Syringe Pumps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.91 Billion |

| Market Size (2031) | USD 6.06 Billion |

| Growth Rate (2026 - 2031) | 4.27% CAGR |

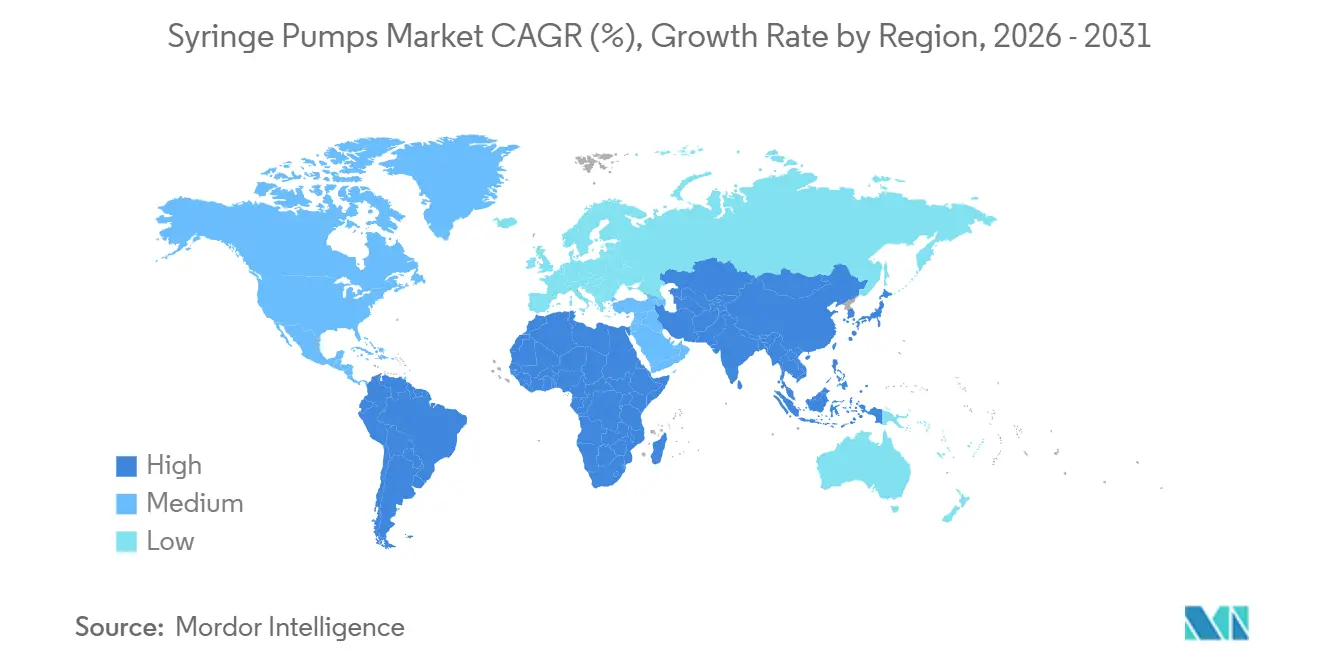

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

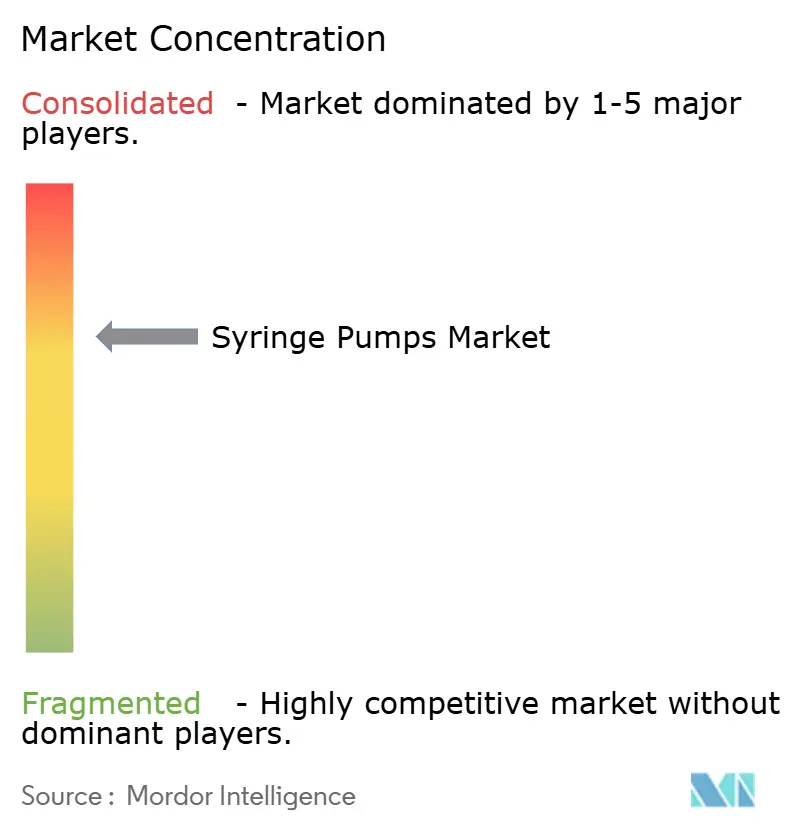

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Syringe Pumps Market Analysis by Mordor Intelligence

The Syringe Pumps Market size is expected to increase from USD 4.77 billion in 2025 to USD 4.91 billion in 2026 and reach USD 6.06 billion by 2031, growing at a CAGR of 4.27% over 2026-2031.

The forecast values underline a steady but not rapid expansion in line with the sector’s move from high-growth to mid-growth maturity. Progress is sustained by stricter cybersecurity rules, the spread of hospital automation, and rising chronic-disease prevalence, even as semiconductor shortages and post-pandemic budget discipline curb short-term momentum. North America dominates because Joint Commission rules compel dose-error reduction software, while Asia-Pacific is the clear volume engine, spurred by China’s Healthy China 2030 modernization plan and India’s critical-care build-out. Oncology infusions remain the largest end use, but veterinary critical care and home-based pain therapy appear as fresh pockets of demand. Competitive pressure revolves around smart-pump interoperability and long-term service contracts rather than headline device price, with five global suppliers already holding a majority of revenue.

Key Report Takeaways

- By type, infusion syringe pumps commanded 64.36% of syringe pumps market share in 2025, while programmable pumps are advancing at an 8.24% CAGR through 2031.

- By channel, single-channel devices held 39.52% share in 2025; multi-channel systems are projected to expand at a 7.11% CAGR between 2026 and 2031.

- By application, oncology and chemotherapy led with 43.73% share in 2025, whereas veterinary medicine is forecast to post the fastest 6.33% CAGR through 2031.

- By end user, hospitals accounted for 71.22% of the syringe pumps market size in 2025, yet homecare settings are growing at a 6.83% CAGR over the same period.

- By geography, North America captured 42.42% market share in 2025, while Asia-Pacific is projected to record the highest 7.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Syringe Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic diseases requiring continuous drug infusion | +0.9% | Global, centered in North America and Europe | Long term (≥ 4 years) |

| Growing number of surgical procedures globally | +0.7% | Global, strongest in Asia-Pacific | Medium term (2-4 years) |

| Increasing adoption of smart infusion systems and hospital automation | +1.1% | North America, European Union, urban Asia-Pacific | Medium term (2-4 years) |

| Expansion of outpatient chemotherapy services | +0.6% | North America, Western Europe, Australia | Short term (≤ 2 years) |

| Integration of closed-loop drug-delivery algorithms | +0.8% | North America, Germany, United Kingdom | Long term (≥ 4 years) |

| Surge in veterinary critical care demand | +0.3% | North America, Western Europe, urban China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Diseases Requiring Continuous Drug Infusion

Global non-communicable diseases are projected to cause 73% of all deaths by 2030, ensuring a durable need for precise infusion platforms. Syringe pumps titrate vasopressors in heart-failure management and insulin in diabetic ketoacidosis where a 10% mis-dose risks arrhythmia. U.S. hospital admissions for acute heart failure rose 19% between 2023 and 2025, mirrored by a 22% uptick in critical-care pump use.[1]American Heart Association, “Heart Failure Hospitalization Trends 2023-2025,” American Heart Association, heart.org The diabetic population requiring intensive insulin therapy already exceeds 537 million and continues to expand at a double-digit rate, locking in demand for network-ready smart pumps that liaise with continuous glucose monitoring.[2]International Diabetes Federation, “IDF Diabetes Atlas 2024,” International Diabetes Federation, idf.org Oncology maintains the largest clinical footprint; however, the pivot to oral targeted medicines in select cancers could trim future growth in legacy chemotherapy infusions. Overall, the driver adds 0.9 percentage points to the long-term syringe pumps market CAGR.

Increasing Adoption of Smart Infusion Systems and Hospital Automation

Hospitals are migrating from siloed volumetric pumps to networked syringe fleets linking directly to electronic medical records via HL7 FHIR interfaces. By the end of 2025, 68% of U.S. hospitals with more than 200 beds had interoperable platforms in place, up from 41% in 2023. Automated drug-library uploads slash manual entry by 87% and cut programming time per infusion from 4.2 to 1.1 minutes, freeing clinician bandwidth. The European Union’s Medical Device Regulation escalates post-market surveillance duties, compelling suppliers to build secure over-the-air patch processes. Budget-constrained hospitals in emerging markets stretch replacement cycles, but refurbished smart pumps offer an on-ramp, sustaining penetration. With a +1.1% contribution, this driver carries the highest positive weight on the syringe pumps market outlook.

Expansion of Outpatient Chemotherapy Services

Outpatient infusion centers delivered 61% of U.S. chemotherapy cycles in 2025 as payers promoted lower-cost care settings. Portable pumps under 500 grams let patients keep mobility during 48-hour 5-fluorouracil infusions, saving an average 3.2 inpatient days per cycle. Updated guidelines from the National Comprehensive Cancer Network now endorse home-based administration for selected tumors.[3] Robert W. Carlson, “NCCN Guidelines for Home-Based Chemotherapy Infusion,” National Comprehensive Cancer Network, nccn.org Battery life remains a constraint; current lithium-ion models last only 8-10 hours, pushing suppliers to pilot solid-state batteries that double runtime. The shift adds 0.6% to near-term growth for the syringe pumps market.

Integration of Closed-Loop Drug-Delivery Algorithms

Manufacturers embed predictive software that alerts clinicians 15 minutes before occlusion alarms, a feature validated in 2025 IEEE trials and credited with a 34% decline in nurse alert fatigue. The FDA’s cybersecurity law, Section 524B, forces “secure-by-design” architecture, which lengthens development cycles by 8-12 months but positions compliant suppliers to win procurement tenders. Hospitals pursuing zero-harm medication goals view closed-loop pumps as a strategic asset, lifting demand for premium programmable models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Medication errors and safety recalls | −0.5% | Global, strictest in North America and EU | Short term (≤ 2 years) |

| High acquisition and maintenance costs | −0.4% | Low- and middle-income countries | Medium term (2-4 years) |

| Supply-chain pressure on semiconductor components | −0.3% | Global, acute in U.S. and EU manufacturing hubs | Short term (≤ 2 years) |

| Increasing regulatory scrutiny on cybersecurity | −0.2% | North America, European Union, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Medication Errors and Safety Recalls Associated With Syringe Pumps

The FDA logged 47 Class I and II syringe-pump recalls from January 2024 to December 2025, with software faults and mechanical failures responsible for 72% of incidents. Baxter withdrew 13,800 Novum IQ pumps in September 2024 after firmware errors caused neonatal underdosing, prompting a safety bulletin. False high-pressure alarms on BD’s Alaris module generated clinician desensitization, a risk outlined in a 2025 Critical Care Medicine study. Only 38% of U.S. hospitals completed bi-annual competency checks in 2025 despite ISMP guidance. Recall-linked downtime and liability fears reduce trust and dent the syringe pumps market by 0.5 percentage points over the next two years.

High Acquisition and Maintenance Costs

Smart pumps list for USD 8,000–18,000 apiece versus USD 3,500 for basic models, while annual service contracts add another 12–18%. Many public hospitals in sub-Saharan Africa defer maintenance, producing downtime above 22% and limiting clinical access. Fresenius Kabi’s EUR 450 per-month leasing program cuts upfront investment by 70% but raises total cost over seven years by 23%. Budget pressure thus subtracts 0.4% from the medium-term syringe pumps market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Programmable Pumps Redefine Safety Standards

Infusion syringe pumps owned 64.36% of the syringe pumps market share in 2025, anchored by universal use in anesthesia and neonatal ICUs. Programmable models, however, post an 8.24% CAGR as hospitals seek devices that auto-populate drug libraries and cut transcription errors by 41%. Nine FDA-cleared designs released in 2024-2025 include predictive algorithms certified to IEC 60601-2-24, positioning them for premium adoption.

Basic pumps still serve settings with unstable electricity and scant IT support, yet their slice is shrinking, especially in China where Healthy China 2030 mandates dose-error reduction in tertiary centers. Withdrawal pumps face displacement from automated lab platforms, and dual syringe pumps, selling at USD 22,000, remain confined to high-complexity radiology suites. Over the forecast, programmable units move the syringe pumps market toward higher average selling prices and new recurring-software revenue streams.

By Channel: Multi-Channel Systems Gain ICU Traction

Single-channel devices held 39.52% market share in 2025 thanks to their ubiquity in outpatient clinics and veterinary practices. Intensive-care wards, though, are shifting to multi-channel pumps, attracted by the ability to co-infuse vasopressors, sedatives, and analgesics. These systems post a 7.11% CAGR and are backed by evidence showing a 27% cut in medication administration time and an 18% fall in line-related infections.

Dual-channel models remain popular in pediatric hospitals where antibiotic and fluid lines need isolation, but rapid European rules that demand unified cumulative-dose displays are rendering older units obsolete. IT upgrades for data-rich multi-channel integration can reach USD 500,000 for a mid-size hospital, yet Bluetooth Low-Energy-enabled designs lower the hurdle and accelerate adoption. Regulatory focus on end-to-end encryption further drives hospitals toward modern hardware portfolios.

By Application: Veterinary Medicine Emerges as Growth Outlier

Oncology and chemotherapy applications accounted for 43.73% of syringe pumps market share in 2025, underlining the need for tightly controlled cytotoxic delivery. Veterinary medicine, however, records the fastest 6.33% CAGR as pet owners increasingly authorize ICU-level interventions.

Anesthesia continues to expand on the back of growing surgical volumes, yet price commoditization in anesthetic agents restrains hardware budgets. Ultra-low flow neonatal pumps are constrained by a limited number of compliant models, fuelling demand for specialized designs. Pain management shifts to outpatient care as Medicare now reimburses ambulatory devices, supporting home use. Meanwhile, veterinary clinicians still repurpose human pumps, signaling a white-space opportunity for purpose-built low-flow hardware that could reshape this portion of the syringe pumps market size.

By End User: Homecare Settings Accelerate Amid Reimbursement Shifts

Hospitals represented 71.22% of end-user value in 2025, driven by stringent Joint Commission software mandates and high patient acuity. Yet homecare providers grow fastest at a 6.83% CAGR following Medicare’s durable medical equipment expansion that now funds ambulatory infusion pumps for chronic pain and parenteral nutrition.

Ambulatory surgical centers adopt pumps for same-day cases, but payer-driven opioid reduction lowers PCA demand. Clinics rely on bundled payment incentives but lag IT sophistication, keeping standalone pumps in service. Research laboratories purchase programmable devices with ultra-stable flow for microfluidics, a niche but stable contribution to the syringe pumps industry. Lost or damaged homecare units, at 12% per year, underline the importance of rugged design and asset-tracking features.

Geography Analysis

North America commanded 42.42% syringe pumps market share in 2025, buoyed by a USD 180 million Veterans Health Administration contract for ICU Medical’s Plum 360 systems and FDA cybersecurity mandates that lengthen rival product launches. Canada earmarked CAD 420 million (USD 310 million) in 2025 to replace legacy pumps, targeting 80% smart-pump penetration by 2028. Mexico expanded ICU capacity by 3,200 beds during 2024-2025, choosing refurbished pumps priced 40% below new imports to ease budget strain.

Asia-Pacific is projected at a 7.04% CAGR through 2031, making it the fastest-growing regional slice of the syringe pumps market. China’s CNY 2.1 trillion (USD 295 billion) Healthy China 2030 plan funds smart infusion infrastructure, while India’s National Health Mission adds 40,000 critical-care beds annually. Japan aligned its cybersecurity rules with IEC 80001 in April 2025, compelling domestic suppliers to retrofit encrypted modules. South Korea boosted reimbursement for smart-pump chemotherapy by 15% in 2025, accelerating oncology center upgrades. Australia approved four new programmable models but stretches replacement cycles to nine years amid flat capital budgets.

Europe holds steady share with Germany, France, and the United Kingdom accounting for 62% of regional volume in 2025. MDR-driven compliance costs rose by up to 22% per device, causing smaller suppliers to exit. Middle East and Africa show mixed performance: Gulf Cooperation Council states invest heavily, whereas sub-Saharan Africa faces persistent supply-chain gaps. South America benefits from Brazil’s purchase of 8,400 pumps for oncology services in 2024, though Argentina delays upgrades until macroeconomic stability returns.

Competitive Landscape

The syringe pumps market reflects moderate consolidation. Competition focuses on EHR interoperability, cybersecurity compliance, and lifecycle cost rather than upfront device pricing. Installed bases grant incumbents leverage to sell consumables and service contracts that deliver up to 38% of profit, creating switching friction.

ICU Medical’s 2022 acquisition of Smiths Medical merged two broad infusion portfolios and cut hospital IT integration costs by roughly 24%. Smaller firms pursue niches: Zyno emphasizes sub-400-gram ambulatory pumps and New Era supplies research labs with programmable micro-flow units. AI-enhanced occlusion prediction, proven to reduce alarm fatigue by one-third, emerges as a differentiator attractive to nurse leadership.

Regulatory adherence defines market access; IEC 60601-2-24 certification and Section 524B cybersecurity evidence are now prerequisite bid requirements. Fourteen Class I recalls in 2024-2025 illustrate the reputational risk of software defects, highlighting the need for robust quality systems. White-space opportunities persist in closed-loop insulin delivery and dedicated veterinary oncology pumps, segments still underserved by the top five players.

Syringe Pumps Industry Leaders

Becton, Dickinson and Company

B. Braun Medical

Baxter International Inc.

Fresenius Kabi AG

ICU Medical, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Terumo India introduced Terufusion Advanced Infusion Systems for ICU use in the country.

- May 2025: Penlon released the HP TCi Syringe Pump line featuring an intuitive 3-inch touchscreen and multiple target-controlled infusion models.

- April 2025: ICU Medical secured FDA 510(k) clearance for the Plum Solo precision IV pump that complements the dual-channel Plum Duo.

Global Syringe Pumps Market Report Scope

As per the scope of the report, syringe pumps are used to infuse fluid with medication or without medication in some circumstances. The syringe Pumps Market is segmented by Type (Infusion Pumps and Withdrawal Pumps), By End-User (Hospitals, Clinics, and Ambulatory Care Settings), Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America).

| Infusion Syringe Pumps |

| Withdrawal Syringe Pumps |

| Push-Pull / Dual Syringe Pumps |

| Programmable / Smart Syringe Pumps |

| Single-Channel |

| Dual-Channel |

| Multi-Channel (≥3) |

| Oncology & Chemotherapy |

| Anesthesia |

| Neonatal & Pediatric Care |

| Pain Management |

| Critical Care & ICU |

| Veterinary Medicine |

| Hospitals |

| Ambulatory Surgical Centers |

| Clinics |

| Homecare Settings |

| Research Laboratories |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Infusion Syringe Pumps | |

| Withdrawal Syringe Pumps | ||

| Push-Pull / Dual Syringe Pumps | ||

| Programmable / Smart Syringe Pumps | ||

| By Channel | Single-Channel | |

| Dual-Channel | ||

| Multi-Channel (≥3) | ||

| By Application | Oncology & Chemotherapy | |

| Anesthesia | ||

| Neonatal & Pediatric Care | ||

| Pain Management | ||

| Critical Care & ICU | ||

| Veterinary Medicine | ||

| By End-user | Hospitals | |

| Ambulatory Surgical Centers | ||

| Clinics | ||

| Homecare Settings | ||

| Research Laboratories | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the syringe pumps market and its growth outlook?

The market stands at USD 4.91 billion in 2026 and is projected to reach USD 6.06 billion by 2031, reflecting a 4.27% CAGR.

Which application holds the largest revenue share in syringe pump demand?

Oncology and chemotherapy account for 43.73% of global revenue based on 2025 data.

Why are programmable syringe pumps gaining traction?

Hospitals favor programmable models because HL7 FHIR connectivity cuts programming errors by 41% and supports cybersecurity compliance.

Which region is expanding fastest in syringe pump adoption?

Asia-Pacific leads with a forecast 7.04% CAGR through 2031, propelled by large-scale hospital modernization in China and India.

How are recalls influencing purchasing decisions for infusion devices?

Forty plus recalls in 2024-2025 heightened scrutiny; many hospitals now insist on secure-by-design pumps with predictive occlusion software to mitigate liability.

Page last updated on: