India Digital Transformation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

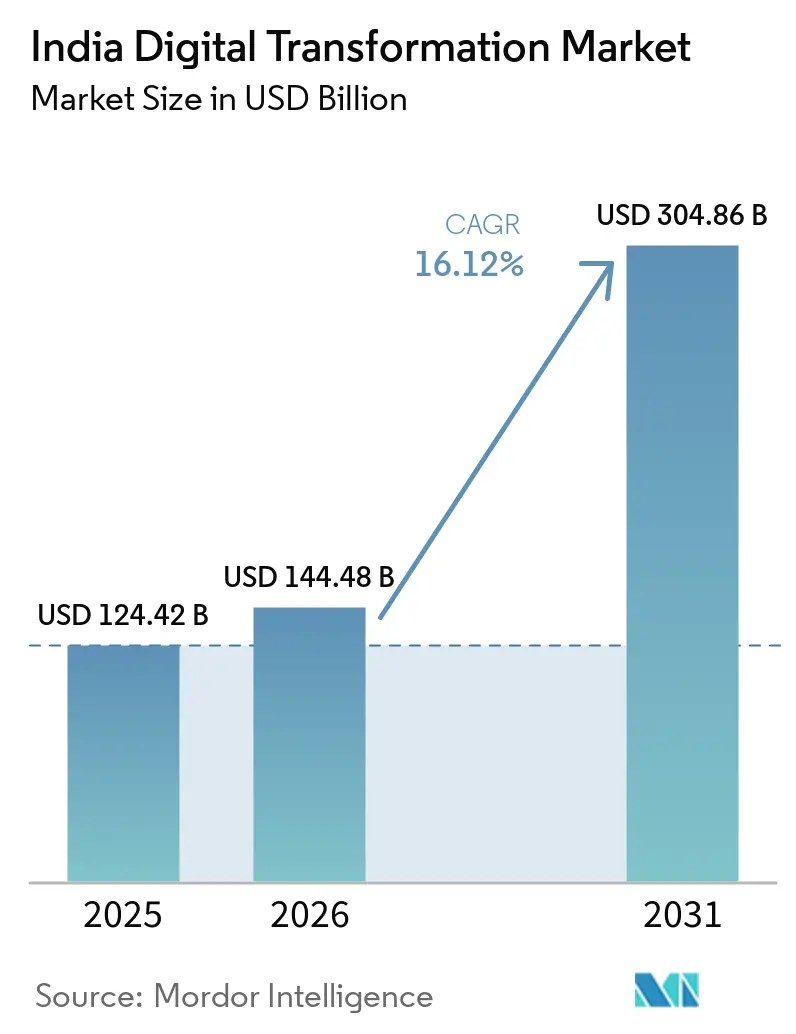

| Base Year Market Size (2025) | USD 124.42 Billion |

| Market Size (2026) | USD 144.48 Billion |

| Market Size (2031) | USD 304.86 Billion |

| Growth Rate (2026 - 2031) | 16.12% CAGR |

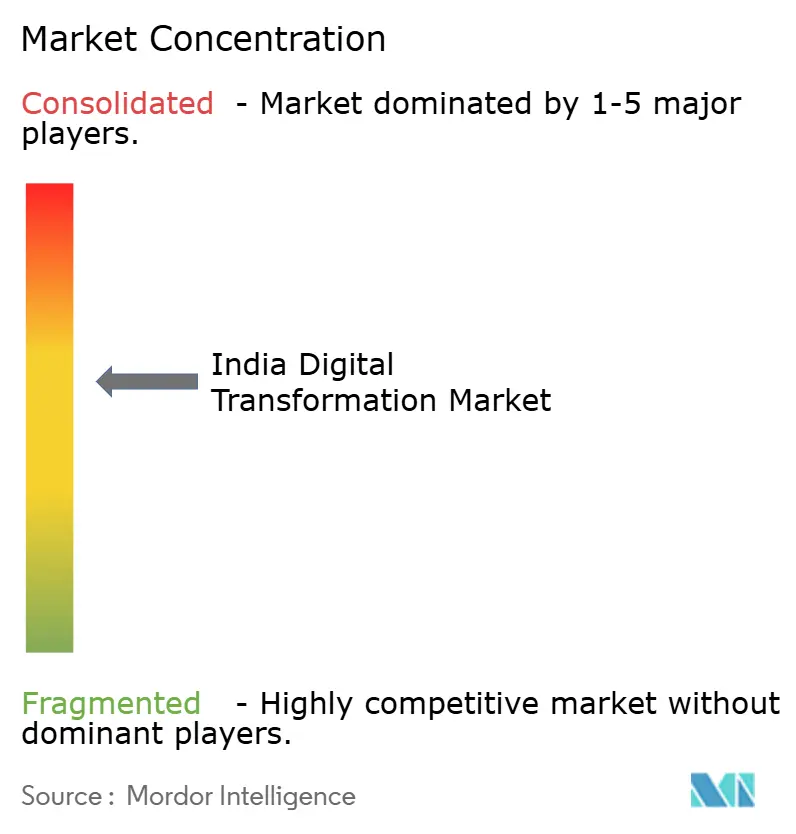

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Digital Transformation Market Analysis by Mordor Intelligence

India Digital Transformation Market size in 2026 is estimated at USD 144.48 billion, growing from 2025 value of USD 124.42 billion with 2031 projections showing USD 304.86 billion, growing at 16.12% CAGR over 2026-2031. Critical momentum originates from the government’s Digital India programme, robust cloud-edge infrastructure build-outs, and rising enterprise AI adoption. Enterprises accelerate spending on generative AI, cybersecurity, and private 5G networks to drive operational efficiency, customer experience, and regulatory compliance. Hyperscalers expand domestic datacenter footprints to satisfy data-localization rules, while local IT services providers compete on industry-specific solutions and outcome-based contracts. Growing smartphone penetration in tier-2 and tier-3 cities extends digital services to new consumer cohorts, creating fertile ground for fintech, health-tech, and edu-tech platforms. Structural headwinds include escalating cyber-attack risks, an acute digital-skills gap, and power-grid instability in rural locations that restrain edge deployments.

Key Report Takeaways

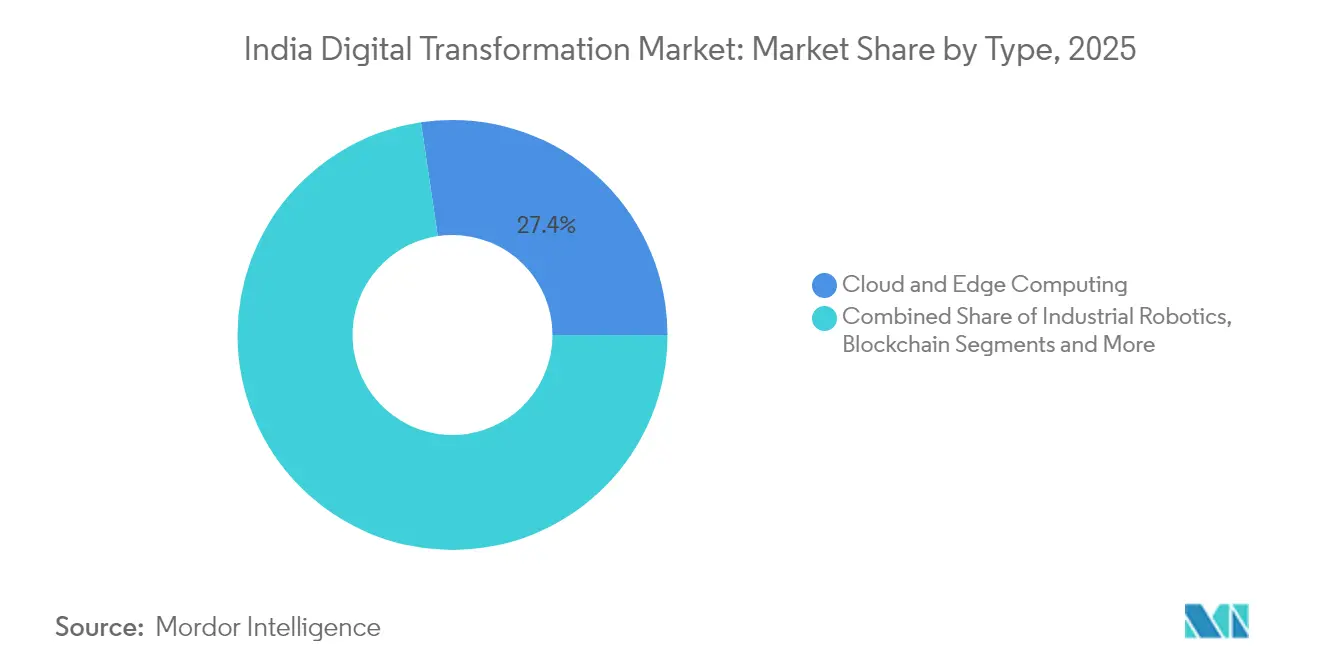

- By technology type, Cloud & Edge Computing led with 27.35% of the India digital transformation market share in 2025; Generative AI within Analytics is projected to post the fastest 23.25% CAGR through 2031.

- By component, the Services segment commanded 53.05% share of the India digital transformation market size in 2025 and is projected to expand at a 20.15% CAGR to 2031.

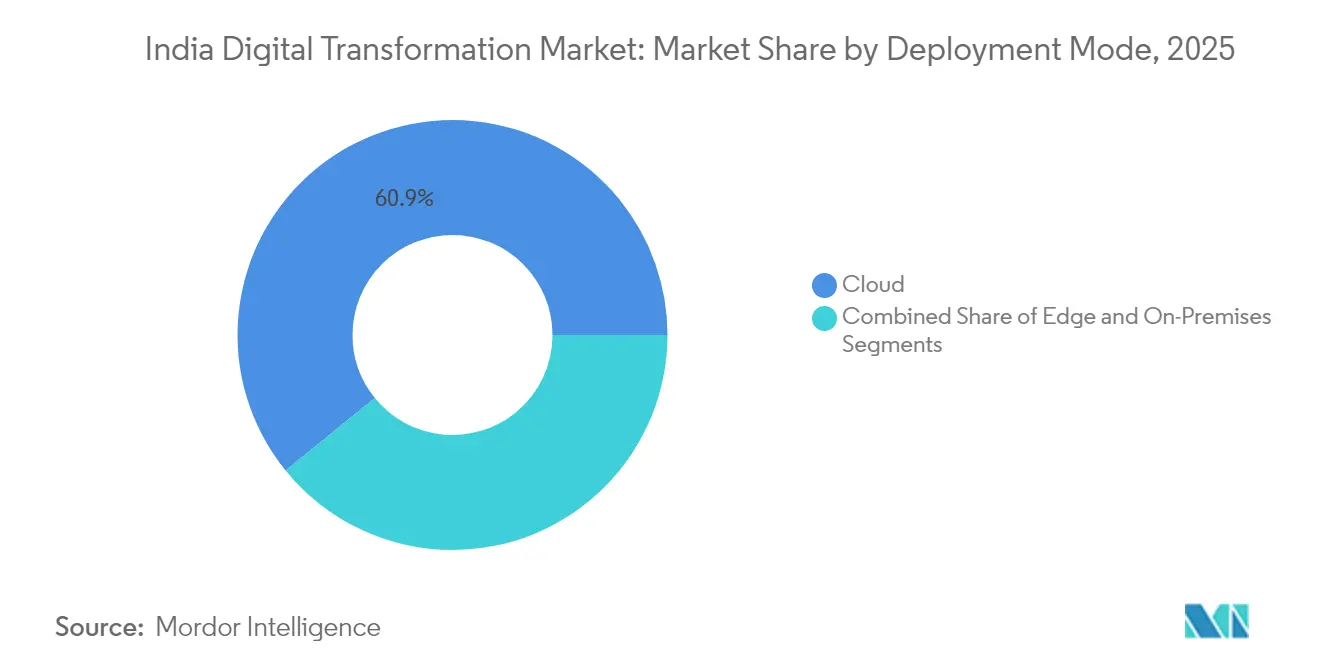

- By deployment mode, Cloud solutions captured 60.85% revenue share in 2025, while Edge computing is forecast to grow at a 27.1% CAGR through 2031.

- By organization size, Large Enterprises accounted for 68.15% of 2025 spending; Small & Mid-Sized Enterprises (SMEs) record the highest projected CAGR at 21.1% through 2031.

- By end-user industry, BFSI held the largest 18.05% revenue share in 2025, whereas Healthcare is set to grow the quickest at a 18.45% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

The contribution of India is incorporated into a multi-country and multi-region total that reflects the full breadth of industry. The digital transformation (dx) market size by Mordor Intelligence expresses that combined magnitude.

India Digital Transformation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-led Digital India and India Stack momentum | +3.2% | Nationwide; early gains in Maharashtra, Telangana, Karnataka | Medium term (2–4 years) |

| Rapid growth in mobile-internet and smartphone adoption | +2.8% | Nationwide; fastest uptake in tier-2/3 cities | Short term (≤2 years) |

| Enterprise push for cloud, AI, and efficiency gains | +2.5% | Nationwide; strongest in BFSI and manufacturing hubs | Medium term (2–4 years) |

| Large-scale 5G and broadband capital outlays | +2.1% | Urban centers and industrial corridors across India | Long term (≥4 years) |

| Build-out of hyperscale GPU datacenters and IndiaAI clusters | +1.8% | Maharashtra, Telangana, Gujarat, Karnataka | Long term (≥4 years) |

| GST 2.0 e-invoicing mandate covering 6 million+ SMEs | +1.6% | Nationwide; immediate effect on manufacturing and services | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Government-led Digital India and India Stack momentum

The central government extended Digital India funding to INR 14,903 crore through FY 2026, channeling resources toward digital public infrastructure, reskilling 625,000 IT professionals, and training 265,000 information-security specialists.[1]Press Information Bureau of India, “Union Cabinet approves expansion of the Digital India programme with an outlay of ₹ 14,903 crore,” pib.gov.in India Stack layers, such as Aadhaar, UPI, and DigiLocker, standardize identity, payments, and data exchange, lowering integration costs for enterprises rolling out at a population scale. The Unified Payments Interface processed 38 billion transactions valued at INR 71.95 trillion in 2021, demonstrating transaction-layer maturity. State governments replicate platform thinking; Andhra Pradesh delivers 161 public services via “Mana Mitra” WhatsApp governance, widening last-mile reach. The Digital Personal Data Protection Rules 2025 introduce clear consent and data-fiduciary obligations, cementing regulatory certainty for private-sector investment, Press Information Bureau of India.

Rapid growth in mobile-internet and smartphone adoption

India added 120 million 4G subscribers between 2023 and 2025 as affordable handsets and aggressive data tariffs bridged the connectivity gap.[2]Telecom Talk, “Indian Government Plans USD 4 Billion Investment to Connect Every Village with Broadband,” telecomtalk.info With monthly average data consumption per user exceeding 19 GB in 2025, digital content, OTT video, and mobile gaming ecosystems flourish, propelling demand for cloud delivery networks and fintech micro-services. Smartphone penetration surpasses 73%, catalyzing inclusive digital-payment adoption in tier-3 towns and rural areas. E-commerce, ride-hailing, and food-delivery platforms leverage the expanding addressable base, while telcos monetize higher data-consumption tiers through bundled content and device financing. The positive spill-over benefits the India digital transformation market as enterprises redesign customer journeys for mobile-first engagement.

Enterprise push for cloud, AI, and efficiency gains

Indian enterprises are projected to direct USD 160 billion of IT spending toward cloud, AI, and cybersecurity in FY 2025, up 11.2% year on year.[3]ETCFO Editorial, “Indian Enterprises to Spend USD 160 Billion on Cloud, AI and Cybersecurity in FY25,” etcfo.com Cloud migration unlocks on-demand scalability; 87% of surveyed firms have reached “Enthusiast” or “Expert” AI-maturity stages, particularly in manufacturing and telecom. Partnerships such as Bharti Airtel with Google Cloud target 2,000 large enterprises and 1 million emerging businesses to accelerate public-cloud adoption. Generative AI is estimated to add USD 200 billion of productivity gains by 2030 as BFSI automates fraud detection and healthcare deploys AI-assisted diagnostics. The resulting OPEX savings and data-driven decision-making propel incremental investment across the India digital transformation market.

Large-scale 5G and broadband capital outlays

Private 5G deployments commenced in 2024, with Airtel enabling Bosch’s smart-factory operations for real-time quality inspection and predictive maintenance.[4]GSMA, “Private 5G for Smart Manufacturing in India,” gsma.com Operators earmark over INR 2 lakh crore for 5G coverage in industrial corridors and urban clusters through 2027. Fixed-wireless access trials extend high-speed broadband to semi-urban households where fiber rollout remains cost-prohibitive. The Bharat 6G Initiative allocates INR 10,000 crore to next-generation research, signaling policy continuity beyond the current technology cycle. Enhanced connectivity underpins edge-computing use cases, opening fresh revenue pools for cloud, analytics, and automation vendors within the India digital transformation market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mounting data-privacy worries and rising cyber-attacks | −2.1% | Nationwide, most acute in BFSI and healthcare hubs | Short term (≤2 years) |

| Persistent shortage of digital-ready talent | −1.8% | Country-wide, especially tier-2/3 cities and rural areas | Medium term (2–4 years) |

| Fragmented legacy IT systems across public bodies | −1.5% | All India, pronounced in government departments and PSUs | Long term (≥4 years) |

| Unreliable power supply in smaller cities | −0.8% | Tier-3/4 cities and rural communities across regions | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Escalating data-privacy & cyber-attack risks

India recorded more than 1.5 million cyber incidents in 2025, with projected losses of INR 20,000 crore to fraud, ransomware, and phishing scams. Banks reported 2,500 targeted attacks in H2 2024 alone, prompting a 30% rise in cybersecurity budgets across BFSI and healthcare. The government raised its national cybersecurity allocation to INR 1,900 crore for FY 2025, yet the attack surface expands as enterprises adopt multicloud and edge architectures. Brand-impersonation scams inflicted INR 9,000 crore losses in 2024, eroding consumer trust in digital channels. Heightened risk perception slows digital rollouts in sensitive sectors, tempering near-term growth for the India digital transformation market.

Acute digital-skills shortage

NASSCOM estimates a requirement for 2.2 million cloud professionals by 2025, but supply gaps persist, especially in AI, cybersecurity, and industrial IoT domains. Only 18% of SMEs are aware of government digitization support schemes, signaling knowledge-transfer deficiencies that curb technology uptake. Reskilling programs under Digital India address 625,000 IT workers, yet industry growth outpaces talent production. Corporations launch proprietary academies—Microsoft’s ADVANTA(I)GE INDIA plans to train 2 million individuals in AI skills—to bridge the deficit, though meaningful impact remains medium term. The talent crunch pressures wage costs and delays project timelines, restraining the India digital transformation market’s full-potential CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Generative AI redefines analytics ecosystems

Cloud & Edge Computing contributed 27.35% of the India digital transformation market share in 2025, reflecting large-scale workload migration and sovereign-cloud adoption for regulated industries. Generative-AI-driven analytics posts a 23.25% CAGR, as language models automate customer service chatbots, code generation, and business-intelligence narrative insights. The India digital transformation market size for AI-centric analytics is forecast to surpass USD 29.3 billion by 2031, underpinned by hyperscaler GPU clusters in Maharashtra and Telangana. Industrial robotics gains traction in automotive facilities, where Hyundai integrated 2,000 smart robots, cutting maintenance downtime by 5%. IoT sensors over private 5G enable real-time asset monitoring, while extended-reality tools facilitate remote training for shop-floor workers. Blockchain adoption remains niche, focused on supply-chain traceability, whereas additive manufacturing scales in aerospace prototyping. Cybersecurity tools increasingly embed AI to counter advanced persistent threats, rounding out a converged technology stack.

New market entrants differentiate through domain-specific AI models, low-code IoT platforms, and pay-per-use robotic-as-a-service offerings. Pricing flexibility and outcome-based contracts resonate with mid-market manufacturers seeking rapid ROI. Synergies among these technologies compound business value, reinforcing India’s position as a global testbed for integrated digital-transformation solutions.

By Component: Services catalyze implementation excellence

Services represented 53.05% of the India digital transformation market size in 2025 and are positioned to grow at a 20.15% CAGR to 2031 as enterprises seek consulting, integration, and managed-service expertise. Large transformation programs span multicloud strategy, cybersecurity hardening, and composable ERP modernization, requiring cross-functional advisory capabilities. Solutions (software and platforms) account for the balance, with verticalized applications gaining traction in manufacturing execution systems, tele-health, and regulatory reporting for BFSI.

India’s established IT-services ecosystem, led by TCS, Infosys, and Wipro, deepens alliances with hyperscalers to co-develop industry accelerators. Accenture’s acquisition of TalentSprint augments its LearnVantage platform, fostering AI and data-engineering talent pipelines. Managed-services demand surges as Bharti Airtel’s Pune center supports more than 2,000 enterprises on multicloud governance. Outcome-linked contracts tie vendor remuneration to KPIs such as process-scrap reduction and customer-churn minimization, shifting risk to providers yet increasing long-term wallet share.

By Deployment Mode: Edge computing powers time-critical workloads

Cloud deployment retained a 60.85% hold in 2025, buoyed by trust in ISO 27001-certified facilities and data-localization compliance frameworks. Edge computing, however, registers the fastest 27.1% CAGR, driven by latency-sensitive use cases in digital transformation in manufacturing, autonomous warehouses, and tele-surgery. The India digital transformation market size for edge solutions is slated to exceed USD 15.4 billion by 2031 as 500-MW green datacenters come online in Hyderabad and Navi Mumbai.

Hybrid architectures prevail, combining central cloud orchestration with on-premise micro-datacenters to satisfy data-sovereignty regulations. Telcos bundle private 5G, MEC (multi-access edge compute), and device-management services, offering one-stop solutions for factories. On-premise deployments persist in BFSI and defense segments that store classified data, though containerization reduces hardware lock-in. The converged approach balances performance, compliance, and cost, expanding total addressable value for vendors across the India digital transformation market.

By Organization Size: SMEs unlock digital-credit channels

Large Enterprises captured 68.15% of 2025 revenue, driven by holistic modernization programs spanning supply-chain digitization, customer-experience revamps, and AI-enabled decision-support. SMEs, however, record a 21.1% CAGR through 2031 as digital lending platforms reduce financing friction. The Open Credit Enablement Network (OCEN) uses cash-flow-based underwriting to improve credit access, catalyzing technology investment among micro-enterprises. Government schemes such as Udyam Registration and MSME Champions provide technology subsidies, yet awareness remains low, spotlighting outreach opportunities.

Cloud-first subscription models resonate with SMEs lacking CAPEX budgets for on-premise infrastructure. E-commerce channels extend market reach; the sector could jump to USD 350 billion by 2030, supported by integrated logistics and digital payments. The democratization of advanced tools widens the India digital transformation market, simultaneously easing urban-rural economic disparities.

By End-User Industry: Healthcare outpaces traditional leaders

BFSI maintained an 18.05% lead in 2025, propelled by 38 billion annual UPI transactions and stringent Reserve Bank of India compliance mandates. Healthcare posts the fastest 18.45% CAGR, fueled by Ayushman Bharat Digital Mission’s creation of 500 million health IDs and linked 300 million electronic records. Voice-AI deployments at Apollo Hospitals delivered a 46% productivity lift for physicians and 21× ROI, validating digital-health economics. Manufacturing uptake accelerates through Industry 4.0; RPG Group doubled digital spending in 2023 and logged scrap-rate declines. Transportation & Logistics relies on IoT telematics for route optimization, while retail leverages computer-vision analytics for real-time shelf monitoring. Government departments adopt chat-based citizen-service platforms, demonstrating scalability of low-code automation. Cross-industry synergies reinforce adoption curves, anchoring sustained growth for the India digital transformation market.

Geography Analysis

North India benefits from proximity to national policy-making and hosts multiple smart-city projects integrating e-governance, surveillance analytics, and intelligent traffic management. The Delhi–NCR corridor houses a dense cluster of IT and cybersecurity firms that collaborate with ministries on cloud-migration roadmaps. Educational institutions in Uttar Pradesh launch AI curricula, supplying talent to emergent analytics startups. Public-sector undertakings digitize procurement and payroll systems, expanding addressable flows for platform vendors.

South India stands as the primary digital-transformation powerhouse. Telangana attracted INR 1.78 lakh crore (USD 21.3 billion) at Davos 2025, earmarked for green datacenters, semiconductor packaging, and AI research. Karnataka’s Bengaluru tech ecosystem anchors over 3,500 deep-tech startups and advanced R&D centers. Tamil Nadu funnels incentives through its Electronics Components Manufacturing Scheme, luring global chip assemblers. Andhra Pradesh’s Quantum Valley Tech Park hosts India’s largest quantum computer via an IBM–TCS consortium, evidencing frontier-tech aspirations. The talent concentration, venture-capital inflows, and policy clarity coalesce to keep South India at the epicenter of the India digital transformation market.

West India leverages Maharashtra’s USD 1 trillion economic target and Gujarat’s capital-expenditure spree. Maharashtra pioneers India’s first 1.5-GW green datacenter parks worth USD 20 billion and announces the country’s inaugural AI university. Gujarat hosts Reliance’s 3-GW AI-datacenter and Micron’s USD 2.75 billion semiconductor plant, reinforcing supply-chain localization. These investments deepen industrial automation, fintech innovation, and R&D, solidifying the region as a manufacturing and services hub within the India digital transformation market.

East & North-East India prioritize digital-inclusion initiatives. Government broadband spend of USD 4 billion extends fiber and fixed-wireless connectivity to underserved districts. Startups in Kolkata and Guwahati pilot agritech IoT platforms that optimize yield forecasts. Renewable-powered edge nodes address grid instability, enabling low-latency e-health and ed-tech services. Although the spend base remains smaller, high growth potential positions the region as the next frontier.

Mordor Intelligence provides coverage of the digital transformation (dx) market across other key regional markets, including North America, Africa, and Middle East, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to Indonesia, Thailand, Canada, Nigeria, Oman, and Colombia incorporating local coverage and market participation, as required.

Competitive Landscape

The India digital transformation market is moderately fragmented, with global hyperscalers, domestic IT-services giants, telecom operators, and niche SaaS vendors jostling for wallet share. Microsoft’s USD 3 billion commitment amplifies cloud-GPU capacity, placing pressure on AWS and Google Cloud to accelerate local availability zones. Tata Communications partners with CoRover.ai to launch sovereign-AI chatbots tailored for Hindi and regional languages, differentiating on compliance and cultural nuance. Infosys and Adobe co-develop data-driven marketing platforms, targeting consumer-products firms eager for hyper-personalization.

Telecom operators monetize 5G infrastructure through enterprise campus networks, bundling edge compute and security services. System integrators invest in low-code accelerators and domain-specific reference architectures to shorten time-to-value. Startups exploit white spaces in AI-powered agri-advisory, tele-radiology, and supply-chain visibility, often collaborating with incumbents for distribution. Consolidation trends emerge as Capgemini eyes WNS Holdings and SoftBank scouts mid-tier IT-BPO targets, signaling valuation upticks. Vendor success hinges on partner ecosystems, IP ownership, and the ability to translate pilots into production at national scale.

India Digital Transformation Industry Leaders

Tata Consultancy Services

Infosys

Wipro

Tech Mahindra

Accenture

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Infosys and Adobe announce strategic collaboration to enhance AI-led marketing transformation using Infosys Aster and Adobe Experience Cloud.

- June 2025: SoftBank begins evaluating USD 1 billion acquisitions of Indian IT-BPO firms such as AGS Health and WNS Global.

- May 2025: IBM and TCS deploy India’s largest quantum computer at Quantum Valley Tech Park, Amaravati.

- May 2025: Microsoft and Yotta partner to accelerate AI adoption using expanded cloud infrastructure.

India Digital Transformation Market Report Scope

Digital transformation is the process of incorporating digital technologies such as artificial intelligence and machine learning, extended reality (VR & AR) for industrial applications, IoT, industrial robotics, blockchain, digital twins, 3D printing/ additive manufacturing, industrial cyber security, wireless connectivity, edge computing, smart mobility, and others across various end-user industries.

India digital transformation market is segmented by type (analytics, artificial intelligence, and machine learning extended reality (XR), IoT, industrial robotics, blockchain, additive manufacturing/3D printing, cybersecurity, cloud and edge, computing, and others (digital twin, mobility, and connectivity), by end-users (manufacturing, oil, gas, and utilities, retail & e-commerce, transportation, and logistics, healthcare, BFSI, telecom, and IT, government and public sector, Others (education, media & entertainment, environment, etc). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| Analytics, AI and ML |

| Extended Reality (XR) |

| Internet of Things (IoT) |

| Industrial Robotics |

| Blockchain |

| Cloud and Edge Computing |

| Others (Digital Twin, Mobility and Connectivity) |

| Solutions |

| Services |

| Cloud |

| Edge |

| On-Premises |

| Large Enterprises |

| Small and Mid-Sized Enterprises |

| Manufacturing |

| Oil, Gas and Utilities |

| Retail and E-commerce |

| Transportation and Logistics |

| Healthcare |

| BFSI |

| Telecom and IT |

| Government and Public Sector |

| Others |

| By Type | Analytics, AI and ML |

| Extended Reality (XR) | |

| Internet of Things (IoT) | |

| Industrial Robotics | |

| Blockchain | |

| Cloud and Edge Computing | |

| Others (Digital Twin, Mobility and Connectivity) | |

| By Component | Solutions |

| Services | |

| By Deployment Mode | Cloud |

| Edge | |

| On-Premises | |

| By Organisation Size | Large Enterprises |

| Small and Mid-Sized Enterprises | |

| By End-User Industry | Manufacturing |

| Oil, Gas and Utilities | |

| Retail and E-commerce | |

| Transportation and Logistics | |

| Healthcare | |

| BFSI | |

| Telecom and IT | |

| Government and Public Sector | |

| Others |

Key Questions Answered in the Report

What is the current size of the India digital transformation market?

It is valued at USD 144.48 billion in 2026 and is projected to grow to USD 304.86 billion by 2031.

Which segment leads the India digital transformation market by component?

Services dominate with a 53.05% share in 2025 and are expanding at a 20.15% CAGR through 2031.

How fast is edge computing growing within the India digital transformation industry?

Edge deployments are set to rise at a 27.1% CAGR to 2031, fueled by private 5G and industrial IoT rollouts.

Which industry vertical is forecast to grow fastest?

Healthcare is expected to register a 18.45% CAGR, driven by digital health IDs and AI-based diagnostics.

What are the main restraints on India’s digital transformation progress?

Heightened cyber-attack risks and a shortage of cloud-AI talent act as primary growth constraints.

How are hyperscalers positioning themselves in the India digital transformation market?

Firms like Microsoft, AWS, and Google are expanding regional datacenters, investing billions to meet data-localization and AI-compute demand.

Page last updated on: