Agentic AI Developer Ecosystem And SDK Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

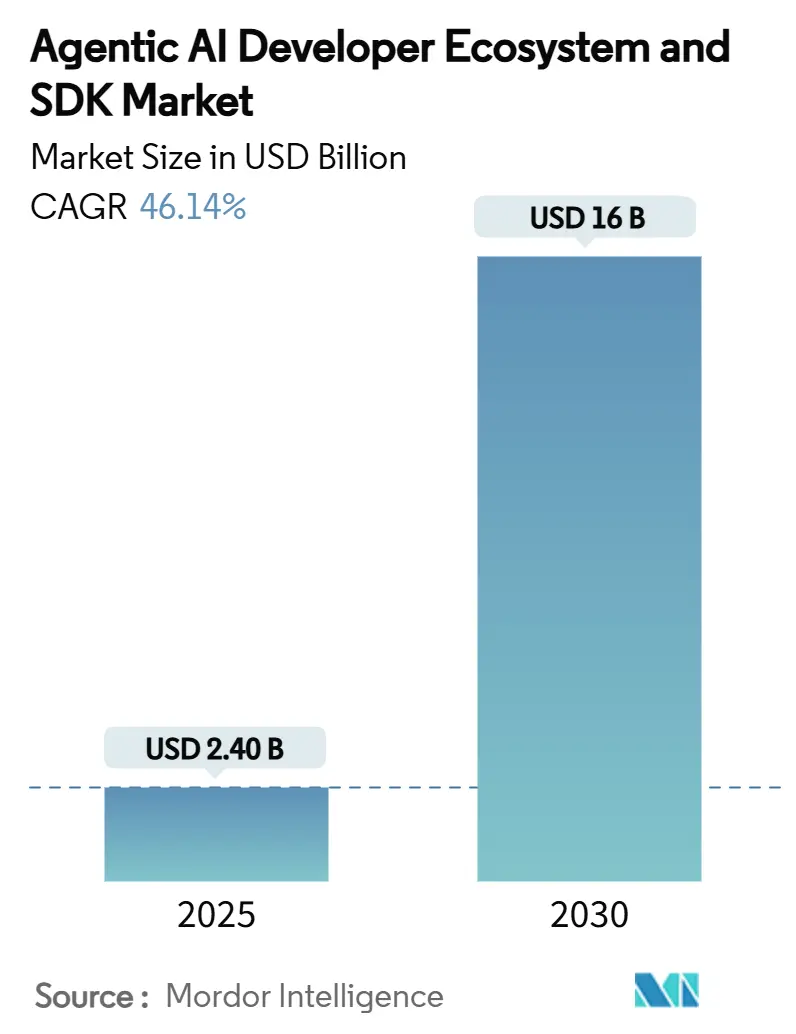

| Market Size (2025) | USD 2.40 Billion |

| Market Size (2030) | USD 16 Billion |

| Growth Rate (2025 - 2030) | 46.14% CAGR |

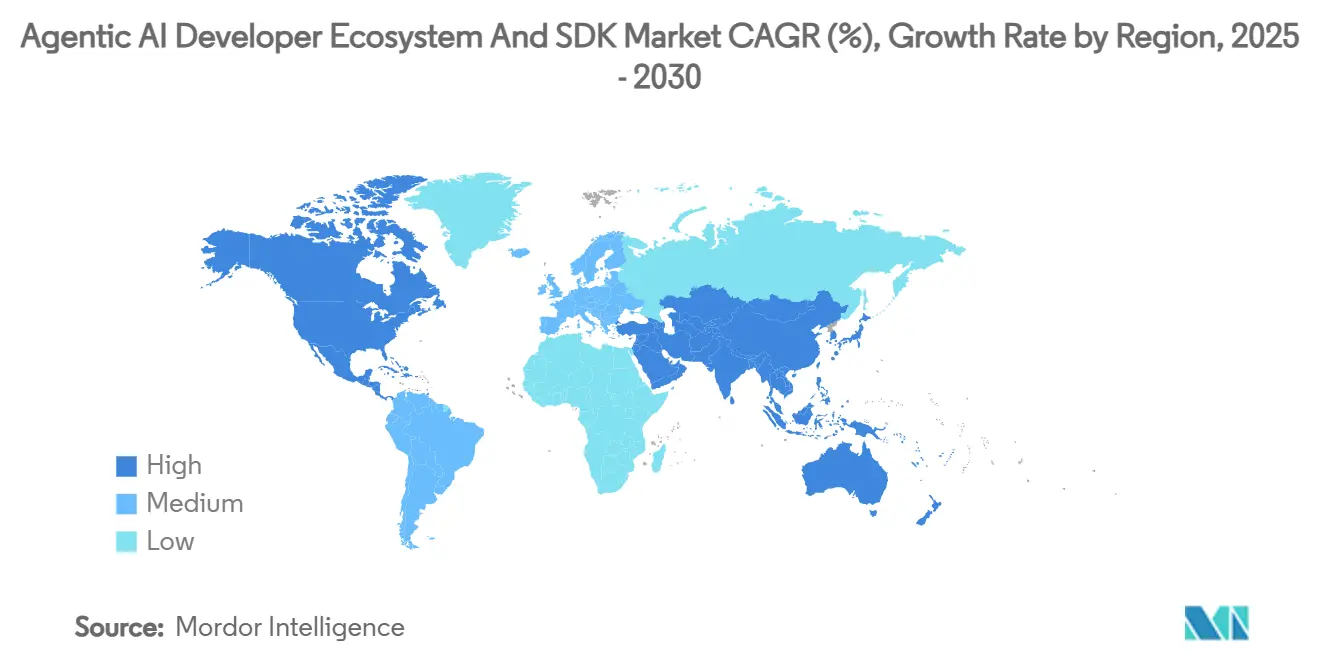

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agentic AI Developer Ecosystem And SDK Market Analysis by Mordor Intelligence

The agentic AI developer ecosystem and SDK market size stood at USD 2.40 billion in 2025 and is forecast to reach USD 16.00 billion by 2030, expanding at a 46.14% CAGR, underscoring the sector’s powerful growth momentum. Demand for autonomous GenAI workflows, rapid advances in orchestration technology, and government procurement programs validate commercial adoption and stimulate new revenue pools. North American enterprises, buoyed by robust cloud infrastructure and venture funding, continue to lead early deployment, while Asia-Pacific capitalizes on policy support and manufacturing uptake to emerge as the fastest-growing regional arena. Open-source frameworks remain dominant thanks to vibrant communities and lower total cost of ownership, yet orchestration-layer SDKs record the sharpest acceleration as businesses recognize the value of multi-agent coordination. Healthcare, life sciences, and BFSI verticals now prioritize agentic AI for compliance-ready automation, and cloud deployment retains clear scale advantages even as latency-sensitive edge scenarios multiply.

Key Report Takeaways

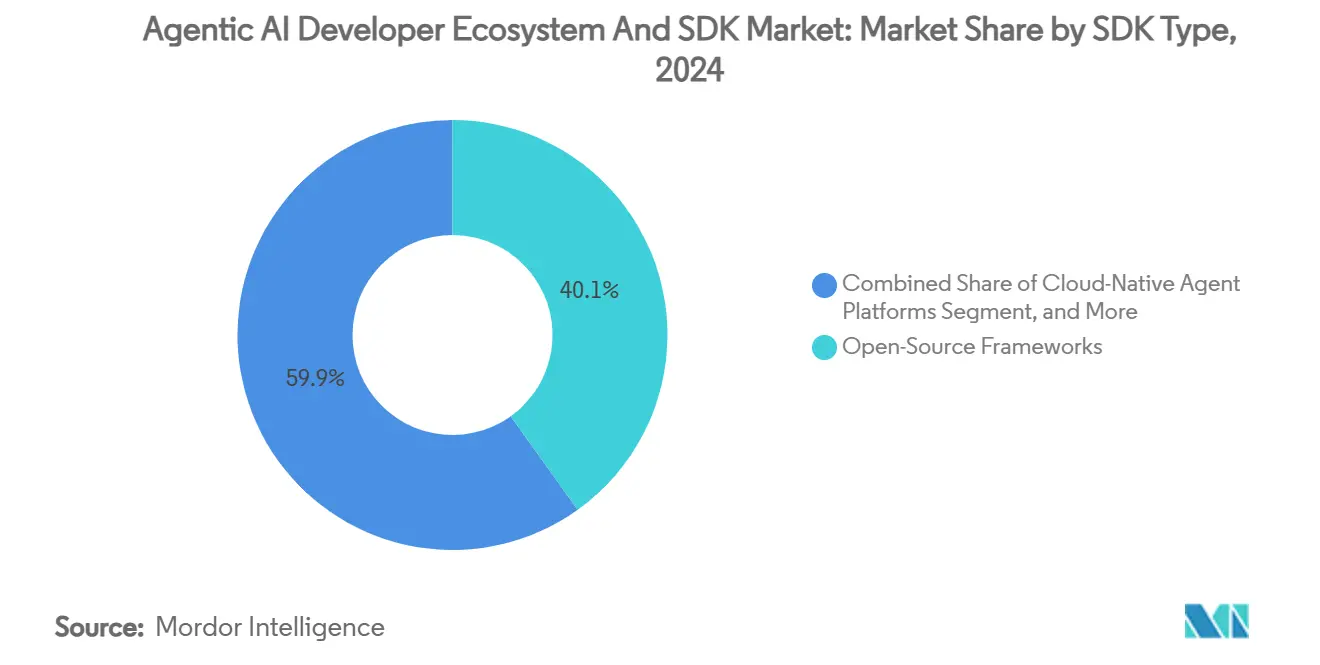

- By SDK type, open-source frameworks held 40.1% of the agentic AI developer ecosystem and SDK market share in 2024, while orchestration-layer SDKs are projected to grow at a 52.0% CAGR through 2030.

- By application, customer support automation accounted for 34.8% of the agentic AI developer ecosystem and SDK market size in 2024; software engineering productivity is poised to post a 50.0% CAGR to 2030.

- By end-user industry, IT and telecommunications retained 48.6% share of the agentic AI developer ecosystem and SDK market in 2024, yet healthcare and life sciences are forecast to expand at a 50.2% CAGR over the same horizon.

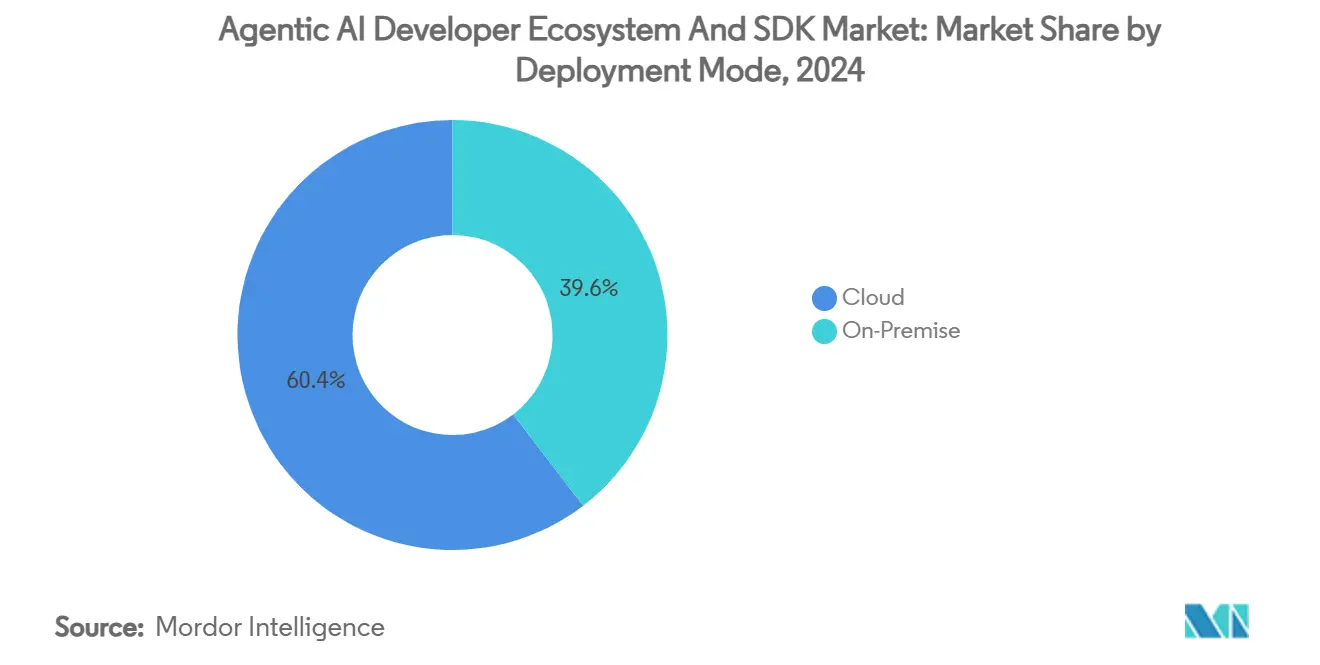

- By deployment mode, cloud solutions captured 60.4% revenue in 2024 and are advancing at a 48.4% CAGR, supported by elastic compute requirements and emerging interoperability protocols such as A2A and MCP.

- By organization size, large enterprises commanded 70.0% revenue in 2024 and SMEs are advancing at a 48.1% CAGR,

- By geography, North America led with 40.1% share in 2024; Asia-Pacific is expected to deliver a 50.5% CAGR, propelled by large-scale AI infrastructure roll-outs and favorable regulatory frameworks.

Global Agentic AI Developer Ecosystem And SDK Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enterprise race to automate GenAI workflows | +12.5% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Open-source SDKs collapse entry barriers | +8.2% | Global, highest in Asia-Pacific and emerging markets | Short term (≤ 2 years) |

| VC and M&A cash surge for agent-platform start-ups | +6.8% | North America and EU core; spill-over to Asia-Pacific | Medium term (2-4 years) |

| Inter-operability protocols standardize agent stacks | +7.1% | Global, with adoption in developed enterprise markets | Long term (≥ 4 years) |

| Falling AI-chip USD/TOPS enables on-device agents | +5.4% | Asia-Pacific manufacturing hubs, North America edge sites | Long term (≥ 4 years) |

| Audit-ready governance toolkits become mandatory | +4.6% | North America and EU regulated markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Enterprise Race to Automate GenAI Workflows

Organizations are shifting from conversational chatbots to end-to-end autonomous workflows, and 25% of large enterprises now pilot multi-agent architectures in customer support, finance, and supply-chain functions. Cost-down targets of 30% or more are increasingly tied to rapid decision cycles delivered by agent orchestration engines. Governments also drive momentum: the U.S. Department of Defense awarded four multiyear contracts worth up to USD 800 million in July 2025 to advance mission-critical agentic AI, boosting private-sector confidence [1]U.S. Department of Defense, “DOD Selects Companies to Advance AI Capabilities,” defense.gov. First movers already report accelerated ticket resolution and significant accuracy gains, reinforcing the business case for scaled adoption.

Open-Source SDKs Collapse Entry Barriers

Well-maintained open-source repositories such as LangChain and CrewAI eliminate six-figure annual license fees and shorten proof-of-concept cycles from months to weeks. Community contributions produce continuous feature updates that rival proprietary suites, while transparent codes reduce vendor-lock risks for compliance-conscious buyers. Asia-Pacific developers capitalize on cost-efficient stacks to address language localization and industrial automation challenges. The cumulative effect widens the talent pool and amplifies innovation velocity, setting a high bar for closed-source rivals.

VC and M&A Cash Surge for Agent-Platform Start-ups

Venture investors poured unprecedented capital into the segment in 2024, with SuperAGI’s USD 10-million seed and /dev/agents’ USD 56-million Series A fueling roadmap acceleration. Strategic buyers followed suit: Amazon committed USD 3 billion to acquire Adept, and Salesforce finalized the Tenyx takeover to enhance domain-specific orchestration expertise. Capital inflows validate market durability, help standardize best practices, and provide early-stage innovators with enterprise sales channels. The funding wave also signals premium valuations for specialized orchestration capabilities over generalist toolkits.

Inter-operability Protocols Standardize Agent Stacks

Google’s Agent-to-Agent (A2A) protocol and Anthropic’s Model Context Protocol (MCP) create common languages for delegation, tool invocation, and resource sharing across heterogeneous agents. These frameworks mitigate integration overhead and safeguard long-term system scalability for buyers wary of vendor lock-in. Early enterprise trials show 25% faster deployment times once interoperability layers replace bespoke connectors [2] Clarifai Engineering, “MCP vs A2A: Standardizing Agent Communication,” clarifai.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Privacy and security fears over autonomous code execution | -8.7% | Global, strongest in regulated industries | Short term (≤ 2 years) |

| Sparse reliability benchmarks for multi-agent systems | -5.3% | Global, critical in enterprise deployments | Medium term (2-4 years) |

| Framework fragmentation inflates integration cost | -4.2% | Global, acute in multi-vendor environments | Medium term (2-4 years) |

| Shortage of prompt-systems engineers for debugging | -3.8% | North America and EU talent markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Privacy and Security Fears Over Autonomous Code Execution

Financial services, healthcare, and defense CIOs flag autonomous code execution as a top three cyber-risk, citing potential lateral-movement attacks if agents gain unwarranted system privileges. The EU AI Act places autonomous agents in its highest-risk tier, compelling rigorous impact assessments and audit trails before deployment. Enterprises now demand agent-level zero-trust controls, real-time telemetry, and kill-switch capabilities as prerequisites for production rollouts. Security-ready SDK vendors that integrate encryption, policy enforcement, and dynamic isolation win procurement preference in compliance-sensitive verticals[3]European Parliament, “Artificial Intelligence Act: High-Risk Classification Explained,” europarl.europa.eu.

Sparse Reliability Benchmarks for Multi-Agent Systems

Buyers lack universally accepted yardsticks to measure end-to-end reliability for agent swarms executing asynchronous tasks. Existing metrics focus on language-model accuracy rather than orchestration resilience, leading to procurement hesitation for mission-critical workloads. Several industry consortia have begun drafting benchmark suites that track hand-off success rates and recovery times, yet consensus standards remain at least two years away. As a result, system integrators must over-engineer redundancy, inflating the total cost of ownership and prolonging sales cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By SDK Type: Open-Source Dominance Faces Orchestration Challenge

Open-source frameworks commanded 40.1% of the agentic AI developer ecosystem and SDK market in 2024 as enterprises favored transparent code, active communities, and fast iteration. Proprietary vendors still capture premium service contracts, but their influence wanes as engineering teams standardize open repositories for agent scaffolding. Orchestration-layer SDKs log a 52.0% CAGR, making them the fastest-expanding subsegment as businesses prioritize multi-agent coordination, resource sharing, and observability.

The agentic AI developer ecosystem and SDK market size for orchestration-layer SDKs is projected to climb steeply as firms adopt protocol-driven collaboration patterns that unify heterogeneous stacks without sacrificing compliance requirements. Vendors that marry open-source extensibility with managed-service guarantee themselves to win large-scale enterprise rollouts. Competitive intensity revolves around scheduling efficiency, fault tolerance, and plug-and-play toolchains that shorten integration timelines.

By Application: Support Automation Leads, Engineering Productivity Accelerates

Customer support automation contributed 34.8% revenue in 2024, benefiting from well-defined ROI metrics and tight coupling with CRM systems. Banking contact centers cite sub-30-second first-response times and double-digit NPS improvements after deploying conversational and task-execution agents. Software engineering productivity, however, is on track to register the swiftest gains, expanding at a 50.0% CAGR through 2030 as DevOps teams embed agents into code review, test generation, and CI/CD pipelines.

The agentic AI developer ecosystem and SDK market size allocated to engineering-focused tools is forecast to widen as enterprises pressure development teams to ship features faster amid rising codebase complexity. Early adopters report 20% cycle-time reductions and fewer escaped defects, reinforcing the economic case for agent-driven productivity boosters. Over time, customer support and engineering use cases will converge as multi-function agent swarms share contextual data to resolve issues proactively.

By End-User Industry: IT Leadership Challenged by Healthcare Growth

IT and telecommunications retained a 48.6% share of the agentic AI developer ecosystem and SDK market in 2024, thanks to mature cloud footprints and teams skilled in scaling distributed systems. Telcos apply network-optimization agents to reduce downtime and automate traffic routing, driving measurable opex savings. Healthcare and life sciences, meanwhile, deliver the most aggressive growth at a 50.2% CAGR through 2030 on the back of stringent audit needs and incentives to streamline clinical operations.

Increasing electronic health-record interoperability and FDA guidance on software as a medical device underscore the necessity for governance-first agent platforms. Hospitals deploying autonomous prior-authorization agents report claims-processing speed improvements of 35%, demonstrating tangible patient-care benefits. As compliance toolkits expand and reimbursement models reward efficiency, healthcare adoption momentum is set to erode the historic leadership enjoyed by IT services.

By Deployment Mode: Cloud Supremacy Sustains Despite Edge Interest

Cloud deployments controlled 60.4% revenue in 2024 and are forecast to grow at a 48.4% CAGR through 2030, enabled by elastic compute pools that orchestrate thousands of concurrent agent threads. The agentic AI developer ecosystem and SDK market share of cloud offerings benefits from native security layers, integrated monitoring, and pay-as-you-scale pricing.

On-premise and edge scenarios nevertheless occupy important niches. Central banks and defense agencies deploy on-premise clusters to satisfy sovereign-data mandates, while automotive OEMs embed on-device agents for real-time perception and control. Protocol-driven interoperability lets enterprises blend cloud scale with edge responsiveness, fostering distributed topologies in which governance remains centralized even as execution becomes decentralized.

By Organization Size: Enterprise Dominance Faces SME Disruption

Large enterprises accounted for 70.0% revenue in 2024, leveraging deep pockets and in-house AI centers of excellence to integrate agentic capabilities across business functions. They experiment with hierarchical agent swarms that coordinate marketing, finance, and supply-chain tasks, boosting real-time decision-making. The agentic AI developer ecosystem and SDK market size accruing to SMEs is projected to expand rapidly at a 48.1% CAGR, reflecting open-source affordability and SaaS delivery models that slash entry barriers.

New-generation platform vendors bundle orchestration, monitoring, and governance into subscription tiers aligned to headcount, helping smaller firms tap advanced automation without hefty capex. As SME adoption rises, competitive dynamics will increasingly reward agility and process re-engineering skill over sheer capital strength.

Geography Analysis

North America maintained 40.1% revenue leadership in 2024 as hyperscale cloud providers, a vibrant venture capital scene, and early regulatory clarity converged to accelerate rollout of experimental and production agent stacks. Federal contracts, particularly the USD 800 million multi-vendor award from the U.S. Department of Defense, further underpin commercial confidence and create spill-over demand among adjacent civilian agencies. State-level innovation grants facilitate SME participation, helping diffuse capabilities beyond tier-one tech hubs.

Asia-Pacific is on course to record a 50.5% CAGR, the fastest worldwide trajectory, propelled by aggressive sovereign AI policies in South Korea, Singapore, and Japan. Local semiconductor and robotics manufacturers embed agentic control loops into smart-factory retrofits, and open-source ecosystems flourish in India and Indonesia, where developer communities gravitate toward zero-license-fee frameworks. China continues to invest heavily in models tailored to Mandarin, but cross-border interoperability standards gain ground as exporters seek seamless integration with Western platforms.

Europe pursues a compliance-first stance shaped by the AI Act, catalyzing demand for audit-ready governance modules. Enterprises in Germany and France pilot agentic workflows in regulated sectors such as utilities and pharmaceuticals. Iberian and Nordic countries, supported by EU innovation funding, adopt cloud-edge hybrids to bypass data-residency hurdles while retaining latency performance. The agentic AI developer ecosystem and SDK market size across EMEA is expected to grow steadily, though at a moderate pace compared with Asia-Pacific, as organizations balance innovation with stringent oversight.

Competitive Landscape

Competition in the agentic AI developer ecosystem and SDK market remains moderately fragmented, with hyperscalers, specialist vendors, and open-source communities vying for orchestration primacy. Microsoft deepened its USD 13 billion investment in OpenAI and recently introduced Azure AI Foundry Agent Service, bundling security controls and managed scaling to reinforce Azure cloud lock-in [4]Microsoft Azure Blog, “Introducing Azure AI Foundry Agent Service,” microsoft.com. Yet friction over revenue sharing and AGI milestone definitions injects uncertainty, potentially opening room for alternative alliances.

Google counters with Agent Development Kit and robust support for the open A2A protocol, positioning its cloud as the default hub for heterogeneous agent interoperability [5]Google Cloud Blog, “Agent Development Kit Now Generally Available,” blog.google. Amazon accelerates through M&A: the Adept acquisition fast-tracks domain-specific orchestration modules that align with AWS Bedrock. IBM focuses on governance and hybrid cloud deployment, with Watson Agent Orchestrator targeting customers in finance and healthcare that demand audit trails and data residency assurances.

Open-source innovators remain critical disruptors. LangChain’s monthly release cadence delivers cutting-edge connectors and observability features, while CrewAI and AutoGen pioneer role-based collaboration and conversational multi-agent frameworks. Patent activity concentrates on scheduling algorithms and protocol gateways, signaling that intellectual-property moats will shape future competitive positioning. Market watchers anticipate increased vertical-specific partnerships as vendors strive to differentiate beyond generic orchestration.

Agentic AI Developer Ecosystem And SDK Industry Leaders

OpenAI, L.L.C.

Microsoft Corporation

Google LLC

Amazon Web Services, Inc.

LangChain, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The U.S. Department of Defense awarded contracts worth up to USD 200 million each to Anthropic, Google, OpenAI, and xAI to advance mission-critical agentic workflows.

- May 2025: IBM introduced Watson Agent Orchestrator for hybrid-cloud, compliance-ready agent management.

- May 2025: Microsoft unveiled Azure AI Foundry Agent Service, combining OpenAI models with enterprise-grade governance.

- April 2025: LangChain launched LangGraph Cloud, a managed multi-agent deployment service with integrated monitoring.

Global Agentic AI Developer Ecosystem And SDK Market Report Scope

| Open-Source Frameworks |

| Proprietary Frameworks |

| Cloud-Native Agent Platforms |

| Orchestration-Layer SDKs |

| Customer Support Automation |

| Software Engineering Productivity |

| Data and Knowledge Management |

| DevOps and IT Operations Automation |

| IT and Telecommunications |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Retail and E-commerce |

| Manufacturing |

| Cloud |

| On-Premise |

| Large Enterprises |

| Small and Medium-sized Enterprises |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By SDK Type | Open-Source Frameworks | ||

| Proprietary Frameworks | |||

| Cloud-Native Agent Platforms | |||

| Orchestration-Layer SDKs | |||

| By Application | Customer Support Automation | ||

| Software Engineering Productivity | |||

| Data and Knowledge Management | |||

| DevOps and IT Operations Automation | |||

| By End-User Industry | IT and Telecommunications | ||

| Banking, Financial Services and Insurance (BFSI) | |||

| Healthcare and Life Sciences | |||

| Retail and E-commerce | |||

| Manufacturing | |||

| By Deployment Mode | Cloud | ||

| On-Premise | |||

| By Organisation Size | Large Enterprises | ||

| Small and Medium-sized Enterprises | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is driving the rapid growth of the agentic AI developer ecosystem and SDK market?

Enterprise automation initiatives, large government contracts, and the rise of open-source orchestration tools collectively push the market toward a 46.14% CAGR through 2030.

Which SDK category is expanding the fastest?

Orchestration-layer SDKs are projected to deliver a 52.0% CAGR as businesses prioritize multi-agent coordination across heterogeneous stacks.

Multi-agent coordination across heterogeneous stacks. How big is the cloud segment within this market?

Cloud deployments captured 60.4% revenue in 2024, and the subsegment is forecast to grow at 48.4% annually through 2030, driven by elastic compute needs.

Which region will grow the quickest?

Asia-Pacific is projected to post a 50.5% CAGR thanks to aggressive national AI strategies and manufacturing-led adoption.

Page last updated on: