Polyhydroxyalkanoates Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

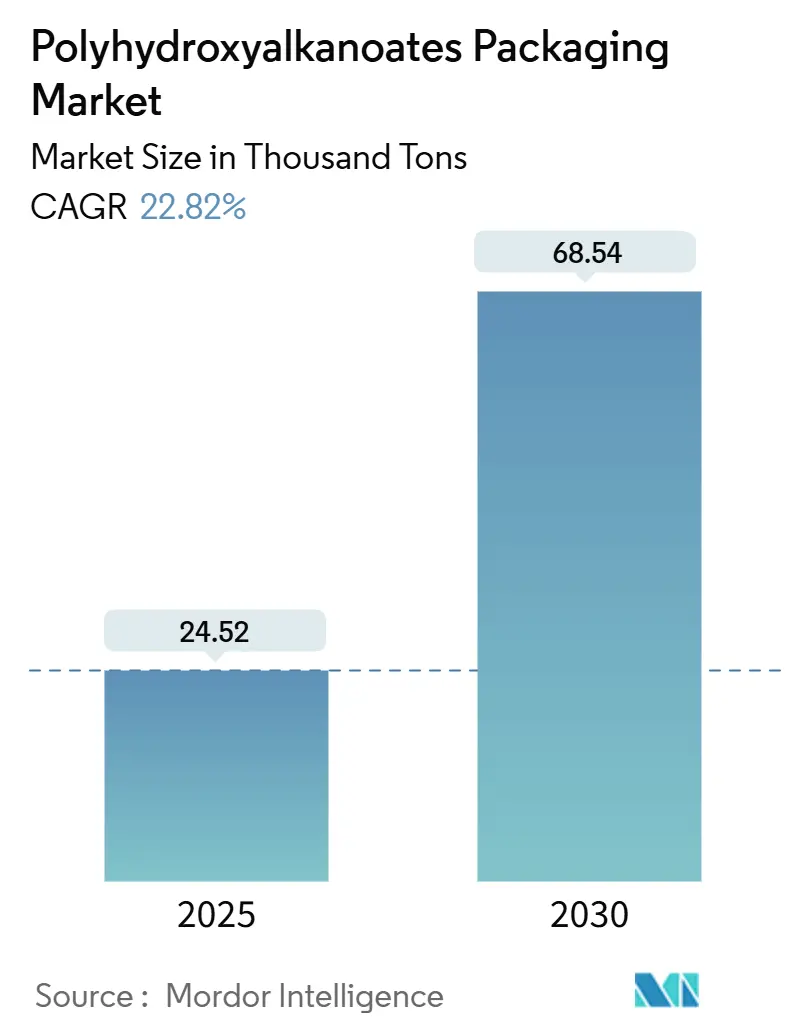

| Market Volume (2025) | 24.52 Thousand tons |

| Market Volume (2030) | 68.54 Thousand tons |

| Growth Rate (2025 - 2030) | 22.82% CAGR |

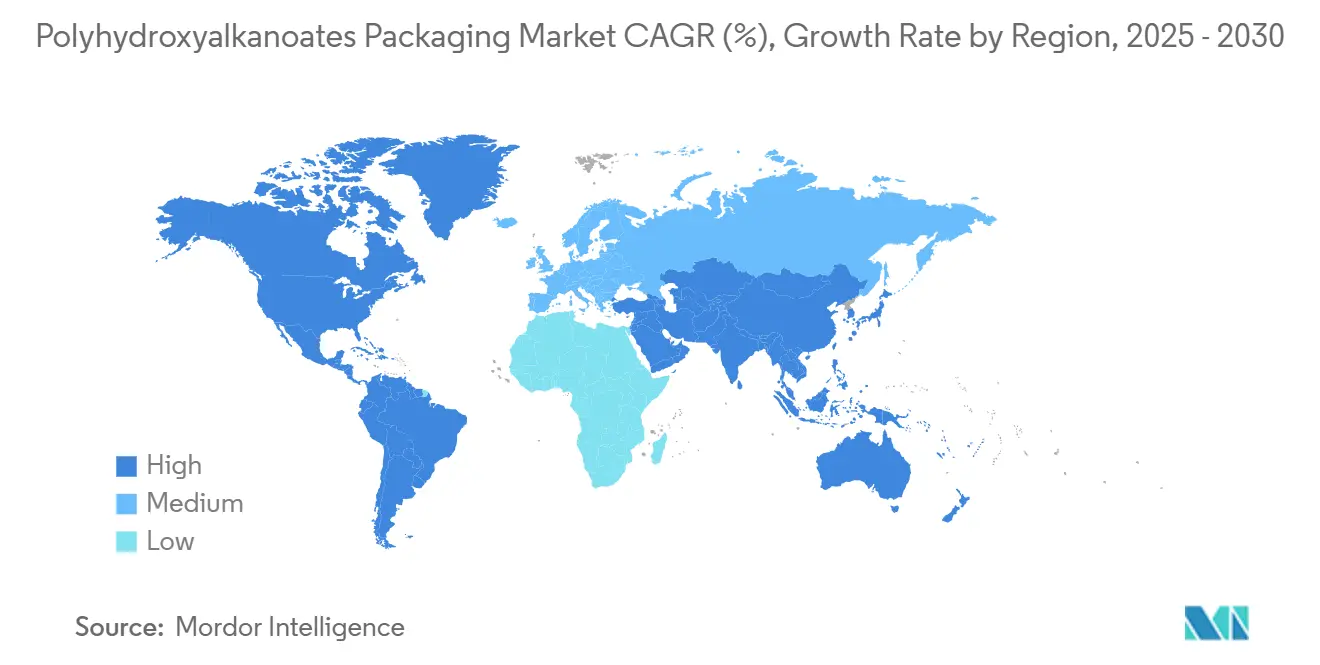

| Fastest Growing Market | South America |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polyhydroxyalkanoates Packaging Market Analysis by Mordor Intelligence

The Polyhydroxyalkanoates (PHA) Packaging Market size is estimated at 24.52 Thousand tons in 2025, and is expected to reach 68.54 Thousand tons by 2030, at a CAGR of 22.82% during the forecast period (2025-2030). Regulatory bans on single-use plastics, large-scale cost breakthroughs from third-generation feedstocks, and brand owners’ sustainability commitments are combining to accelerate demand. Europe’s regulatory push, South America’s feedstock advantage, and rapid innovations in processing are shaping competitive positioning. Rigid applications are consolidating early demand, while high-growth foam and fiber formats signal the next wave of adoption. Producers that scale marine-degradable grades, secure waste-based feedstocks, and lock in brand contracts are positioned to capture a disproportionate share of the expansion.

Key Report Takeaways

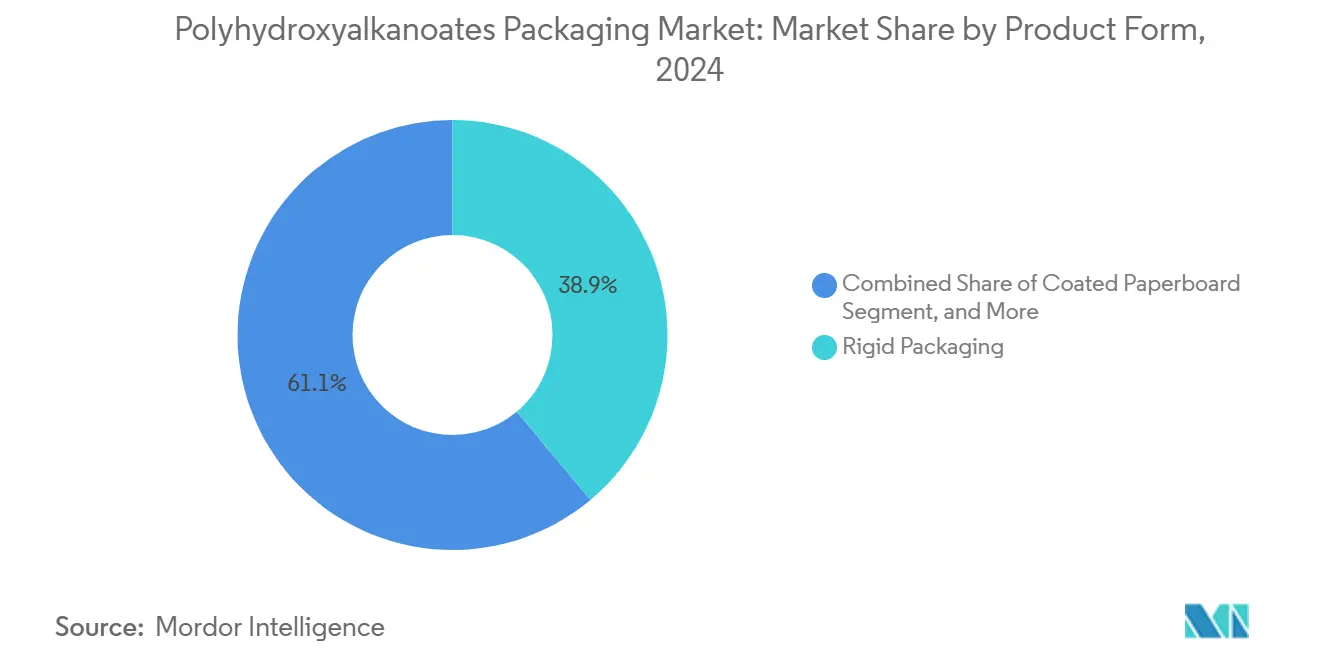

- By product form, rigid packaging captured 38.91% of the PHA packaging market share in 2024.

- By end-use industry, the PHA packaging market size for personal care and cosmetics is forecast to expand at a 23.89% CAGR through 2030.

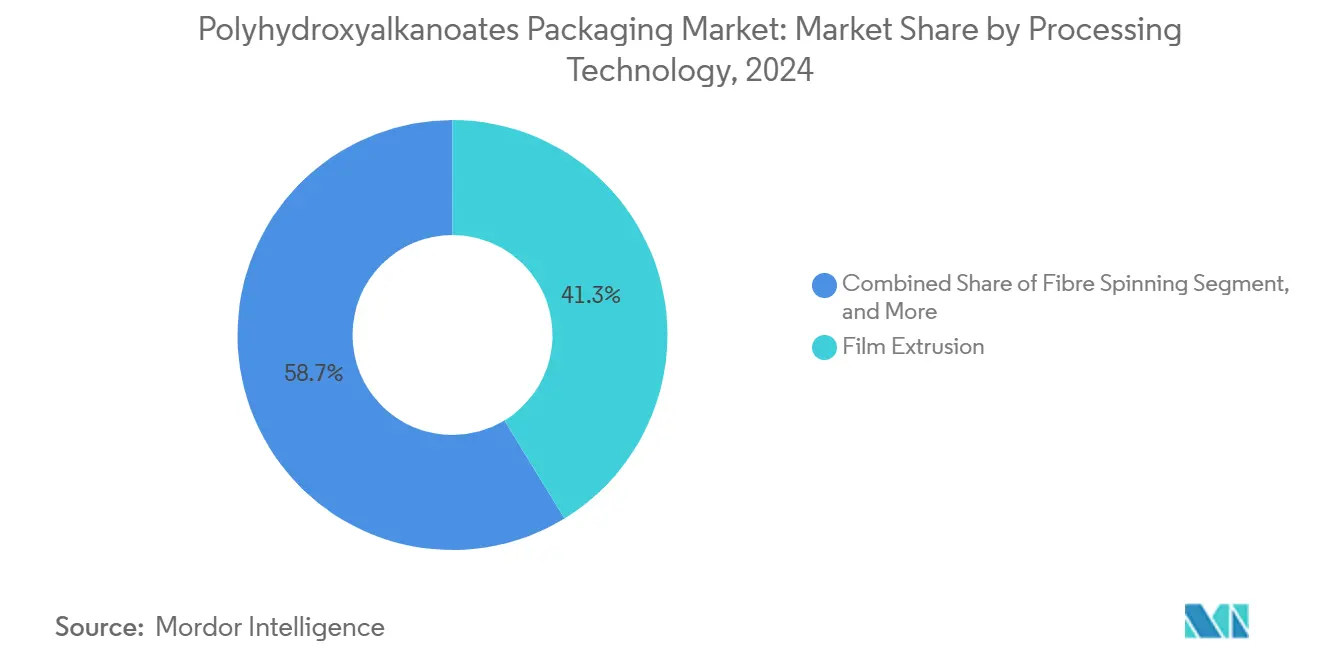

- By processing technology, film extrusion represented 41.29% of the PHA packaging market share in 2024.

- By geography, the PHA packaging market size for South America is projected to record a 24.49% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Polyhydroxyalkanoates Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ban on single-use plastics in OECD markets | +4.2% | Europe and North America expanding to Asia-Pacific | Short term (≤ 2 years) |

| Subsidies for compostable biopolymers in Europe | +3.8% | Core Europe, spillover to United Kingdom and Switzerland | Medium term (2-4 years) |

| Food-grade certifications accelerating brand adoption | +2.9% | Global, early gains in North America and Europe | Medium term (2-4 years) |

| Rapid cost decline from Gen-3 feedstocks | +1.7% | Global, led by Asia-Pacific production hubs | Long term (≥ 4 years) |

| Retailer net-zero packaging mandates | +2.1% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Expansion of decentralised anaerobic digestion capacity | +1.8% | Europe and North America, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ban on Single-Use Plastics in OECD Markets

Legislation in the European Union, Canada, and several U.S. states mandates clear phase-out schedules for conventional items, including straws, cutlery, and takeaway containers. Brand owners are replacing banned formats with PHA grades that meet the ISO 17088 compostability requirements, allowing for global material harmonization. Demand visibility enables producers to justify multi-line fermentation expansions, and international retailers are rolling out the same specifications across developing markets to reduce material complexity.

Subsidies for Compostable Biopolymers in Europe

Fee reductions under Germany’s Packaging Act and extended producer responsibility credits in France lower effective PHA costs by up to 25% when lifecycle compliance fees are included. Additional credits in the Netherlands and Denmark for marine-degradable materials further improve relative economics, incentivizing converters to switch lines ahead of the 2027 review of EU packaging rules.[1]German Environment Agency, “Packaging Act Implementation and Fee Structures,” UBA.DE

Food-Grade Certifications Accelerating Brand Adoption

Recent FDA and EFSA clearances for PHBV and PHBH formulations unlock high-value applications in fresh produce, dairy cups, and beverage films. The 18-month review timeline and multi-million-dollar testing costs favor incumbent suppliers with regulatory capabilities, creating a defensible moat. Harmonized migration testing under EU Regulation 10/2011 shortens European commercialization and underpins cross-regional launches.[2]U.S. Food and Drug Administration, “Food Contact Notifications for PHA Materials,” FDA.GOV

Rapid Cost Decline from Gen-3 Feedstocks

Methane-to-PHA and agricultural-residue pathways lower unit costs by 35-40% versus sugar-based fermentation, while generating tradable carbon credits that widen the advantage. Producers report 20-30% yield gains from synthetic biology enhancements, and scaling demonstrations in the United States and Singapore confirm commercial viability. Accelerated cost parity makes PHA competitive for broader packaging classes, enlarging the addressable pool.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital intensity of PHA fermentation plants | -2.3% | Global, particularly acute in developing markets | Medium term (2-4 years) |

| Limited barrier properties vs. EVOH laminates | -1.9% | Global, focused on food packaging | Long term (≥ 4 years) |

| Supply-chain dependence on cane and corn feedstock volatility | -1.6% | Americas and Asia-Pacific | Short term (≤ 2 years) |

| Fragmented industrial composting infrastructure | -1.4% | Europe and North America core, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Intensity of PHA Fermentation Plants

Commercial plants require USD 150-200 million for fermentation and downstream purification, a figure well above typical converter investments. The specialized equipment base and extended construction cycles limit project finance options for newer entrants. As a result, expansion lags demand, keeping supply tight and reinforcing premium pricing until larger balance sheets commit capital.[3]Danimer Scientific, “Investor Relations and Production Capacity Updates,” DANIMERSCIENTIFIC.COM

Limited Barrier Properties vs. EVOH Laminates

Current PHA oxygen transmission rates are 3-5 times higher than those of EVOH, which restricts its use in extended shelf-life dairy and meat applications. Multilayer structures or barrier coatings add cost and complexity, narrowing PHA’s value proposition. Research into clay nanocomposites is promising, but commercial readiness remains several years out, keeping a portion of the food market inaccessible in the near term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: Cost-effective rigid formats lead while foam scales rapidly

Rigid formats account for 38.91% of the PHA packaging market share in 2024 and continue to anchor early demand given regulatory bans on petroleum clamshells, trays, and hinged lids. The material’s structural strength, moderate barrier performance, and compatibility with existing thermoforming lines ease converter transition costs. Foam formats, enabled by new chemical blowing agents, post the highest 24.59% CAGR as they replace expanded polystyrene in protective transit and takeaway items. Producers targeting this niche are reporting stable order backlogs, and municipal composters highlight PHA foam’s rapid disintegration in aerobic systems, supporting household collection pilots. Flexible films remain the second-largest format, thanks to the polymer’s uniform melt flow and low sealing temperatures, which deliver process energy savings. Paperboard coatings are gaining popularity as mills seek compostable moisture barriers, a trend supported by joint trials between corrugators and biopolymer suppliers.

Progress in coatings and adhesive grades is opening adjacent revenue streams. Specialty suppliers are blending PHA with starch and cellulose to create heat-seal layers for e-commerce mailers that eliminate the need for plastic liners. Rigid format producers are also experimenting with in-mold labels using PHA-based inks to keep mono-material status. Continual improvements in pellet consistency and thermal stability are lowering downtime during changeovers, a key factor for mass-production sites. Collectively, these advances help the PHA packaging market broaden addressable applications while deepening adoption in its early beachheads.

By End-Use Industry: Food service dominates but beauty leads growth

Food service held 34.56% of the PHA packaging market share in 2024 as quick-serve restaurants adopted compostable trays, cutlery, and cup lids ahead of tightening bans. Chain operators report improved consumer sentiment and simplified waste sorting where city composting is available. Beauty and personal care, although smaller, records a 23.89% CAGR as luxury brands leverage marine-degradable credentials to reinforce eco-premium positioning. PHA’s glossy finish and moldability into complex shapes meet branding aesthetics, while low migration rates satisfy sensitive skin claims. Retail grocery is the next frontier as supermarkets test PHA wrap for organic produce, aided by the material’s breathability that reduces condensation.

Pharmaceutical and biomedical packaging remains a niche but high-margin outlet, using PHA capsules and sterile pouches compatible with autoclave conditions. Agriculture applications such as mulch films and seed trays gain traction in regions with organics recycling mandates, linking product lifecycle to soil enrichment. The diverse pull from these industries provides demand resilience and encourages producers to offer grade families tailored to each channel, reinforcing the overall PHA packaging market trajectory.

By Processing Technology: Film extrusion maturity versus fiber spinning acceleration

Film extrusion commands 41.29% of the PHA packaging market size, supported by installed blown-film capacity and straightforward drop-in capability on LDPE lines. Producers cite high output rates, clean edge trims, and lower die build-up compared with PLA. Fiber spinning, however, posts the fastest 24.61% CAGR as luxury goods, apparel, and e-commerce brands test woven PHA wraps and ribbons. The tactile feel, drape, and printable surface appeal to premium unboxing experiences. Injection molding continues to benefit from PHA’s dimensional stability and quick cooling, enabling intricate caps and closures. Blow molding is poised for scalability once higher melt strength grades reach commercial volumes, providing an opportunity for personal care bottles.

Thermoforming stays relevant for salad bowls and deli trays, with converters citing minimal cycle-time adjustments. Multi-technology converters gain margin by funneling a single PHA resin family through extrusion, injection molding, and thermoforming cells, thereby optimizing raw material inventory. As grades diversify, processors are embedding inline compostability markers to simplify sortation, strengthening end-of-life valorization for the PHA packaging market.

Geography Analysis

Europe, with a 32.92% share in 2024, remains the anchor region, supported by the Packaging and Packaging Waste Regulation’s compostable carve-outs and widespread access to industrial composting. Municipal waste audits reveal increasing biopolymer capture rates, and subsidy frameworks are narrowing the price differential with petrochemical plastics. Suppliers are clustering their capacity around feedstock hubs in France, Italy, and the Netherlands to shorten logistics and secure sugar beet and whey waste streams. Brand owners in Germany and Scandinavia are piloting mono-material PHA sleeves for beverage multipacks, reinforcing regional leadership.

South America posts the fastest 24.49% CAGR, driven by Brazil’s tax credits on fermentation equipment imports and abundant sugarcane residue. State development banks offer low-interest loans that lower capital hurdles, attracting joint ventures between domestic agro-processors and multinational packaging converters. Argentina’s expansion of bagasse processing yields low-cost feedstock streams, making Buenos Aires a budding export hub. Regulatory clarity follows the revisions to Brazil’s National Solid Waste Policy, which include compostable targets that align public procurement with biopolymer uptake.

The Asia-Pacific region exhibits balanced dynamics: China scales up its fermentation capacity alongside state-backed methane-to-PHA pilots, while Japan’s electronics sector demands high-purity grades for component packaging. North America benefits from recent FDA clearances and corporate zero-waste pledges, though higher labor costs keep some capacity offshore. The Middle East and Africa remain in the early stages, yet refinery diversification strategies in the Gulf include biopolymer lines, and agricultural economies from Kenya to Egypt are exploring PHA mulch film projects. Collectively, these regional vectors underpin the long-run expansion of the PHA packaging market.

Competitive Landscape

The PHA packaging market is moderately fragmented, comprising a mix of established biotechnology firms and agile newcomers that exploit waste-stream feedstocks. Danimer Scientific and Kaneka Corporation leverage extensive patent estates covering fermentation strains and downstream purification, supporting premium pricing. RWDC Industries, Newlight Technologies, and Mango Materials are developing disruptive pathways for methane and palm waste that sidestep crop-based volatility. Recent capacity announcements signal a shift toward 50,000-tonne modules, striking a balance between scale economies and financing risk.

Strategic partnerships dominate deal activity. Consumer goods leaders sign multi-year offtakes to secure compostable supply ahead of regulation deadlines, while converters seek co-development agreements for application testing. Mergers focus on geographic reach and feedstock access, rather than technology alone, as illustrated by TotalEnergies Corbion’s acquisition of Bluepha’s Chinese assets to anchor its Asia-Pacific exposure. Patent filings in USPTO Class 435 rose 18% year on year, reflecting intensified process optimization battles. Producers differentiate through rapid certification cycles, embedded LCA services, and drop-in resin grades that minimize retooling, reinforcing entry barriers and supporting pricing defensibility.

Despite these moves, capital intensity curbs outright consolidation. Green-field plants require lengthy permitting cycles and specialized microbiological talent, keeping the combined share of the top five players below 35%. This openness leaves room for specialty firms focusing on marine, medical, or textile niches. As brands add portfolio-wide compostable targets, suppliers with matrixed end-market exposure and gen-3 feedstock optionality are poised to gain outsize traction, defining competitive contours of the next five years.

Polyhydroxyalkanoates Packaging Industry Leaders

Danimer Scientific Inc.

CJ Biomaterials Inc.

RWDC Industries Ltd.

Kaneka Corporation

TianAn Biologic Materials Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Danimer Scientific completed a USD 350 million Kentucky expansion that lifts annual PHA output to 75,000 tonnes and embeds agricultural-waste feedstock capability.

- September 2025: RWDC Industries raised USD 150 million in Series C funding to build a 25,000-tonne plant in Singapore using palm oil waste.

- August 2025: Kaneka Corporation obtained FDA clearance for PHBH copolymers in direct food contact, opening U.S. fresh produce and dairy markets.

- July 2025: CJ Biomaterials partnered with Unilever to co-develop PHA packs for premium beauty lines in Europe.

Global Polyhydroxyalkanoates Packaging Market Report Scope

| Rigid Packaging |

| Flexible Films |

| Coated Paperboard |

| Foam |

| Other Product Forms |

| Food Service |

| Food and Beverage Retail |

| Personal Care and Cosmetics |

| Pharmaceutical and Biomedical |

| Industrial and Agriculture |

| Film Extrusion |

| Injection Molding |

| Blow Molding |

| Thermoforming |

| Fibre Spinning |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Form | Rigid Packaging | ||

| Flexible Films | |||

| Coated Paperboard | |||

| Foam | |||

| Other Product Forms | |||

| By End-Use Industry | Food Service | ||

| Food and Beverage Retail | |||

| Personal Care and Cosmetics | |||

| Pharmaceutical and Biomedical | |||

| Industrial and Agriculture | |||

| By Processing Technology | Film Extrusion | ||

| Injection Molding | |||

| Blow Molding | |||

| Thermoforming | |||

| Fibre Spinning | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is driving rapid capacity additions for PHA packaging?

Clear global bans on single-use plastics and generous European subsidies are giving producers long-term demand visibility and attractive economics.

How large will global supply be by 2030?

Installed capacity is forecast to reach 68.54 Thousand tons, more than doubling current output as new plants in North America, South America, and Asia come online.

Which application will outpace the overall market?

Foam packaging is projected to grow at 24.59% CAGR as PHA replaces expanded polystyrene in protective transit and food service items.

Why are beauty brands adopting PHA ahead of other sectors?

Personal care players value marine biodegradability for sustainability messaging and can absorb modest cost premiums in premium price tiers.

What limits wider use in extended shelf-life food packs?

PHA still trails EVOH in oxygen barrier performance, requiring multilayer structures that raise cost and processing complexity.

How fragmented is the supplier base?

Moderate fragmentation persists because high capital intensity slows consolidation, leaving significant room for specialized new entrants.

Page last updated on: