Agentic AI In Tool Use And API Integration Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.43 Billion |

| Market Size (2031) | USD 14.22 Billion |

| Growth Rate (2026 - 2031) | 26.27% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agentic AI In Tool Use And API Integration Market Analysis by Mordor Intelligence

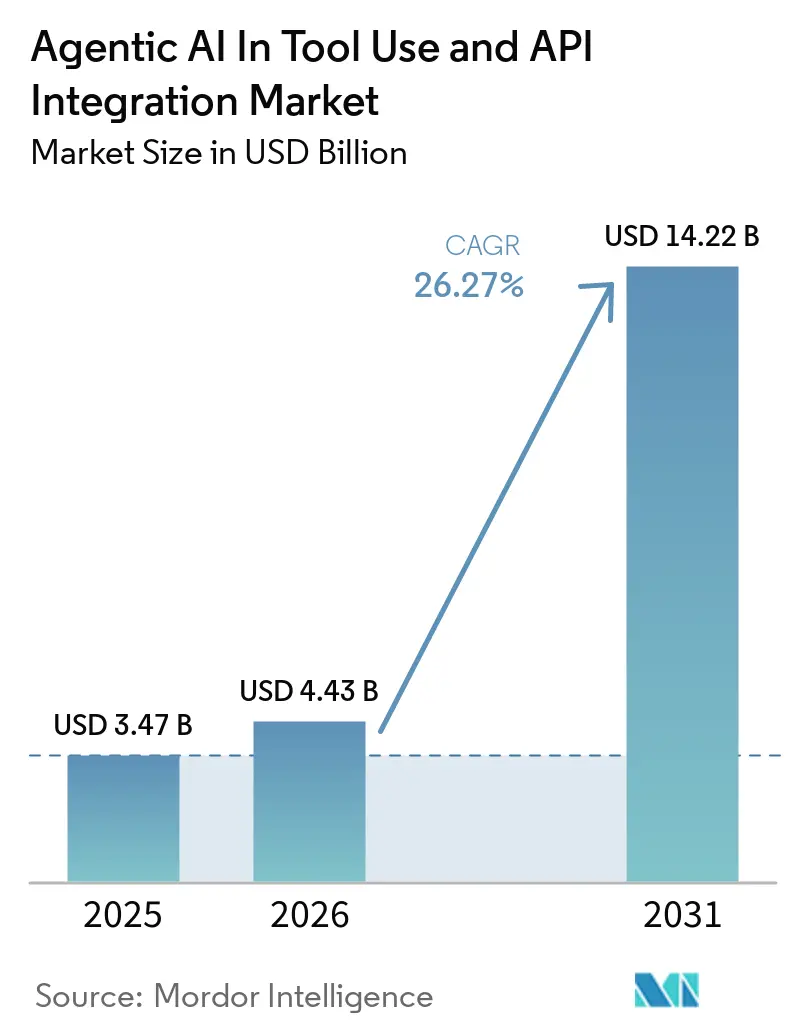

The agentic AI market for tool use and API integration is expected to grow from USD 3.47 billion in 2025 to USD 4.43 billion in 2026, and is forecast to reach USD 14.22 billion by 2031 at a 26.27% CAGR over 2026-2031. This expansion reflects a shift in enterprise software, where AI is moving from a query-support layer to an execution layer that can invoke tools, call APIs, and complete multi-step tasks with limited human supervision. The spread of the Model Context Protocol across major model and cloud ecosystems in 2026 is lowering integration friction and making production deployment easier for buyers who previously had to fund custom API wiring for each workflow. That change is widening the addressable market for agentic AI in the tool-use and API-integration market, especially among mid-sized enterprises that need faster rollouts with lower engineering effort. Competitive pressure is rising at the same time, as hyperscalers embed orchestration into their own stacks while open-source ecosystems draw developers toward common frameworks and reusable tool definitions. The commercial opportunity is therefore shifting toward reliability, governance, observability, and workflow depth, where buyers need stable execution rather than model access alone.

Key Report Takeaways

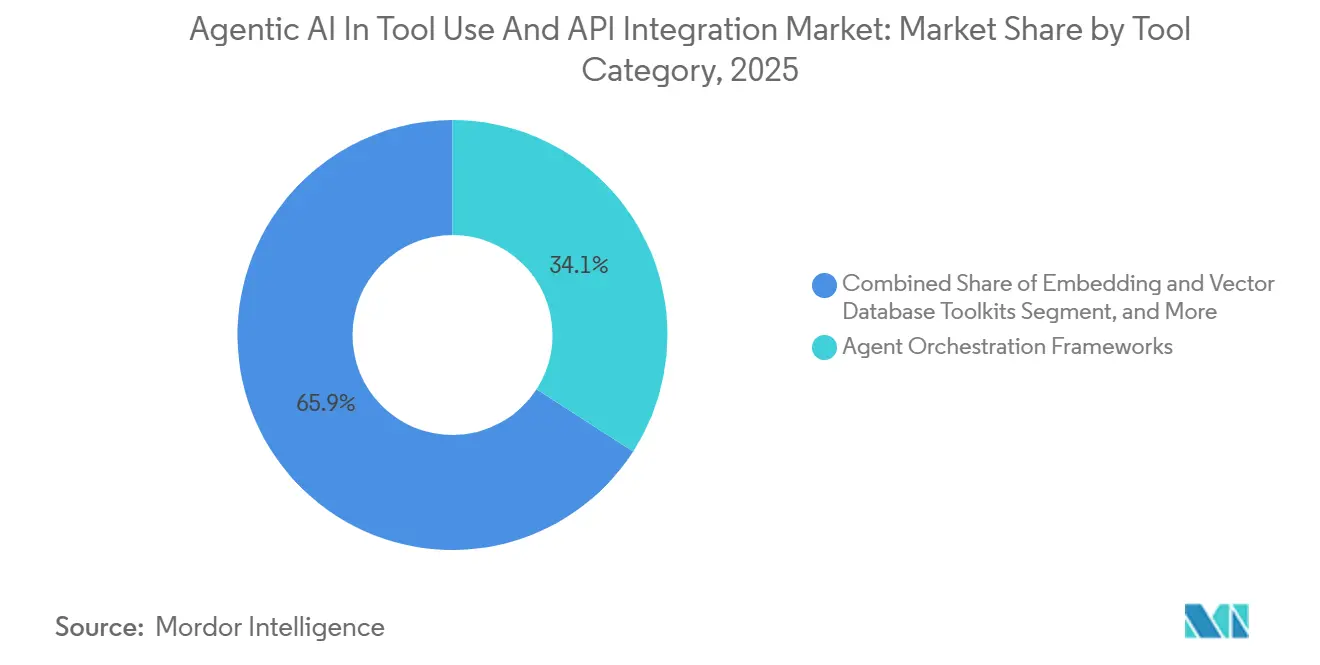

- By tool category, Agent Orchestration Frameworks led with 34.12% revenue share in 2025, while Task Planning and Scheduling Tools are projected to expand at 27.47% CAGR through 2031.

- By API integration style, REST APIs held 46.58% share in 2025, while gRPC APIs recorded the highest projected CAGR at 27.39% through 2031.

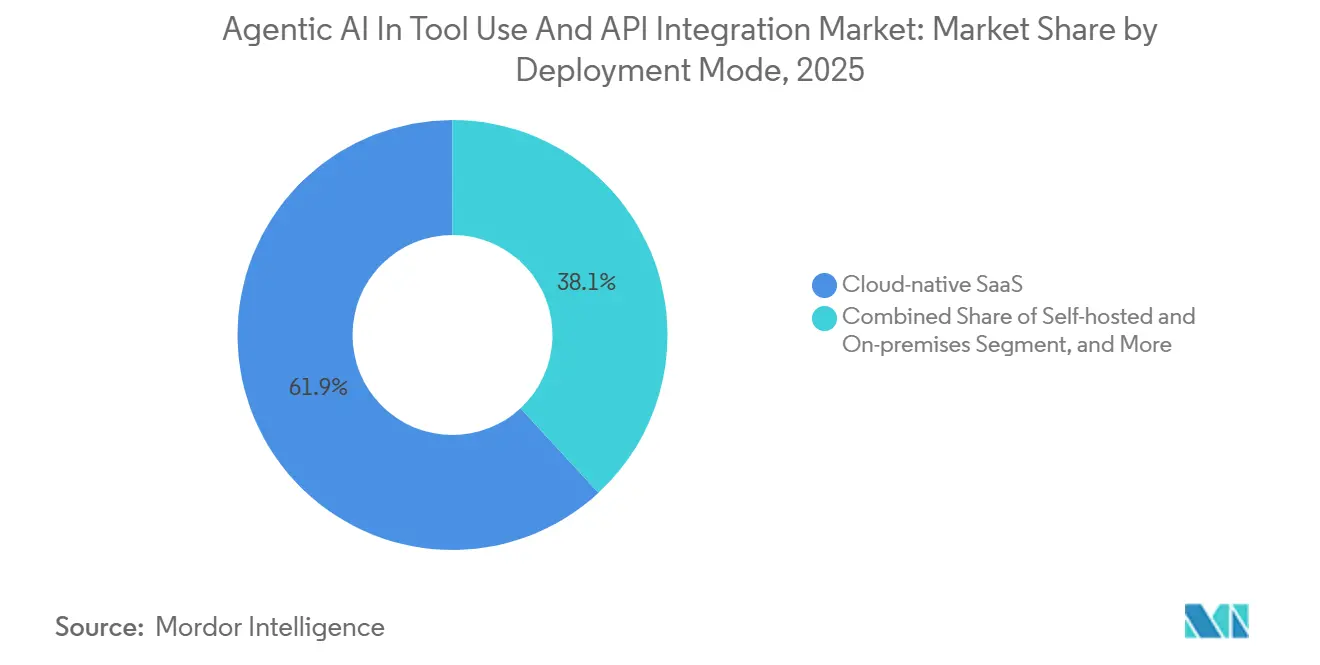

- By deployment mode, Cloud-native SaaS accounted for 61.89% of the market in 2025, while the hybrid model is advancing at a 26.87% CAGR through 2031.

- By end-user industry, Technology and IT Services providers accounted for 29.13% of the market in 2025, while Healthcare and Life Sciences are forecast to grow at a 27.67% CAGR through 2031.

- By geography, North America held a 38.32% share in 2025, while Asia-Pacific is expected to expand at a 27.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Agentic AI In Tool Use And API Integration Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Maturation of Open-source Agent Frameworks | +6.5% | Global, with early gains in North America and Western Europe | Short term (≤ 2 years) |

| Expansion of Domain-specific Vector Databases | +5.2% | Global, APAC core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Accelerated Adoption of Autonomous Workflows in DevOps | +4.8% | North America and Europe, with secondary gains in India and Australia | Short term (≤ 2 years) |

| Growing Demand for Multimodal Prompt Optimization | +3.9% | Global, with early concentration in North America and East Asia | Medium term (2-4 years) |

| Vendor Neutrality Mandates in Regulated Industries | +3.1% | Europe and North America primarily, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Emergence of AutoML-generated Agents Reducing Integration Lead Time | +2.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Maturation of Open-source Agent Frameworks

Rapid improvements in open-source frameworks are changing the buying logic for agentic AI in the tool-use and API-integration market. LangChain expanded its reach in 2025 with 47 million monthly downloads, and the company released LangGraph 1.0 as it raised USD 125 million in Series B funding, showing that open ecosystems now sit close to enterprise production use rather than pure experimentation.[1]LangChain, “LangChain Raises USD 125 million to Build the Platform for Agent Engineering,” LangChain, langchain.com This reduces the time and cost required to build initial workflows, making the agentic AI tool and API integration market more accessible to engineering teams that do not want to start with a full proprietary stack. It also reduces vendors' pricing power for those that sell only framework access, because users can assemble capable orchestration layers from widely adopted open tooling. As a result, commercial differentiation is moving toward observability, governance, security, and enterprise support instead of framework ownership alone.

Expansion of Domain-specific Vector Databases

The expansion of specialized retrieval layers is widening the functional scope of agentic AI in the tool-use and API-integration market. Enterprises increasingly want systems that can supply agents with domain-aware context rather than simple semantic lookup, because tool-calling workflows break down when retrieval quality is poor or poorly governed. That need is shifting value away from raw vector indexing and toward context assembly, access control, and structured knowledge packaging for downstream agent use. The result is a broader role for retrieval infrastructure within the agentic AI tool-use and API-integration market, especially in sectors where agents must combine documents, records, and workflow data before acting. This also raises the strategic value of platforms that can connect retrieval, policy enforcement, and tool execution within a single operational layer.

Accelerated Adoption of Autonomous Workflows in DevOps

DevOps is becoming one of the clearest commercial entry points for agentic AI in the tool-use and API-integration market. GitHub introduced Agentic Workflows in technical preview in February 2026, allowing repository tasks such as triage, test generation, and other automations to be authored in natural language and executed through GitHub Actions. Opsera also launched advanced reasoning AI and autonomous remediation agents in February 2026, with integrations across more than 150 enterprise DevOps tools, demonstrating that buyers want agent control across fragmented delivery environments rather than within a single software estate. These launches matter because software teams already work through API-heavy toolchains, which makes DevOps a natural use case for rapid deployment in the agentic AI tool-use and API-integration market. Vendors that can combine action autonomy with auditability are likely to gain faster traction in regulated software delivery settings.

Growing Demand for Multimodal Prompt Optimization

Multimodal prompt tuning is becoming a practical growth engine for agentic AI in the tool-use and API-integration market. Research presented at ICLR 2025 showed that a VLM-tuned T3-Agent improved tool-use accuracy by 20% relative to untrained multimodal baselines, supporting the commercial case for model and prompt adaptation in tool-driven systems. MLflow also released GEPA-based prompt optimization in October 2025 and reported a 10-percentage-point absolute improvement in accuracy on multi-hop reasoning tasks for OpenAI agents, with a short optimization cycle over small training sets. This improves the practical performance ceiling of the agentic AI in the tool-use and API-integration market, because better prompts often translate into more reliable tool selection and cleaner workflow execution. It also increases the value of lifecycle tooling that can test, refine, and govern prompts as part of standard deployment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of Benchmarking Standards for Agent Reliability | -2.8% | Global | Short term (≤ 2 years) |

| Escalating Cloud-GPU Compute Costs | -2.1% | Global, acute in North America and APAC high-compute hubs | Medium term (2-4 years) |

| Intellectual Property Concerns Around Proprietary SDKs | -1.6% | North America and Europe | Medium term (2-4 years) |

| Talent Gaps in Complex Orchestration Tool Chains | -1.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Benchmarking Standards for Agent Reliability

A lack of accepted reliability standards is holding back the agentic AI in the tool-use and API-integration market, especially in sectors with formal risk review. NeurIPS 2025 research on the Agentic Benchmark Checklist found that applying the checklist to CVE-Bench reduced overestimation of performance by 33%, demonstrating how easily weak benchmark design can distort buyer expectations. Brookings also argued in April 2026 that benchmark-led evaluation alone is insufficient and that field tests, monitored trials, and continuous post-deployment review are needed for real-world assurance. MLCommons is building an AILuminate Agentic initiative, but achieving broad alignment still takes time, leaving buyers with incomplete procurement baselines today.[2]MLCommons, “AILuminate Agentic,” MLCommons, mlcommons.org Until common standards improve, enterprises will continue to move cautiously with high-risk implementations of agentic AI in the tool-use and API-integration market.

Escalating Cloud-GPU Compute Costs

Cloud-GPU costs remain a meaningful restraint on the agentic AI market for tool use and API integration, even as model access becomes easier. Production systems do not only pay for inference; they also incur costs for orchestration, observability, storage, networking, and reliability controls, which can make the total deployment bill materially larger than API access alone. This matters most for organizations that want always-on agents or high-frequency tool calling, because every reliability layer adds operating cost before the workflow reaches scale. The result is a slower buying cycle in the agentic AI tool-use and API-integration market for mid-sized firms that need clear payback before committing to broad deployment. Cost pressure also favors vendors that can improve utilization, reduce waste in tool invocations, and maintain stable performance without constant overprovisioning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tool Category: Orchestration Frameworks Anchor the Stack, Task Planners Accelerate

Agent Orchestration Frameworks held 34.12% of segment revenue in 2025, giving them the leading position in this part of the agentic AI tool use and API integration market. That lead reflects their role as the control layer between reasoning engines and external tools, where workflow state, action routing, and execution order must remain coordinated. The Microsoft Agent Framework entered general availability in Q1 2026 as the production successor to AutoGen, showing how major platform vendors now treat orchestration as a core product layer rather than an experimental feature. LangGraph 1.0 also increased the visibility of graph-based execution models in enterprise design decisions, as part of the broader LangChain expansion in late 2025. Within the agentic AI in tool use and API integration industry, orchestration remains central because it is the point where reliability, tool access, and model reasoning must work together under production constraints.

Task Planning and Scheduling Tools are projected to grow at a 27.47% CAGR through 2031, which makes them the fastest-growing sub-segment in this category. That growth shows that enterprises are moving beyond loose reasoning chains and want stronger workflow control, fallback paths, and approval gates for important tasks. The agentic AI market for tool use and API integration in orchestration-heavy environments is also being reinforced by prompt and optimization tooling, because better planning only works when prompts produce consistent action sequences. MLflow’s October 2025 release of GEPA-based optimization supports that pattern by showing measurable gains in multi-step reasoning quality for agent applications. Over time, value in this category is likely to cluster around vendors that can integrate planning, execution, durability, traceability, and continuous tuning into a single operational workflow.

By API Integration Style: REST Dominates, but gRPC Defines the Performance Frontier

REST APIs commanded 46.58% of this segment in 2025, maintaining their leading position across the agentic AI tool use and API integration market. Their lead is tied to broad compatibility with enterprise SaaS tools, internal services, and public endpoints that agents already need to access. This makes REST the practical default in early deployments, especially where buyers want faster integration across existing software estates rather than a full redesign of transport layers. The installed base also gives REST a durable role in the agentic AI in tool use and API integration market, because most organizations will extend current interfaces before they replace them. Even so, that dominance partly reflects legacy system design rather than the highest possible performance profile for complex agent workflows.

gRPC APIs are projected to expand at a 27.39% CAGR through 2031, making them the fastest-growing integration style. Growth is strongest in architectures where repeated tool calls and low-latency feedback matter, because transport efficiency starts to shape end-user experience once agents handle more than one action in sequence. WebSocket and streaming interfaces are also gaining relevance as workflows depend on live events rather than repeated polling, which is important for real-time responses. Proprietary SDKs still retain influence within closed vendor ecosystems, but their position is under pressure from more standardized connectivity models as the broader agent stack matures. In that context, the agentic AI in the tool-use use API-integrationtion market is moving from simple connectivity toward performance-sensitive integration choices that affect reliability and throughput at scale.

By Deployment Mode: Cloud-native SaaS Leads, Hybrid Tracks Regulatory Tailwinds

Cloud-native SaaS accounted for 61.89% of deployment revenue in 2025, making it the largest deployment model across the agentic AI tool use and API integration market. Buyers favored it because managed delivery shortens deployment cycles, supports elastic scaling, and reduces the internal burden of maintaining early-stage agent infrastructure. This model fits especially well in software-heavy organizations that can tolerate multi-tenant architecture and want rapid iteration as tools and models keep changing. Salesforce strengthened this part of the market in April 2026 by expanding Agent Fabric and extending Runtime Fabric deployment into Canada and Japan, while adding governance and MCP bridge functions for enterprise environments. Within the agentic AI in tool use and API integration industry, cloud delivery remains the fastest way for many buyers to reach production, even when the long-term architecture later becomes more mixed.

Hybrid deployment is projected to grow at a 26.87% CAGR through 2031, making it the fastest-growing model in this segment. The shift reflects stricter requirements for data residency, audit trails, and regulated workflow controls, especially in banking, healthcare, and public-sector use cases. A 2025 German study of nearly 150 IT decision-makers found that API and cloud-native solution integration was viewed as a core IT capability, but compliance obligations are also pushing organizations toward more controlled deployment patterns. That balance is important because the agentic AI in the tool-use and API-integration market increasingly depends on whether vendors can support both agility and governed execution within a single operating model. Self-hosted and on-premises options, therefore, retain strategic importance in sovereign and highly regulated environments, even if they do not generate current revenue.

By End-user Industry: IT Services Sets the Baseline, Healthcare Rewrites the Growth Curve

Technology and IT Services providers accounted for 29.13% of end-user revenue in 2025, putting them at the forefront of adoption in the agentic AI tool and API integration market. Their early lead is tied to greater engineering depth, greater familiarity with the cloud, and a higher tolerance for iterative deployment than most other sectors. Financial services followed with active production movement in 2026, including Goldman Sachs deploying Anthropic Claude agents for trade accounting reconciliation and client onboarding workflows. This supports the view that adoption is shifting from isolated pilots toward governed workflow execution in settings where auditability matters. The agentic AI market share in tool use and API integration for enterprise-heavy verticals is therefore being shaped as much by process control and compliance readiness as by model performance alone.

Healthcare and Life Sciences is projected to expand at a 27.67% CAGR through 2031, making it the fastest-growing end-user vertical. Amazon Connect Health became generally available in March 2026 as a HIPAA-eligible service with agents for patient verification, appointment management, ambient clinical documentation, and ICD-10/CPT medical coding. That launch matters because it targets repetitive administrative workflows with clear labor intensity and strong documentation requirements, which are well-suited to managed-agent execution. The same pattern suggests that healthcare growth in the agentic AI tool-use and API-integration market will be driven first by operational efficiency and workflow accuracy, before broader clinical uses scale further. Manufacturing, media, retail, and other sectors are also moving forward, but their deployment paths still appear less mature than the current pace in healthcare and financial operations.

Geography Analysis

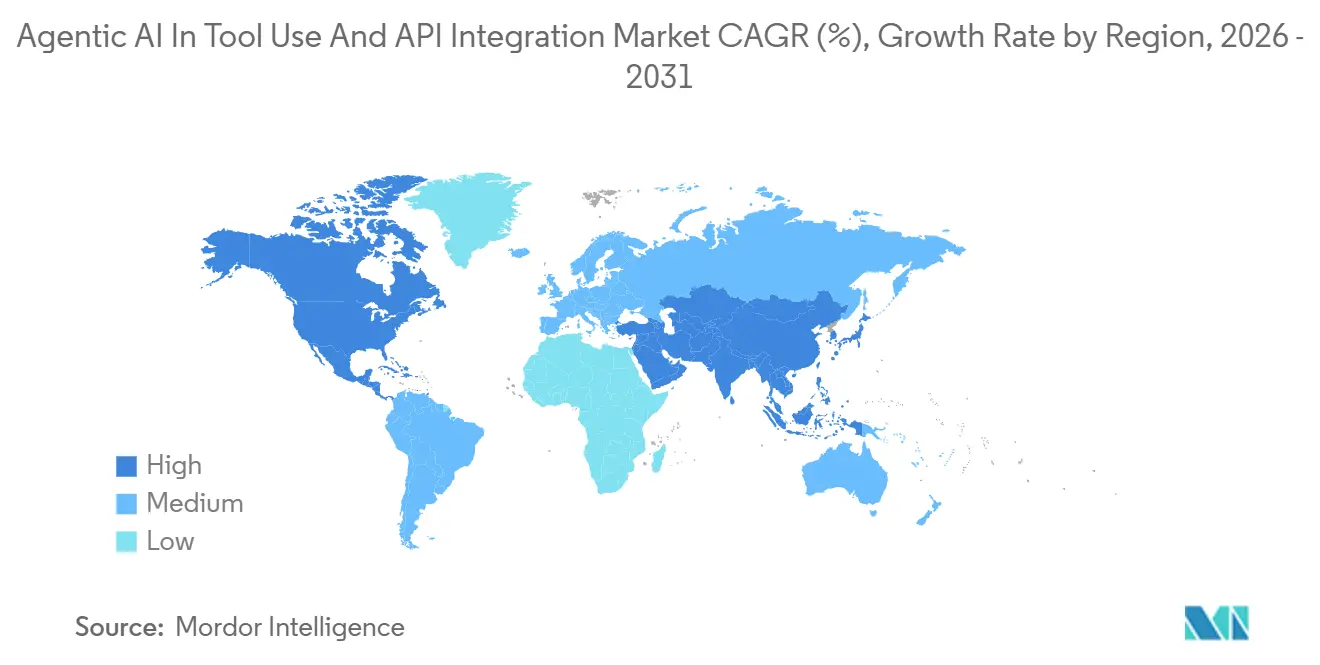

North America accounted for 38.32% of global revenue in 2025, giving the region the largest share of the agentic AI tool use and API integration market. The region benefits from dense hyperscaler infrastructure, major model providers, deep enterprise software demand, and buyers with budgets large enough to move from pilot to production. The Microsoft and OpenAI partnership reset in April 2026 widened cross-cloud access to OpenAI offerings, while Amazon announced an expanded partnership that would place OpenAI models on Amazon Bedrock, strengthening infrastructure choice for enterprise agent builders.[3]Microsoft Corporate Blogs, “The Next Phase of the Microsoft-OpenAI Partnership,” Microsoft, blogs.microsoft.com The United States remains the core revenue base, while Canada and Mexico are contributing incremental adoption in service-heavy sectors. North America also continues to set the pace for production-grade financial applications, as shown by deployments such as Goldman Sachs and the FIS partnership around financial crimes workflows.

Asia-Pacific is expected to grow at a 27.27% CAGR through 2031, making it the fastest-growing geography in the agentic AI tool use and API integration market share analysis. The region’s momentum stems from a mix of enterprise software adoption, hyperscaler partnerships, and a large developer base already using AI in software delivery workflows. Opsera reported in 2026 that 90% of enterprise teams across Asia-Pacific were using AI in the software development lifecycle, which indicates a strong operational foundation for broader agent deployment. Growth is likely to remain uneven across countries, but the regional trajectory is strong because adoption drivers differ by market and still point in the same direction.

Europe held the third-largest regional position, with the United Kingdom and Germany serving as the main demand centers for agentic AI tools, use, and API integration. Compliance requirements under GDPR, the EU AI Act, and local governance standards are shaping deployment choices here more directly than in many other regions. German enterprise buyers are placing greater emphasis on controlled infrastructure and compliant API integration models, which support hybrid and regional hosting patterns. In the United Kingdom and wider European banking environment, Microsoft has highlighted agent deployment in customer-facing and service workflows, reinforcing that regulated sectors are moving ahead when governance tooling is clear. The Middle East, Africa, and South America remain smaller today, but expanding cloud zones and enterprise modernization programs are improving their long-term readiness.

Competitive Landscape

The agentic AI market for tool use and API integration remains moderately fragmented at the product layer, but is consolidating more quickly at the infrastructure and platform layers. Amazon Web Services, Microsoft, and Google are each embedding orchestration and agent services more deeply into their cloud stacks, which shifts bargaining power toward vendors with scale, distribution, and integrated governance. AWS moved further in this direction in May 2026 when it announced general availability of the Claude Platform on AWS, including access to Claude Managed Agents in beta, MCP connector support, Skills API, and web fetch through existing AWS accounts That kind of bundling changes the terms of competition in the agentic AI in tool use and API integration market because buyers can increasingly source core runtime, tooling, and model access from one provider. Specialized vendors, therefore, need stronger cross-cloud interoperability, deeper workflow specialization, or clearer operational differentiation to hold their position.

Strategic moves in 2026 show how quickly adjacent capabilities are being absorbed into wider platform offerings. Google committed up to USD 40 billion to Anthropic in April 2026, which underlined the strategic importance of model access and compute alignment in future enterprise agent ecosystems. Snowflake also expanded Snowflake Intelligence and Cortex Code in April 2026 with MCP connectors, an Agent Software Development Kit for Python and TypeScript, a Claude Code plugin, and a VS Code extension, showing how data platform vendors are trying to become operational control points for enterprise agents. Salesforce took a similar step by broadening Agent Fabric with agent scanners, MCP bridge functions, AI Gateway governance, and wider regional support.[4]Salesforce, “Salesforce Advances Agent Fabric,” Salesforce, salesforce.com These moves suggest that control over integration, observability, and policy layers is becoming as important as the models themselves.

Open ecosystems still matter, which keeps the agentic AI tool-use and API-integration market from becoming fully closed around hyperscaler stacks. LangChain’s scale and the continued visibility of open frameworks show that developers still value portable building blocks and faster experimentation beyond a single vendor's boundaries. This creates room for vendors that serve specific workflow domains such as financial crime review, healthcare documentation, and compliant enterprise automation. FIS, for example, partnered with Anthropic in May 2026 on a Financial Crimes AI Agent, demonstrating that sector-specific execution layers can remain defensible even as general platform capabilities improve. Competition is therefore likely to stay active across three levels: foundational platforms, shared orchestration layers, and specialized workflow solutions.

Agentic AI In Tool Use And API Integration Industry Leaders

OpenAI, L.L.C.

Amazon Web Services, Inc.

Microsoft Corporation

Google LLC

Salesforce, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: AWS announced general availability of Claude Platform on AWS, the first cloud provider to offer direct access to Anthropic's native platform experience, including Claude Managed Agents (beta), MCP connector, Skills API, and web fetch, through existing AWS accounts, enabling enterprise teams to access frontier agentic capabilities without managing separate billing infrastructure.

- May 2026: FIS announced a partnership with Anthropic to deploy a Financial Crimes AI Agent, powered by Claude's reasoning engine combined with FIS's banking compliance infrastructure, to compress AML investigation timelines from hours to minutes.

- April 2026: Google committed up to USD 40 billion in Anthropic at a USD 380 billion valuation, including an immediate USD 10 billion tranche, while separately securing a 5-gigawatt compute arrangement starting in 2027.

- April 2026: Microsoft and OpenAI restructured their partnership, removing exclusivity and allowing OpenAI to sell products across any cloud provider. Amazon concurrently announced it would invest up to USD 50 billion in OpenAI, including USD 15 billion initially, with OpenAI's Frontier agent-building platform hosted exclusively on Amazon Web Services (AWS) via Amazon Bedrock.

Global Agentic AI In Tool Use And API Integration Market Report Scope

The Agentic AI in Tool Use and API Integration market refers to the ecosystem of software platforms, frameworks, middleware, and intelligent orchestration solutions that enable autonomous or semi-autonomous artificial intelligence agents to interact with external tools, enterprise systems, databases, applications, and APIs in order to execute tasks, retrieve information, automate workflows, and support decision-making processes. This market encompasses technologies that allow AI agents to dynamically select, invoke, manage, and coordinate tools and API connections across cloud, on-premises, and hybrid environments with minimal human intervention.

The Agentic AI in Tool Use and API Integration Report is Segmented by Tool Category (Agent Orchestration Frameworks, Embedding and Vector Database Toolkits, Prompt Engineering and Optimization Tools, Task Planning and Scheduling Tools, Monitoring and Observability Tools, and Other Tool Categories), API Integration Style (REST APIs, GraphQL APIs, gRPC APIs, WebSocket and Streaming APIs, Proprietary SDKs, Other API Integration Styles), Deployment (Cloud-native SaaS, Self-hosted and On-premises, and Hybrid), End-User Industry (Technology and IT Services Providers, Financial Services, Healthcare and Life Sciences, Media and Entertainment, Manufacturing and Industrial, Retail and E-commerc, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Agent Orchestration Frameworks |

| Embedding and Vector Database Toolkits |

| Prompt Engineering and Optimization Tools |

| Task Planning and Scheduling Tools |

| Monitoring and Observability Tools |

| Other Tool Categories |

| REST APIs |

| GraphQL APIs |

| gRPC APIs |

| WebSocket and Streaming APIs |

| Proprietary SDKs |

| Other API Integration Styles |

| Cloud-native SaaS |

| Self-hosted and On-premises |

| Hybrid |

| Technology and IT Services Providers |

| Financial Services |

| Healthcare and Life Sciences |

| Media and Entertainment |

| Manufacturing and Industrial |

| Retail and E-commerce |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Tool Category | Agent Orchestration Frameworks | ||

| Embedding and Vector Database Toolkits | |||

| Prompt Engineering and Optimization Tools | |||

| Task Planning and Scheduling Tools | |||

| Monitoring and Observability Tools | |||

| Other Tool Categories | |||

| By API Integration Style | REST APIs | ||

| GraphQL APIs | |||

| gRPC APIs | |||

| WebSocket and Streaming APIs | |||

| Proprietary SDKs | |||

| Other API Integration Styles | |||

| By Deployment Mode | Cloud-native SaaS | ||

| Self-hosted and On-premises | |||

| Hybrid | |||

| By End-User Industry | Technology and IT Services Providers | ||

| Financial Services | |||

| Healthcare and Life Sciences | |||

| Media and Entertainment | |||

| Manufacturing and Industrial | |||

| Retail and E-commerce | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and forecast value of the agentic AI in tool use and API integration market?

The agentic AI in tool use and API integration market was valued at USD 3.47 billion in 2025, stands at USD 4.43 billion in 2026, and is forecast to reach USD 14.22 billion by 2031 at a 26.27% CAGR.

Which tool category leads revenue generation in this space?

Agent Orchestration Frameworks led with 34.12% share in 2025 because they sit between model reasoning and external tool execution, making them central to production workflow control.

Which API style is growing the fastest for enterprise agent deployments?

GRPC APIs are forecast to grow at 27.39% CAGR through 2031, reflecting stronger demand from low-latency and multi-step workflows where transport efficiency matters more.

Why is hybrid deployment gaining ground despite Cloud-native SaaS leadership?

Cloud-native SaaS led with 61.89% share in 2025, but hybrid deployment is growing at 26.87% CAGR because regulated buyers need stronger control over residency, audit trails, and sensitive workflows.

Which end-user group is growing the fastest in 2026 and beyond?

Healthcare and Life Sciences is the fastest-growing vertical, with a projected 27.67% CAGR through 2031, supported by demand for patient verification, documentation, and coding automation.

Which region offers the strongest growth outlook through 2031?

Asia-Pacific is expected to grow at 27.27% CAGR through 2031, while North America remains the largest regional base with 38.32% share in 2025.

Page last updated on: