AI In Healthcare Governance And Safety Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

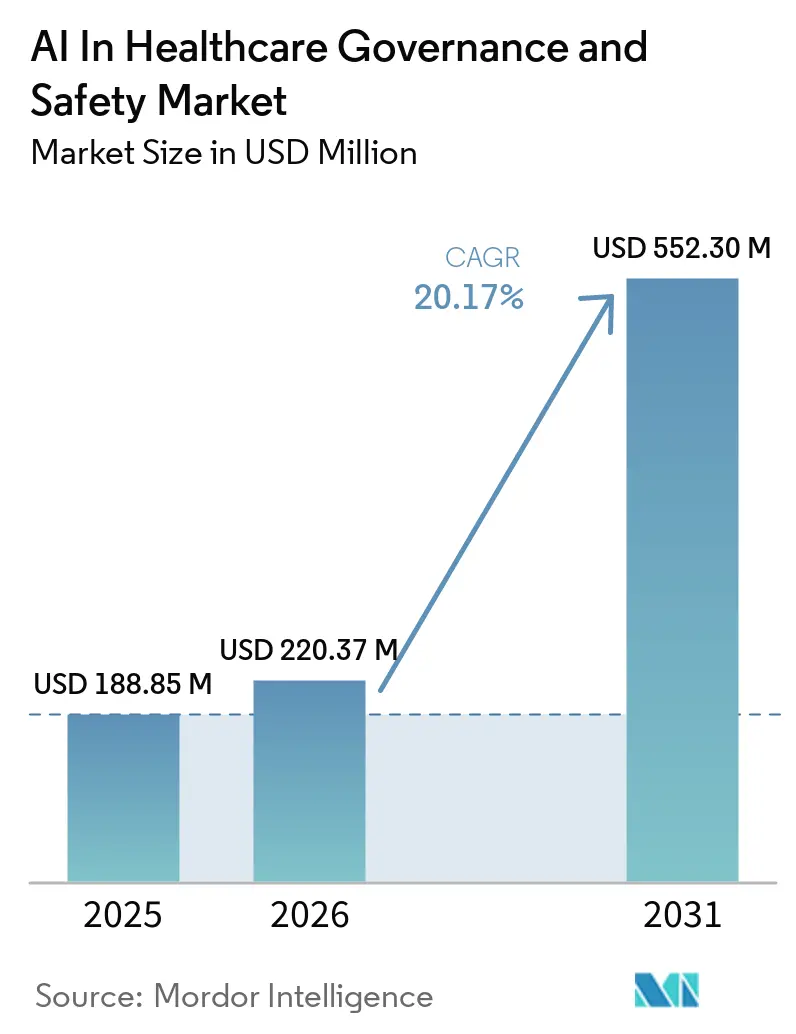

| Market Size (2026) | USD 220.37 Million |

| Market Size (2031) | USD 552.30 Million |

| Growth Rate (2026 - 2031) | 20.17% CAGR |

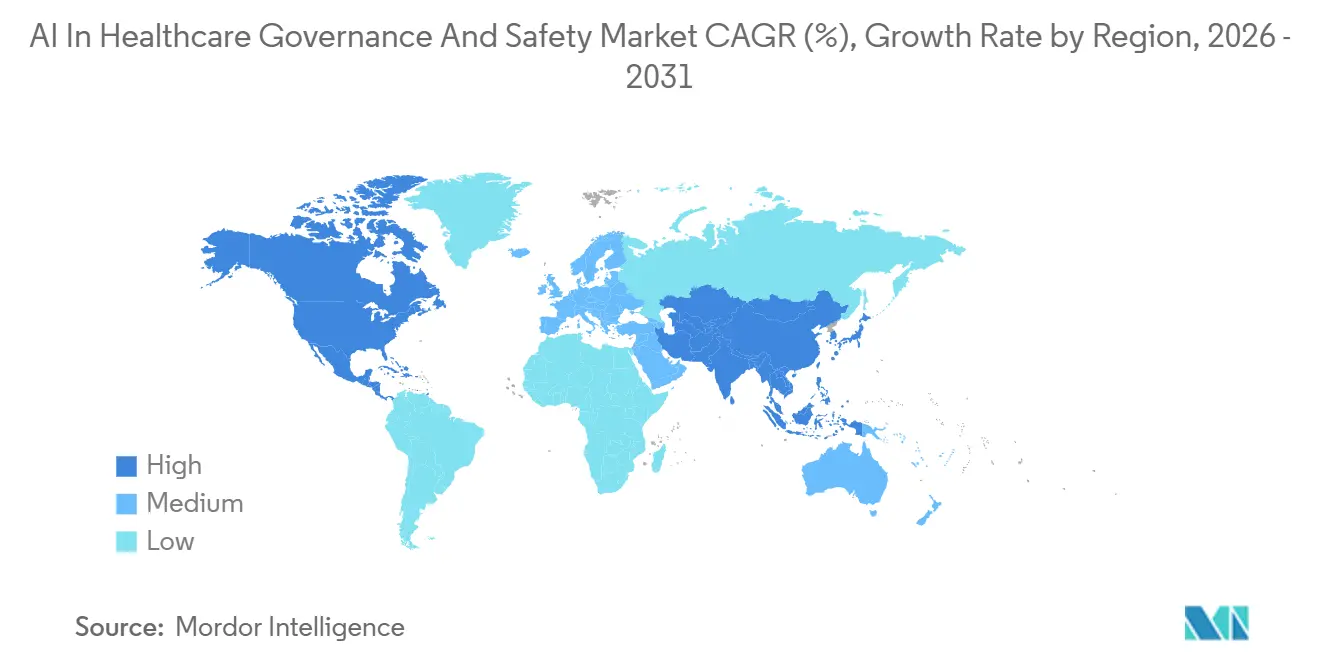

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

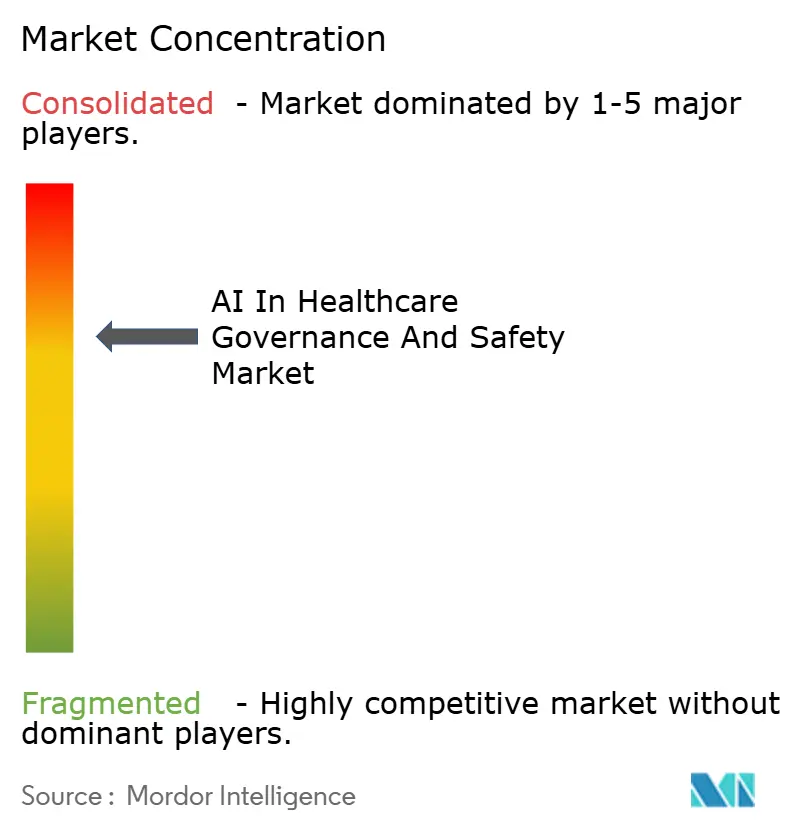

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Healthcare Governance And Safety Market Analysis by Mordor Intelligence

The AI in healthcare governance and safety market size is expected to grow from USD 188.85 million in 2025 to USD 220.37 million in 2026 and is forecast to reach USD 552.30 million by 2031 at a 20.17% CAGR over 2026-2031. Rising regulatory scrutiny, payer-driven surveillance clauses, and hyperscaler bundles position governance software as a core layer of digital-health infrastructure. U.S. FDA guidance that permits iterative software updates only if real-world performance is continuously tracked has pushed many hospitals to expand monitoring budgets. In Europe, the AI Act classifies most clinical algorithms as high-risk devices, forcing MedTech firms to budget for third-party conformity assessments well before the 2027 deadline. At the same time, cyber-insurance carriers are discounting premiums for health systems that can prove certified model inventories and drift detection, turning governance from a discretionary project into a line-item cost of care delivery. Together, these shifts elevate the AI in healthcare governance and safety market from a compliance add-on to a prerequisite for algorithmic reimbursement.

Key Report Takeaways

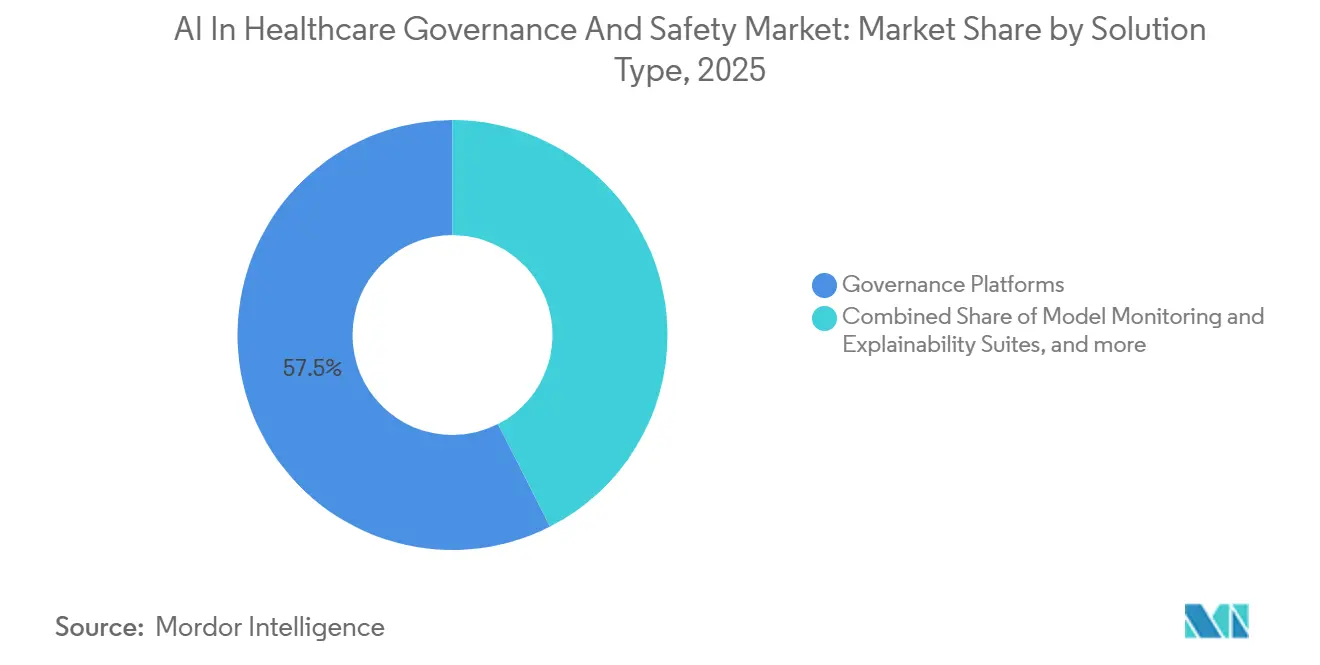

- By solution type, governance platforms held 57.47% of the AI in healthcare governance and safety market share in 2025. Data-privacy and security modules are projected to expand at a 22.24% CAGR through 2031, the fastest pace among solution types.

- By deployment model, cloud deployment commanded 60.33% share of the AI in healthcare governance and safety market size in 2025, while the segment is poised to advance at a 22.74% CAGR over the forecast window.

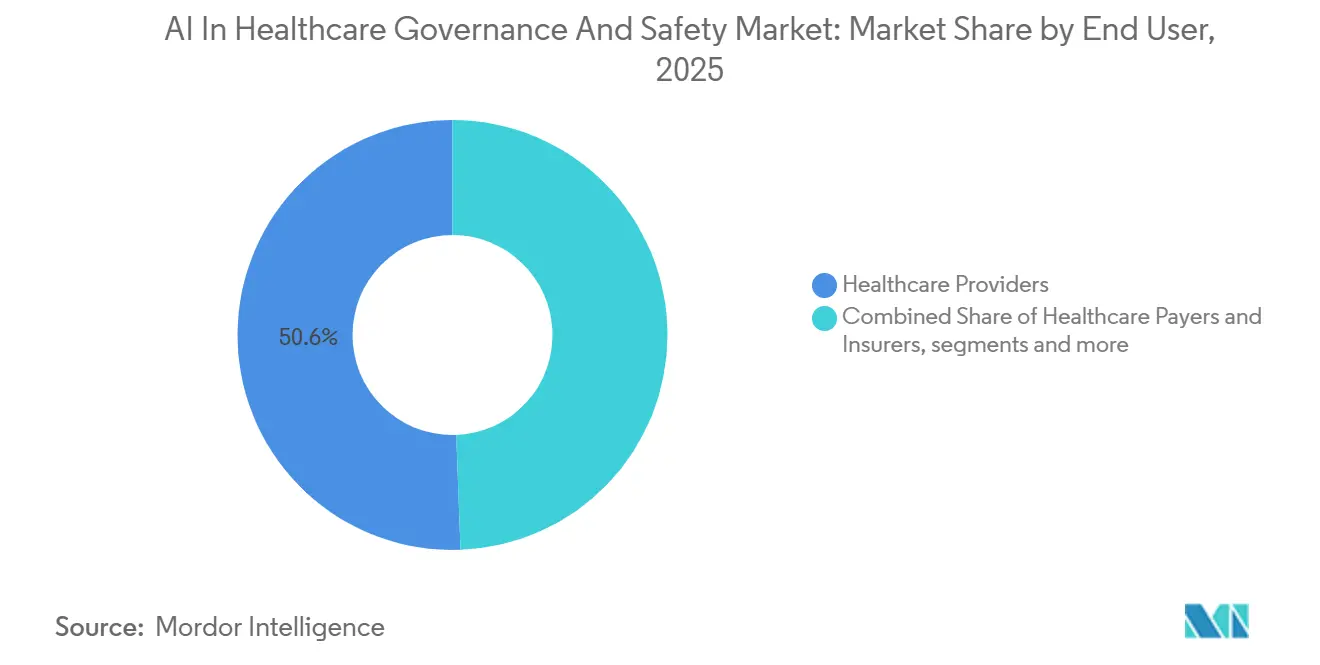

- By end user, healthcare providers accounted for 50.64% spending in 2025; healthcare payers and insurers are forecast to register the highest 21.41% CAGR to 2031.

- By region, North America led with 51.10% regional share in 2025, whereas Asia-Pacific is anticipated to post the strongest 23.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Healthcare Governance And Safety Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mainstream Regulatory Push for SaMD Lifecycle Oversight | +4.2% | Global, early enforcement in EU and U.S. | Medium term (2-4 years) |

| Workforce Shortages Driving Adoption of Governance Automation | +3.1% | North America, Europe, spillover to APAC urban centers | Short term (≤2 years) |

| Cloud Hyperscaler Responsible-AI Toolkits Bundled with Compute | +3.8% | Global, strongest in North America and Europe | Short term (≤2 years) |

| Post-Market Surveillance Mandates by Payers and Insurers | +2.9% | North America, emerging in Western Europe | Medium term (2-4 years) |

| Emergence of AI Audit-as-a-Service Vendors | +2.3% | North America and Europe, nascent in APAC | Medium term (2-4 years) |

| Hospital Cyber-Insurance Requiring Certified AI-Governance Stack | +1.9% | North America, early uptake in UK and Germany | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Mainstream Regulatory Push for SaMD Lifecycle Oversight

The FDA’s Predetermined Change Control Plan, finalized in August 2025, allows vendors to ship software updates without fresh submissions if ongoing drift and performance dashboards remain within approved bounds.[1]U.S. Food and Drug Administration, “Predetermined Change Control Plan Guidance,” fda.gov Europe’s AI Act extends even stricter rules by demanding third-party conformity assessments and structured post-market monitoring for high-risk medical algorithms, with enforcement beginning August 2027. Japan and China have introduced parallel documents that require traceable data provenance and documented update protocols, effectively synchronizing global expectations. Vendors now architect governance workflows to satisfy the most stringent jurisdiction first, anchoring a multiyear tailwind for the AI in healthcare governance and safety market. The cumulative effect is an estimated 4.2 percentage-point lift to forecast CAGR as legacy SaMD portfolios are retrofitted with monitoring pipelines.

Workforce Shortages Prompting Governance Automation

Hospitals face acute clinician and data-science vacancies, which pushes informatics leaders toward platforms that auto-generate audit trails, bias reports, and regulatory filings. IBM’s watsonx.governance exports complete model-lineage dossiers in minutes, freeing scarce compliance analysts for higher-value clinical reviews. Similar automation is gaining traction in European health systems constrained by statutory work-hour caps. Because these tools offset labor gaps better than incremental hiring, demand spikes immediately, contributing to growth.

Cloud Hyperscaler Responsible-AI Toolkits Bundled with Comput

Google Cloud’s Vertex AI Monitoring, HIPAA-eligible since 2024, supplies explainability charts and drift alarms within the same console clinicians already use for model training.[2]Google Cloud, “Vertex AI Monitoring,” cloud.google.com Microsoft followed with Responsible AI dashboards inside Azure AI Studio in 2026, providing fairness metrics and automated EU AI Act documentation.[3]Microsoft, “Azure AI Studio Responsible AI,” microsoft.com Bundling collapses procurement cycles, because governance becomes a default checkbox rather than a standalone purchase, and it erects switching costs that deepen long-term cloud reliance. This synergy adds roughly 3.8 percentage points to the market’s CAGR.

Post-Market Surveillance Mandates by Payers

The U.S. Centers for Medicare & Medicaid Services proposed in 2025 that any AI tool influencing coverage must undergo annual bias auditing, effectively forcing providers to maintain continuous monitoring. Private insurers are inserting similar language into prior-authorization contracts, transforming transparency from a best practice into a reimbursement prerequisite. These clauses accelerate platform uptake among hospitals that previously delayed governance investments, boosting the AI in healthcare governance and safety market trajectory by 2.9 percentage points through the medium term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Cross-Border Data-Sovereignty Regimes | -2.7% | Global, acute along EU-U.S.-China corridors | Medium term (2-4 years) |

| GPU Export Controls Limiting On-Premises Compliance Builds | -1.8% | China, Russia, spillover to Middle East | Short term (≤2 years) |

| Talent Gap in Clinical-AI Risk Management | -1.6% | Global, most severe in North America and Europe | Medium term (2-4 years) |

| Vendor-Lock-In Fears Slowing Multi-Year Contracts | -1.3% | North America and Europe | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Fragmented Cross-Border Data-Sovereignty Regimes

Regulations such as GDPR, HIPAA, and China’s PIPL create incompatible rules for healthcare data storage and transfer across regions. While GDPR restricts cross-border data movement, HIPAA allows conditional flexibility, and PIPL enforces strict data localization. This forces multinational healthcare providers to maintain separate data pipelines, model training environments, and compliance systems for the same AI algorithms. The resulting duplication increases infrastructure and regulatory costs, slows simultaneous global product launches, and limits the ability to train models on unified datasets. Overall, this fragmentation reduces deployment efficiency and is estimated to shave 2.7 percentage points off market growth.

GPU Export Controls Limiting On-Premises Builds

U.S. restrictions on advanced AI chips, especially high-performance GPUs like NVIDIA’s A100 and H100, limit access for healthcare institutions in regions such as China. As a result, hospitals often rely on lower-performance domestic chips, which reduces computing capacity for real-time AI applications. This impacts workloads like clinical decision support, imaging analysis, and continuous model monitoring, particularly drift detection systems. The reduced compute power slows down real-time governance and pushes systems toward less effective batch processing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Governance Platforms Anchor, Privacy Modules Accelerate

Governance Platforms generated 57.47% of 2025 revenue as health systems prioritized foundational model inventories, lineage tracking, and change control, the core capabilities that every other module builds upon. IBM, Oracle, and SAP dominate because their suites integrate directly into existing EHR and ERP architectures, minimizing integration costs. The AI in healthcare governance and safety market size for Data-Privacy and Security Modules is projected to expand at 22.24% CAGR, reflecting the EU AI Act’s encryption mandates and rising cross-border research. Oracle’s Health Data Intelligence and Microsoft’s Confidential Computing enable federated learning without raw-data pooling, ensuring compliance with strict localization laws. Model-Monitoring and Explainability Suites capture spend from device makers facing FDA lifecycle scrutiny, while Bias-Auditing Tools gain momentum as payers demand equity clauses. Compliance-and-Reporting Services flourish among mid-market MedTech manufacturers that lack in-house regulatory teams; ValidMind’s auto-generated documentation accelerates CE-mark submissions by several weeks.

Although consolidation pressures grow, point solutions persist where interoperability matters. Credo AI’s vendor-neutral fairness engine plugs into any cloud and exports PDF certificates accepted by both FDA and European notified bodies. SAP’s enterprise-wide AI Ethics module, released in 2025, governs not just clinical models but also scheduling and billing algorithms, pushing the AI in healthcare governance and safety market toward horizontal expansion across hospital departments.

By Deployment Model: Cloud Dominance Reinforced by Hyperscaler Bundling

Cloud implementations held 60.33% of AI in healthcare governance and safety market share in 2025 and will record a 22.74% CAGR through 2031, propelled by embedded governance inside major ML platforms. Google Cloud’s HIPAA-eligible Vertex AI Monitoring allows cardiology departments to deploy drift alerts without exporting data outside the health-system perimeter. Microsoft embeds fairness dashboards into Azure AI Studio, letting radiologists generate EU AI Act files from the same workspace used for model tuning. This frictionless path reinforces cloud as the default venue for new workflows and steadily grows the AI in healthcare governance and safety market.

On-premises remains essential for military hospitals, genomic research centers, and Chinese providers constrained by data-localization edicts. However, export-control limits on high-end GPUs erode performance advantages and slow new procurements. Hybrid architectures emerge as a bridge: sensitive images stay on-site, while anonymized predictions stream to a cloud dashboard for centralized oversight. IBM’s watsonx.governance offers central policy authoring with edge enforcement, a model expected to gain share in regions with complex sovereignty laws.

By End User: Healthcare Providers Lead, Healthcare Payers Accelerate on Reimbursement Leverage

Healthcare providers contributed 50.64% of 2025 revenue as they sought to govern internally developed decision-support algorithms and vendor SaaS offerings. The AI in healthcare governance and safety market size tied to payers and insurers is expected to climb rapidly, driven by new contract clauses that make bias audits a reimbursement condition. CMS’s draft rule requires annual fairness certificates for AI systems influencing coverage determinations, a stipulation that pushes governance spend directly onto provider ledgers. Pharmaceutical firms adopt lineage and provenance tracking to defend intellectual property in adaptive-trial models, while device manufacturers face direct regulatory pressure and remain heavy investors in real-time monitoring to satisfy FDA change-control rules. Public agencies are smaller buyers but influential, as national health systems publish procurement templates that private hospitals quickly emulate.

Geography Analysis

North America held 51.10% of AI in healthcare governance and safety market share in 2025, anchored by FDA lifecycle oversight and payer-imposed surveillance. The U.S. leads in integrated cloud deployments, helped by HIPAA-eligible offerings from all three hyperscalers. Canada follows similar patterns, with Health Canada signaling in 2025 that EU AI Act conformity reports will be accepted as supporting evidence, simplifying cross-border launches.

Europe is pacing toward full AI Act enforcement by 2027, spurring early spending on conformity-assessment dry runs. Germany and France are the largest buyers, supported by national grants that cover up to 30% of platform costs for SMEs building high-risk algorithms. The region favors federated architectures that keep data inside domestic clouds yet maintain centralized oversight. The AI in healthcare governance and safety market size for Europe is consequently expanding in mid-teens percentages, despite macroeconomic softness.

Asia-Pacific is the fastest-growing region at a projected 23.36% CAGR. China’s NMPA approved 60 AI-enabled devices in 2024, each requiring lifecycle documentation and post-market monitoring, which lifts platform demand even under GPU constraints. Japan’s PMDA released ML-specific guidance in early 2025 that recommends continuous drift tracking between software updates, driving first-wave procurement among diagnostic-imaging vendors. Australia, South Korea, and India are streamlining SaMD frameworks to align with FDA terminology, reducing localization overhead for global vendors and making cloud-based governance commercially viable across the region.

Competitive Landscape

The AI in healthcare governance and safety market remains moderately fragmented. IBM, Microsoft, Oracle, and SAP bundle governance into expansive health-data portfolios, leveraging incumbent EHR footprints. Google Cloud and Microsoft deepen embedded controls, turning governance into a near-zero-incremental-cost feature that scales with compute consumption. This dynamic pressures pure-play startups to specialize; ValidMind and Credo AI focus on audit-grade documentation and demographic-parity scoring, winning contracts from mid-market device makers that fear hyperscaler lock-in.

Hardware constraints and regional privacy rules open white-space for hybrid-deployment specialists. IBM’s edge policy enforcement and Oracle’s confidential VM enclaves appeal to hospitals that must straddle cloud convenience and on-premises sovereignty. No supplier yet offers a turnkey translator that maps FDA change-control dossiers to AI Act conformity files and China NMPA annexes, so multinational MedTech firms juggle three parallel governance stacks. Vendors racing to build this translation layer could secure outsized share.

Technology leadership is shifting toward causal inference and counterfactual explainability. IBM Research published peer-reviewed causal-AI methods in 2025, and Microsoft integrated counterfactual generators into its Responsible AI toolkit in 2026, promising regulators clearer evidence that model outputs reflect clinically meaningful drivers. Such advances, plus bundled pricing, reinforce the two-tier market: full-stack clouds for integrated delivery networks and audit-focused point solutions for specialized payers or device makers.

AI In Healthcare Governance And Safety Industry Leaders

IBM

Microsoft

Google Cloud

SAS Institute

Credo AI

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: The FDA finalized its Predetermined Change Control Plan guidance, legalizing algorithm updates within preset safety bounds as long as real-world performance dashboards remain in spec.

- March 2025: SAP embedded AI Ethics controls across its enterprise suite, allowing hospitals to enforce version-controlled policies organization-wide.

- January 2025: The FDA released Good Machine Learning Practice principles, outlining continuous monitoring and human-oversight expectations for SaMD vendors.

Global AI In Healthcare Governance And Safety Market Report Scope

According to the report’s scope, AI in healthcare governance and safety refers to the systems, policies, and oversight mechanisms that ensure AI tools used in clinical and operational settings are safe, ethical, transparent, and compliant with regulatory standards. It covers how health systems validate algorithms, manage risks, protect patient data, monitor model performance, prevent bias, and maintain accountability throughout the AI lifecycle, from pre‑deployment evaluation to continuous post‑deployment surveillance, so that AI improves care without compromising patient safety, equity, or trust.

The AI in healthcare governance and safety market is segmented into solution type, deployment model, end user, and geography. By solution type, the market is segmented into governance platforms, model monitoring and explainability suites, bias and fairness auditing tools, data-privacy and security modules, compliance and reporting services, and others. By deployment type, the market is segmented into on-premises and cloud. By end user, the market is segmented into healthcare providers, healthcare payers and insurers, pharmaceutical and biotech firms, medtech and device manufacturers, regulators and public agencies. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Governance Platforms |

| Model Monitoring and Explainability Suites |

| Bias and Fairness Auditing Tools |

| Data-Privacy and Security Modules |

| Compliance and Reporting Services |

| Others |

| On-Premises |

| Cloud |

| Healthcare Providers |

| Healthcare Payers and Insurers |

| Pharmaceutical and Biotech Firms |

| MedTech and Device Manufacturers |

| Regulators and Public Agencies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Solution Type | Governance Platforms | |

| Model Monitoring and Explainability Suites | ||

| Bias and Fairness Auditing Tools | ||

| Data-Privacy and Security Modules | ||

| Compliance and Reporting Services | ||

| Others | ||

| By Deployment Model | On-Premises | |

| Cloud | ||

| By End User | Healthcare Providers | |

| Healthcare Payers and Insurers | ||

| Pharmaceutical and Biotech Firms | ||

| MedTech and Device Manufacturers | ||

| Regulators and Public Agencies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the AI in healthcare governance and safety market be by 2031?

According to Mordor Intelligence, it is projected to reach USD 552.30 million, growing at a CAGR of 20.17% during 2026 to 2031.

Which segment leads AI governance spending today?

Governance Platforms captured 57.47% of 2025 revenue, reflecting their role as the backbone for model inventory and change control.

What region is growing fastest?

Asia-Pacific is projected to post a 23.36% CAGR through 2031, fueled by Chinese and Japanese regulatory momentum.

Why are payers important to adoption?

U.S. and European insurers now embed bias-audit requirements into reimbursement contracts, pushing providers to buy continuous-monitoring tools.

Page last updated on: