Application Transformation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

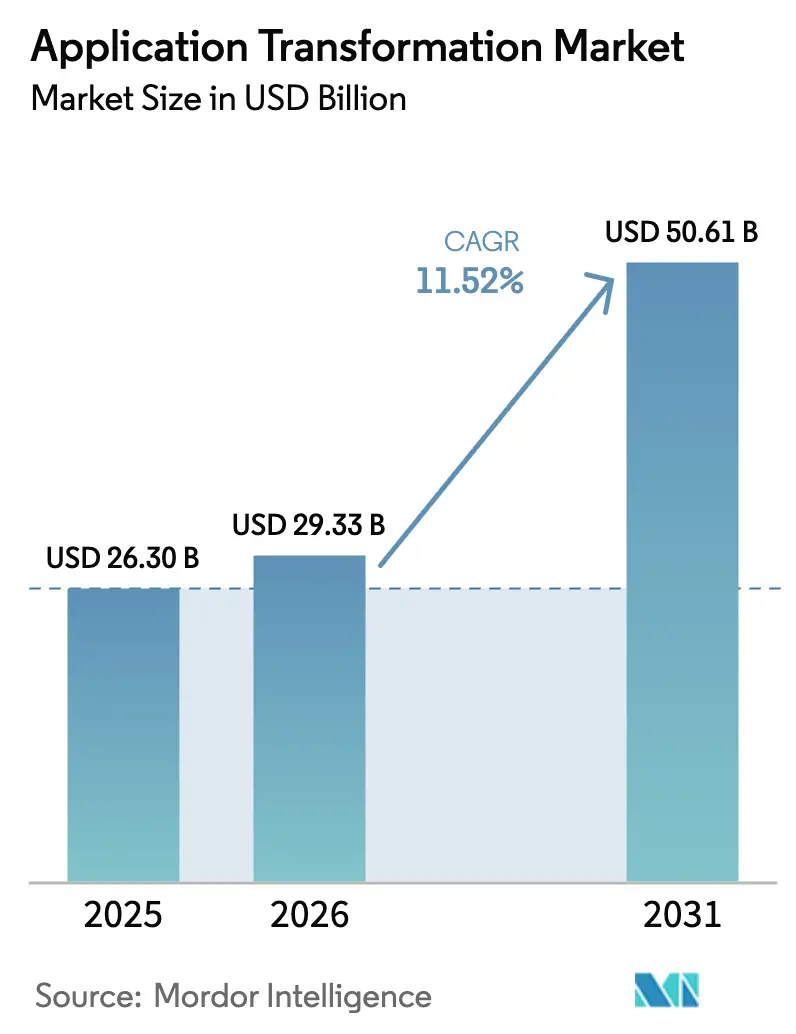

| Market Size (2026) | USD 29.33 Billion |

| Market Size (2031) | USD 50.61 Billion |

| Growth Rate (2026 - 2031) | 11.52% CAGR |

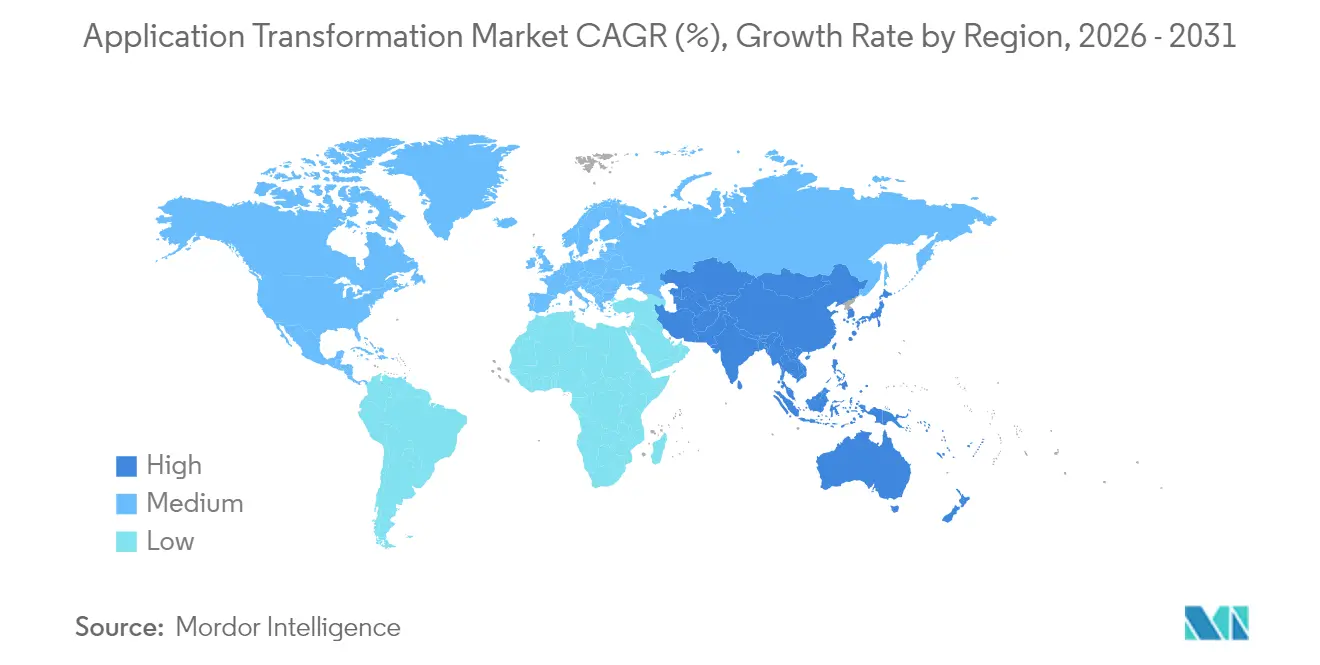

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Application Transformation Market Analysis by Mordor Intelligence

The application transformation market size is expected to grow from USD 26.3 billion in 2025 to USD 29.33 billion in 2026 and is forecast to reach USD 50.61 billion by 2031 at 11.52% CAGR over 2026-2031. The growth results from enterprises retiring legacy infrastructure in favor of cloud-native architectures, which lower operating costs and speed up digital delivery. Standardization around Kubernetes, rapid uptake of AI-assisted code refactoring tools, and vendor-managed outcome pricing shorten transformation timelines and reduce risk. Enterprises also favor hybrid cloud deployment because it strikes a balance between control and scalability, while government programs that fund digital modernization accelerate demand across regulated industries. Competitive intensity increases as global system integrators add AI capabilities to defend share against born-in-cloud specialists.

Key Report Takeaways

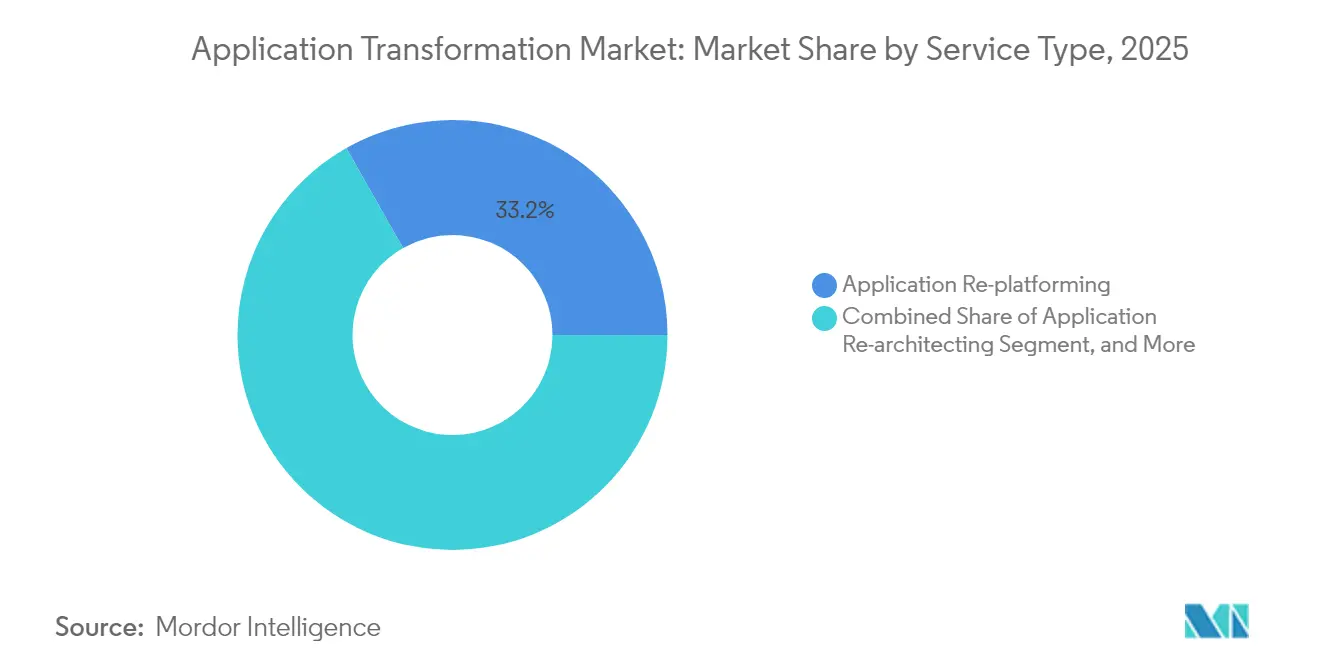

- By service type, application re-platforming captured 33.22% of the application transformation market share in 2025; re-architecting is projected to advance at a 12.42% CAGR through 2031.

- By deployment mode, the hybrid cloud segment held a 41.02% market share in the application transformation market in 2025, also recording the fastest growth rate of 12.85% through 2031.

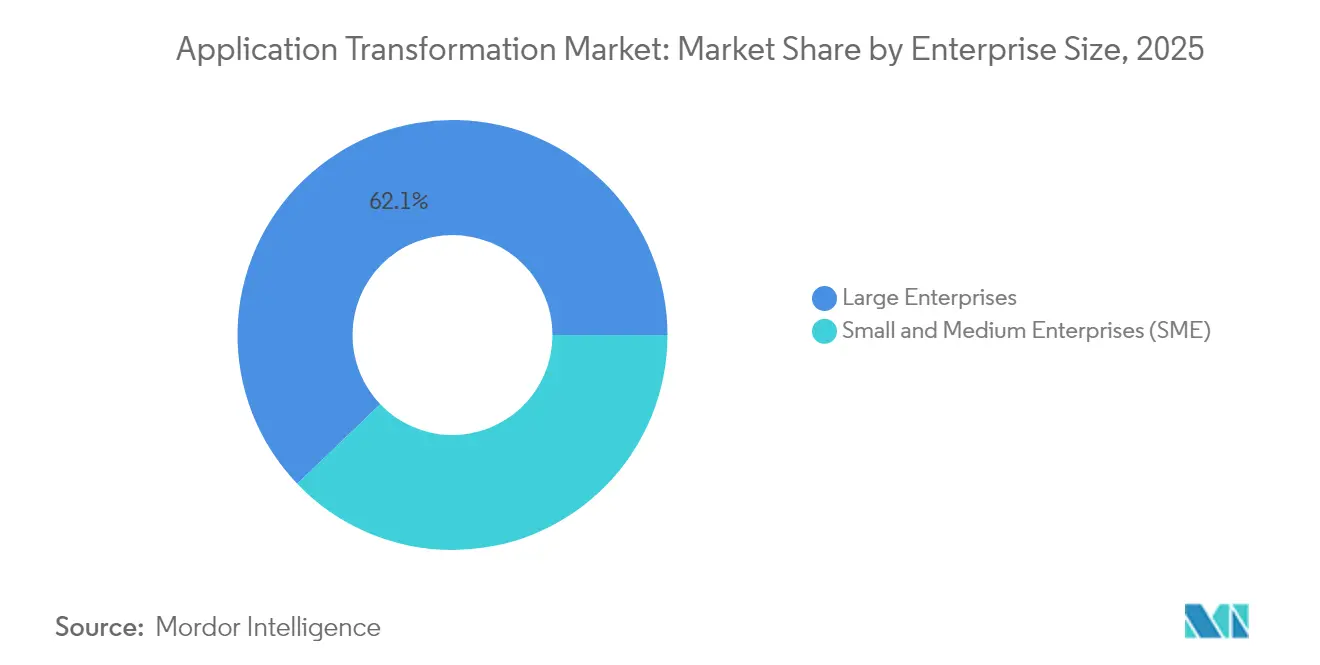

- By enterprise size, large enterprises accounted for 62.15% of the application transformation market size in 2025, while SMEs are projected to grow at a 14.05% CAGR through 2031.

- By industry vertical, BFSI led with a 26.10% share of the application transformation market size in 2025, and healthcare is expected to expand at a 13.76% CAGR through 2031.

- By geography, North America commanded a 37.78% share of the application transformation market in 2025, whereas the Asia-Pacific region is projected to grow at a 14.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Application Transformation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy-Modernization Cost Savings | +2.10% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Cloud-Native Adoption Acceleration | +2.80% | Global, led by Asia-Pacific and North America | Short term (≤ 2 years) |

| Shift-Left Security Mandates | +1.40% | North America and Europe, expanding to APAC | Medium term (2-4 years) |

| Container Orchestration Standardization | +1.90% | Global, with early adoption in North America | Short term (≤ 2 years) |

| AI-Assisted Code Refactoring | +2.30% | North America and Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Vendor-Managed Outcome-Based Pricing | +1.20% | Global, with pilot programs in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy-modernization cost savings

Enterprises continue to prioritize modernization because legacy systems consume as much as 70% of IT budgets for maintenance alone. Mainframe re-platforming can reduce operating costs by up to 50%, while containerized deployment increases resource utilization from 15% to nearly 70%. Global banks validate the benefits; JPMorgan Chase reported USD 2 billion in annual technology savings after systematically modernizing thousands of workloads.[1]JPMorgan Chase & Co., “Annual Report 2024,” JPMorgan Chase, jpmorganchase.com Predictable subscription pricing further stimulates initiatives by converting capital outlays into manageable operating expenses.

Cloud-native adoption acceleration

Enterprises shift to cloud-native architectures because microservices, serverless, and API-first design shorten release cycles and reduce system-wide failure risk. In 2024, the Cloud Native Computing Foundation found that Kubernetes adoption reached 96% among companies already running containers. Organizations deploying microservices report 50% faster time-to-market for new features and 75% fewer deployment incidents.[2]Google Cloud Architecture Center, “Cloud Architecture Framework,” Google Cloud, cloud.google.com The economic payoff of continuous delivery compels boards to fund aggressive modernization roadmaps.

Container orchestration standardization

Kubernetes has become the de facto runtime target for both legacy and greenfield applications, eliminating provider lock-in and enabling uniform DevOps tooling.[3]Red Hat Analysts, “State of Kubernetes Security Report 2024,” Red Hat, redhat.com Enterprises cite a 40% reduction in infrastructure management overhead and a 60% increase in deployment consistency once legacy applications are containerized. A rich ecosystem of plug-ins for policy, networking, and observability now rivals traditional app-server stacks, allowing risk-averse sectors to migrate critical workloads.

AI-assisted code refactoring

Large language model–powered tools automatically discover dependencies, generate modernization roadmaps, and write new unit tests. GitHub Copilot shows 55% productivity gains in code generation tasks, while IBM watsonx Code Assistant reduces analysis time by 60% on mainframe workloads.[4]GitHub Research Group, “Quantifying GitHub Copilot Impact on Developer Productivity,” GitHub Blog, github.blog These gains convert multiyear rewrites into quarterly goals, making business cases far easier to approve.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technical Debt Visibility Gaps | -1.80% | Global, particularly acute in North America and Europe | Short term (≤ 2 years) |

| Migration-Induced Downtime Risk | -2.10% | Global, with higher impact in regulated industries | Medium term (2-4 years) |

| Mainframe Skill Shortages | -1.30% | North America and Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Cloud Cost Inflation | -1.60% | Global, with concentration in mature cloud markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Technical debt visibility gaps

Seventy-three percent of enterprises are unable to quantify technical debt, which complicates scoping and budgeting.[5]SonarSource Team, “2024 State of Software Quality Report,” SonarSource, sonarsource.com Hidden dependencies and outdated documentation inflate transformation timelines, erode executive confidence, and often force mid-project replanning. Reverse-engineering tools help, but the wide heterogeneity of technology still limits automation coverage.

Migration-induced downtime risk

Mission-critical systems remain online around the clock, leaving tiny migration windows. Financial services platforms, for example, tolerate near-zero outages because every minute of downtime jeopardizes revenue and compliance. Blue-green and canary release strategies mitigate the threat, yet require sophisticated orchestration and mature DevOps skills that many firms still lack.[6]Microsoft Azure Writers, “Azure Architecture Documentation,” Microsoft, docs.microsoft.com Boards thus insist on incremental pilots before funding wider programs, slowing full-portfolio modernization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Re-architecting Gains Momentum Despite Re-platforming Dominance

Application re-platforming held a 33.22% application transformation market share in 2025 and generated USD 8.74 billion of revenue, validating its appeal as a fast, lift-and-shift path to the cloud. Re-architecting, however, is projected to expand at a 12.42% CAGR to 2031 as enterprises seek long-term agility through microservices, event streaming, and domain-driven design. Walmart migrated 95% of its commerce stack with minimal code change in an early phase, then moved to re-architecting to unlock further scalability.

The shift occurs because re-platforming alone cannot meet evolving latency, compliance, and resilience expectations. Containers, service meshes, and serverless runtimes encourage deeper rewrites that decompose monoliths into loosely coupled domains. Enterprises prioritizing security also prefer re-architecting since it embeds granular identity control and zero-trust patterns. Consulting partners thus market phased journeys that start with re-platforming for quick ROI and transition to re-architecting for sustained competitiveness.

By Deployment Mode: Hybrid Cloud Sustains Leadership Through Risk Mitigation

Hybrid cloud accounted for 41.02% of the application transformation market share in 2025 and is also forecast to lead growth at 12.85% CAGR, contributing more than USD 22 billion to the application transformation market size by 2031. Enterprises keep sensitive data on-premises or in private clouds to satisfy data-residency laws while exploiting public cloud elasticity for burst workloads. Financial institutions in Canada route regulated customer data to in-country zones but run analytics in multiregion public clouds.

Hybrid architectures lower egress fees by processing data where it is generated and reduce vendor lock-in. Edge computing nodes inside factories or retail branches further reinforce hybrid footprints by adding near-device analytics. Reported savings average 35% when workloads are optimally placed between environments. Cloud providers now ship integrated portals, billing, and policy engines that present single-pane-of-glass governance, making hybrid the strategic end state rather than an interim step.

By Enterprise Size: SME Acceleration Challenges Large-Enterprise Dominance

Large enterprises generated 62.15% of revenue in 2025 because they manage extensive application estates and allocate multi-year budgets. They pursue rationalization waves that retire low-value portfolios first and redirect savings to cloud-native rebuilds. Yet SMEs exhibit the quickest 14.05% CAGR thanks to managed low-code platforms that remove infrastructure barriers.

SMEs often rebuild outright instead of migrating, since smaller footprints allow for greenfield development. Industry-specific SaaS accelerators provide composable building blocks, letting mid-market players launch digital products faster than larger rivals. This democratization of tooling intensifies competition for talent but also opens partner-ecosystem opportunities for system integrators.

By Industry Vertical: Healthcare Disrupts BFSI Leadership Through Regulatory Modernization

BFSI held 26.10% of the application transformation market size in 2025, fueled by instant-payment rails, open-banking mandates, and anti-money-laundering analytics. Core banking rewrites cost USD 12 billion annually at leading banks like Bank of America. Healthcare, however, is expected to outpace all verticals at 13.76% CAGR through 2031 as regulations such as the 21st Century Cures Act require interoperable electronic health records.

FHIR-compliant APIs, telemedicine scalability, and AI-supported clinical trials motivate hospitals to modernize on cloud-native data platforms. Vendors embed audit trails and role-based security to satisfy HIPAA, while life-science firms refactor legacy lab systems to speed molecule discovery. These dynamics elevate healthcare from laggard to pacesetter, putting pressure on legacy EHR vendors to release modular, open architectures.

Geography Analysis

North America led the revenue in 2025 due to its advanced cloud infrastructure, extensive partner ecosystems, and supportive regulations that strike a balance between innovation and privacy safeguards. Federal agency mandates such as the ongoing Cloud Smart strategy create stable demand as public bodies retire COBOL and mainframe applications. Venture-backed startups also force incumbents to modernize, keeping the region at the forefront.

The Asia-Pacific region is projected to post the fastest growth rate of 14.35% CAGR, primarily driven by government stimulus, 5G rollouts, and the increasing expectations of digital-native consumers. Singapore’s Smart Nation program, Japan’s Society 5.0 agenda, and India’s Digital Public Infrastructure drive large multicloud migrations. Domestic hyperscalers in China and South Korea offer sovereign options that align with data-localization rules, further accelerating adoption.

Europe is showing steady growth, underpinned by the GDPR and the Digital Markets Act, which compel companies to modernize their identity, consent, and cross-border data workflows. Energy-efficient data center mandates boost container optimization projects, while post-Brexit realignment forces financial institutions to re-platform their operations to separate EU and U.K. operations. German automotive suppliers also modernize predictive-maintenance apps to meet Industry 4.0 goals.

Competitive Landscape

The market is moderately fragmented. Accenture, IBM, and Cognizant leverage global delivery and sector expertise to retain enterprise accounts, yet face rising competition from cloud-native boutiques and AI tool vendors. Accenture integrates Udacity’s training assets to close DevSecOps skill gaps and differentiate on workforce transformation. IBM pushes watsonx Code Assistant to automate COBOL modernization and secure mainframe migrations.

AWS, Microsoft, and Google embed orchestration hubs into their clouds to capture services pull-through revenue. Application migration factories delivered as managed services appeal to clients who prefer outcome-based contracts over time-and-materials models. Smaller firms specialize in niche domains, such as POS modernization or SAP S/4HANA transformation, allowing them to win deals that global integrators often overlook.

AI-driven refactoring, contract commitments tied to business KPIs, and pre-built compliance accelerators are the primary weapons for differentiation. Providers that own both IP and delivery talent achieve higher margins and client stickiness, signaling an industry shift toward platform-enabled services rather than pure labor arbitrage.

Application Transformation Industry Leaders

Accenture plc

International Business Machines Corporation

Cognizant Technology Solutions Corporation

Infosys Limited

Tata Consultancy Services Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Microsoft released Azure Modernization Center, folding GitHub Copilot enterprise plugins into a unified workflow that auto-documents legacy code and recommends refactor patterns. The move aligns AI tooling with Azure consumption goals.

- November 2024: AWS debuted Application Migration Hub Orchestrator with dependency mapping and automated rollback to minimize downtime in multi-app cutovers. The launch strengthens AWS professional services upsell potential.

- October 2024: IBM rolled out watsonx Code Assistant for Enterprise Apps, claiming 60% faster code analysis in early pilots. The product reinforces IBM’s hybrid-cloud consulting moat.

- September 2024: Accenture purchased Udacity’s enterprise unit for USD 400 million to scale micro-credential programs that accelerate client DevOps maturity. The deal plugs a talent-enablement gap in end-to-end transformations.

Global Application Transformation Market Report Scope

| Application Re-platforming |

| Application Re-hosting |

| Application Re-architecting |

| Application Re-engineering |

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Large Enterprises |

| Small and Medium Enterprises (SME) |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Retail and E-Commerce |

| Manufacturing |

| Government and Public Sector |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Application Re-platforming | ||

| Application Re-hosting | |||

| Application Re-architecting | |||

| Application Re-engineering | |||

| By Deployment Mode | Public Cloud | ||

| Private Cloud | |||

| Hybrid Cloud | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises (SME) | |||

| By Industry Vertical | Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | |||

| Retail and E-Commerce | |||

| Manufacturing | |||

| Government and Public Sector | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the application transformation market in 2026?

It totals USD 29.33 billion in 2026 and is forecast to reach USD 50.61 billion by 2031.

Which region grows fastest through 2031?

Asia-Pacific posts a 14.35% CAGR due to government digital programs and rapid cloud adoption.

Which deployment model holds the largest share?

Hybrid cloud leads with 41.02% share and also shows the fastest 12.85% CAGR.

Why is healthcare modernization accelerating?

Regulations such as the 21st Century Cures Act mandate interoperable records, pushing a 13.76% CAGR.

What restrains transformation projects most?

Migration-induced downtime risk and unclear technical debt remain the top hurdles.

Who are the leading service providers?

Accenture, IBM, Cognizant, AWS, Microsoft, and Google dominate through integrated service portfolios.

Page last updated on: