AI Code Tools Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

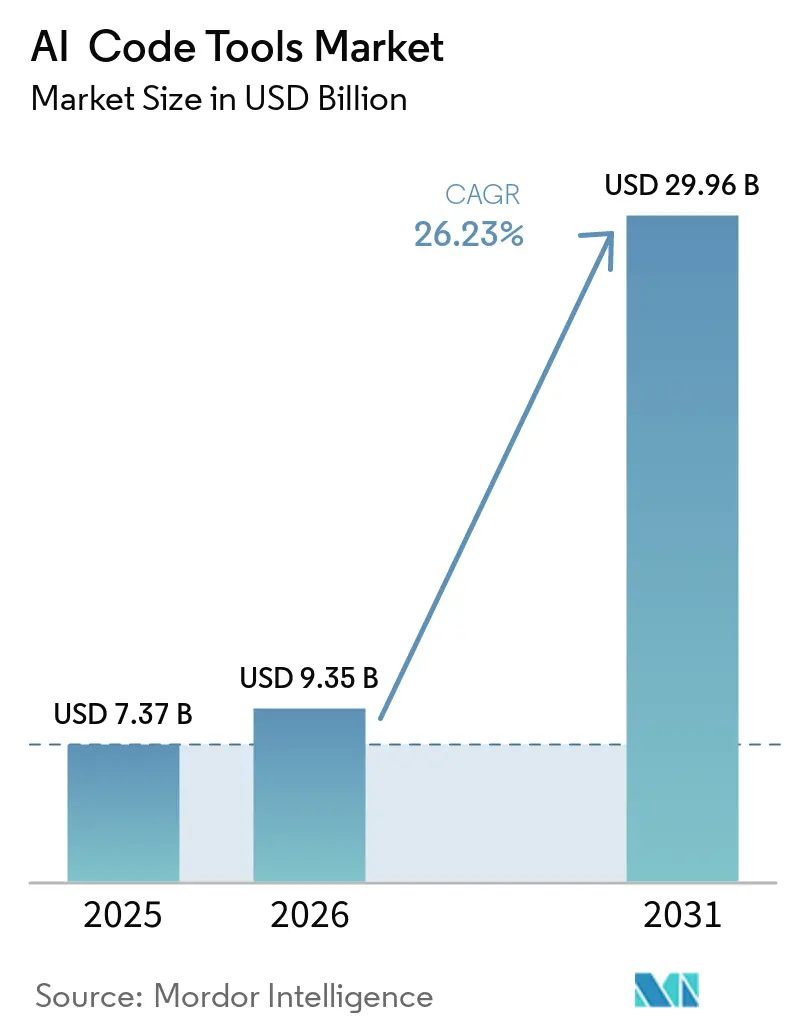

| Market Size (2026) | USD 9.35 Billion |

| Market Size (2031) | USD 29.96 Billion |

| Growth Rate (2026 - 2031) | 26.23% CAGR |

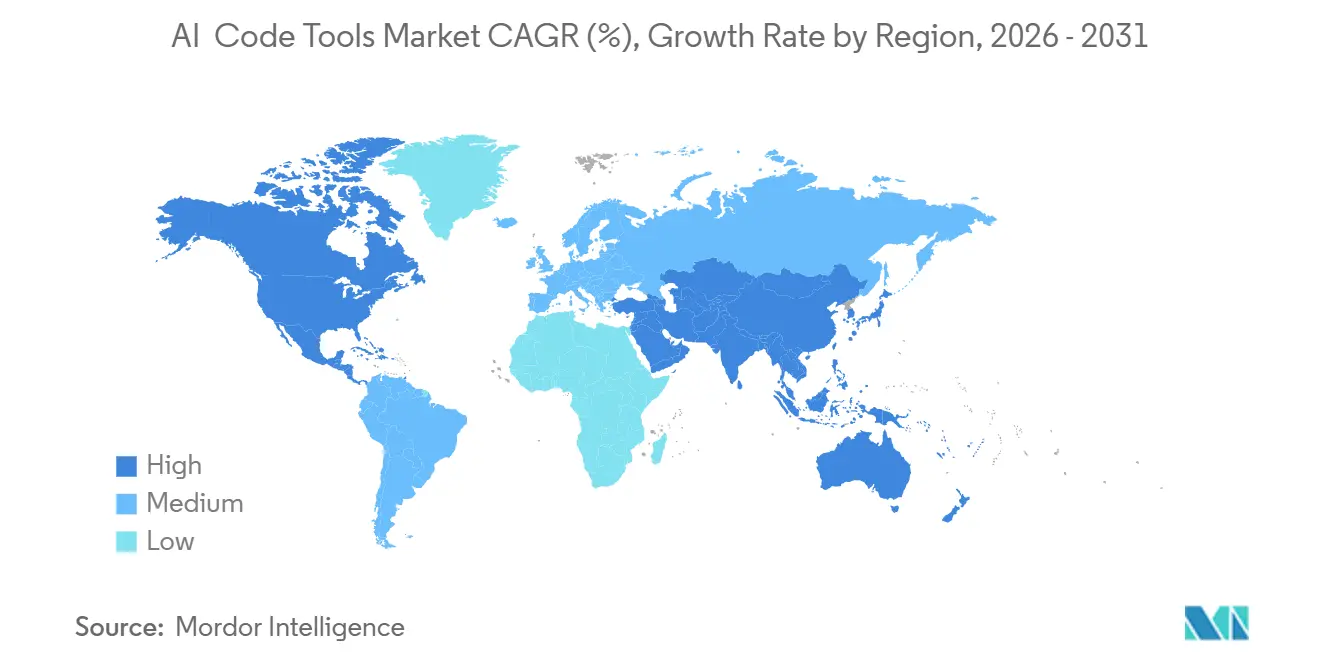

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

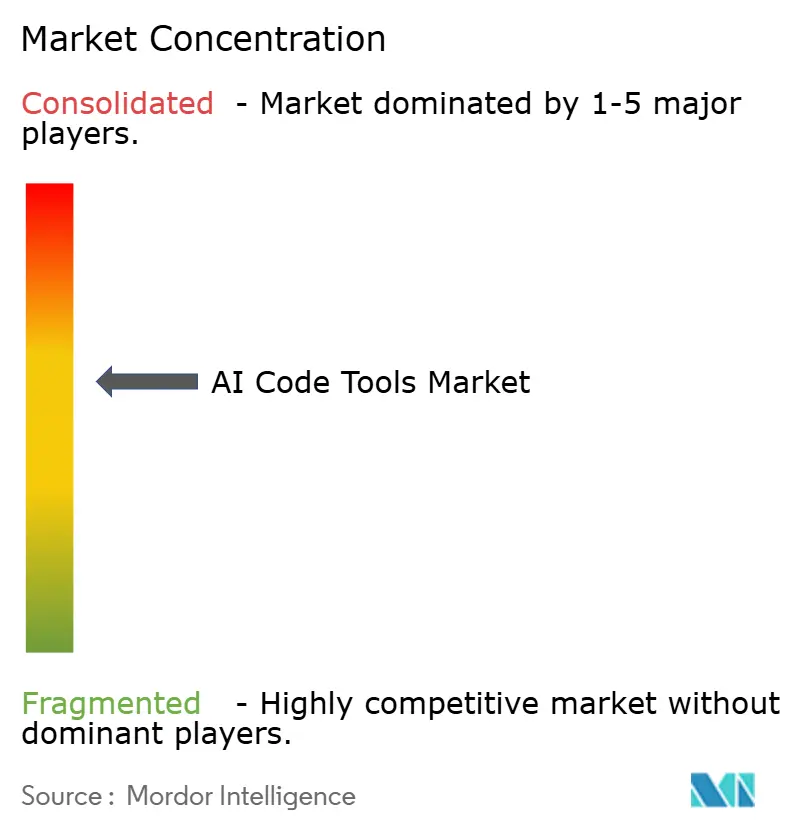

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI Code Tools Market Analysis by Mordor Intelligence

The Artificial Intelligence (AI) code tools market size is projected to be USD 7.37 billion in 2025, USD 9.35 billion in 2026, and reach USD 29.96 billion by 2031, growing at a CAGR of 26.23% from 2026 to 2031. This rapid expansion reflects a structural change in software development after foundation models crossed the 92% HumanEval accuracy threshold, moving AI assistants from pilot projects to default features inside integrated development environments. Financial services adoption illustrates the shift. NatWest reports that 12,000 engineers now let AI write more than 35% of their production code, while agentic workflows deliver tenfold productivity gains in its financial crime units. Enterprise buyers increasingly demand governance tooling, observability dashboards, role-based access controls, and audit trails over raw model performance, a priority highlighted by Microsoft’s Frontier Suite launch in March 2026. Cloud deployments still dominate, yet on-premises clusters are gaining as regulated industries weigh data-sovereignty rules and EU AI Act penalties against the convenience of managed services. Heightened competitive pressure, persistent GPU shortages, and escalating copyright litigation combine to create a landscape where cost, compliance, and capacity now rank alongside accuracy as primary buying criteria. Functionality shifts from simple completion toward full code generation, automated reviews, and in-line security scanning. Competitive intensity rises as Microsoft, Amazon, Google, and IBM convert acquisitions into end-to-end agentic platforms while well-funded challengers such as Anysphere push multi-model strategies.

Key Report Takeaways

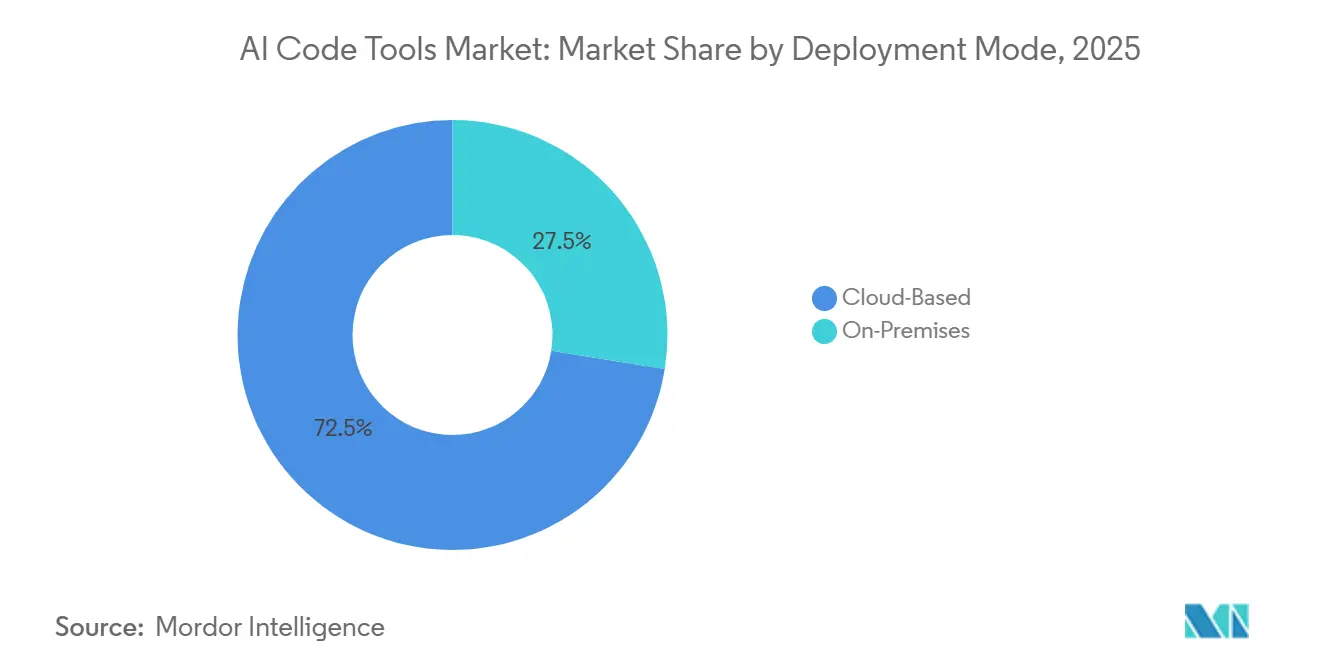

- By deployment mode, cloud-based tools accounted for 72.47% of the AI Code Tools Market's revenue in 2025, while on-premises options are forecast to grow at a 26.55% CAGR through 2031.

- By tool functionality, code completion led with a 38.19% share in 2025; security and compliance assistants are the fastest-growing segment, with a 26.83% CAGR.

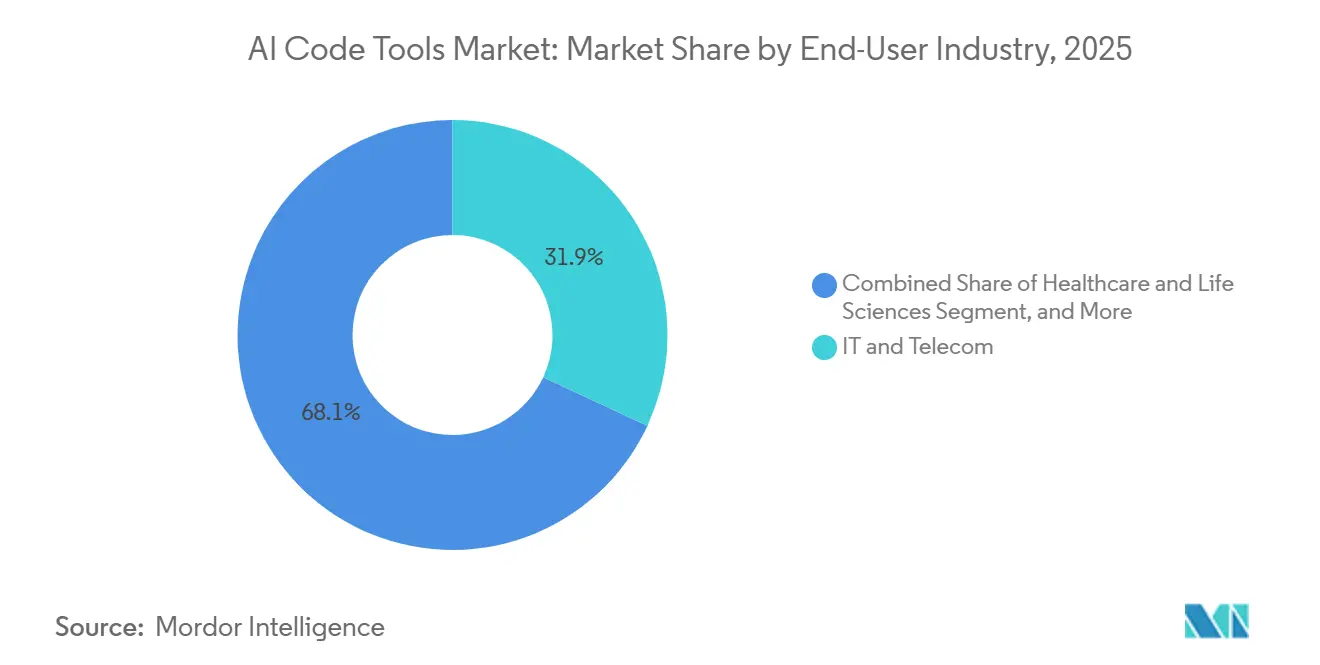

- By end-user industry, IT and telecom accounted for 31.94% in 2025, whereas healthcare and life sciences are projected to expand at a 26.94% CAGR.

- By organization size, large enterprises accounted for 59.47% of the AI Code Tools Market's revenue in 2025; SMEs are catching up at a 26.61% CAGR on the back of per-seat SaaS pricing.

- By geography, North America retained 41.89% share of the AI Code Tools Market in 2025, but Asia-Pacific is set to grow the fastest at 26.68% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI Code Tools Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exploding LLM Accuracy (>90% HumanEval) | +8.2% | Global, early enterprise uptake in North America and Europe | Medium term (2-4 years) |

| Soaring IDE Plug-in Adoption | +6.5% | Global, clustered in major tech hubs across all key regions | Short term (≤ 2 years) |

| Vendor-Bundled Cloud Credits | +3.1% | Global, particularly influential for SMEs in emerging markets | Short term (≤ 2 years) |

| 75% of Enterprise Developers Using AI by 2028 | +5.8% | Global, led by large enterprises in North America and Europe | Medium term (2-4 years) |

| Shift to Private or Local Models | +4.7% | Regulated industries worldwide | Long term (≥ 4 years) |

| Edge-Optimized LLMs for AR/VR Coding | +2.3% | Niche gaming and industrial-design clusters in North America, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Exploding LLM Accuracy Drives Enterprise Confidence in Code Generation

Foundation-model accuracy surged past 90% on HumanEval in 2025, with OpenAI’s o1-mini and Anthropic’s Claude 3.5 Sonnet both hitting 92.4%, effectively matching senior-developer performance on standardized tasks. Enterprises that once rejected AI-generated code at double-digit error rates now accept agentic refactors without manual, line-by-line review. Moonshot AI’s Kimi K2 pushed the ceiling to 94.5%, proving the improvement arc is still steep. NatWest’s operational data shows that once accuracy exceeded 90%, AI code assistants moved from shadow testing into production pipelines. Higher accuracy also unlocks multi-agent workflows in which models plan, refactor, and compile code across repositories, though Anthropic’s 2026 survey notes that engineers delegate only 0-20% of tasks fully, signaling persistent human oversight.

IDE Plug-in Proliferation Embeds AI into Daily Developer Workflows

AI assistants are now native features inside Visual Studio Code and JetBrains IDEs rather than standalone sidebars. Google Cloud’s Gemini Code Assist added enterprise-grade GitHub integrations in October 2025, targeting the 60.2% of teams whose code-review cycles exceed a day. Cursor, an AI-native fork of VS Code, reached USD 500 million ARR by mid-2025, proving that context-aware AI editors can outpace plug-in approaches when multi-file reasoning is essential.[1]M. Sen, “Cursor AI Statistics 2026: Users, Revenue, Adoption & Key Growth Metrics,” getpanto.ai, Apr. 8, 2026 Microsoft doubled down in March 2026 by embedding agentic features across Word, Excel, and Outlook, signaling that generative coding is no longer a developer-only phenomenon. Citing 40 minutes saved per developer transaction and more than 500,000 hours saved overall, the move highlights the tangible hours freed by plug-in ubiquity.

Vendor-Bundled Cloud Credits and Free Tiers Expand Access

Generous credits and free tiers make the AI code tools market accessible to SMEs that previously lacked AI budgets. Google Cloud offers Gemini Code Assist Standard at USD 19-22.80 per user per month and runs an unlimited free tier for individuals. Anysphere’s Cursor offers a two-week free trial, followed by a USD 20 monthly Pro plan, converting hobbyists into paying users and fueling a revenue-doubling cycle every two months in 2025. Free tokens lower procurement barriers, while usage analytics and seat management let IT directors scale licenses smoothly. Deloitte’s 2025 survey shows that AI use among small banks jumped from 22% in 2023 to 52% in 2025 once per-seat SaaS options emerged. As credits normalize, most SMEs treat AI assistants as a baseline cost similar to Git hosting.

75% of Enterprise Developers to Use AI Assistants by 2028

Analyst projections suggest three-quarters of professional developers will rely on AI assistants within two years, driven by rising IDE integrations and board-level mandates to boost velocity. Telcos, banks, and pharmaceutical firms are setting adoption quotas in performance metrics, turning AI use into a career expectation. Anthropic’s Accenture alliance trains 30,000 consultants on Claude Code, providing enterprises with ready-made change-management playbooks. Microsoft’s renewal of its OpenAI partnership secures exclusive Azure rights through 2032, giving CIOs confidence in the platform's long-term stability. As usage normalizes, buying decisions shift from feature checklists to integration depth and compliance readiness, reinforcing incumbent platform positions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IP and Copyright Liability Concerns | -3.8% | Global, heavy litigation in North America, regulatory focus in Europe | Medium term (2-4 years) |

| Model Hallucination and Security-Bug Risk | -4.2% | Global, especially in BFSI, Healthcare, and Government | Short term (≤ 2 years) |

| Rising GPU or ASIC Shortages | -2.9% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Developer-Skill Erosion | -1.7% | Global, education and training sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

IP and Copyright Liability Concerns Slow Enterprise Procurement

Copyright disputes intensified in 2025, creating uncertainty for CIOs drafting indemnity clauses. A Southern District of New York judge let class-action claims against OpenAI proceed, ruling that substantial-similarity arguments merited discovery. GitHub Copilot faces a Ninth Circuit appeal over alleged DMCA violations for stripping attribution. News Corp’s suit against Perplexity AI claims retrieval-augmented generation harms publishers by bypassing paywalls. These high-profile cases push buyers to demand duplication-detection tools that flag license conflicts before committing code. The EU AI Act compounds risks by requiring providers to publish summaries of their training data and to handle rights-holder complaints, with enforcement starting in August 2026.[2]European Union, “EU AI Act,” europa.eu, enforcement provisions effective Aug. 2026.

Model Hallucination and Security Vulnerabilities Constrain Production Deployment

LLMs still hallucinate API calls, package names, and logic branches, injecting silent bugs. A January 2025 arXiv paper recorded hallucination rates as high as 46.15% and warned that attackers could register bogus package names to hijack supply chains. The CoderEval benchmark shows that 43.53% of failures stem from task-requirement conflicts, indicating specification drift more than factual ignorance. HalluCodeDetector, published in March 2026, achieves an AUROC of 0.76 but is not foolproof. Deloitte’s survey reveals that over half of financial firms cite explainability gaps as their top barrier, as undetected hallucinations can trigger fraud or compliance violations. Until static-analysis defenses mature, many auditors mandate manual review of AI-generated pull requests.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Compliance Pressures Propel On-Prem Momentum

The cloud-based slice of the Artificial Intelligence (AI) code tools market accounted for 72.47% of overall revenue, while on-premises deployments accounted for the balance. On-premises options are set to grow at a 26.55% CAGR as banks, health systems, and defense agencies shun third-party data processing that might breach sovereignty rules. Vault’s 200-server footprint and Anaconda’s Llama 2 fine-tuning kits exemplify the appetite for self-hosted stacks. The EU AI Act’s transparency fines strengthen the case for keeping models behind corporate firewalls, especially where sensitive personally identifiable information appears in code comments.

Cloud providers retain an edge in speed and diversity. Google Cloud’s March 2026 rollout of Gemini 3.1 Pro with a 1-million-token window illustrates innovations that would be costly to replicate on-site. Microsoft’s Frontier Suite dynamically routes prompts among Anthropic and OpenAI models, a feature that single-tenant clusters struggle to match. Hybrid strategies dominate roadmaps, sensitive repositories remain on-premises while low-criticality tasks use SaaS APIs, enabling firms to maximize capabilities without breaching compliance guardrails. As a result, the AI code tools market continues to bifurcate into cloud-native convenience and on-premises control.

By Tool Functionality: Governance Takes Center Stage

Code completion accounted for 38.19% of 2025 revenue, yet the security-assistant niche is now the fastest-growing at a 26.83% CAGR. Automated scanners cross-reference generated snippets against vulnerability databases and flag incompatible licenses before merge, easing audit fatigue. Anthropic’s 2026 usage data shows that developers invoke security checks in 42% of agentic sessions, up from 18% in early 2025. This acceleration aligns with EU mandates that require documentation of training data and governance controls.

Documentation bots and AI-powered test generators follow close behind. Continuous-integration pipelines pass off flaky test detection and coverage analysis to LLMs, shortening release cycles by double-digit percentages. The AI code tools market share for code-review bots remains sticky because many teams treat AI as a second pair of eyes rather than an autonomous approver. As compliance automation drives adoption, the functionality hierarchy is shifting from productivity to risk management, cementing security as the new killer feature.

By End-User Industry: Healthcare Emerges as the Growth Engine

IT and telecom’s 31.94% market share in 2025 reflects its early-adopter culture and its ability to directly monetize AI tools as external services. This sector has consistently embraced cutting-edge technologies, leveraging AI to enhance operational efficiency and develop innovative solutions for clients. Meanwhile, healthcare and life sciences are projected to achieve the fastest compound annual growth rate (CAGR) of 26.94%, driven by the increasing complexity of clinical-trial documentation and the need to comply with stringent regulatory requirements. Anthropic’s partnership with Accenture highlights high-return-on-investment (ROI) use cases, such as medical coding, adverse-event reporting, and protocol drafting, that are transforming how healthcare organizations manage their workflows and meet compliance standards.

The banking, financial services, and insurance (BFSI) sector continues to integrate AI agents for critical applications, including updates to the anti-money-laundering model and the development of challenger models. According to Deloitte’s research, 58% of global banks have adopted generative coding to enhance their fraud-detection models, underscoring the sector's commitment to leveraging AI for risk management and operational improvements. Additionally, BFSI organizations are increasingly using AI to streamline processes, reduce costs, and improve customer experiences. While the retail, media, and public-sector segments lag in adoption, they are still experiencing robust double-digit growth. This growth is fueled by applications such as e-commerce personalization, game-engine scripting, and the modernization of legacy systems, which are helping these sectors remain competitive in a rapidly evolving digital landscape.

By Organization Size: SaaS Economics Democratize Advanced Features

Large enterprises accounted for 59.47% of the revenue in 2025, maintaining a dominant position in the market. However, their incremental growth is slowing due to market saturation and scaling challenges. On the other hand, small and medium-sized enterprises (SMEs) are experiencing significant growth, driven by the adoption of per-seat Software-as-a-Service (SaaS) plans. SMEs are projected to grow at a compound annual growth rate (CAGR) of 26.61%, gradually closing the functional gap with larger Fortune 500 companies. Google's introduction of the USD 19 entry-level Gemini Code Assist tier has made advanced frontier models accessible to smaller startups, including those with as few as ten employees. Additionally, features such as usage analytics and spend controls are helping SMEs manage costs effectively, reducing the risk of unexpected expenses for teams operating on tight budgets.

Deloitte highlights that process rigidity significantly hampers large-enterprise rollouts, with 24% of these enterprises citing legacy workflows as a major obstacle, compared to only 3% of small banks. This rigidity often results in slower adoption of innovative technologies. On the other hand, small and medium-sized enterprises (SMEs) benefit from the flexibility of green-field DevOps stacks, which allow them to bypass procurement delays and legacy system constraints. This adaptability has enabled SMEs to accelerate the adoption of AI assistants, particularly in underserved markets such as Latin-American fintech and Southeast Asian e-commerce. These regions are witnessing rapid growth as SMEs leverage AI-driven solutions to enhance operational efficiency, improve customer engagement, and gain a competitive edge in their respective industries.

Geography Analysis

North America accounted for 41.89% of 2025 revenue, reflecting hyperscaler investments, venture funding density, and early enterprise adoption. US banks and Canadian telcos have institutionalized AI governance offices that standardize prompt libraries and risk controls, embedding assistants deeply into secure software development lifecycles. Intellectual property litigation remains a regional headwind, but legal certainty often arrives more quickly in US courts, encouraging first-mover experimentation.

Europe is progressing under a compliance-first approach, emphasizing adherence to regulatory frameworks. The General-Purpose AI Code of Practice, introduced in July 2025, offers providers a set of voluntary checklists focusing on critical aspects such as copyright compliance and transparency.[3]European Commission, “Contents of the Code of Practice for General-Purpose AI (GPAI),” digital-strategy.ec.europa.eu. This initiative is designed to prepare the region for the enforcement of the EU AI Act, which is scheduled to come into effect in August 2026. In response to these regulatory developments, banks and insurers are increasingly adopting on-premises clusters to comply with stringent data-residency requirements. This shift is driving growth in the AI code tools market across the continent, while also redirecting spending priorities toward governance-related features to ensure compliance with the evolving regulatory landscape.

Asia-Pacific is the standout growth engine, with a 26.68% CAGR. Chinese vendors like Alibaba’s Qwen now offer multimodal, agent-ready models at one-sixth the US cost, unlocking adoption among Indian outsourcers and Southeast-Asian startups. Government grants in Singapore and South Korea fund in-country accelerators that waive GPU fees for SMEs. The price-performance edge tilts spending toward cost-optimized stacks, even as English-language proficiency broadens addressable developer bases. South America, the Middle East, and Africa sit at earlier stages of AI adoption, but government digital-transformation agendas and offshore support hubs are beginning to pull AI code tools into public tenders and local tech ecosystems.

Competitive Landscape

Competition in the Artificial Intelligence (AI) code tools market is intensifying, yet it remains moderately fragmented. Microsoft renewed its OpenAI deal in October 2025, extending exclusive Azure hosting through 2032 and committing USD 250 billion in future cloud spend.[4]OpenAI, “The next phase of the Microsoft OpenAI partnership,” openai.com, Apr. 27, 2026. This strategic move provides Azure with a durable distribution advantage, positioning it strongly in the market. In response, Anthropic invested USD 100 million in its Claude Partner Network, creating a robust channel of systems integrators. This initiative has sparked a competitive race to capture enterprise wallets, with Anthropic aiming to establish a significant foothold. Meanwhile, Anysphere’s Cursor has demonstrated that AI-native challengers can scale rapidly, achieving USD 500 million in annual recurring revenue (ARR) within two years by focusing on owning the developer desktop.

Startups in the AI tools market are differentiating themselves through innovations such as multi-agent orchestration and repository-aware retrieval. For instance, Cursor 2.0 introduced an eight-agent composer framework that accelerates complex tasks by a factor of 4 compared to standard large language model (LLM) loops. Established players like Google and Microsoft are embedding model-selection logic into their platforms, allowing them to hedge dependencies on any single provider. This strategic approach ensures flexibility and resilience in their offerings. These advancements highlight the dynamic nature of the market, where both incumbents and challengers are leveraging technology to address evolving developer needs.

White-space opportunities are emerging in legacy-language coverage, offering significant growth potential. Anthropic has begun handling COBOL and Fortran refactors to address the trillion-dollar modernization backlog. This focus on legacy system modernization addresses a critical market need, offering solutions for enterprises looking to upgrade outdated infrastructure. Overall, the AI code tools market is balancing the influence of platform incumbents, who wield control planes, against the agility of nimble upstarts optimizing for developer satisfaction. This competitive landscape underscores the importance of innovation and strategic investments in shaping the industry's future.

AI Code Tools Industry Leaders

Microsoft Corporation

GitHub, Inc.

Amazon.com, Inc. (AWS)

Google LLC

OpenAI OpCo, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Microsoft debuted Frontier Suite inside Microsoft 365 Copilot, pricing the E7 bundle at USD 99 per user per month.

- March 2026: Anthropic committed USD 100 million to the Claude Partner Network for training and joint go-to-market initiatives.

- March 2026: Google Cloud rolled out Gemini 3.1 Pro and 3.0 Flash in preview for VS Code and IntelliJ integrations.

- February 2026: Alibaba upgraded Qwen with multimodal input and agent-task support.

Global AI Code Tools Market Report Scope

The Artificial Intelligence (AI) code tools market refers to software solutions that leverage artificial intelligence and machine learning to assist in software development, including code generation, completion, debugging, testing, and optimization. These tools integrate with development environments to enhance developer productivity, reduce errors, and accelerate application delivery. They utilize technologies such as natural language processing and large language models to translate user intent into functional code and automate repetitive programming tasks.

The AI Code Tools Market Report is Segmented by Deployment Mode (Cloud-Based, and On-Premises), Tool Functionality (Code Completion, Code Generation, Code Review and Optimization, Automated Testing, Security and Compliance Assistants, and Documentation and Commenting), End-User Industry (IT and Telecom, BFSI, Healthcare and Life Sciences, Retail and E-Commerce, Media and Entertainment, Government and Public Sector, and Other End-User Industries), Organization Size (Large Enterprises, and Small and Medium Enterprises), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Based |

| On-Premises |

| Code Completion |

| Code Generation |

| Code Review and Optimization |

| Automated Testing |

| Security and Compliance Assistants |

| Documentation and Commenting |

| IT and Telecom |

| BFSI |

| Healthcare and Life Sciences |

| Retail and E-Commerce |

| Media and Entertainment |

| Government and Public Sector |

| Others End-User Industry |

| Large Enterprises |

| Small and Medium Enterprises |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Deployment Mode | Cloud-Based | ||

| On-Premises | |||

| By Tool Functionality | Code Completion | ||

| Code Generation | |||

| Code Review and Optimization | |||

| Automated Testing | |||

| Security and Compliance Assistants | |||

| Documentation and Commenting | |||

| By End-User Industry | IT and Telecom | ||

| BFSI | |||

| Healthcare and Life Sciences | |||

| Retail and E-Commerce | |||

| Media and Entertainment | |||

| Government and Public Sector | |||

| Others End-User Industry | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will spending become by 2031?

The AI code tools market size is projected to reach USD 29.96 billion by 2031.

What CAGR is expected for AI coding platforms through 2031?

The AI code tools market is forecast to grow at a 26.23% CAGR between 2026 and 2031.

Which region is poised for the fastest growth?

Asia-Pacific is expected to post the strongest 26.68% CAGR as low-cost, open-source models fuel adoption.

Why are on-premises deployments gaining interest?

Regulated industries prefer on-prem clusters to meet data-sovereignty rules and EU AI Act transparency mandates while avoiding vendor lock-in.

What functionality segment is rising the quickest?

Security and compliance assistants are expanding at a 26.83% CAGR as firms automate vulnerability scanning and license checks.

How are SMEs affording advanced AI coding tools?

Vendors provide free tiers and per-seat SaaS pricing, letting small teams start for under USD 25 per user per month.

Page last updated on: