Marketing Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

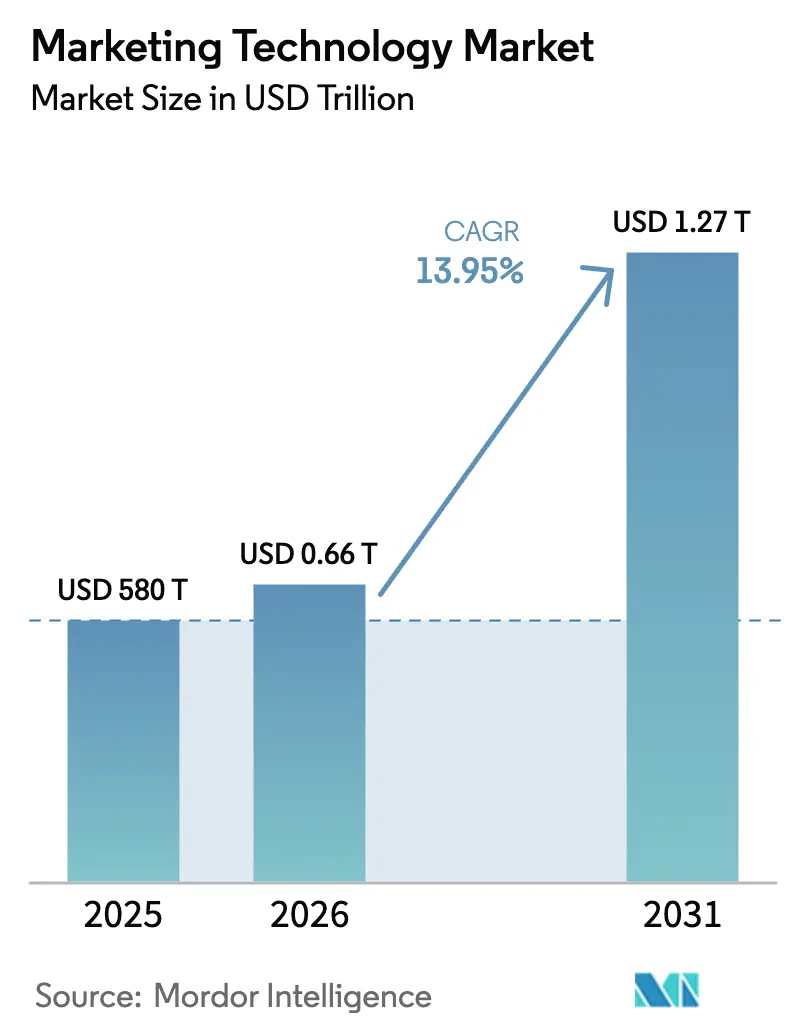

| Market Size (2026) | USD 0.66 Trillion |

| Market Size (2031) | USD 1.27 Trillion |

| Growth Rate (2026 - 2031) | 13.95% CAGR |

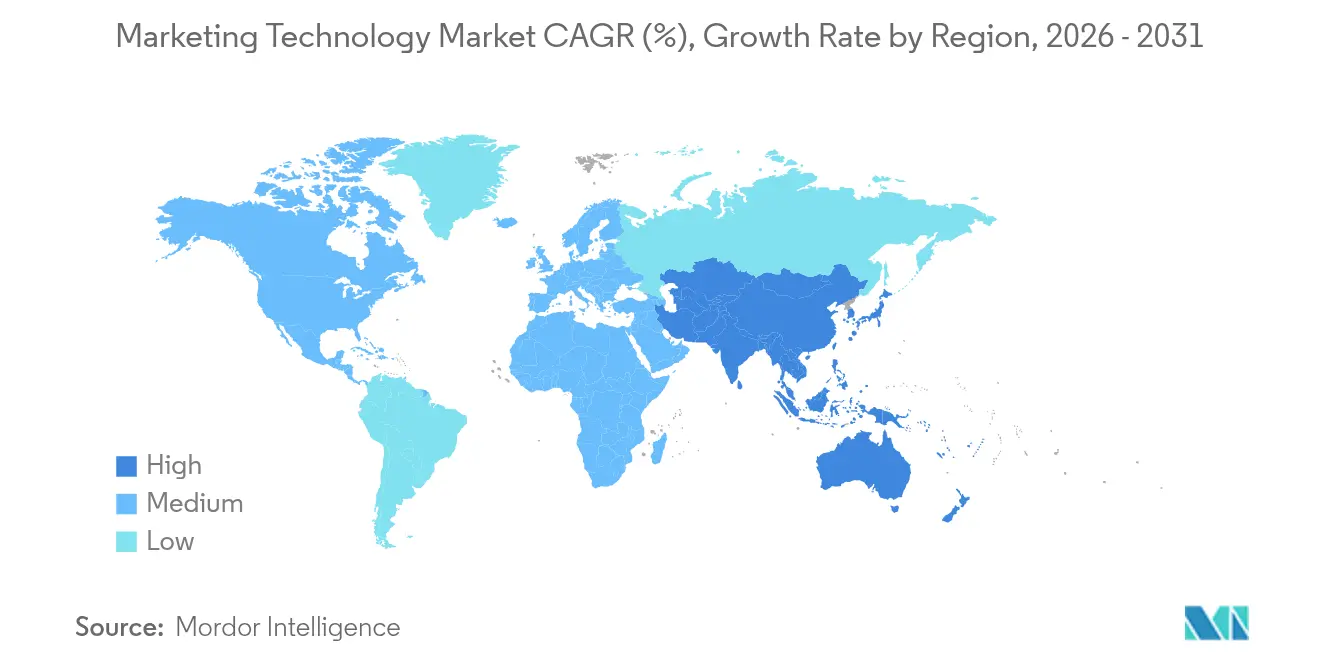

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Marketing Technology Market Analysis by Mordor Intelligence

The Marketing Technology Market size was valued at USD 580 billion in 2025 and estimated to grow from USD 660.91 billion in 2026 to reach USD 1,270.82 billion by 2031, at a CAGR of 13.95% during the forecast period (2026-2031).

Enterprise demand for cloud-first, AI-embedded stacks is the primary accelerator, enabling real-time orchestration of campaigns, dynamic content generation, and cross-channel attribution at scale. Market leaders are embedding generative AI in core products, while regulatory pressure to transition toward privacy-first data strategies raises the value of first-party and zero-party data assets. Competitive dynamics favor vendors that can unify creative, data, and activation workflows inside a composable architecture, giving enterprises granular control over costs, latency, and compliance. Operational efficiency gains from automated content pipelines are already improving campaign ROI enough to offset rising AI compute expenditures.

Key Report Takeaways

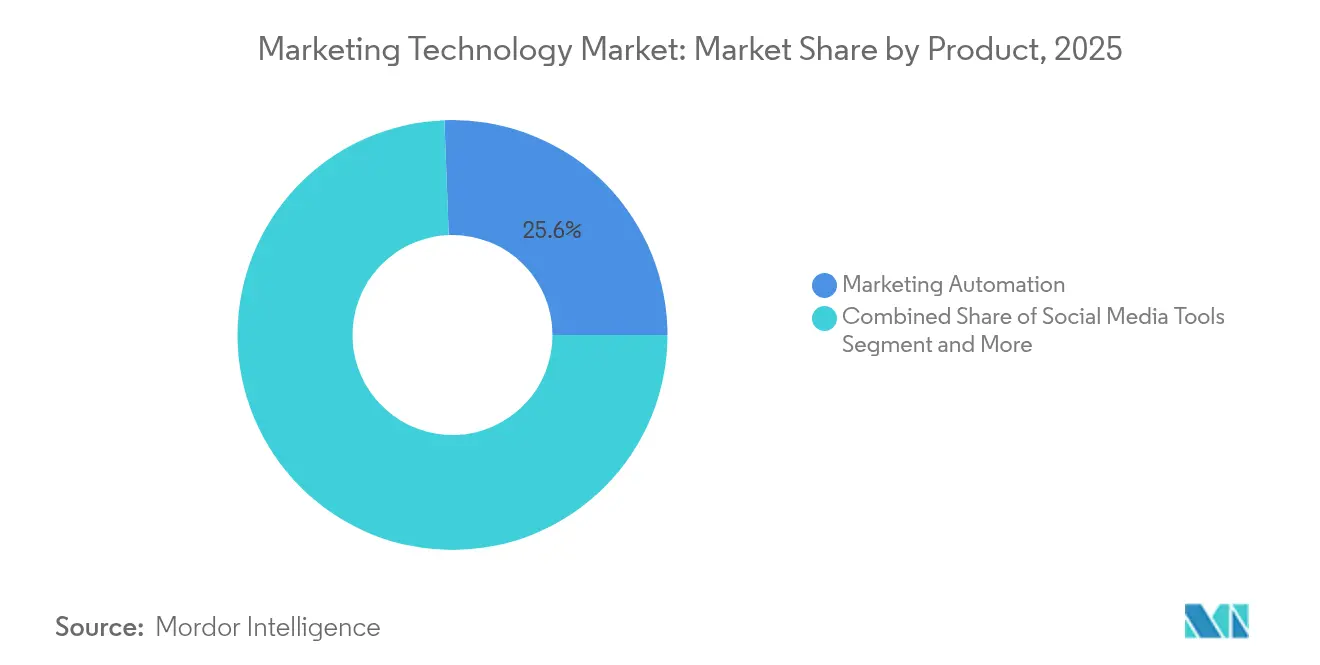

- By product category, Marketing Automation led with 25.60% of the marketing technology market share in 2025, while GenAI-Powered Content Tools are projected to expand at a 25.92% CAGR through 2031.

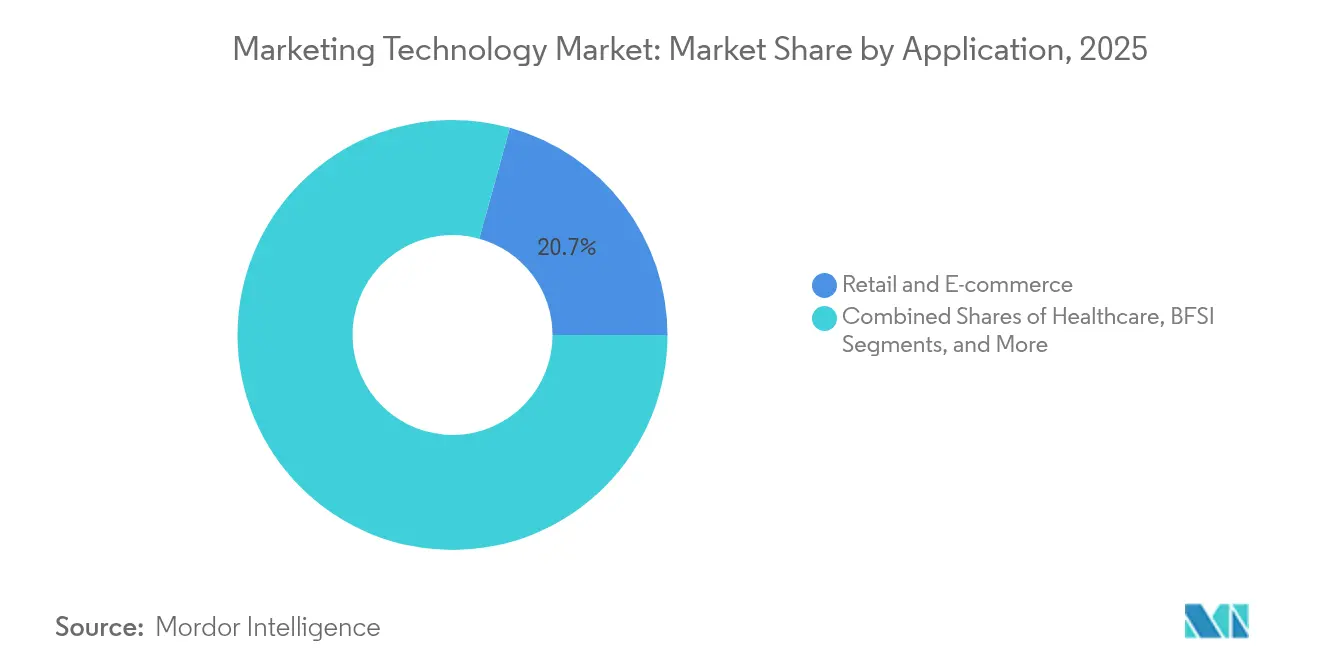

- By application, Retail and E-commerce held 20.70% revenue share of the marketing technology market in 2025; Healthcare is advancing at an 18.10% CAGR over 2026-2031.

- By geography, North America commanded 37.60% share of the marketing technology market in 2025, whereas APAC is set to post the fastest 15.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Marketing Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first marketing stacks adoption surge | 4.20% | Global with APAC leadership | Medium term (2-4 years) |

| GenAI embedded across campaign orchestration | 3.80% | North America and EU early adopters | Short term (≤ 2 years) |

| Privacy-driven first-party data strategies | 2.10% | EU catalyst, global expansion | Long term (≥ 4 years) |

| Zero-party data micro-exchange programs | 1.40% | North America and APAC pilots | Long term (≥ 4 years) |

| Composable CDP architectures beating suite lock-in | 1.80% | Global enterprise tier | Medium term (2-4 years) |

| Operational efficiency gains offset AI compute outlays | 1.00% | Global cost-conscious adopters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cloud-First Marketing Stacks Adoption Surge

Enterprises continue an aggressive pivot toward cloud-native architectures to collapse data silos and enable real-time decisioning across every customer touchpoint. Microsoft’s USD 1.3 billion Mexico and USD 2.7 billion Brazil data-center commitments underscore the need for regional infrastructure that supports low-latency customer data processing.[1]Microsoft, “Mexico and Brazil Data-Center Investments,” microsoft.com IT teams report cycle-time reductions that let marketers shrink campaign rollouts from weeks to hours, boosting personalization accuracy and revenue velocity.

GenAI Embedded Across Campaign Orchestration

Generative AI is transforming what used to be manual, reactive workflows into proactive experience orchestration engines. Adobe’s Customer Experience Orchestration platform illustrates how AI unites creative and marketing functions under one roof, enabling continuous content optimization without relying on labor-intensive A/B testing. Enterprises highlight margin expansion as proprietary models deliver 50-60% gross margins versus legacy SaaS tools.

Privacy-Driven First-Party Data Strategies

GDPR 2025 enhancements force brands to prioritize first-party relationships over third-party cookies. Google’s updated consent framework now requires explicit opt-ins to sustain measurement fidelity, pushing marketers to invest in robust customer data platforms designed for compliance.[2]Google, “Updated Consent Mode for EEA,” google.com Firms that pivot early are capturing higher customer lifetime value as data quality improves trust-based personalization.

Zero-Party Data Micro-Exchange Programs

Leading brands are experimenting with micro-value exchanges in which customers willingly share preferences in return for tailored offers. Early adopters report 40% improvements in relevance scores and 25% jumps in retention when zero-party data fuels marketing automation. Gamified preference centers and progressive profiling are fast becoming standard features of modern engagement hubs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising total cost of ownership and integration debt | -2.80% | Global enterprise tier | Short term (≤ 2 years) |

| Skills gap for complex martech stacks | -1.90% | North America and EU acute | Medium term (2-4 years) |

| Regulatory compliance complexity | -1.50% | EU influence, global scope | Medium term (2-4 years) |

| Escalating AI compute and storage expenses | -1.20% | Global hyperscaler regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Total Cost of Ownership and Integration Debt

Organizations layering AI tools onto legacy stacks face unplanned data-migration and maintenance bills that exceed initial budgets by 40-60%. Cloud storage alone surpassed USD 200 billion of IT spend in 2025, pressuring CFOs to reassess platform choices.

Skills Gap for Complex Martech Stacks

Eighty-seven percent of marketers fear technology displacement, yet 63% of leaders cite insufficient technical talent to run AI-heavy stacks effectively. This shortage inflates implementation timelines and compels vendors to ship low-code modules to accelerate value realization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Marketing Automation Retains the Lion’s Share

Marketing Automation captured 25.60% of the marketing technology market share in 2025, validating its role as the control center for omnichannel journey management. The marketing technology market size tied to Marketing Automation is projected to grow alongside enterprises’ pivot to unified orchestration engines that connect data, content, and activation workflows. GenAI-Powered Content Tools, while representing a smaller revenue base today, are forecast to post a 25.92% CAGR through 2031 as brands redistribute spend toward scalable, AI-driven content generation. Social media and content marketing suites post steady gains by enabling direct audience engagement, whereas rich-media creation tools benefit from rising video demand.

Enterprises view content velocity as a durable moat, directing budgets toward platforms that marry creative excellence with real-time performance insights. Adobe’s GenStudio Foundation exemplifies how vendors integrate automation into the content supply chain, allowing marketers to publish without sacrificing brand integrity. Sales-enablement suites now embed predictive lead scoring that draws on AI-trained historical win data to accelerate pipeline conversion.

By Application: Healthcare Emerges as the Growth Leader

Retail and E-commerce held 20.70% of the marketing technology market in 2025, reflecting its historic leadership in digital engagement sophistication. The segment retains healthy growth as omnichannel brands double down on hyper-personalized promotions. Yet Healthcare is set to outpace every other vertical at an 18.10% CAGR between 2026-2031, pushing the marketing technology market size for patient engagement platforms sharply upward. Telehealth expansion and HIPAA-compliant automation are the main catalysts, enabling providers to match consumer-grade experience standards.

Healthcare organizations apply marketing automation beyond patient acquisition to drive adherence and outcome-focused communication. Kaiser Permanente’s community-centric campaigns showcase how purpose-driven marketing builds trust while delivering measurable health benefits. BFSI, IT and Telecom, and Media and Entertainment also step up investment to personalize services, manage churn, and maximize lifetime value.

Geography Analysis

North America controlled 37.60% of the marketing technology market in 2025 due to mature cloud adoption, venture funding, and advanced AI research capabilities. Regional leaders leverage deep ecosystem integrations to maintain competitive edge, even as state-level privacy statutes multiply compliance tasks. Canadian enterprises refine consent strategies in anticipation of Bill C-27, while US-based firms deploy privacy-preserving analytics to stay ahead of litigation exposure.

APAC is the fastest-growing region, projected to log a 15.95% CAGR over 2026-2031. Governments support digital infrastructure build-outs, enabling widespread uptake of marketing tech among mobile-first consumers. India expects its digital marketing sector to reach INR 1.12 lakh crore (USD 13.4 billion) by 2025, powered by local-language content and AI-enabled ad-targeting innovations. Southeast Asian advertisers are directing larger shares of media spend toward social commerce, and Australian enterprises are expanding AI marketing budgets to capture incremental conversion gains.

Europe’s outlook is colored by stringent regulations: GDPR 2025, the Digital Markets Act, and the Digital Services Act collectively redefine data stewardship obligations. Vendors serving the region must design default-privacy architectures that comply across all 27 member states, often rolling those standards global. In Latin America, Mexico welcomed both Netflix’s USD 1 billion production pledge and Alibaba’s first local cloud region, signals that international players foresee robust digital growth. Meanwhile, Middle East and Africa developers accelerate e-commerce stack adoption as payment rails mature and cross-border logistics improve.

Competitive Landscape

The market shows moderate concentration around full-suite incumbents Adobe, Salesforce, and Microsoft, which bundle creative, data, and activation layers into cohesive clouds. Salesforce’s USD 8 billion takeover of Informatica boosts its unified profile capability, aiming to cut data-latency bottlenecks in large enterprises. Adobe capitalizes on Creative Cloud synergies to cross-sell AI-enhanced marketing modules, while Microsoft activates Azure-based AI services to deepen engagement across Dynamics 365.

Competitive differentiation now pivots on AI maturity, latency, and trust. Meta’s multimodal patent filings point to smart assistant roadmaps that could radically reduce friction in customer interactions. Specialized vendors exploit composable architecture momentum, carving profitable niches around privacy-preserving analytics and sector-specific workflows such as HIPAA-aligned patient engagement.

Price pressure mounts as buyers benchmark the total cost of ownership across full-suite and best-of-breed alternatives. Vendors respond with usage-based billing and low-code accelerators to ease implementation. The rise of no-code orchestration appeals to mid-market firms starved for technical talent, while open APIs allow in-house teams to extend platform functions without incurring integration debt.

Marketing Technology Industry Leaders

Amazon Inc.

Acoustic L.P.

Active Campaign

Adobe Inc

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Salesforce closed its USD 8 billion acquisition of Informatica, creating a unified data and AI foundation for enterprise marketing.

- March 2025: Adobe launched Customer Experience Orchestration, integrating generative AI for real-time content adaptation across all channels.

- February 2025: Microsoft announced a USD 2.7 billion Brazil data-center expansion to support AI-driven marketing workloads.

- January 2025: HubSpot rolled out an AI-first marketing automation suite with predictive analytics and generative content features.

Global Marketing Technology Market Report Scope

Marketing technology, also known as MarTech, defines a range of tools and software that assist in achieving marketing objectives or goals. When a marketing group utilizes a grouping of marketing technologies, this is known as its marketing technology stack. MarTech has evolved into a staple in digital marketing campaigns and can also be used to optimize marketing measures across any marketing channel.

The marketing technology market is segmented by product (social media tools, content marketing tools, rich media tools, automation tools, data and analytics tools, sales enablement tools), by application (IT and telecommunication, retail, and e-commerce, healthcare, media and entertainment, sports and events, BFSI), by geography (North America, Europe, Asia Pacific, Latin America, Middle East, and Africa).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Social Media Tools |

| Content Marketing Tools |

| Rich-Media Creation Tools |

| Marketing Automation Platforms |

| Data and Analytics Tools |

| Sales Enablement Tools |

| IT and Telecommunications |

| Retail and E-commerce |

| Healthcare |

| Media and Entertainment |

| Sports and Events |

| BFSI |

| North America |

| South America |

| Europe |

| Asia-Pacific |

| Middle East |

| Africa |

| By Product | Social Media Tools |

| Content Marketing Tools | |

| Rich-Media Creation Tools | |

| Marketing Automation Platforms | |

| Data and Analytics Tools | |

| Sales Enablement Tools | |

| By Application | IT and Telecommunications |

| Retail and E-commerce | |

| Healthcare | |

| Media and Entertainment | |

| Sports and Events | |

| BFSI | |

| By Geography | North America |

| South America | |

| Europe | |

| Asia-Pacific | |

| Middle East | |

| Africa |

Key Questions Answered in the Report

How big is the Marketing Technology Market?

The Marketing Technology Market size is expected to reach USD 0.66 trillion in 2026 and grow at a CAGR of 13.95% to reach USD 1.27 trillion by 2031.

What is the current size of the marketing technology market?

The market was valued at USD 660.91 billion in 2026.

How fast is the marketing technology market expected to grow?

It is forecast to register a 13.95% CAGR, reaching USD 1,270.82 billion by 2031.

Which product segment holds the largest market share?

Marketing Automation platforms led with 25.60% share in 2025.

Which application area is growing the fastest?

Digital infrastructure build-outs, rising mobile-first consumer bases, and supportive government policies are pushing APAC to a 15.95% CAGR.

What is the main restraint hindering market growth?

Rising total cost of ownership and integration debt is reducing expected ROI for enterprises deploying complex AI-driven stacks.

Page last updated on: