quickly and are on track for an 8.63% CAGR to 2031. These platforms ingest physiological data streams, model individual drug responses, and auto-adjust flow rates without clinician intervention. Hospitals see value in reduced alarm fatigue and tighter therapeutic windows, which in turn lowers sentinel events. The infusion pump software market size allocated to AI modules is therefore expanding by at least high single digits each year.

Clinical workflow and asset-management suites populate the mid-tier of customer demand. They improve pump fleet utilization and reduce rental costs through real-time location services and centralized firmware updates. Interoperability middleware has become the glue that binds pumps to electronic health records, pharmacy systems, and alarm servers. Cybersecurity packages entered purchasing checklists once Section 524B became law. The combination of these needs encourages larger vendors to sell bundled platforms, displacing point solutions. Software publishers that facilitate predictive maintenance with Internet-of-Things telemetry add yet another revenue layer. This multi-module strategy keeps the overall infusion pump software market on a diverse, innovation-led footing.

Note: Segment shares of all individual segments available upon report purchase

By Application: Pain Management Leadership Challenged by Diabetes Innovation

Pain and anesthesia workflows generated 32.41% of the infusion pump software market size in 2025. Perioperative teams rely on target-controlled infusion to titrate propofol and remifentanil precisely. Algorithms incorporate pharmacokinetic models validated in peer-reviewed trials, creating trusted clinical protocols. Enhanced-recovery programs further require tight fluid management, so anesthesiologists adopt advanced dashboards that permit rapid parameter changes. Higher surgical throughput sustains license renewals, cementing this segment’s revenue base.

Insulin infusion software is the fastest riser, with a 9.66% CAGR projected through 2031. Automated pancreas systems fuse continuous glucose monitoring with dose calculators to keep glucose within narrow ranges. Payers approve these systems due to demonstrated reductions in emergency admissions and long-term complications. Chemotherapy infusion also grows as precision oncology tailors body-surface-area dosing and leverages pharmacogenomics. Parenteral nutrition modules handle complex metabolic targets for critical-care patients while antimicrobial stewardship programs push timed antibiotic infusions. Each added use case inserts new revenue streams, so vendors capable of modular expansion capture incremental share of the infusion pump software market.

By End User: Hospital Dominance Erodes as Home Care Accelerates

Hospitals owned 60.55% of infusion pump software market share in 2025. They deploy multilayer IT backbones that connect pumps, electronic health records, and central surveillance. Budget cycles align with regulatory upgrades, which makes hospitals the first buyers of cybersecurity-hardened releases. Yet reimbursement rules now encourage earlier discharge, so home-care installations are climbing at an 11.79% CAGR. Patients appreciate freedom from repeated outpatient visits, and payers value lower overhead. Software that highlights intuitive screens, voice prompts, and remote alerts therefore resonates in consumer settings.

Ambulatory surgical centers capture a moderate slice of demand by combining rapid case turnover with compact fleets of high-utilization pumps. Specialty infusion clinics address therapies like biologics for autoimmune diseases and monoclonal antibodies for oncology. They seek software that tracks vial wastage and integrates with inventory records. All non-hospital sites benefit when platforms remain cloud-agnostic, scale down to single-user dashboards, and support bring-your-own-device monitoring. As a result, end-user diversification acts as a durable tailwind for the infusion pump software market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America remained the highest-revenue region with 41.12% of 2025 sales, supported by early cybersecurity mandates, routine smart-pump auditing, and well-funded hospital IT teams. Providers in the United States demonstrate high drug-library compliance and quickly adopt AI-based closed-loop modules that promise outcome improvements. Canada follows the same path due to similar accreditation rules. Reimbursement clarity lets vendors price premium software confidently, keeping average selling prices firm.

Europe maintains a robust installed base but faces certification delays under EU-MDR. As only 43 notified bodies check filings, launch timelines extend, favoring incumbents with in-house regulatory staff. Strong data-privacy laws also prompt investment in encrypted data exchange, which lifts total cost of ownership and lengthens decision cycles. Despite these frictions, clinical leaders in Germany, France, and the Nordic countries remain eager for algorithms that lower medication errors, preserving a mid-single-digit demand pattern.

Asia-Pacific leads global growth with an 11.08% CAGR through 2031. Japan’s USD 40 billion medical device sector expands annually on the back of an ageing population and hospital digitization programs. China is scaling provincial procurement of smart pumps as it upgrades county hospitals. India, South Korea, and Australia each invest in national e-health networks that make pump-to-EHR integration easier. Rural connectivity gaps create a bifurcated market, yet metropolitan installations mirror Western purchasing patterns. The infusion pump software market therefore enjoys a broad demand spread across public and private sectors.

The Middle East and Africa plus South America represent emerging pockets. Tertiary centers in Saudi Arabia and the United Arab Emirates procure AI-ready software to meet medical-tourism standards. Brazil modernizes oncology clinics in major cities, but limited broadband in remote districts slows cloud deployment. These regions contribute incremental volume rather than shaping global pricing, yet they keep the addressable user base growing.

Competitive Landscape

Market Concentration

Market concentration is moderate. Established device manufacturers integrate proprietary software to reinforce hardware lock-in. Baxter’s Novum IQ launch reached 97% drug-library compliance one month post-activation, far exceeding the industry baseline of 84%. This performance differentiates Baxter in competitive tenders. Becton, Dickinson and Company (BD) extended its hemodynamic monitoring reach by acquiring Edwards Lifesciences’ critical-care unit for USD 4.2 billion in 2024, then layered algorithms for cerebral autoregulation prediction onto the combined product line BD. Such moves widen product portfolios and raise cross-selling potential.

ICU Medical pursues precision dosing with its Plum Solo IV pump, securing 510(k) clearance in April 2025. The company bundles LifeShield safety software to form a cohesive platform that addresses both hospital and outpatient workflows. Fresenius Kabi emphasizes scalable cloud dashboards within its Ivenix line, positioning itself as a connectivity leader. Smaller startups focus on cloud-only models, mobile phone control, or niche algorithms such as pediatric drug titration. They rely on software agility but face high regulatory costs and limited installed bases.

Cybersecurity robustness now sits at the top of buyer checklists. Vendors issue scheduled patches, penetration-test certificates, and Software Bill of Materials (SBOM) disclosures to satisfy Section 524B. Platforms able to ingest EHR data without middleware earn faster acceptance. Consequently, pure-hardware advantages diminish while code quality, analytics, and service wraparounds determine contract awards. Market share therefore shifts toward companies that demonstrate measurable reductions in adverse drug events and faster clinical workflows.

Infusion Pump Software Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: ICU Medical Inc. has achieved a significant milestone with the receipt of 510(k) clearance from the U.S. FDA for its Plum Solo precision IV pump, adding a single-channel option to its established Plum Duo platform. The company has also received FDA clearance for enhanced versions of the Plum Duo and its LifeShield infusion safety software, marking the completion of the initial rollout of the ICU Medical IV Performance Platform.

- April 2025: BD launched HemoSphere Alta platform featuring AI-driven hemodynamic monitoring with Cerebral Autoregulation Index and Acumen Hypotension Prediction Index software, demonstrating advanced clinical decision support integration.

- March 2025: Baxter unveiled Voalte Linq device powered by Scotty assistant at HIMSS25, marking first voice-activated technology integration for hospital communication systems, expected to be available in second half of 2025.

- February 2025: Baxter reported fourth-quarter 2024 results highlighting strong Novum IQ infusion pump performance following FDA 510(k) clearance and Dose IQ Safety Software integration.

Table of Contents for Infusion Pump Software Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Increasing Prevalence of Chronic Diseases

- 4.2.2Rising Demand for Ambulatory & Home-Care Infusion Pumps

- 4.2.3Surge In Global Surgical Volume

- 4.2.4Enforcement of FDA / EU-MDR Interoperability Mandates

- 4.2.5AI-Driven Closed-Loop Infusion Algorithms

- 4.2.6Escalating Cybersecurity Requirements for Networked Devices

- 4.3Market Restraints

- 4.3.1Frequent Product Recalls & Safety Alerts

- 4.3.2Limited Wireless Connectivity in Low-Resource Settings

- 4.3.3High EHR-Integration & Validation Costs

- 4.3.4Needle-Free & Subcutaneous Delivery Alternatives

- 4.4Porter’s Five Forces Analysis

- 4.4.1Threat of New Entrants

- 4.4.2Bargaining Power of Buyers

- 4.4.3Bargaining Power of Suppliers

- 4.4.4Threat of Substitutes

- 4.4.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value in USD)

- 5.1By Software Type

- 5.1.1Dose Error Reduction Software (DERS)

- 5.1.2Clinical Workflow & Asset Management

- 5.1.3Interoperability Middleware

- 5.1.4AI-Driven Closed-Loop Control

- 5.1.5Predictive Maintenance & Analytics

- 5.1.6Cybersecurity & Compliance Suites

- 5.2By Application

- 5.2.1Pain & Anesthesia Management

- 5.2.2Insulin Infusion

- 5.2.3Chemotherapy

- 5.2.4Parenteral Nutrition

- 5.2.5Antibiotic & Antiviral Therapies

- 5.2.6Enteral Infusion

- 5.3By End User

- 5.3.1Hospitals

- 5.3.2Ambulatory Surgical Centers

- 5.3.3Home-care Settings

- 5.3.4Specialty Clinics & Infusion Centers

- 5.4By Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4Australia

- 5.4.3.5South Korea

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4Middle East & Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East & Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Baxter International

- 6.3.2B. Braun Medical Inc.

- 6.3.3Becton, Dickinson and Company

- 6.3.4Fresenius Kabi

- 6.3.5ICU Medical Inc.

- 6.3.6Medtronic

- 6.3.7Smiths Medical

- 6.3.8Q Core Medical Ltd

- 6.3.9Terumo Corporation

- 6.3.10Epic Medical

- 6.3.11Pfizer Inc.

- 6.3.12Mindray Medical International

- 6.3.13InfuSystem Holdings Inc.

- 6.3.14Roche Diagnostics

- 6.3.15Insulet Corporation

- 6.3.16Tandem Diabetes Care

- 6.3.17Flowonix Medical Inc.

- 6.3.18Ypsomed AG

- 6.3.19Zhejiang Kindly Medical Devices

- 6.3.20Micrel Medical Devices SA

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global infusion-pump software market as the full commercial value generated by embedded or add-on applications that set, monitor, and record infusion parameters across smart intravenous, enteral, and syringe pumps, as well as clinical dashboards that reside on the pump or its dedicated server. According to Mordor Intelligence, this universe spans Dose-Error-Reduction Systems, interoperability modules, workflow analytics, and asset-management tools that ship with or are licensed for active pumps worldwide.

Scope exclusion: hardware pumps, tubing sets, and standalone middleware that never executes on the pump are outside this analysis.

Segmentation Overview

- By Software Type

- Dose Error Reduction Software (DERS)

- Clinical Workflow & Asset Management

- Interoperability Middleware

- AI-Driven Closed-Loop Control

- Predictive Maintenance & Analytics

- Cybersecurity & Compliance Suites

- Dose Error Reduction Software (DERS)

- By Application

- Pain & Anesthesia Management

- Insulin Infusion

- Chemotherapy

- Parenteral Nutrition

- Antibiotic & Antiviral Therapies

- Enteral Infusion

- Pain & Anesthesia Management

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Home-care Settings

- Specialty Clinics & Infusion Centers

- Hospitals

- By Geography

- North America

- United States

- Canada

- Mexico

- United States

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Germany

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- China

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- GCC

- South America

- Brazil

- Argentina

- Rest of South America

- Brazil

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed biomedical engineers in tertiary hospitals, infusion-device product managers, and regulatory consultants across North America, Europe, and Asia-Pacific to verify attach rates, average software fees, and refresh triggers. Structured surveys with clinical pharmacists and home-care operators confirmed usage intensity and cloud-upgrade penetration that were not visible in public filings.

Desk Research

We gathered foundational data from open regulators such as the FDA MAUDE recall database, Eudamed vigilance notices, and the U.S. Centers for Medicare & Medicaid Services reimbursement files. Trade bodies, AAMI Infusion Standards Committee, HIMSS interoperability workgroups, and the International Diabetes Federation offered prevalence rates, installed-base clues, and software adoption benchmarks. Company 10-Ks, pump 510(k) summaries, patent analytics via Questel, and news flows in Dow Jones Factiva helped size revenues, licensing models, and upgrade cycles. D&B Hoovers supplied hard-to-find regional sales splits. The sources named are illustrative; many further publications and data portals fed into secondary validation.

Market-Sizing & Forecasting

A top-down construct begins with the global smart-pump installed base and annual shipments, rebuilt from trade statistics and manufacturer disclosures, which are then multiplied by verified software license penetration and average selling price. Supplier roll-ups and sampled contract checks provide a bottom-up reality check before final alignment. Key variables driving the model include smart-pump shipments, bed density per acute-care hospital, diabetes prevalence influencing insulin modules, elective surgery volume that raises analgesia software demand, and regulatory recall frequency that pulls forward replacements. Forecasts use multivariate regression blended with ARIMA to project each driver, after which scenario analysis adjusts for cybersecurity rule changes flagged by our experts. Data gaps in low-visibility countries are bridged through regional analogs vetted during primary calls.

Data Validation & Update Cycle

Outputs face variance checks against historical vendor revenue, import values, and hospital software spend; anomalies trigger rework and peer review. Reports refresh every twelve months, with interim flashes if a material recall, major acquisition, or reimbursement change shifts the baseline. A closing analyst pass ensures clients receive the latest view before release.

Why Mordor's Infusion Pump Software Baseline Commands Reliability

Benchmark comparison

Published estimates often diverge because firms mix hardware with software, assume uniform license fees, or freeze models for years. Mordor's disciplined scope, annual update cadence, and dual-path modeling anchor a figure purchasers can confidently deploy.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 1.21 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 0.43 B (2024) | Regional Consultancy A | excludes workflow and cloud-upgrade revenues | ||

USD 1.04 B (2024) | Global Consultancy B | lower ASP assumption, limited geographic coverage | ||

USD 10.30 B (2024) | Industry Association C | combines pump hardware and accessories with software |