Agentic AI Development Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

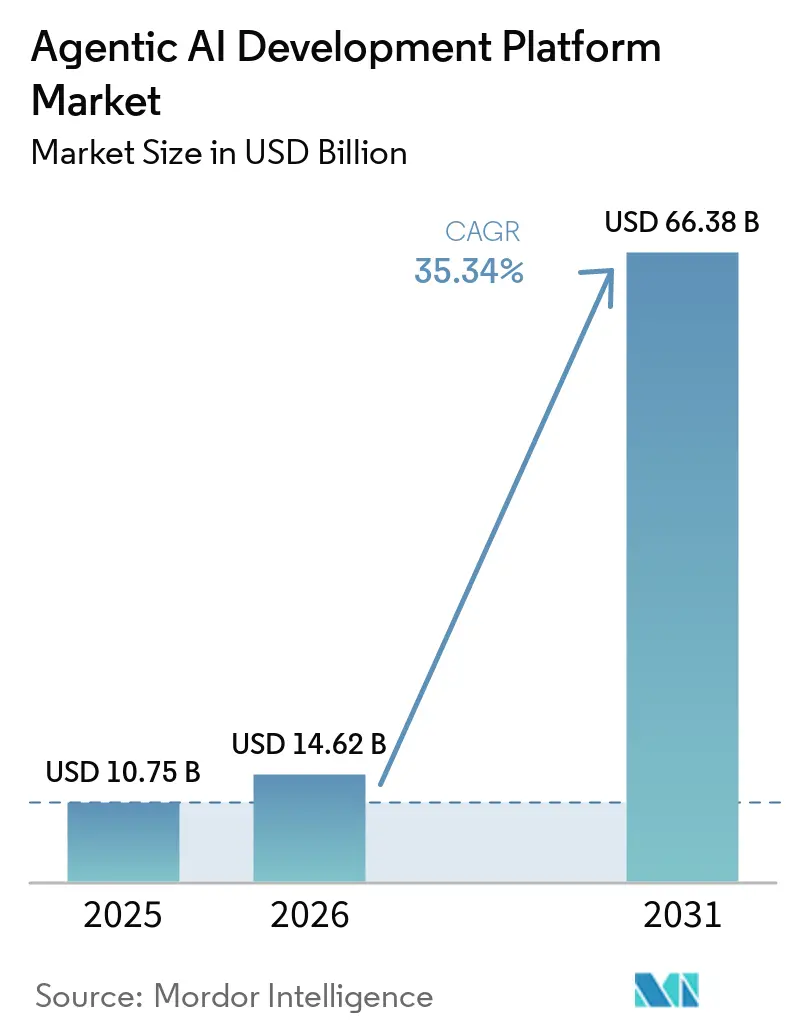

| Market Size (2026) | USD 14.62 Billion |

| Market Size (2031) | USD 66.38 Billion |

| Growth Rate (2026 - 2031) | 35.34% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agentic AI Development Platform Market Analysis by Mordor Intelligence

The agentic AI development platform market size is expected to grow from USD 10.75 billion in 2025 to USD 14.62 billion in 2026 and is forecast to reach USD 66.38 billion by 2031 at 35.34% CAGR over 2026-2031. The agentic AI development platform market is expanding faster than most enterprise software categories because buyers are now funding dedicated orchestration layers for autonomous agents rather than adding isolated AI features to existing tools. This shift is being reinforced by stronger reasoning quality in large language models, lower interoperability friction from emerging protocols, and workflow software vendors embedding agent control planes into products that enterprises already use in production. Cost pressure has also supported adoption, as autonomous agent systems align with management priorities for shorter process cycles and workforce support without a corresponding rise in headcount. Competitive pressure is strongest in orchestration and governance because buyers now place more weight on runtime control, memory design, auditability, and cross-agent trust than on raw model access alone. A near-term limit remains agent sprawl, since enterprises that deploy many disconnected agents without clear governance often slow approvals in regulated settings and delay broader spending.

Key Report Takeaways

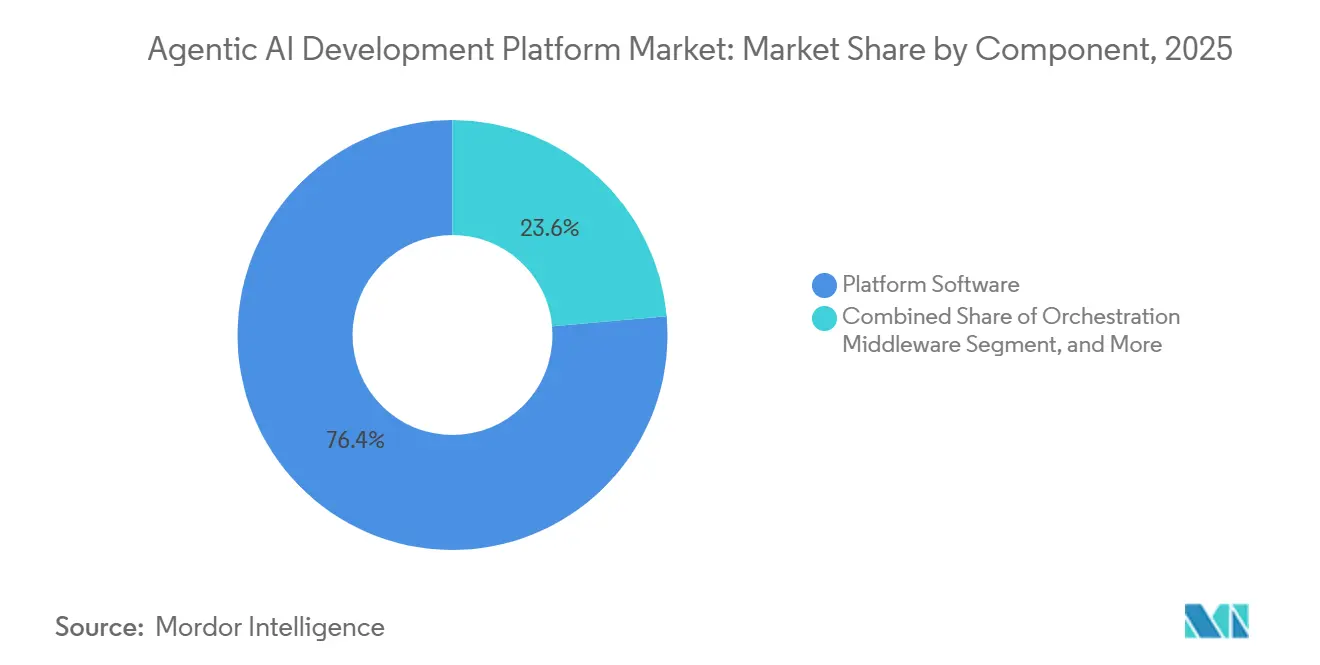

- By component, platform software accounted for 76.39% of the agentic AI development platform market in 2025, and professional services are projected to grow at a 36.14% CAGR through 2031.

- By deployment model, public cloud accounted for 52.61% of revenue in 2025, and hybrid and edge deployments are projected to grow at 36.09% CAGR through 2031.

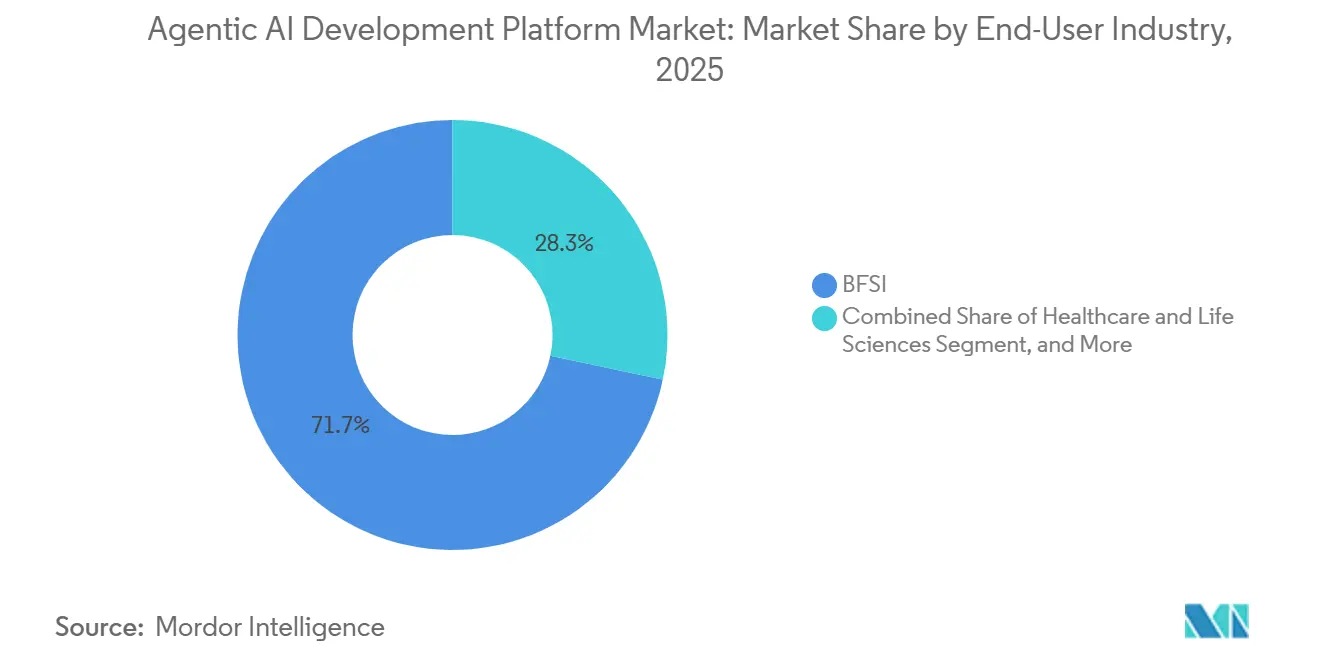

- By end-user industry, BFSI held 71.68% of revenue in 2025, and retail and e-commerce is projected to grow at 36.74% CAGR through 2031.

- By organization size, large enterprises held 66.31% of revenue in 2025, and SMEs are projected to grow at 35.74% CAGR through 2031.

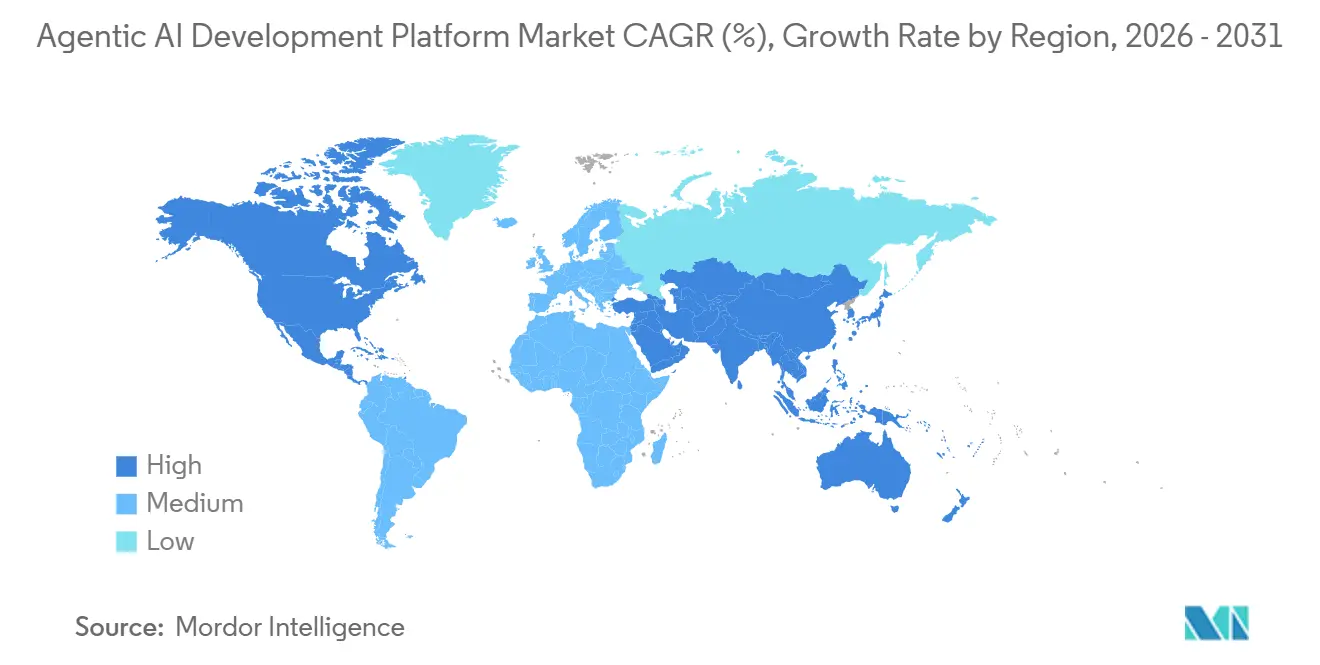

- By geography, North America held 38.73% of revenue in 2025, and Asia-Pacific is projected to grow at 36.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Agentic AI Development Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift From Copilots To Autonomous Workflow Orchestration | +5.8% | Global | Short term (≤ 2 years) |

| Rapid Improvement In LLM Reasoning, Tool Use, And Multi-Agent Frameworks | +4.2% | Global | Short term (≤ 2 years) |

| Falling Deployment Friction Through Low-Code Builders And Managed Agent Runtimes | +3.5% | Global, with early SME gains in North America and APAC | Short term (≤ 2 years) |

| Rising Demand For Governed AI In Regulated Verticals | +3.0% | North America and EU, spill-over to APAC and MEA | Medium term (2-4 years) |

| Standardization Around MCP And Emerging Agent-To-Agent Protocols | +1.8% | Global | Short term (≤ 2 years) |

| ERP And Workflow-System Modernization Creating A New Agent Control Plane Opportunity | +1.5% | APAC and Europe, spill-over to North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift From Copilots to Autonomous Workflow Orchestration

Autonomous orchestration marks the clearest break between earlier copilot tools and the current agentic AI development platform market. Copilots mainly provide prompts and recommendations, while autonomous agents plan tasks, invoke tools, check results, and adjust their next actions with much less human input. That operating model requires a dedicated runtime, stronger state management, and tighter control over actions across enterprise systems. ServiceNow reported in 2026 that its Autonomous Workforce handled more than 90% of employee IT requests and resolved more than 100 million customer cases each month, which shows the operational scale now expected from enterprise agent deployments.[1]ServiceNow, “Knowledge 2026, Otto, AI Control Tower, and AWS Marketplace Milestone,” ServiceNow Newsroom, newsroom.servicenow.com Once workflows are built around a chosen runtime, replacement becomes difficult because integration testing, retraining, and workflow validation must be repeated.

Rapid Improvement in LLM Reasoning, Tool Use, and Multi-Agent Frameworks

The agentic AI development platform market has also advanced, as model and framework performance now enable more reliable completion of conditional workflows in production. Research on the AdaptOrch framework showed that topology-aware scheduling improved performance by 12-23% over static orchestration baselines, with the strongest gains in tasks that require sequential tool use and branching logic. A separate 2026 study on the DOVA framework found that adaptive thinking protocols reduced inference costs by 40-60% on routine tasks by skipping unnecessary extended reasoning. As model outputs converge, buyers are spending more time comparing topology design, memory management, and task coordination than comparing a single foundation model vendor. This is helping specialized runtime vendors in the agentic AI development platform market defend their position even when hyperscalers offer broader model access.

Falling Deployment Friction Through Low-Code Builders And Managed Agent Runtimes

Lower deployment friction is widening the buyer base for the agentic AI development platform market beyond organizations with large in-house machine learning teams. Salesforce stated that Agentforce implementations can reach production in 4-6 weeks, compared with close to 12 months for organizations that build custom agent pipelines from scratch. Microsoft reported that more than 100,000 companies used Copilot Studio to create AI agents by 2025, demonstrating how existing software ecosystems can convert installed customers into platform users without a separate enterprise sales motion. OECD data from 2025 showed AI adoption at 11.9% among small firms, compared with 40% among large firms, and managed runtimes are reducing part of that gap by removing much of the engineering burden. The result is that implementation and customization work remain important even as front-end deployment becomes easier.

Rising Demand For Governed AI In Regulated Verticals

Governance demand is shaping the next phase of the agentic AI development platform market, particularly in financial services, healthcare, and public-sector environments. Cisco reported in 2026 that only 29% of organizations felt ready to secure agentic AI deployments, leaving a significant opening for platforms that offer native controls rather than separate compliance add-ons. The EU AI Act moved into enforcement for high-risk systems in August 2026, and the covered use cases include credit decisioning, hiring automation, and healthcare triage, with penalties that can reach EUR 35 million (USD 39.55 million) or 7% of global turnover. Singapore's Model AI Governance Framework for Agentic AI, published in January 2026, set out accountability expectations that match what many enterprise procurement teams now request in formal vendor reviews. This is pushing vendors in the agentic AI development platform market to treat policy enforcement, audit trails, and access control as core product features rather than later additions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Governance, Auditability, And Security Gaps In Autonomous Agents | -3.5% | Global | Short term (≤ 2 years) |

| Legacy-System Integration Complexity And Unclear ROI Beyond Narrow Workflows | -2.5% | Asia-Pacific and Europe, spill-over to North America | Medium term (2-4 years) |

| Token-Intensive Inference Economics And Agent-Sprawl FinOps Pressure | -1.8% | Global | Short term (≤ 2 years) |

| Evaluation Gaps For Multi-Agent Systems And Weak Traceability Of Agent Memory | -1.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Governance, Auditability, and Security Gaps in Autonomous Agents

Security concerns remain one of the clearest brakes on the agentic AI development platform market because autonomous agents act across multiple systems where traditional controls were not designed to follow them. The MIT AI Agent Index reported in 2025 that only 1 of 200 reviewed production agents used cryptographic signing for action verification, underscoring the continued limitations of current auditability.[2]MIT AI Agent Index Team, “MIT AI Agent Index 2025,” Massachusetts Institute of Technology, agentindex.mit.edu OWASP published its MCP Security Top 10 in 2026 and formalized risks such as prompt injection via tool outputs and overly broad memory-retrieval permissions. These issues prompt enterprise security teams to request lineage tracking, rollback controls, and policy-based access enforcement before approving live use. Vendors that cannot show these controls often face longer sales cycles and higher proof-of-concept costs in regulated accounts.

Legacy-System Integration Complexity And Unclear ROI Beyond Narrow Workflows

The agentic AI development platform market also faces a practical barrier in older enterprise environments where core systems were not built for autonomous orchestration. Many organizations still rely on legacy ERP instances, proprietary manufacturing systems, and fragmented data environments that require middleware for agents to interact with them safely. A 2026 governance maturity study found that only 21% of organizations had reached the level needed to move from narrow single-system tasks to broader cross-system orchestration. Returns are easier to prove in document-heavy workflows such as invoice handling, claims review, and compliance checks, but they become harder to defend in knowledge-intensive processes where a single error can create much higher downstream cost. This keeps proven deployments concentrated in a limited set of use cases, slowing wider account expansion in the agentic AI development platform market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platform Software Leads While Services Growth Reflects Integration Demand

Platform software accounted for 76.39% of the agentic AI development platform market share in 2025, which shows that spending still centers on orchestration engines, agent runtimes, and LLM gateway layers. Enterprises treated this layer as core infrastructure, so buying behavior favored long-term platform commitments before implementation ecosystems had fully scaled. This pattern fits an early-cycle market where foundational control and workflow reliability matter more than adjacent tools. It also explains why platform decisions in the agentic AI development platform market tend to carry longer evaluation windows and higher switching barriers than many standard software purchases.

Professional services are projected to grow at a 36.14% CAGR through 2031, as deployment still requires connector work, memory schema design, governance policy setup, and cross-system authentication planning. Research on adaptive orchestration showed that topology-aware agent management can deliver 12-23% performance gains over static systems, and that finding is feeding demand for architecture design and tuning support. Orchestration middleware is gaining relevance as MCP and agent-to-agent protocol adoption increases the value of cross-protocol adapters and interoperability layers.[3]Anthropic, “Anthropic Contributes Model Context Protocol (MCP) to Linux Foundation AI Alliance,” Anthropic Blog, anthropic.com Evaluation and safety tools are also moving from optional add-ons toward procurement requirements as buyers seek stronger validation, monitoring, and policy testing for production agents.

By Deployment Model: Public Cloud Stays Ahead As Hybrid And Edge Use Cases Expand

Public cloud captured 52.61% of the agentic AI development platform market size in 2025, making it the default starting point for many enterprise deployments. Managed runtimes from hyperscalers gave buyers a faster path to production because model access, orchestration tools, and infrastructure controls were already bundled in a single environment. Microsoft stated that Azure AI Foundry processed more than 100 trillion tokens in a single quarter in 2025, highlighting the extent to which early enterprise demand remained concentrated on public cloud infrastructure. The public cloud lead also reflects the fact that many organizations began with lower-risk pilots before deciding where stricter residency or latency controls were needed.

Hybrid and edge deployments are projected to grow at 36.09% CAGR through 2031 as more buyers run agents closer to data sources, operating systems, and regulated workloads. That push is strongest in industrial settings, public-sector environments, and sectors where round-trip latency or data-transfer rules make centralized cloud processing less practical. AWS expanded this path in 2026 with Bedrock AgentCore, a managed agent-harness platform, and early support for managed multi-agent pipelines. UiPath also released on-premises support for public-sector environments in May 2026, which shows that sovereign and air-gapped deployments are becoming a distinct part of the agentic AI development platform industry. Private cloud continues to matter most in financial services and healthcare, where system-of-record proximity and full audit trails remain central to deployment design.

By End-User Industry: BFSI Holds The Revenue Base While Retail And E-Commerce Builds Fastest

BFSI accounted for 71.68% of end-user revenue in 2025, making it the largest vertical in the agentic AI development platform market. The sector entered this phase with strong data infrastructure, API layers, and compliance tooling already in place from earlier AI and automation programs. That background lowered the barrier to deploying agents for fraud detection, regulatory reporting, and personalized advisory work. It also meant that the agentic AI development platform industry found one of its earliest large-scale production environments in a sector where operational and compliance costs were already easy to measure.

Retail and e-commerce are projected to grow at a 36.74% CAGR through 2031 as agent use cases shift toward personalization, inventory coordination, and real-time customer interaction. Salesforce reported USD 67 billion in AI-influenced global sales during Cyber Week 2025, and AI accounted for 20% of all orders placed during that period. Adobe reported that AI-driven e-commerce traffic rose 693% during the 2025 holiday season compared with 2024, which confirms how quickly shopper-facing automation is expanding. IEEE IT Professional published research in 2026 that estimated agentic AI could generate up to USD 1 trillion in U.S. B2C retail value and USD 3-5 trillion globally by 2030. Healthcare and life sciences, manufacturing, government, and media each remain smaller in 2025 revenue terms, but they are developing clearer production pathways around documentation, maintenance orchestration, procurement review, and content workflows.

By Organization Size: Large Enterprises Still Dominate While SMEs Gain Access Faster

Large enterprises accounted for 66.31% of revenue in 2025, giving them the leading position in the agentic AI development platform market. Their advantage came from wider data access, stronger security infrastructure, and dedicated teams that could support multi-agent deployment and governance. OECD data from 2025 showed AI adoption at 40% among firms with 250 or more employees, compared with 11.9% among firms with 10-49 employees. That adoption gap has long translated into higher platform spending among larger organizations, and the same pattern carried into this market.

SMEs are projected to grow at a 35.74% CAGR through 2031, driven by no-code builders, managed runtimes, and consumption pricing that lower the entry barrier. Microsoft reported that more than 100,000 companies used Copilot Studio to build AI agents by 2025, demonstrating how installed software ecosystems can quickly scale access among smaller organizations. This shift does not remove the advantage held by large vendors, because many SME users still depend on infrastructure and tooling from the same hyperscaler and enterprise software platforms. As a result, the agentic AI development platform market is becoming more accessible to smaller buyers even as platform power becomes increasingly concentrated among a few large providers. That balance supports wider adoption but keeps pricing pressure high for stand-alone developer-focused vendors.

Geography Analysis

North America held 38.73% of the agentic AI development platform market share in 2025, maintaining its revenue leadership. The region benefits from hyperscaler infrastructure, a large enterprise software buyer base, and a regulatory environment favoring voluntary governance. Microsoft reported over 70,000 Azure AI Foundry customer organizations in 2025, highlighting the scale of its enterprise base. OpenAI launched its Frontier enterprise platform in March 2026 with adopters like HP, Intuit, Oracle, and Uber. ServiceNow's USD 1 billion in AWS Marketplace transactions in 2026 indicates cloud marketplaces are becoming key distribution channels.

Asia-Pacific is projected to grow at 36.34% CAGR through 2031, driven by enterprise deployment in China, productivity-led adoption in India, and practical implementation in Japan. NTT Docomo Business planned to offer 200 agent types to enterprise customers in 2026, reflecting structured deployments in Japan.[4]NTT Docomo Business, “Enterprise AI Agent Deployment Plan, 200 Agent Types in 2026,” NTT Docomo Business, nttdocomo.co.jp South Korea is advancing in semiconductor manufacturing and financial services, with private cloud models addressing data-sovereignty concerns. The region is transitioning from experimentation to production workflows and compliance-focused models.

Europe's tighter regulations are shaping the agentic AI development platform market. The EU AI Act enforcement for high-risk systems began in August 2026, alongside increased auditability under the Digital Operational Resilience Act. Germany, the UK, and France lead deployments due to large enterprise bases and compliance spending. European Commission data shows enterprise adaptation budgets of EUR 2.1-4.5 million (USD 2.37-5.09 million) over 18 months for EU AI Act readiness. South America shows early adoption, with Brazil and Argentina gaining traction. The Middle East and Africa are growing through sovereign AI investments, telecom deployments, and banking use cases, led by the UAE, Saudi Arabia, South Africa, and Egypt, though spending remains lower than in other regions through 2031.

Competitive Landscape

The agentic AI development platform market is moderately fragmented, with enterprise deal flow concentrated among a few large vendors, while the wider tooling base remains fragmented. Microsoft, Google, Amazon, Salesforce, and ServiceNow dominate enterprise procurement by leveraging cloud infrastructure, installed software, and access to large accounts. Meanwhile, specialist orchestration vendors compete in developer tools, memory layers, workflow interfaces, and governance features, creating visible concentration in large contracts but not across the full product stack.

Salesforce reported Agentforce reached USD 540 million in annualized recurring revenue with 18,500 enterprise customers, showcasing how quickly incumbents can scale within existing relationships. ServiceNow aims for USD 30 billion in subscription revenue by 2030, with AI contributing over 30% of annual contract value, reflecting the integration of agent capabilities into broader platforms. Microsoft strengthened its position with the March 2026 general availability of the Azure AI Foundry Agent Service, which KPMG adopted for its Clara AI audit platform. SAP expanded its Business AI Platform in May 2026 with over 200 cross-module AI agents, supported by a EUR 100 million (USD 113 million) partner fund and a development agreement with Anthropic. These moves highlight how major vendors are embedding agent orchestration into broader platform strategies.

Differentiation is shifting toward governance, memory handling, and trust across agents. Anthropic's December 2025 donation of MCP to the Linux Foundation's AI Alliance promoted open standards, reducing the value of proprietary connection layers. AWS advanced competition with Bedrock AgentCore, offering enterprises a managed harness for production-grade agents and easing infrastructure burdens. Pure-play vendors like LangChain, LlamaIndex, and Kore.ai remain relevant for their agility in framework design and developer experience but face pressure as standards mature and larger vendors absorb similar capabilities. The market still has opportunities in vertical governance tooling, cross-cloud federation, and multi-agent benchmarking, where no vendor has secured a clear lead.

Agentic AI Development Platform Industry Leaders

Microsoft Corporation

Google LLC

Amazon Web Services, Inc.

Salesforce, Inc.

OpenAI, L.L.C.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: SAP unveiled its Business AI Platform at SAP Sapphire 2026, integrating an Autonomous Suite of over 200 cross-module AI agents, a EUR 100 million (USD 113 million) partner enablement fund, and a joint development agreement with Anthropic to embed Claude models across the SAP portfolio.

- May 2026: ServiceNow at Knowledge 2026 launched Otto (an autonomous IT operations agent) and the AI Control Tower governance dashboard, and announced cumulative AWS Marketplace transactions totaling USD 1 billion.

- May 2026: UiPath announced native integration of Anthropic Claude Code and OpenAI Codex as first-class coding agents within Automation Suite, extending the platform from RPA into software development lifecycle automation and adding enterprise engineering organizations as a new buyer category.

- April 2026: Salesforce released Agentforce Operations to general availability; early enterprise customers reported 50-70% reductions in process cycle times and elimination of 80% of manual data-entry steps, representing the most operationally significant Agentforce release to date.

Global Agentic AI Development Platform Market Report Scope

The Agentic AI Development Platform market comprises global software platforms, orchestration frameworks, development environments, evaluation tools, safety and governance solutions, and related professional services that enable organizations to design, develop, deploy, manage, and optimize autonomous or semi-autonomous artificial intelligence agents. These platforms facilitate the creation of AI systems capable of reasoning, planning, memory management, tool usage, workflow orchestration, and multi-step task execution with minimal human intervention across enterprise and consumer applications.

The Agentic AI Development Platform Market Report is Segmented by Component (Platform Software, Orchestration Middleware, Evaluation and Safety Tools, and Professional Services), Deployment (Public Cloud, Private Cloud, On-Premises, and Hybrid and Edge), End-user Industry (BFSI, Healthcare and Life Sciences, Retail and E-commerce, Media and Entertainment, Manufacturing and Public Sector, and More), Organization Size (Large Enterprises, and Small and Med-size Enterprises), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts Are Provided in Terms of Value (USD).

| Platform Software |

| Orchestration Middleware |

| Evaluation and Safety Tools |

| Professional Services |

| Public Cloud |

| Private Cloud |

| On-premises |

| Hybrid and Edge |

| BFSI |

| Healthcare and Life Sciences |

| Retail and E-Commerce |

| Manufacturing |

| Media and Entertainment |

| Government and Public Sector |

| Other End-user Industries |

| Large Enterprises |

| Small and Mid-size Enterprises (SMEs) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Component | Platform Software | ||

| Orchestration Middleware | |||

| Evaluation and Safety Tools | |||

| Professional Services | |||

| By Deployment Model | Public Cloud | ||

| Private Cloud | |||

| On-premises | |||

| Hybrid and Edge | |||

| By End-user Industry | BFSI | ||

| Healthcare and Life Sciences | |||

| Retail and E-Commerce | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Government and Public Sector | |||

| Other End-user Industries | |||

| By Organization Size | Large Enterprises | ||

| Small and Mid-size Enterprises (SMEs) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and forecast value of the agentic AI development platform space?

The agentic AI development platform market was valued at USD 10.75 billion in 2025, is projected at USD 14.62 billion in 2026, and is forecast to reach USD 66.38 billion by 2031 at a 35.34% CAGR.

Which region leads current demand for agentic AI development platforms?

North America led with 38.73% of 2025 revenue, supported by hyperscaler infrastructure, large enterprise software buyers, and strong marketplace-based procurement activity.

Which region is growing fastest through 2031?

Asia-Pacific is the fastest-growing region with a projected 36.34% CAGR through 2031, supported by rising enterprise deployment activity across China, India, Japan, and other regional markets.

Which component generates the most revenue today?

Platform software led the component mix with 76.39% of 2025 revenue because enterprises first prioritized orchestration engines, runtimes, and LLM gateway layers.

Which end-user group is creating the largest revenue pool?

BFSI accounted for 71.68% of 2025 end-user revenue, reflecting stronger readiness in data infrastructure, compliance tooling, and workflow automation.

Why are SMEs becoming more active buyers?

SMEs are projected to grow at 35.74% CAGR through 2031 because no-code builders, managed runtimes, and consumption pricing reduce the need for large in-house AI engineering teams.

Page last updated on: