AI Writing Assistant Software Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

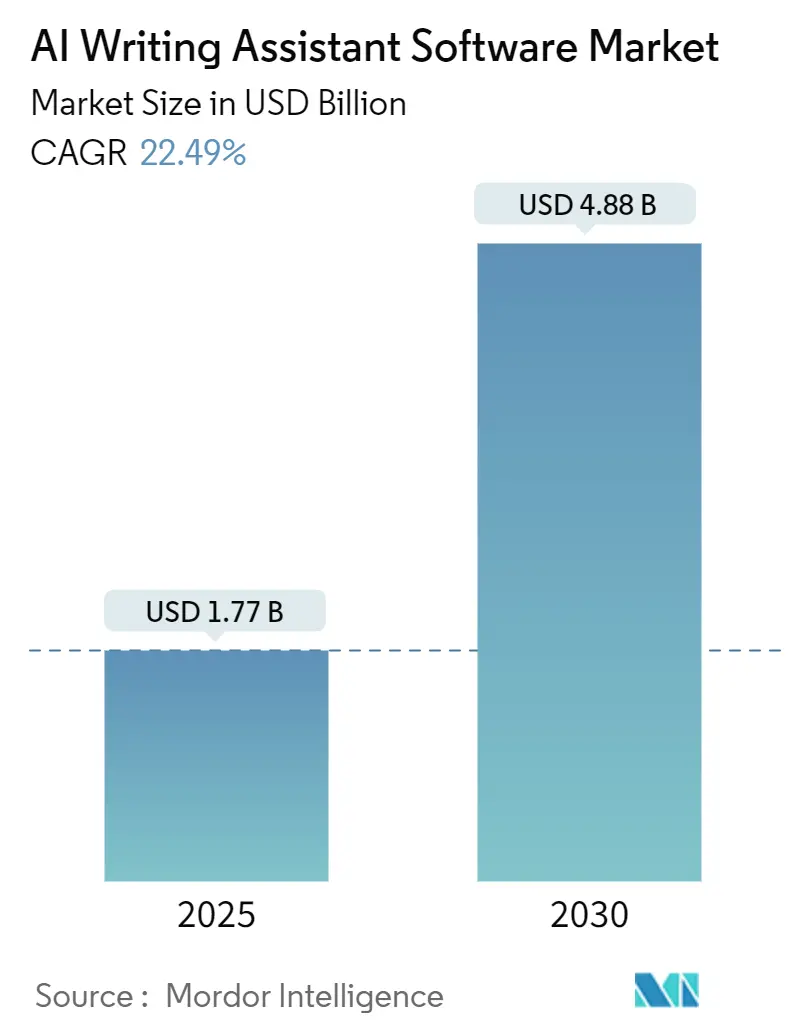

| Market Size (2025) | USD 1.77 Billion |

| Market Size (2030) | USD 4.88 Billion |

| Growth Rate (2025 - 2030) | 22.49% CAGR |

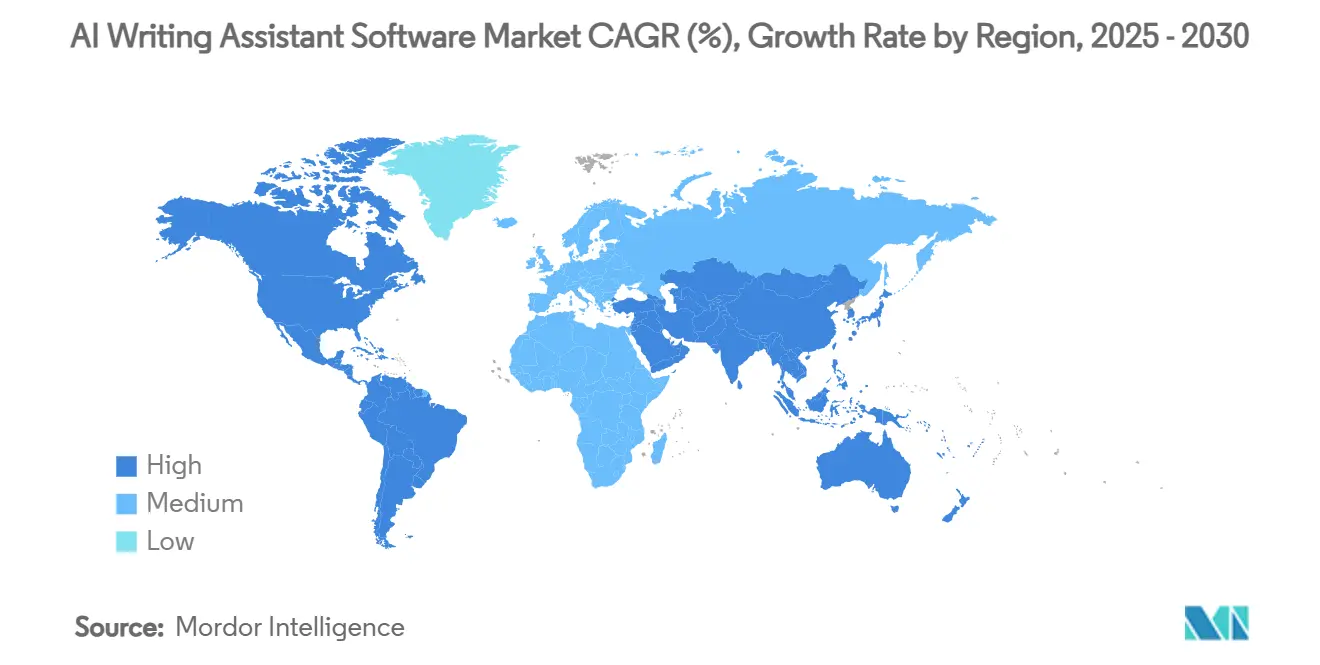

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

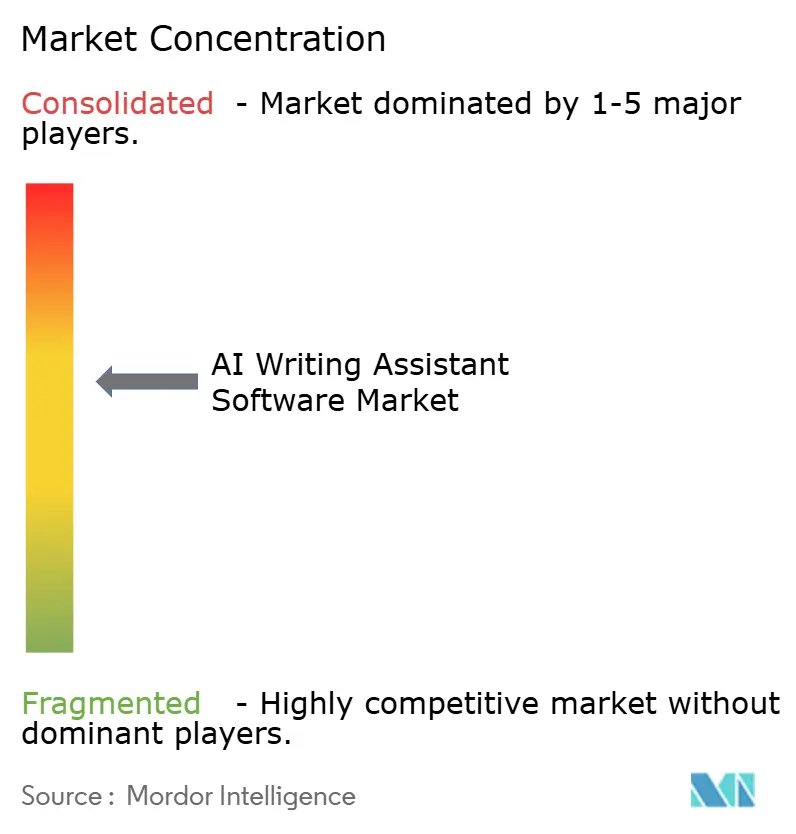

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

AI Writing Assistant Software Market Analysis by Mordor Intelligence

The AI writing assistant software market size stands at USD 1.77 billion in 2025 and is projected to advance to USD 4.88 billion by 2030, reflecting a 22.49% CAGR. The expansion is driven by rapid improvements in large-language-model performance, tighter enterprise security frameworks, and expanding use cases across highly regulated industries. Competitive activity is intensifying as technology platforms use capital scale to bundle writing assistants into productivity suites while specialist vendors differentiate through domain-tuned models and compliance features. Enterprises are moving past grammar-checking pilots toward full-workflow automation, shifting purchase decisions from experimental budgets to core productivity spending. On the supply side, GPU shortages are easing gradually, yet compute costs remain volatile and continue to influence pricing strategy across tiers of the AI writing assistant software market.

Key Report Takeaways

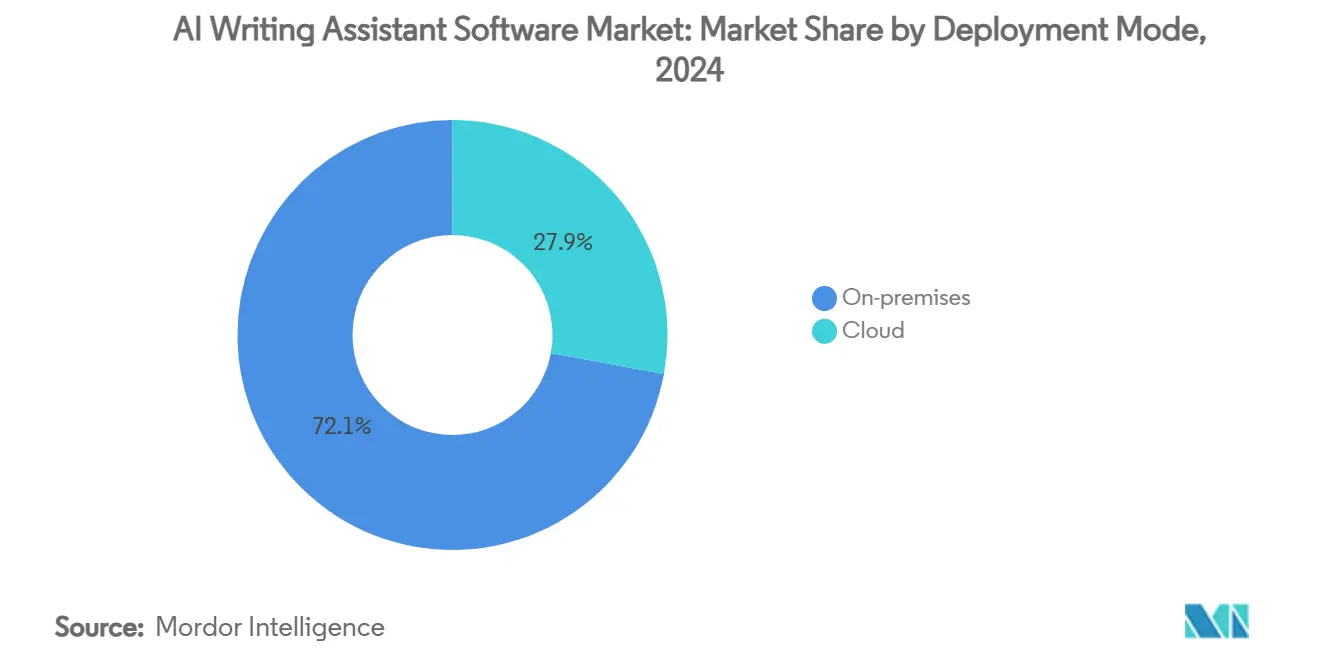

- By deployment mode, on-premises solutions held 72.1% of the AI writing assistant software market share in 2024 while cloud deployment is forecast to grow at a 24.2% CAGR through 2030.

- By organization size, large enterprises commanded 66.7% share of the AI writing assistant software market size in 2024; small and medium enterprises are projected to expand at 23.7% CAGR to 2030.

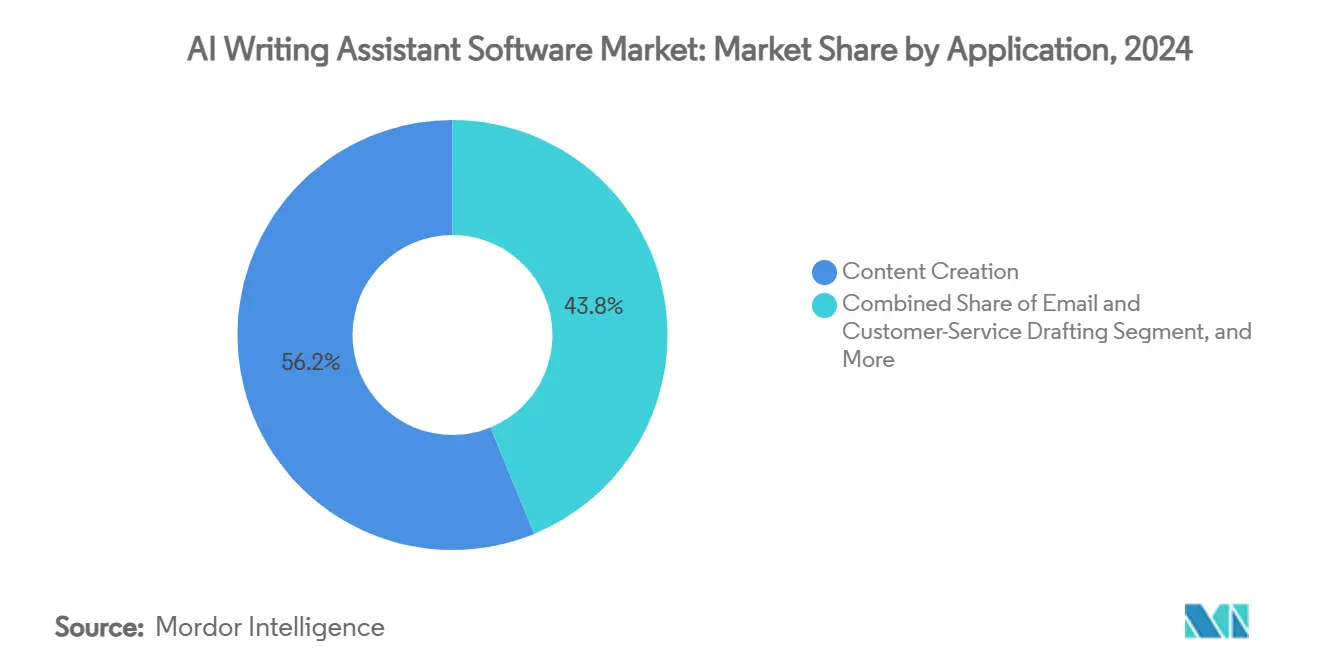

- By application, content creation accounted for 56.2% share of the AI writing assistant software market size in 2024 and academic and technical writing is advancing at a 23.1% CAGR through 2030.

- By end-user industry, IT and telecom led with 24.3% revenue share in 2024 while media and entertainment is set to record the fastest CAGR of 22.7% to 2030.

- By geography, North America retained 35.9% of the AI writing assistant software market share in 2024; Asia-Pacific is poised to grow at a 23.5% CAGR between 2025 and 2030.

Global AI Writing Assistant Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Generative-AI LLM capability escalation | +6.2% | Global | Short term (≤ 2 years) |

| Enterprise demand for productivity SaaS | +5.8% | North America, EU, APAC | Medium term (2-4 years) |

| Surge in digital-marketing content needs | +4.1% | Global | Medium term (2-4 years) |

| Remote and hybrid work communication growth | +3.7% | Global | Long term (≥ 4 years) |

| API-first bundling into vertical software | +2.9% | North America, EU | Medium term (2-4 years) |

| Private domain-tuned models for regulated use | +2.1% | North America, EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosive Growth of Generative-AI LLM Capabilities

Accelerated LLM research has lifted technical ceilings for writing assistants, allowing tools to deliver context-aware drafting, translation, and summarization at near-human quality. Capital concentration underpins this progress; Microsoft’s USD 13 billion commitment to OpenAI was cleared by UK regulators in March 2025, signaling confidence that continued scale is defensible. Enterprises now integrate advanced models behind corporate firewalls, replacing earlier single-function plug-ins with multi-agent systems that orchestrate brainstorming, outline generation, and tone adjustments. GPU advances enable larger context windows that reduce prompt engineering overhead. The result is faster iteration cycles and expanded domain coverage, positioning the AI writing assistant software market for sustained double-digit growth.

Rising Enterprise Demand for Productivity-Oriented SaaS Tools

Procurement teams treat writing assistants as foundational productivity infrastructure rather than experimental add-ons. Microsoft’s Copilot Control System, released in March 2025, embedded policy controls, permission tiers, and data logging that satisfy board-level governance standards.[1]Patton Seth, “Introducing Copilot Control System,” Microsoft Tech Community, microsoft.comFinancial-services and healthcare firms that once restricted AI now green-light internal pilots after security audits verify data residency and access logs. Purchasing committees increasingly tie payback calculations to measurable cycle-time reductions in proposal writing, customer-support scripting, and policy documentation. This outcome-driven lens produces stickier contracts with annual-recurring-revenue commitments that lengthen customer lifetimes and elevate the AI writing assistant software market value.

Surge in Digital-Marketing and SEO Content Requirements

The volume of brand content required to stay visible across owned channels, e-commerce listings, and social platforms is outstripping human bandwidth. AI writing assistants bridge the gap by generating first-draft product descriptions, landing-page copy, and localized posts in seconds, freeing marketers to refine voice and strategy. Concern about search-engine penalties continues, so enterprise users blend AI drafts with human edits and analytics feedback loops. Vendors answer with brand-style-guide training features that enforce approved terminology and guardrails, a capability that is becoming a baseline purchase criterion. As omni-channel marketing intensifies, the AI writing assistant software market sees consistent demand from agencies and in-house digital teams.

Remote and Hybrid Work Driving Up Digital Written Communication Volume

Permanent shifts to distributed work have multiplied asynchronous communication touchpoints. Email threads, chat updates, intranet posts, and project documentation now replace many synchronous meetings. Writing assistants help employees draft concise status summaries, translate technical jargon, and adjust tone across cultures, improving clarity and speed. Young knowledge workers natively adopt AI tools, accelerating penetration as they enter management roles. The remote-work catalyst, combined with BYO-AI policies inside global firms, reinforces baseline usage frequency and enlarges the active-user base of the AI writing assistant software market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and IP-ownership concerns | -4.3% | Global (EU focus) | Short term (≤ 2 years) |

| Hallucination and brand-risk | -3.8% | Global | Medium term (2-4 years) |

| GPU-compute shortages | -2.7% | North America, APAC | Short term (≤ 2 years) |

| Content watermarking regulations | -2.4% | EU, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and IP-Ownership Concerns

Mandatory labeling rules under the European AI Act took effect in May 2025, raising compliance costs as vendors retrofit watermarking pipelines.[2]“European AI Act: Mandatory Labeling for AI-Generated Content,” Imatag, imatag.com Global enterprises require audit trails, on-premises inference options, and granular permission controls before enabling AI on sensitive data. Contract clauses now demand liability coverage for copyright claims and explicit ownership of generated text. Vendors respond with private-instance deployments, differential-privacy techniques, and indemnity programs. These measures add sales-cycle complexity that slows short-term adoption yet ultimately professionalizes the AI writing assistant software market.

Hallucination and Brand-Risk Impacting Roll-Outs

Factual errors and inconsistent tone threaten brand credibility when AI drafts external content. Enterprises introduce multi-stage review workflows, reducing the time savings promised by automation. Vendors invest in retrieval-augmented generation, provenance tracking, and citation insertion to mitigate hallucination. Confidence scores and highlight-to-source features are becoming standard capabilities. While accuracy improvements continue, many firms limit AI use to internal documents before expanding outward, temporarily capping growth momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Accelerates Under Security Assurance

On-premises deployments held 72.1% of the AI writing assistant software market share in 2024 as chief information security officers preferred data-silo control for proprietary text. The segment remains vital among financial-services, healthcare, and defense organizations that manage stringent data-residency requirements. However, cloud-based offerings are forecast to post a 24.2% CAGR through 2030, the fastest of any deployment type. Vendors now provide private virtual networks, customer-managed keys, and region-locked GPU clusters that address sovereignty mandates while unlocking elastic capacity. As compute intensity of newer models rises, cloud economics create compelling total-cost-of-ownership advantages, prompting gradually rising migration rates even among compliance-sensitive clients.

The AI writing assistant software market size tied to cloud deployment is predicted to surpass on-premises spending by the end of the forecast period as multi-tenant architectures drive down marginal costs and accelerate feature delivery. In parallel, hybrid approaches allow real-time drafting in secure edge environments with heavy model fine-tuning executed in vendor clouds, offering a bridge for risk-averse institutions.

By Organization Size: SMEs Unlock Productivity Upside

Large enterprises captured two-thirds of revenue in 2024, leveraging specialist teams to integrate writing assistants into knowledge-management platforms. Their budgets favor multi-year enterprise agreements bundled into broader productivity stacks. The fastest growth, however, comes from SMEs, driven by subscription models that bundle advanced LLM access with intuitive dashboards. As smaller firms compete globally, they use AI to level the playing field in proposal writing, customer-support scripting, and multilingual marketing. The AI writing assistant software market size linked to SMEs is expected to nearly triple through 2030, outpacing overall market velocity.

Government-backed digital-transformation grants in developing economies further catalyze SME adoption by subsidizing cloud-based AI software. Lightweight APIs simplify integration into low-code environments, lowering technical barriers. Consumption-based pricing aligns with variable workloads, enabling seasonal industries to capture value without rigid license commitments.

By Application: Academic and Technical Writing Takes Center Stage

Content creation dominated 2024 revenue as marketing, blogging, and general business writing tools matured. Academic and technical writing now represents the most dynamic sub-segment, predicted to grow at more than 23% annually. Universities, research institutes, and R&D functions adopt AI to accelerate literature reviews, citation formatting, and plain-language translations. Domain-specific terminology libraries improve precision in engineering and life-science drafts, reducing iteration cycles between subject-matter experts and editors. Licensing partnerships with scientific-publisher databases further enhance reference accuracy.

Email drafting, customer-support case summarization, and meeting-minute generation remain steady growers. Coding-aware writing assistants that auto-document functions and generate component descriptions are nascent but illustrate how verticalized natural-language models expand total addressable markets. The AI writing assistant software market size allocated to specialized technical applications is likely to widen as regulated industries demand compliance-ready outputs with embedded citation trails.

By End-User Industry: Media and Entertainment Surges

IT and telecom commanded the largest share in 2024 owing to early experimentation with internal documentation and user-manual automation. Media and entertainment emerges as the fastest-growing industry adopter, buoyed by streaming services, publishing houses, and newsrooms racing to localize and personalize content across multi-format channels. AI tools generate synopses, headline variants, and subtitle drafts that accelerate editorial pipelines. Large entertainment groups increasingly train models on proprietary script libraries to maintain narrative voice consistency.

The BFSI sector deepens usage for regulatory reporting, risk commentary, and investor-relations briefs.[3]Tata Consultancy Services, "Generative AI in Finance: Opening up a Sea of Possibilities," tcs.com Healthcare organizations introduce AI-assisted clinical note generation inside electronic-health-record systems to reduce physician burnout. Government agencies pilot AI for citizen-facing communication, although procurement cycles and security reviews prolong roll-outs. Each vertical’s distinct compliance framework drives demand for configurable governance modules, fostering a diverse competitive landscape within the AI writing assistant software market.

Geography Analysis

North America accounted for 35.9% of 2024 revenue thanks to mature cloud infrastructure and sustained venture funding. The Microsoft–OpenAI investment approval underscored regulatory openness to AI growth. Nonetheless, Asia-Pacific is projected to record a 23.5% CAGR, faster than any other region, fueled by public-sector AI stimulus packages and rapid enterprise adoption following China’s USD 2.1 billion generative-AI spending in 2024. Baidu’s Wenku platform reaching 40 million paying users exemplifies local platform scale. Europe maintains solid uptake but faces higher compliance costs due to watermarking mandates, prompting demand for audits and provenance features.

Middle East and Africa along with South America present late-adopter profiles but benefit from improving connectivity and multilingual model support. Cross-border data-flow negotiations influence deployment decisions, with regionally hosted GPU clusters emerging to comply with sovereignty laws. The geographic dispersion of the AI writing assistant software market reinforces the need for localized training data and native-language UIs to unlock new revenue streams.

Competitive Landscape

The AI writing assistant software market is moderately concentrated yet highly dynamic. Platform incumbents such as Microsoft, Google, and Apple bundle assistants into operating systems and productivity suites, leveraging distribution advantages. Foundation-model providers like OpenAI and Anthropic license APIs to both platform players and independent software vendors. Enterprise-focused specialists including Writer and Jasper differentiate by offering domain-tuned models, on-premises deployment, and granular security controls.

Capital allocation trends highlight escalating stakes: Microsoft’s USD 13 billion OpenAI investment, Google’s cumulative USD 3 billion stake in Anthropic, and Writer’s USD 200 million Series C round underscore resource intensification. Consolidation is also evident as Grammarly acquired Coda to extend beyond proofreading into workspace collaboration. White-space opportunities persist in industry-specific templates, non-English language support, and agentic workflow automation that chains multiple writing tasks without human intervention. Competitive advantage increasingly hinges on compliance certifications, transparent model-auditing tools, and flexible deployment architectures aligning with customer trust requirements.

AI Writing Assistant Software Industry Leaders

-

Grammarly, Inc.

-

Microsoft Corporation (Copilot)

-

International Business Machines Corporation (watsonx Assistant)

-

Google LLC (Gemini)

-

OpenAI, Inc. (ChatGPT)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: OpenAI considers USD 3 billion acquisition of WindSurf to enhance AI coding assistant capabilities and compete directly with Microsoft’s GitHub Copilot, following failed attempts to acquire Anysphere and reflecting strategic focus on enterprise developer tools market.

- July 2025: Maestro Labs acquires Flowrite to build the largest independent AI email assistant, expanding into Gmail ecosystem across 150+ countries and leveraging funding from Microsoft and Softbank executives to compete with enterprise email automation solutions.

- June 2025: Microsoft and OpenAI experience partnership tensions over revenue sharing and technology access rights, with contentious AGI clause potentially eliminating Microsoft’s 20% revenue share if OpenAI achieves Artificial General Intelligence, creating market uncertainty about future collaboration.

- May 2025: Anthropic achieves USD 3 billion annualized revenue milestone, tripling growth in under one year through enterprise-focused code-generation AI models, reaching USD 61.4 billion valuation and positioning as primary OpenAI competitor in business applications.

Global AI Writing Assistant Software Market Report Scope

| Cloud |

| On-premises |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Content Creation |

| Marketing Copy and SEO |

| Email and Customer-Service Drafting |

| Academic and Technical Writing |

| Coding-Aware Writing Assist |

| Other Applications |

| Media and Entertainment |

| IT and Telecom |

| BFSI |

| Education |

| Healthcare and Life Sciences |

| E-commerce and Retail |

| Government and Public Sector |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Deployment Mode | Cloud | |

| On-premises | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

| By Application | Content Creation | |

| Marketing Copy and SEO | ||

| Email and Customer-Service Drafting | ||

| Academic and Technical Writing | ||

| Coding-Aware Writing Assist | ||

| Other Applications | ||

| By End-User Industry | Media and Entertainment | |

| IT and Telecom | ||

| BFSI | ||

| Education | ||

| Healthcare and Life Sciences | ||

| E-commerce and Retail | ||

| Government and Public Sector | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the AI writing assistant software market?

The AI writing assistant software market size is USD 1.77 billion in 2025 and is projected to reach USD 4.88 billion by 2030.

Which geographic region will grow the fastest through 2030?

Asia-Pacific is forecast to record a 23.5% CAGR, the fastest worldwide, supported by large-scale enterprise adoption and public-sector investment.

How large is the on-premises segment today?

On-premises deployment captured 72.1% of AI writing assistant software market share in 2024 due to data sovereignty concerns.

Which end-user industry is expanding quickest?

Media and entertainment is the fastest-growing industry segment, projected at a 22.7% CAGR from 2025 to 2030 as content volumes proliferate.

What is the primary restraint facing vendors in 2025?

Data-privacy and intellectual-property concerns remain the top restraint, particularly in the EU where new labeling rules have raised compliance costs.

Are small businesses adopting AI writing assistants?

Yes. SMEs constitute the fastest-growing organization segment, expected to post a 23.7% CAGR as subscription models and cloud delivery lower adoption barriers.

Page last updated on: